Sample Category Title

EUR/GBP Surges as Markets Price “Zombie Government” Risk as Starmer Crisis Deepens

Sterling plunged sharply today while UK bond yields surged above 5.1% after the first ministerial resignation calling for Prime Minister Keir Starmer to step down transformed simmering political anxiety into something much more dangerous for markets: the perception that Britain may now be drifting toward a “zombie government.”

The trigger came shortly after 9:15 a.m. London time when junior minister Miatta Fahnbulleh announced her resignation and publicly urged Starmer to “do the right thing for the country and the Party and set a timetable for an orderly transition.” Markets had already been increasingly nervous following Labour’s disastrous local election results last week. But Fahnbulleh’s resignation suddenly made the leadership crisis feel real rather than theoretical.

The political arithmetic has also deteriorated rapidly. Reports now indicate that more than 80 Labour MPs — roughly one-fifth to one-quarter of the Parliamentary Labour Party — have either privately or publicly demanded that Starmer resign immediately or commit to a timetable for departure by September. The situation intensified after Catherine West revealed she had received overwhelming encouragement for a potential leadership transition.

For traders, 80 MPs is not just another headline number. It represents a psychological tipping point. Under Labour Party norms, a prime minister whose authority is widely seen as “fatally wounded” often struggles to regain control once coordinated resignation pressure begins building internally.

Markets are now increasingly pricing a full leadership contest as effectively inevitable.

The problem for investors is not simply who replaces Starmer. The deeper fear is that Britain may temporarily end up with a government too politically weakened to respond coherently to mounting economic challenges. Rising oil prices linked to the Iran conflict, elevated borrowing costs, and growing fiscal pressures are all hitting simultaneously while Labour increasingly appears consumed by internal survival battles.

That concern was visible immediately in markets. Sterling sold off aggressively while the 10-year gilt yield surged back above 5.1%, suggesting investors are demanding a growing political risk premium to hold UK assets. Importantly, the simultaneous fall in Sterling and rise in yields signals markets are not merely reacting to global macro conditions, but specifically reassessing confidence in Britain’s political management capacity.

