Sample Category Title

Gold Remains Below 1,250 Mark

'There is a strong technical resistance at $1,250 and that seems to have been felt strongly at this juncture.' – Barnabas Gan, OCBC (based on Reuters)

Pair's Outlook

During the early hours of Thursday's trading session the yellow metal was in a retreats, which was initiated by the end of Wednesday's trading. Although initially it might seem that the 50.00% Fibonacci retracement level at 1,248.96 has reversed the direction of the bullion that is not true. The commodity price was pushed lower by a long term downwards aimed trend line, which can be drawn by connecting the August and September heights with the high level of February. It is, however, a high possibility that the metal will attempt to break this resistance and surge to the 1,256 level, where the next resistance level is located at.

Traders' Sentiment

Traders are neutral bearish on the metal, as 51% of open positions are short. Meanwhile, 65% of trader set up orders are to buy the bullion.

EUR/USD – Euro Unchanged, German Consumer Confidence Dips

EUR/USD – Euro Unchanged, German Consumer Confidence Dips

EUR/USD has edged lower on Thursday, as the pair trades at 1.0770. On the release front, GfK German Consumer Climate dipped to 9.8 points, shy of the forecast of 10.1 points. Later in the day, the eurozone releases consumer confidence data. The US will publish unemployment claims and New Home Sales. Federal Reserve Chair Janet Yellen will speak at an event in Washington, and FOMC members Neel Kashkari and Robert Kaplan will also deliver speeches on Thursday. On Friday, Germany and the eurozone release Manufacturing PMIs, and the US will publish durable goods orders.

German consumer confidence lost ground for a second straight week, as the GfK indicator fell to 9.8, its lowest level since November 2016. The drop is largely a result of higher inflation, as consumers are more concerned that their purchasing power has been reduced. Still, the German economy, the largest in Europe, remains in solid shape, as the economy is expected to expand 1.5% in 2017. German data is regarded as a bellwether for the eurozone, so the markets will be keeping a close eye on the upcoming German Manufacturing PMI report.

With a dearth of economic releases this week, the markets have been focusing on speeches from FOMC members. Earlier this week, Chicago Fed President Charles Evans said he expected the Fed to raise rates two more times this year. This projection was in line with the Fed’s dot point plan (which remain unchanged) as well as last week’s rate statement. Although one could make a strong case that three rate hikes in 2017 would be impressive, the markets appear disappointed, and would like four hikes, given the strong performance of the US economy. The Fed’s cautious approach has soured sentiment towards the greenback, resulting in the dollar heading lower against its major rivals, including the euro. On Wednesday, EUR/USD touched a high of 1.0825, its highest level since the start of February.

Daily Technical Analysis

EURUSD

The EURUSD was indecisive yesterday. The bias is neutral in nearest term. Overall price is still in a bullish phase, still respecting the EMA 200 and the trend line support as you can see on my H1 chart below. Immediate resistance is seen around 1.0820. A clear break above that area would expose 1.0873 area but note that from a daily chart perspective 1.0830 – 1.0873 area remains a good place to sell with a tight stop loss. Immediate support is seen around 1.0775. A clear break below that area could trigger further bearish pressure testing 1.0725 and the EMA 200/trend line support. On the upside, a clear break above 1.0873 would activate my bullish mode.

GBPUSD

The GBPUSD was indecisive yesterday but overall still able to maintain its bullish bias so far. As you can see on my H1 chart below price is moving inside a bullish channel and above the EMA 200 suggests a valid bullish outlook. The bias remains bullish in nearest term testing 1.2570 region. Immediate support is seen around 1.2420. A clear break below that area would be a threat to the bullish phase testing the EMA 200 and 1.2350/00 region. Overall I remain neutral.

USDJPY

The USDJPY had a bearish momentum yesterday bottomed at 110.73 but closed higher at 111.15 and hit 111.54 earlier today in Asian session. As you can see on my H4 chart below, we have 2 pin bars (hammer) formed around 111.30 key support suggests a potential bullish pullback. The bias is bullish in nearest term testing 111.80 – 112.00. A clear break and daily close above that area would expose 113.00 region. Key support is seen around 110.73 (yesterday’s low). A clear break and daily close below that area would activate my bearish mode.

