Sample Category Title

UK payrolled employment falls -59k in Aug, unemployment rate ticks down to 4.1% in Jul

In August, UK payrolled employees fell by -59k or -0.2% month-on-month, marking a significant contraction. Meanwhile, median monthly pay increased by 6.2% yoy, an acceleration from the previous month's 5.5%. Claimant count rose by 23.7k to 1.792m, below the expected 95.5k rise.

For the three months leading up to July, unemployment rate fell slightly from 4.2% to 4.1%, in line with expectations. Wage growth showed signs of further slowing, with regular earnings (excluding bonuses) rising by 5.1% yoy, down from 5.4%, matching market expectations. Total earnings, including bonuses, rose by 4.0% yoy, a deceleration from the previous month's 4.6%, and just below the forecast of 4.1%.

The Debate

The European and US indices rebounded on Monday, though the rebound was probably not based on high conviction, but looked more like the correction of last week’s decent selloff.

The European Stoxx 600 rebounded to flirt with the 50-DMA resistance, but the investor confidence index unexpectedly worsened in September, the British FTSE 100 recorded the best performance among the major European indices on Monday, but the energy and mining heavy FTSE 100 investors don’t sleep on their both ears given the selling pressure in energy and commodities that is backed by slowing China, and slowing global growth worries beyond China. Iron ore prices for example have now hit the lowest levels in almost two years, copper futures remain comfortably in the negative trend building since May peak, US crude has slipped below the $70pb last week on ample end-of summer driving season supply and growing demand worries (yes, yes also due to China) and Brent crude could soon join its US peer below the $70pb mark.

Consequently, Rio Tinto and Glencore in the FTSE 100 are among the worse performers of the index so far this year, while BP sank to the lowest levels in almost two years. So, yes, the FTSE 100’s ytd performance isn’t bad thanks to aerospace and defense companies. But the global growth concerns and gloomy outlook will likely limit the FTSE 100’s upside potential.

FTSE futures are in the negative at the time of writing.

In the US, the 2-year yield consolidated below the 3.70% level, but the US dollar index rebounded ahead of Wednesday’s CPI data – that will certainly not change the expectation of a 25bp cut from the Federal Reserve (Fed) at next week’s policy meeting, but that could – if significantly different than expectations – revive or temper the dovish Fed expectations for the rest of the year. The EURUSD extended losses to 1.1040 on rising dovish bets into Thursday’s European Central Bank (ECB) meeting, while the USDJPY rebounded from August lows.

Meh...

Apple closed nearly flat after revealing its new products yesterday. Apple Intelligence failed to impress. Many investors think that the AI capabilities remain relatively weak and can’t trigger a massive surge in new product sales, even less so as these features will be gradually updated and won’t even be available at the products’ launch date. As a result, Apple plunged as much as 1.5% during the event and closed the session slightly in the positive.

Trump vs Harris

Market’s attention will shift to politics as Donald Trump and Kamala Harris will face off in a debate today. We already mentioned that a Trump win would benefit Big Oil companies, small domestic businesses and cryptocurrencies. If we do the same exercise for Kamala Harris, a Harris win would support the ESG and green focused companies, healthcare, infrastructure and technology as she puts a particular emphasis on sustainable and inclusive growth.

Harris and Trump in Their First Face-Pff

In focus today

In the US, we get the NFIB Small Business Survey. Also, Fed Governor Barr is expected to announce a reduction in the biggest banks' capital hike in the latest Basel plan, from 19% to 9%, according to Bloomberg. Later, Kamala Harris and Donald Trump will have their first live debate at 9 pm ET, which could shift momentum in the still-open race. Read more on US politics in the US Election Monitor - Latest data shows Harris in a narrow lead, 6 September.

In Germany, the final August inflation data will be published, providing insight into inflation drivers, especially the 'LIMI' indicator of domestic inflation.

In the UK, the labour market report for July/August will be released at 8:00 CET. A range of indicators point to a gradually loosening labour market, and we expect this to be increasingly reflected in the official data.

