Sample Category Title

GBP/JPY Two POC zones for Now Moment Buyers

The GBP/JPY got a backwind by renewed GBP strength and currently we can see nice intraday rejections off the supporting trend line. Two POC zones that might spur additional buying interest are 139.50-65 (EMA89, H4, 50.0). H4 camarilla is breakout point which we already covered in Price Action Trading School and on subsequent retests we might see another rejection. If the pair retraces deeper to POC2 zone pay attention to 139.20-35 (H3, 78.6, trend line). Target is Weekly camarilla H4 140.75.

Canadian Retail Sales Bounced Back in January

- Nominal retail sales surged 2.2% in January following a 0.4% dip in December.

- Auto sales were, as expected, a large contributor (+3.8%) but sales excluding autos also bounced-back 1.7% following a 0.5% dip in December.

- Sale volumes posted a strong 1.3% gain to reverse the 1.0% drop in December.

- 'E-commerce' sales rose 17.2% from a year-ago in January

Our Take:

The 1.3% bounce-back in retail sale volumes in January more-than-reversed the 1.0% decline in December that in turn had marked only the first dip in six months. The measure in January is already 3.3% (at an annualized rate) above its Q4 average. Employment gains have been solid, as has household income growth (with the latter in part supported by increased federal government child tax benefit payments that began in the summer). Interest rates remain at extremely low levels and consumer confidence jumped to a more-than seven year high in February with increasing optimism about the economic outlook seemingly outweighing uncertainty about the future of Canada's trading relationship with the United States. In terms of 'hard' data, auto sales in February, by our estimate, ticked higher from what were already highly elevated levels in January (with sales over the two months pacing well-above the fourth consecutive annual auto sales record posted in 2016). In short, there is little to suggest that consumer spending is slowing from levels that already accounted for a record share of GDP in 2016.

Strong retail numbers for January followed earlier solid increases in sale volumes in both the manufacturing (+0.7%) and wholesale (+3.4%) sectors. As a whole, the data suggests stronger economic momentum in the second half of 2016 may have carried over more significantly than we previously assumed into early 2017. Data to-date suggests January GDP growth may have matched the solid 0.3% December increase which would leave Q1 growth tracking closer to a 2½% to 3% range than the 1.9% pace projected in our current forecast.

Canadian Retail Sales Kick Off the Year with a Bang

Retail sales kicked off 2017 on a strong note, with January's 2.2% increase in sales more than recouping December's loss. In real terms, sales were up by a robust 1.3%.

January's gains were widespread, with sales at health and personal care stores (+6%), motor vehicle and parts dealers (+3.8%) and electronics and appliance stores (+3.7%) leading the way – all of which bounced back from a decline in December.

Regionally, sales were up across the board, led by PEI (+4.3%), Saskatchewan (+3.7%) and B.C. (+2.9%).

Key Implications

This was a good report all around. The bounce back in retail sales in January is in line with our outlook for consumer spending growth of around 2.5% in the first quarter, and puts overall economic growth on track to record a pace of 3% (annualized) or more in the first quarter.

Supported by robust job creation and wealth effects related to home price gains, consumers will remain a key driver of economic activity this year. Nonetheless, the strength is likely to fade somewhat in the coming quarters. A gradual rise in longer-term interest rates consistent with higher borrowing costs stateside, and some signs of a cooling in the housing market, will likely prompt highly-indebted Canadian consumers to rein in spending. That said, at close to 2%, overall consumer spending growth will remain at a healthy level.

Accelerating Inflation Elevates Sterling

Sterling received a solid boost on Tuesday after February's accelerating inflation figure of 2.3% sparked speculations of the Bank of England raising UK interest rates in the medium to longer term. The persistent currency weakness created from Brexit has effectively propelled inflation above the Bank of England's golden target for the first time in more than three years with even the critical core CPI hitting 2%. While the immediate market reaction to this blockbuster inflation figure was bullish, gains may be limited as investors start to reevaluate the ramifications it may have to the UK economy. With the 2.3% inflation level superseding average earnings which currently stand at 2.2%, consumer spending may be negatively impacted and such could trigger fears over the sustainability of the UK's consumer fueled economic growth. Although expectations may mount over the BoE raising UK interest rates amid the spiraling inflation, the uncertainty around Brexit and concerns over the health of the economy could prompt the Central Bank to remain on standby.

While the repeated gains seen on Sterling have been impressive, a chunk of the upside momentum may be attributed to Dollar weakness. The bullish combination of Dollar vulnerability and slight optimism over the BoE hawks coming back into town continues to entice bulls to install rounds of buying. This technical bounce could come to an abrupt end when the focus is redirected back towards the Brexit developments. The first crucial test for Sterling may be when Article 50 is invoked on the 29th of March. Technical traders may observe how the GBPUSD reacts below 1.2500 with any noticeable weakness encouraging bears to jump back in.

