Sample Category Title

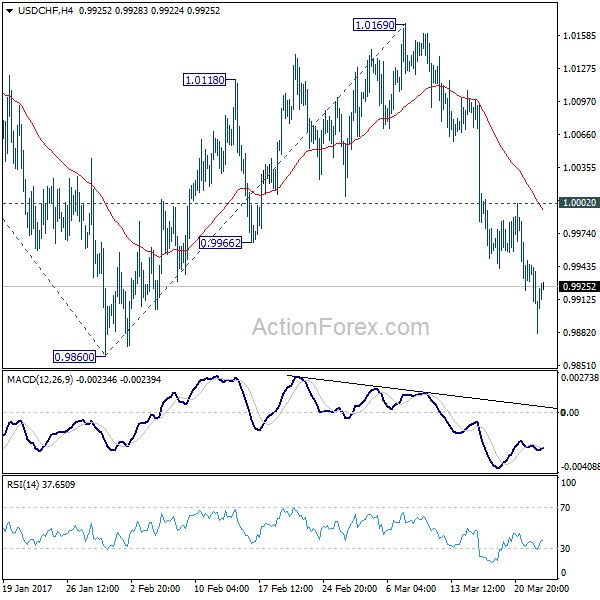

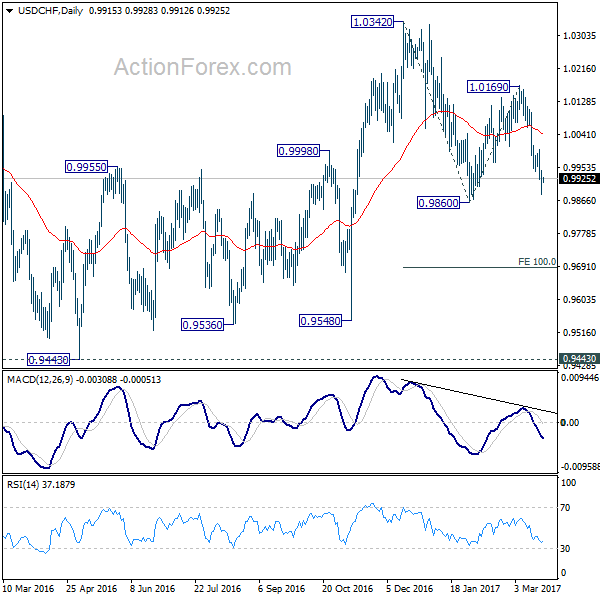

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9881; (P) 0.9913; (R1) 0.9946; More.....

No change in USD/CHF's outlook as fall from 1.0169 is still in progress. Intraday bias stays on the downside for 0.9860 support next. Whole decline from 1.0342 is likely resuming and break of 0.9860 will target 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687. Nonetheless, on the upside, break of 1.0002 minor resistance will turn bias back to the upside for 1.0169 resistance instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.67; (P) 111.22; (R1) 111.72; More...

USD/JPY dipped to as low as 110.27 but quickly recovered. At this point, we'd still expecting strong support around 111.12/13 cluster support to bring rebound. This level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. Break of 112.86 resistance will turn bias back to the upside for 115.49 resistance first. However, sustained break of 111.12/13 will bring deeper decline to 100% projection of 118.65 to 111.58 from 115.49 at 108.42.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.19) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Foreign Exchange Market Commentary

EUR/USD

Following a consolidative stage that extended during the first half of the day, the EUR/USD extended its monthly advance up to 1.824 after the US opening, as the dollar got dragged lower by poor US data and falling equities. The EUR/USD pair however, was unable to hold on to gains, and closed the day pretty much flat a few pips above the 1.0800 level. Risk aversion was again the main theme leading the markets, as following Wednesday's equities slump, a terrorist incident took place near the UK Parliament with at least two people dead.

In the data front, the EU released a minor report, the its current account for January, which recorded a surplus of €24.1 billion, below market's expectations, and December result, this last revised lower to €30.8B. In the US, sales of existing homes fell by 3.7% in February, at a 5.48 million seasonally adjusted annual rate, below previous 5.69M and expectations of 5.58M. Also, Fed's Kaplan hit the wires, reaffirming that the US Central Bank would need just two more rate hikes this year, and that policymakers will continue trimming its massive balance sheet gradually.

