Sample Category Title

Yen Steady as Japanese Inflation Improves

USD/JPY is almost unchanged in the Monday session. Currently, the pair is trading at 114.70. In Japan, PPI climbed to 1.0%, matching the forecast. This marked a second straight gain after a long string of declines. Core Machinery Orders disappointed with a sharp decline of 3.2%, well short of the forecast of 0.0%. In the US, there is one minor event on the schedule. On Tuesday, the US releases PPI, with the index expected to slip to 0.1%.

Japanese manufacturing numbers were mixed last week. After over a year of declines, Preliminary Machine Tool Orders has posted two straight gains, including a strong gain of 9.1% in February. The BSI Manufacturing Index, based on a survey of large manufacturers, disappointed in the first quarter, dropping to 1.1 points. The markets had predicted a much stronger reading of 8.4 points.

The US economy continues to steam ahead at full speed, buoyed by a red-hot labor market. On Friday, Nonfarm Payrolls sparkled with a gain of 235 thousand. This easily beat the estimate of 196 thousand. The strong release makes it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room with the economy performing well.

Scottish Referendum Shocker Rattles Sentiment

A fresh layer of uncertainty was added to the Brexit woes on Monday following reports of Scottish First Minister Nicola Sturgeon demanding a new Scottish independence referendum between autumn of 2018 and spring 2019. This bombshell development comes at a time where speculations have heightened over UK Prime Minister Theresa May potentially triggering Article 50 on Tuesday. With Sturgeon on a quest to obtain permission from the Scottish Parliament for a second referendum via the Section 30 process, the rising anxiety may expose Sterling to downside shocks. It should be kept in mind that the live threat of an independence vote in Scotland, destabilizing the United Kingdom, while it is in the critical process of leaving the European Union could weigh heavily on sentiment.

With the Brexit launch around the corner participants most likely will remain edgy from the terrible cocktail of uncertainty, revived hard Brexit fears and concerns of a Scottish referendum. Markets will be paying very close attention to how the Brexit negotiations take place with any early complications exposing the unstable Sterling to further losses. Sentiment remains bearish towards the Pound and with the Brexit developments repeatedly limiting gains, the sharp appreciation on the GBPUSD during early trading on Monday was likely attributed to Dollar weakness. The current technical bounce on the pair could provide a foundation for sellers to attack with targets stretching back towards 1.2100.

WTI gripped by oversupply concerns

The recent bearish reports of U.S crude inventories surging to record highs have renewed the oversupply concerns ultimately exposing oil prices to downside risks this month. Oil markets remain vulnerable to losses moving forward with gains limited as optimism starts to wane over the effectiveness of OPEC's production cut. Although OPEC members may be commended on their attempt to stabilizing the oil markets by cutting production, the fact that oil prices are almost where they were when the initial production cut deal was announced is a major cause for concern. Sentiment towards oil is firmly bearish and the threat of OPEC not renewing its production cut deal for the second half of the year could spell further depreciations for oil in the medium to longer term. Oil market weakness should remain a dominant theme with the current price action suggesting that supply continues to outweigh demand and fears heightening over U.S shale destabilizing the OPEC production cut deal. From a technical standpoint, WTI Crude is bearish on the daily charts as there have been consistently lower lows and lower highs. Previous support at $50 could transform into a dynamic resistance that encourages a further decline lower towards $47.

Dollar regains some ground

The rising prospects of higher US interest rates this year have supported the Greenback with bulls propelling the Dollar Index back above 101.00 during Monday's trading session. Expectations have solidified over the Federal Reserve raising US interest rates this week following February's solid NFP figure with investors seeking clarity on future rate hike timings. If the economic projections of the FOMC members are bullish and suggest further US rate hikes this year then the Greenback may charge back above 102.00 in the short to medium term. From a technical standpoint, although the Dollar Index is slightly pressured on the daily charts, a breakout back above 101.50 could encourage an incline higher towards 102.00.