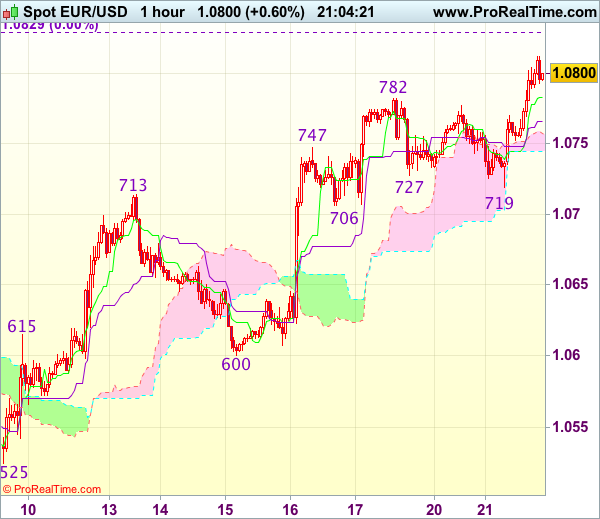

EURUSD punches above 1.0800

The Euro bulls were unleashed on Tuesday with the EURUSD punching above 1.0800 as political concerns in Europe eased after independent candidate Emmanuel Macron performed quite impressively in France's first presidential debate. With fears somewhat receding over the political uncertainty in France coupled with the ECB slowly adopting a hawkish stance, the Euro has found itself back in fashion. A vulnerable Dollar has played a part in the EURUSD resurgence with further Dollar weakness potentially paving a path higher. From a technical standpoint, much focus may be directed to how prices react to the 1.0800 resistance level. A daily close above 1.0800 could encourage bullish investors to attack the next relevant level at 1.08500. On the other hand, if 1.0800 remains defensive then 1.0700 could be a possibility for the bears.

Commodity spotlight - Gold

A vulnerable Dollar has supported Gold on Tuesday with the metal trading around $1232 as of writing. With the lingering impacts of last week's "dovish hike" still reverberating across the board, bulls may exploit this period of ongoing Dollar weakness to propel Gold prices towards $1240. While additional gains may be realized in the short term, the upside could be limited in the longer term when the Dollar regains its attitude. From a technical standpoint, although prices are turning bullish on the daily charts, exhaustion below $1240 could still encourage bears to send prices lower.

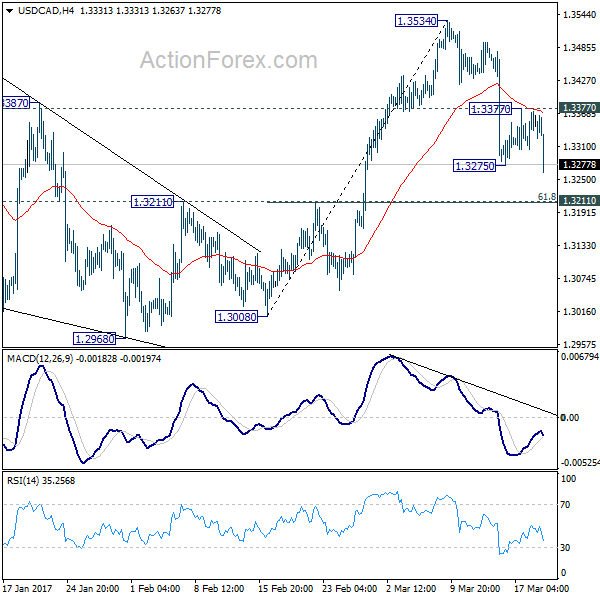

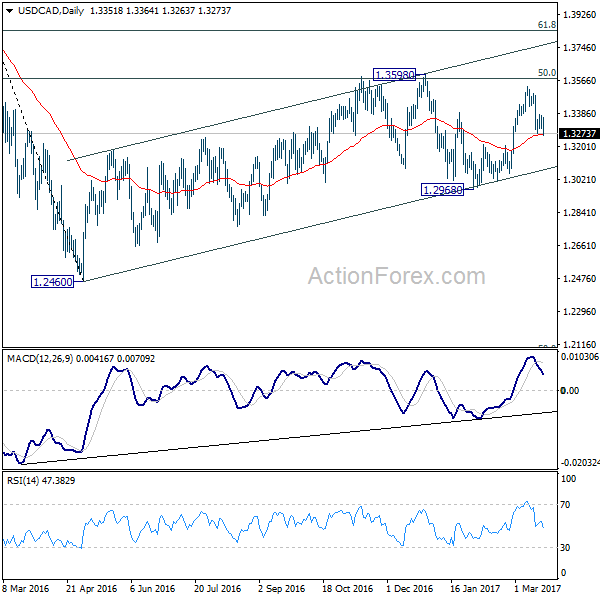

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3313; (P) 1.3343; (R1) 1.3382; More...

