Sample Category Title

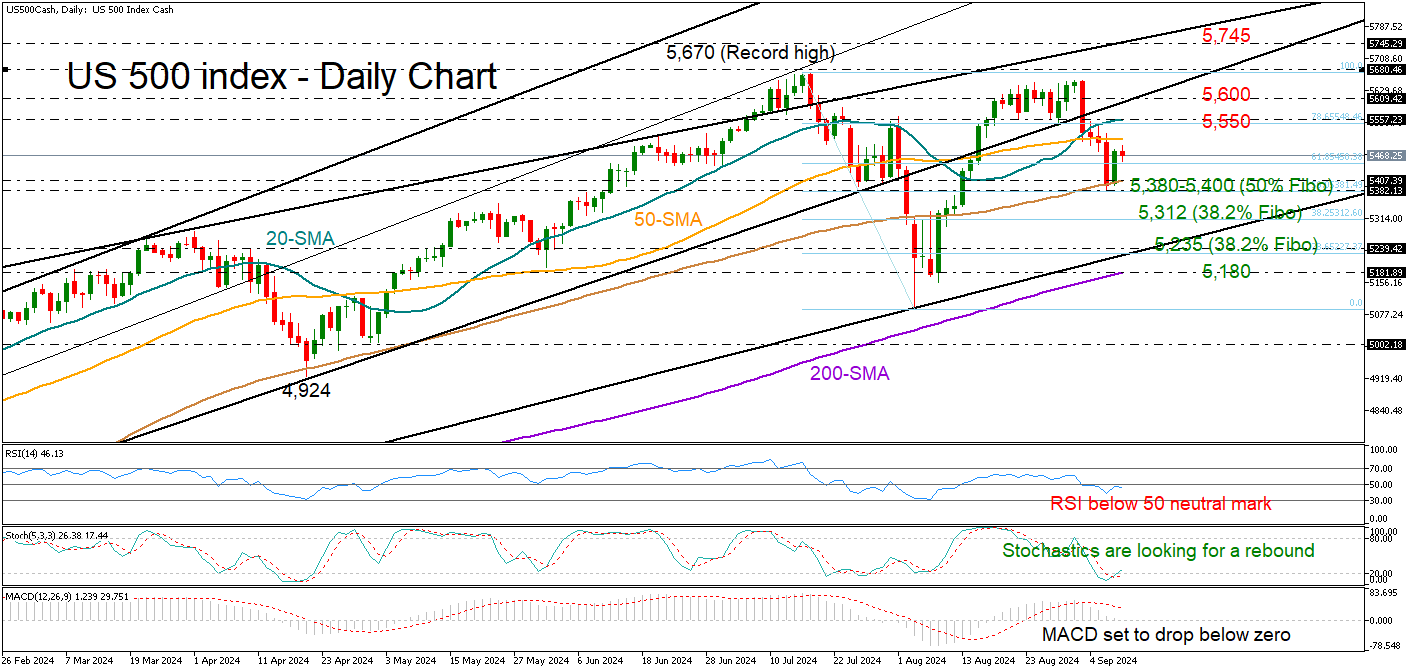

US 500 Index Halts Decline, But Will It Pivot?

- US 500 stock index pauses decline near 100-SMA, but negative risks remain

- Breaking above 5,600 could positively impact buying sentiment

The US 500 stock index maintained support close to its 100-day simple moving average (SMA) for a second consecutive day, raising hopes that the current bearish phase may soon diminish.

From a technical perspective, there are still some negative developments that should be considered. The price could not reverse its latest bearish candlestick, remaining below its 20- and 50-day SMAs. Additionally, although the stochastic oscillator is preparing to exit its oversold region, the RSI continues to trend below its 50 neutral mark and the MACD is ready to step into the negative zone.

The first debate between Kamala Harris and Donald Trump today could be the last one before the US election. Hence the event could be the next catalyst, and buyers would like to see a decisive bounce above the 5,600 trendline area before charting a new record high likely near the former ascending line at 5,745. Further up, the price could face a tough test near the 6,000 psychological mark, which overlaps with the 161.8% Fibonacci retracement of the latest downfall and the rising constraining line from December 2023.

Should the bears breach the floor between the 100-day SMA and the 50% Fibonacci number of 5,380, the door will open for the 38.2% Fibonacci of 5,312. If the latter fails to hold, the decline could stretch towards the tentative support trendline and the 23.6% Fibonacci of 5,235. Another violation there could immediately stall near the 200-day SMA at 5,180.

