Sample Category Title

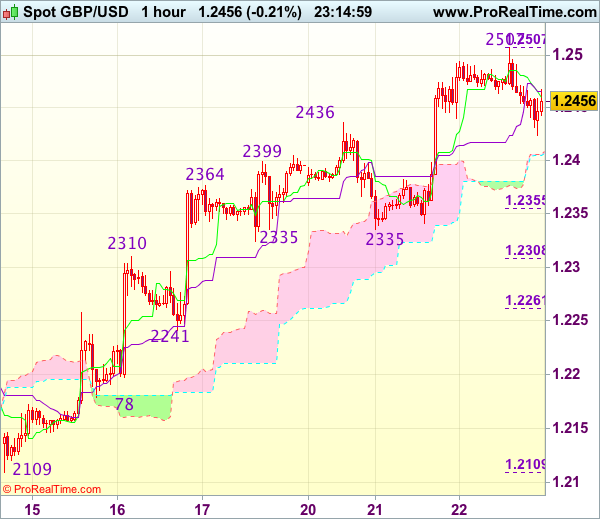

Trade Idea Wrap-up: GBP/USD – Buy at 1.2355

GBP/USD - 1.2466

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2460

Kijun-Sen level : 1.2466

Ichimoku cloud top : 1.2406

Ichimoku cloud bottom : 1.2405

Original strategy :

Buy at 1.2355, Target: 1.2500, Stop: 1.2320

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2355, Target: 1.2500, Stop: 1.2320

Position : -

Target : -

Stop : -

As cable has retreated after intra-day brief rise to 1.2507, suggesting consolidation below this level would be seen and pullback to 1.2400-10 is likely, however, reckon downside would be limited to 1.2350-55 (38.2% Fibonacci retracement of 1.2109-1.2507) and bring rebound later, above said resistance at 1.2507 would signal the rise from 1.2109 has resumed and extend gain to 1.2540-50 but loss of upward momentum would limit upside and price should falter below previous chart resistance at 1.2570.

In view of this, would not chase this move from here and we are looking to buy cable on subsequent pullback as 1.2350-55 should limit downside. Below strong support at 1.2335 would abort and signal top is formed instead, risk correction to 1.2305-10 (50% Fibonacci retracement of 1.2109-1.2507) first.

Yen Climbs on Strong Japanese Trade Surplus, Soft US Housing Report

The Japanese yen continues to make inroads against the US dollar in Wednesday trading. In the North American session, USD/JPY is trading at the 111 line, as the yen hit a 4-month high earlier in the day. On the release front, Japan's trade surplus soared to JPY 0.68 trillion, well above the forecast of JPY 0.55 trillion. As well, the BoJ released the minutes of its January policy meeting. In the US, housing and inflation data was a disappointment. Existing Home Sales dropped to 5.48 million, missing the forecast of 5.59 million. As well, the House Price Index fell to a flat 0.0%, short of the estimate of 0.4%. On Thursday, the US releases unemployment claims.

With little in the way of key fundamentals this week, the markets are focusing on comments from FOMC members who will be speaking this week, including Fed Chair Janet Yellen on Thursday. On Monday, Chicago Fed President Charles Evans said he expects the Fed to raise rates two more times this year. This echoes the Fed's dot point plot as well as last week's rate statement. Although three rate hikes in 2017 would be no mean feat, the markets would like four hikes, given the strong performance of the US economy. The Fed's cautious approach has disappointed the markets, as the US dollar continues to post broad losses. The yen has taken full advantage, gaining 3.3 percent against the dollar since the Fed policy meeting last week.

Donald Trump continues to trumpet his "America first" slogan, and the US president's protectionist stance has sent off alarm bells in Japan, which is heavily dependent on free trade. Immediately after taking office, Trump pulled the US out of the Trans-Pacific Partnership deal, an enormous free-trade agreement which Japan had enthusiastically supported. Japan has embarked on finding other trading partners in order to lessen its dependence on the US. Japanese Prime Minister Shinzo Abe met with EU President Donald Tusk on Tuesday, and the two discussed the Japanese-EU trade agreement, which was supposed to be finalized in 2015. With Europe still fuming over the 'Brexit burn' delivered by Britain, there is likely more appetite on the part of the EU to conclude an agreement with Japan, the world's third largest economy.

