Sample Category Title

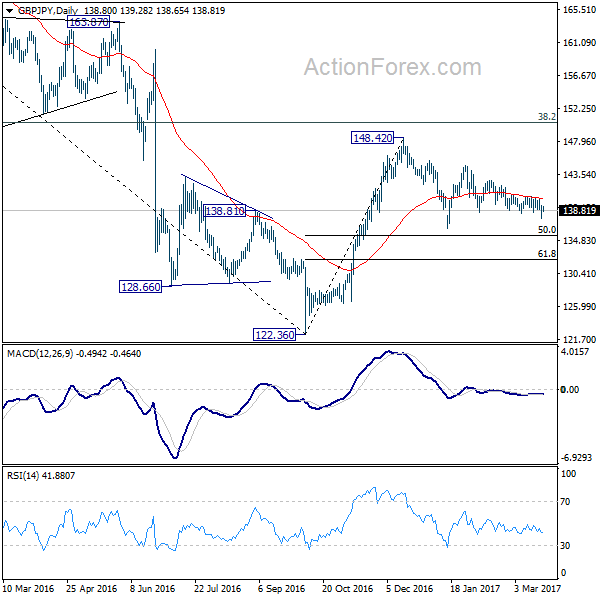

GBP/JPY Daily Outlook

Daily Pivots: (S1) 137.84; (P) 138.66; (R1) 139.59; More...

GBP/JPY breached 138.53 support but quickly recovered. Current development suggests that deeper fall is underway back to 136.44 support at possibly below. Overall, price actions from 148.42 are viewed as a consolidation pattern. We'd expect 50% retracement of 122.36 to 148.42 at 135.39 to contain downside and bring rebound. On the upside, break of 140.60 resistance will turn bias to the upside and send GBP/JPY through 144.77 resistance.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern. Or, sustained break of 50% retracement of 122.36 to 148.42 at 135.39 will turn outlook bearish for a test on 122.36 low. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement of 195.86 to 122.36 at 167.78.

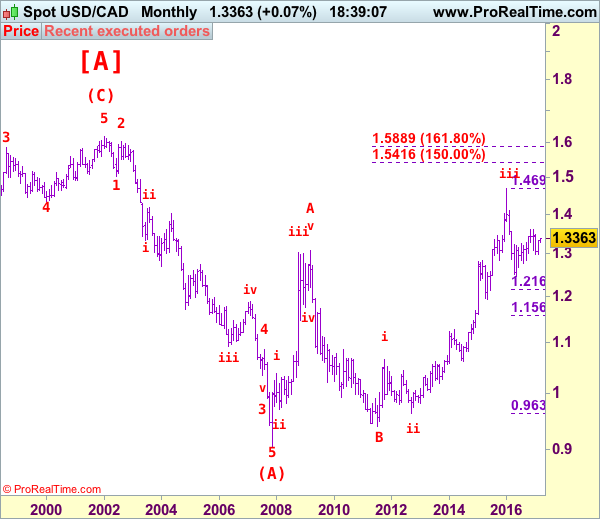

USD/CAD Elliott Wave Analysis

USD/CAD – 1.3348

USD/CAD – Wave v ended at 0.9407 and a-b-c correction may extend gain to 1.4700

As the greenback’s retreat from 1.3535 turned out to be deeper than expected, dampening our bullishness and suggesting a temporary top has been formed there, hence consolidation with mild downside bias would be seen and another test of 1.3264 support cannot be ruled out, break there would add credence to this view, bring correction of recent upmove to previous resistance at 1.3210-12 (now support). Only below this level would suggest the rebound from 1.2969 has ended and prolong choppy trading, bring weakness to 1.3100 but downside should be limited to 1.3056 support, bring rebound later.

We are keeping our view that the wave b from 1.0657 (a leg top) has possibly ended at 0.9633 with (a): 0.9800, wave (b): 1.0447 and wave c at 0.9633, the subsequent rise from there is now treated as wave c exceeded indicated upside target at 1.3770-80 and 1.4000 and wave (3) has possibly ended at 1.4690 and wave (4) correction has commenced for retracement back to 1.2832 support, then 1.2410-20.

On the daily chart, our latest preferred count remains that the A of (B) rally from 0.9059 low (7 Nov 2007) unfolded into an impulsive wave with i: 0.9059-1.0380, ii ended at 0.9819, iii at 1.3019 followed by triangle wave iv at 1.2026 , then wave v formed a top at 1.3066 and also ended the wave A. The wave B is unfolding as an double three a-b-c-x-a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c at 1.0784, followed by wave x at 1.1725, another set of a-b-c unfolded with 2nd a at 0.9931, 2nd b at 1.0674. the 2nd c has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3900 had been met and gain to 1.4700 would follow.

