Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1049; (P) 1.1102; (R1) 1.1138; More....

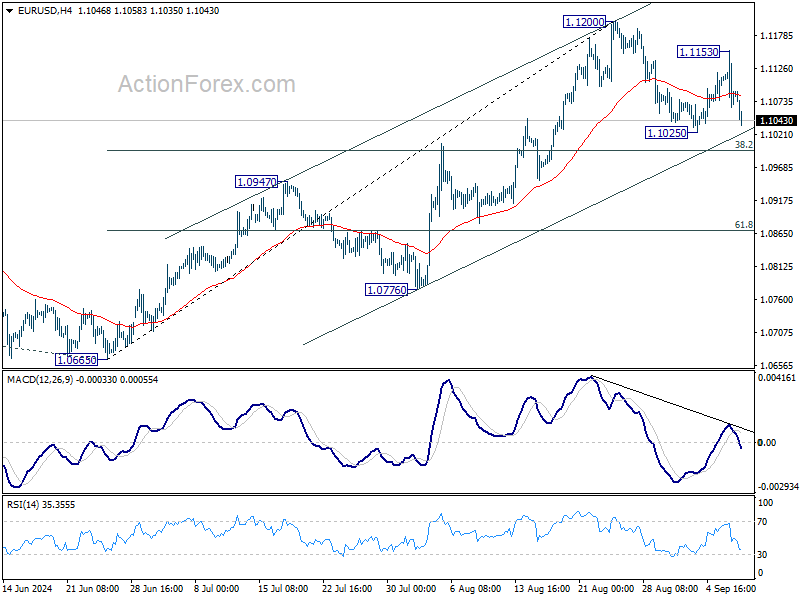

EUR/USD dips notably today but stays in range above 1.1025. Intraday bias remains neutral for the moment. Consolidation from 1.1200 could extend with deeper pull back, but downside should be contained by 38.2% retracement of 1.0665 to 1.1200 at 1.0996 to bring rebound. Break of 1.1200 will resume larger rise towards 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside.

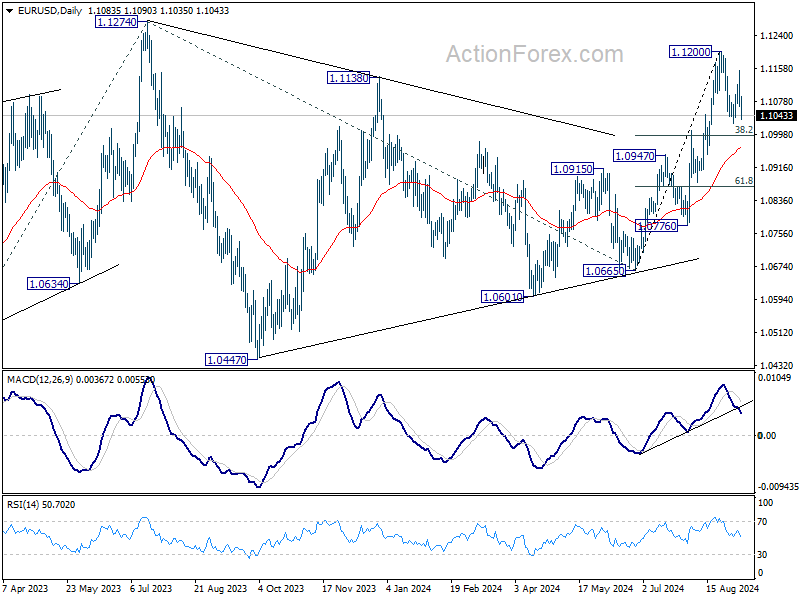

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Euro Pressured by Weak Investor Confidence Sentiment, Dollar Edges Higher

Dollar strengthened modestly in today's quiet trading as market participants continued to scale back expectations for a more aggressive 50bps rate cut by Fed this month. However, the greenback's momentum remains modest as it awaits a crucial test from the upcoming US CPI data this week. Stabilizing risk sentiment is also keeping a lid on further gains for Dollar for now.

Euro, on the other hand, is on the defensive after Eurozone investor sentiment plummeted to its lowest level this year. Germany, the region's economic powerhouse, is at the center of the downturn, with data signaling that the country may already be in recession. Investor confidence continues to erode, with expectations index showing little sign of improvement, casting doubt on a near-term recovery for Germany and the broader Eurozone.

In terms of currency performance today, Yen and Swiss Franc have emerged as the weakest performers, with Kiwi trailing closely behind. Loonie leads the market, followed by Dollar and Aussie. Euro and British Pound are positioned in the middle of the pack. With no major data releases from the US and Fed in its blackout period ahead of its next meeting, market activity is expected to remain subdued through the remainder of the day.

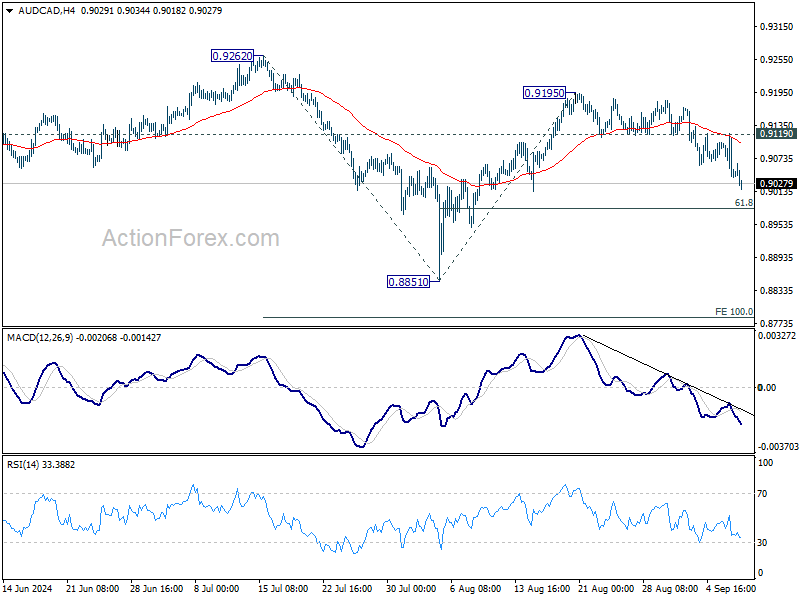

Technically, AUD/CAD's fall from 0.9195 extends lower today. Prior rejection by 55 4H EMA suggests that rebound from 0.8851 has completed already. Deeper fall is now expected as long as 0.9119 resistance holds, towards 61.8% retracement of 0.8851 to 0.9195 at 0.9064. Strong support could be seen there to bring rebound. However, decisive break of 0.9064 will raise the chance that fall from 0.9262 is resuming through 0.8851 to 100% projection of 0.9262 to 0.8851 from 0.9195 at 0.8784.