In Norway, August inflation data is released, where we expect core inflation at 3.0 % y/y. The figure will be negatively affected by a reduction in maximum kindergarden prices from 1 August. Statistics Norway will publish a core figure adjusted for this, which we estimate to 3.2 % y/y, compared to Norges Bank's estimate of 3.6% y/y from the June MPR. In general, we expect a broad-based decline in price pressures, with a particular focus on domestic service price inflation.

In Sweden, July activity data will be released at 8:00 CET, including industrial production, household consumption, industrial orders, and the GDP indicator. While the latter should be viewed cautiously amid the prediction capability, it provides an initial gauge for Q3 GDP. In the afternoon, the ceremonial opening of the parliament takes place, where the PM will present the government declaration and his new government.

Economic and market news

What happened overnight

In China, trade data for August showed exports unexpectedly rising 8.7% y/y (cons: 6.5%), the fastest pace since March 2023, while imports were weaker than expected at 0.5% y/y (cons: 2.0%), reflecting soft domestic demand. Despite momentum fading recently amid a weaker global manufacturing sector, exports continue to be a key driver of the Chinese economy.

What happened yesterday

In the US, the NY Fed Survey of Consumer Expectations showed little change in inflation outlooks for August, with 1y and 5yr expectations remained unchanged at 3% and 2.8%, respectively. The 3y outlook edged up to 2.5% from 2.3% in July.

In the euro area, the Sentix index was weaker than expected at -15.4 (cons: -12.5). The reading was the third straight month with deteriorating investor sentiment, primarily due to the frail German economy.

Former ECB president, Mario Draghi, presented his report on EU competitiveness, calling for a "new industrial strategy for Europe". He recommends raising EU investments by EUR 750-800bn annually to fund reforms to stop the EU from falling behind China and the US. While Draghi has no formal legislative power in the EU, the report serves as an expert input for EU lawmakers, with some of the measures already spelled out in EC President Ursula von der Leyen's new political guidelines. However, significant initiatives that could really boost the Unition are less likely due to the political landscape and budgetary problems.

Equities: Global equities were higher on Monday, following a significant sell-off last week. Most trends from last week were reversing, although they only reclaimed a minor part of the losses. Please note, bond yields were relatively flat and defensive stocks only marginally underperformed. In other words, there was nothing yesterday that suggested growth concerns have abated. In the US yesterday, Dow +1.2%, S&P 500 +1.2%, Nasdaq +1.2%, and Russell 2000 +0.3%. Asian markets are mixed this morning, as are US futures. Core European futures are marginally higher.

FI: Initially, global bond yields rose in Asian trading this morning, however at the end of the day, yields have declined and are back at the level from Friday with 10Y US Treasuries trading around the 3.70%-level, while 2Y US Treasuries are trading at 3.67%. In the European market, 10Y Bunds ended at 2.16%, so there is a bit of distance to the levels seen in January 2024, when 10Y Bunds were trading at the 2%-level. However, the curves have steepened since January as the market is pricing in more rate cuts compared to the pricing in January especially in the US, where the first move could be a 50bp rate cut on September 18 from the Federal Reserve. Today, the US Treasury will sell USD 58bn in a 3Y benchmark and given the solid demand for Treasuries it will be interesting to see the demand ahead of the FOMC meeting next week. The Treasury will also tap in the 10Y and 30Y segments on Wednesday and Thursday, respectively.

FX: The USD was the primary outperformer in the first session of the week which notably saw the Scandies trade poorly despite a recovery in risk sentiment.

UK Employment Data Takes Center Stage Amid Market Caution

The forex markets have remained largely subdued in today's Asian session, with most major currency pairs moving within a narrow range from yesterday. Investor sentiment stabilized overnight, with major US stock indexes closing higher. However, caution is still the prevailing mood as traders await tomorrow's US CPI data, which will be pivotal in shaping Fed's next move. The inflation data will likely be the key determinant in whether Fed opts for a modest 25bps rate cut or a more aggressive 50bps cut at its upcoming meeting.

Earlier today, Australian data had little impact on market sentiment. Consumer confidence in Australia continues to linger at low levels, a trend that has persisted for over two years. Business confidence, meanwhile, has turned negative, signaling rising concerns about the economic outlook. These concerns suggest that RBA's restrictive policies are cooling the economy as intended, but there is little to suggest that the central bank will bring forward its policy easing cycle, which is supposed to begin next year.

