Sample Category Title

US: Small Business Optimism Pulls Back in August

NFIB's Small Business Optimism Index fell 2.5 points to 91.2 in August, coming in below market expectations calling for a flat print.

Eight of the ten subcomponents fell on the month, while only two improved. Large declines were recorded in expectations regarding higher real sales (-9 points to -18%), earnings trends (-7 points to -37%) and expectations about an improvement in the economy (-6 points to -13%). Plans to increase inventories also pulled back 3 points to -1%.

Labor market indicators were mixed. The share of businesses planning to increase employment fell 2 points to 13% in August. On the other hand, the share of firms with unfilled job openings rose 2 points to 40%. Quality of labor concerns trended higher, with 21% of business owners (up 2 points on the month) identifying this as their top business problem. Inflation concerns continued to top the list, with 24% of owners identifying this as their top business problem (down 1 point from July).

The share of firms increasing employee compensation held steady at 33%, while the share firms planning to do so in the months ahead rebounded by 2 points to 20%. Both of these measures are at or near their respective post-pandemic lows. Moving over to pricing metrics, the share of businesses 'raising' average selling prices fell 2 points to 20%, while the share of those 'planning’ to raise average selling prices ahead ticked up 1 point to 25%.

Key Implications

Small business confidence retreated in August, fully erasing the improvement made in the month prior. The decline reflected a worsening in earning trends, along with a deterioration in expectations for future sales and business conditions. With the election at our doorstep, uncertainly among small business owners has been rising, with the corresponding subindex increasing further in August to a level that's now rivalling the highs experienced during the onset of the pandemic and those just prior to the 2016 election.

The U.S. labor market is cooling and small business data is partially playing the same tune, with plans to increase employment losing some steam at the end of summer. At the same time, small business job openings have held up recently and labor quality concerns remain elevated. But, despite the latter, businesses are not splurging on wage increases to the same degree that they were earlier in the pandemic. Easing wage metrics, together with more muted price plans add further credence to the view that inflation should continue to trend lower ahead.

