Sample Category Title

Euro Area PMIs Set Stage for ECB

In focus today

Today, in the euro area we receive November PMIs, an important factor for the ECB decision in December. The growth momentum has recently decreased, particularly driven by a slowdown in Germany. We expect manufacturing sector to remain well in contractionary territory, with the PMI expected to rise marginally to 46.4 in November (prior: 46.0), aligning closely with hard data due to the PMI index's construction. Meanwhile, the service PMI is likely to remain above 50, indicating growth, but we expect a slight decrease to 51.2 (prior: 51.6), influenced by a modest contraction in expansion and seasonal effects.

We also receive country-specific November PMIs for France, Germany, the US, and the UK.

We have plenty of ECB speeches today including Lagarde and Schnabel.

Economic and market news

What happened overnight

In Japan, October core CPI was reported at 2.3% (cons: 2.2%, prior: 2.4%), holding above the BOJ's 2% target. Additionally, Japanese manufacturing PMI decreased to 49.0 in November (prior: 49.2), indicating a contraction for the fifth month in a row. The figures will be among factors the BOJ will discuss at its next policy meeting in December

What happened yesterday

In the euro area, consumer confidence declined to -13.7 in November (cons: -12.4, prior: -12.5). The decline comes after a long upward trend during the past two years. Taken at face value the decline increases downside risks to the growth outlook. However, the series does fluctuate a bit from month to month and we have seen similar declines in single months in past two years that are then reverted in the following month. As private consumption is expected to be the main growth driver in the coming year it is important to follow consumer confidence going forward to see whether this month's decline was just one blip or a more serious change to the previous upward trend.

In the US, jobless claims reached a six-month low at 213k (cons: 220k), indicating a relatively resilient labour market. However, we got a slightly weaker Philly Fed index registering at -5.5 for November (cons: 8.0, prior: 10.3). This figure remains within typical range observed over the past few years, albeit somewhat below average pre-covid levels. Neither of these data releases is expected to have a significant impact on the markets.

Yesterday, one of the Federal Reserve officials Golsbee said that he could see policy rates moving "a fair bit lower", but that the Federal Reserve would still need to determine the level for the neutral rate, but it was a "long way from where we are right now". This morning, we have seen US Treasury yields decline modestly in Asian trading.

In Norway, mainland GDP grew by 0.5% q/q (cons: 0.3%, prior: 0.1%). This robust growth in Q3 was largely driven by the petroleum related-, chemical- and pharmaceutical industries, which performed much better than anticipated. From the expenditure perspective, it is evident that oil investments and public sector spending were the primary catalysts for growth, with public investments and consumption alone contributing a full percentage point to Q3 growth.

Equities: Global equities were higher yesterday, with Europe registering a slight outperformance in a global context after a roller-coaster day. The situation in Europe is particularly intriguing at present. While most investors would agree that European equities are considerably cheaper compared to those in the US, just as many would probably concur that the European outlook is much cloudier, with uncertainty leading to a pattern of one step forward and two steps back. A potential game changer for Europe, both in relative and absolute terms, could be a pickup in manufacturing activity. Therefore, today's flash PMI figures are, in our opinion, the most important data point of the month for Europe.

It is worth noting that yesterday saw relatively broad-based gains, with the utilities sector outperforming along with small caps on the style side. Consequently, we are increasingly observing markets returning to being macro-driven, with the influence of Trump's trade policies gradually diminishing.

In the US yesterday, the Dow closed up by 1.1%, the S&P 500 by 0.7%, Nasdaq by 0.1%, and Russell 2000 by 1.9%.

This morning, we have Asia excluding China trading higher, with European futures also on the rise, while US futures were slightly lower.

FI: There was a modest decline in European government bond yields yesterday, while US Treasury yields rose modestly. This morning, we have seen a modest decline in US Treasury interest rates in Asian trading. One of the Fed members Golsbee stated that he could see rates "a fair bit lower" over the next year and that the neutral rate was a lower than the current level.

FX: The JPY and the USD gained yesterday and in particular vis-à-vis the EUR and the GBP. Notable mentions from yesterday, was the drop in EUR/USD below 1.05 and the rally in NOK/SEK back to parity.

UK retail sales drop sharply by -0.7% mom in Oct, but broader trends show resilience

UK retail sales volumes plunged by -0.7% mom in October, significantly underperforming expectations of a -0.3% mom decline. Also, volumes remained -1.5% below their pre-pandemic level in February 2020.