Looking ahead, the spotlight is now on the UK, where employment data is due for release. BoE is expected to take a measured approach to rate cuts, with many analysts believing that next week's BoE meeting may be too early for another rate reduction. However, this cautious stance depends heavily on no major negative surprises in today's job data, tomorrow's GDP figures, and next week's CPI report.

For the week so far, Loonie is leading the pack as the strongest performer, followed by Aussie and then Dollar. At the other end, Swiss Franc is the weakest, with Yen and Kiwi also under pressure. Euro and Sterling are positioned in the middle.

Technically, GBP/AUD's pullback from 2.0034 could have completed at 1.9276 already. Multiple support from 55 D EMA is a near term bullish sign too. Further rise is now expected to retest 2.0034 first. Firm break there will resume larger rally. However, break of 1.9536 will suggest that correction from 2.0034 is probably extending with another falling leg through 1.9276.

In Asia, at the time of writing, Nikkei is up 0.08%. Hong Kong HSI is up 0.28%. China Shanghai SSE is up 0.28%. Singapore Strait Times is up 0.38%. Japan 10-year JGB yield is down -0.0001 at 0.895. Overnight, DOW rose 1.20%. S&P 500 rose 1.16%. NASDAQ rose 1.16%. 10-year yield fell -0.013 to 3.697.

Australian Westpac consumer sentiment falls to 84.6, economic concerns deepen

Australia's Westpac Consumer Sentiment Index saw a marginal decline of -0.5% mom in September, falling from 85.0 to 84.6, reflecting the ongoing pessimism that has gripped Australian consumers for more than two years. According to Westpac, this persistent negativity shows "no real signs of lifting," with key indicators pointing to growing anxiety about the country's economic outlook.

Sentiment around economic conditions for the next 12 months dropped from 83.3 to 81.2, while unemployment expectations rose sharply from 133.5 to 138.4, signaling growing concerns about job security. However, the interest rate expectations index saw some relief, falling from 135.5 to 123.8, as consumers became less worried about further rate hikes.

Westpac noted that the focus among consumers appears to be shifting. "While cost-of-living pressures are becoming a little less intense and fears of further interest rate rises have eased, consumers are becoming more concerned about where the economy may be headed and what this could mean for jobs," the report highlighted.

Australia's NAB business confidence falls to -4, conditions fairly clearly below average

Australia's NAB Business Confidence fell from 1 to -4 in August. Business Conditions also declined, dropping from 6 to 3. Trading conditions dipped by 2 points, while profitability slid by 1 point. Forward orders remained unchanged at -4.

NAB Chief Economist Alan Oster commented on the data, noting that "conditions are now fairly clearly below average compared to the history of the survey," underscoring the broader weakness in the private sector as the economy slows.

The decline in the employment gauge is particularly notable, as it "suggests the period of very strong private sector labor demand seen throughout the post-Covid period may be coming to an end," Oster added.

China's exports grow 8.7% yoy in Aug, imports up only 0.5% yoy

China's exports grew by a robust 8.7% yoy to USD 308.7B in August, surpassing market expectations of 6.5% yoy growth. However, this impressive figure is largely attributed to base effect, as exports contracted by -8.8% yoy during the same period last year.

Exports to key regions such as the US, the EU, and the ASEAN all posted solid gains. Notably, exports to the EU saw the largest increase, growing 13% yoy.

In terms of imports, China's intake from the US rose by 12% yoy, while imports from the EU showed a decline. Imports from ASEAN grew by 5% yoy. Overall import growth remained weak, increasing by just 0.5% yoy compared to the expected 2.0% yoy.

China's trade surplus widened significantly, rising from USD 84.65B in July to USD 91.02B, exceeding expectation of USD 83.9B.

Looking ahead

UK employment data is the key focus in European session today. The US calendar is empty.