Overall, the current bounce-back in the US 500 doesn’t seem encouraging because the bears are still favored by the technical indicators. An extension above 5,600 could shift the odds to the bullish side.

GBP/USD Steady as UK Wage Growth Eases GDP Next

The British pound has edged lower on Tuesday. In the North American session, GBP/USD is trading at 1.3055, down 0.14% on the day.

UK wage growth drops to 2-year low

UK wage growth eased in the three months to July, an encouraging sign for the Bank of England as it looks to continue lowering rates.

Average earnings excluding bonuses climbed 5.1% y/y, down from 5.4% in the previous period and in line with the market estimate. This was the lowest level since June 2022. Wage growth is moving in the right direction but is still much too high for the BoE’s liking as it is incompatible with the target of keeping inflation at 2%.

The UK labour market remains strong, as the unemployment rate edged down to 4.1%, down from 4%. The economy created 265 thousand jobs in the three months to July, up sharply from 97 thousand in the previous report and blowing past the market estimate of 115 thousand. The solid data means that the BoE isn’t under pressure to cut rates next week, and the markets are looking at another cut in November.

The UK economy gets a report card on Wednesday, with the release of GDP for July. The economy flatlined in June and rose just 0.6% in the three months to June. Another weak GDP release could put pressure on the British pound.

Investors will be keeping a close eye on Wednesday’s US inflation release. The Federal Reserve is now focused on employment now that inflation is between 2% and 3%, but a CPI surprise could shake up the markets and change market pricing for a Fed rate cut. The odds of a 50-basis point cut have been slashed to 29%, compared to 59% on Friday.

GBP/USD Technical

- There is resistance at 1.3167 and 1.3225

- 1.3069 and 1.3011 are providing support

Sunset Market Commentary

Markets

Spotting significant market moves is like looking for a needle in a haystack today. We give it our best shot anyway by diving into a bumper bond sale taking place in Italy. The southern country’s 30-yr auction drew a record €130bn+ in demand, allowing it to tighten the final terms from BTPS+15 bps area to BTPS+13. It eventually raked in an amount of €8bn. Italian bonds (marginally) outperform regional peers with spreads easing 2 bps (10-yr). It’s 30-yr bond yield is hovering near the recent lows just north of 4.2%. Yields in core areas including the US and Germany trade little changed. US Treasuries gained a slight upper hand over Bunds in early US dealings with yields easing 1.5 bps at the front. Currency markets are an ocean of calm. EUR/USD oscillates around the 1.104 opening levels. The trade-weighted dollar index takes a breather at 101.65 after some proper gains over the previous two trading gains. The Norwegian krone outperforms G10 peers. The Scandinavian currency’s recent track record was poor with EUR/NOK moving from 11.6 end of August towards but below 12. Slightly weaker than expected Norwegian headline inflation this morning nudged EUR/NOK within inches of that psychologically important figure. But lacking strength for a technical break higher, it triggered some return action instead (EUR/NOK currently offered at 11.90). Sterling reversed some earlier gains after a slightly better than expected labour market report this morning to trade virtually unchanged at EUR/GBP 0.844 and GBP/USD 1.307. The slow start of the week after today is giving way for hopefully some more live action. The eco calendar from tomorrow on heats up with the first (and probably only) presidential debate starring Trump and Harris at 3am CEST, followed by US inflation numbers in the afternoon. The ECB takes center stage on Thursday with a second 25bps rate cut all but certain.

News & Views

Czech inflation slowed from 0.7% M/M in July to 0.3% in August, though consensus hoped for a sharper slowdown to no growth. Main price drivers were “alcoholic beverage, tobacco” and “food and non-alcoholic beverages”. Prices of goods in total increased by 0.1% (0.5% Y/Y) and prices of services by 0.5% (5% Y/Y). Actual rent prices rose by 0.3%. Annual inflation remained stuck at 2.2% Y/Y. In the Y/Y-comparison, the impact of higher food prices was offset by lower fuel prices. The biggest influence came again from “housing, water, electricity, gas and other fuels”. Today’s inflation number compares with a 1.8% Y/Y forecast in the Czech National Bank’s summer forecasts. Core inflation (2.4% Y/Y) is also somewhat higher than predicted, as is monetary policy-relevant inflation (2.1% instead of 1.7%). The CNB commented that core inflation is being driven by wage growth in the domestic economy, which is affecting services prices in particular. Partly offsetting this is a decrease in the profit mark-ups of producers, retailers and service providers. The recent property market recovery has been reflected in faster growth in imputed rent. Today’s release didn’t alter market thinking on the outcome of the next, September 25, monetary policy meeting (25 bps rate cut). EUR/CZK made another minor attempt to dive below 25, but failed as it has been doing since the end of August.