USDCHF

The USDCHF attempted to push lower yesterday bottomed at 0.9881 but closed a little bit higher at 0.9913. The bias is neutral in nearest term probably with a little bullish bias testing 1.0000 region. On the downside, key support is seen around 0.9870. A clear break and daily close below that area would continue the bearish scenario testing 0.9800 region. Overall I remain neutral.

Trump’s First Congressional Test: The American Healthcare Act

Today, market participants will turn their attention to the US, where the House of Representatives is expected to vote on whether to repeal and replace the Affordable Care Act (Obamacare) with President Trump's new alternative, The American Healthcare Act (Trumpcare). A few weeks ago Trump pledged to deliver a "phenomenal" tax reform plan, but only after he took care of the health care issue. As a result, we think that this vote will be closely watched by investors. If the bill is voted down, markets could begin to speculate that tax reform is likely to take much longer to be introduced and implemented. This could also heighten doubts as to whether the new administration can deliver on its fiscal promises altogether, thereby raising uncertainty around the subject and leading to further downside correction in the assets that have priced in the "Trump effect", such as the dollar and US equities. Escalating political uncertainty could also benefit safe havens, like JPY and gold.

USD/JPY tumbled yesterday, breaking below 111.60 (R1), the lower bound of the range that contained the price action since the 11th of January. The rate hit support at 110.70 (S1) and then rebounded to challenge the key hurdle of 111.60 (R1) as a resistance. A rejection of the plan today is likely to encourage sellers to take advantage of that resistance zone and perhaps aim for another test near 110.70 (S1). If they prove strong enough to overcome that support, then we may experience extensions towards the psychological round figure of 110.00 (S2).

On the other hand, if the House votes for the bill, we could see a relief bounce in USD and US stocks as the risk of extended tax reform delays diminishes and as market participants become more confident that Trump can implement his overall agenda. In this case, USD/JPY could emerge back above 111.60 (R1) and signal its return back within the range it had been trading since early January.

Having said that though, even if it passes the House today, it has to be approved by the Senate, perhaps as early as next week. Therefore, although a House pass could spread some market euphoria, there is still a lot to be done before we have a concrete outcome.

RBNZ remains on hold, keeps the door open for further easing

The RBNZ kept its Official Cash Rate unchanged yesterday, as was widely anticipated. The meeting statement did not contain any major surprises and as such, there was a relatively limited reaction in NZD. The officials noted that the trade-weighted exchange rate has fallen 4% since February and that although this is encouraging, further depreciation is needed to achieve more balanced growth. With regards to inflation, the Bank noted that it is expected to return to the midpoint of the target band over the medium-term, an upgrade from the previous statement where it expected this to happen "gradually". Last but not least, the officials kept the door open for further easing by reiterating that numerous uncertainties persist, particularly in the global outlook, and that policy may need to adjust accordingly.

NZD/USD traded somewhat higher ahead of the decision to find once again resistance near the 0.7075 (R1) obstacle and the downtrend line taken from the peak of the 7th of February. In the aftermath of the meeting, the rate slid again, but the slide remained limited above the 0.7015 (S1) support line. We hold the view that the short-term path is negative, but we would like to see a clear break below 0.7015 (S1) before we assume that the recovery started on the 14th of March is over and that we are back in the direction of the trend. Such a break is possible to initially aim for the next support of 0.6970 (S2).

As for the bigger picture, the outlook of the pair remains cautiously negative as well, in our view. The RBNZ has been very vocal about wanting a weaker Kiwi, and has even threatened to intervene in the FX market in previous meetings. Combined with the fact that it has kept the door for further easing open and that domestic economic data are mixed, the currency could stay on the back foot for a while. Nevertheless, in order to get more confident on larger declines, we would like to see a decisive close below the strong support of 0.6880.

