Sample Category Title

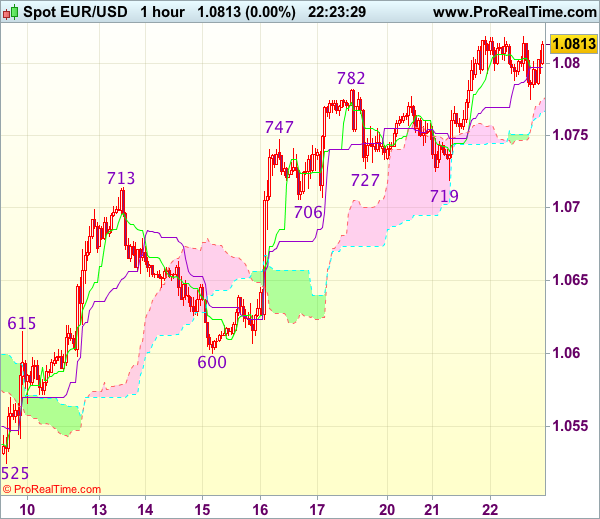

Trade Idea Update: EUR/USD – Buy at 1.0725

EUR/USD - 1.0810

Original strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

As the single currency has maintained a firm bias after surging again yesterday, suggesting recent erratic upmove from 1.0493 low is still in progress and may extend further gain to previous chart resistance at 1.0829, however, loss of near term upward momentum should prevent sharp move beyond 1.0850-60 and price should falter well below 1.0890-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0706 support should limit downside and bring another rise later. Below 1.0675-80 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

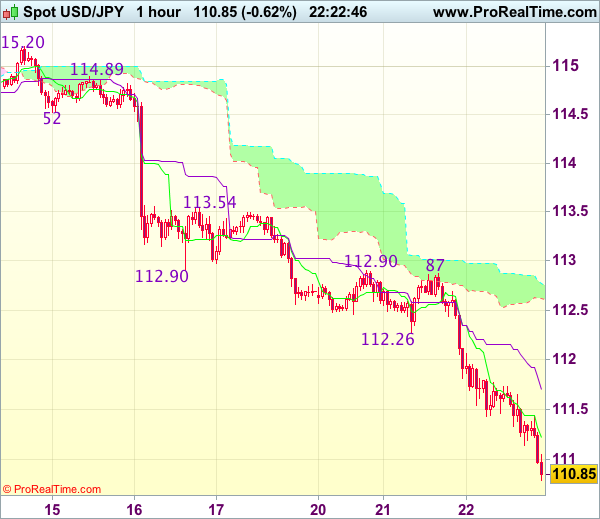

Trade Idea Update: USD/JPY – Sell at 111.70

USD/JPY - 110.88

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.62

Kijun-Sen level : 112.15

Ichimoku cloud top : 112.88

Ichimoku cloud bottom : 112.54

New strategy :

Sell at 111.70, Target: 110.60, Stop: 112.05

Position : -

Target : -

Stop : -

As the greenback has dropped again in US morning, adding credence to our view that recent decline is still in progress and may extend further fall to 110.50-55, however, near term oversold condition should prevent sharp fall below 110.20-25 and reckon 110.00 would hold from here, risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as the Kijun-Sen (now at 111.70) should limit upside. Above 112.00 would defer and risk test of previous support at 112.26 but break there is needed to signal low is formed instead.

Dow is Riding on Extended Wave C

Dow is riding on extended wave C from 21028 lower top that so far extended to its 123.6% Fibonacci expansion at 20549.

Tuesday's strong fall completed Failure Swing pattern on daily chart that signals further downside.

The wave could travel towards 20492 and 20401, its FE 138.2% and 161.8% respectively, driven by building negative sentiment, weakening daily studies and strong bearish signals on reversal of weekly RSI / slow stochastic from overbought territory.