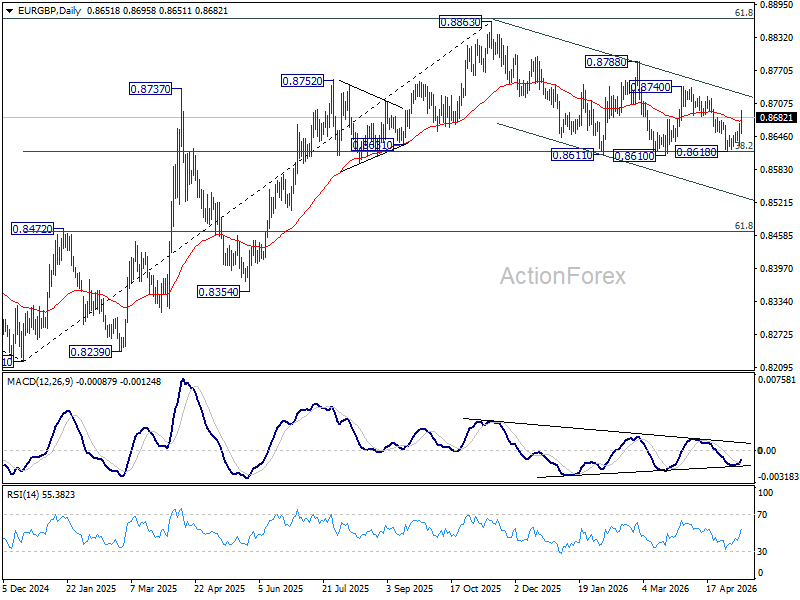

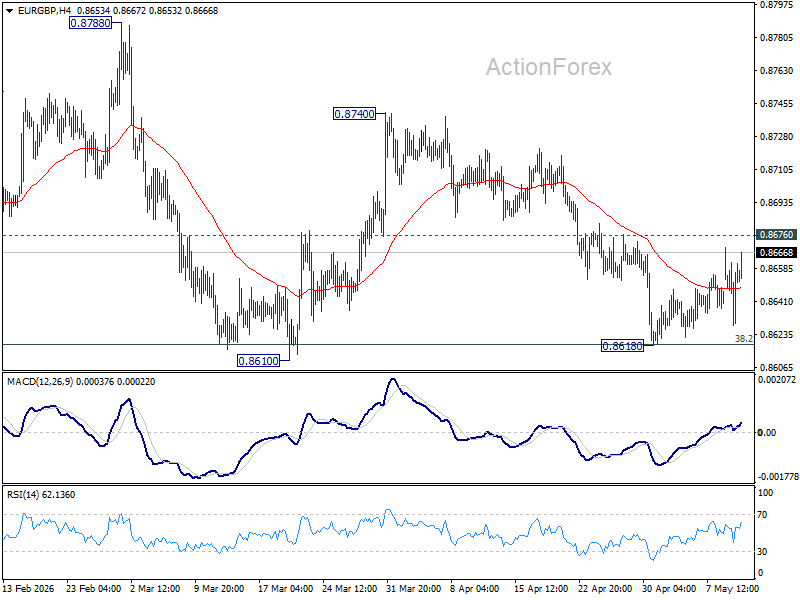

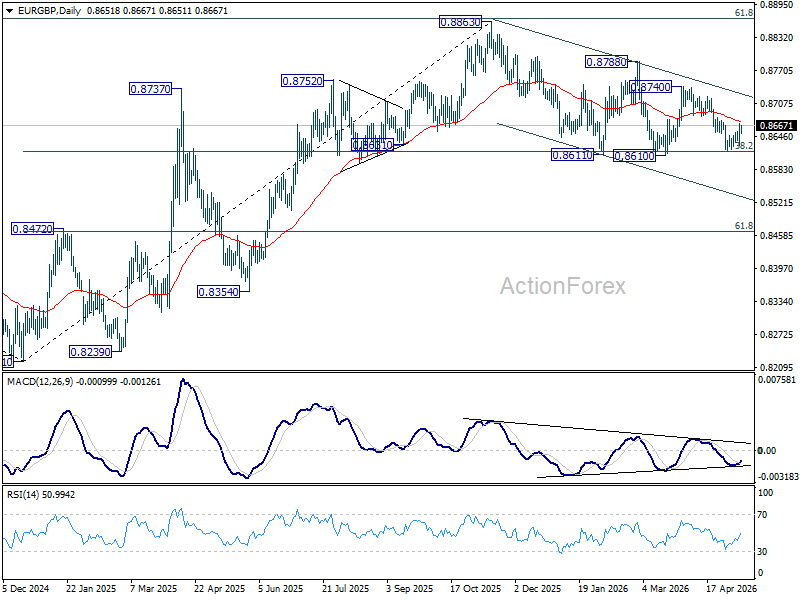

Technically, EUR/GBP’s breakout above 0.8676 confirms that fall from 0.8740 likely ended at 0.8618. Just as importantly, the repeated defense of 38.2% retracement of 0.8821 to 0.8863 at 0.8618 continues preserving the broader medium-term bullish structure in the pair.

The next upside target now sits at 0.8740 resistance. A decisive break above that level could open the way toward a retest of 0.8863, the 2025 high.

EUR/USD on Edge: Middle East and China in Focus

EUR/USD dipped slightly on Tuesday, retreating to 1.1762. The US dollar has returned to favour as a defensive asset after US President Donald Trump questioned the sustainability of the truce with Iran and rejected Tehran’s latest peace proposal.

Trump also plans to convene a meeting with his national security team to discuss a potential resumption of military operations and a review of plans to escort commercial vessels through the Strait of Hormuz.

The ongoing conflict continues to keep oil prices elevated, fuelling inflationary pressures and expectations that interest rates may remain higher for longer to contain price pressures.

Investors are now turning their attention to US inflation data for April, which is expected to indicate how the Iran conflict is impacting the economy and help guide potential Federal Reserve decisions.

An additional market factor is the expected meeting later this week between Donald Trump and Chinese President Xi Jinping, which is likely to focus on trade relations and the development of artificial intelligence.