It was the other way around for Hungarian inflation. From a similar 0.7% M/M-pace in July to flat price growth in August (vs +0.2% consensus) with the Y/Y-number falling back in the tolerance band around the central bank’s 3% inflation target (3.4% Y/Y from 4.1% vs 3.6% consensus). Details showed stable food prices in August while services prices rose by 0.4% and rents by 0.9%. Prices for clothing and footwear and for electricity, gas and other fuels, fell. It’s welcome news for the central bank who skipped a rate cut in August, hoping to find the right settings in September. Inflation developments, the reaction function of the Fed/ECB and risk perception (HUF) are key in the decision making process. Only the latter is becoming an issue in continuing the cutting cycle with EUR/HUF yesterday spiking to 397 on reports that PM Orban intends to raise spending going into 2026 elections, potentially derailing public finances.

Graphs

EUR/CZK: Czech crown attempt to strengthen beyond 25 fails as higher-than-expected inflation had no strong enough legs

EUR/HUF: forint is trying to look for a bottom after a recent drop amid resurgent fiscal spending worries

Italian 30-yr yield nearing the lower bound of a sideways trading range. Today’s auction drew record demand

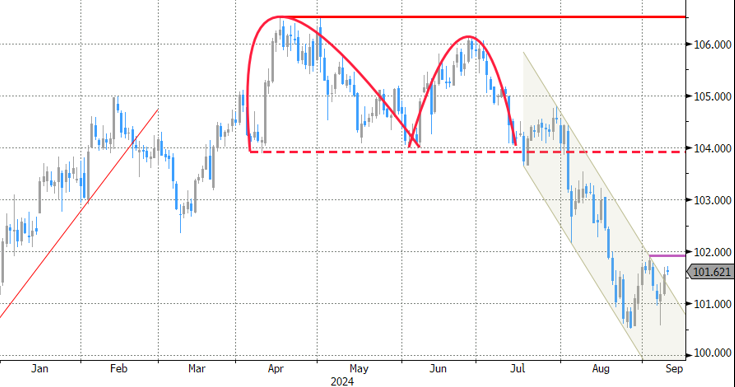

DXY has set its sights on first resistance around 102. Will inflation numbers tomorrow do the trick?