Despite still contained by a major Fibonacci resistance at 1.0820, the 50% retracement of the post-US election slide, the pair retains its bullish bias, at least technically, given that in the 4 hours chart, technical indicators have resumed their advances within positive territory after approaching their mid-lines, whilst 20 SMA maintains a sharp bullish slope below the current level. The pair peaked at 1.0828 last Friday, the level to surpass to confirm additional gains up to 1.0873, December monthly high. As long as the price holds above the 1.0700 region, bulls will remain in control of the pair.

Support levels: 1.0765 1.0730 1.0700

Resistance levels: 1.0830 1.0870 1.0910

USD/JPY

The USD/JPY pair trades at its lowest for this 2017 and not far from a daily low of 110.74, as risk aversion fueled demand for the safe-haven currency, exacerbated by the technical breakout of the 111.60 level earlier in the day. The pair plummeted at the beginning of the day after Wall Street's sharp decline weighed on Asian equities, further weighed through the day by the continued weakness in US Treasury yields, with the 10-year note benchmark falling down 2.39% after closing on Tuesday at 2.44%. The decline paused during the Asian session, as the Japanese trade surplus surged to a multi-year high of ¥813.4 billion in February. Exports in the same month surged by 11.3%, beating expectations, albeit imports increased by just 1.2%, from previous 8.5% advance. The technical outlook is clearly bearish according to the 4 hours chart, with technical indicators heading sharply lower within extreme oversold territory, whilst the price has extended further below its 100 and 200 SMAs. A break below 110.70, the immediate support, should lead to a continued decline towards 109.90, the 50% retracement of the November/December rally.

Support levels: 110.70 110.30 109.90

Resistance levels: 111.15 111.60 112.00

GBP/USD

Despite multiple negative headlines coming from the UK, the GBP/USD pair managed to close the day flat around 1.2481. There were no macroeconomic releases in the UK, but Brexit jitters were at top of the list, as, ahead of the trigger of the Art. 50 next week, the EU and the UK are already engaged in a discussion. EU authorities are claiming a bill that can go up to £60 billion for different liabilities including UK's share of pensions liabilities, loan guarantees and spending on UK-based projects, whilst UK government don't recognize such debt, talking about a maximum payment of £2-3 billion. Also, the Scottish parliament was set to debate on a second independence referendum, but got suspended it in the wake of the Westminster terror attack. At least two people died in an incident at the Housed of Parliament, with a vehicle mowing down about a dozen pedestrians on London's Westminster Bridge, before crashing into the Houses of Parliaments and stabbing a police officer being shot down. The GBP/USD pair bottomed at 1.2423 with the news, and slowly moved back higher to match its opening level. From a technical point of view, the risk remains towards the downside, given that the pair held above 1.2425, a major Fibonacci support, while in the 4 hours chart the price bounced sharply after flirting with a bullish 20 SMA. In the same chart, technical indicators have resumed their advances within positive territory, now nearing overbought territory, with scope to extend up to 1.2540, on a break above 1.2505, the daily high.

Support levels: 1.2460 1.2425 1.2390

Resistance levels: 1.2505 1.2540 1.2585

GOLD

Gold prices kept rallying this Wednesday, with spot reaching a fresh 1-month high of $1,25.24 a troy ounce, to settled around 1,249.75. The commodity advanced for a fifth consecutive day, backed by a decline in high-yielding assets, although gains were moderated considering the slump in worldwide equities. A weaker dollar alongside with falling yields and increasing risk aversion, supported the metal. From a technical point of view, the daily chart shows that technical indicators have extended their advances, maintaining their upward momentum now near overbought readings, whilst the price has settled above a still bearish 200 DMA for the first time since last October, supporting some further advances up to 1,263.79, February high. Shorter term, and according to the 4 hours chart the risk is also towards the upside, as technical indicators have resumed their advances within overbought territory, whilst the 20 SMA accelerated its advance below the current level, after surpassing the 100 and 200 SMAs.