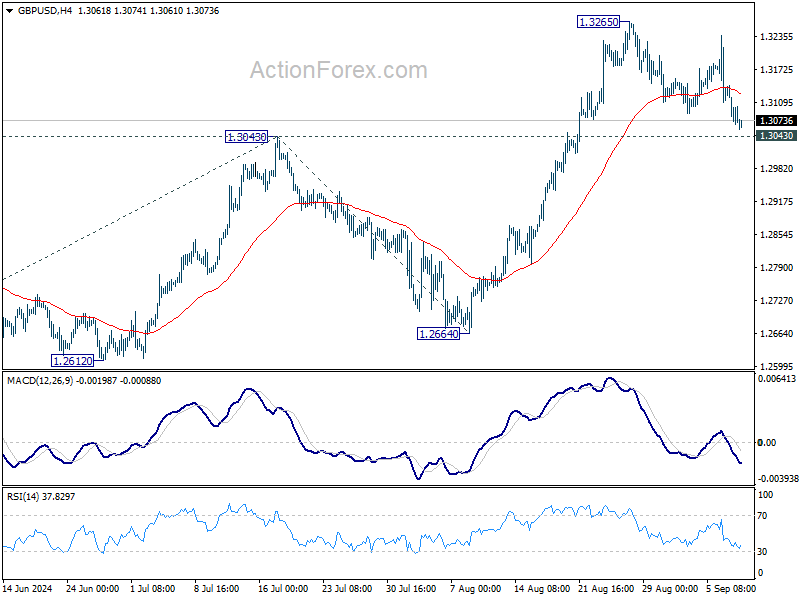

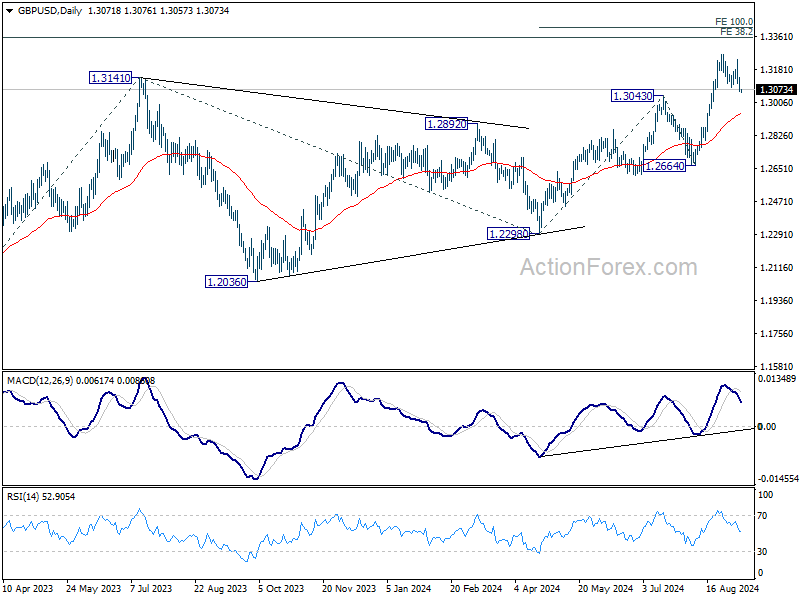

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3046; (P) 1.3095; (R1) 1.3121; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. Further rise is expected with 1.3043 resistance turned support intact. On the upside, firm break of 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Manufacturing Sales Q2 | 0.10% | 0.70% | 0.80% | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Aug | 1.30% | 1.50% | 1.40% | |

| 00:30 | AUD | Westpac Consumer Confidence Sep | -0.50% | 2.80% | ||

| 01:30 | AUD | NAB Business Conditions Aug | 3 | 6 | ||

| 01:30 | AUD | NAB Business Confidence Aug | -4 | 1 | ||

| 03:00 | CNY | Trade Balance (USD) Aug | 91.0B | 82.1B | 84.7B | |

| 06:00 | GBP | Claimant Count Change Aug | 95.5K | 135K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jul | 4.10% | 4.20% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jul | 4.10% | 4.50% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jul | 5.10% | 5.40% | ||