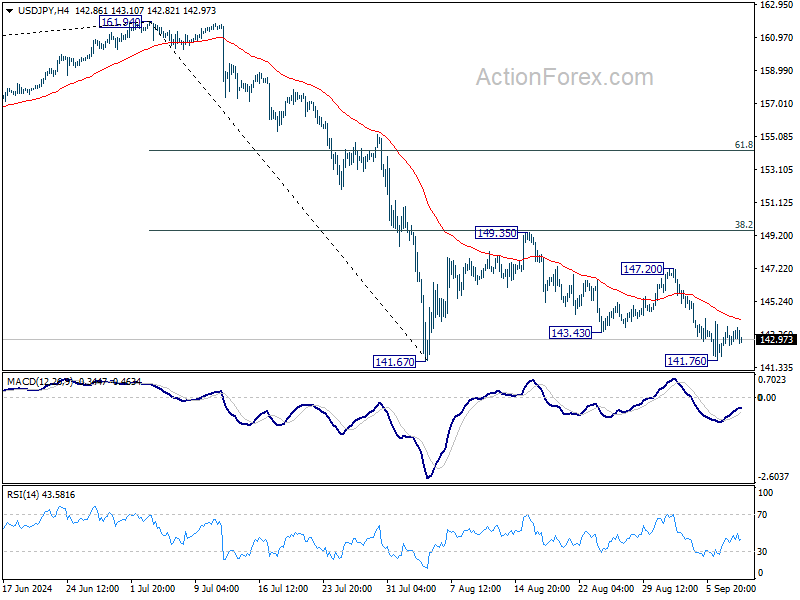

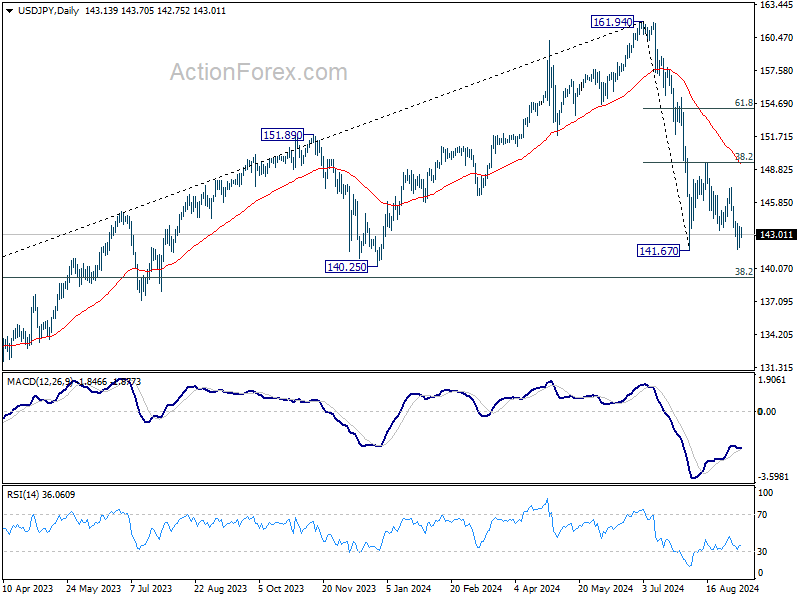

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.15; (P) 142.97; (R1) 144.00; More...

Range trading continues in USD/JPY and intraday bias stays neutral for the moment. Further decline is expected as long as 147.20 resistance holds. On the downside, decisive break of 141.67 will resume whole decline from 161.95 high. Next target will be 140.25 support.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.21) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

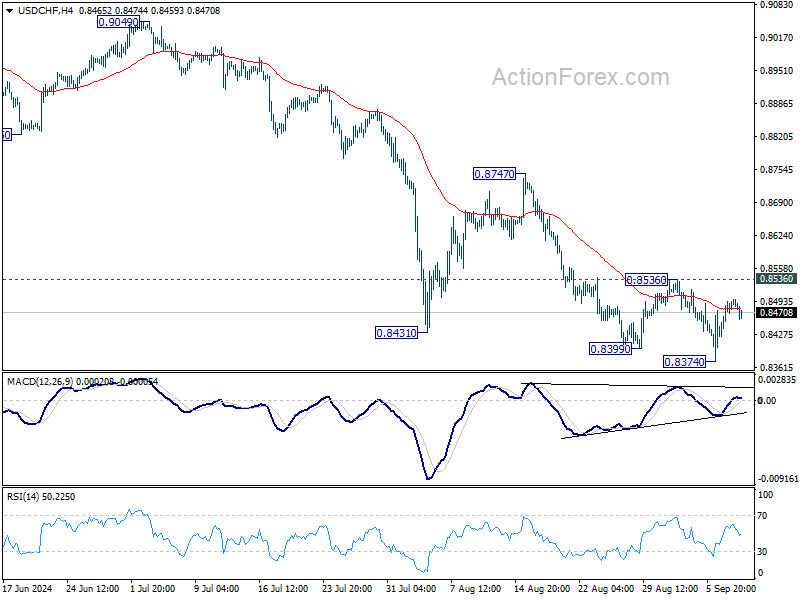

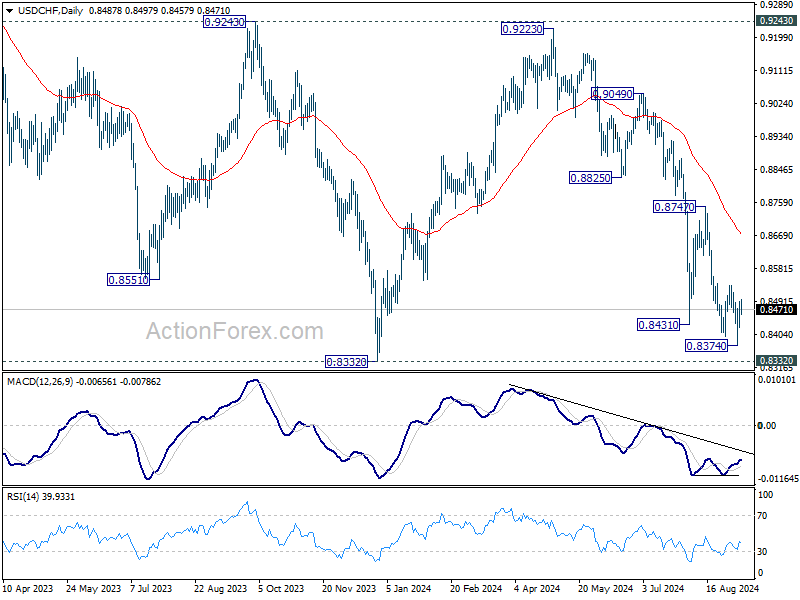

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8449; (P) 0.8472; (R1) 0.8517; More…