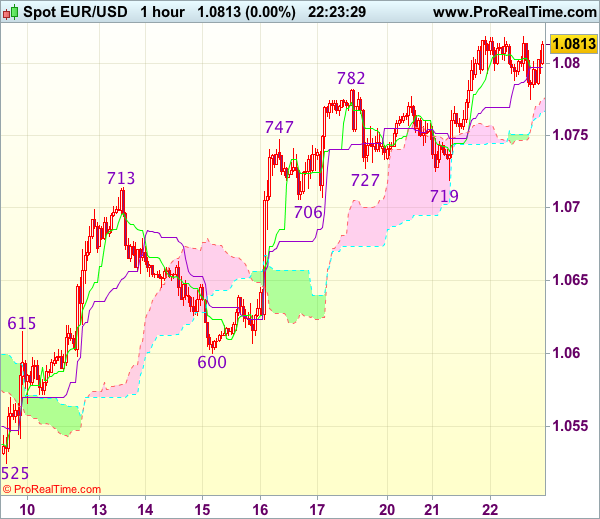

Trade Idea Wrap-up: EUR/USD – Buy at 1.0725

EUR/USD - 1.0810

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0800

Kijun-Sen level : 1.0800

Ichimoku cloud top : 1.0776

Ichimoku cloud bottom : 1.0768

Original strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

As the single currency has maintained a firm bias after surging again yesterday, suggesting recent erratic upmove from 1.0493 low is still in progress and may extend further gain to previous chart resistance at 1.0829, however, loss of near term upward momentum should prevent sharp move beyond 1.0850-60 and price should falter well below 1.0890-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0706 support should limit downside and bring another rise later. Below 1.0675-80 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

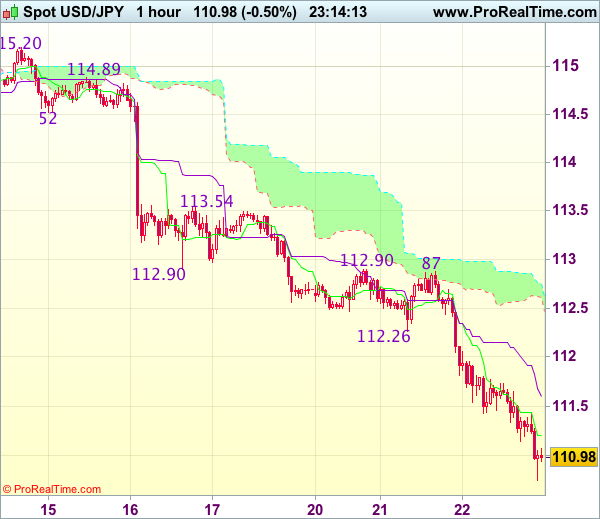

Trade Idea Wrap-up: USD/JPY – Sell at 112.00

USD/JPY - 111.14

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.20

Kijun-Sen level : 111.60

Ichimoku cloud top : 112.75

Ichimoku cloud bottom : 112.61

Original strategy :

Sell at 111.70, Target: 110.60, Stop: 112.05

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.00, Target: 110.80, Stop: 112.35

Position : -

Target : -

Stop : -

As the greenback has dropped again in US morning, adding credence to our view that recent decline is still in progress and may extend further fall to 110.50-55, however, near term oversold condition should prevent sharp fall below 110.20-25 and reckon 110.00 would hold from here, risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 112.00 should limit upside. Only above indicated previous support at 112.26 would abort and signal low is formed instead, bring a stronger rebound to 112,59 but resistance at 112,87-90 should cap upside.

USD/JPY Losing First Important Support Area

Headlines

European stock markets lost up to 1% at some stage, but partly erased losses as Brent crude manages to stay above $50/barrel support. The Trump reflation trade continues to show signs of fatigue though with US equities slightly extending losses in the opening. US existing home sales disappointed (-3.7% M/M in February), but are ignored.

The PBOC pumped $5.8B into China's money market, intervening for a third day after the benchmark money rate hit its highest level since April 2015 as some smaller lenders were said to have missed payments in the interbank market.

