Sample Category Title

Japan’s PMI manufacturing falls to 49.0, services rises to 50.2

Japan’s PMI Manufacturing index edged down to 49.0 from 49.2 in November, signaling a deepened contraction in the sector. In contrast, PMI Services rose slightly to 50.2 from 49.7, indicating a renewed, albeit modest, expansion. PMI Composite improved marginally but remained below the neutral mark at 49.8, up from 49.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, noted that demand conditions were "stagnant," while employment grew at the fastest rate in four months. Price pressures persisted across sectors, driven by rising raw material costs and Yen’s weakness. Firms responded with sharper increases in prices charged for goods and services, aiming to pass on these higher cost burdens to customers.

Australia’s PMI composite falls to 49.4, second contraction in three months

Australia’s PMI Manufacturing improved sharply from 47.3 to 49.3 in November, marking a six-month high but remaining in contraction territory. Conversely, PMI Services index dropped from 51.0 to 49.6, hitting a 10-month low and signaling contraction. PMI Composite fell from 50.2 to 49.4, its lowest level in 10 months, indicating a slight overall contraction in private sector output for the second time in three months.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, highlighted the significance of the services sector’s slowdown. “The November S&P Global Flash Australia PMI posted the lowest reading since January, bringing the fourth-quarter average thus far below that of the prior quarter,” Pan said.

The report also noted that easing capacity pressures and subdued activity contributed to slower employment growth, which fell further below the long-term average. In addition, selling price inflation eased as businesses showed caution in raising charges. This combination of softer employment growth and reduced price pressures supports expectations of lower interest rates.

Cliff Notes: Calm Conditions

Key insights from the week that was.

In Australia, the RBA’s November Meeting Minutes provided a deep dive into the Board’s baseline views and assessment of risks. Chief Economist Luci Ellis subsequently discussed a number of noteworthy developments, one being the statement that the Board “would need to observe more than one good quarterly inflation outcome to be confident that such a decline in inflation was sustainable.” This is in line with the Board’s policy strategy to take and signal a patient and careful approach to assessing current disinflation. It should also be noted that the RBA’s economic and policy forecasts incorporate technical assumptions on the cash rate path based on market pricing. Of late, market pricing has shifted the start date for cuts back and also reduced the expected quantum of easing; the RBA have expressed a greater degree of comfort with such a view, considering known risks at this time.

Following these developments, we adjusted our view on the most probable path for monetary policy. We have moved back the start date for the cutting cycle from February to May, but have retained 100bps of easing in 2025, with a terminal rate of 3.35% still forecast for the December quarter. We see risks to the timing of the first cut in May as broadly balanced. Some of the more notable risks include the pace of the expected recovery in consumer spending following Stage 3 tax cuts – the hit to real incomes in prior years and caution shown by consumers towards spending in recent months leads us to expect a slower recovery in consumption growth than the RBA – and the tightness of the labour market. Both of these uncertainties have important implications for inflation’s trajectory. Next week’s October monthly inflation gauge will be another important update on Australia’s immediate inflation pulse and the risks (see here for our preview).

Over in the UK, annual inflation accelerated to 2.3% in October as electricity price rebates from 2023 cycled out. Core inflation was unaffected by this development, but edged higher to 3.3%yr in the month as services inflation remained sticky around 5.0%yr. Inflation is on track to overshoot the Bank of England’s 2.0%yr target for 2024 overall – the CPI needs to rise just 0.1% in the next two months for annual inflation to print at 2.25%yr come December 2024. The BoE’s more cautious tone around back-to-back cuts hence speaks to the lingering uncertainty for inflation.

In Japan meanwhile, while the data has not pushed rate hikes off the table, it is also yet to convince that the virtuous cycle of prices and wages is being sustained. Governor Ueda noted this week that the December meeting would be ‘live’ and that data between now and December would dictate their decision. CPI ex. fresh food came in slightly above expectations at 2.3%yr in October, below September’s 2.4%yr and August’s 2.8%yr, but above the 2.0%yr policy target. Services inflation has shown greater momentum in the past three months. RENGO leader Tomoko Yoshino has called on the new Prime Minister to support small businesses in raising wages ahead of the union’s wage negotiations in March. RENGO will be targeting another 5.0% increase in wages for FY25 after it secured a 5.1% increase in FY24. Persistence in inflation will help make the union’s case, as will support from the government. Large businesses in Japan have been quieter this year about their wage plans. Arguably, the BoJ will want to see evidence that businesses intend to maintain wage growth in FY25 before they raise rates again.