Intraday bias in USD/CHF stays neutral and more consolidations could be seen above 0.8374. With 0.8356 resistance intact, further decline is expected. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8536 resistance will now confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

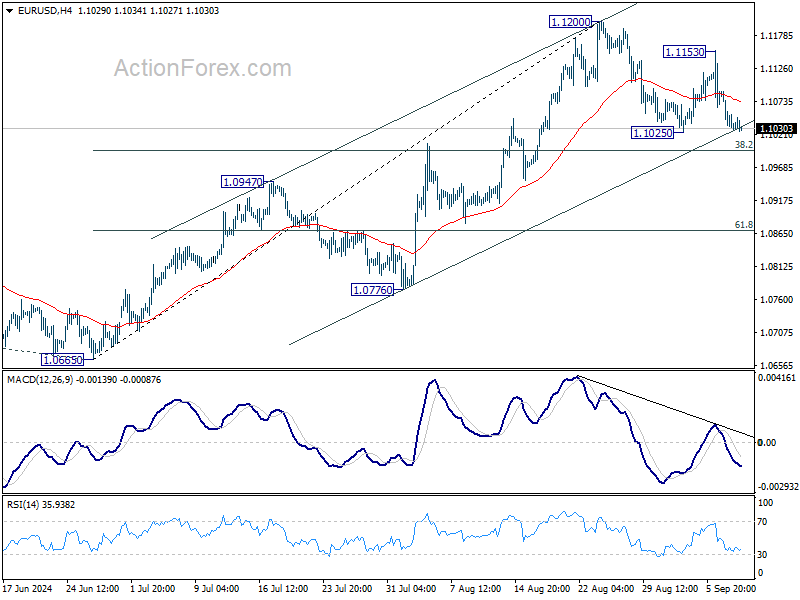

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1016; (P) 1.1053; (R1) 1.1073; More....

Outlook in EUR/USD remains unchanged and intraday bias stays neutral. Consolidation from 1.1200 could extend with deeper pull back, but downside should be contained by 38.2% retracement of 1.0665 to 1.1200 at 1.0996 to bring rebound. Break of 1.1200 will resume larger rise towards 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

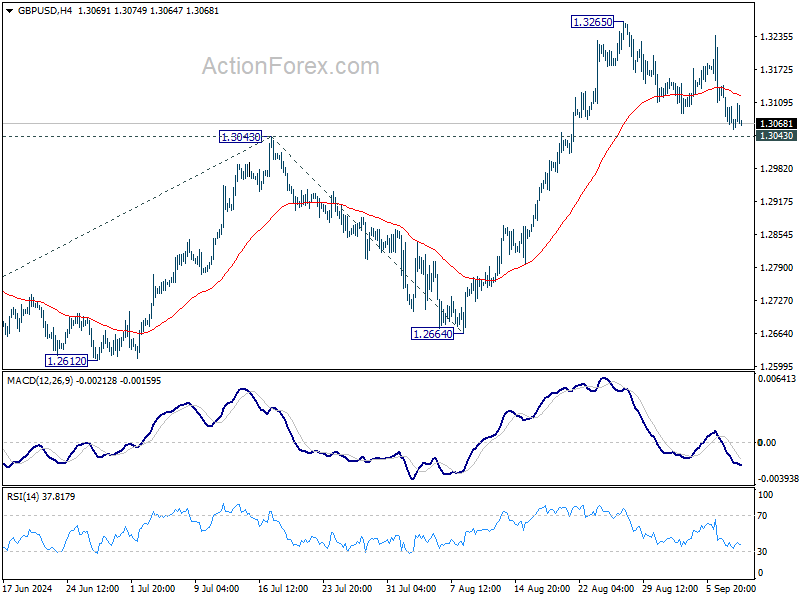

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3046; (P) 1.3095; (R1) 1.3121; More...