USD/CAD's fall from 1.3534 resumed by taking out 1.3275 and reaches as low as 1.3263 so far. Intraday bias is back on the downside for 1.3211 cluster level (61.8% retracement of 1.3008 to 1.3534 at 1.3209). As such decline is viewed as a correction pattern, we'd expect downside to be contained by 1.3209/11 to bring rebound. On the upside, break of 1.3377 resistance will turn bias back to the upside for 1.3534 resistance and then 1.3598. However, sustained break of 1.3211 will dampen this view and target 1.2968 key support level next.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 wold at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

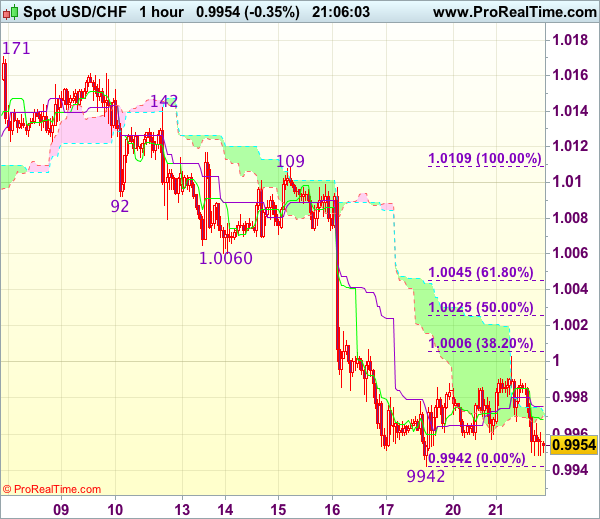

Trade Idea Update: USD/CHF – Sell at 1.0000

USD/CHF - 0.9950

Original strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0000, Target: 0.9900, Stop: 1.0035

Position : -

Target : -

Stop : -

As the greenback has remained under pressure, suggesting recent decline from 1.0171 is still in progress and may extend weakness to 0.9915-20 (50% projection of 1.0109-0.9942 measuring from 1.0003), however, loss of downward momentum should prevent sharp fall below 0.9900 (61.% projection) and reckon 0.9870-75 would hold from here, risk from there has increased for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0000-05 should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

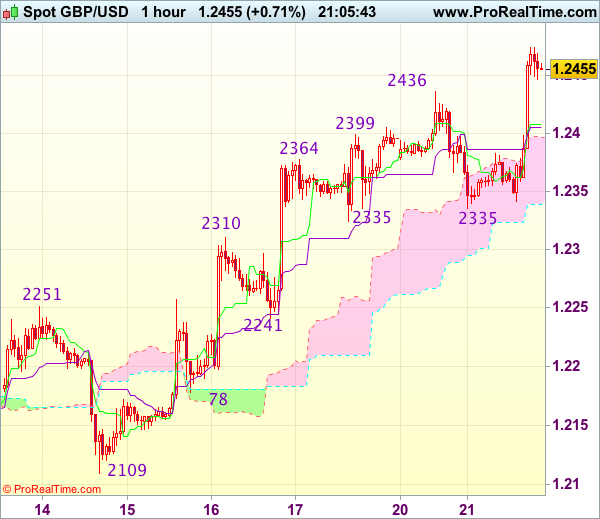

Trade Idea Update: GBP/USD – Buy at 1.2400

GBP/USD - 1.2450

Original strategy :

Buy at 1.2400, Target: 1.2500, Stop: 1.2365

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2400, Target: 1.2500, Stop: 1.2365

Position : -

Target : -

Stop : -

As cable has surged again in London morning and broke above previous resistance at 1.2436, confirming the rise from 1.2109 has resumed and bullishness remains for further gain to previous resistance at 1.2479, then 1.2500, however, near term overbought condition should prevent sharp move beyond 1.2540-50 and price should falter below previous chart resistance at 1.2570, risk from there has increased for a retreat to take place later.

In view of this, would not chase this move from here and we are looking to buy cable on pullback as 1.2400-10 should limit downside. Below 1.2380-85 would defer and risk correction to 1.2350 but support at 1.2335 should remain intact.

