Sample Category Title

New Home Sales Follow Climb in Sentiment

Following an upwardly revised January reading, new home sales jumped 6.1 percent in February to a 592,000-unit pace due to mild temperatures. Previous months' data were revised down by a net 4,000 units.

Strong Reading in New Homes Sales Activity

New home sales surged well ahead of the consensus estimate, likely due to unusually mild weather in February, which pulled sales forward. We suspect sales will slow in the coming months as the Nor'easter likely stalled activity. On a regional basis, activity advanced in the Midwest, South and West, but fell in the Northeast. The median price of a new home fell 4.9 percent year over year, while the average jumped almost 12 percent.

Builder Sentiment Jumps to Previous Peak Level

The NAHB/Wells Fargo Housing Market Index surged in March, reaching the highest level in more than a decade at 71. We suspect much of the post-election lift in sentiment reflects hope that the Trump Administration will follow through on curbing regulation, which could ease permit costs. The EPA's 2017 Construction General Permit, which authorizes storm water discharge from construction sites, is the latest source of angst.

Strong Retail Sales Sends Pound Above 1.25

GBP/USD continues to push upwards, and has climbed above the 1.25 level on Thursday. In the North American session, the pair is trading at 1.2510. On the release front, British Retail Sales posted a strong gain of 1.4%, crushing the estimate of 0.4%. As well, CBI Realized Sales held steady at 9 points, above the forecast of 4 points. In the US, unemployment claims jumped to 258 thousand, well above the forecast of 240 thousand. There was better news from New Home Sales, which improved to 592 thousand, compared to a forecast of 566 thousand.

This week's focus has been on British consumer indicators. Retail Sales sparkled in February with a gain of 1.4%, its highest gain since October 2016. At the same time, for the three months to February, retail sales suffered their biggest slide since 2010. This points to an erosion in consumer spending due to the weak pound, which has fallen 17% since the Brexit vote. The weak currency and higher oil prices have also sent inflation higher. CPI climbed 2.3% in February, beating the forecast of 2.1%. This is a significant reading, as it surpassed the BoE's inflation target of 2.0% for the first time in three years. Higher inflation levels has increased speculation that the Bank of England, which has had a neutral stance on rate policy, could raise rates this year. On Thursday, BoE deputy governor Ben Broadbent said that a rate hike was a possibility.

With the Fed pressing the rate trigger last week, what's next for the central bank? The Fed's rate statement and dot plot indicated that the Fed is looking at another two hikes in 2017, which would make three in total. This forecast was reiterated by Chicago Fed President Charles Evans earlier this week. Although one could make a strong case that three rate hikes in 2017 would be impressive, the markets appear disappointed, and would like four hikes, given the strong performance of the US economy. The Fed's cautious approach has soured sentiment towards the greenback, resulting in the dollar heading lower against its major rivals. The pound has taken full advantage, rising 3.0% since the Fed rate announcement last week.

Trade Idea: EUR/GBP – Hold long entered at 0.8620

EUR/GBP - 0.8615

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Bought at 0.8620, Target: 0.8750, Stop: 0.8580

Position : - Long at 0.8620

Target : - 0.8750

Stop : - 0.8580

New strategy :

Hold long entered at 0.8620, Target: 0.8750, Stop: 0.8580

Position : - Long at 0.8620

Target : - 0.8750

Stop : - 0.8580

Although the single currency has slipped again after yesterday’s brief bounce to 0.8700 and near term downside risk remains for marginal weakness from here, reckon downside would be limited to 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) and bring another rebound later, break of said resistance at 0.8700 would bring test of 0.8727, above there would suggest low is formed, then gain to 0.8760 would follow, break there would suggest the pullback from 0.8788 has ended, bring retest of this level, a breach there would extend the rise from 0.8403 low to 0.8800 and later 0.8825-30.