No change in GBP/USD's outlook and intraday bias remains neutral. Further rise is expected with 1.3043 resistance turned support intact. On the upside, firm break of 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Sterling Briefly Lifted by UK Jobs Data, But Forex Markets Remain Subdued

Trading in the forex markets remained relatively subdued today, with limited momentum across major pairs. Sterling saw a brief uptick following robust UK employment data, but the rally quickly lost steam. The data did little to alter expectations that BoE will likely keep rates unchanged next week and wait until November to reassess its stance. However, upcoming key releases, including tomorrow’s GDP data and next week's inflation figures, could still shift market expectations.

Elsewhere, Swiss Franc and Yen are regaining some strength today as recent pullbacks stall. Both currencies remain in a consolidative phase, with traders awaiting further cues from broader risk sentiment. On the weaker side, Canadian Dollar is the worst performer for the day, followed by Euro and Sterling, while Dollar and Australian Dollar are holding a middle ground.

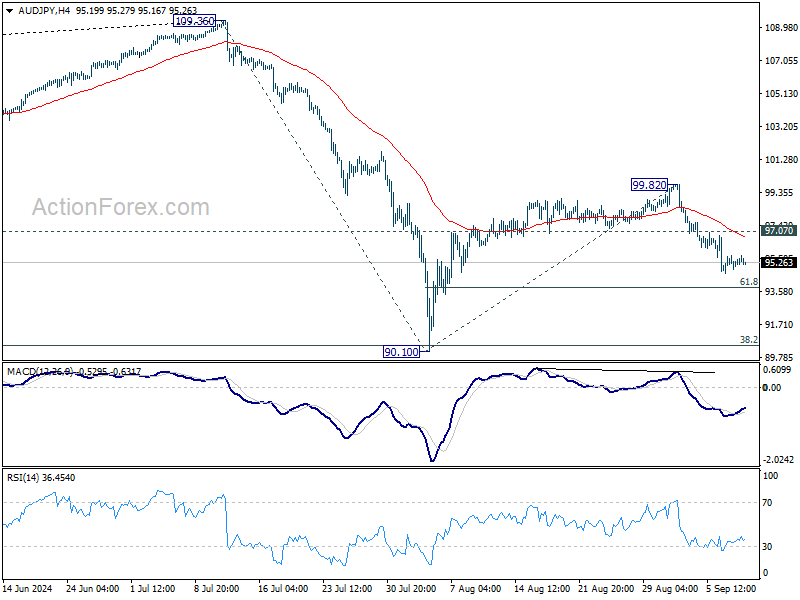

Technically, AUD/JPY turned into sideway trading this week but lacks momentum for a solid recovery. Rise from 90.10 has likely completed at 99.82 already. Deeper fall remains in favor as long as 97.07 resistance holds, for 61.8% retracement of 90.10 to 99.82 at 93.81. Decisive break there will raise the chance of resumption of whole fall from 109.36, and target 90.10 low next.

In Europe at the time of writing, FTSE is down -0.25%. DAX is down -0.46%. CAC is up 0.16%. UK 10-year yield is up 0.0023 at 3.864. Germany 10-year yield is up 0.0106 at 2.181. Earlier in Asia, Nikkei fell -0.16%. Hong Kong HSI rose 0.22%. China Shanghai SSE rose 0.28%. Singapore Strait Times rose 0.46%. Japan 10-year JGB yield fell -0.0001 to 0.895.

BoC Governor Macklem warns of persistent inflation pressures amid global trade slowdown

BoC Governor Tiff Macklem in a speech today raised concerns about the long-term implications of slowing globalization on inflation, indicating that price pressures may remain elevated for some time. Macklem highlighted that "with globalization slowing, the cost of global goods may not decline to the same degree," which could result in upward pressure on inflation.

Macklem also pointed to the ongoing risks of trade disruptions, noting that such disruptions could increase the "variability" of inflation, making it harder to control price stability. He drew on lessons from the pandemic, emphasizing that supply shocks, especially when the economy is overheated, can have an outsized impact on inflation volatility.

The BoC governor acknowledged the challenges supply shocks present to central banks, stating that "monetary policy can’t stabilize growth and inflation at the same time." This, he added, requires central banks to focus on risk management, balancing the risks of rising inflation against the downside to economic growth.