On a broader basis, retail activity was more encouraging. Sales volumes increased by 0.8% in the three months to October compared to the preceding three months. When measured against the same period last year, sales volumes grew by 2.5%. This represents the strongest annualized growth since March 2022, despite a downward revision of September's annual figure from 2.6% to 2.1%.

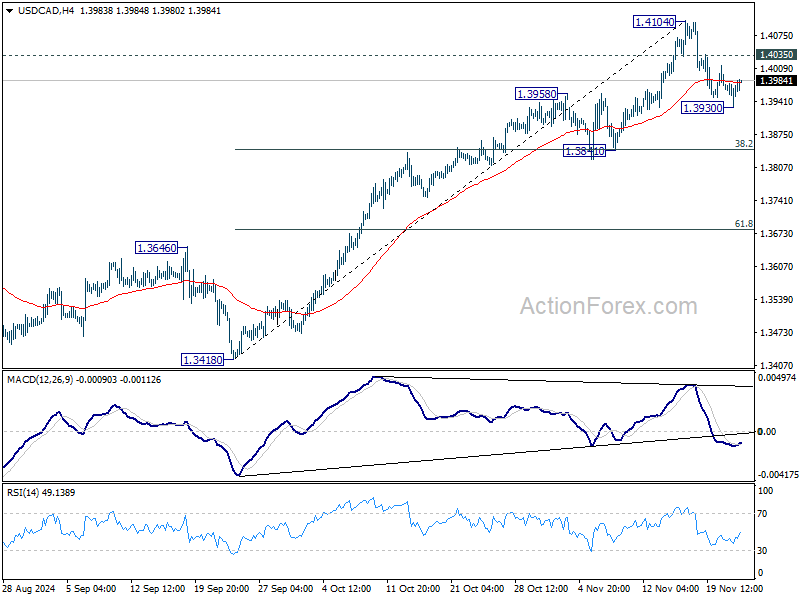

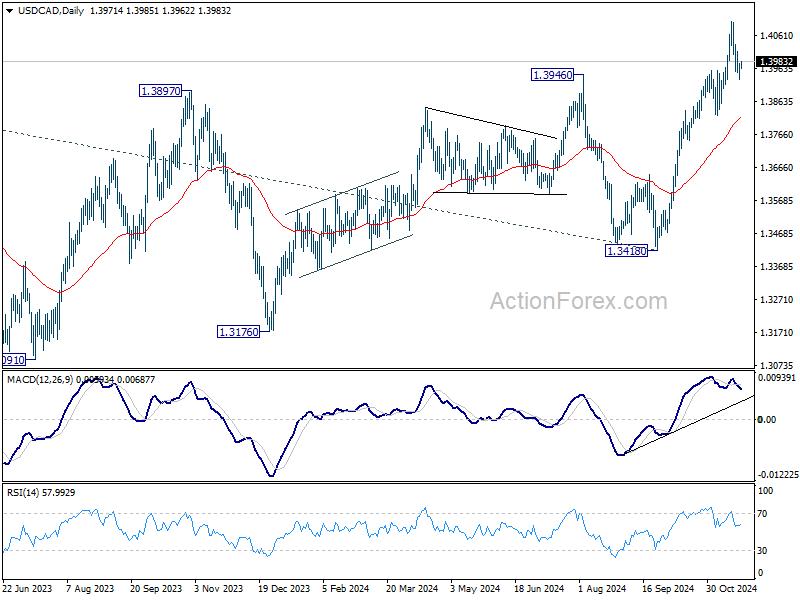

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3944; (P) 1.3963; (R1) 1.3994; More...

USD/CAD recovered after brief dip to 1.3930 and intraday bias stays neutral first. On the downside, break of 1.3930 will extend the corrective fall from 1.4104 to 1.3841 cluster support (38.2% retracement of 1.3418 to 1.4104 at 1.3842). Nevertheless, above 1.4035 minor resistance will bring retest of 1.4104 high.

In the bigger picture, up trend from 1.2005 (2021) is resuming with break of 1.3976 key resistance (2022 high). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391. Now, medium term outlook will remain bullish as long as 1.3418 support holds, even in case of deep pullback.