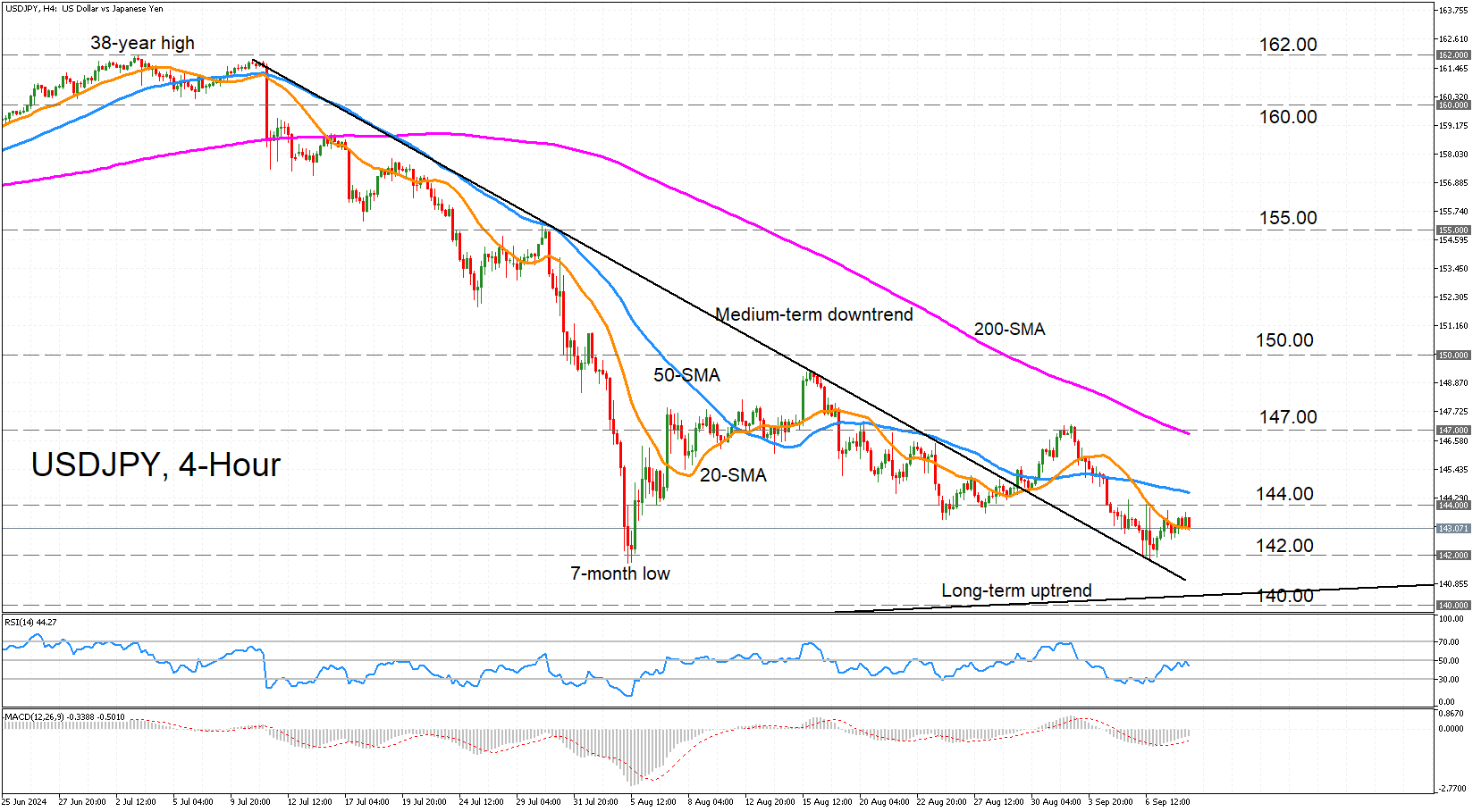

USDJPY Lacks Direction, Looks to US CPI

- USDJPY hovers around 20-period moving average (SMA)

- Some upside momentum still present

- Next move will likely depend on US CPI report

USDJPY is consolidating around its 20-period SMA after the rebound from the one-month low of 141.76 quickly ran out of steam. The RSI is fluctuating right beneath the 50-neutral mark, but the MACD continues to rise above its red signal line in the negative territory.

If the bulls manage to regain control, there’s likely to be a tough battle ahead as the 144.00 level is a short distance away and the 50-period SMA lies slightly higher around 144.50. A break above these obstacles is needed to set course for the 200-period SMA slightly below 147.00.

A climb higher would also take the price above the previous high from early September before the mid-August peak of 149.38 comes into view. After this, all eyes would turn to the 150 handle, which the bulls need to reclaim if they stand any chance of switching the negative medium-term trend to a more bullish one.

However, if the pair slips below its 20-period SMA, the 142.00 level could be tested again. Falling beneath this support barrier would risk a breach of the longer-term ascending trendline, after which there would be a danger of the price falling below 140.00, cementing the bearish structure.

For the moment, though, it’s a very neutral picture, which could last until Wednesday’s inflation report out of the United States at 12:30 GMT, with the data possibly determining the next direction.

AUD/USD Shrugs After Weak Confidence Data

The Australian dollar continues to have a quiet week. AUD/USD is trading at 0.6671 in the European session, up 0.17% today at the time of writing.

With the Australian economy sputtering, it should come as no surprise that today’s confidence indicators pointed downward. Westpac consumer confidence change declined 0.5% m/m in September, falling from 85.0 to 84.6. This was better than the forecast of -1.2% but points to pessimistic consumers who remain nervous about potential job losses in a weak economy.