As for the rest of today's highlights

During the European day, the only major indicator we get is UK retail sales for February. Both the headline and the core rates are expected to have risen following two consecutive months of declines. Coming on top of the latest acceleration in the nation's CPIs, rebounding retail sales could fuel further market expectations over a reduction in BoE stimulus and thereby, bring GBP under renewed buying interest.

From Eurozone, we get the preliminary consumer confidence index for February.

From the US, we get new home sales for February and initial jobless claims for the week ended on the 17th of March. New home sales are forecast to have risen for the second consecutive month, while initial jobless claims are expected to have ticked down, something that would drag the 4-week moving average somewhat lower too.

As for the speakers, today's agenda includes only Fed Chair Janet Yellen. Even though she is one of the most important speakers in the financial world, we do not expect her to deliver any new market moving information. It has only been a week since we heard her views at the press conference of the latest FOMC meeting and there have been no major changes in the US economy's outlook since then.

USD/JPY

Support: 110.70 (S1), 110.00 (S2), 108.80 (S3)

Resistance: 111.60 (R1), 111.90 (R2), 112.40 (R3)

NZD/USD

Support: 0.7015 (S1), 0.6970 (S2), 0.6945 (S3)

Resistance: 0.7075 (R1), 0.7110 (R2), 0.7170 (R3)

EURUSD – Consolidation Ahead Of Fresh Attempts Higher

The Euro remains biased higher and eyes immediate target at 1.0827 (02 Feb high/Fibo 38.2% of larger 1.1614/1.0339, May 2016 / Jan 2017 descend), with extension towards 200SMA (1.0884) seen on break. The pair hit new high at 1.0823 on Wednesday, coming just ticks ahead of its initial target, but Thursday's action shows signs of further easing, after previous day ended in red. This suggests further consolidation before fresh bulls emerge, with dips expected to be contained by hourly cloud base (1.0768) to keep structure intact. Otherwise, signals of deeper correction could be expected on break below hourly cloud that would expose pivotal supports at 1.0700 zone (rising Tenkan-sen/Fibo 38.2% of 1.0493/1.0823 upleg). The pair will be also focusing events today: speech of Fed Chief Yellen, House vote for healthcare bill and releases from US jobs and housing sector, for stronger signals.

Res: 1.0803, 1.0827, 1.0884, 1.0931

Sup: 1.0780, 1.0768, 1.0719, 1.0697

Forex Technical Analysis

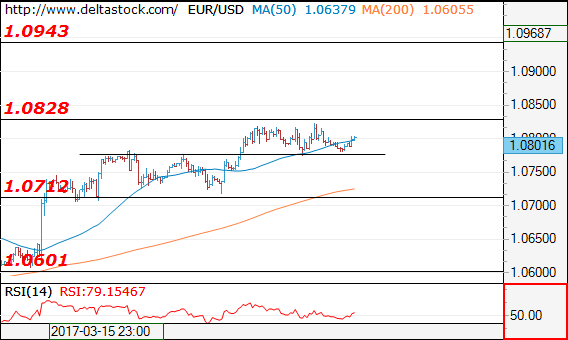

EUR/USD

Current level - 10801

My outlook here remains positive above 1.0780 support area, for a break through 1.0940 and continuation of the upmove towards 1.0940 target mark. Crucial on the downside is 1.0712.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.0828 |

1.0870 |

1.0712 |

1.0600 |

|

1.0870 |

1.0945 |

1.0600 |

1.0490 |

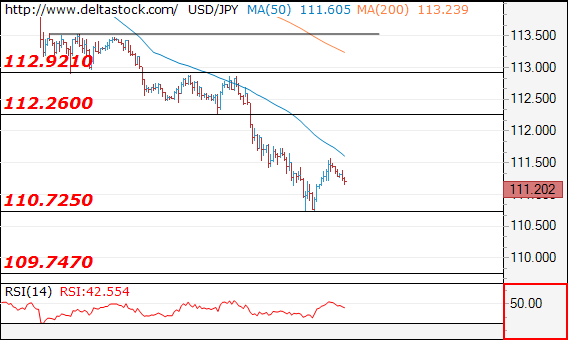

USD/JPY

Current level - 111.20

The rebound after 110.72 low should be considered corrective, preceding another leg downwards, to 109.75. Key resistance lies at 112.26.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