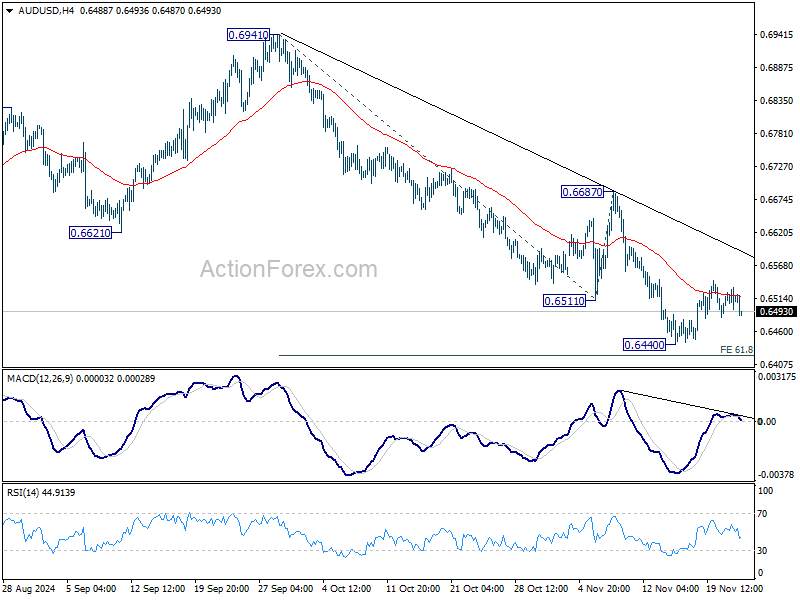

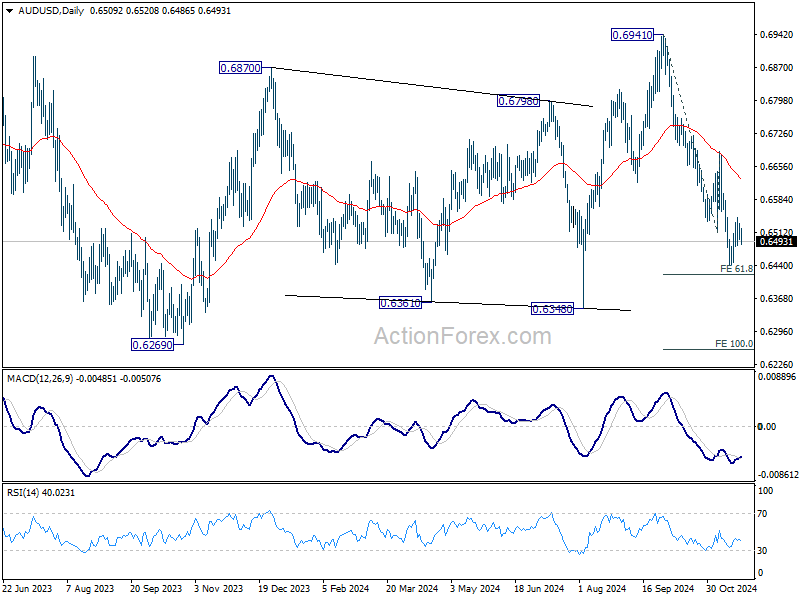

AUD/USD Daily Report

Daily Pivots: (S1) 0.6494; (P) 0.6514; (R1) 0.6530; More...

AUD/USD is staying in consolidation from 0.6440 and intraday bias remains neutral. Outlook will stay bearish as long as 0.6687 resistance holds. On the downside, decisive break of 61.8% projection of 0.6941 to 0.6511 from 0.6687 at 0.6421 will resume the fall from 0.6941 to 100% projection at 0.6257 next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