Support levels: 1,244.50 1,236.80 1,230.10

Resistance levels: 1,251.30 1,263.80 1,272.80

WTI CRUDE

West Texas Intermediate crude oil futures fell down to $47.07 a barrel, following the US EIA stockpiles report, showing that crude inventories in the country rose by more than expected in the week ended March 17th, up by 4.954 million barrels, ringing total US crude oil inventories to 533.1 million barrels. The commodity bounced from the mentioned low, which was last seen in November, when the OPEC announced its output cut deal, and settled at $48.06 a barrel, down by 20 cents daily basis. The recovery was a consequence of persistent dollar's weakness rather than positive news from the sector, implying that the risk of additional declines on US increasing production headlines remains high. From a technical point of view, the bearish strength remains intact according to the daily chart, with the price further below all of its moving averages, and technical indicators consolidating within oversold levels. In the 4 hours chart, WTI remains below a bearish 20 SMA, whilst technical indicators have managed to bounce from oversold readings, but remain well below their mid-lines, limiting chances of a steeper recovery.

Support levels: 47.70 47.00 46.40

Resistance levels: 48.30 48.90 49.50

DJIA

US indexes managed to pared losses, with Wall Street closing mixed after Tuesday's slump. The Dow Jones Industrial Average closed at 20,661.30, down 6 points, whilst the Nasdaq Composite advanced 27 points and settled at 5,821.64 and the S&P also closed higher, up 4 points or 0.19%, to 2,348.45. The Dow was weighed by a sharp decline in industrials, with Nike leading losers, closing down 6.88%. Verizon Communications followed, but lost just 0.92%. The technology sector led the advance, with Microsoft up 1.1%, Apple adding 1.08% and Intel 0.98%. The DJIA established a fresh March low at 20,578, and the daily chart shows that it remains well below a now horizontal 20 DMA, whilst technical indicators have turned flat near oversold territory, not enough to suggest downward exhaustion. In the 4 hours chart, the bearish stance persists from a technical perspective, as indicators have resumed their declines within oversold territory, whilst the index was unable to recover above any of its moving averages, with the nearest being the 200 SMA at 20,707.

Support levels: 20,610 20,578 20,526

Resistance levels: 20,707 20,732 20,783

FTSE 100

The FTSE 100 extended its slide, shedding 53 points or 0.73%, to close at 7,324.72, as Wall Street's Tuesday decline weighed on investors' mood. Analysts blame the ongoing slump in equities to disappointment over US President Trump, as the promises made at the beginning of his mandate remained unfilled, particularly as the financial and industrial sectors were the worst performers these days. Within the Footsie, mining-related equities led gainers, with Antofagasta up 1.69%, followed by Anglo American that added 1.44% and Randgold Resources that closed 1.39% higher. In the losers' list, Kingfisher shed 5.09%, while Standard Life closed 2.78% lower. The index recovered modestly after the cross, as Wall Street pared losses. Nevertheless, the daily chart shows that the index remains below its 20 DMA, while technical indicators hold below their mid-lines, although having lost their bearish strength. In the 4 hours chart, the technical setting favors the downside, as the 20 SMA has turned lower well above the current level, whilst technical indicators have resumed their declines near oversold levels.

Support levels: 7,294 7,262 7,239

Resistance levels: 7,367 7,400 7,439

DAX

European equities tracked losses from their overseas counterparts, with all of the major benchmarks closing in the red. The German DAX lost 57 points or 0.48% and closed at 11,904.12, as investors continued to unwind the so-called "Trump-trade." Volkswagen was the best performer, up 2.0%, followed by SAP that added 1.05%. Deutsche Boerse, on the other hand, led decliners, down 2.79%, and followed by Linde that closed 1.38% lower. From a technical point of view, the downward potential moderated, but is still present, given that in the daily chart, the index settled again below a now flat 20 SMA, but technical indicators lost bearish strength and stand horizontal right below their mid-lines. In the 4 hours chart, the German benchmark remained below its 20 and 100 SMAs, with the shortest gaining bearish strength above the largest, whilst technical indicators have recovered modestly from near oversold readings, but remain well below their mid-lines.