The National Australia Bank business confidence index fell to -4 in August, its lowest level since November 2023. This followed back-to-back gains. Confidence was down across a range of sectors and business expectations also declined. Business confidence has been stronger than consumer sentiment this year but has now converged as both are showing deep pessimism about economic conditions.

The financial markets have been showing strong swings and the market pricing of a Federal Reserve rate cut are also moving wildly. After Friday’s lukewarm nonfarm payrolls report, the odds of a 50-basis point cut shot up to 59%, up from 43% before the release, according to CME’s FedWatch. That has plunged to just 27% on Tuesday, ahead of tomorrow’s CPI report. We could see the rate-cut odds continue to swing if inflation surprises the markets, which expect a 2.6% gain for August, down from 2.9% in the previous reading.

The Fed meets on Sept. 18 and is widely expected to deliver its first rate cut after a lengthy rate-hike cycle. Now that inflation is largely under control, the Fed is keeping a close eye on the US labor market as it tries to guide the economy to a soft landing. The labor market hasn’t crashed but recent nonfarm payrolls numbers indicate that the labor market is cooling and that could mean a series of rate cuts extending into 2025.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6666. Above, there is resistance at 0.6684

- 0.6643 and 0.6625 are the next support levels

GBP/USD Rises on Robust Labor Data – Challenges Ahead for the BoE

- UK labor data beats expectations, with regular pay rising by 5.1% and employment increasing by 265k.

- BoE faces challenges in balancing strong employment figures with moderating wage growth and rate cut hopes.

- US CPI and PPI, and BoE Deputy Governor Sarah Breeden’s comments, could impact GBP/USD’s trajectory.

The GBP benefitted following a positive UK labor data release this morning. Cable rallied around 30 pips following the data release but has since surrendered the post data gains.

The implications for the Bank of England (BoE) will be interesting as the Central Bank was already expected to cut rates less than peers at the ECB and Federal reserve. The strong employment numbers will no doubt raise inflation concerns however, the moderation in wage growth may be a point that keeps dovish MPC members on board regarding further rate cuts.

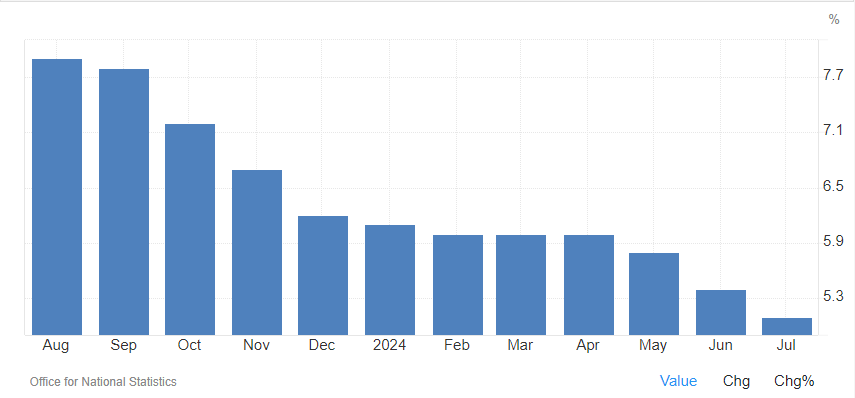

In the UK, regular pay, excluding bonuses, rose by 5.1% year-on-year to GBP 647 per week for the three months leading up to July 2024. This marks the smallest increase since June 2022 and follows a 5.4% rise in the prior period, aligning with market expectations. Wage growth decelerated in both the private sector, decreasing to 4.9% from 5.3%, and the public sector, dropping to 5.7% from 6%. The manufacturing sector experienced the highest annual regular wage increase at 5.9%, followed by the finance and business services sector at 5.4%, and the services sector at 5.1%.

UK Wage Growth YoY

Source: TradingEconomics, ONS

Employment increased by 265k smashing estimates of 115k which is the highest rise in employment over the past 18 months. The drop in unemployment to 4.1% is of course another positive for the UK economy but only compounds the headache facing the Bank of England (BoE).

