Sample Category Title

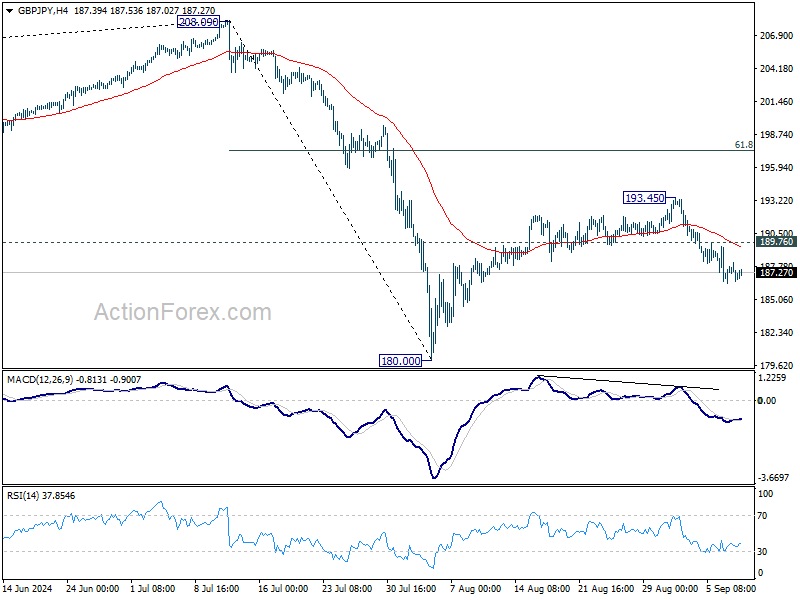

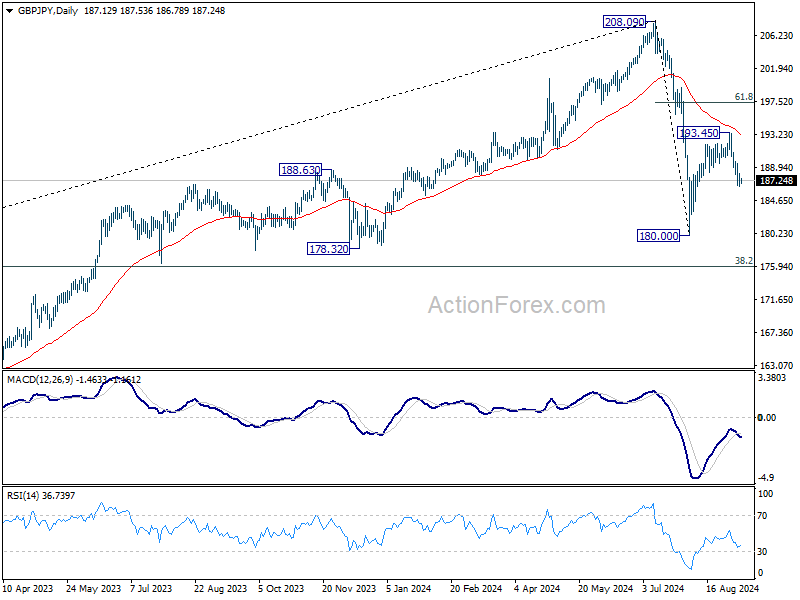

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.36; (P) 187.24; (R1) 188.05; More...

Intraday bias in GBP/JPY stays on the downside at this point, and fall from 193.45 is in progress for retest 180.00 low first. Break there will resume whole fall from 208.09. On the upside, above 189.76 minor resistance will turn intraday bias neutral.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