112.26 |

113.50 |

110.72 |

109.75 |

|

112.90 |

115.65 |

109.75 |

107.80 |

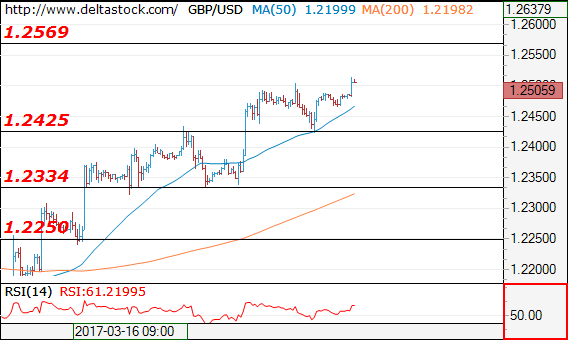

GBP/USD

Current level - 1.2505

The uptrend has been renewed after the failure at 1.2425 support and the bias is positive, for a rise towards 1.2570 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.2570 |

1.2570 |

1.2425 |

1.2107 |

|

1.2570 |

1.2705 |

1.2335 |

1.1984 |

Dollar Still Struggles To Stay Above Key Support Levels

Sunrise Market Commentary

- Rates: Outcome healthcare bill vote reflection of prospects fiscal stimulus plans?

Today's eco calendar heats up, but investors could turn to wait-and-see mode. If US President Trump manages to push through the new healthcare bill, it bodes well for pursuing his economic agenda and supports the reflation trade. Failure to do so might bring more of Tuesday's risk off scenes to markets. - Currencies: Dollar still struggles to stay above key support levels.

Yesterday, the dollar remained in the defensive even as the equity correction eased. EUR/USD and USD/JPY are still within reach of key technical levels. Global sentiment on risk and the first votes on the replacement of Obamacare might decide to which side the USD domino will fall. Sterling lost only temporary ground on the terrorist attack in London.

The Sunrise Headlines

- US equities ended between flat (Dow) and +0.5% (Nasdaq), recovering from Tuesday's sudden sell-off. Overnight, Asian stock markets trade mostly positive as well.

- A suspected Islamist terrorist mowed down pedestrians on a crowded bridge before crashing his car near the gates of Parliament and stabbing a policeman, leaving 4 dead in an attack that struck at the heart of British democrac

- US President Trump and House leaders pushed for votes for their plan to overhaul Obamacare and said they were making progress in their efforts to win over conservative Republicans. A vote on the bill is possible as soon as today

- The RBNZ kept its policy rate unchanged at 1.75%. Governor Wheeler said that while NZD had weakened by 4% since February, partly thanks to softer dairy prices, “further depreciation is needed to achieve more balanced growth.”

- A study to be presented at the Brookings Papers conference this week by two Federal Reserve Board economists finds that rates could hit zero as much as 40% of the time – far more often than predicted by other studies.

- Fitch downgraded Saudi Arabia by one notch to A+ (stable outlook) from AA- (negative outlook). It said that that while the leadership was strongly committed to diversifying the economy beyond oil, that intention might not be enough.

- Today's eco calendar heats up with UK retail sales, US weekly jobless claims & new home sales and EMU consumer confidence. The ECB announces the results of its final TLTRO and publishes its economic bulletin. Fed Yellen, Fed Kashkari, ECB Lautenschlaeger and ECB Nouy speak.

Currencies: Dollar Still Struggles To Stay Above Key Support Levels

USD holding near key technical levels

On Wednesday, investors tried to find out what could be next after Tuesday's risk-off correction. Risk sentiment remained fragile and core yields declined further. This weighed on the dollar, with USD/JPY (temporary) sliding below the 111 big figure. However, the decline in core bond yields and in the dollar halted as there were no sustained follow-through losses of US equities. USD/JPY closed the session at 111.16 (from 111.71). EUR/USD finished the day at 1.0797 (from 1.0811).