We are looking for fresh negative signal on daily close below broken support at 20607 (Fibo 38.2% of 19713/21160 upleg that now acts as initial resistance), for extension of the third wave.

Daily Tenkan-sen / Kijun-sen bear-cross at 20790, marks upper trigger, break of which is needed to neutralize existing downside risk.

Res: 20607; 20736; 20790; 20848

Sup: 20549; 20492; 20401; 20266

USD/CAD 1.3435-55 Possible Sell Zone

The USD/CAD dropped substantially from 1.3470 zone making a strong momentum candle that marked end of uptrend on intraday/week time frames. As I showed in my previous USD/CAD coverage, the piar dropped from POC zone in range bound market. Now we have another POC zone 1.3435-55 (88.6, Daily H5, order block Weekly H4, ATR top) where now moment sellers might be waiting. The rejection from POC zone is targeting 1.3377, 1.3325 and possibly 1.3300. have in mind that price needs to break 1.3405 H4 in order to retrace to POC zone.

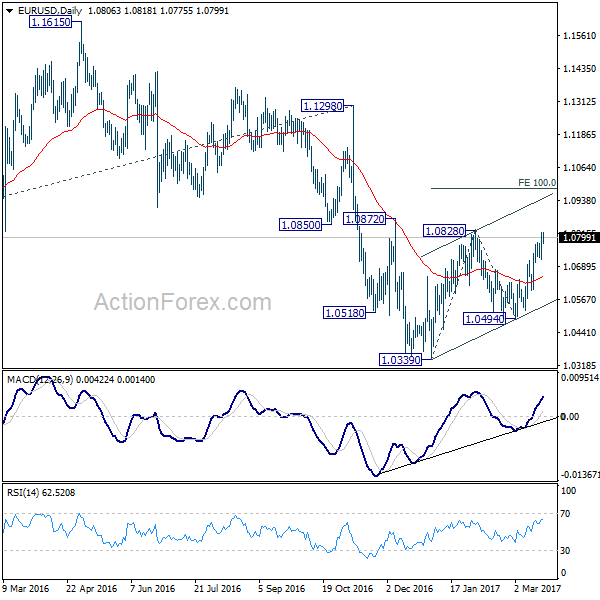

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0747 (R1) 1.0769; More.....

With 1.0718 minor support intact, intraday bias in EUR/USD remains on the upside for 1.0828 resistance. Break there will target 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. However, as rise from 1.0339 is seen as a corrective move. We'd expect upside to be limited by 1.0983 to complete the correction. On the downside, break of 1.0718 minor support will turn bias to the downside for 1.0494 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to resume later. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