In Europe, at the time of writing, FTSE is up 0.55%. DAX is up 0.36%. CAC is up 0.52%. UK 10-year yield is up 0.0088 at 3.907. Germany 10-year yield is up 0.032 at 2.211. Earlier in Asia, Nikkei fell -1.42%. Hong Kong HSI fell -1.42%. China Shanghai SSE fell -1.06%. Singapore Strait Times rose 1.22%. Japan 10-year JGB yield rose 0.0449 to 0.895.

Eurozone Sentix investor confidence falls to -15.4, deepening German recession concerns,

Eurozone Sentix Investor Confidence fell sharply again in September, dropping from -13.9 to -15.4, significantly below the expected -11.7. This marks the third consecutive month of declines and the lowest reading since January. The Current Situation Index also weakened, falling to -22.5, its lowest point since December 2023. Meanwhile, the Expectations Index offered a slight improvement, rising from -8.8 to -8.0, but it remains deep in negative territory.

Germany's outlook painted an even bleaker picture. Investor confidence in Europe's largest economy plunged from -31.1 to -34.7, its lowest point since October 2022. Current Situation Index dropped significantly from -42.8 to -48.0, reaching levels not seen since June 2020. Meanwhile, Expectations Index dipped further from -18.5 to -20.3, hitting its lowest since October 2023.

Sentix analysts described the situation as increasingly dire, stating that the German economy is approaching a new "climax" in its deepening recession. The report emphasized that the recession is "raging ever stronger," with expectations continuing to fall, highlighting the "hopelessness" felt by investors.

The report also highlighted that the broader Eurozone is grappling with "dangerous recessionary tendencies," driven largely by Germany's economic struggles. The prospect of a more accommodative monetary policy is now the key hope for market participants, as the ECB is widely expected to announce another rate cut in its upcoming meeting this week.

China's CPI inches up to 0.6% yoy in Aug, but deflationary pressures persist as PPI declines again

China's inflation data for August showed a slight rise in consumer prices, but deflationary pressures continue to weigh on the economy. CPI increased from 0.5% yoy in July to 0.6% yoy, falling short of market expectations of 0.7% yoy.

Food prices saw a notable rise, jumping 2.8% yoy, driven by a 16.1% yoy surge in pork prices and a 21.8% yoy increase in vegetable prices. However, non-food inflation eased significantly, dropping from 0.7% yoy to just 0.2%. Core CPI also fell slightly, rising only 0.3% yoy compared to 0.4% yoy in July.

On a month-over-month basis, China's CPI rose by 0.4% mom , following a 0.5% mom increase in the prior month. While positive, this figure also came in below expectations of 0.5% mom.

Producer prices, on the other hand, extended their negative streak for the 23rd consecutive month. PPI fell from -0.8% yoy in July to -1.8% yoy in August, worse than the anticipated decline of -1.4% yoy.

This persistent deflation in factory-gate prices is being attributed to weak market demand and a continued decline in international commodity prices, according to NBS statistician Dong Lijuan.

Dong also noted that the slight rise in consumer prices in August was largely influenced by seasonal factors, such as high temperatures and rainfall, which boosted food prices.

However, the underlying weakness in both consumer and producer prices points to broader structural issues in China's economy. Economists warn that the ongoing deflationary pressures are a result of production outpacing demand, contributing to a growing surplus and continued challenges for the manufacturing sector.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1049; (P) 1.1102; (R1) 1.1138; More....

EUR/USD dips notably today but stays in range above 1.1025. Intraday bias remains neutral for the moment. Consolidation from 1.1200 could extend with deeper pull back, but downside should be contained by 38.2% retracement of 1.0665 to 1.1200 at 1.0996 to bring rebound. Break of 1.1200 will resume larger rise towards 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Aug | 3.00% | 3.20% | 3.20% | |

| 23:50 | JPY | Current Account (JPY) Jul | 2.80T | 2.10T | 1.78T | |

| 23:50 | JPY | GDP Q/Q Q2 F | 0.70% | 0.80% | 0.80% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 F | 3.20% | 3.00% | 3.00% | |

| 01:30 | CNY | CPI Y/Y Aug | 0.60% | 0.70% | 0.50% | |

| 01:30 | CNY | PPI Y/Y Aug | -1.80% | -1.40% | -0.80% | |

| 05:00 | JPY | Eco Watchers Survey: Current Aug | 49 | 47.6 | 47.5 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Sep | -15.4 | -11.7 | -13.9 | |

| 14:00 | USD | Wholesale Inventories Jul F | 0.30% | 0.30% |

Could US CPI Tip the Balance in Favour of a 50bps Fed Rate Cut?

- Market is digesting last week’s US labour market data

- The August CPI report could fuel 50bps rate cut expectations

- Dollar weakness could continue if inflation surprises to the downside

- The US inflation report will be published at 12:30 GMT on Wednesday

Markets are preparing for the first Fed rate cut

At the recent Jackson Hole Symposium, Fed Chairman Powell indirectly pre-announced the September 18 rate cut and highlighted the importance of the labour market in the current decision process. As a result, last week's mixed jobs market data sealed the rate cut. However, last Friday’s non-farm payrolls figure also increased the market’s concern about the magnitude of the expected economic slowdown, forcing a negative reaction in most stock indices.

Ahead of the usual blackout period, a number of Fed members were on the wires on Friday, essentially confirming the worst kept secret and offering their support for the first, and usually most difficult, decision in an interest rate cycle. But most refrained from openly stating their preference for a 50bps rate move.

Could inflation produce a surprise?

The focus this week turns to inflation as the August report will be released on Wednesday. Powell was quite direct at Jackson Hole about his inflation assessment. He mentioned that inflation is now much closer to the Fed's objective and that "upside risks to inflation have diminished". As such, the importance of the inflation prints has dropped a bit, but this release still holds significant market-moving ability.