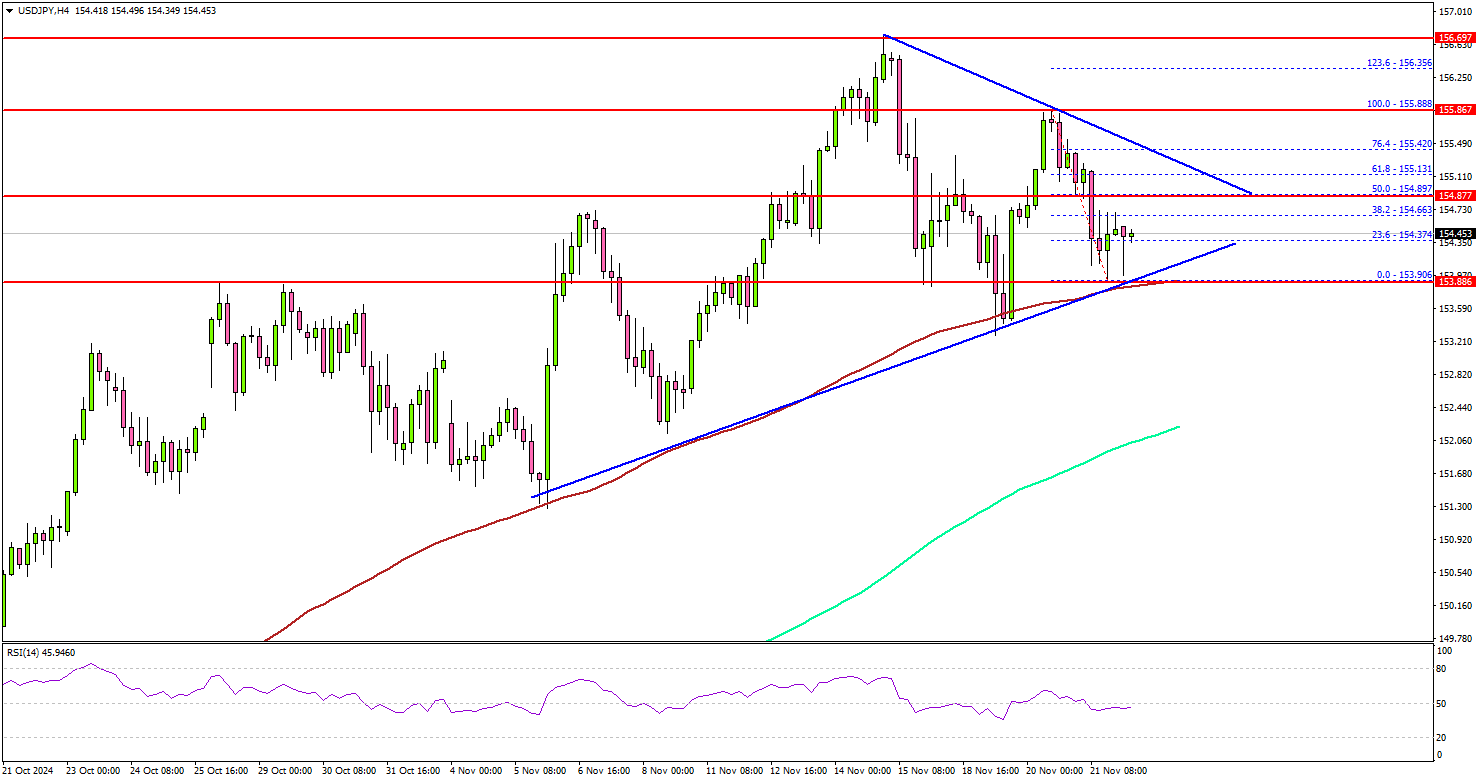

USD/JPY Consolidates: Is a Fresh Upside Move Ahead?

Key Highlights

- USD/JPY started a consolidation phase above the 154.00 zone.

- A major contracting triangle is forming with resistance at 155.30 on the 4-hour chart.

- Bitcoin remains in a strong uptrend and traded to a new all-time high above $95,000.

- EUR/USD dipped further and traded below the 1.0500 support zone.