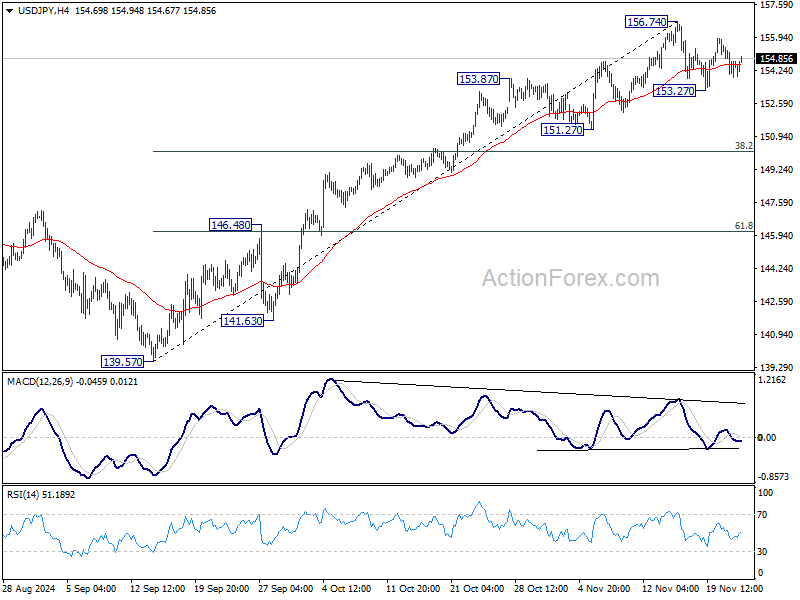

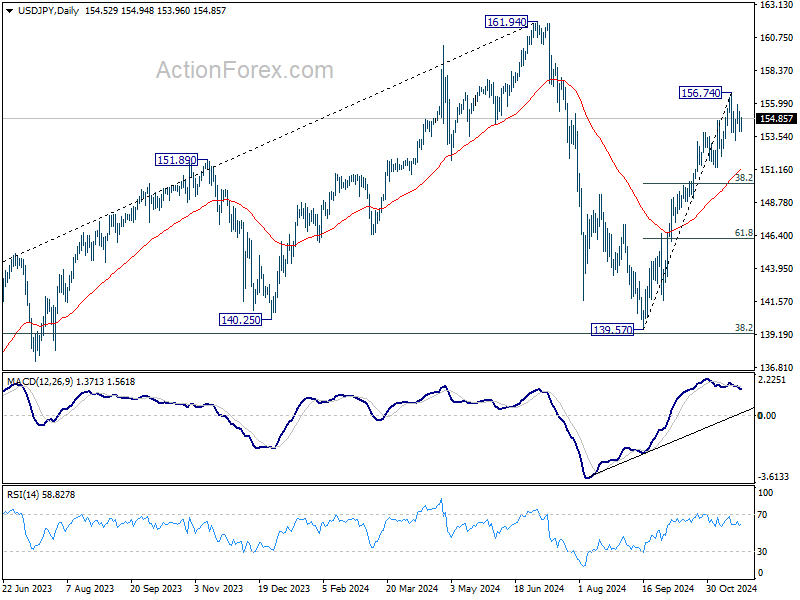

USD/JPY Daily Outlook

Daily Pivots: (S1) 153.82; (P) 154.64; (R1) 155.36; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the upside, break of 156.74 will resume the whole rally from 139.57 towards 161.94 high. On the downside, though, break of 153.27 will resume the correction towards 38.2% retracement of 139.57 to 156.74 at 150.18.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