Profitability is now the most important challenge facing the eurozone's banks, France's top central banker has said, in an acknowledgement of the pain caused by low interest rates. However, ECB Villeroy added it was necessary for the ECB to keep its ultra-loose monetary policy in place for now.

Greece said it hopes for a deal with its international lenders within the month of April and is working to bridge differences on labour, pension and energy reforms. The onus for an agreement was not only on the Greek government, but on its EU and IMF lenders too, government spokesman Tzanakopoulos told reporters.

Right-wing presidential candidate Fillon was back under fire following new media reports of conflicts of financial and political interest while a party ally, the head of the influential national association of French mayors, attacked a key part of his radical economic recovery programme.

Portugal's PM has joined the chorus of southern European leaders for the resignation of Dutch FM Dijsselbloem as head of the Eurogroup. Costa said that Dijsselbloem's comments that crisis-hit eurozone countries had wasted their money on "drinks and women" were "absolutely unacceptable" and "very dangerous".

Negative interest rates in Sweden have "had the intended effect" without significantly damaging the wider economy or financial markets, the Riksbank has said, as it strongly defended its programme of monetary stimulus despite the strength of the wider economy.

Rates

Reflation trade shows more signs of fatigue

Global core bonds eked out gains as the Trump reflation trade shows more signs of fatigue. German Bunds outperform US Treasuries in a catch-up move. At the time of writing, the German yield curve bull flattens with yields 2 bps (2- yr) to 5.8 bps (30-yr) lower. Changes on the US yield curve vary between -1.6 bps (2-yr) and -3.1 bps (10-yr). Key support in US yield terms stands at 1.13% (2-yr), 1.8% (5-yr), 2.3% (10-yr) and 2.9% (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany are unchanged with Spain (-4 bps) outperforming.

Intraday, the Bund profited from a bad equity market opening (catching up with US yesterday) and downward pressure on oil prices from the start of European trading. The up-leg lost steam around noon, after which sideways trading kicked in going into the start of US dealings. European stock markets recovered some of the opening losses and Brent crude held above the psychological $50/barrel mark. ECB Villeroy said that at this stage ECB stimulus is still needed while ECB Lautenschlaeger didn't touch on monetary policy. During US dealings, USD/JPY dropped below key support (111.60; see FX) and pushed core bonds to new intraday highs. In this move, US Treasuries profited more than German Bunds. US existing home sales disappointed in February (-3.7% M/M), but didn't influence trading.

The German Finanzagentur tapped the on the run 10-yr Bund (€3B 0.25% Feb2027). Total bids amounted to a disappointing €3.73B (vs €5.24B average at previous 4 Bund auctions) despite the highest auction yield since early 2016 (0.41%). The Bundesbank retained €0.48B of the amount on offer for secondary market operations, resulting in an official bid cover of 1.5.

Currencies

USD/JPY losing first important support area

Today, investors tried to find out what could be next after yesterday's risk-off correction. Risk sentiment remained fragile and core yields declined further, which weighed on the dollar. USD/JPY was still vulnerable. The pair slipped below the 111 big figure. There were no further dollar losses against the euro as the US-German interest rate differential didn't widen further. EUR/USD hovers around the 1.08 big figure.

Overnight, Asian equities joined the risk-off correction from the US, with Japanese equities hit the hardest. USD/JPY tested the key 111.60/36 support area. EUR/USD is held north of 1.08, within reach of the recent highs.

The risk-off correction continued early in Europe. European equities lost up to around 1%, but the decline gradually petered out, as investors were awaiting guidance from the US about the fate of the correction on the reflation trade. USD/JPY hovered in the key support area in the low 111 area. The 111.60/36 support levels were broken, but a new real down-leg didn't occur (yet). The trading pattern of EUR/USD was different. The pair returned below 1.08 as interest rates between the US and Europa widened slightly after the recent narrowing. Maybe the euro also wasn't considered as a safe haven. Admittedly, the correction didn't go far as USD weakness remained the mainstream trend.