On the upside, expect recovery to be limited to 1.3400 and bring another decline. Above 1.3425-30 would suggest the retreat from 1.3535 has possibly ended, bring a stronger rebound to 1.3500, then retest of 1.3535. A break of this resistance would revive bullishness and signal the rise from 1.2969 is still in progress for retest of 1.3599 top, once this level is penetrated, this would confirm the erratic rise from 1.2461 low has resumed for a stronger correction of early decline from 1.4690 (2016 high) to 1.3700 and later towards 1.3790-00, however, reckon upside would be limited to 1.3835-40 (61.8% Fibonacci retracement of 1.4690-1.2461) and bring retreat later.

Recommendation: Stand aside for this week.

Longer term - The selloff from 1.6194 (21 Jan 2002) to 0.9059 (07 Nov 2007) is viewed as (A) wave which is a 5-waver as labeled on the monthly chart as below, the subsequently rally is labeled as (B) with impulsive A leg of (B) ended at 1.3066, wave B of (B) is unfolding which has either ended at 0.9407 or would extend one more fall but downside should be limited to 0.9200 and 0.9000 should hold.

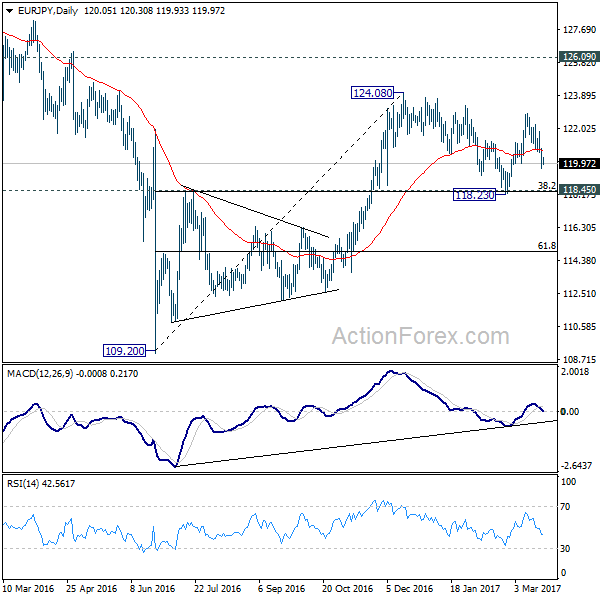

EUR/JPY Daily Outlook

Daily Pivots: (S1) 119.53; (P) 120.18; (R1) 120.69; More...

EUR/JPY's fall from 122.88 is still in progress and intraday bias stays on the downside for the moment. With a break of 120.01 minor support, the cross should now target 118.39/45 key cluster level again (38.2% retracement of 109.20 to 124.08 at 118.39). However, as such decline is viewed as part of the consolidation pattern from 124.08, we'd expect strong support from 118.39/45 to contain downside and bring rebound. On the upside, above 120.81 minor resistance will turn bias back to the upside for 122.88 and then 124.08.

In the bigger picture, we're holding on to the view that medium term rise from 109.20 is still in progress. Focus is on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09, or firm break of 118.45 cluster support, will likely extend the fall from 149.76 through 109.20 low.

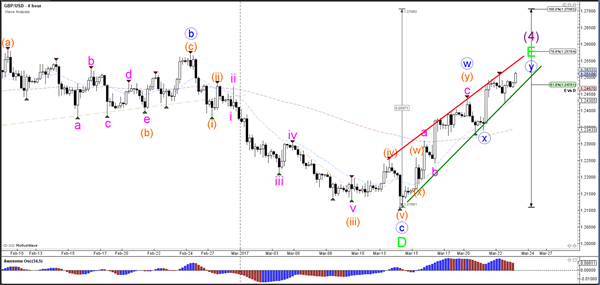

GBP/USD Breaks 1.25 Resistance within Bullish Trend Channel

Currency pair GBP/USD

The GBP/USD is in an uptrend channel indicated by the support (green) and resistance (red) trend lines. Price seems to be breaking above the 61.8% Fibonacci level which means that price could test the next Fib at 78.6%.

The GBP/USD is trying to build a bullish breakout above resistance (dotted red).