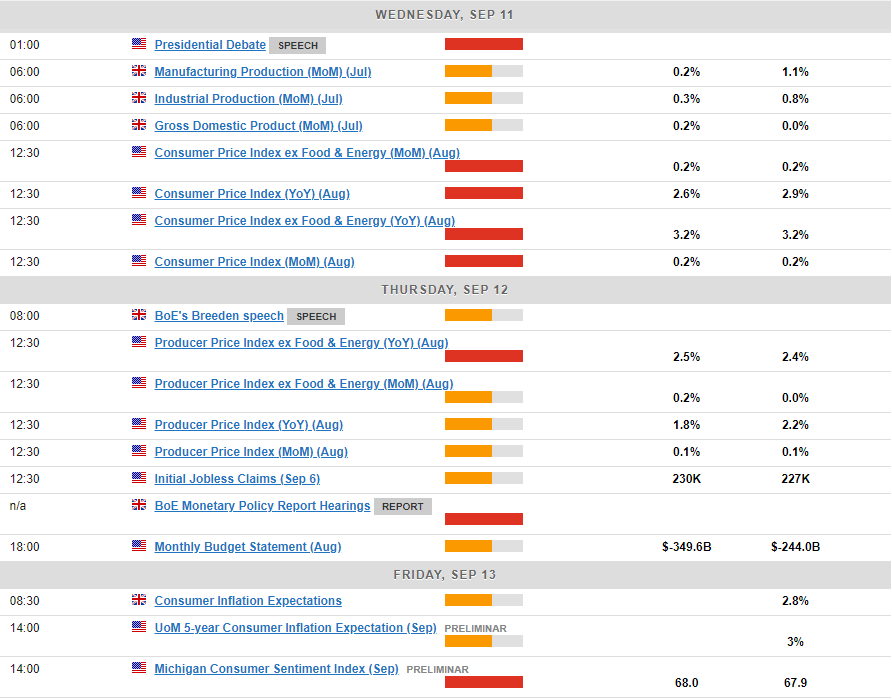

Economic Data Ahead

There is quite a bit of data ahead this week which could impact GBP/USD. The majority of the data comes from the US with CPI released tomorrow and of course PPI on Thursday.

However, I will be more interested in comments from BoE Deputy Governor Sarah Breeden. Given the labor data today it will be key to gauge where BoE policymakers stand regarding rate cuts moving forward. Any sign of diverging policy with the Federal Reserve could have medium to long-term implications for GBP/USD and could be key in where the pair may end up come year-end.

Technical Analysis

Looking at GBP/USD from a technical standpoint and the pair does look like a move lower may continue to unfold. Cable is on a two day losing streak having printed a lower high last week Friday at resistance around 1.3181.

One of the concerns for bears from a price action perspective is that a lower low has already been printed which could pave the way for a short-term pullback. This coupled with UK labor data earlier in the day could prompt some short-term buying pressure.

Looking at the downside and immediate support rests at the 1.3000 psychological level, although cable may find support at around the 1.30400 handle which was the July 17 high.

Conversely, a move higher here will first need to take out the current daily high around 1.3100 before the recent swing high at 1.3181 comes into focus.

GBP/USD Daily Chart, September 10, 2024

Source:TradingView.com

Support

- 1.3040

- 1.3000

- 1.2942

Resistance

- 1.3100

- 1.3181

- 1.3250

Analysis of GBP/USD Today: Bulls Face Challenges

UK labour market data was released today.

According to Dow Jones Newswires:

→ Employment growth exceeded expectations, and unemployment benefit claims came in lower than forecast. ING analysts believe this supports the view that the Bank of England will cut interest rates more cautiously compared to the Federal Reserve.

→ Capital Economics analysts also suggest that the Bank of England is unlikely to lower rates for a second consecutive month at next week’s policy meeting.