In view of this, we are holding on to our long position entered at 0.8620. A firm break below 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) would defer and suggest top has possibly been formed at 0.8788, risk test of 0.8560-65 (61.8% Fibonacci retracement) but support at 0.8547 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Hold short entered at 1.3400

USD/CAD - 1.3327

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Sold at 1.3400, Target: 1.3240, Stop: 1.3435

Position: - Short at 1.3400

Target: - 1.3240

Stop: - 1.3435

New strategy :

Hold short entered at 1.3400, Target: 1.3240, Stop: 1.3410

Position: - Short at 1.3400

Target: - 1.3240

Stop:- 1.3410

Although the greenback found support at 1.3264 and rebounded, as the pair met resistance at 1.3409 and has retreated again, retaining our bearishness for another test of said support, a break below there would add credence to our view that top has been made at 1.3535 earlier this month, bring further fall to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) but previous resistance at 1.3210 would hold due to loss of downward momentum.

In view of this, we are holding on to our short position entered at 1.3400. Above previous support at 1.3421 (now resistance) would suggest low is formed instead, bring a stronger rebound to 1.3450 and possibly test of resistance at 1.3479, however, only break of 1.3495 resistance would indicate the pullback from 1.3535 has ended and bring retest of this level later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

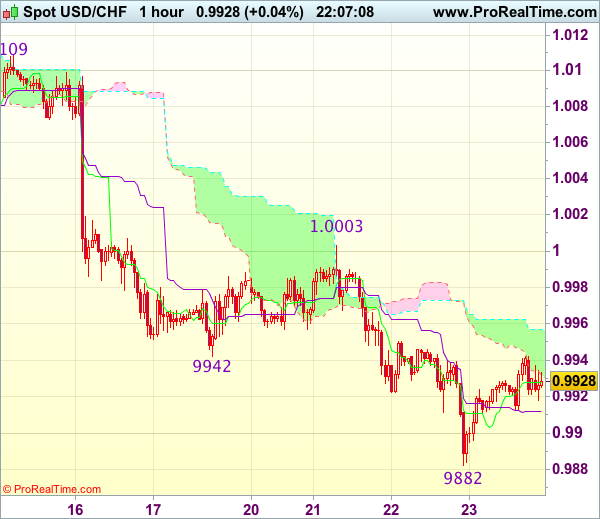

Trade Idea Update: USD/CHF – Sell at 1.0000

USD/CHF - 0.9928

Original strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 0.9882 yesterday suggests consolidation above this level would be seen and corrective bounce to 0.9945-50 cannot be ruled out, however, reckon upside would be limited to 0.9980 and renewed selling interest should emerge around 1.0003 resistance, bring another decline later. A break of said support at 0.9882 would add credence to our view that recent decline from 1.0171 is still in progress and may extend weakness to 0.9865-70 but loss of downward momentum should prevent sharp fall below 0.9850 and reckon 0.9825-30 would hold.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0000-05 should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

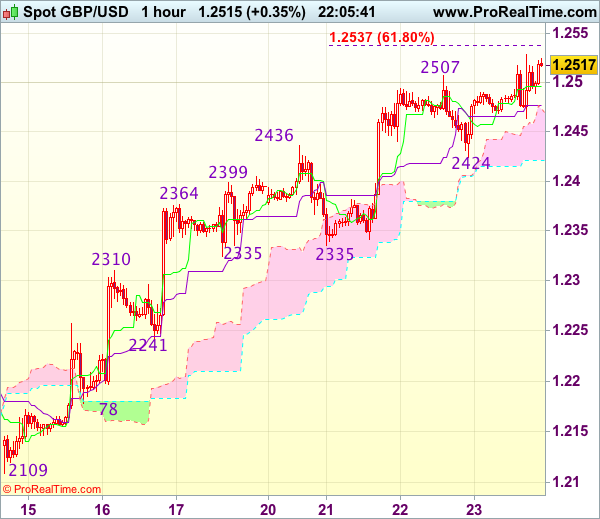

Trade Idea Update: GBP/USD – Buy at 1.2425

GBP/USD - 1.2512

Original strategy :

Buy at 1.2400, Target: 1.2520, Stop: 1.2365

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2425, Target: 1.2540, Stop: 1.2390

Position : -

Target : -

Stop : -

As cable has continued trading with a firm undertone, adding credence to our bullish view that recent upmove from 1.2109 is still in progress and may extend further gain to 1.2540-50 but loss of upward momentum would limit upside to previous chart resistance at 1.2570 and price should falter below 1.2600-10, risk from there has increased for a retreat to take place later.