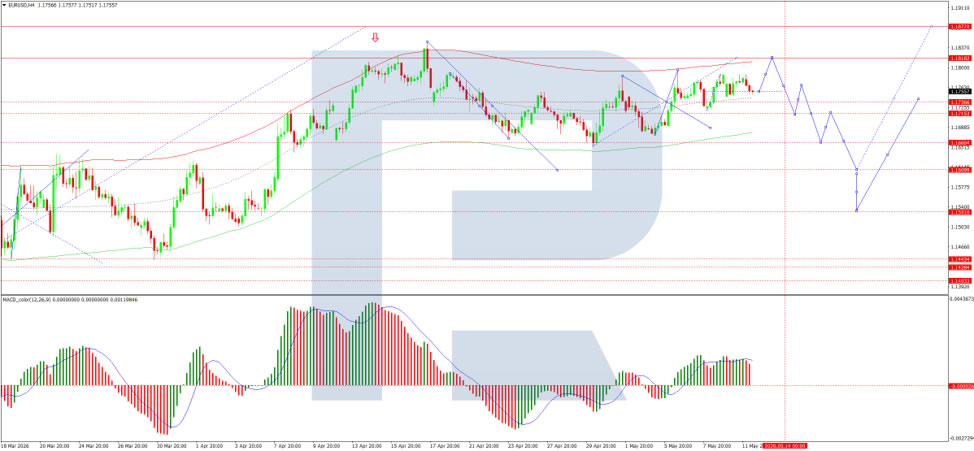

Technical Analysis

On the H4 chart, EUR/USD is trading within a consolidation range around 1.1755, with potential downside towards 1.1688. At the same time, a move higher towards 1.1818 remains possible, with further upside to 1.1870. This scenario is supported by the MACD indicator, with its signal line above zero and pointing firmly upwards, indicating continued bullish momentum.

On the H1 chart, EUR/USD has reached 1.1786. A decline towards 1.1740 is likely, followed by a possible rebound to 1.1760 and further upside towards 1.1818. This scenario is confirmed by the Stochastic oscillator, with its signal line near 20 and pointing firmly upwards.

Conclusion

EUR/USD remains sensitive to geopolitical developments in the Middle East and upcoming US–China discussions. Strong inflation data could support the US dollar, while positive diplomatic progress may ease pressure on the pair and support further euro gains.

