Sample Category Title

Fed, UK Brexit Bill And Oil In Focus On Monday

- Traders in wait and see mode after the Fed sets a high bar;

- UK in focus this week with BOE, jobs data and most importantly, the Brexit bill amendments being debated in parliament;

- Oil continues slide as US oil rigs climb and doubts rise over necessary output deal extension.

- It's been a relatively calm start to a week that is likely to be anything but, with European markets broadly mixed and US futures pointing to a flat open.

Traders appear to be in wait and see mode at the start of the week, with attention firmly on the central bank meetings this week, most notably the Federal Reserve on Wednesday when we'll find out if policy makers successfully guided market expectations in the right direction or went too far. The clearly coordinated effort to convince investors that a rate hike is firmly on the table on Wednesday, from a position in which it appeared out the question, has almost worked too well with markets now almost fully pricing one in. The risk is that the Fed now struggles to live up to expectations and should it for whatever reason delay raising interest rates, it may have unintentionally dramatically misguided investors which could result in significant volatility come Wednesday.

The UK will also be in focus this week but it may not necessarily be the Bank of England monetary policy decision or the jobs data that grabs our attention. With Theresa May's end of March article 50 deadline fast approaching, parliament is set to debate two amendments to the bill added by the House of Lords that would guarantee the rights of EU nationals in the UK and give parliament a vote on the final Brexit deal. The vote is particularly important for investors as it would theoretically reduce the possibility of a hard Brexit, the only downside being that in turn it may weaken May's negotiating position.

Should these amendments be approved by parliament today though, it would allow May to trigger article 50 and begin the divorce proceedings as early as tomorrow. There appears to be more appetite than May and some of her colleagues would like for a vote on the deal to be included in the bill, which is helping to support sterling this morning. The pound has come under pressure again as of late, with a number of economic releases appearing to show the economic cracks starting to appear following what has been a much smoother ride since the vote than many anticipated. Should the amendments be approved, it could offer more upside for the pound, with 1.2350-1.24 providing the next test to the upside against the dollar.

Oil remains in focus this morning, once again trading lower after Baker Hughes reported on Friday that the number of oil rigs in the US rose by eight to 617, the highest there's been since September 2015. The deal between OPEC and non-OPEC producers appears to be having little effect on the glut at the moment, with three of the last four weeks showing substantial inventory increases. Of course, these changes take time to have an impact and non-OPEC compliance is still a little low but with an extension to the deal in doubt, prices are reverting back towards pre-deal levels, although I doubt we'll get close to the lows any time soon.

DAX – Quiet Start To Week, Markets Eye German ZEW Economic Sentiment

The DAX Index has posted slight gains on Monday, trading at 11,977.00 in the European session. In economic news, there are no major releases in the Eurozone. ECB President Mario Draghi will deliver remarks on Tuesday. On Tuesday, German releases will be on center stage. ZEW Economic Sentiment is expected to climb to 13.2, and Final CPI is forecast to rebound to 0.6%.

On Friday, the DAX dropped below the symbolic 12,000 level, as some ECB policymakers raised the possibility of higher interest rates at last week's policy meeting. At the meeting, the ECB held course and maintained interest rates at a flat 0.00%. The markets were left to pick up on nuances, as ECB President Mario Draghi noted that the central bank removed one phrase from its standard introductory statement – 'using all the instruments available within its mandate'. Draghi stated that the removal of this phrase means that the ECB 'no longer has a sense of urgency in taking further actions …. prompted by the risk of deflation'. With growth and inflation showing signs of improvement, the ECB has been under pressure to tighten policy and reduce its asset-purchase program. Germany, in particular, is unhappy with the ECB's ultra-loose policy and on Thursday, German Finance Minister Wolfgang Schaeuble bluntly stated that he wanted to see a 'timely start to the exit' from the ECB's asset-purchase scheme. For his part, Mario Draghi must balance the improved economy with upcoming elections in the Netherlands and France. Euro-skeptics are a strong force throughout Europe and Draghi is reluctant to make any major moves in the middle of heated political campaigns.

The US economy continues to steam ahead at full speed, buoyed by a red-hot labor market. On Friday, Nonfarm Payrolls sparkled with a gain of 235 thousand. This easily beat the estimate of 196 thousand. The strong release makes it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room with the economy performing well.