| 06:00 | EUR | Germany CPI M/M Aug F | -0.10% | -0.10% | ||

| 06:00 | EUR | GermanyCPI Y/Y Aug F | 1.90% | 1.90% | ||

| 08:00 | EUR | Italy Industrial Output M/M Jul | -0.10% | 0.50% | ||

| 10:00 | USD | NFIB Business Optimism Index Aug | 93.6 | 93.7 |

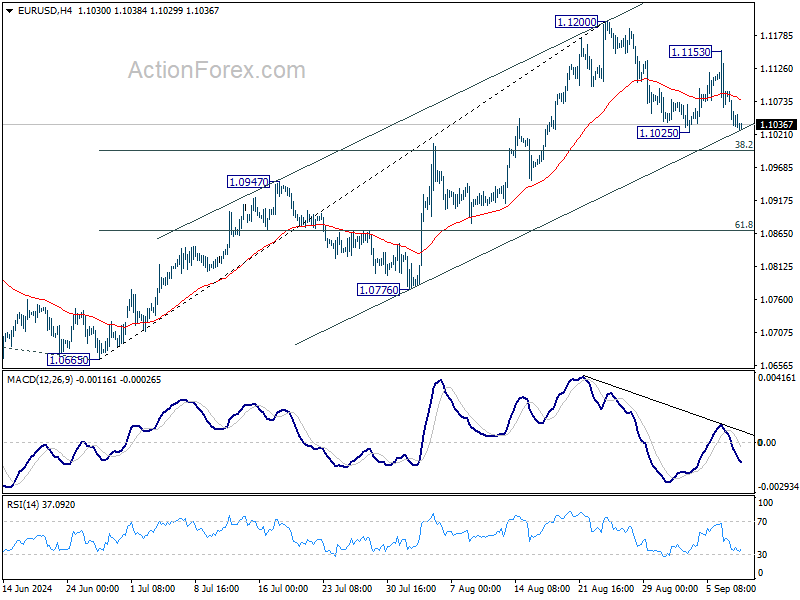

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1016; (P) 1.1053; (R1) 1.1073; More....

Intraday bias in EUR/USD remains neutral at this point. Consolidation from 1.1200 could extend with deeper pull back, but downside should be contained by 38.2% retracement of 1.0665 to 1.1200 at 1.0996 to bring rebound. Break of 1.1200 will resume larger rise towards 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