Overnight, Asian equities are trade slightly stronger, while the gains of both equities and the dollar are modest. Amongst others, global investors are awaiting a first vote in US house of representatives to repeal Obamacare. It is seen as a condition to pass other fiscal legislation. USD/JPY is trading in the 111.35 area. EUR/USD is trading a narrow range close to, slightly below 1.08. The Reserve Bank of New Zealand kept its policy rate unchanged at 1.75%, as expected, and maintained a neutral bias. The domestic economy performs solidly, but the bank sees many risk outside the country. The RBNZ still sees a need for a weaker kiwi dollar. NZD /USD trades currently slightly softer in the mid 0.70 area.

The calendar is better filled today, but still misses a real market mover. In EMU, several confidence data will be published. They are a precursor for tomorrow's more important PMI confidence. In the US, the initial claims are expected little changed at 240K and New Home sales are expected up 1.8% M/M in February. Given the recent easing of sales and the low inventory of existing homes for sale, we expect sales to have increased in February. Fed Yellen and Kaskhari speak but on non-policy issues (community development & education). ECB Lautenschlaeger, a hawk, speaks too, but she often shies away from the policy outlook. Markets will keep a close eye whether a replacement for Obamacare can pass Parliament. In case of a an agreement, sentiment on risk might again improve, which might help to put a floor for the dollar. With only second tier eco data on the agenda, sentiment on risk and the political developments in the US (healthcare bill) will set the tone for USD trading. The jury is still out, but yesterday's price action was not too bad as there were no follow-through losses on Tuesday's equity correction. However, a clear signal of an USD bottoming out process is needed. Especially USD/JPY remains vulnerable as the pair still struggles not to fall below the 111.36/60 support.

The picture for EUR/USD remains slightly different. Of late, the narrowing of the US-German 2- and 10-year yield spread weighed on the dollar, but this narrowing halted yesterday and capped the topside of EUR/USD. The jury is still out whether or not interest rate differentials will narrow further, but for now, the 1.0829/74 resistance remains intact. A test of the 1.0829/74 resistance is very well possible, but the EUR/USD rebound might further slow. Even so, it is still too early to row against the USD downtrend/ EUR/USD rebound. In a longer term perspective, we don't change our USD-constructive bias based on the eco fundamentals. However, this doesn't tell anything on the short-term momentum dynamics

EUR/USD holding near the key 1.0829/74 resistance

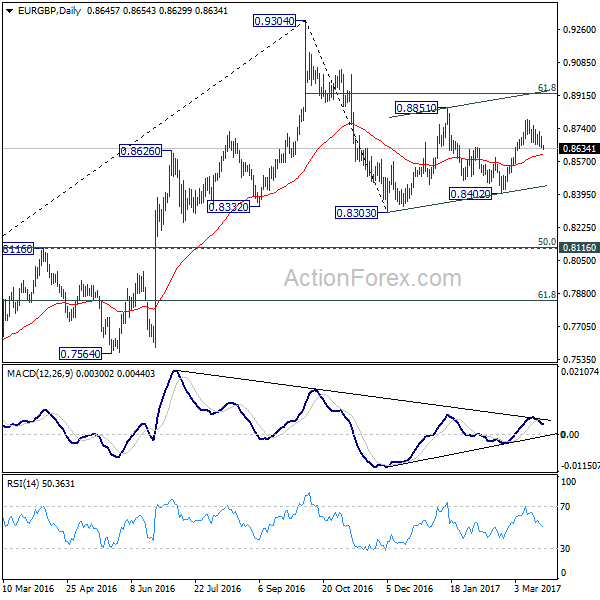

EUR/GBP

UK retail sales in focus for sterling trading

Yesterday, no data or other high profile UK specific news events was scheduled. Sterling tried to establish some follow-through gains on Tuesday's post-CPI rally. However, the focus was on the global factors. EUR/USD and cable broadly followed a similar trading pattern till the headlines on the London terrorist attack hit the screens. This triggered some temporary sterling selling with EUR/GBP jumping to the 0.87 barrier. EUR/GBP closed the session at 0.8649 (from 0.8663). Cable finished the session also marginally stronger at 1.2485.