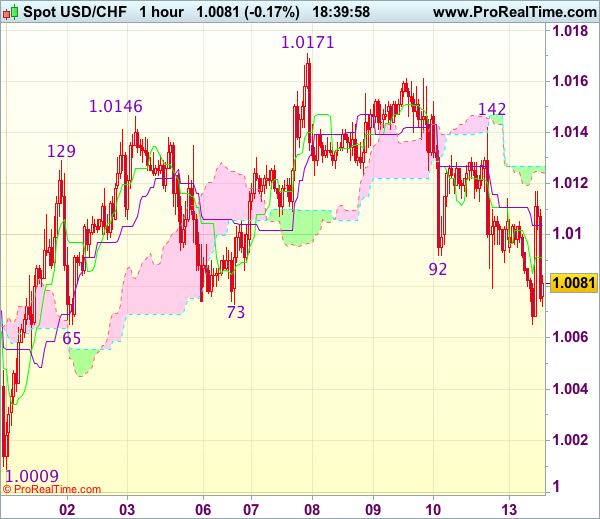

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 1.0077

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback met renewed selling interest at 1.0114 earlier today and has dropped again, suggesting the erratic fall from 1.0171 top is still in progress, however, break of support at 1.0065 is needed to retain bearishness and signal recent erratic rise from 0.9861 has ended and bring further fall to 1.0035-40 but support at 1.0009 should remain intact, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above 1.0114 would bring test of indicated resistance at 1.0142 but break there is needed to signal low is formed instead, bring further gain towards last week’s high at 1.0171.

Trade Idea Update: GBP/USD – Hold long entered at 1.2215

GBP/USD - 1.2218

Original strategy :

Bought at 1.2215, Target: 1.2320, Stop: 1.2180

Position : - Long at 1.2215

Target : - 1.2320

Stop : - 1.,2180

New strategy :

Hold long entered at 1.2215, Target: 1.2320, Stop: 1.2180

Position : - Long at 1.2215

Target : - 1.2320

Stop : - 1.2180

Current rally above indicated resistance at 1.2195 suggests a temporary low is possibly formed at 1.2135 last week and consolidation with upside bias is seen for retracement of recent decline, hence further gain to 1.2260-65 (38.2% Fibonacci retracement of 1.2471-1.2135) would be seen, however, break of 1.2301-03 (previous resistance and 50% Fibonacci retracement) is needed to signal low is formed, bring a stronger rebound to 1.2340-45 (61.8% Fibonacci retracement) later.

In view of this, we are holding on to our long position entered at 1.2215\. Below the Kijun-Sen (now at 1.2190) would defer and risk weakness to 1.2170 but said support at 1.2135 should hold. Only break there would abort and signal recent decline has resumed and extend weakness to 1.2100.

Trade Idea Update: EUR/USD – Buy at 1.0640

EUR/USD - 1.0666

Original strategy :

Buy at 1.0660, Target: 1.0760, Stop: 1.0625

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0640, Target: 1.0740, Stop: 1.0610

Position : -

Target : -

Stop : -

As the single currency has retreated after rising to 1.0714 earlier today, suggesting consolidation below this level would be seen and pullback to 1.0640 (previous resistance now support) cannot be ruled out, however, reckon downside would be limited and bring another rise later, above 1.0714 would signal the erratic rise from 1.0493 low is still in progress and may extend gain to 1.0740-45 (1.5 times projection of 1.0495-1.0640 measuring from 1.0525) but loss of near term upward momentum should prevent sharp move beyond 1.0760 (1.618 times projection of 1.0495-1.0640 measuring from 1.0525).

In view of this, we are looking to buy euro on further pullback as 1.0540 should limit downside, bring another rise later. Below another previous resistance at 1.0615 would abort and signal top has been formed, risk further fall to 1.0575-80 first.

AUDUSD – Return Above 200SMA Is Bullish Signal, Daily Cloud Continues To Underpin

The Aussie dollar extended bounce from last week's correction low at 0.7489 on Monday and returned above a cluster of strong supports between 0.7531 and 0.7504 (consisting of 55 / 100 and 200SMA's) that was cracked last week but without clear break lower.

Fresh weakness of the US dollar and strong bullish signals that are generating on the daily chart, suggest further recovery.