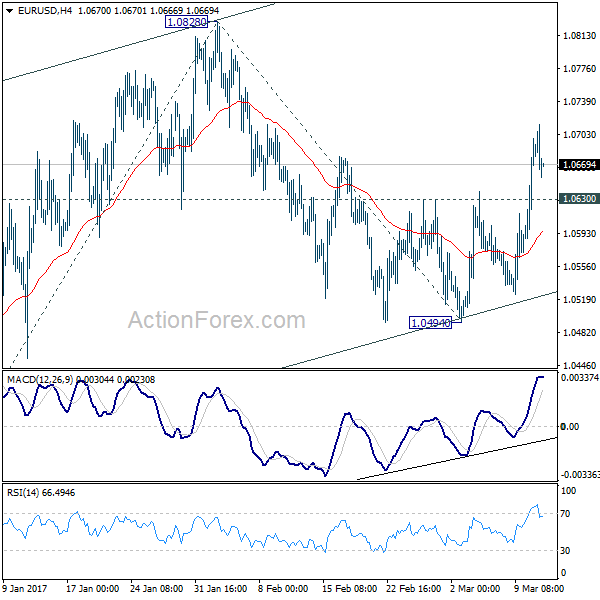

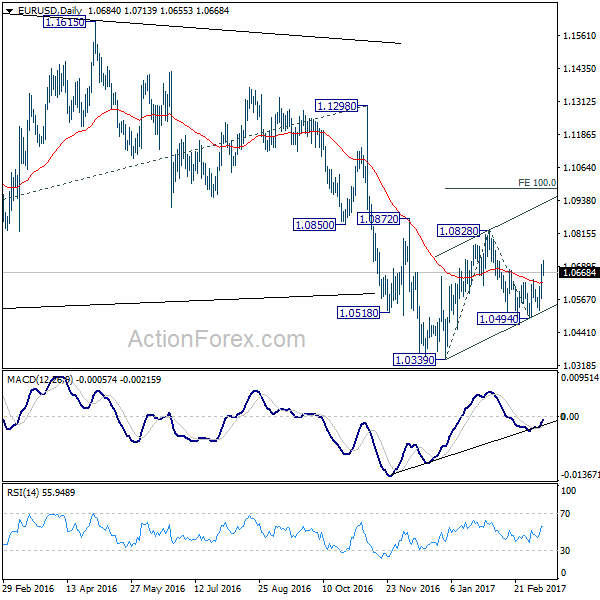

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0595; (P) 1.0647 (R1) 1.0723; More.....

With 1.0630 minor support intact, intraday bias in EUR/USD remains on the upside. Rise from 1.0494 is expected to extend to 1.0828 resistance and above. Note again that rise from 1.0339 low is seen as a corrective move. Hence, we'd expect upside to be limited by 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. The larger down trend is still expected to resume later. On the downside, break of prior resistance at 1.0630 will turn bias back to the downside for retesting 1.0494 low.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115.