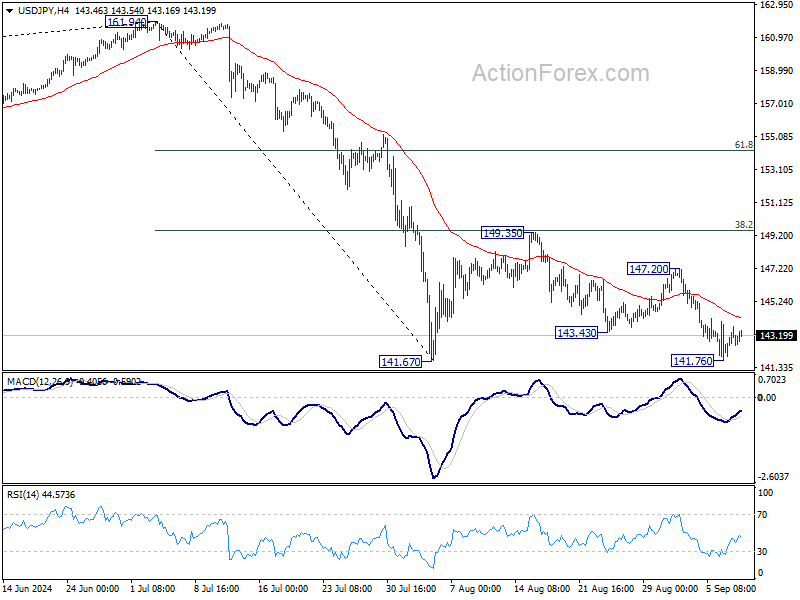

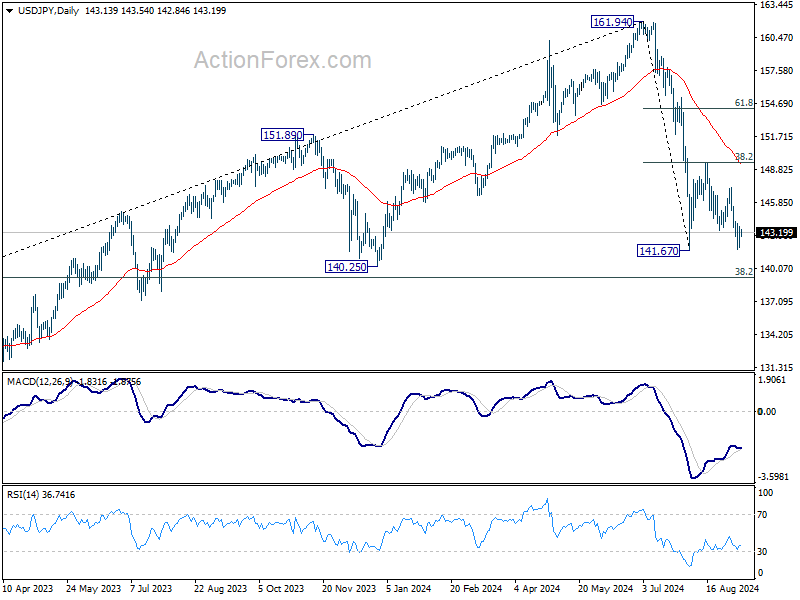

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.15; (P) 142.97; (R1) 144.00; More...

Intraday bias in USD/JPY remains neutral for the moment. Further decline is expected as long as 147.20 resistance holds. On the downside, decisive break of 141.67 will resume whole decline from 161.95 high. Next target will be 140.25 support.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.21) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3046; (P) 1.3095; (R1) 1.3121; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. Further rise is expected with 1.3043 resistance turned support intact. On the upside, firm break of 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

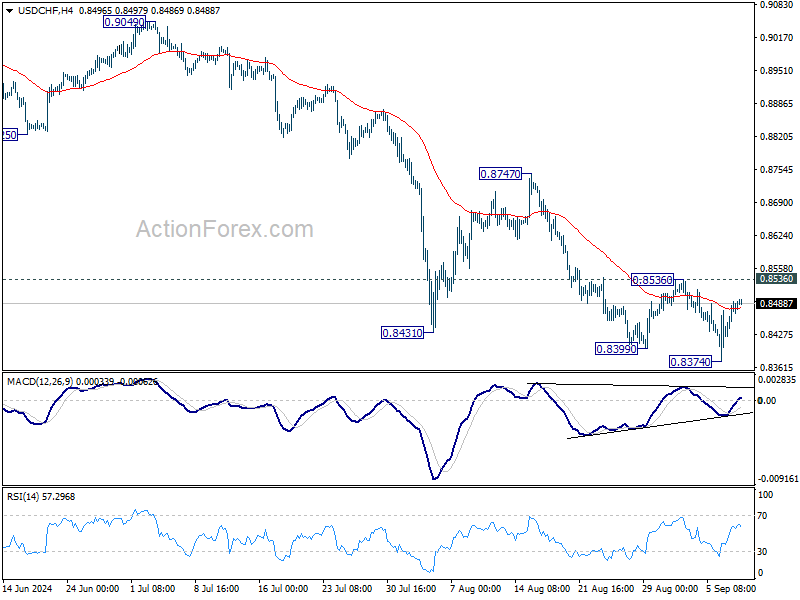

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8449; (P) 0.8472; (R1) 0.8517; More…

