Sample Category Title

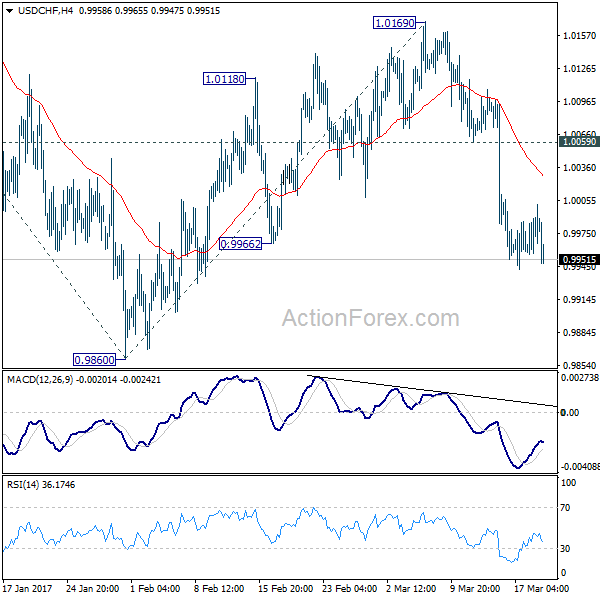

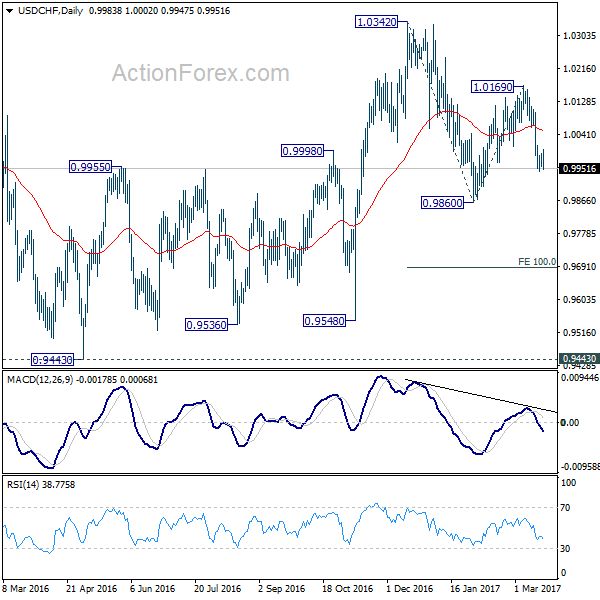

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9965; (P) 0.9978; (R1) 0.9998; More.....

With 1.0059 resistance intact, deeper decline is expected in USD/CHF for 0.9860 low. Whole decline from 1.0342 is likely resuming and break of 0.9860 will target 100% projection of 1.0342 to 0.9860 from 1.0169 at 0.9687. Nonetheless, on the upside, break of 1.0059 will turn bias back to the upside for 1.0169 resistance instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

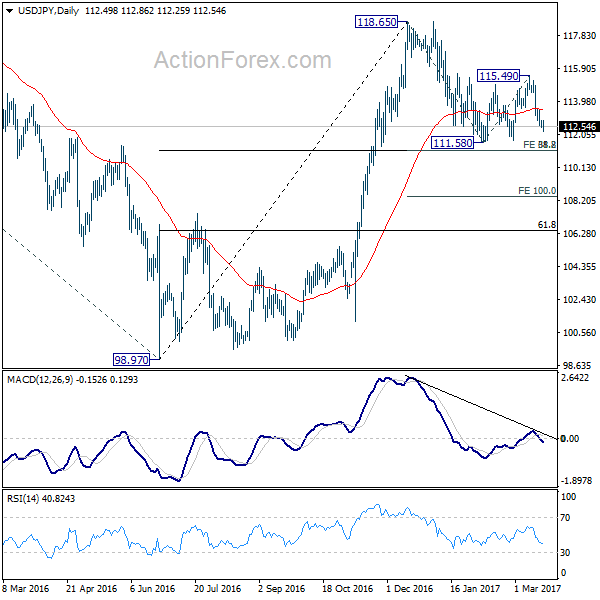

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.37; (P) 112.63; (R1) 112.82; More...