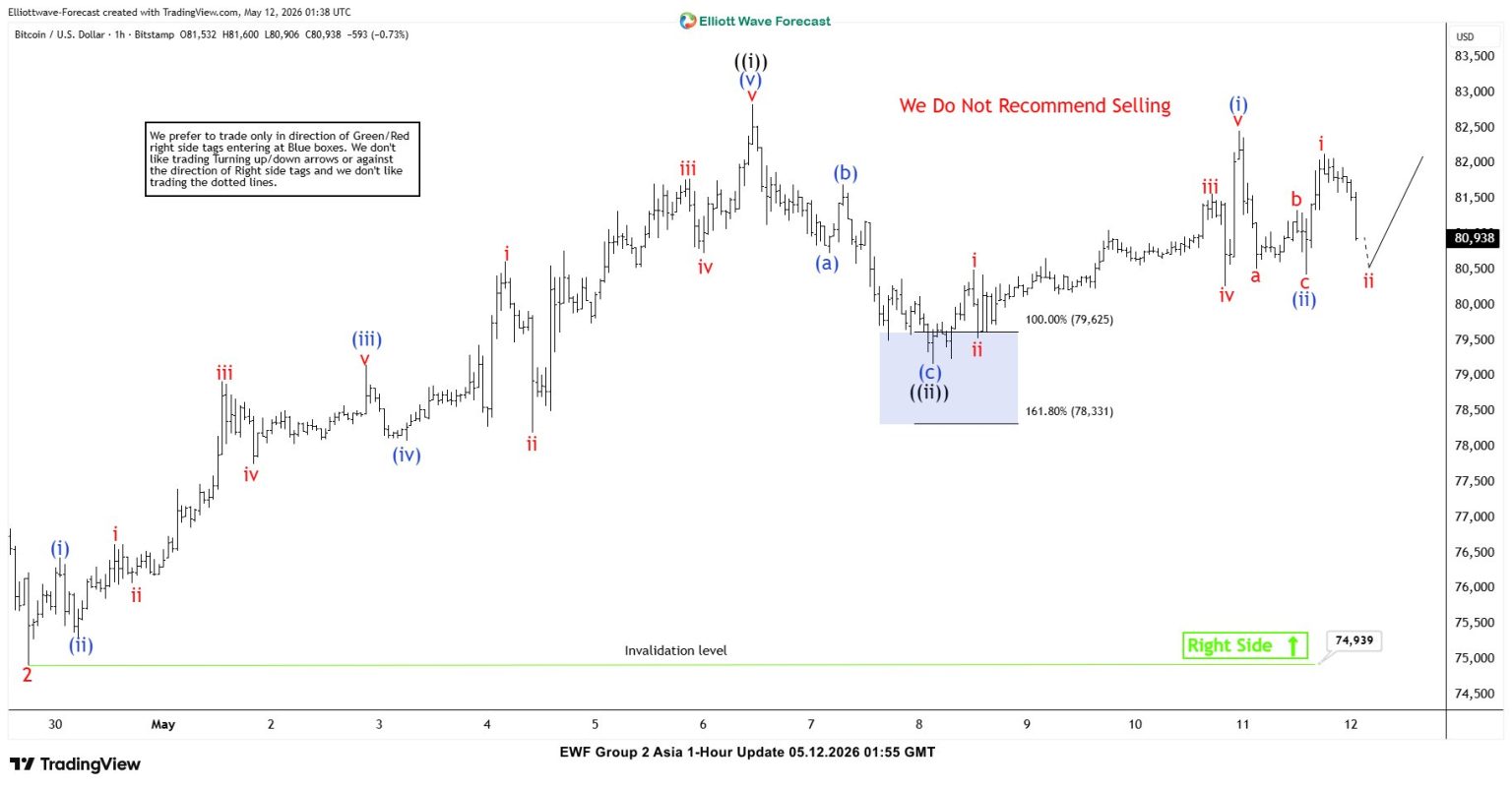

Bitcoin Smoothly Reacts Higher from Blue Box Zone

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of Botcoin ticker symbol: BTCUSD. In which, the rally from the 29 April 2026 low unfolded as an impulse structure. Showing a higher high sequence in larger time frame charts favored more upside extension to take place. Therefore, we advised members not to sell the pair & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

Bitcoin 1-Hour Elliott Wave Chart From 5.07.2026

Here’s the 1-hour Elliott wave chart from the 5.07.2026 New York update. In which, the cycle from the 4.29.2026 low ended in wave 1 at $82833 high. Down from there, the BTCUSD made a pullback in wave 2 to correct that cycle. The internals of that pullback unfolded as Elliott wave zigzag structure where wave ((a)) ended at $80728 low. Wave ((b)) bounce ended at $81706 high and wave ((c)) managed to reach the blue box area at $79625- $78331. From there, buyers were expected to appear looking for the next leg higher or for a 3 wave bounce minimum.

Bitcoin Latest 1-Hour Elliott Wave Chart From 5.12.2026

This is the latest 1-hour Elliott wave Chart from the 5.12.2026 Asia update. In which the Bitcoin is showing a reaction higher taking place, right after ending the zigzag correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. However, a break above $82833 high is needed to confirm the next leg higher towards $87072- $91961 target area.

Chart Alert: Nikkei 225 Bullish Run Is Facing Minor Exhaustion Below 64,145

Key Takeaways

- Nikkei 225 continued its strong rally to a fresh record high of 63,788, driven largely by technology-related heavyweights such as SoftBank Group and Murata Manufacturing.

- Despite the broader medium-term bullish trend remaining intact, technical indicators now suggest a near-term corrective pullback risk below the 64,145 resistance level, supported by a developing bearish “Head & Shoulders” pattern.

- Momentum conditions have weakened as hourly RSI bearish divergence and Elliott Wave/Fibonacci analysis point to exhaustion in the recent five-wave bullish impulsive sequence, increasing the probability of a short-term retracement toward 61,945 and lower support zones.

The price actions of the Japan 225 CFD index, a proxy of the Nikkei 225 index futures, have rallied as expected in the past four weeks and surpassed 62,044, as highlighted in our earlier report.

It hit a fresh intraday all-time high of 63,788 on Monday, 11 May 2026, led by technology-related component stocks in the past month, such as SoftBank Group, up 58%, and Murata Manufacturing, up 53%.

However, the price actions of financial assets do not move vertically, as there will be periods of countertrend movements or trend reversals due to changing sentiment.

Right now, the Nikkei 225 faces the risk of a minor corrective countertrend decline within a medium-term uptrend phase.

Let’s unpack in greater detail.

Nikkei 225: Minor Bearish “Head & Shoulders” Sighted

Fig. 1: Japan 225 CFD index minor trend as of 12 May 2026. Source: TradingView.

Trend bias: Minor bearish corrective decline within medium-term uptrend below 64,145 key short-term pivotal resistance.

Supports: 61,945, neckline of “Head & Shoulders”, 61,180/60,795, and 59,970, also the 20-day moving average.

Next resistances: 65,010/65,040 and 66,190/66,568, Fibonacci extension and upper boundary of the medium-term ascending channel from the 30 March 2026 low.

Key Elements to Support the Near-Term Bearish Bias on the Nikkei 225

- Since 7 May 2026, its price action has traced out a minor bearish reversal “Head & Shoulders” configuration, indicating a potential end of its minor uptrend phase from the 30 April 2026 low.