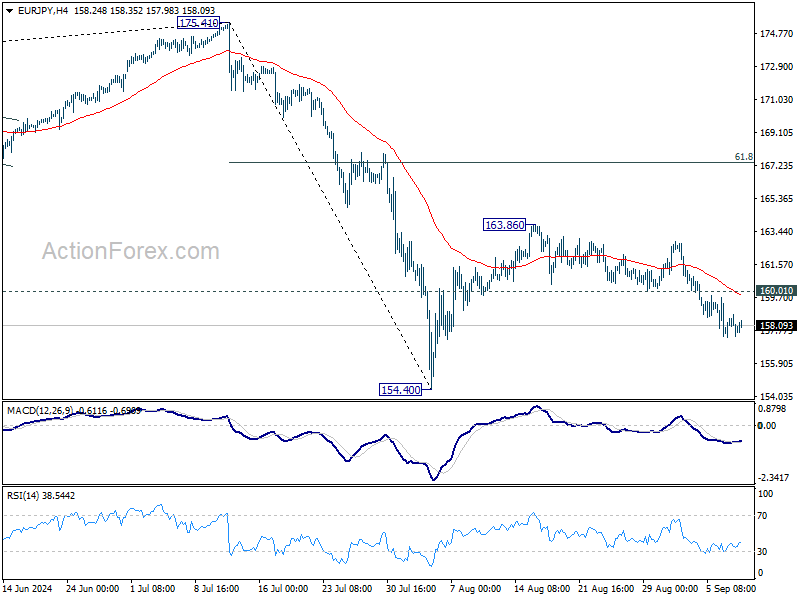

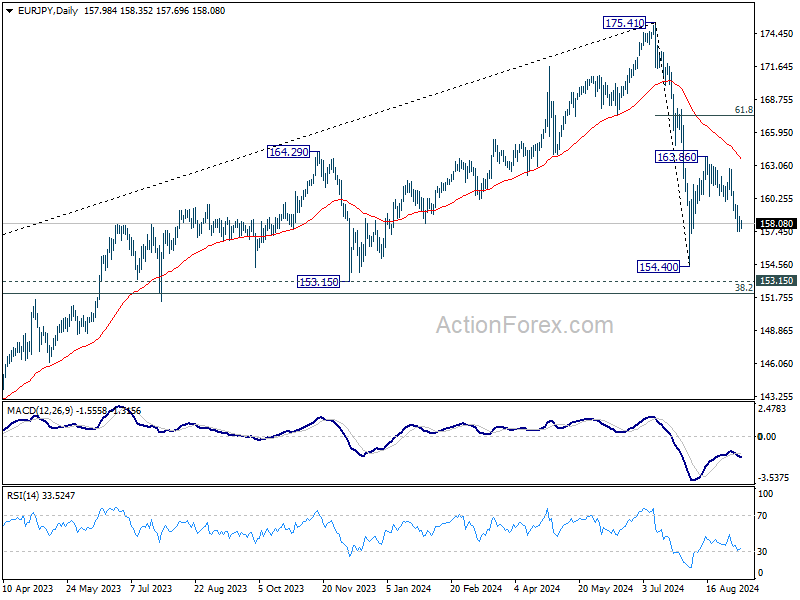

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.35; (P) 158.04; (R1) 158.66; More....

Intraday bias in EUR/JPY stays on the downside for the moment. Fall from 163.86 is in progress for retesting 154.40 low. Firm break there will resume whole decline from 175.41 to 153.15 support. On the upside, above 160.01 support turned resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