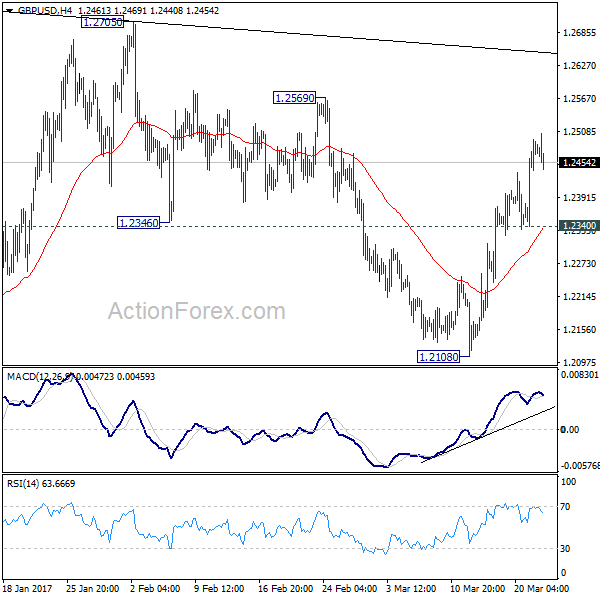

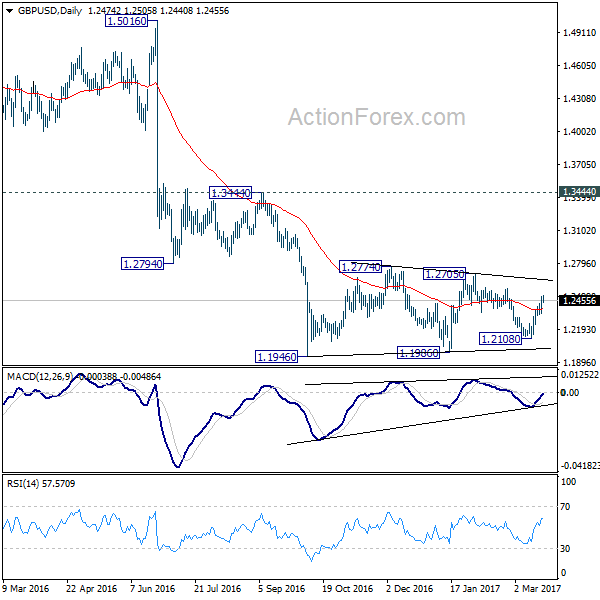

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2437; (R1) 1.2535; More...

Intraday bias in GBP/USD remains on the upside as rise from 1.2108 continues. Their pair would target 1.2569 resistance first and break will target 1.2705/74 resistance zone. But still, price actions from 1.1946 are seen as a consolidation pattern. Hence, we'd expect strong resistance from 1.2705/2774 to limit upside and bring down trend resumption. On the downside, break of 1.2340 support will turn bias back to the downside for 1.2108 support. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

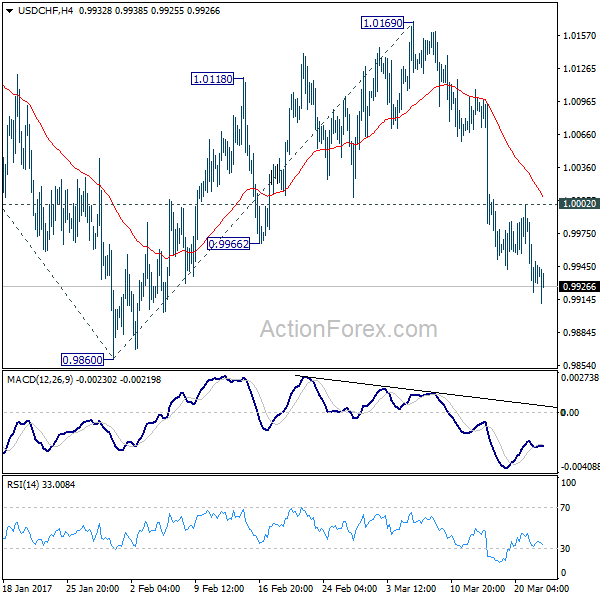

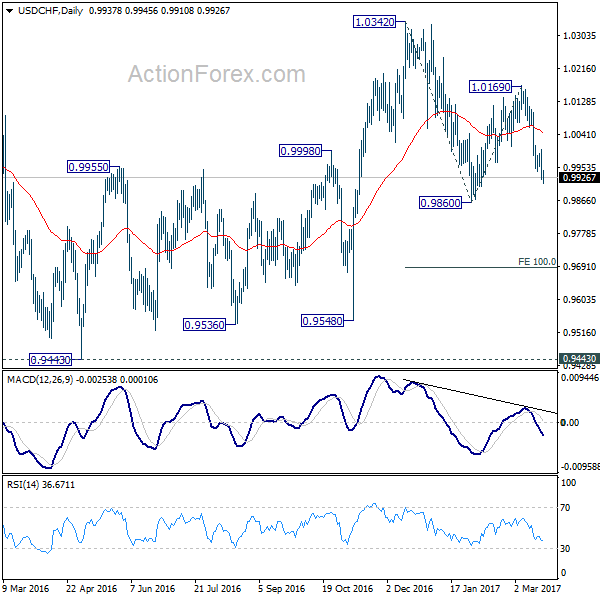

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9905; (P) 0.9953; (R1) 0.9985; More.....