Today, the UK calendar is better filled with both the February retail sales and the CBI March distributive sales. Official retail sales are expected to have rebounded (0.4% M/M and 2.6% Y/Y) after a setback December and January. After last week's BoE statement, price data have again become more important for sterling trading rather than activity data. Even so, a positive surprise might make markets pondering the probability of a BoE rate hike further down the road. At the same time, the euro also remains well bid, slowing any potential decline of EUR/GBP. Last week, the sterling decline took a breather. Some time ago, EUR/GBP cleared 0.8592 resistance, improving the MT technical picture. However, this week's (substantially) higher than expected UK inflation probably put a decent floor for sterling short-term. We changed our short-term bias on EUR/GBP from positive to neutral. Some further consolidation in the 0.85/0.88 area might be on the cards. Longer term, Brexit complications remain a potential negative for sterling, but this issue isn't in the spotlights right now.

EUR/GBP: sterling remains well bid after higher UK inflation earlier this week

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8631; (P) 0.8679; (R1) 0.8708; More...

EUR/GBP's pull back from 0.8786 extends lower today and breached 38.2% retracement of 0.8402 to 0.8786 at 0.8639. There is no sign of bottoming yet. Sustained trading below 0.8639 will target 61.8% retracement 0.8549 and possibly below. On the upside, above 0.8699 minor resistance will turn bias back to the upside for 0.8786 resistance. Break will extend the rise from 0.8402 to 0.8851. Overall, price actions from 0.8303 are seen as the second leg of the corrective pattern from 0.9304. Fall from 0.9304 should resume later.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).

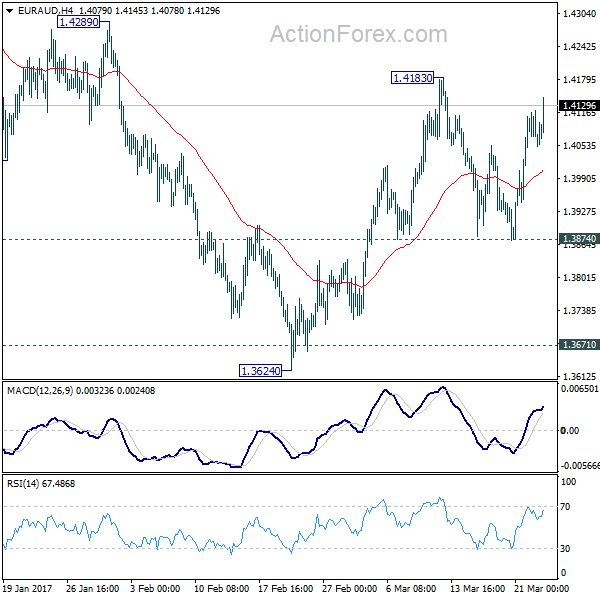

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.3929; (P) 1.3999; (R1) 1.4123; More...

EUR/AUD rebounded further today but it's limited below 1.4183 resistance so far. Intraday bias stays neutral first. Overall, with 1.3874 minor support intact, we're still favoring the case of trend reversal after defending key support level at 1.3671. This is supported by bullish convergence condition in daily MACD. On the upside, above 1.4183 will turn bias to the upside for 1.4289 resistance next. Break will affirm our view and target next key resistance level at 1.4721. However, break of 1.3874 minor support will invalidate our view and turn bias back to the downside for retesting 1.3624 low.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. We'd expect strong support from 1.3671 key level to contain downside and bring rebound. Up trend from 1.1602 should not be finished and will resume later. Break of 1.4721 resistance will indicate completion of such correction and turn outlook bullish for retesting 1.6587 high. However, sustained break of 1.3671 will invalidate our bullish view and would turn focus back to 1.1602 long term bottom.