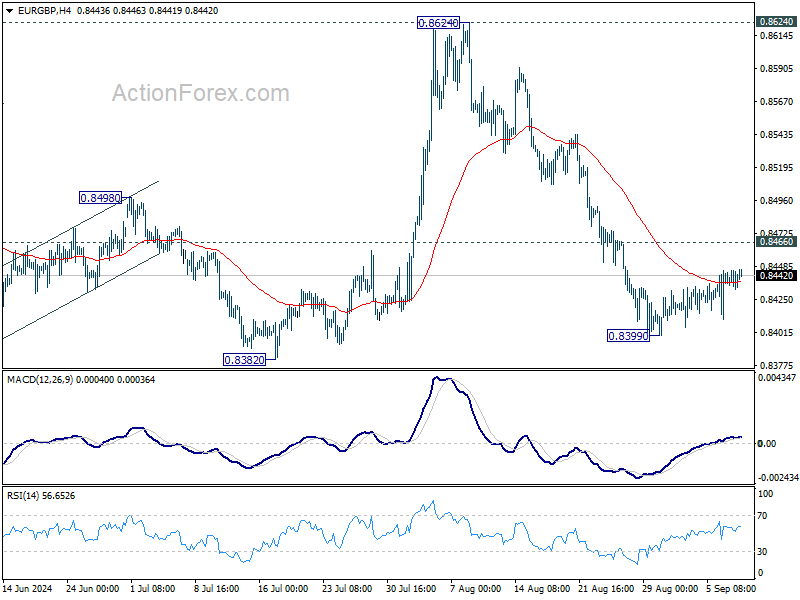

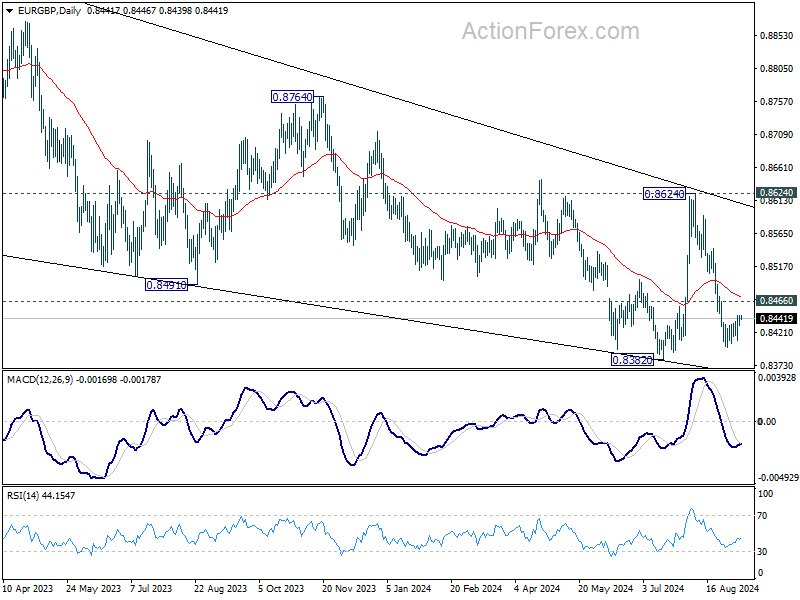

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8434; (P) 0.8440; (R1) 0.8448; More...

EUR/GBP is still extending the consolidation from 0.8399 and intraday bias remains neutral. Further decline is expected with 0.8466 resistance intact. On the downside, below 0.8399 will resume the fall from 0.8624 and target 0.8382 support. Firm break there will resume larger down trend.

In the bigger picture, as long as 0.8624 resistance holds, down trend from 0.9267 is expected to continue. Firm break of 0.8382 will target 0.8201 (2022 low). However, decisive break of 0.8624 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

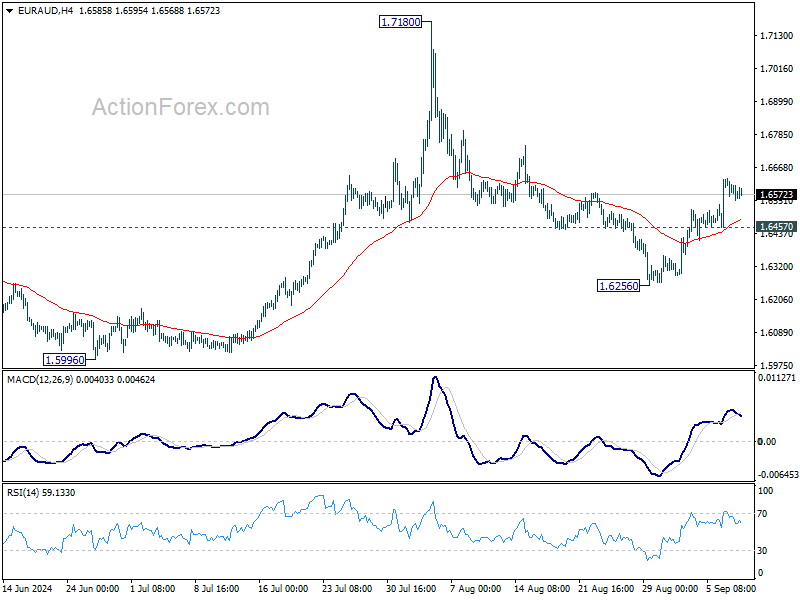

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6537; (P) 1.6585; (R1) 1.6614; More...