Rising daily cloud that so far contained pullback from 0.7739 peak, continues to underpin, with 55/100SMA Golden Cross and another one forming on attempts of rising 55SMA to break above 200SMA, are also seen as supportive factors, along with slow stochastic bullish divergence and reversal from oversold territory.

Extended recovery tested 0.7584 pivot so far (Fibo 38.2% of 0.7739/0.7489 pullback), with next two triggers (daily Tenkan-sen at 0.7593 and daily Kijun-sen at 0.7614) laying above, break f which to generate stronger signals that corrective phase might be over.

Top of rising daily cloud currently lies at 0.7515 and should contain extended corrective dips to keep near-term bulls in play.

Res: 0.7586, 0.7593, 0.7614, 0.7643

Sup: 0.7531, 0.7515, 0.7489, 0.7448

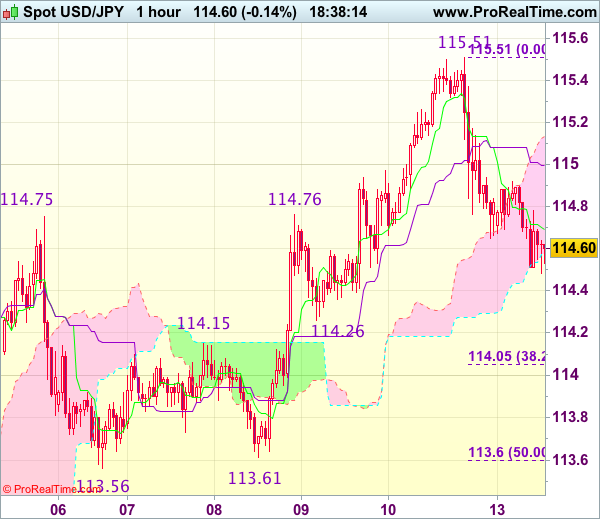

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 114.59

Original strategy :

Exit long entered at 114.70

Position : - Long at 114.70

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback recovered after finding support at 114.65, renewed selling interest emerged at 114.92 and dollar has fallen again today, suggesting near term downside risk remains for the fall from 115.51 top (last week’s high) to bring at least a retracement of recent upmove to 114.26 support but reckon downside would be limited to 114.00-05 (38.2% Fibonacci retracement of 111.69-115.51) and price should stay well above strong support at 113.56-61), bring rebound later.

In view of this, would be prudent to stand aside for now. Above the Kijun-Sen (now at 115.01) would suggest an intra-day low is formed, bring a stronger rebound to 115.25-30 but still reckon said resistance at 115.51 would cap upside. Only break there would revive bullishness and extend recent upmove to previous resistance at 115.62, then towards 115.90-00.

European Market Update: Quiet Start To Busy Week

Quiet start to busy week

Notes/Observations

Quiet EU session on Monday; Looking ahead numerous key events includes Netherlands election (Wed), G20 gathering in Germany and possible trigger to UK’s article 50. There are also numerous rate decision (FOMC on Wed, SNB, Norges and BOE on Thurs)

Italy Jan Industrial production saw its biggest monthly decline in 5 years (MoM: -2.3$ v -0.8%e)

Overnight:

Asia:

China Commerce Min (MOFCOM) Zhong Shan reiterated view that outlook for foreign trade faced lots of risks and uncertainties; Trade war between China and US would harm both economies

PBoC Gov Zhou Xiaochuan: Reiterates view that CNY currency (yuan) would remain stable and added it did not have a ‘bottom line’ for either dollar/yuan rate or FX reserves

China National Development and Reform Commission (NDRC) Vice Chairman Ning Jizhe: China's economic growth still mainly relied on domestic demand; unemployment rate in 31 major cities was about 5% in Jan-Feb period; industrial output grew more that 6%

Europe:

German Chancellor Merkel said to warn US President Trump that changes to US corporate tax could prompt retaliatory measures when they meet this Tuesday, Mar 14th; reviewing responses to border adjust tax, levying only US companies imports and not exports; May label the measure aprotective tariffwhich violates WTO rules.