In view of this, would not chase this move here and we are looking to buy cable on subsequent pullback as 1.2400 should limit downside. Below 1.2380-85 would defer and risk correction to 1.2350-55 but still reckon support at 1.2335 would remain intact, bring another rise later.

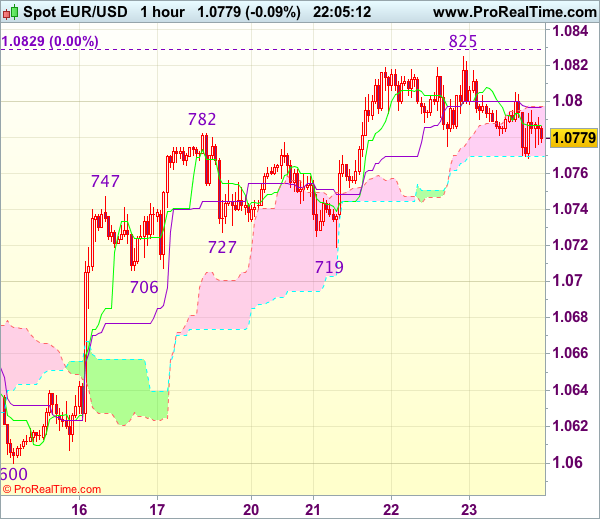

Trade Idea Update: EUR/USD – Buy at 1.0725

EUR/USD - 1.0784

Original strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

As the single currency retreated after rising to 1.0825 yesterday, suggesting minor consolidation below this level would be seen and pullback to 1.0750-60 cannot be ruled out, however, reckon support at 1.0719 would limit downside and bring another rise later, above indicated resistance at 1.0825-29 would extend further rise to 1.0850-60 but loss of near term upward momentum should prevent sharp move beyond 1.0880 and price should falter below 1.0900, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0719 support should limit downside and bring another rise later. Below 1.0690-00 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

Trade Idea Update: EUR/USD – Buy at 1.0725

EUR/USD - 1.0784

Original strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0725, Target: 1.0840, Stop: 1.0690

Position : -

Target : -

Stop : -

As the single currency retreated after rising to 1.0825 yesterday, suggesting minor consolidation below this level would be seen and pullback to 1.0750-60 cannot be ruled out, however, reckon support at 1.0719 would limit downside and bring another rise later, above indicated resistance at 1.0825-29 would extend further rise to 1.0850-60 but loss of near term upward momentum should prevent sharp move beyond 1.0880 and price should falter below 1.0900, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0719 support should limit downside and bring another rise later. Below 1.0690-00 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

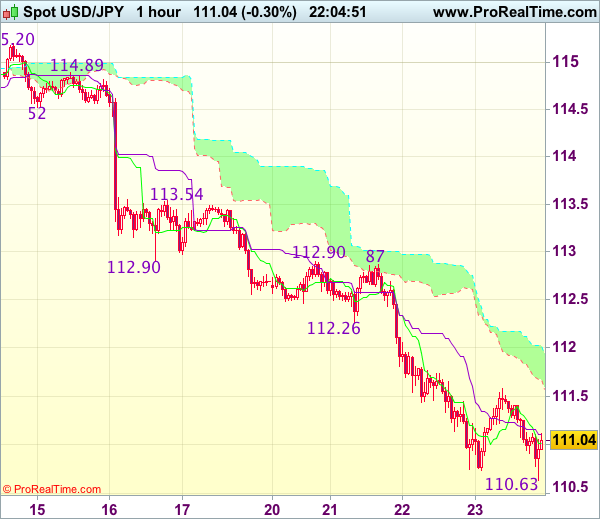

Trade Idea Update: USD/JPY – Sell at 112.00

USD/JPY - 111.00

Original strategy :