Intraday bias in EUR/AUD stays on the upside at this point. As noted before, corrective pullback from 1.7180 could have completed at 1.6256 already. Further rise should be seen to retest 1.7180 high next. On the downside, however, break of 1.6457 support will turn bias back to the downside for 1.6256 again.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

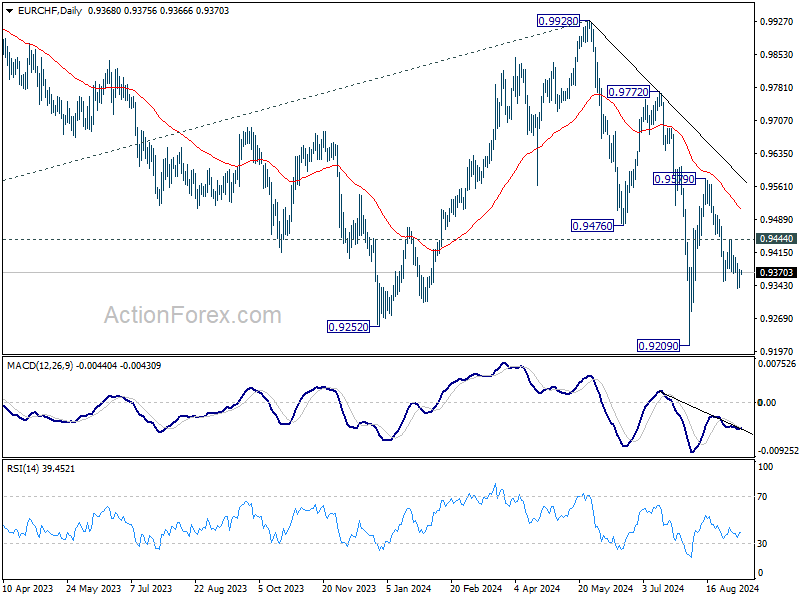

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9349; (P) 0.9364; (R1) 0.9388; More....

As long as 0.9444 resistance holds, further decline is still expected in EUR/CHF despite weak momentum as seen in 4H MACD. As noted before, rebound from 0.9209 could have completed at 0.9579 already, ahead of 55 D EMA. Deeper fall should be seen to retest 0.9209 first. Firm break there will resume larger down trend. However, break of 0.9444 will turn bias back to the upside for 0.9579 resistance instead.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

China’s exports grow 8.7% yoy in Aug, imports up only 0.5% yoy

China's exports grew by a robust 8.7% yoy to USD 308.7B in August, surpassing market expectations of 6.5% yoy growth. However, this impressive figure is largely attributed to base effect, as exports contracted by -8.8% yoy during the same period last year.

Exports to key regions such as the US, the EU, and the ASEAN all posted solid gains. Notably, exports to the EU saw the largest increase, growing 13% yoy.

In terms of imports, China's intake from the US rose by 12% yoy, while imports from the EU showed a decline. Imports from ASEAN grew by 5% yoy. Overall import growth remained weak, increasing by just 0.5% yoy compared to the expected 2.0% yoy.

China's trade surplus widened significantly, rising from USD 84.65B in July to USD 91.02B, exceeding expectation of USD 83.9B.