PM May reportedly could trigger Article 50 as soon as Tuesday, March 14th if Parliament passed Brexit bill on Monday night

Brexit Min Davis stated that the govt was drawing up contingency plans for the unlikely event it had to walk away from talks with the European Union without a deal

Netherlands banned several Turkey ministers from entering Rotterdam over political campaigning among Turksih emigres; President Erdogan vowed to retaliate in the "harshest way" and called the Netherlands a "Nazi remnant"

Italy govt said to be working on plan to cut public debt which would transfer main assets of €50-60B into a vehicle which it would sell on market to raise money to cut public debt

Energy:

Weekly Baker Hughes US Rig Count: 768 v 756 w/w (+1.6%) (8th straight weekly rise)

Goldman Sachs analyst said to maintain positive outlook across the commodity complex; upholds Q2 WTI Oil & copper forecasts

Economic data

(TR) Turkey Jan Current Account: -$2.8B v -$2.8Be

(SE) Sweden Feb PES Unemployment Rate: 4.0% v 4.1% prior

(IT) Italy Jan Industrial Production M/M: -2.3% (largest decline in 5 years) v -0.8%e; Y/Y: 5.7% v 3.4% prior; Industrial Production WDA Y/Y: -0.5% v +3.2%e

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 09:30 GMT)

Indices [Stoxx50 -0.2% at 3,414, FTSE flat at 7,346, DAX flat at 11,967, CAC-40 flat at 4,992, IBEX-35 -0.2% at 9,985, FTSE MIB +0.1% at 19,669, SMI flat at 8,667, S&P 500 Futures -0.1%]

Market Focal Points/Key Themes: European equity indices are trading relatively flat after a generally positive end to the Asian session overnight; Banking stocks mixed in the Eurostoxx with shares of Deutsche Bank and Intesa Sanpaolo trading higher, despite shares of Santander and BNP Paribas weighing in the index; Commodity and mining stocks trading notably higher in the FTSE 100 as copper prices trade sharply higher intraday; conversely energy stocks are trading lower as oil prices gapped lower over the weekend, despite trading higher intraday.

Upcoming scheduled US earnings (pre-market) include Lifetime Brands, Del Taco Restaurants, and Townsquare Media.

Equities (as of 09:30 GMT)

Consumer Discretionary: [Aryzta ARYN.CH -6.4% (H1 results), Bang & Olufsen BO.DK -1.0% (Divests Czech subsidiary), Bovis Homes BVS.UK +7.3% (Rejects proposals from Redrow and Galliford Try)]

Consumer Staples: [HOCHDORF Holding HOCN.CH -0.5% (FY16 results)]

Energy: [Amec Foster Wheeler AMFW.UK +15.4% (to be acquired by Wood Group for £5.64/shr; FY16 results; contract win), Innogy IGY.DE -1.4% (FY16 results), Seadrill SDRL.NO +8.6% ($170M West Mira arbitration settlement), Senvion SEN.DE +2.5% (restricting measures, job cuts)]

Financials: [Helvetia Holding HELN.CH -3.9% (FY16 results), HSBC HSBA.UK +0.8% (Confirms Mark Tucker as new Chairman), Klepierre LI.FR +1.1% (€500M share repurchase)]

Healthcare: [TiGenix TIG.BE +1.6% (Top-Line Phase I/II Results of AlloCSC-01 in Acute Myocardial Infarction), Virbac VIRP.FR -7.7% (final FY16 results)]

Industrials: [ABB ABBN.CH -0.1% (Lower Pre-tax profit impact in 2016 from Korea case from $100M to $73M)]

Telecom: [Telit Communications TCM.UK +12.6% (FY16 results)]

Speakers

ECB's Smets (Belgium): improved economic outlook did not in itself signal a coming change in policy stance. Reiterated ECB view that it has not taken first step towards removing stimulus as it saw no considerable improvement in March inflation assessment (Staff Projections) compared to Dec outlook.

ECB's Visco (Italy): Reiterates view that a higher employment level is key to revive Italian growth. Euro skepticism was growing in member States and Europe political paralysis risk was never as high as it is today. USD currency appreciation and Fed hikes could intensify; have negative impact on emerging market economies

Swiss Stats Office updated inflation forecasts which raised 2017 CPI forecast from 0.0% to 0.5% and raise2018 CPI forecast from 0.2% to 0.3%

Poland Central Bank commented on inflation and growth outlook for 2017-19 period. Forecasted 2017 GDP at 3.7%, 2018 GDP at 3.3% and 2019 GDP at 3.2%. Forecasted 2017 and 2018 CPI at 2.0% and 2019 CPI at 2.3%. Inflation to stay below the 2.5% target in horizon period

France Presidential candidate Le Pen (Far right): New French franc currency would decline approx 10% against the Euro; falling currency will help more than it hurts

Japan reportedly to dispatch biggest warship on tour through South China Sea

Currencies

Busy week on central bank meetings and other key events. Wednesday’s Netherlands election outcome may well set the scene for the French April/May Presidential election. UK Govt could trigger Article 50 at any time in the next three weeks

Euro firmed to 1-month high during Asia in the aftermath of press reports last week that ECB discussed whether rates could rise before QE ended (idea did not get much discussion and did not have broad support). EUR/USD steady just ahead of the NY morning at 1.0670 area.