Interestingly, the recent inflation-related information is mixed. Last week’s prices paid sub-components for both the services and manufacturing ISM surveys managed to produce upside surprises, thus revealing renewed strength in inflation. Similarly, the mid-August University of Michigan consumer sentiment survey had 1-year expected inflation at 2.9%.

Economists are forecasting a slowdown in the headline figure to 2.6% from 2.9% recorded in July, with the core indicator, which excludes food and energy prices, expected to ease to 3.2%. These forecasts match the Cleveland Fed Nowcast models estimates.

However, there is considerable risk for a downside shift in the headline CPI figure when examining the performance of oil in both August 2023 and last month. In 2023, oil prices increased by 2.3% on a monthly basis, but a sizeable 7% drop was recorded last month. In layman terms, inflation could fall more aggressively and thus add to the Fed doves’ arguments for a more aggressive monetary policy decision next week.

Could a 50bps rate cut become the central scenario?

The market is currently pricing in a 25% probability for a 50bps rate cut on September 18, and a downside inflation surprise would most likely prop-up these expectations. On the flip side, an unsurprising release, which confirms forecasts or even shows a small pick up in inflationary pressures, won’t impact the Fed rate move expectations but could, on the margin, curtail the dovish commentary accompanying the much-expected rate move.

Yen’s outperformance might have legs

The yen has been consistently outperforming the dollar since July. After stalling in August, the move lower in dollar/yen appears to have started again as the Fed is preparing for its first rate cut. A downside surprise to Wednesday’s inflation report could further fuel the ongoing dollar weakness and could help the dollar/yen bears to finally overcome the 142.49 level.

EUR/CHF: Another Potential Downleg May Intensify After Weak China Inflation

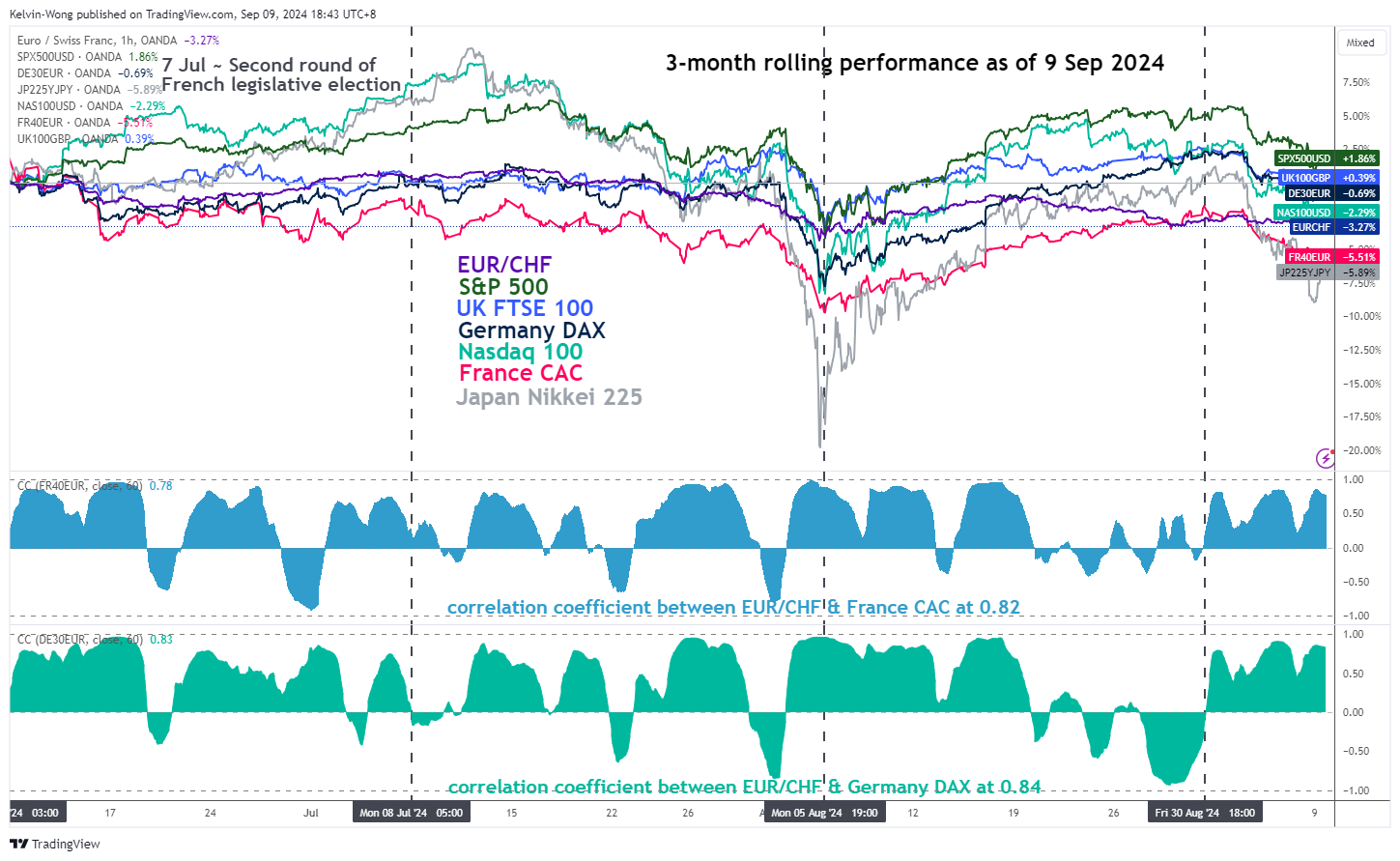

- EUR/CHF has continued to exhibit a high direct correlation with France CAC and Germany DAX.

- China’s core inflation and producer prices for August have indicated a persistent trend of lackluster internal demand.

- Sluggish China’s consumer demand may hurt the profits of key European makers of luxury goods, cars, and machinery.

- Watch the key intermediate support of 0.9255 on the EUR/CHF.

Since the start of September, global benchmark stock indices wobbled where the MSCI All-Country World Index exchange-traded fund (ACWI) ended last Friday, 6 September with a weekly loss of 4%, its worst performance since the week of 6 March 2023 during the onset of the US regional banking crisis.