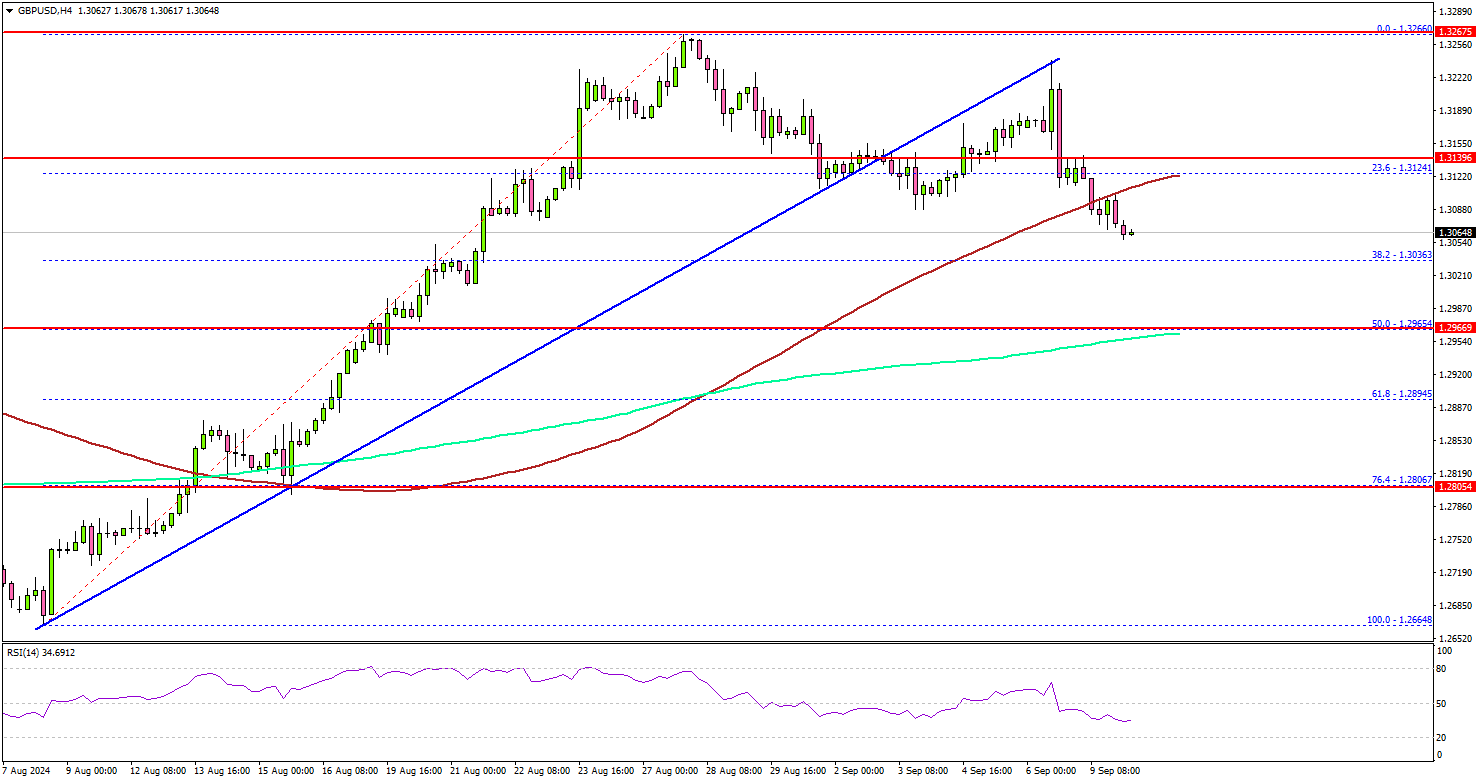

GBP/USD Starts Pullback, UK Employment Report Next

Key Highlights

- GBP/USD struggled near 1.3260 and started a downside correction.

- It traded below a key bullish trend line with support at 1.3140 on the 4-hour chart.

- EUR/USD is struggling to start a fresh increase above 1.1100.

- The UK Claimant count could change by 95.5K in August 2024.

GBP/USD Technical Analysis

The British Pound faced heavy resistance near 1.3250 against the US Dollar. GBP/USD formed a short-term top and started a downside correction below 1.3200.

Looking at the 4-hour chart, the pair traded below the 23.6% Fib retracement level of the upward move from the 1.2664 swing low to the 1.3266 high. It also traded below a key bullish trend line with support at 1.3140.

The pair broke the 1.3100 level and the 100 simple moving average (red, 4-hour), but it stayed above the 200 simple moving average (green, 4-hour).

On the downside, immediate support sits near the 1.3035 level. The next key support sits near the 1.2965 level and the 200 simple moving average (green, 4-hour). It is close to the 50% Fib retracement level of the upward move from the 1.2664 swing low to the 1.3266 high.

A downside break below the 1.2965 level could set the pace for a larger decline. The next major support is near the 1.2800 level. On the upside, the pair could face resistance near the 1.3140 level.

The next key resistance sits near the 1.3180 level. A clear move above the 1.3180 level could set the pace for a move toward the 1.3250 zone. Any more gains might call for a test of the 1.3350 zone.

Looking at EUR/USD, the pair struggled to start a fresh increase above 1.1100 and might extend its downside correction.

Upcoming Economic Events:

- UK Claimant Count Change for August 2024 – Forecast 95.5K, versus 135K previous.

- UK ILO Unemployment Rate for July 2024 (3M) – Forecast 4.1%, versus 4.2% previous.