With 113.53 minor resistance intact, deeper decline is expected in USD/JPY for 111.58 low. Consolidation pattern from 111.58 has completed with three waves up to 115.49. And decline from 118.65 is likely resuming. However, we'd tentatively expect strong support from 111.12/13 cluster support to contain downside. This level represents 61.8% projection of 118.65 to 111.58 from 115.49 at 111.12 and 38.2% retracement of 98.97 to 118.65 at 111.13. On the upside, above 113.53 minor resistance will turn bias back to the upside for 115.49 resistance. However, sustained break of 111.12/13 will bring deeper decline to 100% projection of 118.65 to 111.58 from 115.49 at 108.42.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.19) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

EURUSD: Bullish, Threatens Further Upside Pressure

EURUSD: With the pair rallying back above its key resistance, further bullishness is likely. On the upside, resistance comes in at 1.0850 level with a cut through here opening the door for more upside towards the 1.0900 level. Further up, resistance lies at the 1.0950 level where a break will expose the 1.1000 level. Its daily RSI is bullish and pointing higher suggesting further upside pressure. Conversely, support lies at the 1.0750 level where a violation will aim at the 1.0700 level. A break of here will aim at the 1.0650 level. All in all, EURUSD faces pullback threats.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0747 (R1) 1.0769; More.....

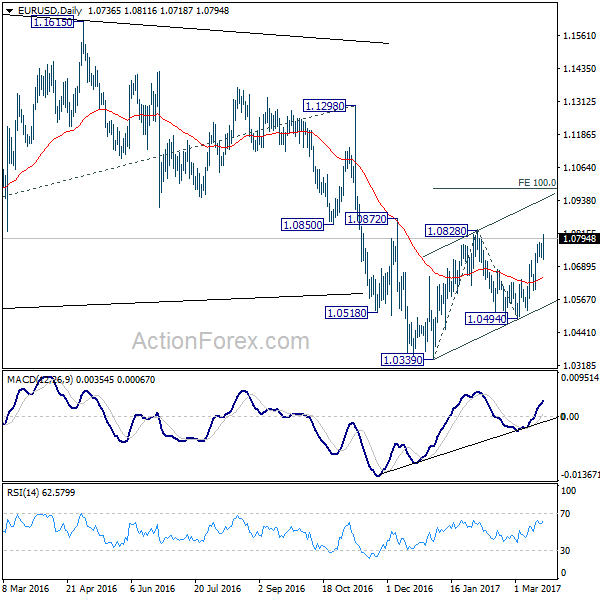

EUR/USD's rally re-accelerates and reaches as high as 1.0811 so far. Intraday bias stays on the upside for 1.0828 resistance and above. Nonetheless, we maintain that rise from 1.0339 is a corrective move. Hence, we'd expect upside to be limited by 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983 to completion the correction. On the downside, break of 1.0705 minor support will turn bias to the downside for 1.0494 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to resume later. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

Sterling Jumps as CPI Sparkles Rate Speculations, Euro Boosted by Centrist Macron’s Performance in Debate

Sterling strengthens against all other major currencies as its boosted by strong inflation data. Headline CPI accelerated to 2.3% yoy in February, up from 1.8% yoy and beat expectation of 2.1% yoy. Core CPI also accelerated to 2.0% yoy, up from 1.6% yoy and beat expectation of 1.7% yoy. Headline CPI is now back inside BoE's target zone. iIt's also the highest reading since September 2013. While BoE has been clear that it will allow inflation to overshoot for sometime, there are continuous speculation of the timing of a rate hike.

The pound was shot higher last week as BoE minutes showed that Kristin Forbes actually voted for a hike. While we're not seeing any chance of a hike in the first half, some market participants are already speculating for it. Also from UK, PPI input slowed to 19.1% yoy, PPI output rose to 3.7% yoy, PPI output core was unchanged at 2.4%. House price index rose 6.2% yoy in January. Public sector net borrowing rose to GBP 1.1b in February.

Euro lifted by Emmanuel Macron

Euro surges broadly, except versus Sterling, today as lifted by political news in France. It appears that the markets see centrist Emmanuel Macron as the winner of the first TV debate for presidential election that lasted more than three hours. A snap opinion poll showed that Macron was seen as the most convincing candidate among the top five running for the election. 25% of viewers thought Macron was the most convincing, comparing to leftist Jean-Luc Melenchon's 20%, who came second. That eased some concerns over the win of far right Marine Le Pen in the election, as that is seen a a big risk for Frexit. EUR/USD surges past 1.08 handle and recent rally from 1.0494 extends.

Also from Europe, Swiss trade surplus narrowed to CHF 3.11b in February.