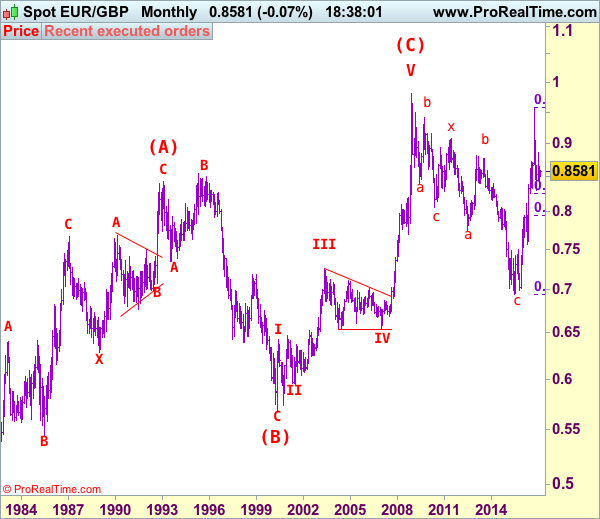

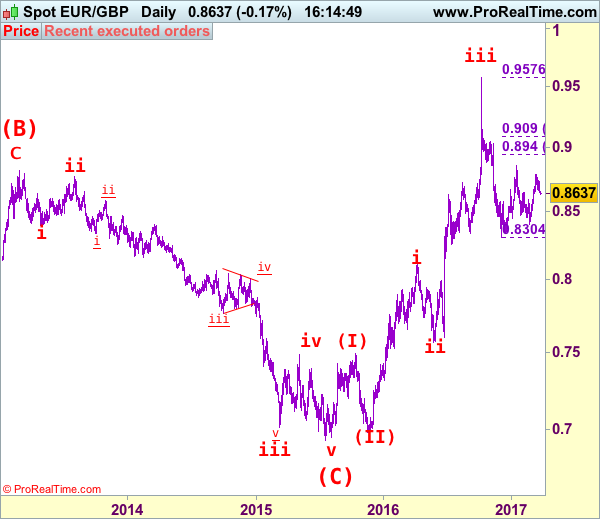

EUR/GBP Elliott Wave Analysis

EUR/GBP – 0.8661

EUR/GBP – The major (A)(B)(C)-(X)-(A)(B)(C) correction from 0.9805 is unfolding and 2nd (A) has possibly ended at 0.6936.

As the single currency has retreated after meeting resistance at 0.8788 earlier this month, retaining our view that minor consolidation below this level would be seen and pullback to 0.8630-35 cannot be ruled out, however, reckon downside would be limited to 0.8595-00 and renewed buying interest should emerge around there, bring another rise later. Above said resistance at 0.8788 would extend the rebound from 0.8403 towards indicated resistance at 0.8857 which is likely to hold from here.

Our latest preferred count is that the wave V of a 5-wave series from 0.5682 ended at 0.9805 earlier and major from there has possibly ended at 0.8067 as A-B-C-X-A-B-C. We are keeping our view that the entire correction from 0.9805 has possibly ended at 0.7756 and as labeled as the attached daily chart and impulsive move from 0.9084 has ended at 0.7756 as a 5-waver which marked either the (C) wave or the A leg of (C), a daily close above resistance at 0.8831 would suggest (C) leg has ended and headway towards 0.9084.

On the downside, whilst pullback to 0.8630-35 cannot be ruled out, reckon downside would be limited to 0.8595-00 and bring another rise later. Below 0.8545-50 would defer and suggest top is formed instead, and risk weakness to 0.8500-10 but break there is needed to provide confirmation and suggest the rebound from 0.8403 has ended.

Recommendation: Buy at 0.8600 for 0.8750 with stop below 0.8500.

Euro's long term uptrend started in Feb 1981 at 0.5039 and is unfolding as a (A)-(B)-(C) move with (A): 0.8433 (Feb 1993), (B): 0.5682 (May 2000) and impulsive wave (C) should have ended at 0.9805 with wave III ended at 0.7254 (May 2003), triangle wave IV at 0.6536 (23 Jan 2007) and wave V as well as wave (C) has ended at 0.9805.

We are keeping an alternate count that only wave III ended at 0.9805 and the correction from there is the wave IV and may extend weakness to 0.7700, however, it is necessary to see a daily close above resistance at 0.9143 would change this to be the preferred count.