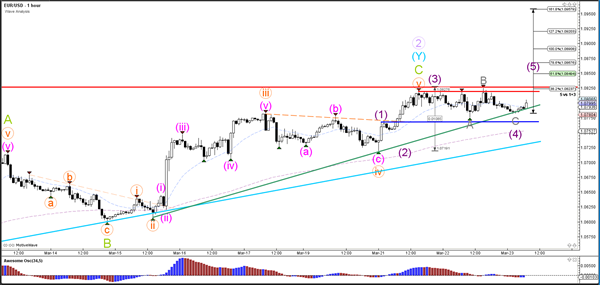

Currency pair EUR/USD

The EUR/USD is building a rising wedge chart pattern (red/green) trend lines. A break below the wedge could send the EUR/USD to test the next support (blue). A break above it could see price invalidates wave 2 (purple) at the horizontal line (red) and see a potential breakout within wave 5 (purple).

The EUR/USD could have completed an ABC correction (grey) within wave 4 (purple). The support and resistance trend lines are key. A break below the blue line invalidates the 5 wave pattern (purple).

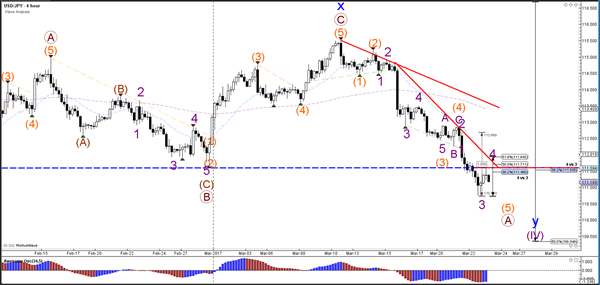

Currency pair USD/JPY

The USD/JPY broke below the bottom (dotted blue) and made a pullback to the broken bottom which has now become resistance (dotted red). The retracement could be part of a wave 4 (purple) unless price breaks above the 61.8% Fib of wave 4 vs 3.

The USD/JPY could be building a 4 wave (purple/orange) within a larger wave 5 (orange).

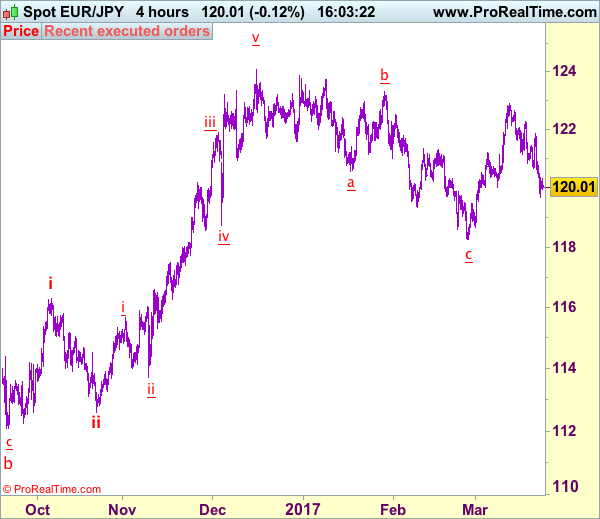

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 120.05

Recent wave: wave v of (C) ended at 94.12 and major correction in wave A has ended at 149.79

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

As the single currency has remained under pressure after meeting renewed selling interest at 121.84 earlier this week, adding credence to our view that recent rise from 118.24 has ended at 122.89 last week, hence downside risk remains for this fall from 122,89 top to extend further weakness to 119.65-70 and then 119.35-40, however, near term oversold condition should limit downside to 119.00 and support at 118.67 should hold from here,

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. On the upside, whilst recovery to 120.60-70 cannot be ruled out, reckon upside would be limited to 121.15-20 and bring another decline later. Only break of said resistance at 121.84 would revive bullishness and suggest low is formed instead, bring test of indicated resistance at 122.26 first.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

Is The Party Over?

Did the market just experience a mini-correction? Or is this the beginning of something bigger? Why are news headlines making a big issue of a 1% drop in U.S. equities? Shall investors buy on the dips, or better protect themselves from the downside?

These were the top questions I received since Tuesday's more than 1% drop in U.S. equities, but unfortunately, there are no black or white answers in our gray world.

A 1% fall in equities isn't frightening. In 2016 we experienced 21 days of more than 1% drop in S&P 500, and the index still managed to gain 5% from January 2016 until the presidential election on November 8. Most of the gains since November 9 until the beginning of March of 12.4% were attributed to Trump trade and improving economic conditions in the U.S. and globally.