Sell at 112.00, Target: 110.80, Stop: 112.35

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.00, Target: 110.80, Stop: 112.35

Position : -

Target : -

Stop : -

As the greenback recovered after falling to 110.63, suggesting consolidation above this level would be seen and corrective bounce to 111.55-60 is likely, however, still reckon upside would be limited to 112.00-10 and bring another decline later, a break of said support at 110.73 would signal recent decline is still in progress and may extend further fall to 110.50 but near term oversold condition should prevent sharp fall below 110.20-25 and reckon 110.00 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 112.00 should limit upside. Only above indicated previous support at 112.26 would abort and signal low is formed instead, bring a stronger rebound to 112,59 but resistance at 112,87-90 should cap upside.

Trump Rally to Be Tested by Healthcare Vote

A growing sense of caution has gripped the financial markets this week with investors on standby ahead of Thursday's key healthcare vote in Congress which may thoroughly test the Trump bump. Uncertainty over Donald Trump's proposed economic agenda has already triggered risk aversion and any complications in the healthcare reform could spell trouble for this phenomenal stock market rally. Global stocks may be exposed to downside shocks with the threat of a potential setback in the healthcare bill raising doubts over Trump's ability to move forward with the proposed tax cuts and infrastructure spending. Today will be the first major test for Trump's legislative ability and the outcome may either create a Trump slump or technical bounce for bulls to exploit.

Sterling hovering around 1.2500

Sterling has staged a remarkable rebound this week with bulls almost rebelling against the Brexit woes by propelling the GBPUSD above 1.2500 during Thursday's trading session. The Dollar's persistent weakness combined with February's blockbuster retail sales figure of 1.4% may have created an illusion of a bullish bias returning to Sterling. Although the retail sales figure for February was unquestionably impressive and illustrated strong growth, the underlying three-month view from December and January still displayed a slowdown.

With the Article 50 set to be triggered next week and the focus redirected towards Brexit, Sterling could be instore for a messy rollercoaster ride. The lingering concerns over complications arising in the negotiation process may compound to the jitters consequently exposing Sterling to downside risks.

While bulls may be commended on their ability to exploit Dollar's weakness and elevate Sterling repeatedly despite the Brexit anxieties, questions may be asked over how much steam the over-extended technical bounce has left. With uncertainty still the name of the game when dealing with Sterling, there remains a likelihood of the Brexit developments dictating where the currency trades with macro fundamentals becoming secondary.

From a technical standpoint, Sterling bulls may win the battle this week if 1.2500 is conquered. A decisive breakout and daily close above 1.2500 could open a path towards 1.2600. On the other hand, if 1.2500 remains defensive then bears have a chance to test Wednesday's daily low at 1.2420.

Yellen conference in focus

King Dollar was on the back foot this week with the Dollar Index struggling to break back above 100.00 as sellers exploited the renewed Trump jitters to attack prices incessantly. Dollar bulls remain on the hunt for inspiration to pump life into the Greenback with Yellen's speech today at a Community Development Conference seen as an opportunity. If Yellen dishes a hawkish surprise or any fresh insights on rate hike timings, then bulls could be encouraged to elevate the Dollar Index back towards the psychological 100.00 level. On the other hand, if bulls are left empty handed then the Greenback could be instore for further punishment in the short term.

Commodity spotlight - Gold

The risk-off trading environment has boosted appetite for safe-haven assets with Gold becoming an investor's popular choice this week. Prices have climbed to a three-week high above $1250 with Dollar weakness fueling the upside momentum. Although Gold may find itself under pressure in the longer term when the Dollar stabilizes, risk aversion could uplift the yellow metal higher in the short term. From a technical standpoint, the fact that bulls have conquered $1240 on the daily charts suggests that the upside still has some steam. A decisive breakout above $1250 may open a path towards $1260.