Intraday bias in USD/CHF remains on the downside and fall from 1.0169 should target 0.9860 support next. Whole decline from 1.0342 is likely resuming and break of 0.9860 will target 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687. Nonetheless, on the upside, break of 1.0002 minor resistance will turn bias back to the upside for 1.0169 resistance instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.21; (P) 112.03; (R1) 112.54; More...

USD/JPY drops to as low as 111.13 so far today and is pressing 111.12/13 cluster support. Such support level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. At this point, we'd still anticipate strong support around 111.12/13 to contain downside and bring rebound. Break of 112.86 resistance will turn bias back to the upside for 115.49 resistance first. However, sustained break of 111.12/13 will bring deeper decline to 100% projection of 118.65 to 111.58 from 115.49 at 108.42.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.19) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Risk Aversion Dominates and Global Selloff Continues

Risk aversion dominates the financial markets today. European indices are trading broadly lower with FTSE leading the way by losing more than -0.7%. CAC and DAX are both down -0.5% respectively. DJIA had the worst day for this year yesterday and is set to extend the sharp fall as suggested by futures. Nikkei lost -2.13% earlier today as additionally pressured by report of North Korea's failed missile test. Stocks are sold off sharply on concerns that US president Donald Trump doesn't have the ability to fulfil his election promises and push through his policies. Those include tax cuts and infrastructure spending. US House is set to vote on Trump's healthcare plan and that is seen as a litmus test for him. In the currency markets, Yen is leading the way higher on safe haven flow, followed by Swiss Franc. Aussie is trading as the weakest one.

ECB: Protectionism may increase trade deficit

ECB said in a study paper released today that protectionist trade policies may increase a country's trade deficit, rather than reduce it. The paper noted that "adopting policies that facilitate innovation and reduce protectionist barriers may help to improve an economy's competitiveness." And, "multilateral initiatives aimed at trade and financial liberalization may also reduce an economy's external imbalances." Meanwhile, "participating in global value chains may give an economy a temporary competitive edge that results - in order to smooth consumption over time - in a rise in its current account balance.

Separately, ECB governing council member, Bank of France head François Villeroy de Galhau said that it's a "clear no" for the central to stop accommodative monetary policy. He said that "without monetary stimulus, the recovery in inflation would not yet be self-sustained or durable throughout the euro area."

BoJ members rejected lifting bond yield targets

BOJ's minutes for the January meeting sent little news about Japan's monetary policy stance. Policymakers discussed about rising JGB yields but the majority rejected the idea of raising the 10-year JGB yield target to match expected gains in Treasury yields. The members suggested that BOJ should focus on achieving the 2% inflation target. As noted in the minutes, "although some market participants speculated that the Bank might consider raising the target level of the long-term interest rate in response to such factors as a rise in the U.S. long-term interest rates, its monetary policy decisions should be made solely based on the viewpoint of aiming to achieve the 2% price stability target".

Japan trade surplus widened to JPY 0.68T in February, above expectation of 0.55T. Exports jumped 11.3% yoy, fastest since January 2015. Exports to China jumped 28.2% yoy, accelerated from 3.1% yoy in the prior month. Some analysts noted that even stripping out the Lunar New Year effects, exports still picked up as a trend. All industry activity index rose 0.1% mom in January.