Dollar extends post FOMC decline

Yesterday, Chicago Fed President Charles Evans suggested he would not rule out the possibility of four rate hikes "if things really pick up", with, e.g. inflation rising over +2% but it is certainly not his base case. At an interview with Fox Business, Evans noted that "as I gain more confidence in the outlook I could support three total this year. If inflation began to pick up, that would certainly solidify (that expectation). It could be three, it could be two, it could be four if things really pick up". Commenting on Donald Trump's GDP growth outlook, Evans suggested that "4% would be really an outsized number".

Meanwhile, Minneapolis Fed President Neel Kashkari, who dissented a rate hike last week suggested that he would be "very surprised" if core inflation reached 2% this year. He reiterated that there is no urgency to hike interest rate as there is no "high-inflation threat right around the corner".

Released in US session, US current account deficit narrowed slightly to USD -112b in Q4. Canada retail sales jumped sharply by 2.2% mom in January. Ex-auto sales rose 1.7% mom.

RBA concerned over household debts, rising housing bubble

At the RBA minutes for the March meeting, policymakers raised concerns over the increasing levels of household debts which would be exacerbated by rising unemployment and falling consumption. The members also noted there had been a "buildup of risks associated with the housing market". While the central bank has been paying close attention to the housing market, including prices, supply, rents, debts and supervisory markets, the reference of "a buildup of risks" was non-existent in the March meeting statement and the February minutes.

On the economic growth outlook, RBA acknowledged that the domestic economy continued to move away from mining investment while terms of trade increased in recent months. Moreover, the members expected that inflation would continue to rise, albeit gradually. Policymakers reiterated that economic growth would be supported by low interest rates. More in RBA Minutes Highlighted Concerns over Household Debts, Rising Housing Bubble.

Also from Australia, house price index jumped 4.1% qoq in Q4, highest quarterly rise since 2015.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0716; (P) 1.0747 (R1) 1.0769; More.....

EUR/USD's rally re-accelerates and reaches as high as 1.0811 so far. Intraday bias stays on the upside for 1.0828 resistance and above. Nonetheless, we maintain that rise from 1.0339 is a corrective move. Hence, we'd expect upside to be limited by 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983 to completion the correction. On the downside, break of 1.0705 minor support will turn bias to the downside for 1.0494 support first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to resume later. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | House Price Index Q/Q Q4 | 4.10% | 2.50% | 1.50% | |

| 00:30 | AUD | RBA Minutes | ||||

| 06:45 | CHF | SECO March 2017 Economic Forecasts | ||||

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.11B | 3.85B | 4.73B | 4.83B |

| 09:30 | GBP | CPI M/M Feb | 0.70% | 0.50% | -0.50% | |

| 09:30 | GBP | CPI Y/Y Feb | 2.30% | 2.10% | 1.80% | |

| 09:30 | GBP | Core CPI Y/Y Feb | 2.00% | 1.70% | 1.60% | |

| 09:30 | GBP | RPI M/M Feb | 1.10% | 0.80% | -0.60% | |

| 09:30 | GBP | RPI Y/Y Feb | 3.20% | 2.90% | 2.60% | |

| 09:30 | GBP | PPI Input M/M Feb | -0.40% | 0.10% | 1.70% | 1.60% |

| 09:30 | GBP | PPI Input Y/Y Feb | 19.10% | 20.10% | 20.50% | 20.10% |

| 09:30 | GBP | PPI Output M/M Feb | 0.20% | 0.30% | 0.60% | |

| 09:30 | GBP | PPI Output Y/Y Feb | 3.70% | 3.70% | 3.50% | 3.60% |

| 09:30 | GBP | PPI Output Core M/M Feb | 0.00% | 0.20% | 0.50% | |

| 09:30 | GBP | PPI Output Core Y/Y Feb | 2.40% | 2.50% | 2.40% | |

| 09:30 | GBP | House Price Index Y/Y Jan | 6.20% | 6.30% | 7.20% | 5.70% |

| 09:30 | GBP | Public Sector Net Borrowing (GBP) Feb | 1.1B | 2.9B | -9.8B | -11.7B |

| 11:00 | GBP | CBI Trends Total Orders Mar | 8 | 5 | 8 | |

| 12:30 | CAD | Retail Sales M/M Jan | 2.20% | 1.30% | -0.50% | -0.40% |

| 12:30 | CAD | Retail Sales Less Autos M/M Jan | 1.70% | 1.30% | -0.30% | -0.50% |

| 12:30 | USD | Current Account (USD) Q4 | -112B | -129B | 113B | -116B |

Canadian Dollar Edges Higher Ahead of Canadian Retail Sales

USD/CAD has edged lower in the Tuesday session. In North American trade, the pair is trading at the 1.33 line.