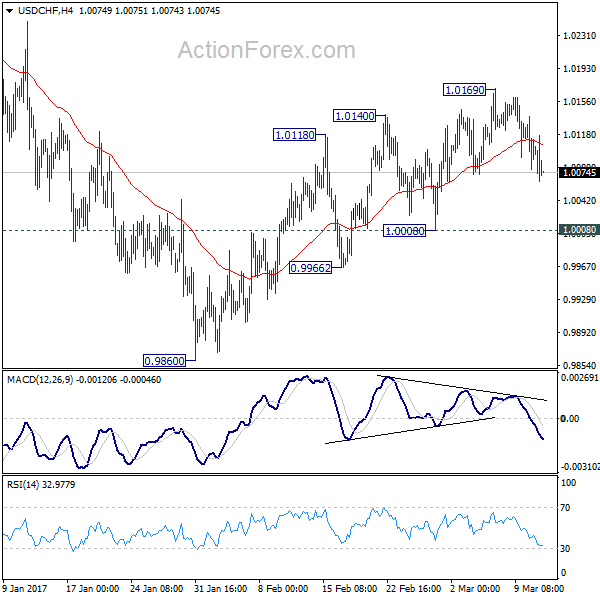

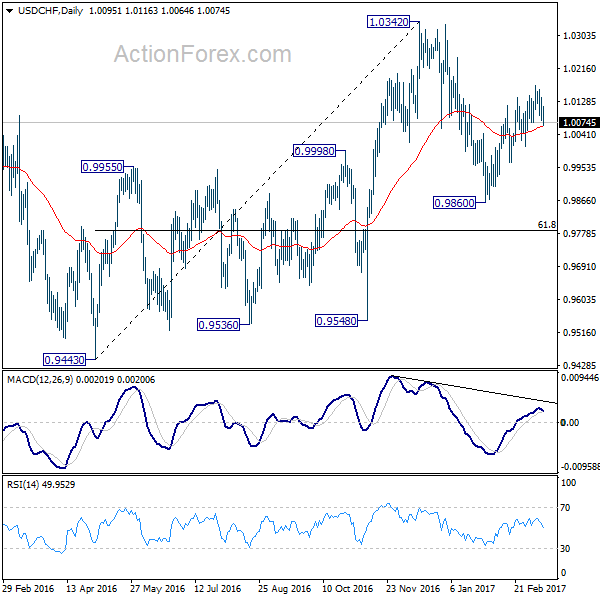

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0078; (P) 1.0107; (R1) 1.0135; More.....

USD/CHF is still staying well above 1.0008 minor support and intraday bias stays neutral for the moment. Another rise is mildly in favor. Above 1.0169 will turn bias to the upside and target a test on 1.0342 resistance. Based on neutral medium term outlook, we'd be cautious on topping below 1.0342. On the downside, break of 1.0008, however, will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

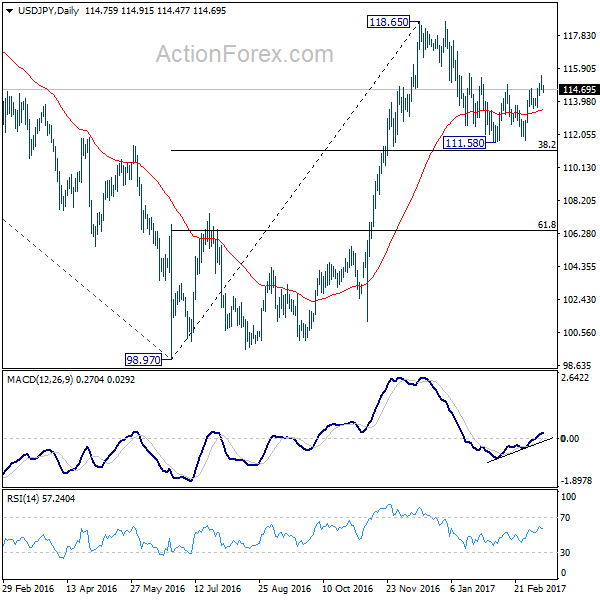

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 114.42; (P) 114.96; (R1) 115.28; More...

USD/JPY retreats further today but loss is limited so far. Intraday bias stays neutral for consolidation below 115.49 temporary top. Deeper retreat could be seen to 4 hour 55 EMA (now at 114.22). But downside should be contained well above 113.60 support and bring another rally. As noted before, corrective decline from 118.65 should have completed with a a double bottom pattern (111.58, 111.68). Above 115.49 should turn bias to the upside and pave the way for a test on 118.65. Decisive break there will extend whole rise from 98.97 and target 125.85 high next. However, break of 113.60 will invalidate our view and turn bias back to the downside for 111.58/68 support zone instead.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

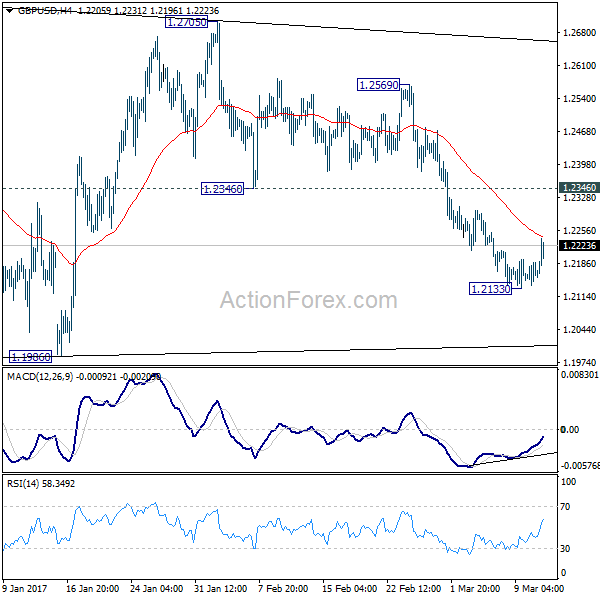

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2160; (R1) 1.2187; More...