Australia’s NAB business confidence falls to -4, conditions fairly clearly below average

Australia's NAB Business Confidence fell from 1 to -4 in August. Business Conditions also declined, dropping from 6 to 3. Trading conditions dipped by 2 points, while profitability slid by 1 point. Forward orders remained unchanged at -4.

NAB Chief Economist Alan Oster commented on the data, noting that "conditions are now fairly clearly below average compared to the history of the survey," underscoring the broader weakness in the private sector as the economy slows.

The decline in the employment gauge is particularly notable, as it "suggests the period of very strong private sector labor demand seen throughout the post-Covid period may be coming to an end," Oster added.

Australian Westpac consumer sentiment falls to 84.6, economic concerns deepen

Australia’s Westpac Consumer Sentiment Index saw a marginal decline of -0.5% mom in September, falling from 85.0 to 84.6, reflecting the ongoing pessimism that has gripped Australian consumers for more than two years. According to Westpac, this persistent negativity shows "no real signs of lifting," with key indicators pointing to growing anxiety about the country's economic outlook.

Sentiment around economic conditions for the next 12 months dropped from 83.3 to 81.2, while unemployment expectations rose sharply from 133.5 to 138.4, signaling growing concerns about job security. However, the interest rate expectations index saw some relief, falling from 135.5 to 123.8, as consumers became less worried about further rate hikes.

Westpac noted that the focus among consumers appears to be shifting. "While cost-of-living pressures are becoming a little less intense and fears of further interest rate rises have eased, consumers are becoming more concerned about where the economy may be headed and what this could mean for jobs," the report highlighted.

ECB Policy Meeting: Another Rate Cut and Emphasis on September’s Data

- ECB widely expected to deliver a second rate cut to 3.50%

- September’s data could be important for October’s meeting

- EURUSD looks bearish; next support could develop near 1.0990

Spotlight turns to economic growth too

Inflation is no longer the sole focus, as economic growth has gained equal importance, although central banks still prioritize maintaining symmetrical price stability around 2.0%.

The story lately was that a couple of disappointing US business and employment data raised speculation that the world’s largest economy might be at the brink of a recession and could drag the rest of the world down with it as US interest rates remain unchanged at restrictive levels.

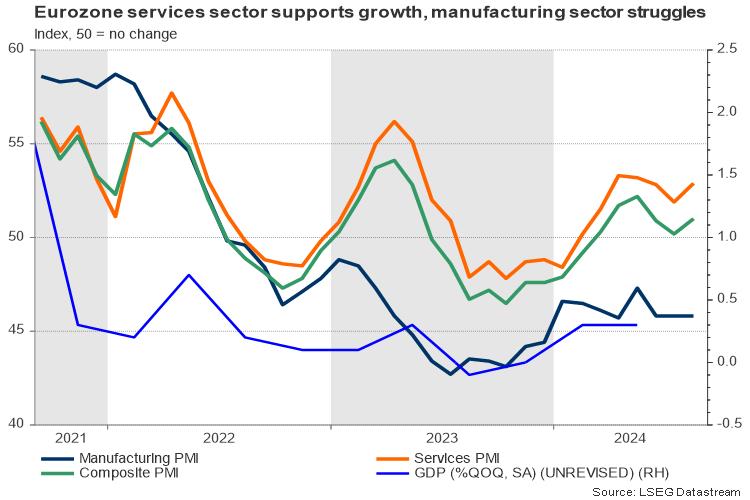

The Eurozone economy exceeded analysts’ expectations in Q2, showing ongoing growth since Q3 2023, but the pace remained modest at 0.3% q/q and 0.6% y/y, falling short of the ECB’s 2024 forecast of 0.8% y/y.

Of course, a glance at member states shows a widening gap, with tourism-led economies such as France and Italy displaying stronger GDP numbers than the struggling industrial-led Germany. The latest S&P Global business PMI report revealed that the Olympic games in France and the tourism boost in Spain and Italy could support Q3 GDP numbers. However, with Germany’s growth engines in artificial intelligence and other technological areas falling behind those of the US and China, and given the presence of geopolitical risks, it is questionable whether the bloc will attract noteworthy investment in the coming years.