Support levels: 11,895 11,851 11,811

Resistance levels: 11,949 11,987 12,039

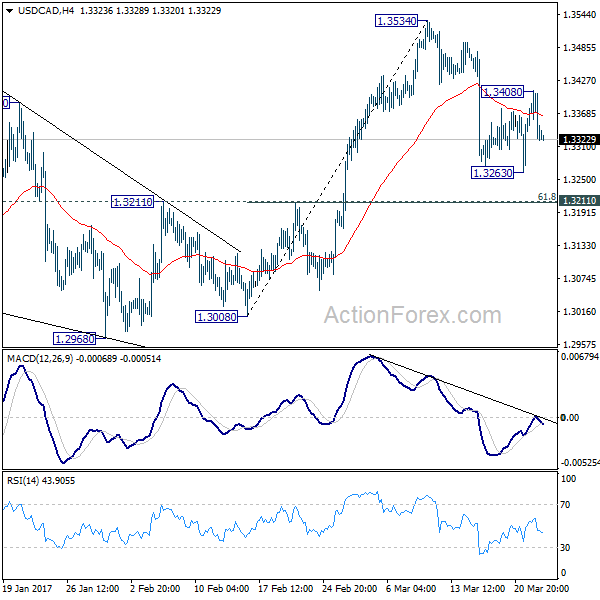

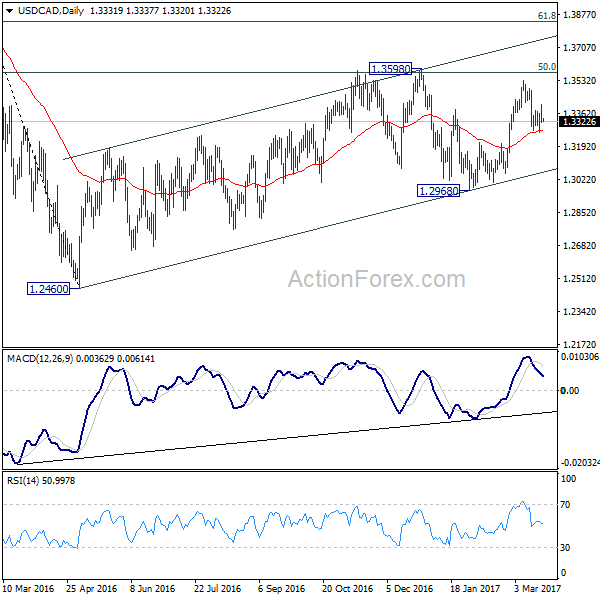

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3296; (P) 1.3352; (R1) 1.3386; More....

USD/CAD's rebound lost momentum after hitting 1.3408. 4 hour MACD crossed below signal line again and it's held by near term trend line too. Intraday bias is turned neutral first. On the upside, above 1.3408 will affirm the case that pull back from 1.3534 has completed. And, intraday bias will be back on the upside for retesting 1.3534. Break there will target 1.3598 high. On the downside, in case of another fall, we'd expect strong support from 1.3211 cluster level (61.8% retracement of 1.3008 to 1.3534 at 1.3209) to contain downside and bring rebound. Overall, we're still expecting the medium term rise from 1.2460 to resume later.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

EM Asia-Don’t Lose The Plot

EM Asia

Reflationary trades have hit a speed bump. But while the latest headlines from the Foggy Dew are negatively impacting, the issue has more to do with the fact that the commodity-linked currencies failed to capitalise on the dovish Fed. At the same time, the confluence of political risk on both sides of the pond weighed and I suspect it is more to do with the recent commodity supply concerns stemming from the oil glut that has commodity traders parked temporarily in neutral.

In the meantime, Asia EM will be held ransom to the ebb and flow in risk appetite and overall commodity market conviction. But if we consider the softer outlook for the USD on the back of the dovish Fed hike, local EMs are unlikely to yield even more so that institutional and retail positioning isn't especially thick, which suggests there will be no sudden rush for the exits due to overweight books.

We've witnessed moderate sell-off in KRW, INR suggests that both pairs will have a high beta correlation to the sell-off in global equities and should reap the rewards on the anticipated return of risk.