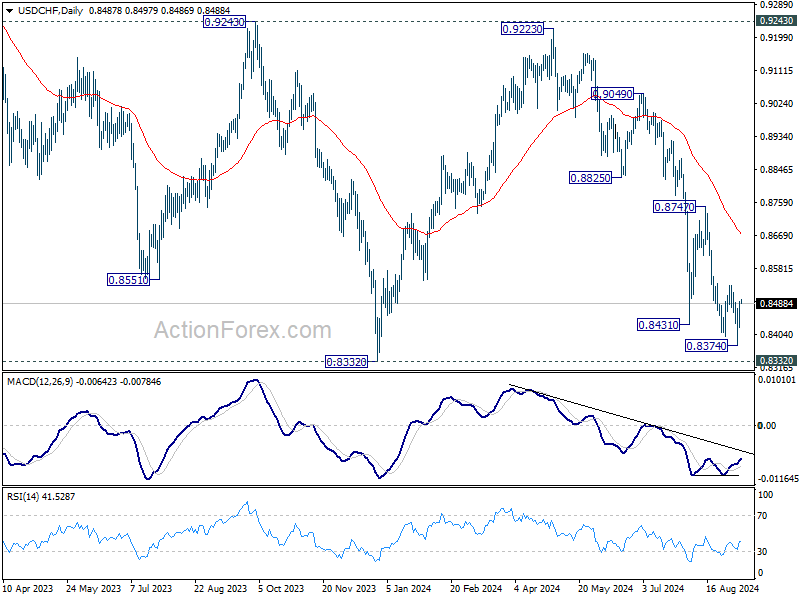

No change in USD/CHF's outlook and intraday bias stays neutral. With 0.8356 resistance intact, further decline is expected. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8536 resistance will now confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

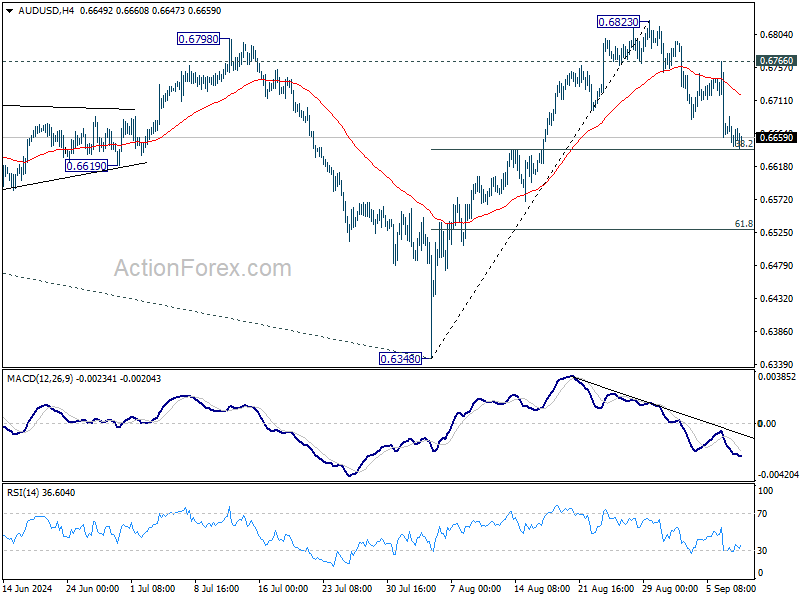

AUD/USD Daily Report

Daily Pivots: (S1) 0.6643; (P) 0.6666; (R1) 0.6684; More...

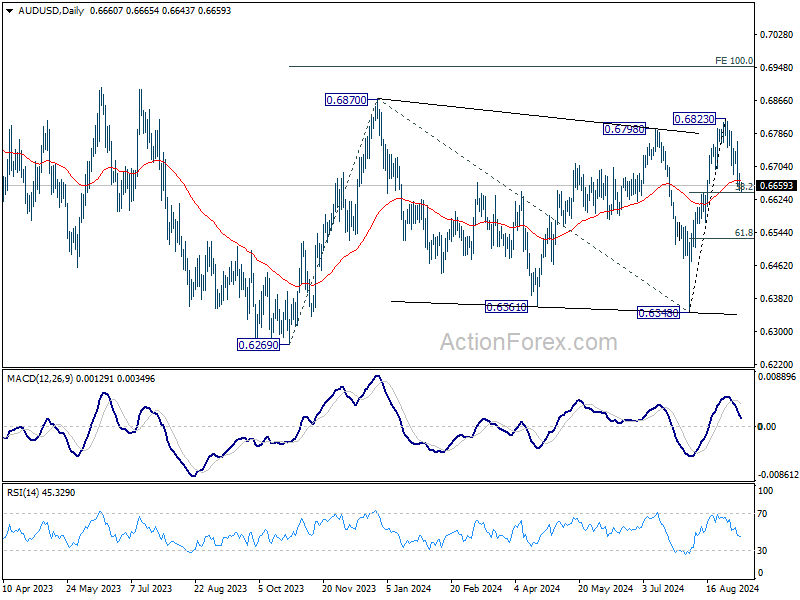

AUD/USD's fall from 0.6823 short term top is still in progress and intraday bias stays on the downside. Decisive break of 38.2% retracement of 0.6348 to 0.6823 at 0.6642 will target 61.8% retracement at 0.6529. On the upside, though, above 0.6766 resistance will bring retest of 0.6823 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