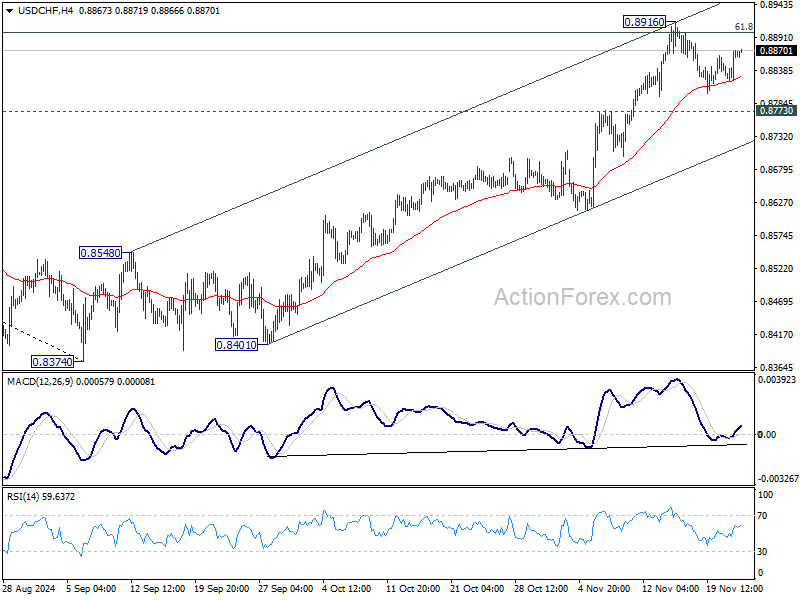

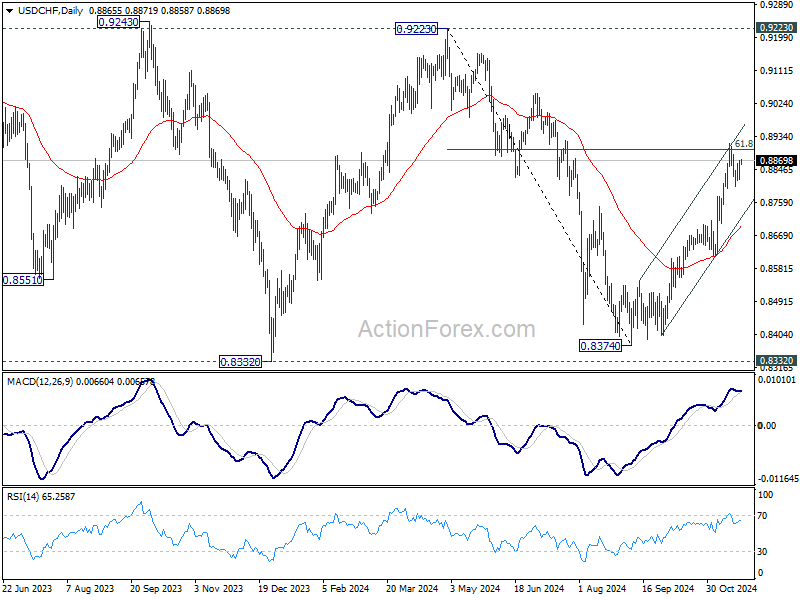

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8835; (P) 0.8854; (R1) 0.8886; More…

Intraday bias in USD/CHF remains neutral as consolidation from 0.8916 is still extending. Further rally is expected as long as 0.8773 resistance turned support holds. On the upside, break of 0.8916 and sustained trading above 61.8% retracement of 0.9223 to 0.8374 at 0.8899 will pave the way back to 0.9223 key resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern. Rise from 0.8374 is seen as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