With the Fed's quarter-rate point behind us, what's next for Janet Yellen & Co.? The CME Group has priced a rate hike in May at just 6%, while a June move is priced at 54%. With a dearth of key fundamentals in the US this week, the markets are left to monitoring comments from FOMC members who will be speaking this week, including Fed Chair Janet Yellen. On Monday, Chicago Fed President Charles Evans said he expects the Fed to raise rates two more times this year. This echoes the Fed's projection in its rate statement. Although three rate hikes in 2017 appears impressive, market players want four hikes, and have reacted with disappointment to the Fed's more cautious approach. This has sent the US dollar lower, as the Canadian dollar posted gains last week.

CAC 40 is Holding above 5000 Mark on Reduced Frexit Fears

The index is at the front foot on Tuesday when it opened higher, as sentiment improved after French presidential candidate Macron won the first TV debate, sidelining fears from far-right candidate Le Pen's victory that could lead France towards exit from the EU. Bullish technical studies remain supportive, as the price remains above psychological 5000 level and eyes target at 5035 (16 Mar peak, the highest traded since mid-Jun 2015). Rising daily 10SMA that tracks the rally since early Feb, offers initial support at 4994, followed by plethora of supports formed by 20/30/55 SMA's at 4958/4928/4892 respectively and thick 4-hr Ichimoku cloud (spanned between 4977 and 4912). Any break below 4900 handle could be considered as strong bearish signal.

Res: 5025; 5035; 5050; 5095

Sup: 5009; 4994; 4958; 4928

EUR En Marche after Macon’s Presidential Debate Performance

- GBP flying as higher CPI supports calls for rate hike;

- EUR En Marche after Macon's Presidential debate performance;

- Fed Speeches eyed as USD remains in correction mode.

US equity markets are expected to open a little higher on Tuesday, tracking broad gains in Europe where only the FTSE is currently trading lower, as sterling's strong gains way on the outward looking UK index.

The British pound is flying this morning after inflation data for February showed prices are rising much faster than thought, with both the CPI and core CPI measures now in line or above the Bank of England's target. The spike in the inflation numbers probably explains why some BoE policy makers turned far more hawkish at the last meeting, with one voting for a rate hike and others suggesting they could soon follow.

The pound had been under a lot of pressure last week and was threatening to break below the 1.20-1.21 support zone that has held firm over the last five months. With the BoE signalling previously that it would tolerate above target inflation, traders were looking through the increases in the data and instead focusing on other data weaknesses that were appearing and the possibility of hard Brexit. With the BoE now indicating it could raise rates much sooner than markets were expecting in response to the inflation data, future downside for the pound now looks far more limited, especially as it's the pounds depreciation that has generated much of the inflationary pressures.

The euro is also making some decent gains against the greenback this morning after a number of polls showed Emmanuel Macron performing best in last night's Presidential debate. Macon is seen as the more market friendly candidate, particularly among the two frontrunners, with Marine Le Pen threatening to pull France out of the euro. While Le Pen still leads in first round polls, Macron is seen by most polls to have a comfortable lead in the second round. Markets continue to price in Le Pen risk, with French 10-year yields still at an early-2014 premium to their German counterparts, but results like last night are offering some reprieve. While the Dutch elections may have gone relatively smoothly as far as markets are concerned, I don't think people will get too complacent ahead of the 23 April and 7 May votes in France after what they experienced last year.

The US dollar remains in correction mode this morning, largely driven on this occasion by gains elsewhere but also aided by the more dovish than expected language that followed last week's rate hike. As other central banks becoming slightly more hawkish as the environment becomes more inflationary and economic and political risks subside, the pace of dollar appreciation should slow. That said, I still expect the Federal Reserve tightening cycle to be much more aggressive than other central banks over the next couple of years which should be supportive for the dollar during that period.

With economic data releases looking thin again today, focus will remain on the US central bank with three policy makers scheduled to make appearances. Of those appearing, William Dudley's will be of most interest, with him being the only voter on the FOMC among them and his views closely correlated with those of Chair Janet Yellen. We'll also hear from Esther George and Loretta Mester, both of whom are seen as being among the more hawkish of the Fed officials. As always, policy makers have been relatively non-committal on the next rate hike since last week's meeting and I expect more of the same today. Investors continue to expect two more rate hikes this year, although the odds have slipped slightly since last week and June is just above 50% for the next hike, with two by December being also just above 50%.