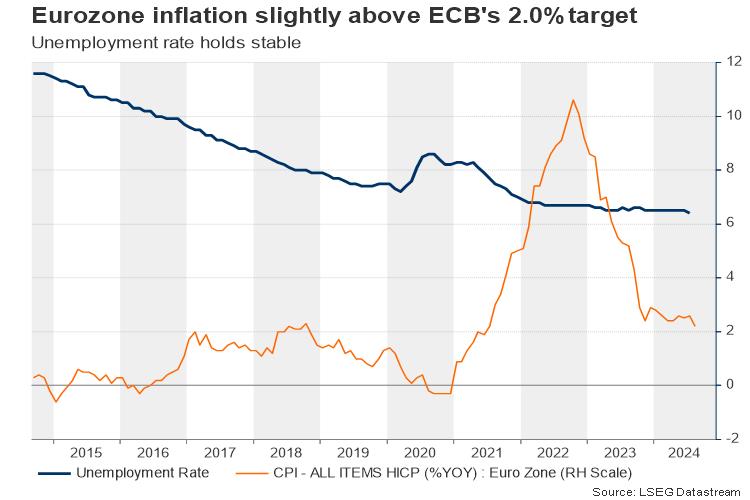

Eurozone's labor market is not a problem

As regards the labor market, the unemployment rate has been steady near a record low of 6.4%, but spending appetite was cautious as reflected by a near-zero growth in the household consumption and the falling savings ratio. Although the dynamics on the wage front are mixed across member states, with Germany demanding more increases, the latest round of negotiations within the bloc averaged at a lower level of 3.6% y/y in Q2 from 4.7% y/y in Q1, easing the risk of a wage-price spiral.

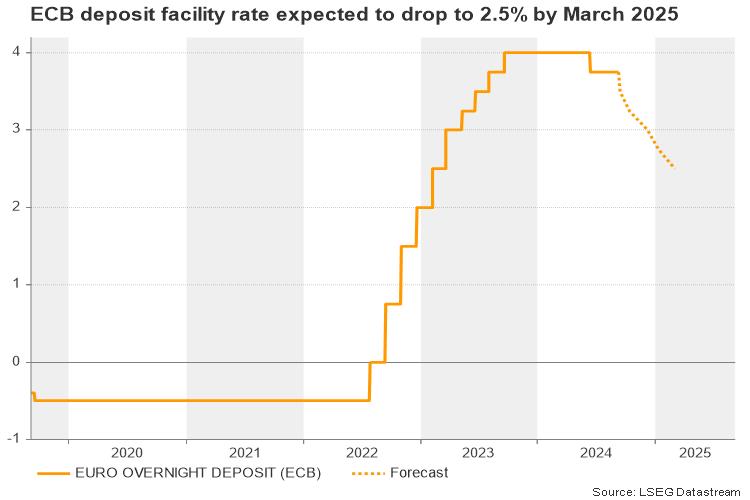

A second 25bps rate cut is a done deal. What's next?

Hence, a second cut of 25bps in the deposit facility rate to 3.50% may not face strong opposition this week. Analysts believe this is a done deal, especially after ECB board member Kazaks admitted that the sideways move in inflation is consistent with further rate cuts. A few days later, headline CPI inflation broke its range to hit a three-year low of 2.2% y/y, standing marginally above the ECB’s target of 2.0%, while the core measure also eased notably to 2.8% y/y.

Similar to the Fed, we must ask if there is a chance for a significant 50bps rate reduction in the eurozone this year. The ECB is scheduled to update its inflation and GDP forecasts along with its rate decision and therefore it could give fresh hints about its next policy steps. However, October’s gathering could be considered a better timing for guiding investors when September’s economic figures are out.

In the meantime, futures markets are pricing in a third 25bps rate cut later his year, though they are uncertain about whether this will happen in October or December. There is also ambiguity about whether a potential reduction in December could be a double one if nothing happens in October. Overall, investors see interest rates at 2.5% by March, which suggests a back-to-back easing or a 50bps base rate cut with a break in the coming meetings.