GBP/USD continued to move off recent 7-week lows and back above the 1.22 level. Amended EU (notification of withdrawal) Bill moved back in House of Commons today and reports that article 50 could be triggered as soon as Tuesday if all goes well in removing the amendments placed by the House of Lords last week.

USD/JPY in the mid-part of the 114 level in quiet trade.

Fixed Income:

Bund futures trade at 159.58 up 57 ticks rebounding sharply following a fortnight of declines having traded below 159 on Friday following the strong US jobs report. Support moves to Friday low of 158.87 followed by 158.74. Resistance moves to 159.85 Friday high followed by 160.20 then 161.06.

Gilt futures trade at 126.63 up 50 ticks trading up with Bunds on slight risk off tone ahead of the House of Commons vote on the Lords amendments to the latest Brexit Bill due to commence later today. Support moves to 125.88 the low seen on Friday followed by 125.57. Resistance remains at 126.87 followed by 127.35. Short Sterling futures trade flat to up 1bp, in slight flattening trade with Jun17Jun18 spread falling to 16/17bp.

Monday liquidity report showed Friday's excess liquidity rose to a record high of €1.371T up €6B from €1.365T prior. Use of the marginal lending facility rose to €450M from €136M prior.

Corporate issuance saw a further $1.1B come to market on Friday via 2 issuers headlined by John Deere 3 part $1B offering bringing last weeks issuance to $45B via 65 tranches, putting the Months volume to just shy of $60B. For the week ahead analysts see issuance to slow to around $15-20B.

In Euro denominated issuance last week saw €27.3B come to market via 37 issuers and 41 tranches, with Tuesday seeing the bulk of the issuance with just over €14B priced.

Looking Ahead

(UK) Amended EU (notification of withdrawal) Bill back in House of Commons

(CH) Swiss Parliament holds Spring Session in Bern

(IL) Israel Central Bank (BOI) Feb Minutes

(MX) Mexico Feb ANTAD Same-Store Sales Y/Y: 3.0%e v 4.1% prior

06:00 (EU) Daily Euribor Fixing

06:00 (ZA) South Africa announces details of upcoming I/L bond sale (held on Fridays)

06:00 (IT) Italy Debt Agency (Tesoro) to sell 2019, 2024, 2033 and 2046 medium BTP Bonds

06:00 (LT) Lithuania to sell Bonds

06:00 (RO) Romania to sell Bonds

06:00 (NO) Norway to sell NOK6.0B in 12-month Bills

06:30 (DE) Germany to sell €2.0B in 6-month BuBills

07:00 (PT) Portugal Jan Trade Balance: No est v -€1.4B prior

07:00 (IL) Israel Jan Trade Balance: No est v -$0.9B prior

07:00 (IL) Israel to sell 2018, 2020, 2021, 2025 and 2027 bonds

07:25 (BR) Brazil Central Bank Weekly Economists Survey

07:30 (TR) Turkey TCMB Survey of Expectations

07:30 (EU) NATO's Stoltenberg Press Conference in Brussels

07:30 (UK) (UK) Scottish First Min Sturgeon (SNP) speech

07:30 (IS) Iceland to sell Bills

07:45 (DE) German Chancellor Merkel meets leaders of German Industry Groups in Munich

07:45 (US) Daily Libor Fixing

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

09:00 (ES) Spain Debt Agency (Tesoro) to announce size of upcoming Bill and bond issuance (held on Tuesday/Thursday)

09:15 (UK) Baltic Dry Bulk Index

09:50 (FR) France Debt Agency (AFT) to sell combined €5.8-7.0B in 3-month, 6-month and 12-month BTF Bills