US existing homes sales were slightly softer than expected, but the focus for global trading was on the fate the reflation trade. US equities opened little changed, but with few signs of a sustained comeback. At the same time, core bond yields are declining further. This is weighing in the dollar with USD/JPY still showing the most vulnerable pair. It is drifting below the 111 figure. EUR/USD reversed this morning's decline and is trading in the 1.0810/15 within reach of the recent top. However, a clean break of the 1.0829/1.0874 won't be easy.

Sterling stabilizes after yesterday's rally

Today was an uneventful trading for sterling traders. There were no data or other high profile UK specific news. Sterling tried to establish some follow-through gains on yesterday's post-CPI rally. However, the focus was on the global trading dynamics after yesterday's US equity sell-off. In this context, EUR/USD and cable broadly followed a similar intraday trading pattern. Cable even slightly underperformed. However, EUR/GBP was locked in a narrow range in the upper half of the 0.86 big figure (currently in the 0.8670 area). Cable dropped off the overnight top just north of 1.25 and trades in the 1.2455 area. The jury is still out on yesterday's global correction. However, the BoE should be cautious to raise interest rates anytime soon if the global (financial) markets would turn more uncertain. This is a potential negative for sterling.

Trade Idea: EUR/GBP – Buy at 0.8620

EUR/GBP - 0.8684

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Buy at 0.8620, Target: 0.8750, Stop: 0.8580

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8620, Target: 0.8750, Stop: 0.8580

Position : -

Target : -

Stop : -

Although the single currency recovered from 0.8643, as long as indicated resistance at 0.8727 holds, near term downside risk remains for the erratic fall from 0.8788 to bring retracement of recent rise, hence weakness to 0.8620 cannot be ruled out, however, reckon downside would be limited to 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) and bring another rise later, break of 0.8727 would bring test of 0.8760, above there would suggest the pullback from 0.8788 has ended, bring retest of this level, break there would extend the rise from 0.8403 low to 0.8800 and later 0.8825-30.

In view of this, we are looking to buy euro on subsequent pullback as 0.8615-20 should limit downside. Below 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) would defer and suggest top is possibly formed, risk test of 0.8560-65 (61.8% Fibonacci retracement) but support at 0.8547 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Hold short entered at 1.3400

USD/CAD - 1.3371

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Sold at 1.3400, Target: 1.3240, Stop: 1.3460

Position: - Short at 1.3400

Target: - 1.3240

Stop: - 1.3460

New strategy :

Hold short entered at 1.3400, Target: 1.3240, Stop: 1.3435

Position: - Short at 1.3400

Target: - 1.3240

Stop:- 1.3460

Although the greenback rebounded after falling briefly to 1.3264 and consolidation above this level would be seen, reckon upside would be limited and as long as 1.3430 holds, mild downside bias remains for another fall to said support, break there would add credence to our view that top has been made at 1.3535, bring further fall to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) but previous resistance at 1.3210 would hold due to loss of downward momentum.

In view of this, we are holding on to our short position entered at 1.3400. Above previous support at 1.3421 (now resistance) would suggest low is formed instead, bring a stronger rebound to 1.3450 and possibly test of resistance at 1.3479, however, only break of 1.3495 resistance would indicate the pullback from 1.3535 has ended and bring retest of this level later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

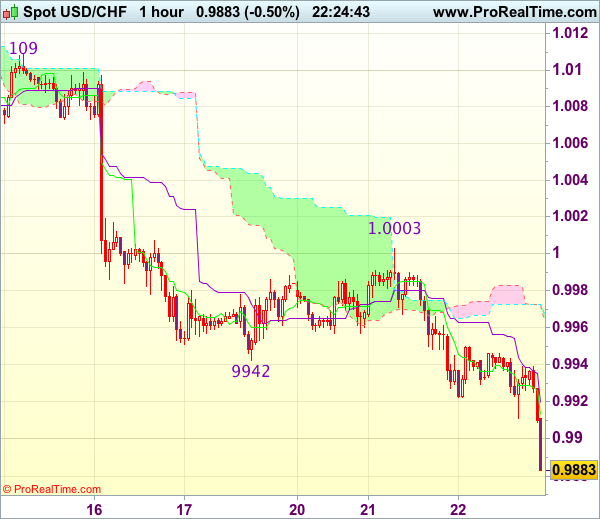

Trade Idea Update: USD/CHF – Sell at 1.0000

USD/CHF - 0.9897

Original strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

Yesterday’s selloff after meeting renewed selling interest at 1.0003 adds credence to our view that recent decline from 1.0171 is still in progress and may extend weakness to 0.9875-80, however, loss of downward momentum should prevent sharp fall below 0.9850 and reckon 0.9825-30 would hold from here, risk from there has increased for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0000-05 should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