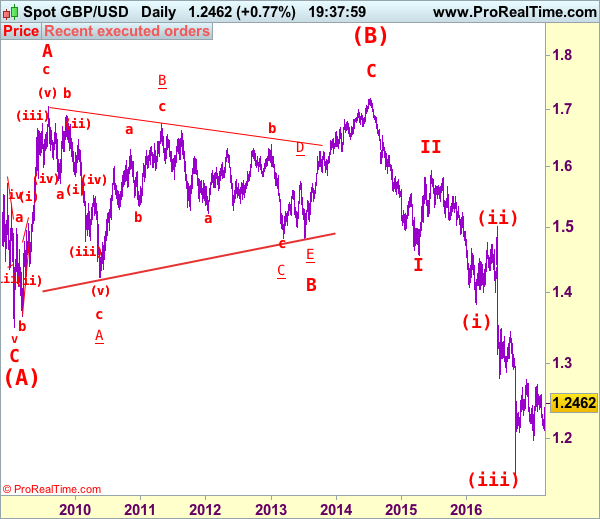

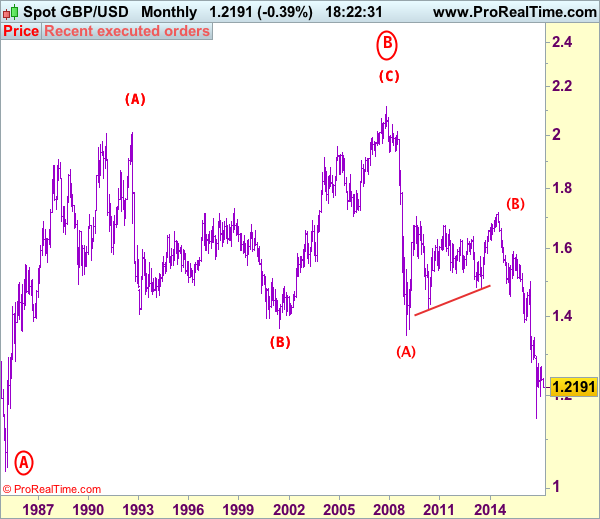

GBP/USD Elliott Wave Analysis

GBP/USD – 1.2463

GBP/USD – Wave 4 is unfolding as an (A)-(B)-(C) and could have ended at 1.7192

Although cable fell briefly to 1.2109 last week, the subsequent stronger-than-expected rebound signals the fall from 1.2706 has ended there and consolidation with upside bias is seen for further gain to 1.2570, however, a daily close above there is needed to add credence to this view, bring retest of this level later. Looking ahead, only above 1.2706 would retain bullishness and signal another leg of corrective upmove from 1.1986 low is underway for further gain to 1.2800 and then 1.2900 but psychological resistance at 1.3000 would remain intact.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has possibly ended at 1.7192, below support at 1.4232 would add credence to this count, then further fall to 1.4000 level would follow but reckon downside would be limited to 1.3655 support and price should stay above previous support at 1.3500.

On the downside, whilst initial pullback to 1.2400 cannot be ruled out, reckon downside would be limited to 1.2350 and bring another rise later. A daily close below support at 1.2335 would dampen this bullish view and bring weakness to 1.2290-00 but reckon 1.2240-50 would hold, bring another rebound. A drop below 1.2240-50 would suggest the rebound from 1.2109 has ended instead, bring further fall to 1.2200 and then 1.2150-60 but said support at 1.2109 should remain intact.

Recommendation: Buy at 1.2350 for 1.2550 with stop above 1.2250.

Longer term - Cable's rise from 1.0520 (Feb 1985) to 2.0100 (September 1992) is seen as [A], the decline to 1.3682 is labeled as (B) and (C) wave rally has ended at 2.1162 (9 Nov, 2007) which is also the top of larger degree wave B with circle. The selloff from there is a 5-waver with wave (A) ended at 1.3500 (23 Jan 2009), wave (B) itself is labeled as A: 1.6733, triangle wave B: 1.4813 and wave C as well as top of wave (B) ended at 1.7192 (2014), hence the selloff from there is an impulsive wave (C) with wave I : 1.4566, wave II 1.5930, an extended wave III is unfolding and already exceeded our downside target at 1.3500 and 1.3000, hence weakness to 1.2500 and possibly 1.2000 cannot be ruled out, however, price should stay well above psychological level at 1.0000.