EUR/CHF continued to move in synch with European stock indices

Fig 1: 3-month rolling performance CAC 40, DAX, EUR/CHF & other major stock indices (US, UK, Japan) as of 9 Sep 2024 (Source: TradingView, click to enlarge chart)

Last week’s risk-off episode, the EUR/CHF has moved in tandem with two key European benchmark stock indices; the France CAC and Germany DAX as their respective 60-period rolling correlation coefficients have remained at a high positive reading of 0.82 and 0.84 at this time of the writing (see Fig 1).

Weak China inflation may stoke further downside pressure in European equities

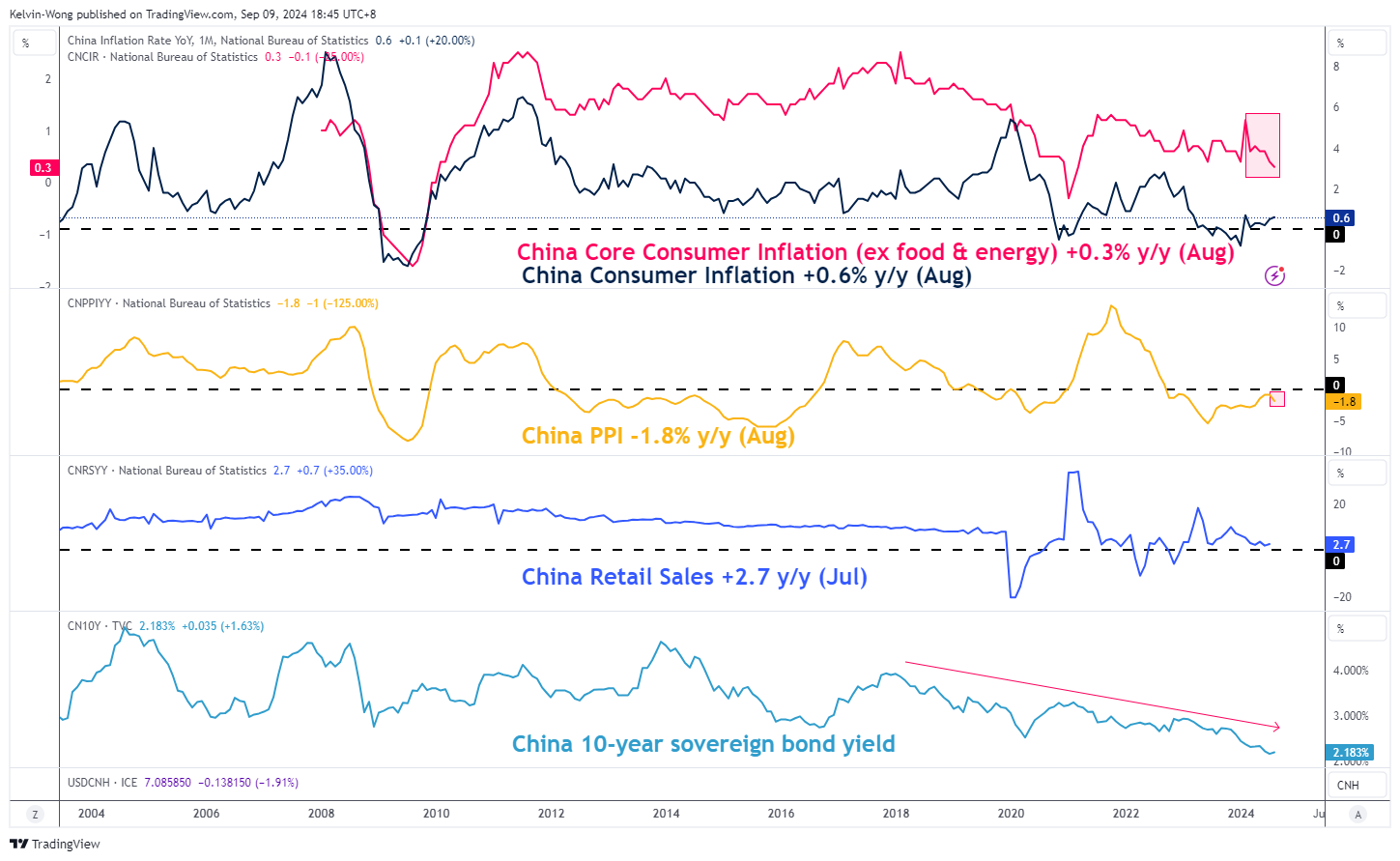

Fig 2: China’s consumer inflation & producer prices trends as of Aug 2024 (Source: TradingView, click to enlarge chart)

Today’s release of China inflation data for August suggests that the state of internal demand in China continued to languish and the deflationary risk spiral narrative is back at the forefront without any clear signals and or initiatives by China’s top policymakers to implement more forceful expansionary policies to drive up consumer and business confidence.

China’s core consumer inflation rate (excluding food and energy) continued to decline for four consecutive months as it fell to 0.3% y/y in August from 0.4% in July. Factory gate prices in China represented by produce prices shrank by 1.8% y/y in August, steeper than its 0.8% drop in the previous month and below expectations of a 1.4% fall (see Fig 2).

Hence, China’s persistent weak consumer demand, a key market for European makers of luxury goods, cars, and machinery is likely to trigger a further toll on these European firms’ profits, in turn, further potential downside on the France CAC and Germany DAX cannot be ruled out.

EUR/CHF is eying the intermediate key support at 0.9255

Fig 3: EUR/CHF medium-term & major trends as of 9 Sep 2024 (Source: TradingView, click to enlarge chart)

During the last synchronized global risk-off episode on 5 August, the EUR/CHF staged a decline but managed to “survive” at the 0.9255 level (29 December 2023 swing low).

However, its rebound from 5 August to 12 August has been capped by its 200-day moving average which has acted as a resistance at around 0.9580 (see Fig 3).

In addition, the weekly MACD trend indicator has now breached below its centreline which suggests that the major downtrend phase of the EUR/CHF is likely in the motion to stage lower lows.

If the 0.9780 key medium-term pivotal resistance is not surpassed to the upside and a break below 0.9255, the EUR/CHF may see further weakness for the next medium-term supports to come in at 0.9085 and 0.8890.

However, a clearance above 0.9780 negates the bearish tone for a potential rebound to expose the long-term pivotal resistance zone of 1.0040/1.1000 (also the upper boundary of the long-term secular descending channel from April 2018 high).