- Based on Elliott Wave Theory and Fibonacci analysis, the price actions have completed a five-wave minor bullish impulsive up move sequence, labelled as i, ii, iii, iv and v, with a potential terminal level at 63,772, based on 0.382 Fibonacci extension from the start of the minor bullish impulsive up move from the 30 April 2026 low. The next probable move is a minor corrective decline to retrace its prior five-wave minor bullish impulsive up move.

- The hourly RSI momentum indicator has shown a bullish exhaustion condition, with bearish divergence since 7 May 2026 at its overbought region, which supports the potential incoming minor corrective decline.

GBP/USD Slides Toward Trendline Support Below 1.3600

- GBPUSD weakens within consolidation.

- Loses ground on US-Iran tensions, UK political pressure, US data in focus.

- Momentum indicators point to a modestly fading positive bias.

GBPUSD is losing ground below the 1.3600 handle, eyeing support at the medium‑term ascending trendline. The pound is under pressure against the dollar amid domestic political uncertainty, lingering Middle East tensions, and ahead of key US CPI data.

Momentum indicators are easing within positive territory, with the MACD muted near its signal line and the RSI drifting toward neutral. This suggests consolidation within the 1.3525-1.3625 range may persist, with downside risks increasing if price breaks below the uptrend line and the 20‑day simple moving average (SMA) at the lower bound of the range.

Below that, further support is seen near 1.3465, followed by the 1.3385-1.3430 zone, which encapsulates the converging 50‑ and 200‑day SMAs and may help shield price action from deeper losses toward the 23.6% Fibonacci retracement of the January-March pullback near 1.3325. A decisive break below this level would expose the multi‑month lows.

On the upside, resistance near the 61.8% Fibonacci and psychological 1.3600 level, alongside the eleven-week high at 1.3625, remains firm. A sustained break above this area could reopen targets at 1.3715 and then the multi‑year high near 1.3985.

Summing up, GBPUSD remains under pressure as it attempts to stabilise around the previously broken uptrend line. Momentum though remains broadly constructive, suggesting that holding this support could still underpin upside attempts in the near term.

Sunrise Market Commentary

Markets

The UK prime minister Keir Starmer is hanging by a thread. A colossal defeat at the regional and local elections last week increasingly looks to be the straw that will break the camel’s back. It is the latest of the multiple hits Starmer took when being in office, ranging from the Mandelson case over policy missteps and dramatic U-turns and near-constant infighting. A speech yesterday by Starmer, in which he also insisted not to leave, failed to persuade many Labour members of his ability to change the party’s fortunes. A formal leadership challenge is triggered when 81 Labour lawmakers (20% of the total) rally behind a single candidate. But fearing for a chaotic process, many MPs prefer Starmer to either quit himself or set out plans for departing. More than 70 of the 403 MPs, among which several senior ministers, have already called on him to do so. According to the Financial Times citing people close, he was weighing things ahead of a crucial cabinet meeting later today. Starmer’s looming exit causes market concern over the UK’s fiscal future when a potential new PM takes over. Gilts underperformed greatly vs global peers yesterday with the 30-yr yield rallying more than 9 bps. Monday’s close at 5.67% is to be compared with the 5.74% multidecade high seen exactly one week ago. Yields rose earlier on the curve too to the tune of 8-8.5 bps, supported by rising oil prices after president Trump dismissed the Iranian counterproposal as “a piece of garbage”. He later called the ceasefire as being on massive life support. Brent finished at $104 and is nearing $105 per barrel this morning. European rates joined the broader move higher with net daily changes varying between 2.7 and 5.5 bps (swap) in a bear flattener. US yields added 5.2-7 bps in a similar curve shift. While most focus is going to its currency lately, Japanese bonds are gradually eroding to their weakest levels in many decades. The 30-yr yield for example rises to 3.8% this morning, extending a bounce higher that started with the Iran war. Closing at that level would only leave January 20 (3.87%) stand in between new record highs. The 10-yr yield (2.55%) is setting a 29-year high as we speak. The yen did show some of the biggest swings on the FX market yesterday with USD/JPY recovering to 157.2 and building on that move this morning (157.7). About half of the intervention impact is being wiped out. Most other currency pairs closed little changed, including sterling – for all of the uncertainty that’s plaguing it.

S April CPI is on tap today. Our in-house headline nowcast stands at a consensus-matching 3.7%, which would mean a quickening from March’s 3.3%. We expect core CPI at 2.6%, the same as in March. For food, after flat monthly growth in March, we cautiously assume 0.2% m/m, implying 2.9% y/y. Energy could rise another 5.4% m/m given further increases in oil and gasoline prices. That would correspond to 19.4% y/y (up from 12.6% in March). We’re particularly interested in the market reaction in an upside surprise. Combined with a labour market in a stable shape, there’s room for US yields rise and the dollar to appreciate. The 2-yr yield is closing in on the 4% barrier.