However, the price action experienced in the last couple of days indicates that the first phase of Trump trade is over. U.S. equities are currently priced for perfection, and now we should be looking for justifications of the overstretched valuations.

Worrying signs

Equity analysts are revising their earnings growth downward, Donald Trump's approval rating by the latest Gallup Poll sank to 37%, and FBI's Director James Comey hurt the President's credibility even further.

Other worrying signs are coming from different asset classes. For example, U.S. 10-year treasury bond yields declined by more than 20 basis points from Mid-March highs. If this drop in yields reminds me of anything, it reminds me of Neel Kashkari, the President of the Federal Reserve Bank of Minneapolis, who was the only dissenter to raise interest rates in Fed's last meeting. He was worried that the economic data did not back up the belief that things had gotten significantly better, and markets seem to share his skepticism by flocking to the safety of bonds.

Energy markets are sharing a similar story as well. Although oil prices were mostly pressured due to increasing U.S. inventories; prices should rally when the dollar falls which did not happen.

So, we need a lot of good news to keep investors buying into the second longest bull market ever.

Repealing Obama Care

Today will be a major test to Trump trade. The U.S. Congress will vote on the bill to repeal Obamacare after some modification took place on Monday. If the bill passed, we might see some relief in equities. However, there's a high chance that more than 21 Republicans will vote against the health care plan, leading to the first significant loss of Trump's administration. Such a loss would be perceived as jeopardizing the President agenda, and could potentially lead to shaking investors' confidence.

I'm not calling for a major correction as of yet, but for investors who want to remain invested largely in equities, I suggest it's a good time to think about buying a protection to protect from a market downturn.

Trade Idea: AUD/USD – Hold long entered at 0.7645

AUD/USD – 0.7647

Recent wave: Wave 5 ended at 1.1081 and major correction has commenced for fall to 0.7000 and then towards 0.6500-10

Trend: Near term up

Original strategy :

Bought at 0.7645, Target: 0.7800, Stop: 0.7585

Position: - Long at 0.7645

Target: - 0.7800

Stop: - 0.7585

New strategy :

Hold long entered at 0.7645, Target: 0.7800, Stop: 0.7585

Position: - Long at 0.7645

Target: - 0.7800

Stop:- 0.7585

Although aussie has remained under near term pressure after retreating quite sharply from 0.7750 (this week’s high) and marginal weakness from here cannot be ruled out, reckon downside would be limited and as long as 0.7592 (previous resistance) holds, mild upside bias remains for another rise, above said resistance would extend gain to 0.7778 (last year’s high), however, break there is needed to retain bullishness and extend headway to 0.7840-50 but price should falter below 0.7900.

In view of this, we are holding on to our long position entered at 0.7645. Only below previous resistance at 0.7592 would abort and signal top is formed instead, then further choppy trading would take place and risk is seen for pullback to 0.7530-40 but indicated support at 0.7491 should remain intact.

On the 4-hour chart, the move from 0.8066 is the wave 5 with i: 0.8860, ii: 0.8315, wave iii is an extended move ended at 1.0183, iv: 0.9706 and wave v has ended at 1.1081 (also the top of entire wave 5). The subsequent selloff is the major correction which is unfolding as ABC-X-ABC and 2nd A leg has ended at 0.8848, followed by a-b-c wave B which ended at 0.9758, hence, 2nd C wave is now in progress and indicated downside target at 0.7000 and 0.6950 had been met, so further fall to 0.6710-20 cannot be ruled out.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0678; (P) 1.0712; (R1) 1.0737; More...

Much volatility is seen in EUR/CHF as consolidative trading continues. But still it's holding above 1.0683 minor support, and in range below 1.0823. Intraday bias remains neutral for the moment. On the upside, break of 1.0823 resistance will re-affirm the case of trend reversal. And intraday bias will be turned back tot he upside for 1.0897 resistance for confirmation. However, break of 1.0683 minor support will turn bias to the downside for 1.0620 key support level again.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Decisive break of 1.0897 resistance should confirm that it's completed. And in that case, larger up trend is resuming for another high above 1.1198. Meanwhile, sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485.