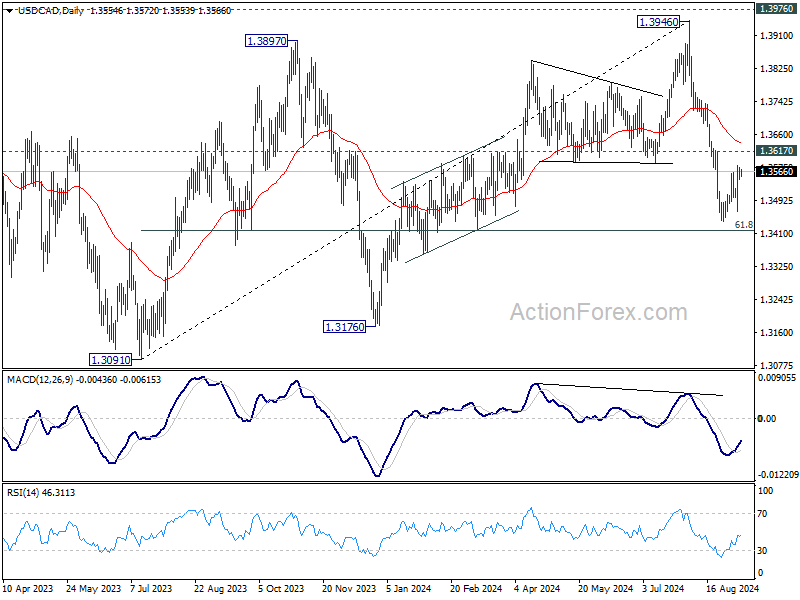

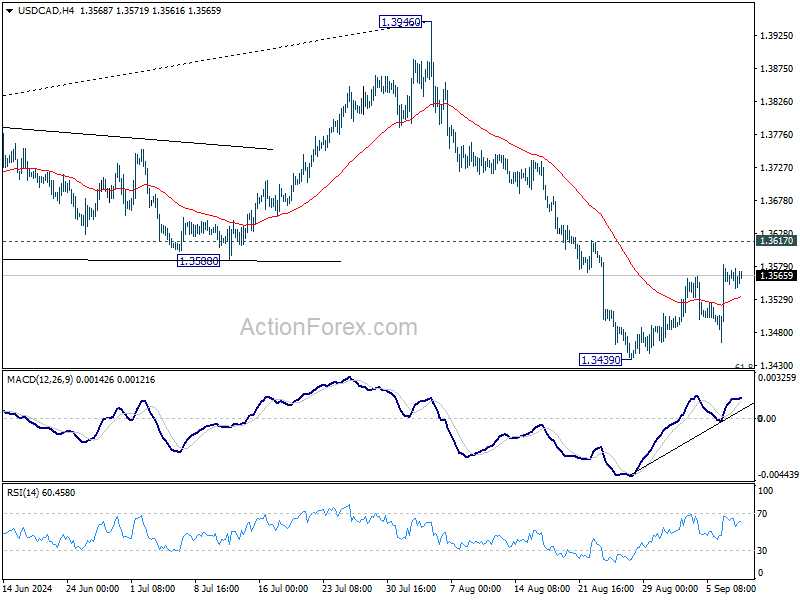

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3544; (P) 1.3561; (R1) 1.3575; More...

USD/CAD is extending consolidation form 1.3439 and intraday bias remains neutral. While stronger recovery cannot be ruled out, further decline will remain in favor as long as 1.3617 resistance holds. On the downside, break of 1.3439 and sustained trading below 61.8% retracement of 1.3091 to 1.3946 at 1.3418 will pave the way to 1.3091/3176 support zone next. However, firm break of 1.3617 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, current development suggests that corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.