09:30 (CH) Swiss Government Question Time in Parliament

09:30 (EU) ECB’s Draghi

10:00 (US) Feb Labor Market Conditions Index Change: +2.5e v +0.25 prior

10:30 (EU) ECB announces Covered-Bond Purchases

10:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:50 (UK) BoE conducts reverse Gilt auction

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

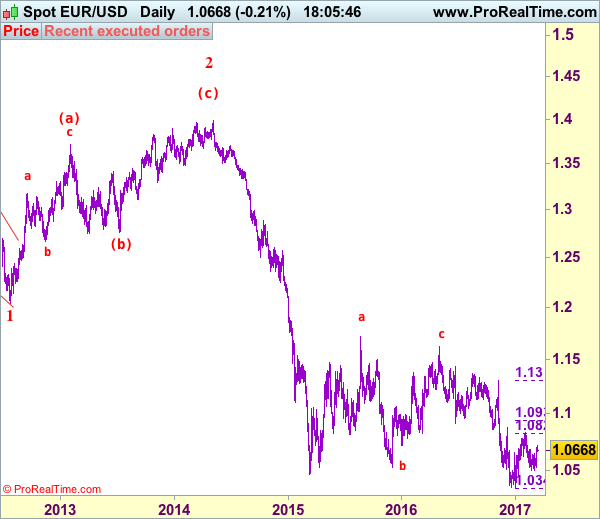

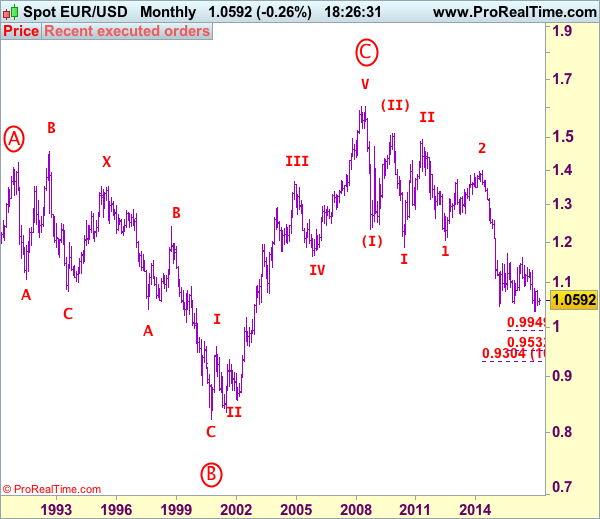

EUR/USD Elliott Wave Analysis

EUR/USD – 1.0668

EUR/USD: Wave (c) of 2 ended at 1.3993 and wave 3 of III has commenced for weakness to 1.0411 (1.236 of wave 1), then 1.0000.

The single currency found renewed buying interest at 1.0525 and has staged a strong rebound, suggesting near term upside risk remains for the rebound from 1.0493 to extend gain to 1.0740-50, however, as broad outlook remains consolidative, reckon upside would be limited and price should falter well below resistance at 1.0829, bring retreat later, below 1.0600 would bring another test of said support at 1.0525 but break there is needed to signal the rebound from 1.0493 has ended, bring another test of this level later.Looking ahead, only a drop below 1.0493-96 support would add credence to our view that the rebound from 1.0340 has ended at 1.0829 and bring further fall to indicated key support at 1.0454. A sustained break below this level would suggest the rebound from 1.0340 has ended, bring subsequent decline to 1.0390-00, then towards said recent low at 1.0340.

Our preferred count on the daily chart remains that a wave (II) from 1.2329 ended at 1.5145 with A-leg ended at 1.4720, followed by wave B at 1.2457, the wave C from there was also a 3 legged move and is labeled as (a): 1.3739, (b): 1.2885, the wave iii of the 5-waver (c) from 1.2885 has ended at 1.4339 and wave iv is a triangle ended at 1.3878 and wave v formed a top at 1.5145. The decline from there is a 5-waver (C) with minor wave (i) of I of (C) ended at 1.4218 with wave (ii) ended at 1.4580, wave (iii) ended at 1.3267 and wave (iv) ended at 1.3692 and wave (v) ended at 1.1876, this is also the low of wave I of (C) and wave II ended at 1.4940, hence wave III is now in progress with a diagonal wave 1 ended at 1.2042, the breach of previous support at 1.1876 (wave I trough) adds credence to our view that the wave 2 has ended at 1.3993, wave 3 has commenced for further weakness to 1.0411, then towards 1.0000.