Supply today includes a $42bn 10-yr US auction and a new syndicated deal in Belgium. The Kingdom intends to issue the last of 2026’s three benchmark deals. This one will have a 5-year maturity and comes after the country raised €8bn and €6bn with the 10-yr and 30-yr deals earlier this year.

News & Views

The British Retail Consortium retail sales monitor shows uncertainty hitting sales in April. UK total retail sales decreased by 3% Y/Y (from +3.6% Y/Y) and by 3.4% Y/Y (from +3.1% Y/Y) on a like-for-like basis. The CEO at BRC said that April’s sales fall was largely driven by the Easter shift, with food hit hardest (food sales -2.5% Y/Y from +6.8% Y/Y). Non-food sales decreased by 3.3% Y/Y (from +0.9% Y/Y). Taking March and April together, and comparing them with the same two-month period in 2025 (to account for the timing of Easter), UK total retail sales increased by 1.5% Y/Y. Weak consumer confidence also played a role in April as fears about the Middle East conflict driving up living costs led shoppers to rein in. Big-ticket purchases fell, with the recent recovery in furniture losing steam, and uncertainty around summer holidays hitting discretionary spend.

South Korean presidential policy chief Kim Yong-beom triggered wild swings in local trading this morning. His suggestion to pay a dividend to South Korean citizens using taxes on AI profits sent the leading Kospi index initially more than 5% lower. He later clarified that he wanted to tap “excess tax revenue” instead of implementing a new windfall tax on corporate profits, but that offered only partial relief. The Kospi currently loses 2.75%. Just ahead of the comments, the index was within reach of the 8k mark for the first time ever.

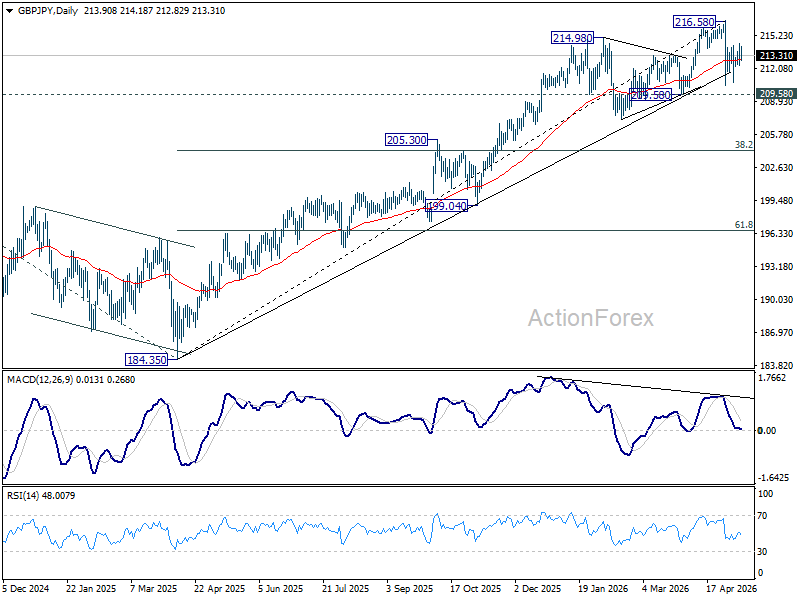

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.51; (P) 213.46; (R1) 214.81; More...

Intraday bias in GBP/JPY is mildly on the upside with breach of 214.21 resistance. Pullback from 216.58 could have completed at 210.43. Further rise would be seen towards retesting 216.58. However, break of 212.35 will turn bias back to the downside for 210.43 again.

In the bigger picture, while the fall from 216.58 is steep, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 205.75) will argue that it's already in medium term down trend for 184.35 support.