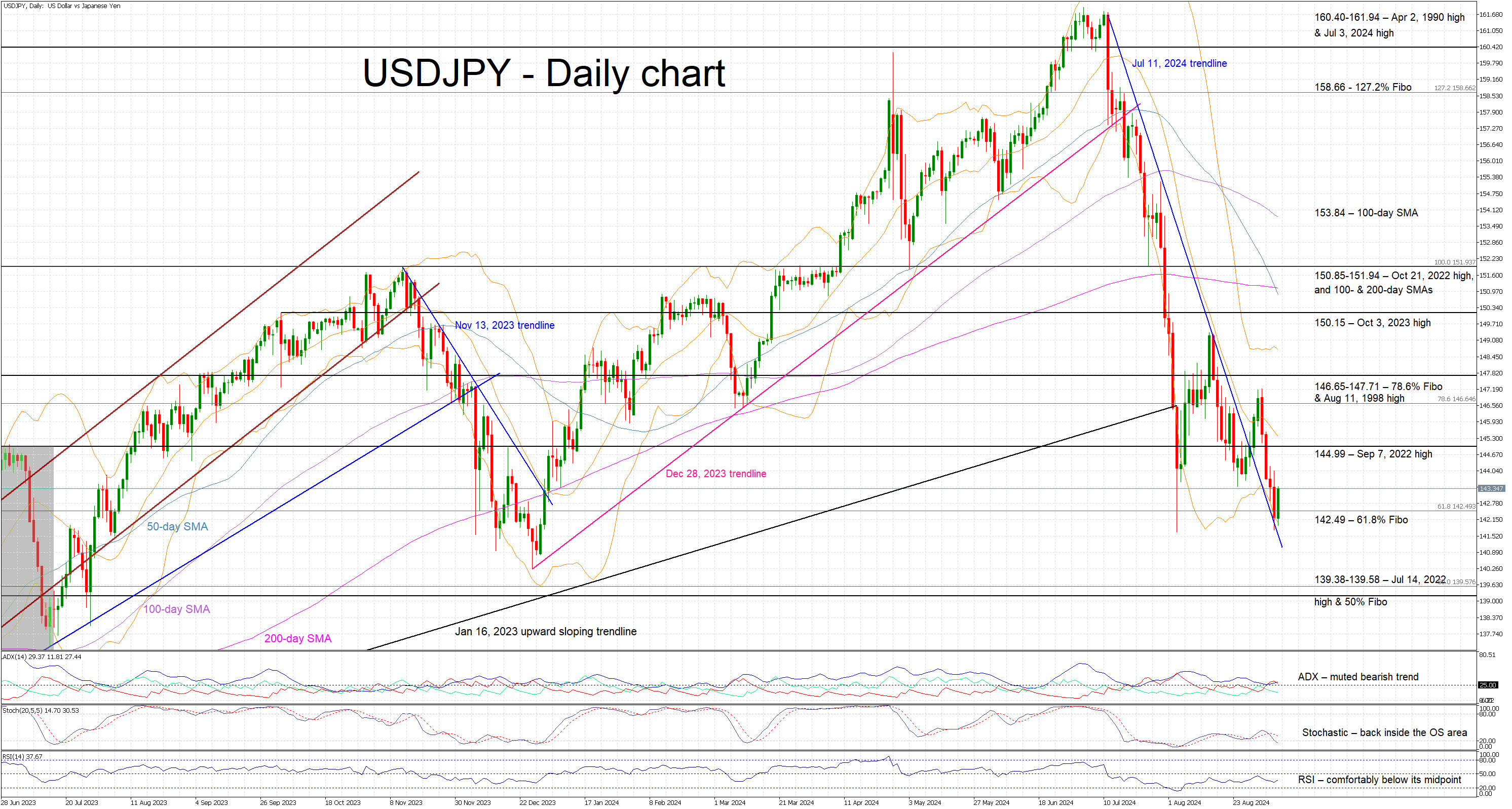

USDJPY Pauses, But This is Temporary

The USDJPY pair halted its decline around 142.98 on Monday. However, this pause in the yen’s rally should not be misleading, as it comes amid uncertainty surrounding the extent of the anticipated monetary policy easing by the US Federal Reserve. The latest US employment report provided little information for adjusting forecasts of the Fed’s interest rate trajectory. Investors must assess fresh inflation data this week before drawing any fundamental conclusions.

Over the past week, the JPY strengthened by almost 3.0% against the US dollar. The USDJPY pair dropped to its annual low amid expectations of decisive action from the Bank of Japan. The BoJ is expected to raise rates by the end of the year, which will be supported by steady economic growth, wage increases, and ongoing inflationary pressure.

If the Bank of Japan’s monetary policymakers’ projections regarding macroeconomic aspects materialise, the central bank will be ready to adjust its monetary policy parameters more actively. Meanwhile, the latest data reflected weak GDP growth in Japan in Q2. The economy expanded by only 2.9% year-on-year, compared to the preliminary estimate of 3.1%.

Technical analysis of USDJPY

On the H4 chart, USD/JPY has formed a consolidation range around the 143.43 level. Due to recent news, the range has widened upwards to 144.00 and downwards to 141.76. Today, a rise towards the 143.43 level (testing from below) is possible, followed by a decline towards 141.70. Breaking this level could signal a continuation of the trend towards 139.70, with the potential for further development towards 137.77. This scenario is technically supported by the MACD indicator, whose signal line is below zero and pointing sharply downwards.

On the H1 chart, USD/JPY completed a downward impulse towards 141.76 and a subsequent rise to 143.00. A new consolidation range has almost formed. Today, a breakout below the lower boundary of this range is likely, with the downward wave continuing towards 140.30 and potentially further towards 139.70. After reaching this level, a correction towards 143.43 is possible. This scenario is also technically supported by the Stochastic oscillator, whose signal line is above 80 and pointing sharply downwards.