The initial reaction to the positive UK labour market news was a bullish impulse for the pound, with GBP/USD rising from around 1.3080 to break above 1.3100 shortly after the release.

However, the pair then retraced towards its “initial levels,” indicating that bulls are struggling to capitalise on the strong data. This could also signal the dominance of bears.

Technical analysis of GBP/USD today points to further bearish signals:

→ The price failed to stay above the previous high around 1.314.

→ A bearish engulfing pattern at the market’s peak (as shown by the first red arrow).

→ A long upper wick on the 6 September candlestick (as indicated by the second red arrow).

Bulls may find support (shown by the blue arrow) from the median of the linear regression channel (in blue). But is this enough to prevent GBP/USD from continuing the downward trend seen since late August and falling towards the channel’s lower boundary?

Much will depend on tomorrow's US inflation data. The Consumer Price Index (CPI) figures will be released at 15:30 GMT+3.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/USD: Faces Again Strong Headwinds at Pivotal Fibo Support

EURUSD is pressuring pivotal support at 1.1040 (Fibo 38.2% of 1.0781/1.1200 bull-leg), after facing several rejections at this level recently.

Tuesday’s action is so far holding in a narrow range, following a strong fall in past two days, with near-term bears hesitating here, due to mixed technical signals on 4-hr and daily chart.

Weaker German inflation in August may add to downside pressure, as well as wide expectations for ECB’s 0.25% rate cut on Thursday however, markets will be closely watching results of US Aug inflation report and signals of a size of Fed rate cut later this month, which will impact the dollar.

Break of 1.1040 pivot would risk test of 1.1000 zone (psychological / 50% retracement of 1.0781/1.1200) and possible extension towards 1.0971 (lower 20-d Bollinger band), which may contain dips.

Strong negative momentum on daily chart works in favor of such scenario, as recently formed 100/200DMA Golden cross adds support, along with rising daily Ichimoku cloud.

The second scenario sees repeated rejection at 1.1040 zone and further signals of formation of a base, although, lift and close above Friday’s peak (1.1065) will be required to confirm, and shift focus to the upside.

Res: 1.1065; 1.1091; 1.1107; 1.1155.

Sup: 1.1026; 1.1000; 1.0971; 1.0935.

Gold Coming Out of Elliott Wave Triangle

On a higher degree time frame, we see gold coming higher into a fifth wave, but it may take some time before it finds the top, as we see an unfinished lower degree impulse.

Gold remains in strong and impulsive five-wave bullish cycle on a daily chart and there's space for more upside, we will just have to be aware of a higher degree wave IV correction still this year, possibly in Q4. Why? Because we see a move out of a triangle here in fifth wave of III, so we know thats the final trust within higher degree extensions, meaning there can be limited upside in weeks ahead, ideally around 2600-2700 area.