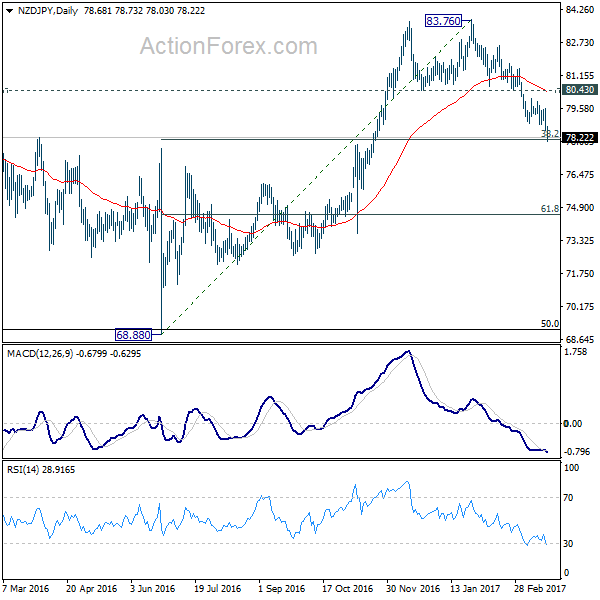

NZD/JPY dives on risk aversion ahead of RBNZ

RBNZ rate decision will be a major focus in the coming Asian session. The central bank is widely expected to keep the Official Cash Rate unchanged at 1.75%. It sounded neutral in last statement and just noted that "monetary policy will remain accommodative for a considerable period." There was no explicitly mentioning of its policy bias. RBNZ will likely maintain such stance. Meanwhile, it would likely reiterate that "exchange rate remains higher than is sustainable for balanced growth". And, "a decline in the exchange rate is needed."

Kiwi is relatively steady against Dollar this week. But NZD/JPY dives notably on risk aversion. The rejection from 83.36 key long term resistance confirmed medium term topping at 83.76 back in January. The development also indicates that rebound from 68.88 (2016 low) has completed. Medium term outlook will now stay bearish as low as 80.43 support resistance holds. 38.2% retracement of 68.88 to 83.76 at 78.07 is seen as an important support. But based on current momentum, this support will likely be taken out as the cross head towards 61.8% retracement of 68.88 to 83.76 at 74.56 ahead.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.21; (P) 112.03; (R1) 112.54; More...

USD/JPY drops to as low as 111.13 so far today and is pressing 111.12/13 cluster support. Such support level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. At this point, we'd still anticipate strong support around 111.12/13 to contain downside and bring rebound. Break of 112.86 resistance will turn bias back to the upside for 115.49 resistance first. However, sustained break of 111.12/13 will bring deeper decline to 100% projection of 118.65 to 111.58 from 115.49 at 108.42.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.19) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Feb | -0.10% | 0.00% | ||

| 23:50 | JPY | BOJ Minutes (Jan 30-31) | ||||

| 23:50 | JPY | Trade Balance (JPY) Feb | 0.68T | 0.55T | 0.16T | 0.20T |

| 4:30 | JPY | All Industry Activity Index M/M Jan | 0.10% | 0.00% | -0.30% | -0.20% |

| 9:00 | EUR | Eurozone Current Account (EUR) Jan | 24.1B | 29.3B | 31.0B | 30.8B |

| 13:00 | USD | House Price Index M/M Jan | 0.40% | 0.40% | ||

| 14:00 | USD | Existing Home Sales Feb | 5.59M | 5.69M | ||

| 14:30 | USD | Crude Oil Inventories | -0.2M | |||

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

DAX Fell Below 11900 Support

DAX fell below 11900 support (Fibo 38.2% of 11459/12177 rally) on Wednesday, in extension of previous day's strong fall, when the index was down 1.34%.

Near-term studies turned into full bearish mode, while daily technicals are losing traction.

Close below 11900 handle is needed to signal further easing that may extend towards 11818 (50% retracement) and 11785 (55SMA).

The notion is supported by overbought weekly studies and bearish divergence on weekly slow stochastic.

Broken daily Kijun-sen so far caps upside attempts at 11932, with extended upticks expected to stay below daily Tenkan-sen (12027) to keep fresh bears in play.

Res: 11932; 11980; 12027; 12098

Sup: 11878; 11818; 11785; 11733