The MYR is in a similar position but as we near the apparent bottom of oil prices, I expect the Ringgit to be more sensitive to volatile oil prices.

The pullback in commodity prices was anticipated, as we all know nothing goes up forever, even more so if we consider over extended positioning in both Copper and Iron Ore. But the Trump reflationary trade is far KO'd. Oil prices could conceivably move lower, but given the hawkish rhetoric from OPEC and the anticipated bounce in global growth, vis a vis US tax and fiscal reform, it's far too early to give up the plot. Don't let this wave of risk-off muddy the big picture as commodity traders are likely waiting in earnest to fade any further capitulation.

I still view the eventual move higher in US fixed income Yields as the most significant headwind for regional EM, and while US 10 year yields are expected to move higher throughout 2017, I suspect the undervalued regional equity markets and the higher yields on offer from local capital markets will keep the regional currencies in check.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7647; (P) 0.7668; (R1) 0.7697; More...

AUD/USD is trying to draw support from 4 hour 55 EMA for the moment but recovery is weak. Intraday bias stays on the downside first. As noted before, rebound from 0.7490 should have completed. Deeper fall would be seen back to 0.7490 support. Break there will confirm completion of whole rise from 0.7158. On the upside, above 0.7748 will resume the rise from 0.7158. But in that case, we'd expect upside to be limited by 0.7849/50 cluster resistance to bring reversal. That level represents 61.8% projection of 0.7158 to 0.7740 from 0.7490 at 0.7850 and key long term retracement level at 0.7849.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8169) and above.

Kiwi Steady as RBNZ Stands Pat, Vote on Trump’s Health Care Act Watched

New Zealand dollar is steadily in range after RBNZ stands pat as widely expected. The central bank left the Official Cash Rate unchanged at record low of 1.75% and maintained a neutral stance. Governor Graeme Wheeler reiterated in the statement that "monetary policy will remain accommodative for a considerable period." And, "numerous uncertainties remain, particularly in respect of the international outlook, and policy may need to adjust accordingly." RBNZ acknowledged that the "trade-weighted exchange rate has fallen 4 percent since February, partly in response to weaker dairy prices and reduced interest rate differentials." While this seen as an "encouraging move" by the central bank, it reiterated that "further depreciation is needed to achieve more balanced growth."

RBNZ said that "quarterly GDP was weaker than expected in the December quarter, but some of this is considered to be due to temporary factors. The growth outlook remains positive, supported by on-going accommodative monetary policy, strong population growth, and high levels of household spending and construction activity." Regarding inflation, RBNZ noted that "headline CPI will be variable over the next 12 months due to one-off effects from recent food and import price movements, but is expected to return to the midpoint of the target band over the medium term."

Canada budget: Stay the course

Canadian dollar recovered as selloff in risk markets stabilized. WTI crude oil also recovered mildly and is back above 48 handle. The Canadian government unveiled a "stay-the-course" federal budget with few surprises. It's perceived that the government would like to wait-and-see what US president Donald Trump would deliver on his policies first. The budget deficit is at CAD 23.0b in fiscal 2016/27 comparing to CAD 25.1b indicated last fall. But the government expects higher deficit onwards, at CAD 28.5b in fiscal 2017/18. Deficit is projected to trend low to CAD 18.8b by fiscal 2021/22.

More on Canada budget

- Canada 2017 Federal Budget: Stay the Course Budget - Expected and Delivered

- Canada 2017 Federal Budget - Back to Business as Usual

House to vote on Trump's AHCA

In US, stocks stabilized after the steep selloff on Tuesday. DJIA dipped to 20578.95 but pared back some losses to close at 20661.30, down -0.03% only. S&P 500 gained 0.19% to close at 2348.45, after hitting as low as 2336.45. NASDAQ was relatively stronger and closed up 0.48% at 5821.64. The major focus today is the vote on US president Donald Trump's American Health Care Act in House. Ahead of the vote, the Congressional Budget Office released a report noting that the AHCA will release in 24 million people losing coverage over the next decade. And the costs for those insured could skyrocket, including the elderly. But nonetheless, the vote is seen as a litmus test for Trump as markets are getting more doubtful in his ability to push through economic policies.