On the upside, whilst initial recovery to 1.0740-50 cannot be ruled out, reckon upside would be limited and bring another decline later. A daily close above this level would risk retest of 1.0829 but break there is needed to signal the corrective rise from 1.0340 low is still in progress for retracement of recent decline to resistance at 1.0873 but still reckon upside would be limited to 1.0930-35 (61.8% Fibonacci retracement of 1.1300-1.0340) but reckon 1.1000 would hold from here, bring another decline in Q2.

Recommendation: Sell at 1.0740 for 1.0540 with stop above 1.0840.

Euro's long-term uptrend started from 0.8228 (26 Oct 2000) with an impulsive structure. The rise from 0.8228 to 0.9593 (5 Jan 2001) is labeled as wave I, the retreat to 0.8352 (6 Jul 2001) is wave II and the rally to 1.3670 (31 Dec 2004) is wave III. Wave IV from there ended at 1.1640 (15 Nov 2005), the subsequent upmove to 1.6040 (July 15, 2008) is treated as wave V, the major selloff from the record high of 1.6040 to 1.2329 (October 27, 2008) signals a reversal has taken place with (I) leg ended at 1.2329 and once (II) ended at 1.5145, wave (III) itself is an extended move with I: 1.1876 and complex wave II ended at 1.4902, wave III has commenced with wave 1 and 2 ended at 1.2042 and 1.3993 respectively, wave 3 of III is now unfolding for weakness towards parity.

USD Lower After Lacklustre Job Report

News and Events:

USD tumbles as real wages dip into negative territory

The US dollar had a tough start into the week as investors remained unmoved after Friday’s job report and even appeared disappointed amid lacklustre data. The US economy created 235k private jobs in February, widely beating the median forecast of 200k, while the previous month’s reading was upwardly revised to 238k. All employment measures improved in February as the unemployment rate eased to 4.7% as participation climbed to 63%. The U-6 measure or the underemployment rate fell to 9.2% from 9.4% a month previous. So, after such a bullish report how come the USD came under pressure this morning?

Well, there are a few explanations for this. Firstly, wage growth clearly failed to impress despite the solid pace of job creation as average hourly earnings grew 0.2%m/m versus 0.3% expected. Indeed, inflation pressures have intensified over the last few months as crude oil prices recovered - the consumer price index reached 2.5% in January. However, nominal wage growth remained stable, which translates into weaker purchasing power for the common American. Looking at how the measure adjusted for inflation, one immediately notices that real wages contracted 0.52%. This is the first time since December 2013 that the gauge has dipped into negative territory. In fact, since December 2015 real wage growth has started to decelerate and actually contracted last month. This negative trend could explain why the Fed was not in such a hurry to raise rates last year. Looking forward, it should not influence Wednesday’s meeting as Janet Yellen cannot take the risk of disappointing the market, especially after selling that rate hike for the past few months. However, it will definitely impact the Fed’s tightening path as the Fed will find itself on the hot seat. On one hand, it will have to control rising inflationary pressures, although the core measure remains stable; while on the other, if the Fed adds too much pressure too quickly on the economy, by increasing borrowing rates, it will slow - if not reverse - the current fragile recovery.

All in all, in the short-term the market will stay focussed on the mounting political risk in Europe, which would help the dollar to hold ground. The dollar’s medium-term outlook is heavily dependent on the results of the EU political elections; however, should the political chessboard stay unchanged, the USD will start to reverse gains.

Brexit: Will Article 50 be triggered this week?

As Brexit proceedings drag on and fears of a hard Brexit continue to loom large, the pound continues to paint a very vivid picture of market worries. At present, UK Parliament remains split on PM May’s EU exit plans with The House of Lords meeting today to debate its proposed amendments.

The outcome however will be of little relevance as May will plough on and trigger Article 50 as planned. From that point, Britain’s EU divorce will take up to two years to complete but in our view, likely much longer as the UK will surely negotiate bilateral agreements. The question on everyone’s lips right now of course is whether the PM will cut the cord with no actual deal in place.

Currency-wise, the pound has been feeling the heat from both the single currency and the greenback over the past couple of weeks on the back of renewed hard Brexit fears. In our view, we believe that there is a strong opportunity to reload bullish pound positions. In our view, the dragging out of these proceedings will be more damaging than the actual exit itself. Brexit will not be the promised apocalyptic nightmare and will allow the UK breathing space to regain its competitive stance, free from constraint from Brussels.