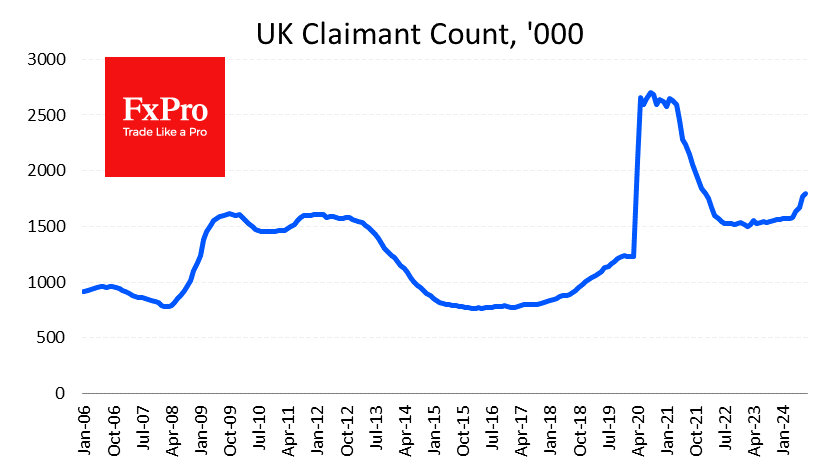

UK payrolled employment falls -59k in Aug, unemployment rate ticks down to 4.1% in Jul

In August, UK payrolled employees fell by -59k or -0.2% month-on-month, marking a significant contraction. Meanwhile, median monthly pay increased by 6.2% yoy, an acceleration from the previous month's 5.5%. Claimant count rose by 23.7k to 1.792m, below the expected 95.5k rise.

For the three months leading up to July, unemployment rate fell slightly from 4.2% to 4.1%, in line with expectations. Wage growth showed signs of further slowing, with regular earnings (excluding bonuses) rising by 5.1% yoy, down from 5.4%, matching market expectations. Total earnings, including bonuses, rose by 4.0% yoy, a deceleration from the previous month's 4.6%, and just below the forecast of 4.1%.

Australian Westpac consumer sentiment falls to 84.6, economic concerns deepen

Australia’s Westpac Consumer Sentiment Index saw a marginal decline of -0.5% mom in September, falling from 85.0 to 84.6, reflecting the ongoing pessimism that has gripped Australian consumers for more than two years. According to Westpac, this persistent negativity shows "no real signs of lifting," with key indicators pointing to growing anxiety about the country's economic outlook.

Sentiment around economic conditions for the next 12 months dropped from 83.3 to 81.2, while unemployment expectations rose sharply from 133.5 to 138.4, signaling growing concerns about job security. However, the interest rate expectations index saw some relief, falling from 135.5 to 123.8, as consumers became less worried about further rate hikes.

Westpac noted that the focus among consumers appears to be shifting. "While cost-of-living pressures are becoming a little less intense and fears of further interest rate rises have eased, consumers are becoming more concerned about where the economy may be headed and what this could mean for jobs," the report highlighted.

Australia's NAB business confidence falls to -4, conditions fairly clearly below average

Australia's NAB Business Confidence fell from 1 to -4 in August. Business Conditions also declined, dropping from 6 to 3. Trading conditions dipped by 2 points, while profitability slid by 1 point. Forward orders remained unchanged at -4.

NAB Chief Economist Alan Oster commented on the data, noting that "conditions are now fairly clearly below average compared to the history of the survey," underscoring the broader weakness in the private sector as the economy slows.

The decline in the employment gauge is particularly notable, as it "suggests the period of very strong private sector labor demand seen throughout the post-Covid period may be coming to an end," Oster added.

China's exports grow 8.7% yoy in Aug, imports up only 0.5% yoy

China's exports grew by a robust 8.7% yoy to USD 308.7B in August, surpassing market expectations of 6.5% yoy growth. However, this impressive figure is largely attributed to base effect, as exports contracted by -8.8% yoy during the same period last year.

Exports to key regions such as the US, the EU, and the ASEAN all posted solid gains. Notably, exports to the EU saw the largest increase, growing 13% yoy.

In terms of imports, China's intake from the US rose by 12% yoy, while imports from the EU showed a decline. Imports from ASEAN grew by 5% yoy. Overall import growth remained weak, increasing by just 0.5% yoy compared to the expected 2.0% yoy.

China's trade surplus widened significantly, rising from USD 84.65B in July to USD 91.02B, exceeding expectation of USD 83.9B.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3046; (P) 1.3095; (R1) 1.3121; More...