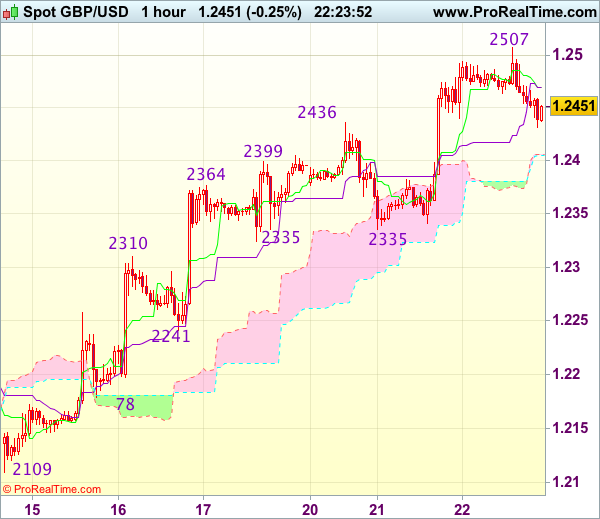

Trade Idea Update: GBP/USD – Buy at 1.2355

GBP/USD - 1.2451

Original strategy :

Buy at 1.2400, Target: 1.2500, Stop: 1.2365

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2355, Target: 1.2500, Stop: 1.2320

Position : -

Target : -

Stop : -

As cable has retreated after intra-day brief rise to 1.2507, suggesting consolidation below this level would be seen and pullback to 1.2400-10 is likely, however, reckon downside would be limited to 1.2350-55 (38.2% Fibonacci retracement of 1.2109-1.2507) and bring rebound later, above said resistance at 1.2507 would signal the rise from 1.2109 has resumed and extend gain to 1.2540-50 but loss of upward momentum would limit upside and price should falter below previous chart resistance at 1.2570.

In view of this, would not chase this move from here and we are looking to buy cable on subsequent pullback as 1.2350-55 should limit downside. Below strong support at 1.2335 would abort and signal top is formed instead, risk correction to 1.2305-10 (50% Fibonacci retracement of 1.2109-1.2507) first.

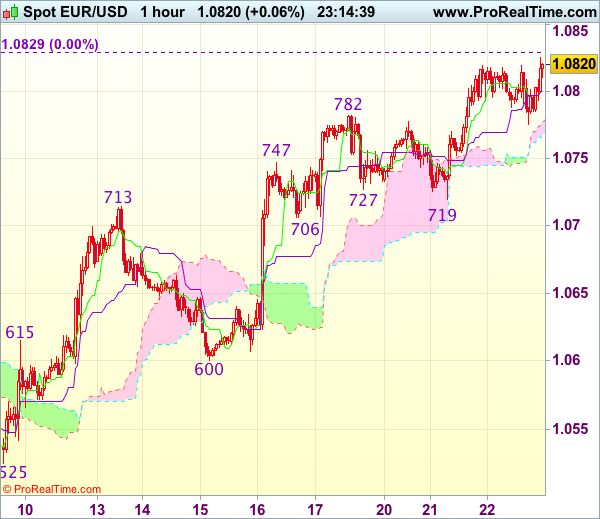

Trade Idea Update: EUR/USD – Buy at 1.0725

EUR/USD - 1.0810

Original strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

As the single currency has maintained a firm bias after surging again yesterday, suggesting recent erratic upmove from 1.0493 low is still in progress and may extend further gain to previous chart resistance at 1.0829, however, loss of near term upward momentum should prevent sharp move beyond 1.0850-60 and price should falter well below 1.0890-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0706 support should limit downside and bring another rise later. Below 1.0675-80 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.