Today's Key Issues (time in GMT):

- Jan Trade Balance ex Ships, last 6.9b, rev 7.9b DKK / 08:00

- Jan Current Account (Seasonally Adjusted), last 19.7b, rev 21.5b DKK / 08:00

- Bank of Italy Governor Visco Attends Foreign Office Conference EUR / 08:30

- mars.10 Total Sight Deposits CHF, last 553.4b CHF / 09:00

- mars.10 Domestic Sight Deposits CHF, last 471.5b CHF / 09:00

- Jan Industrial Production NSA YoY, last 3,40%, rev 3,50% EUR / 09:00

- Jan Industrial Production WDA YoY, exp 3,20%, last 6,60%, rev 6,80% EUR / 09:00

- Jan Industrial Production MoM, exp -0,80%, last 1,40% EUR / 09:00

- ECB's Villeroy De Galhau speaks in Paris EUR / 10:15

- ECB's Liikanen Speaks at Seminar on Rome Treaty in Helsinki EUR / 11:00

- Central Bank Weekly Economists Survey (Table) BRL / 11:25

- TCMB Turkey Survey of Expectations TRY / 11:30

- ECB Board Member Sabine Lautenschlaeger Speaks in Dublin EUR / 12:45

- 2Q Manpower Survey, last 15% NZD / 13:01

- 2Q Manpower Survey, last 8% AUD / 13:01

- ECB President Draghi opens conference in Frankfurt EUR / 13:30

- mars.10 Bloomberg Nanos Confidence, last 57,4 CAD / 14:00

- Feb Labor Market Conditions Index Change, exp 2,5 USD / 14:00

- ECB Vice President Constancio chairs panel in Frankfurt EUR / 14:00

- ECB Publishes Weekly QE Holdings EUR / 14:45

- Bank of England Bond Buying Operation (Reinvestment) GBP / 14:50

- ECB's Praet chairs panel in Frankfurt EUR / 16:30

- mars.12 Trade Balance Weekly, last $697m BRL / 18:00

- Feb Export Price Index MoM, last 1,10% KRW / 21:00

- Feb Export Price Index YoY, last 7,40% KRW / 21:00

- Feb Import Price Index YoY, last 13,20% KRW / 21:00

- Feb Import Price Index MoM, last 2,10% KRW / 21:00

- RBA's Bullock Speech at Bloomberg, Sydney AUD / 21:30

- 4Q BoP Current Account Balance, exp -$12.00b, last -$3.40b INR / 22:00

- mars.12 ANZ Roy Morgan Weekly Consumer Confidence Index, last 113,9 AUD / 22:30

- Feb Foreign Direct Investment YoY CNY, exp -4,20%, last -9,20% CNY / 23:00

- Feb Budget Balance YTD, exp -350.0b, last -23.4b RUB / 23:00

- Feb Tax Collections, exp 93663m, last 137392m BRL / 23:00

- ECB President Mario Draghi Speaks in Frankfurt EUR / 23:00

The Risk Today:

EUR/USD continues to strengthen. Hourly resistance given at 1.0679 (16/02/2017 high) has been broken while hourly support at 1.0493 (22/02/2017 low). The technical structure suggests deeper consolidation towards 1.0500. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD continues to edge lower despite ongoing consolidation since the pair has broken support given at 1.2254 (19/01/2017 low). The road is wide-open for further decline. Hourly resistance is now given at 1.2300 (05/03/2017 high). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY is pushing higher towards key resistance given at 115.62 (19/01/2016 high). Hourly support can be found at 113.56 (06/03/2017 low). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF is still riding within uptrend channel and is on its way to monitor hourly support implied by lower bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Expected to consolidate. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.1731 | 121.69 |

| 1.0954 | 1.3121 | 1.0652 | 118.66 |

| 1.0874 | 1.2771 | 1.0344 | 115.62 |

| 1.0670 | 1.2204 | 1.0079 | 114.57 |

| 1.0454 | 1.1986 | 0.9967 | 111.36 |

| 1.0341 | 1.1841 | 0.9862 | 106.04 |

| 1.0000 | 1.0520 | 0.9550 | 101.20 |