Trade Idea Update: EUR/USD – Buy at 1.0740

EUR/USD - 1.0801

Original strategy :

Buy at 1.0740, Target: 1.0840, Stop: 1.0705

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0740, Target: 1.0840, Stop: 1.0705

Position : -

Target : -

Stop : -

As the single currency has continued trading with a firm undertone after last week’s rally, suggesting recent erratic upmove from 1.0493 low is still in progress and may extend further gain towards previous chart resistance at 1.0829, however, loss of near term upward momentum should prevent sharp move beyond 1.0850-60 and price should falter well below 1.0890-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0706 support should limit downside and bring another rise later. Below 1.0675-80 would defer and suggest top is possibly formed, risk weakness to 1.0640 (previous resistance now support) but still reckon indicated support at 1.0600 would remain intact.

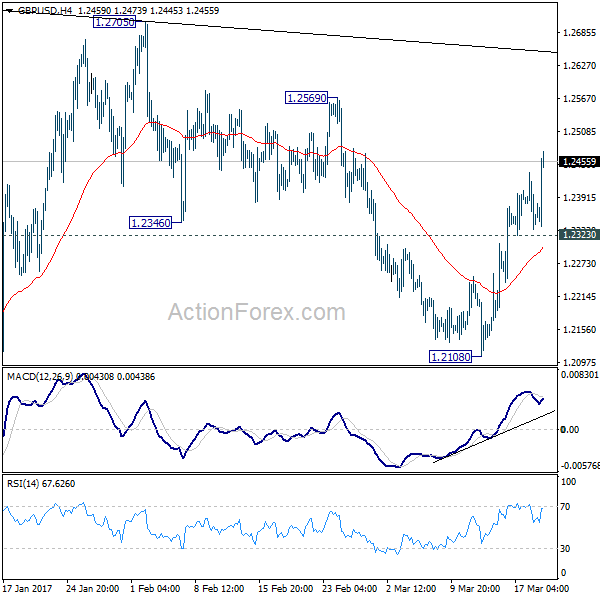

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2316; (P) 1.2375; (R1) 1.2417; More...

GBP/USD's rise from 1.2108 resumed after brief consolidation. Intraday bias is back on the upside for 1.2569 resistance. Break will target 1.2705/74 resistance zone. But still, price actions from 1.1946 are seen as a consolidation pattern. Hence, we'd expect strong resistance from 1.2705/2774 to limit upside and bring down trend resumption. On the downside, break of 1.2323 support will turn bias back to the downside for 1.2108 support. Though, sustained break of 1.2774 will extend the rise towards 1.3444 key resistance level.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

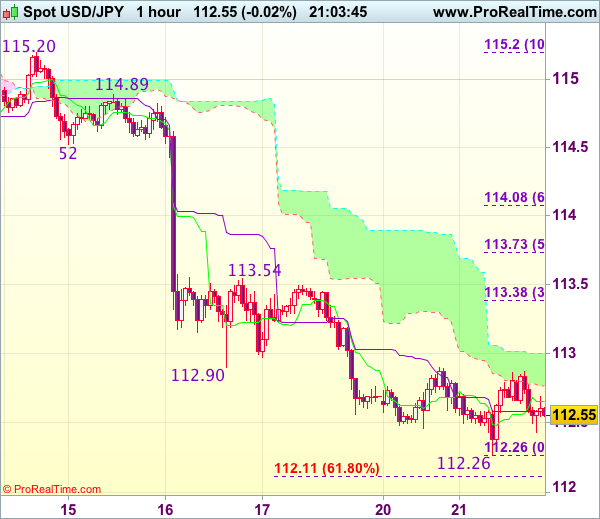

Trade Idea Update: USD/JPY – Hold long entered at 112.55

USD/JPY - 112.55

Original strategy :

Bought at 112.55, Target: 113.55, Stop: 112.20

Position : - Long at 112.55

Target : - 113.55

Stop : - 112.20

New strategy :

Hold long entered at 112.55, Target: 113.55, Stop: 112.20

Position : - Long at 112.55

Target : - 113.55

Stop : - 112.20

Although the greenback fell briefly to 112.26, the subsequent rebound suggests consolidation above this level would be seen and as long as 112.26 holds, mild upside bias is seen for gain to 113.00-05 is likely, above there would suggests low is possibly formed, bring a stronger rebound to 113.35-40 (38.2% Fibonacci retracement of 115.20-112.26), however, break of resistance at 113.54 is needed to provide confirmation, bring further subsequent gain to 113.70-75 (50% Fibonacci retracement).

In view of this, we are holding on to our long position entered at 112.55 but one must exit on such rebound. Below said support at 112.26 would risk one more fall to 112.10-15 (61.8% projection of 115.20-112.90 measuring from 113.54) but loss of downward momentum should prevent sharp fall below previous support at 111.69, risk remains for a rebound to take place later.