Elsewhere...

Germany will release Gfk consumer sentiment while UK will release retail sales and CBI reported sales. Eurozone will release consumer confidence. US will release jobless claims as usual on Thursday, as well as new home sales.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7647; (P) 0.7668; (R1) 0.7697; More...

AUD/USD is trying to draw support from 4 hour 55 EMA for the moment but recovery is weak. Intraday bias stays on the downside first. As noted before, rebound from 0.7490 should have completed. Deeper fall would be seen back to 0.7490 support. Break there will confirm completion of whole rise from 0.7158. On the upside, above 0.7748 will resume the rise from 0.7158. But in that case, we'd expect upside to be limited by 0.7849/50 cluster resistance to bring reversal. That level represents 61.8% projection of 0.7158 to 0.7740 from 0.7490 at 0.7850 and key long term retracement level at 0.7849.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seek to 55 month EMA (now at 0.8169) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% | 1.75% | |

| 7:00 | EUR | German GfK Consumer Confidence Apr | 10 | 10 | ||

| 9:00 | EUR | ECB Economic Bulletin | ||||

| 9:30 | GBP | Retail Sales M/M Feb | 0.40% | -0.30% | ||

| 11:00 | GBP | CBI Retailing Reported Sales Mar | 4 | 9 | ||

| 12:30 | USD | Initial Jobless Claims (MAR 18) | 240k | 241k | ||

| 14:00 | USD | New Home Sales Feb | 566k | 555k | ||

| 14:30 | USD | Natural Gas Storage | -53B | |||

| 15:00 | EUR | Eurozone Consumer Confidence Mar A | -5.8 | -6.2 |

Market Morning Briefing

STOCKS

Equity indices may test immediate support levels which could attempt to produce some bounce in the near term.

Dow (20661.30, -0.03%) has taken support on the daily candles near 20578 and in case this holds, we could see an attempt to move higher towards 21000 in the next few sessions but in case the support breaks on the downside, we would have to get ready to see levels near 20400 or even lower in the medium term.

Dax (11904.12, -0.48%) is headed towards support near 11700 and if that holds, we could see a rise to levels near 12000 again.

Nikkei (19068.22, +0.14%) is trading within the 19600-18600 region. No major movement expected just now and we could possibly see another 1-2 sessions with small or stable movements. Note important 21-week MA that could possibly act as an immediate support.

The channel support on the daily candle is holding well on Shanghai (3257.14, +0.37%). If it continues to holds in the near term, we could see a bounce towards 3275 and higher in the coming sessions.

Nifty (9030.45, -1.0%) could possibly get some support near 8990-9000 from where a bounce could be expected (a max low of 8970/60 is possible on a break of 8990, if seen) towards 9100.

COMMODITIES

Gold (1245) found resistance at 1250 and trading within a narrow range of 1240-1250. A break on either side could be decisive.

Silver (17.54) still shows no sign of direction as it is hovering around its pivot at 17.45 of its trading range of 16.82-18.00.

Copper (2.62) found support at 2.57 levels. While 2.57 hold, a bounce to the interim resistance 2.68-70 can be seen. Only above 2.70, higher resistances of 2.80 can come into consideration. In the medium term 2.55-57 are going to be a strong support now and the chances of a close above 2.70 have increased.

With a 5.0M barrel surplus in U.S. weekly crude inventory, both Brent (50.93) and WTI (47.34) has fallen in line with our expectation. We are bearish on Brent and WTI since 8th March, 17 . Considering the short term oversold sate, we may see some profit taking rally towards their respective resistances of 52-53 for Brent and 48.50-49.80 for WTI respectively. But the trend is still bearish in the near to medium term time frame. Any corrective bounce may face selling pressure at the higher levels.

FOREX

The markets are very quiet, waiting for the Fed Chair Yellen’s speech and the Republican attempt to pass a health-care bill tonight.