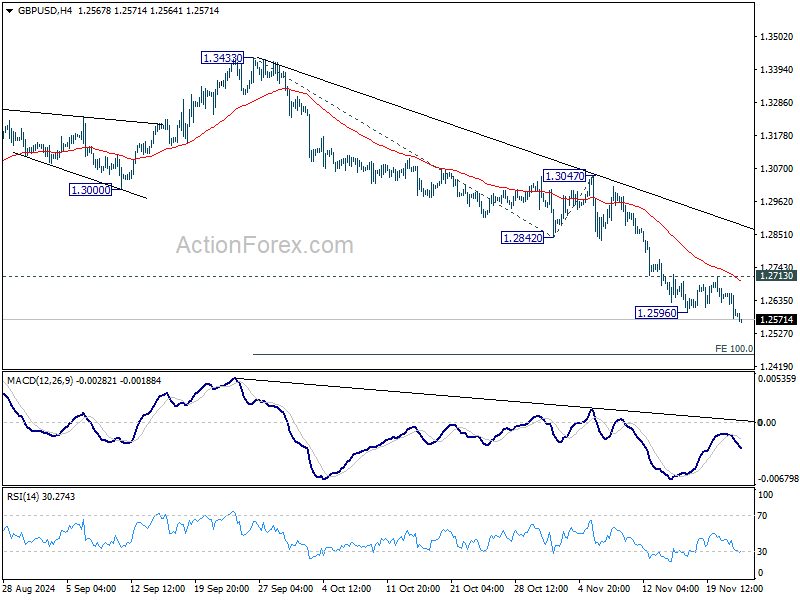

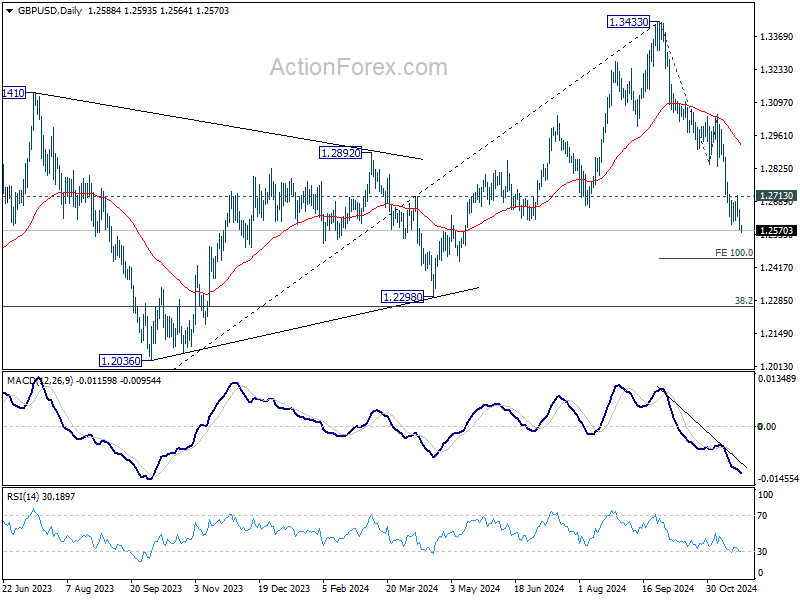

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2557; (P) 1.2609; (R1) 1.2641; More...

GBP/USD's fall from 1.3433 resumed by breaking through 1.2596 and intraday bias is back on the downside. Deeper fall should be seen to 100% projection of 1.3433 to 1.2842 to 1.3047 at 1.2456. For now, risk will stay on the downside as long as 1.2713 resistance holds, in case of recovery.

In the bigger picture, a medium term top should be in place at 1.3433, and price actions from there are correcting whole up trend from 1.0351 (2022 low). Deeper decline is now expected as long as 55 D EMA (now at 1.2977) holds, to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

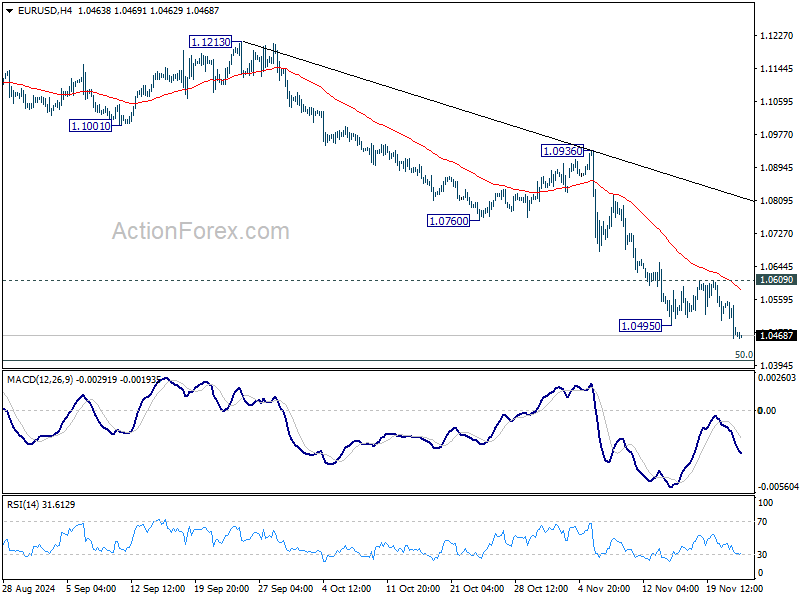

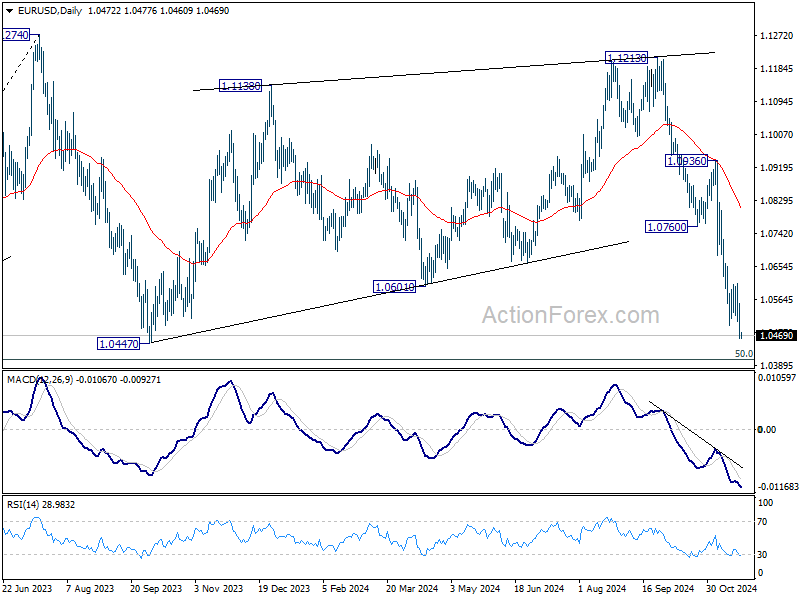

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0439; (P) 1.0497; (R1) 1.0532; More...