https://www.youtube.com/watch?v=c0z1j56onSc

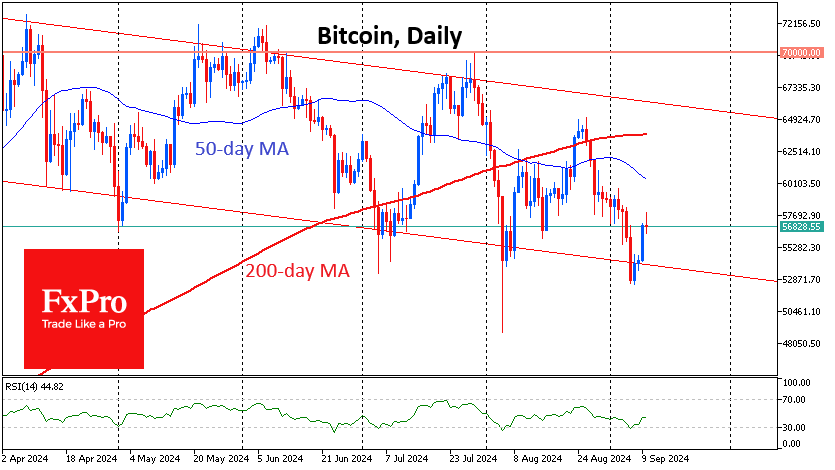

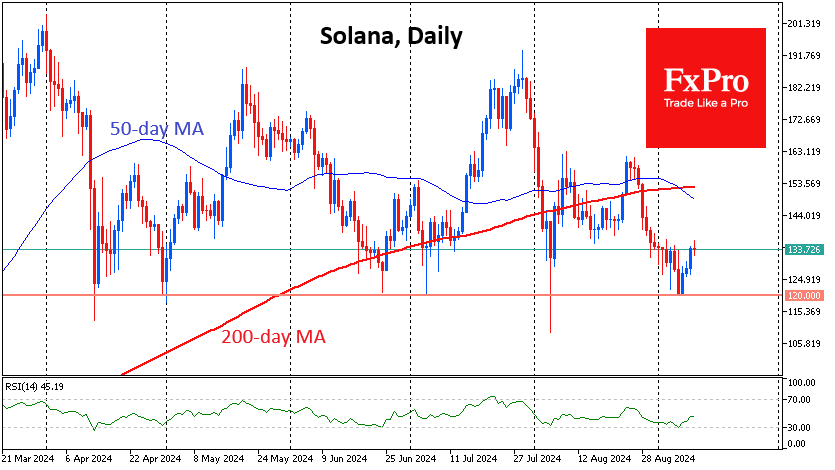

Cautious Rebound in Cryptos

Market Picture

The turnaround in sentiment on the US markets saw the crypto market capitalisation rise by 3.2% in 24 hours to reach $2 trillion. However, it is too early to talk about a reversal in growth, as this level could prove resistant to intensified selling. The Cryptocurrency Sentiment Index rose to 33, the highest since late August, but is still in the ‘fear’ zone.

Bitcoin posted an impressive 7% gain on Monday but corrected some of the gains early in the new day, adding 4% in 24 hours. The technical picture remains supportive of a rebound, but buyers are being cautious and taking profits quickly.

Solana has found support at $120, a key pivot level over the last ten months, and has risen to $134 at the time of writing. Technically, the recovery looks relatively straightforward up to the $149-153 area, where the 50- and 200-day moving averages are centred. A break above $160 would confirm a breakout.

In our view, caution and a tendency to sell growth will prevail in the market, at least until the release of US inflation data on Wednesday. This could continue until the Fed’s interest rate decision on September 18th.

News Background

According to CoinShares, investments in crypto funds fell by $726 million last week, following outflows of $305 million the week before; the figure was the highest since late March. Bitcoin investments fell by $643 million, Ethereum by $98 million and Solana by $6 million.

According to Presto Research, the hash rate hit an all-time high, leaving Bitcoin ‘severely undervalued’. Bianco Research predicts that spot bitcoin ETFs will soon be more in demand in the market.

Bitcoin could reach $90K by the end of the year if Donald Trump wins the US presidential election in November, according to Bernstein. However, if Kamala Harris is successful, BTC could break through the current lows and test levels in the $30K to $40K range. Unlike Trump, Harris did not mention cryptocurrencies in her campaign message.

Cardano founder Charles Hoskinson said that his blockchain has always been the main competitor to the BTC network. The developer is confident that the Cardano cryptocurrency is capable of challenging Bitcoin, the top cryptocurrency by market capitalisation.