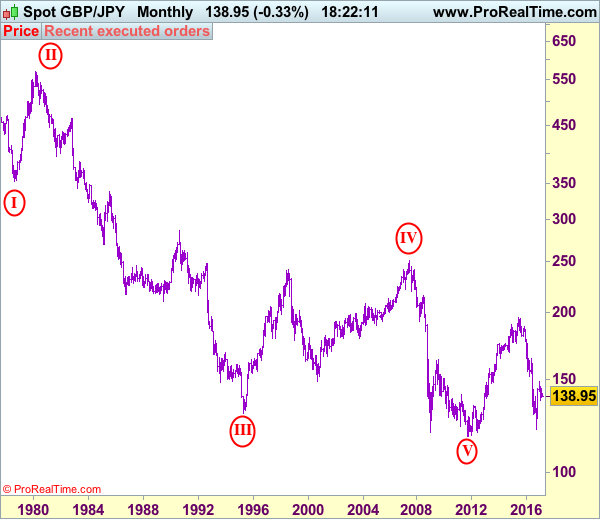

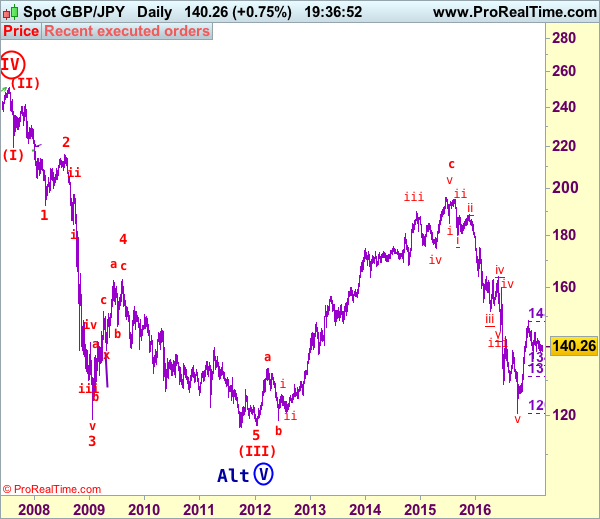

GBP/JPY Elliott Wave Analysis

GBP/JPY – 140.17

GBP/JPY – Wave 5 as well as wave (III) has possibly ended at 116.85

Although sterling fell marginally to 138.60, as the British pound has rebounded after holding above previous support at 138.45, suggesting further consolidation above this level would be seen with mild upside bias for another bounce to 140.70-75 and 141.75-80 but reckon 142.00-10 would hold from here. A daily close above resistance at 142.80 would signal the pullback from 144.75 has ended, bring further gain to 143.40-45 and then test of 144.10-15 but said resistance at 144.75 should hold. Looking ahead, a rise above 144.75 would signal the rebound from 136.50 is still in progress and may bring further upmove to indicated resistance at 145.40, break there would add credence to our bullish scenario that correction from 148.45 has ended at 136.50, bring further gain to 146.40-50, then 147.10-20.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.

On the downside, expect pullback to be limited to 139.50-60 and bring another rebound. Only below said support at 138.45 would suggest a possible downside break of recent established range, bring further fall to 137.50-60 and later 137.00-05, however, reckon previous support at 136.50 would contain downside, bring another rebound later. Looking ahead, only below this level would signal another leg of decline from 148.45 top is underway for retracement of early upmove from 120.50 to 135.90-00, then towards 134.45-50 (50% Fibonacci retracement of 120.50-148.45) which is likely to hold from here.

Recommendation: Buy at 139.50 for 142.50 with stop below 138.50.

The long-term downtrend from 570.99 (29 Feb 1980) is labeled as an impulsive wave with III with circle ended at 129.77 (20 Apr 1995) and the corrective rebound to 251.12 (20 Jul 2007) is treated as wave IV with circle and the wave V with circle selloff from 251.12 has possibly ended at 116.80 (almost reached our indicated target at 116.00) and major correction has commenced from there and indicated upside target at 183.90-00 (50% Fibonacci retracement of 251.10-116.85) had been met, reckon upside would be limited to 199.80-90 (61.8% Fibonacci retracement) and bring wave (V) decline in later part of 2017.