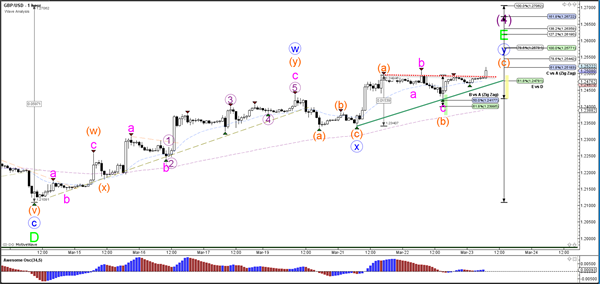

GBPUSD Trading At The Start Of A Big Bullish Impulse

Cable is turning nicely up since start of the month, when pair most-likely completed a deep and complex corrective retracement from February highs down to 1.2110 level. It was a double three pattern that is now finished after a nice recovery back above 1.2384 bullish level, where overlap with wave A and break out of a downward channel confirms a reversal. As such, we will look for even more upside in days ahead, but in the mean-time we still need to be aware of a corrective set-back in wave 2 that may find a support at 1.2300 zone.

GBP/USD, 4H

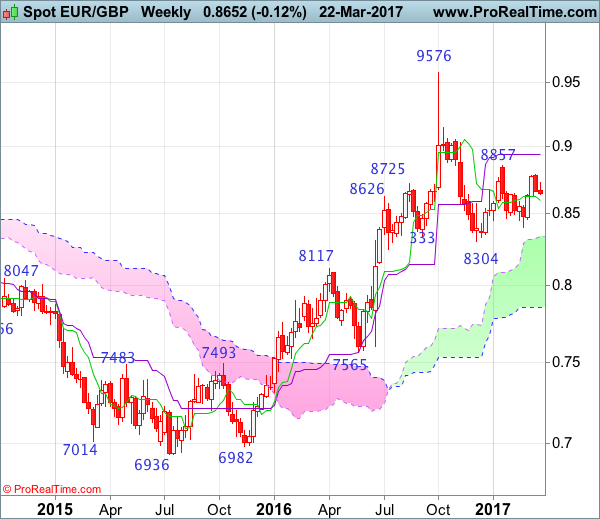

EUR/GBP Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: N/A T

• ime of formation: N/A

• Trend bias: Near term up

Daily

• Last Candlesticks pattern: Hammer

• Time of formation: 3 Feb 2016

• Trend bias: Up

EURGBP – 0.8708

The single currency met resistance at 0.8760 last week and has slipped again, suggesting near term downside risk remains for the retreat from 0.8788 to bring retracement of recent upmove, hence initial downside risk remains for correction to 0.8630-35, however, reckon the Kijun-Sen (now at 0.8596) would limit downside and bring another rise later, above said resistance at 0.8760 would signal pullback from 0.8788 has ended, bring retest of this level. Looking ahead, break there would extend rise from 0.8403 to 0.8810-15 but as broad outlook remains consolidative, reckon upside would be limited to previous resistance at 0.8857, risk from there is seen for a retreat to take place later. Only break of said resistance at 0.8857 would signal the rise from 0.8304 low is underway for headway to 0.8900, then towards 0.8940 (50% Fibonacci retracement of 0.9576-0.8304) which is likely to hold from here.

On the downside, whilst pullback to 0.8630-35 cannot be ruled out, reckon the Kijun-Sen (now at 0.8596) would contain downside and bring another rise later. A daily close below the Kijun-Sen would signal top is formed and bring weakness to 0.8550-55 and then test of 0.8505-10 but break of latter level is needed to signal the rebound from 0.8403 has ended, bring subsequent fall to 0.8460-65, however, price should stay well above said support at 0.8403 and bring another rebound later.

Recommendation: Buy at 0.8605 for 0.8785 with stop below 0.8505.

On the weekly chart, as the single currency has eased after meeting resistance at 0.8788, retaining our view that initial consolidation below this level would be seen and pullback to the Tenkan-Sen (now at 0.8596) cannot be ruled out, however, reckon downside would be limited to 0.8580 and bring another rise later. Above said resistance at 0.8788 would extend the rebound from 0.8403 towards said resistance at 0.8857. Looking ahead, only a break of this level would revive bullishness and extend the rise from 0.8304 to 0.8940 (50% Fibonacci retracement of 0.9576-0.8304 and current level of the Kijun-Sen) but price should falter below resistance at 0.9026.

On the downside, expect pullback to be limited to 0.8630 and 0.8595-00 should hold, bring another rebound. Below 0.8550 would defer and risk weakness to 0.8520 but reckon 0.8495-00 would contain downside. Below 0.8460-65 would bring retest of 0.8403 but break there is needed to revive bearishness and extend the fall from 0.8857 to 0.8350-55. Looking ahead, below there would signal decline from 0.9576 top has resumed for retest of 0.8304 but only break there would extend the fall from 0.9576 top for retracement of medium term upmove to previous support at 0.8251, then 0.8200.