No change in GBP/USD's outlook and intraday bias remains neutral. Further rise is expected with 1.3043 resistance turned support intact. On the upside, firm break of 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q2 | 0.10% | 0.70% | 0.80% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Aug | 1.30% | 1.50% | 1.40% | |

| 00:30 | AUD | Westpac Consumer Confidence Sep | -0.50% | 2.80% | ||

| 01:30 | AUD | NAB Business Conditions Aug | 3 | 6 | ||

| 01:30 | AUD | NAB Business Confidence Aug | -4 | 1 | ||

| 03:00 | CNY | Trade Balance (USD) Aug | 91.0B | 82.1B | 84.7B | |

| 06:00 | GBP | Claimant Count Change Aug | 23.7K | 95.5K | 135K | 102.3K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | 4.10% | 4.10% | 4.20% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | 4.00% | 4.10% | 4.50% | 4.60% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 5.10% | 5.10% | 5.40% | |

| 06:00 | EUR | Germany CPI M/M Aug F | -0.10% | -0.10% | -0.10% | |

| 06:00 | EUR | Germany CPI Y/Y Aug F | 1.90% | 1.90% | 1.90% | |

| 08:00 | EUR | Italy Industrial Output M/M Jul | -0.90% | -0.10% | 0.50% | |

| 10:00 | USD | NFIB Business Optimism Index Aug | 91.2 | 93.6 | 93.7 |

BoC Governor Macklem warns of persistent inflation pressures amid global trade slowdown

BoC Governor Tiff Macklem in a speech today raised concerns about the long-term implications of slowing globalization on inflation, indicating that price pressures may remain elevated for some time. Macklem highlighted that "with globalization slowing, the cost of global goods may not decline to the same degree," which could result in upward pressure on inflation.

Macklem also pointed to the ongoing risks of trade disruptions, noting that such disruptions could increase the "variability" of inflation, making it harder to control price stability. He drew on lessons from the pandemic, emphasizing that supply shocks, especially when the economy is overheated, can have an outsized impact on inflation volatility.

The BoC governor acknowledged the challenges supply shocks present to central banks, stating that "monetary policy can’t stabilize growth and inflation at the same time." This, he added, requires central banks to focus on risk management, balancing the risks of rising inflation against the downside to economic growth.

UK Job Market Stronger Than Expected But Weaker Than US

In the UK, jobless claims rose by 23.7K in August, much better than the 95.5K expected and the 102.3K rise in the previous month. This is relatively positive data as it suggests that the rate of deterioration in the UK labour market is slowing. However, this is still the fastest claims growth since the unemployment spike in 2020 and the 2008 financial crisis.

At the same time, wage growth continues to slow, rising by 4% year on year in the three months to July. This is a sharp slowdown from 4.6% in the previous month and 5.7% two months ago, although wage growth is still above inflation at 2.2% year-on-year.

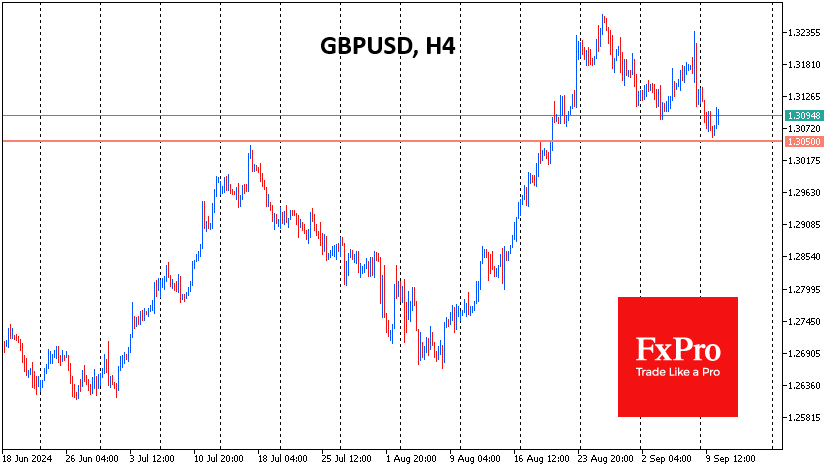

The data did not change the expectations of market analysts, who still do not expect a rate change next week but are forecasting a rate cut in November. The employment data temporarily supported the Pound as speculators played up the positive gap between expectations and reality. GBPUSD found support on Tuesday on the drop to the 1.3050 level, which looks like a bullish attempt to end the corrective pullback and take the Pound into a new round of growth.

While it is wise to wait for tomorrow’s UK CPI figures, which will be released on Wednesday morning, the main movement may be delayed until similar statistics are released from the US. For now, we can only compare labour market figures, and the US figures look stronger. This gives the Bank of England a greater degree of urgency to ease policy than the US, creating bearish risks for GBPUSD.