USD/JPY Technical Analysis

The US Dollar started a downside correction below 156.00 against the Japanese Yen. USD/JPY traded below the 155.50 support to enter a short-term bearish zone.

Looking at the 4-hour chart, the pair dipped below the 154.20 support and tested the 100 simple moving average (red, 4-hour). The pair remained stable above 154.00 and is currently well above the 200 simple moving average (green, 4-hour).

A low was formed at 153.90 and the pair is now trading in a range. On the upside, the pair could face resistance near the 154.90 level.

The first major resistance is near the 155.30 level. There is also a major contracting triangle forming with resistance at 155.30 on the same chart. A close above the 155.30 level could set the tone for another increase.

The next major resistance could be 155.85, above which the price could climb higher toward the 156.50 resistance. Any more gains might send USD/JPY toward 158.00.

On the downside, immediate support sits near the 154.00 level. The next key support sits near the 153.60 level. Any more losses could send the pair toward the 153.00 level or even 152.40 in the near term.

Looking at Bitcoin, the price extended gains, traded to a new all-time high above $94,000 and might continue to move up.

Upcoming Economic Events:

- Euro Zone Manufacturing PMI for Oct 2024 (Preliminary) – Forecast 46.0, versus 46.0 previous.

- Euro Zone Services PMI for Oct 2024 (Preliminary) – Forecast 51.8, versus 51.6 previous.

- US Manufacturing PMI for Oct 2024 (Preliminary) – Forecast 48.8, versus 48.5 previous.

- US Services PMI for Oct 2024 (Preliminary) – Forecast 55.3, versus 55.0 previous.

Bitcoin’s (BTC/USD) Rocket Ride to Near $100,000, More to Come?

- Bitcoin’s price surge is fueled by institutional demand, growing mainstream acceptance, and a derivatives market boom.

- The derivatives market surge, while driving prices higher, also increases volatility and the risk of liquidations.

- ETF inflows have approached $2 billion in three days, further boosting Bitcoin’s rally.

Bitcoin prices continue to rise and print fresh highs as speculation continues to grow around a favorable outlook toward crypto from the incoming Trump administration. To further support these rumors, leaks about a potential White House crypto expert appointment and rumors of Trumps social media companies interest in a buyout of crypto trading firm Bakkt has aided the rally.

The Crypto Fear and Greed index shows markets are in a period of extreme greed.

Source: FinancialJuice

The question is whether this will lead to pullback or are we set for more gains in the coming weeks?

Bitcoin’s Impressive Climb Amid Derivative Market Surge

One big reason Bitcoin’s price has gone up is because institutional demand continues to rise.. They’re putting a lot of money into Bitcoin, which makes it more trustworthy. For example, MicroStrategy has bought a lot of Bitcoin and made a good profit as its value has increased.

The way the market works also helps. More people are accepting Bitcoin as a real type of investment. Since there’s only a limited amount of Bitcoin available and more people want it, the price keeps going up on the basic rule of supply and demand.

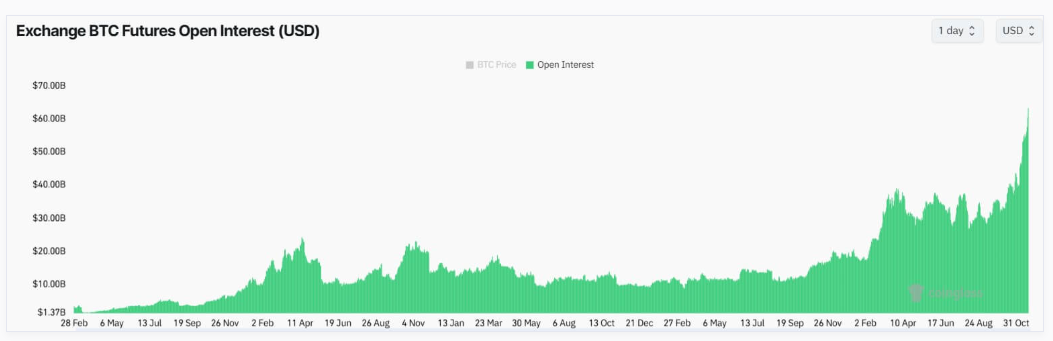

The derivatives market is a big factor in Bitcoin’s price increase. Bitcoin’s Open Interest, which shows how many contracts are active, has reached $63 billion. This is a record amount and is much higher than in 2021 when it was over $20 billion. Back then, Bitcoin’s price was at its highest, around $69,000.