Market reaction

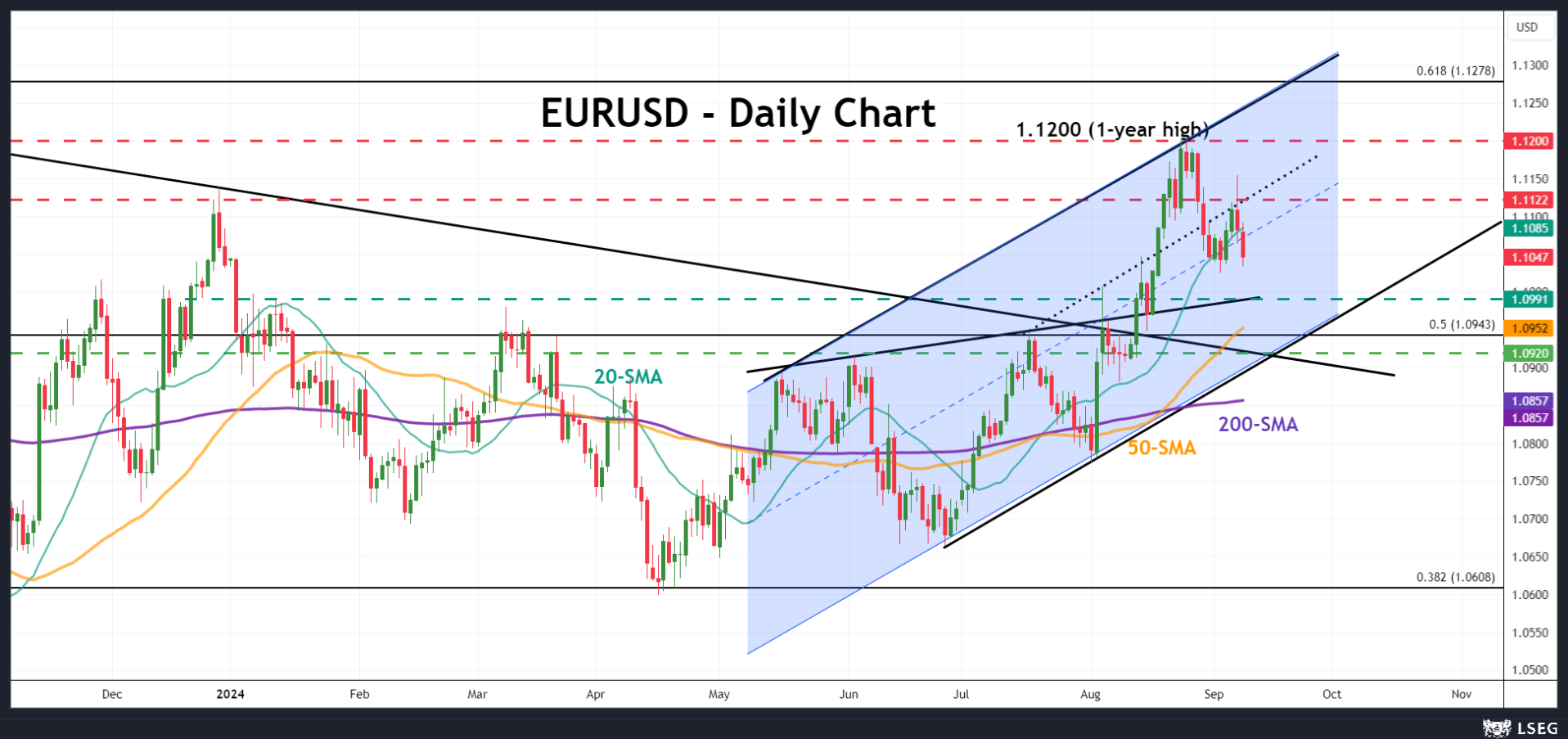

For the time being, policymakers might avoid any strongly dovish language and could show preference for a step-by-step policy monitoring, given the elevated prices in the services sector. If that proves to be the case, investors might translate it as a hawkish signal, helping EURUSD climb back towards its 20-day simple moving average (SMA) at 1.1084 and then up to the 1.1100 tough resistance.

From a technical perspective, today’s drop below the 20-day simple moving average shifted the attention to the 1.0990 area, while lower, the 1.0915-1.0940 zone might pause steeper declines. Yet for the bears to reach the latter, the central bank must discuss the potential for a 50bps rate cut and/or even signal a continuous easing policy into 2025.