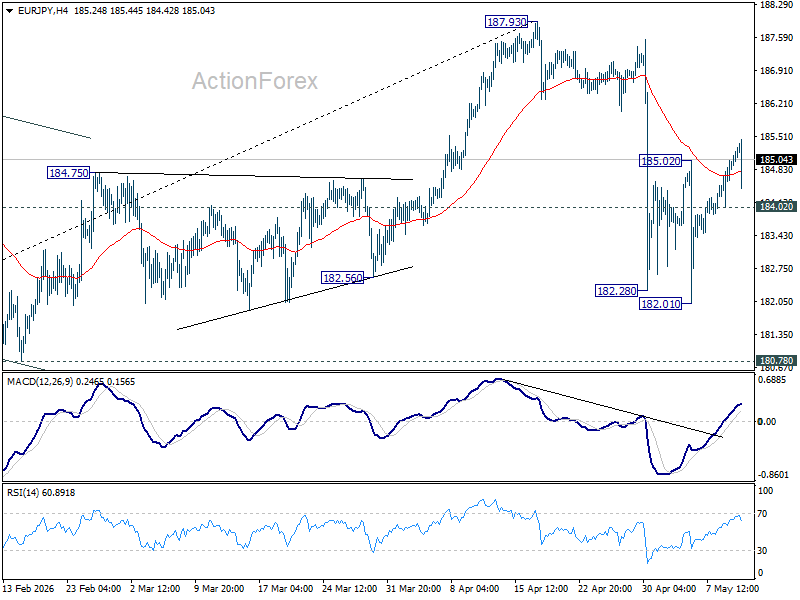

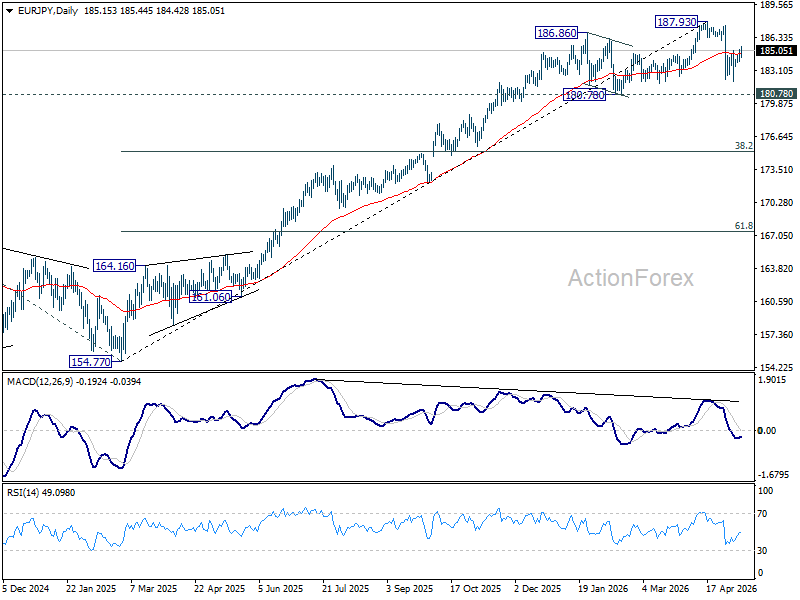

EUR/JPY Daily Outlook

Daily Pivots: (S1) 184.26; (P) 184.75; (R1) 185.65; More...

Intraday bias in EUR/JPY is mildly on the upside with break of 185.02 resistance. Pullback from 187.93 could have completed at 182.01 already. Further rise would be seen back to retest this high. Nevertheless, break of 184.02 minor support will turn bias back to the downside towards 182.01 again.

In the bigger picture, the pullback from 187.93 is steep, there is no sign of reversal yet. Uptrend from 114.42 is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 178.04) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.

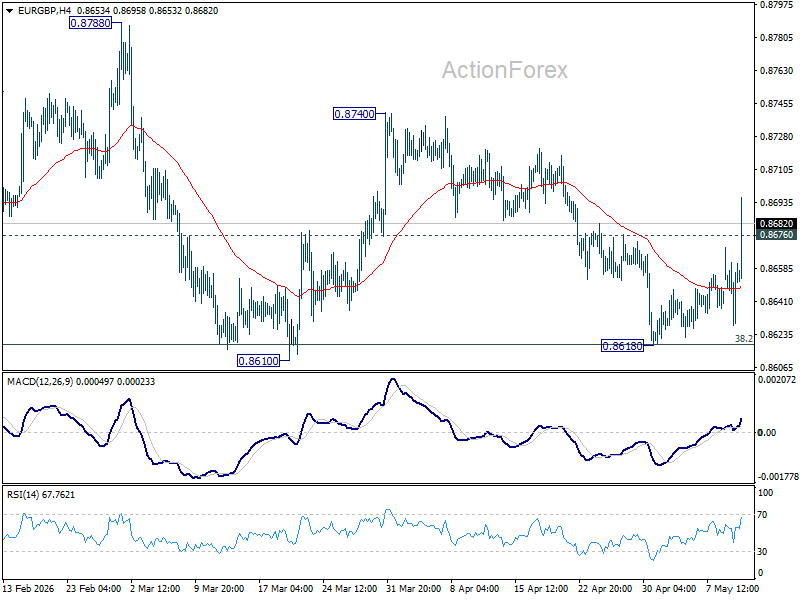

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8632; (P) 0.8651; (R1) 0.8673; More…

EUR/GBP is still bounded in established range above 0.8618 and intraday bias remains neutral. On the downside, firm break of 0.8610 will carry larger bearish implications and pave the way to 0.8466 fibonacci level next. Nevertheless, firm break of 0.8676 will turn bias back to the upside for stronger rebound back to 0.8740 resistance instead.