EUR/USD's fall from 1.1213 resumed by breaking through 1.0495 temporary low. Intraday bias is back on the downside for 1.0447 support and then 1.0404 key fibonacci level next. Strong support could be seen from this zone to bring rebound. But risk will stay on the downside as long as 1.0609 resistance holds. Decisive break of 1.0404 will carry larger bearish implications.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

Swiss Franc and Dollar Gain as Putin Warns of Global War Escalation, Euro Awaits PMIs

Swiss Franc and US Dollar appreciated broadly today as investors sought safe-haven assets in response to escalating geopolitical risks. Gold extended its near-term rebound, while Bitcoin surged to a new record high, reflecting heightened demand for alternative stores of value.

The catalyst for this shift was a warning from Russian President Vladimir Putin that the conflict in Ukraine is escalating toward a global scale. Putin stated that Russia responded to Ukraine's use of US and British-supplied missiles by launching a new hypersonic medium-range ballistic missile at a Ukrainian military facility. He indicated that additional actions could follow, intensifying concerns about a broader confrontation involving major powers.

Despite these developments, the risk-off sentiment was not uniformly reflected across global markets. DOW closed significantly higher overnight, while NASDAQ edged lower. In Asia, market performance was mixed; Japan's Nikkei 225 advanced whereas Hong Kong's HSI and China's SSE trade in red.

Australian Dollar pulled back slightly but remains one of the week's strongest performers, despite mixed PMI data. Meanwhile, Yen continued to trade within familiar ranges, showing limited reaction to both the geopolitical developments and stronger-than-expected Japanese CPI data.

Attention is now turning to the Eurozone's PMI data scheduled for release today. This data will be particularly significant after Euro's broad-based decline yesterday, breaking key support levels against several major currencies.

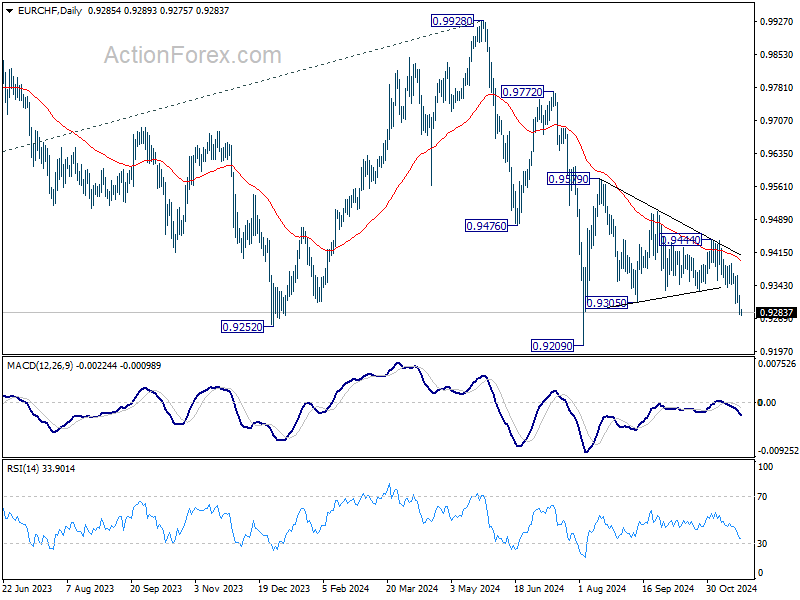

Technically, EUR/CHF's near term decline resumed and breaks through 0.9305 support. Attention is now on whether it picks up downside momentum for breaking through 0.9209 low decisively.

In Asia, at the time of writing, Nikkei is up 0.76%. Hong Kong HSI is down -1.70%. China Shanghai SSE is down -1.58%. Singapore Strait Times is up 0.07%. Japan 10-year JGB yield is down -0.0101 at 1.086. Overnight, DOW rose 1.06%. S&P 500 rose 0.53%. NASDAQ rose 0.03%. 10-year yield rose 0.026 to 4.432.