GBP/USD reaches as high as 1.2398 today so far as recovery from 1.2133 extends. Intraday bias remains neutral for the moment as such rise is seen as a correction. We'd expect upside of recovery to be limited by 1.2346 support turned resistance and bring fall resumption. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. On the downside, below 1.2133 will turn bias to the downside for retesting 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view. However, sustained break of 1.2346 will dampen out view and turn focus back to 1.2569 resistance first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Sterling Higher as PM May Could Trigger Brexit This Week

Sterling surges broadly today on news that UK Prime Minister Theresa May could trigger Article 50 for Brexit this week. The House of Commons is set to debate the Brexit bill today and there is hope for passing the bill unamended. The House of Lords has already approved two amendments to the bill last week, in particular to grant the Parliament a "meaningful vote" on the final agreement. Passing the of bills in Commons today would set the stage for May to start' her plan for a so-called "hard Brexit". And the announcement could happen as soon as tomorrow. GBP/USD is trading above 1.22 at the time of writing, comparing to last week's low at 1.2133. EUR/GBP is back at 0.872, comparing to last week's high at 0.8786. While Sterling recovers today, it's still holding below near term resistance against Dollar and Euro. Thus, it's maintaining bearish outlook.

Scotland seeks another independence referendum

Also from UK, Scotland's First Minister Nicola Sturgeon announced today that she will seek another independence referendum as early as next year as a response to Brexit. She noted that with Brexit, there is a "material change in circumstances" since Scottish voted to stay in UK by 55 to 45 in 2014. She emphasized that "the future of the U.K. looks very different today than it did two years ago." She criticized that while she sought negotiations with UK PM May on Brexit details, the UK government "has not moved even an inch in pursuit of compromise or agreement." Sturgeon targets to have the referendum in late 2018 or early 2019. And by the time, the exact terms of Brexit should be known.

Euro lower as as Dutch vote this week

Euro trades broadly lower today and pares back some of the ECB triggered gains. Focus is turning to the election in the Netherlands this week. Dutch will head to vote and elect their next prime minister. The Netherlands is seen by many as a "fractured" policy environment and as many as 28 parties are running to be a part of the next government. And as many as five parties could be needed to form the coalition even though the Liberals are tipped to secure a majority of votes. While the result of the Dutch election is unlikely to surprise the markets much, some analysts see that as a precursor to French elections in April and May.

Dollar soft ahead of FOMC

Dollar stays weak in general even though in recovers some losses against Euro and Yen. Fed is widely expected to hike interest rate by 25bps this week. However, such expectation should be fully priced in, traders are looking through the FOMC meeting and turning cautious. In particular, Fed's updated Summary of Projections (SEP) and the monetary policy outlook for the rest of the year would be crucial to Dollar's trend in near term.

BoJ, BoE, SNB to meet

In addition to FOMC meeting, BoJ, BoE and SNB will announce monetary policy decisions this week. All are scheduled for Thursday and thus, we'll have a 24 hours of central bank frenzy from Wednesday to Thursday. All, BoJ, BoE and SNB are expected to stand pat. BoJ is expected to maintain the so called yield curve control framework. BoE's bias would likely stay neutral but may adjust its view on upside risks in inflation. The SNB is expected to leave its sight deposit rate unchanged at -0.75%. These three central bank announcements could end up being non-events.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2133; (P) 1.2160; (R1) 1.2187; More...

GBP/USD reaches as high as 1.2398 today so far as recovery from 1.2133 extends. Intraday bias remains neutral for the moment as such rise is seen as a correction. We'd expect upside of recovery to be limited by 1.2346 support turned resistance and bring fall resumption. As noted before, consolidation pattern from 1.1946 is completed at 1.2705 is resuming larger down trend. On the downside, below 1.2133 will turn bias to the downside for retesting 1.1946/86 support zone. Break of 1.1946 will confirm our bearish view. However, sustained break of 1.2346 will dampen out view and turn focus back to 1.2569 resistance first.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Feb | -3.20% | 1.00% | 0.50% | |

| 23:50 | JPY | Machine Orders M/M Jan | 1.00% | 0.00% | 6.70% | |

| 4:30 | JPY | Tertiary Industry Index M/M Jan | 0.00% | 0.20% | -0.40% | -0.30% |

| 14:00 | USD | Labor Market Conditions Index Change Feb | 1.3 |

Canadian Dollar Subdued at Start of Week

USD/CAD is almost unchanged in the Monday session. In North American trade, the pair is trading at the 1.3460. On the release front, it's a very quiet start to the week. There are no Canadian releases until Thursday. In the US, there is one minor event on the schedule. On Tuesday, the US releases PPI, with the index expected to slip to 0.1%.