In the bigger picture, focus is back on 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Sustained break there will confirm that whole rise from 0.8221 has completed at 0.8863. Deeper decline should then be seen to 61.8% retracement at 0.8466 at least. For now, risk will stay mildly on the downside as long as 55 D EMA (now at 0.8677) holds, in case of recovery.

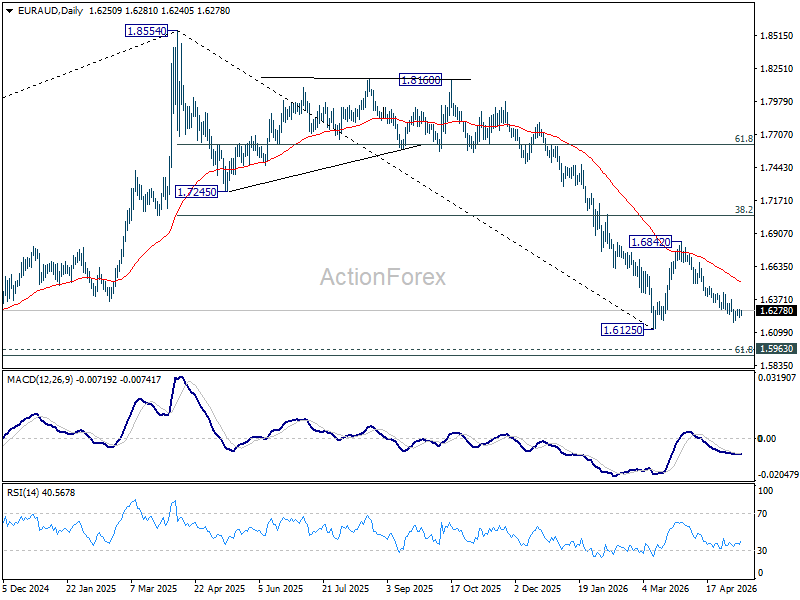

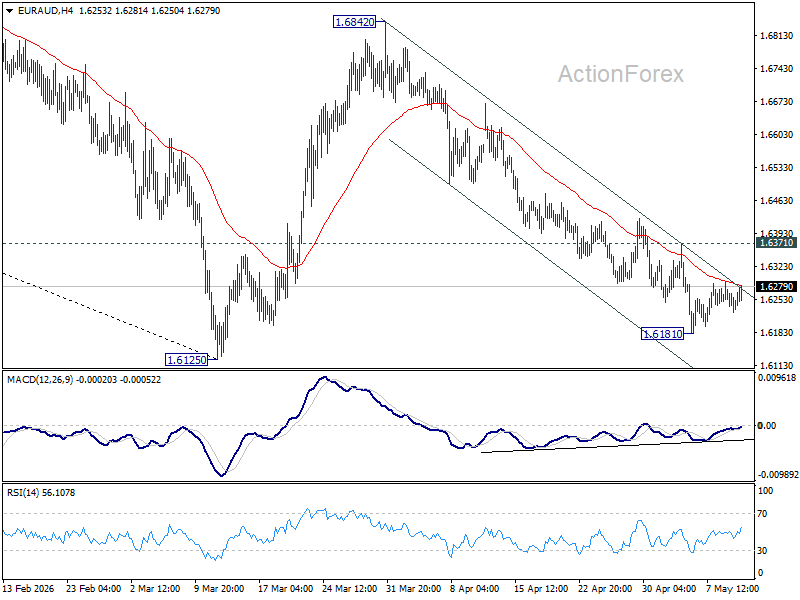

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6220; (P) 1.6254; (R1) 1.6280; More...

Intraday bias in EUR/AUD stays neutral at this point. On the downside, decisive break of 1.6125 will resume larger fall from 1.8554. Nevertheless, break of 1.6371 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound to 55 D EMA (now at 1.6507).

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7039) holds, even in case of strong rebound.