Japan's CPI eases to 2.3% in Oct, core-core rises to 2.3%

Japan’s inflation data for October revealed persistent and broadening price pressures. Core CPI (excluding food) eased slightly to 2.3% yoy, down from 2.4% yoy but exceeding expectations of 2.2% yoy. This marked the 31st consecutive month core CPI has stayed at or above BoJ's 2% target.

Core-core CPI (excluding food and energy) rose from 2.1% yoy to 2.3% yoy, underscoring renewed strength in underlying inflation. Headline CPI moderated from 2.5% to 2.3%, partly due to slowing energy price gains, which decelerated sharply to 2.3% yoy from 6.0% yoy in September. However, food prices surged 3.8% yoy, accelerating from 3.1% yoy, while services prices edged up to 1.5% yoy from 1.3% yoy.

The combination of steady inflation momentum, recovering consumer spending, and Ten's renewed weakening bolsters the argument for a BoJ rate hike at its upcoming policy meeting in December.

Japan's PMI manufacturing falls to 49.0, services rises to 50.2

Japan’s PMI Manufacturing index edged down to 49.0 from 49.2 in November, signaling a deepened contraction in the sector. In contrast, PMI Services rose slightly to 50.2 from 49.7, indicating a renewed, albeit modest, expansion. PMI Composite improved marginally but remained below the neutral mark at 49.8, up from 49.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, noted that demand conditions were "stagnant," while employment grew at the fastest rate in four months. Price pressures persisted across sectors, driven by rising raw material costs and Yen’s weakness. Firms responded with sharper increases in prices charged for goods and services, aiming to pass on these higher cost burdens to customers.

Australia's PMI composite falls to 49.4, second contraction in three months

Australia’s PMI Manufacturing improved sharply from 47.3 to 49.3 in November, marking a six-month high but remaining in contraction territory. Conversely, PMI Services index dropped from 51.0 to 49.6, hitting a 10-month low and signaling contraction. PMI Composite fell from 50.2 to 49.4, its lowest level in 10 months, indicating a slight overall contraction in private sector output for the second time in three months.

Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, highlighted the significance of the services sector’s slowdown. “The November S&P Global Flash Australia PMI posted the lowest reading since January, bringing the fourth-quarter average thus far below that of the prior quarter,” Pan said.

The report also noted that easing capacity pressures and subdued activity contributed to slower employment growth, which fell further below the long-term average. In addition, selling price inflation eased as businesses showed caution in raising charges. This combination of softer employment growth and reduced price pressures supports expectations of lower interest rates.

Looking ahead

UK will release retail sales and PMI flash in European session. Germany will release GDP final. Eurozone will also release PMI flash. Later in the day, Canada will release retail sales. US will also release PMI flash.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0439; (P) 1.0497; (R1) 1.0532; More...

EUR/USD's fall from 1.1213 resumed by breaking through 1.0495 temporary low. Intraday bias is back on the downside for 1.0447 support and then 1.0404 key fibonacci level next. Strong support could be seen from this zone to bring rebound. But risk will stay on the downside as long as 1.0609 resistance holds. Decisive break of 1.0404 will carry larger bearish implications.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage. However, firm break of 1.0404 will raise the chance of reversal and target 61.8% retracement at 1.0199.

Japan’s CPI eases to 2.3% in Oct, core-core rises to 2.3%

Japan’s inflation data for October revealed persistent and broadening price pressures. Core CPI (excluding food) eased slightly to 2.3% yoy, down from 2.4% yoy but exceeding expectations of 2.2% yoy. This marked the 31st consecutive month core CPI has stayed at or above BoJ's 2% target.

Core-core CPI (excluding food and energy) rose from 2.1% yoy to 2.3% yoy, underscoring renewed strength in underlying inflation. Headline CPI moderated from 2.5% to 2.3%, partly due to slowing energy price gains, which decelerated sharply to 2.3% yoy from 6.0% yoy in September. However, food prices surged 3.8% yoy, accelerating from 3.1% yoy, while services prices edged up to 1.5% yoy from 1.3% yoy.

The combination of steady inflation momentum, recovering consumer spending, and Ten's renewed weakening bolsters the argument for a BoJ rate hike at its upcoming policy meeting in December.