Canada's economy continues to create jobs at an impressive clip, as the Canadian economy continues to expand thanks to the strong recovery south of the border. On Friday, Employment Change came in at 15.3 thousand. This was lower than the previous two readings, but easily beat the forecast of 0.6 thousand. The economy has created jobs for seven straight months, as the labor market continues to recover. The unemployment rate also improved, dropping from 6.8% to 6.6%. Still, these figures only tell part of the story. Wage growth remains soft, and many of the recent job gains have been part-time positions. The Canadian dollar posted only modest gains on Friday, as upward movement was limited by a very strong Nonfarm Payrolls report in the US.

The US economy continues to steam ahead at full speed, buoyed by a red-hot labor market. On Friday, Nonfarm Payrolls sparkled with a gain of 235 thousand. This easily beat the estimate of 196 thousand. The strong release makes it a virtual certainty that the Fed will raise rates by a quarter-point on Wednesday. Although a rate hike has been priced in by the markets, there have been disappointments in the past, so a rate move will likely give the dollar a boost against its major rivals, such as the euro. The solid job numbers also give President Trump a much-needed boost. Trump is under pressure to present an economic agenda, but the markets won't mind giving him some additional breathing room with the economy performing well.

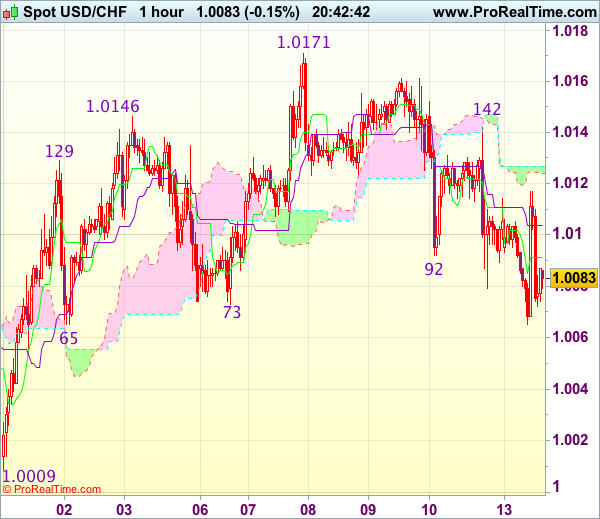

Trade Idea Update: USD/CHF – Stand aside

USD/CHF - 1.0085

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback met renewed selling interest at 1.0114 earlier today and has dropped again, suggesting the erratic fall from 1.0171 top is still in progress, however, break of support at 1.0065 is needed to retain bearishness and signal recent erratic rise from 0.9861 has ended and bring further fall to 1.0035-40 but support at 1.0009 should remain intact, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above 1.0114 would bring test of indicated resistance at 1.0142 but break there is needed to signal low is formed instead, bring further gain towards last week’s high at 1.0171.

Trade Idea Update: GBP/USD – Hold long entered at 1.2215

GBP/USD - 1.2218

Original strategy :

Bought at 1.2215, Target: 1.2320, Stop: 1.2180

Position : - Long at 1.2215

Target : - 1.2320

Stop : - 1.,2180

New strategy :

Hold long entered at 1.2215, Target: 1.2320, Stop: 1.2180

Position : - Long at 1.2215

Target : - 1.2320

Stop : - 1.2180

Current rally above indicated resistance at 1.2195 suggests a temporary low is possibly formed at 1.2135 last week and consolidation with upside bias is seen for retracement of recent decline, hence further gain to 1.2260-65 (38.2% Fibonacci retracement of 1.2471-1.2135) would be seen, however, break of 1.2301-03 (previous resistance and 50% Fibonacci retracement) is needed to signal low is formed, bring a stronger rebound to 1.2340-45 (61.8% Fibonacci retracement) later.

In view of this, we are holding on to our long position entered at 1.2215\. Below the Kijun-Sen (now at 1.2190) would defer and risk weakness to 1.2170 but said support at 1.2135 should hold. Only break there would abort and signal recent decline has resumed and extend weakness to 1.2100.