It is just another session for Dollar Index (99.82) below 100 with little activity seen in the markets. Upside remains limited to 100.50 in the near term. Repeat – the narrow band of 99.00-98.50 is a very significant support zone which may be tested in the coming days

Euro (1.0785) is consolidating at the higher levels not too far away from the major resistance of 1.0830-50.As discussed yesterday, though the upside possibilities must be considered more now, we prefer to wait and watch till a clean break above 1.0850 is seen.

Dollar-Yen (111.44) may face selling pressure near 111.70-112.00 and 113.00, if it manages to rise that high, in any bounce with greater chances of seeing 110 in the near term.

Pound (1.2482) has tested the support of 1.2440-20 and bounced back strongly, indicating its intention to rise higher towards 1.2650-1.2700.

Aussie (0.7654) is stable inside the band of 0.7600-0.7750 as expected and this range may continue for a few sessions more with a downward bias in the medium term.

Dollar Rupee (65.44) moved little in the last session as it closed exactly at the midpoint of our expected range of 65.20-70. As stated before, the sideways consolidation is expected to continue.

INTEREST RATES

The US yields have paused. The 5yr (1.95%), 10YR (2.42%) and the 30Yr (3.03%) are stable and could see a slight bounce in the next couple of sessions.

The US 10-5yr (0.46%) is down 1bps and could head towards 0.45% in the near term.

The US-Japan 10YR (2.35%) could bounce from support at current levels indicating that the strength I Yen could be limited in the near term. While the support holds, the near term looks potentially bullish for the yield spread and Dollar-Yen. 9refer FOREX section above for specific view on Yen)

The German-US 10Yr (-2.01%) is testing resistance near current levels which if holds could bring it down towards -2.05% or lower in the near term. This could coincide with the 1.0830 resistance on euro indicating that a corrective dip is on its way for the coming sessions.

GOLD – Bullish, Risk Remains Higher On Further Strength

GOLD - The commodity looks to recover further higher. On the downside, support comes in at the 1,240.00 level where a break will turn attention to the 1,230.00 level. Further down, a cut through here will open the door for a move lower towards the 1,220.00 level. Below here if seen could trigger further downside pressure targeting the 1,210.00 level. Conversely, resistance resides at the 1,260.00 level where a break will aim at the 1,270.00 level. A turn above there will expose the 1,280.00 level. Further out, resistance stands at the 1,290.00 level. All in all, GOLD looks to strengthen further.

Why the House Health Care Vote Matters

The current version of Trump's healthcare plan will be dead-on-arrival in the Senate yet Thursday's vote in the House is a blockbuster. We explain why. The yen was the top performer on Wednesday while the Australian dollar lagged. A new Premium trade has been issued ahead of the House vote, backed by 4 technical reasons and 4 charts. 5 out of the 7 existing Premium trades are currently in the green.

The risk aversion in markets stopped on Wednesday but a more-accurate description was that it was on pause. The market is trying to figure out if the House vote on Thursday on the bill to replace Obamacare will pass or fail.

The bill itself isn't so much what's at stake. The market is increasingly viewing it as a test of Republican leadership. It's a barometer on whether Paul Ryan and Donald Trump can whip the House into supporting its agenda.

So what's at stake isn't necessarily this bill. It's the tough fights on tax reform, infrastructure and regulation that are ahead. The mantra of 'repeal and replace' Obamacare was the one thing seemingly every Republican agreed upon but exactly how that would work is proving to be a problem.

A risk we see here is that the market is overstating the problem. This isn't a Republican vote on Trump, his leadership or team unity. It's a vote on a specific piece of legislation and some Congressmen want it changed.

In that sense, buying something like USD/JPY or equities could have limited downside risks. If it passes, it's all upside. If the vote fails or is postponed, there will be selling but Republicans will quickly regroup and move forward. Markets will recognize that sooner than some think.

Changing gears to central banking, the RBNZ held rates at 1.75%, as expected. The anti-NZD jawboning continued and the message was largely unchanged. One small shift was language saying inflation will return to target in the medium-term, rather than 'gradually'. NZD initially dipped but is back to pre-RBNZ levels.

The rest of the Asia-Pacific calendar is light but it will pick up later with UK retail sales and Yellen on the agenda.