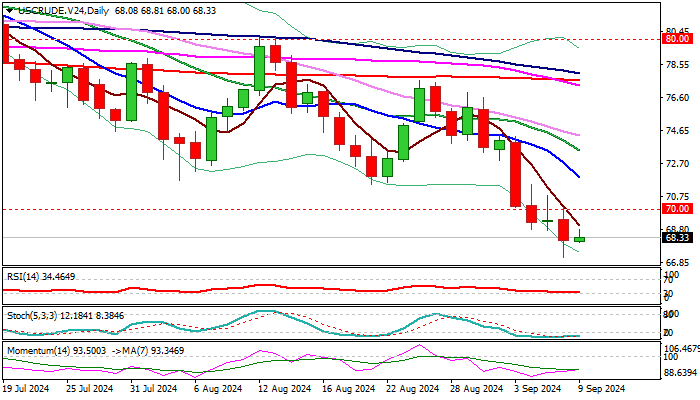

Oil: Bears Pause After Last Week’s 7.3% Drop

Oil price ticked higher on Monday and holding within a narrow consolidation, following 1.8% drop on Friday, sparked by disappointing US jobs data.

Mild rise in early Monday came from a partial profit taking and signals about potential hurricane system developing above US Gulf.

Larger picture shows the oil price in a downtrend which accelerated on growing fears about global demand, due to weak economic data from the US and China, two biggest oil consumers and OPEC decision to start raising output from October, which offsets impact from geopolitical tensions.

Oil price was down over 7% last week, extending the latest bear-leg off $80.14 (Aug 12 lower top) and remaining unaffected by signals of US rate cut that usually boost oil demand.

Daily technical studies are in full bearish setup and reinforced by the latest 50/200DMA death cross, but oversold conditions suggest that bears may take a breather for limited correction before larger bears resume.

Broken psychological $70 level reverted to initial resistance, followed by former double bottom at $71.46/66 (Aug 5/21 lows) reinforced by falling 10DMA ($71.90) which should ideally cap upticks and keep larger bears intact.

Res: 69.03; 70.00; 70.79; 71.66.

Sup: 68.00; 67.15; 67.00; 66.79.

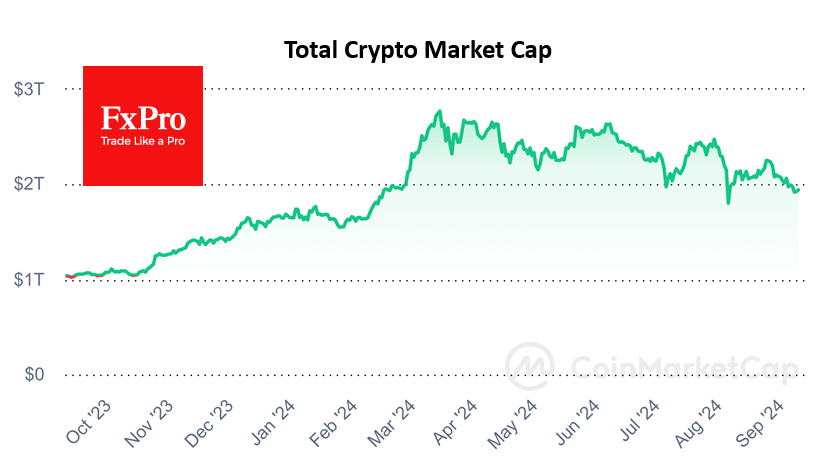

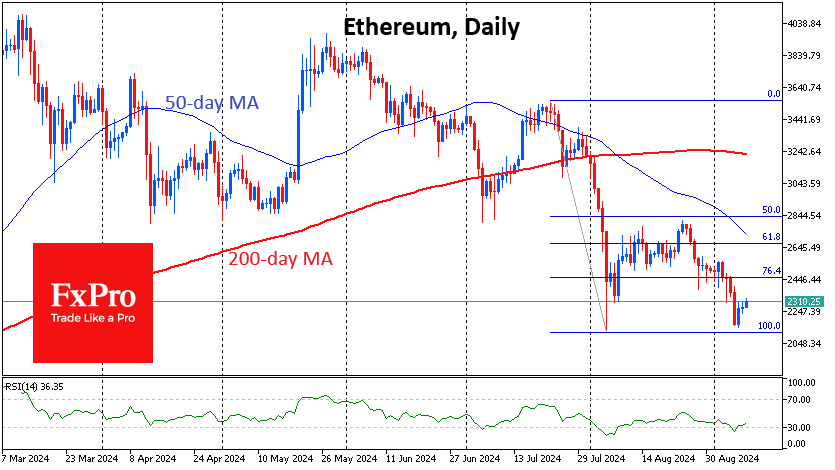

Crypto: Hope for a Bottom

Market Picture

The crypto market is trying to stabilise around the $1.94 trillion mark for the third day (+0.8% in 24 hours and -4% in 7 days) after Friday’s sharp sell-off. It will soon be apparent whether support at the $2 trillion level has turned into resistance.

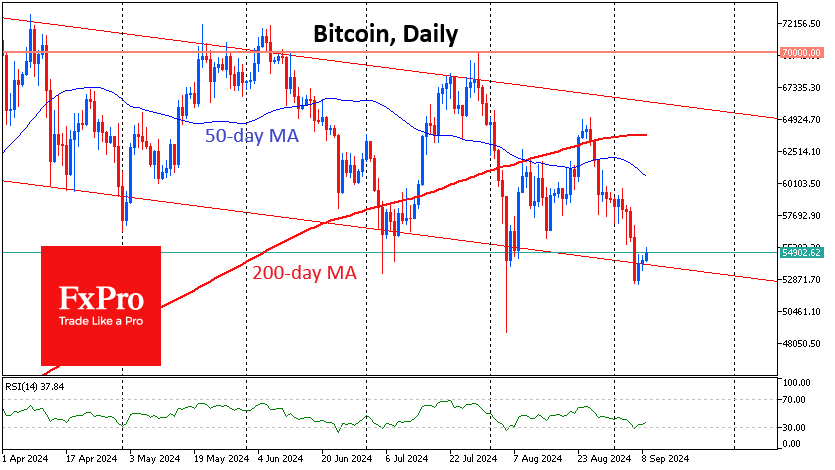

Bitcoin is trading just below $55K on Monday morning, near the bottom of the downward corridor that has been in place since March. Technical indicators are pointing to a possible bounce as the price has moved out of the oversold territory on the daily timeframe, which has preceded rallies several times over the past three months.

Ethereum is trading above $2300, bouncing off the August lows and not yet deepening the decline. The RSI has also moved out of the oversold territory, and the current low on the index is higher than the previous low, indicating that the intensity of the decline has eased.