Source: Coinglass

The derivatives market surge does pose risks however with volatility expected to be higher and price swings a more common occurrence. This is simply down to leverage with wild price swings likely to lead to an increase in liquidations.

Over the past 24 hours, liquidations have totaled $450 million with around 60% of this coming from short positions. The old adage rings true for Bitcoin as well, ‘the trend is indeed your friend’.

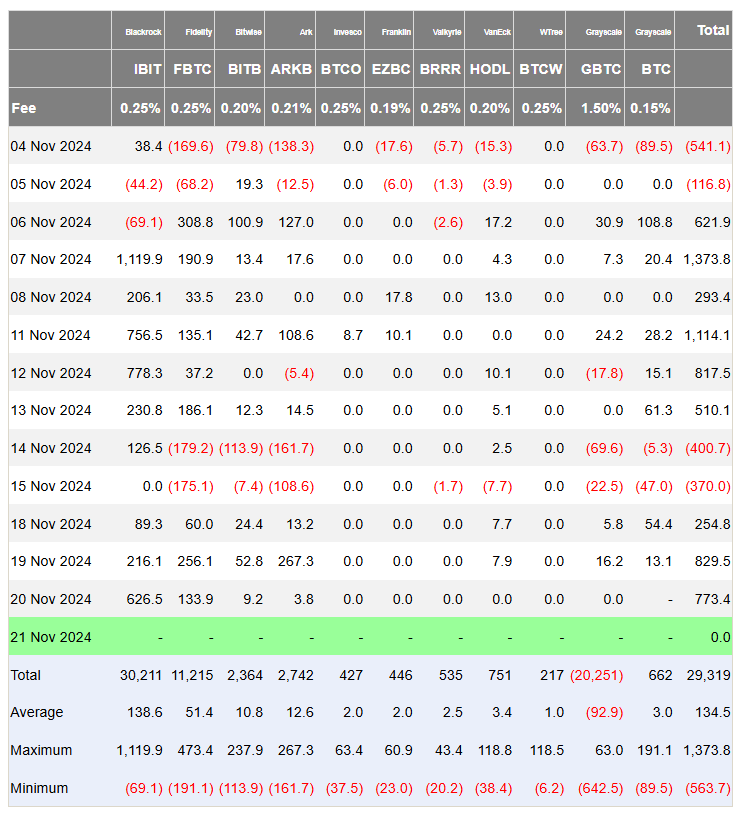

ETF Flows Surge Approaches $2 Billion in Three Days

ETF flows have only increased over the past few days with a total nearing $2 billion over the period 18-20 November. Since November 1, Bitcoin ETFs have only experienced 5 days of outflows with 9 days of inflows.

The rise in ETF adoption is likely to continue now given the hype around the Trump Presidency and his perceived pro crypto stance. If the ETF flows continue to grow it is likely that we have not seen the last of the current Bitcoin rally.

Source: Coinglass

Technical Analysis BTC/USD

Bitcoin (BTC/USD) is on a tear this week in particular, having traded just below $90k handle on Monday.

Since then, we have had 3 consecutive days of gains boosted by a combination of factors. The difficult part about the technical outlook is that there is no historical price action to base any analysis off.

As we discussed earlier in the article, there is the risk of swings due to the surge in the derivatives market. Looking at the RSI, it has been in overbought territory since Bitcoin has breached $75k. Another sign that despite the RSI being in overbought territory there is no guarantee that a pullback will materialize.

For now, immediate support is at 95000 with a break lower eyeing a move toward 91804 and then the 90000 psychological level.

Looking at a move to the upside and the 100000 mark could lead to some wild price swings as market participants may eye some profit taking as well. Beyond this at the moment, I will be keeping an eye on the round numbers/psychological numbers around 105000 and 110000.