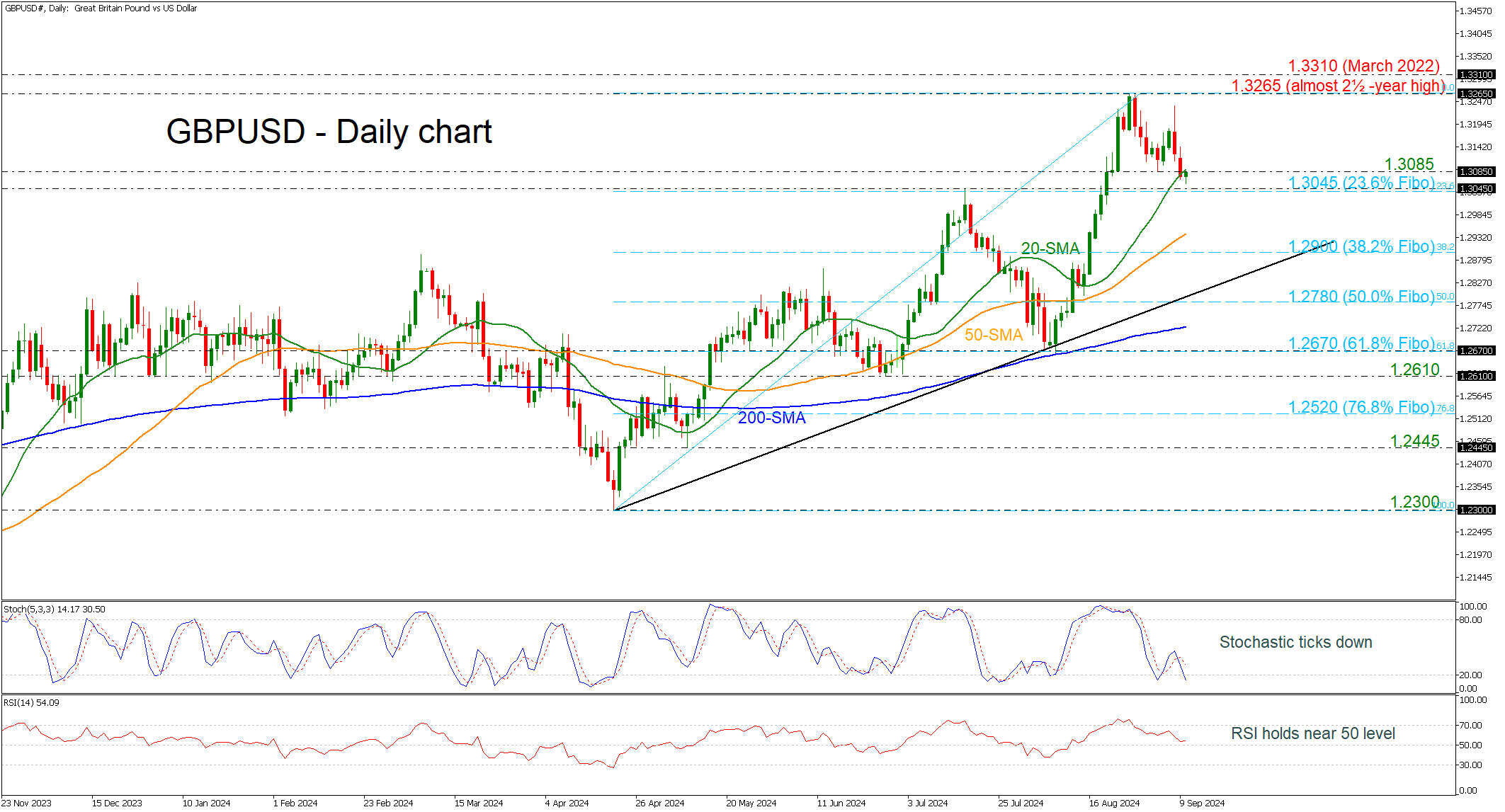

GBPUSD on a Slippery Slope

-

- GBPUSD hovers within critical zone

- Stochastics and RSI lose momentum

GBPUSD has lost its positive momentum after the pullback on the almost two-and-a-half-year high of 1.3265, trading within the restrictive support area of 1.3045-1.3085, which encapsulates the 23.6% Fibonacci retracement level of the upward wave from 1.2300 to 1.3265.