News Background

According to SoSoValue, outflows from spot bitcoin ETFs in the US totalled $706.2 million last week, following outflows of $277.1 million the previous week. Since the launch of BTC ETFs in January, cumulative inflows fell to $16.89 billion (-4% for the week).

In the Ethereum ETF, outflows rose to $91 million last week, continuing the negative trend for the fourth consecutive week. Net outflows since the product launch increased to $568.3 million (+19.1% for the week).

According to CCData, Ethereum’s market depth on exchanges has fallen by 20% since the launch of spot ETFs, indicating reduced liquidity and increased sensitivity to large orders.

Pressman Film, a company known for producing films, will launch a tokenised fund to finance new projects through the Republic platform on the Avalanche network. Asset buyers will be able to become co-owners of six films. The price of Avalanche rose 7% to over $23.

Eurozone Sentix investor confidence falls to -15.4, deepening German recession concerns,

Eurozone Sentix Investor Confidence fell sharply again in September, dropping from -13.9 to -15.4, significantly below the expected -11.7. This marks the third consecutive month of declines and the lowest reading since January. The Current Situation Index also weakened, falling to -22.5, its lowest point since December 2023. Meanwhile, the Expectations Index offered a slight improvement, rising from -8.8 to -8.0, but it remains deep in negative territory.

Germany's outlook painted an even bleaker picture. Investor confidence in Europe’s largest economy plunged from -31.1 to -34.7, its lowest point since October 2022. Current Situation Index dropped significantly from -42.8 to -48.0, reaching levels not seen since June 2020. Meanwhile, Expectations Index dipped further from -18.5 to -20.3, hitting its lowest since October 2023.

Sentix analysts described the situation as increasingly dire, stating that the German economy is approaching a new "climax" in its deepening recession. The report emphasized that the recession is "raging ever stronger," with expectations continuing to fall, highlighting the "hopelessness" felt by investors.

The report also highlighted that the broader Eurozone is grappling with "dangerous recessionary tendencies," driven largely by Germany's economic struggles. The prospect of a more accommodative monetary policy is now the key hope for market participants, as the ECB is widely expected to announce another rate cut in its upcoming meeting this week.

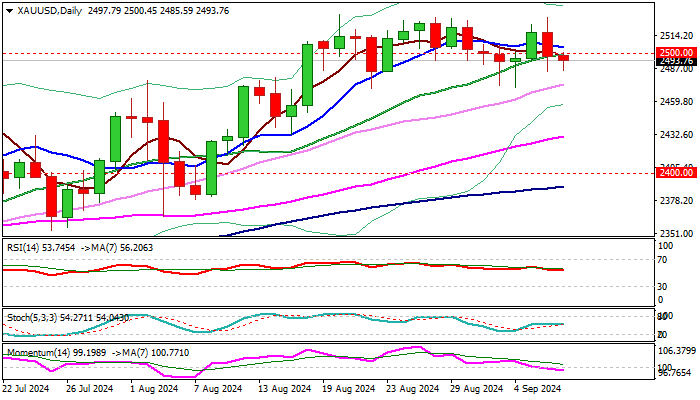

XAU/USD Outlook: Gold Continues to Move Within Larger Range

Gold remains at the back foot at the start of the week, after Friday’s 0.8% drop and a weekly close below $2500.

The metal’s price was deflated by US labor data on Friday, as employment increased below expectations but unexpected drop in jobless rate cooled fears about stronger weakness in the labor sector, contributing to bets for Fed’s rate cut by 0.25% rather than more aggressive approach with 50 basis points cut.

Markets shift focus towards release of US inflation data for August, due later this week, which will provide more details about Fed’s decision in September’s monetary policy meeting.

On the other hand, the yellow metal remains underpinned by growing concerns about the situation in the US economy, as well as persisting geopolitical tensions, which adds to scenario of prolonged consolidation before the price resumes higher.

Technical picture remains bullish overall despite daily studies somewhat weakened, with larger bullish bias to stay intact while the price holds above three-week range floor at $2470 zone.

Three consecutive weekly Doji candles point to strong indecision and signal prolonged sideways mode, with mixed daily studies (14-d momentum turned negative, stochastic and RSI remain in positive territory, MA’s in mixed configuration) contributing to current picture.

Technical studies still favor scenario of $2470 pivot holding dips and offering fresh buying opportunities however, fundamentals are likely to play a key role and to gold’s key driver in the near term.

In case $2470 support is lost, stronger pullback towards $2431 (rising 55DMA) and $2400/$2390 zone (psychological / 100DMA) in extension, could be likely scenario.

Conversely, bulls may strengthen grip if the price returns and stabilizes above $2500 level and shift focus towards new all-time high at $2531, violation of which to spark fresh acceleration higher.

Res: 2500; 2505; 2523; 2531.

Sup: 2485; 2474; 2470; 2457.