Bitcoin (BTC/USD) Daily Chart, November 21, 2024

Source: TradingView.com (click to enlarge)

Support

- 95000

- 91804

- 90000

Resistance

- 100000

- 105000

- 105000

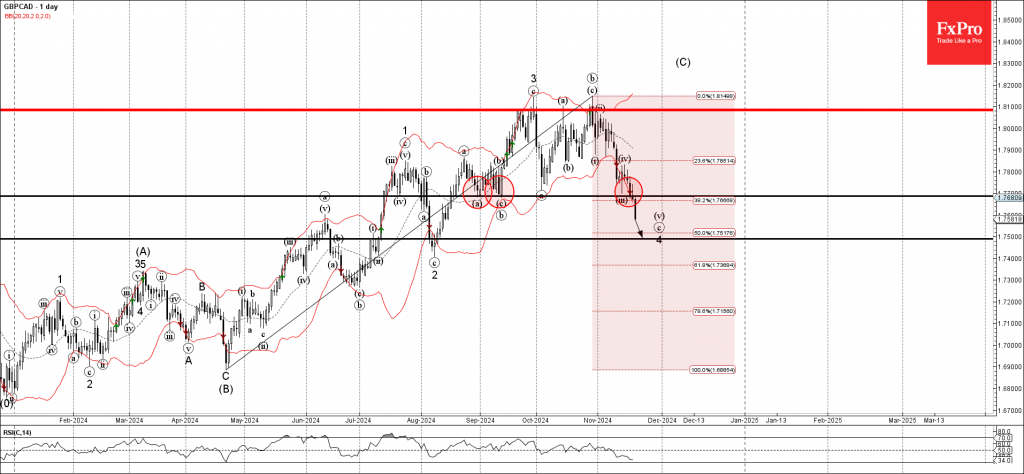

GBPCAD Wave Analysis

- GBPCAD broke support zone

- Likely to fall to support level 1.7500

GBPCAD currency pair today broke the support zone between the support level 1.7700 (which reversed the price in August and September) and the 38.2% Fibonacci correction of the upward price move from April.

The breakout of this support zone accelerated the active minor impulse wave C of the ABC correction 4 from May.

GBPCAD currency pair can be expected to fall further to the next support level 1.7500, target price for the completion of the active wave 4.

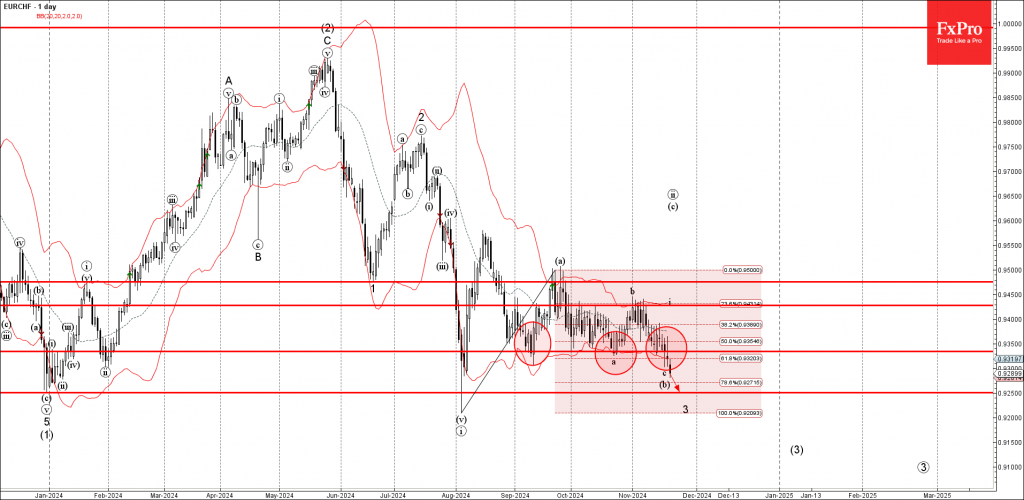

EURCHF Wave Analysis

- EURCHF under bearish pressure

- Likely to fall to support level 0.9250

EURCHF under the bearish pressure after breaking the support zone between the support level 0.9335 (which has been reversing the price from September) and the 61.8% Fibonacci correction of the upward price move from August.

The breakout of this support zone accelerated the active minor impulse wave iii of the higher order impulse wave (3) from May.

EURCHF can be expected to fall further to the next support level 0.9250, former strong support from January and August.

Sunset Market Commentary

Markets

With few data in Europe or the US, markets continued to be haunted by headlines on the war in Ukraine, even as the impact wasn’t unequivocal across markets. Ukraine reporting that Russia used an Intercontinental Ballistic missile for the first time only added to fears on a further escalation. European equites and yields nosedived. In this risk-off, the dollar gained against the euro, but declined further against the yen. Still, equities staged a (wobbling) comeback. The EuroStoxx 50 currently trades little changed. US stocks opened similarly. On interest rate markets, European yields failed to build on recent tentative bottoming. German yields currently decline 4.0/5.0 bps across the curve, with the very long end underperforming(-3.0 bp). Still recent lows survive. US Treasuries underperform. Weekly jobless claims declined further (213k) but was counterbalanced by a disappointing Philly Fed business outlook (-5.5 from 10.3 vs 8.3 expected). US yields currently decline about 2-3 bps. Money markets still see an almost even chance between a 25 bps Fed rate cut (55%) or a pauze at the December meeting. Next reality check comes with the November PMI’s, scheduled tomorrow. Oil gradually leaves recent lows behind with Brent back at $ 74 p/b.

On FX markets, the dollar looked like preparing an attack on recent highs (Ukraine) but momentum faded soon. DXY even trades marginally lower at 106.6. The euro is more vulnerable. At 1.0525, recent low at 1.0497 remains within striking distance. CEE currencies also stay in the defensive. The damage for the Czech koruna remains modest (EUR/CZK 25.33 from 25.28). The zloty trades at EUR/PLN 4.345 with multiple resistance just below/near EUR/PLN 4.40. The forint also trades off intraday lows, but struggles to sustainably return below EUR/HUF 410.

News & Views

Statistics Norway reported that mainland growth economy (excluding the offshore energy industry) accelerated to 0.5% Q/Q inn Q3 from 0.3% Q/Q in Q2. Total activity including the petroleum activities and ocean transport declined 1.8% in Q3, due maintenance operations. Value added in manufacturing and mining increased 2.3% with oil refining, chemical and pharmaceutical manufacturing contributing the most. Manufacturing has increased several quarters in a row, an accelerated further in Q3. Fishing and agriculture also increased 14% . Valued added in construction stays on a negative trajectory. Regarding final expenditure, financial consumption expenditure was almost unchanged from Q2, but Statistics Norway warns this was a complex story. Car purchases decreased, after an uptick in Q2, but service consumption and Norwegians’ consumption abroad increased. After a quick rise after the pandemic, employment growth slowed but the number of employed was still 0.2% higher compared to Q3 2023. Today’s data justify recent guidance from m the Norges Bank (NB) that a restrictive monetary policy is still needed at 4.5% this year. It only sees room for gradual easing in Q1 2025. Markets see that happen in March rather than in February. The krone extends its recent rebound currently testing first important near EUR/NOK 11.60..

The Central Bank of the Republic of Turkey (CBRT) as expected left its policy rate unchanged at 50.0%. Inflation in the country has eased over recent months (headline 48.58%, Core 47.75%). That path probably still develops slower than the CBRT hoped for as it recently raised its end of year inflation forecast to 44% (from 38%) and to 21 % eoy 2025. Still, the CBRT today sees progress as Q3 Indicators suggest domestic demand continues to slow down, reaching disinflationary levels. Core goods inflation remains low and signs for an improvement in services inflation are assessed to have become more apparent. Inflation expectations and pricing behavior tend to improve, but CBRT admits they pose risks to the disinflation process. Looking forward, CBRT assesses that a tight monetary stance will bring down the trend of monthly inflation through moderation in domestic demand, real appreciation in Turkish lira, and improvement in inflation expectations. Increased coordination of fiscal policy will also contribute to this process. CBRT concludes that a tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the forecast range. CBRT holds its final meeting of the year on December 26. Analysts remain divided whether a first limited cut will already be possible in December or whether the CBRT will (have to) wait until next year. The lira recently held near record low levels against the dollar (currently USD/TRY 34.48), but regained modest ground against the euro (EUR/TRY 36. 36).

EUR/AUD Mid-Day Outlook

Daily Pivots: (S1) 1.6190; (P) 1.6214; (R1) 1.6230; More...

EUR/AUD's fall from 1.6598 resumed by breaking through 1.6161, and intraday bias is back on the downside. Deeper decline should be seen to 1.5996/6002 key support zone. Decisive break there will carry larger bearish implications. For now, risk will stay on the downside as long as 1.6359 resistance holds, in case of recovery.

In the bigger picture, as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume through 1.7180 at a later stage. However decisive break of 1.5996 will argue that the medium term trend might have reversed. Deeper fall would be seen to 61.8% retracement of 1.4281 (2022 low) to 1.7180 at 1.5388, even as a correction.