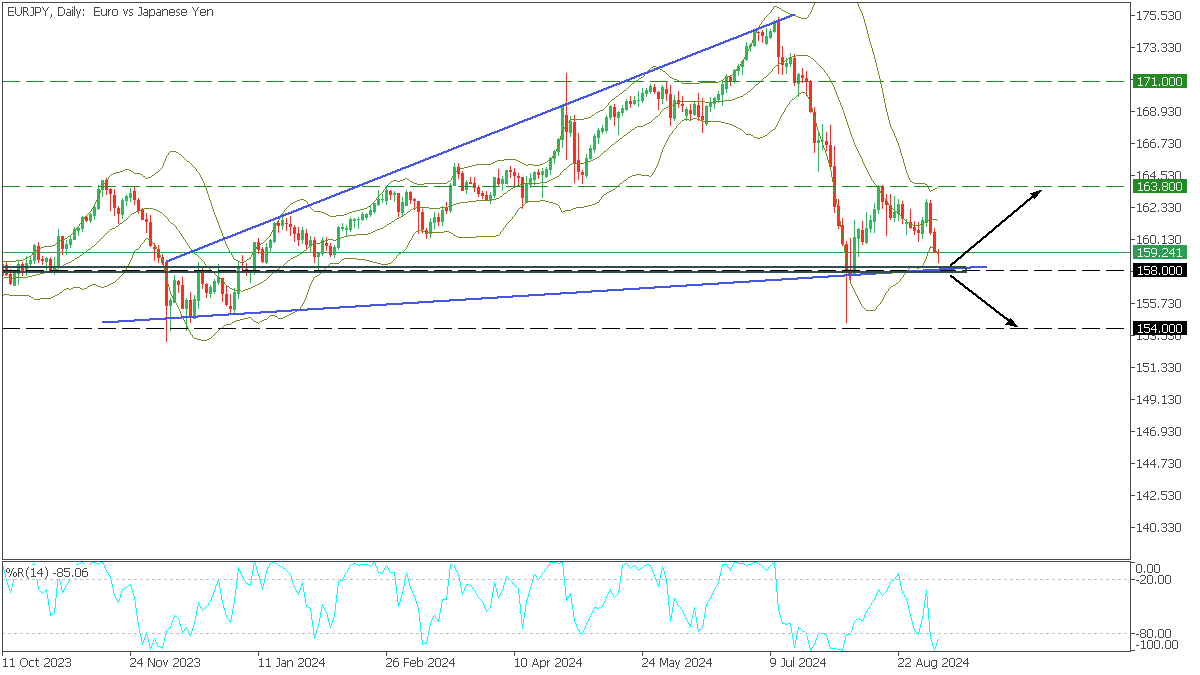

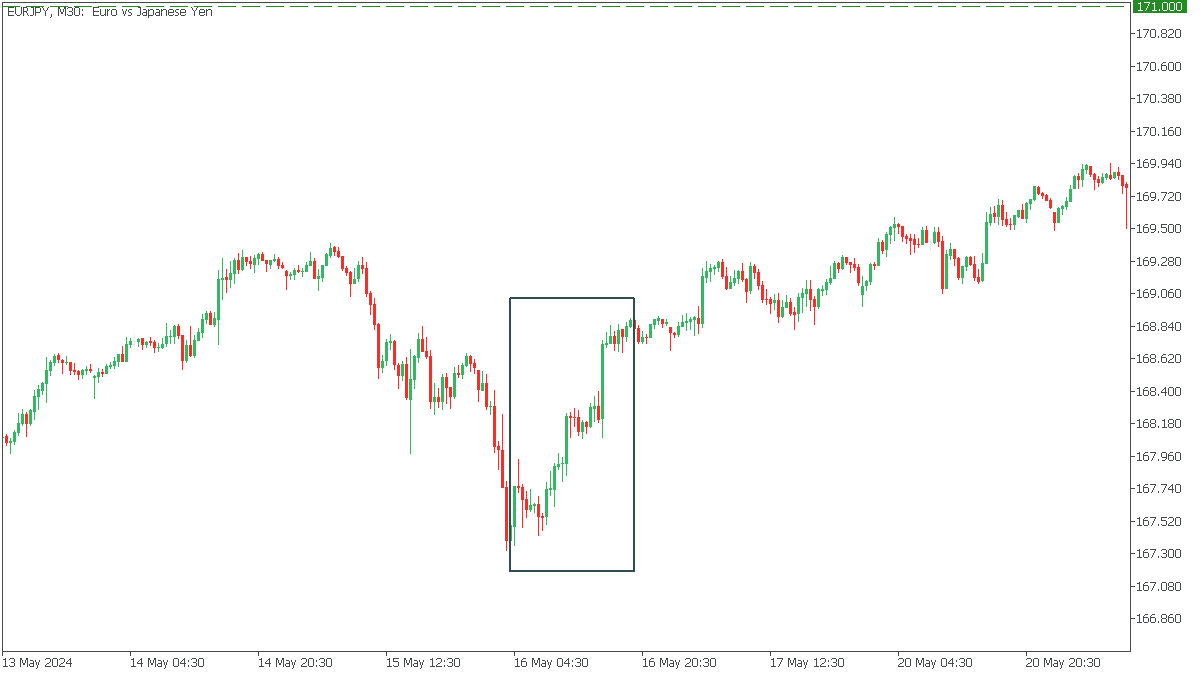

News of the Week (September 9—September 13): EURJPY Market Spotlight

EURJPY is setting up for significant shifts—traders, be ready!

The EURJPY pair reflects the Euro and Japanese Yen exchange rate. Traders frequently use the EURJPY pair to gauge market risk sentiment. The Euro is primarily driven by economic indicators from major economies like Germany and France, monetary policy decisions by the European Central Bank, and geopolitical events within the Eurozone. On the other hand, the Yen is sensitive to Japan’s economic performance but is also known for its status as a safe-haven currency, meaning it often strengthens during global financial uncertainty.

Japan Gross Domestic Product (GDP) QoQ, Sep 09, 01:50 (GMT+2)

The upcoming release of Japan's quarterly GDP is forecasted to show a recovery, with an expected growth of 0.8%, compared to the previous contraction of -0.5%. If the actual GDP figure surpasses this forecast, it would indicate stronger-than-expected economic growth in Japan. A better-than-expected GDP would likely boost the Yen as confidence in Japan's economic recovery grows. And Yen's strength may lower EURJPY.

Conversely, the Yen could lose value if the GDP result is weaker than the forecast, suggesting Japan’s economic recovery is faltering. In this case, traders may move away from the Yen, causing the EURJPY pair to rise as the Euro gains relative strength.

The last time the May 16, 2024, report from the GDP QoQ came in significantly worse than expected, causing EURJPY to rise!

Eurozone Interest Rate Decision, Sep 12, 14:15 (GMT+2)

The Eurozone’s interest rate decision is anticipated to result in a rate cut to 4.0% from the current 4.25%, which would signal a dovish stance from the European Central Bank. If the ECB goes ahead with the forecasted cut, the Euro might weaken as lower interest rates reduce the currency’s appeal to investors seeking higher returns. In this case, the EURJPY pair could decline.

However, if the ECB surprises the market by keeping rates unchanged, signaling concerns about inflation, the Euro could strengthen. A stronger-than-expected stance on interest rates would likely push the EURJPY pair higher.

In the Daily timeframe, EURJPY formed an expanding wedge pattern after a short-term bullish rise. The price fell to the lower trend line, testing the critical support area and the lower Bollinger line. At the same time, the %R shows oversold.

- If the price breaks the lower trend line below 158,000, the downside target would be 154,000.

- A bounce from the lower trend line will bring EURJPY back to the resistance at 163.800.