In the short term, the market could maintain downside risks if the RSI keeps moving around the neutral threshold of 50 and the stochastic continues to move in the oversold territory.

If the pair weakens further, the 50-day simple moving average (SMA) at 1.2940 could provide immediate support ahead of the 38.2% Fibonacci at 1.2900. Even lower, the 50.0% Fibonacci at 1.2780 may attract more attention, as any leg lower could worsen the market’s outlook, opening the way for a bearish bias.

On the other hand, an extension to the upside could meet the area within the 1.3265 peak and the March 2022 top at 1.3310.

To summarize, GBPUSD looks neutral to bearish in the very short-term window; however, the broader picture is strongly positive as long as the market remains well above the medium-term ascending trend line.

Sterling a Tad Stronger After Labour Market Data

Markets

This week’s opening session can be easily classified. Risk sentiment improved somewhat after last week’s beating with key European and US stock markets gaining slightly under/over 1%. That doesn’t cover ground lost though with technical pictures still sending correction vibes. The trade weighted dollar (DXY) last Friday tested the first support in around 100.50/60 in the wake of the payrolls release. The greenback avoided a drop and built on that technical correction momentum yesterday (close 101.55). A move above 102 would be a first technical signal that the USD sell-off momentum since July is morphing into more neutral short term settings. EUR/USD 1.10 is a more or less similar pivot point. Core bonds initially drifted south, but the path of least resistance remains stronger going into this week’s ECB and especially next week’s FOMC meeting. US yields remain stuck at/near this year’s low for all tenors. Today’s empty agenda in the US and EMU suggests more anticipative action ahead of tomorrow’s US August CPI report and Thursday’s ECB meeting. Sterling is a tad stronger after labour market data this morning. Wage growth slowed as expected to 5.1% on an annual basis in the three months to July, while employment rose more than expected in that same time span (+265k 3M/3M). Monthly payrolls for August nevertheless pointed at 59k layoffs (vs +25 k expected).

The ECB is expected to cut its deposit rate for a second time this year by 25 bps, to 3.50%. As announced in March, they will also reduce the spread between the main refinancing rate and the deposit rate from the current 50 bps to only 15 bps implying an MRR rate cut of 60 bps, from 4.25% to 3.65%. Updated GDP and CPI forecasts will be closely watched for clues on the monetary policy trajectory going forward. However, we don’t expect big changes apart from perhaps some minor downward revisions to this year’s GDP and headline CPI data. Recall that ECB staff in June plotted a 0.9%-1.4%-1.6% growth path for 2024-2026 and a 2.5%-2.2%-1.9% inflation trajectory. While keeping an easing bias, we don’t expect the central bank to pre-commit to specific actions at coming meetings. The short intermeeting period between September 12 and October 17 suggests that bar any big surprise, the central bank might be more inclined to sit the October meeting out and stick with the currently, quarterly, rate-reduction scheme with a next 25 bps move coming only in December. Unlike the Fed, the ECB’s options for making policy less restrictive are smaller given limited room towards neutral territory in the current, stubborn, (core) inflationary environment.

News & Views

Investors are urging the Bank of England to expand the maturity range of the bonds it is actively selling under the umbrella of quantitative tightening. The BoE on September 19 announces its new target by which it wants to reduce its gilt portfolio (currently £688bn from a £875bn peak) over the coming 12 months. Sticking to the current pace of £100bn means that the BoE will only actively sell about £13bn (down from about £50bn) of gilts due to a sharp uptick in maturing bonds. These sales will only cover maturities of three years or longer. However, market parties say that the front end of the gilt market is experiencing a notable liquidity problem due to the large stock the BoE holds. Shorter-dated bonds are estimated to be around a third of the total portfolio. Some analysts say this makes them structurally scarce and a potential source of problems in the repo market. Bloomberg’s gilt liquidity tracker has indeed deteriorated in recent weeks to levels seen in the wake of the 2008 financial crisis. Despite the recent improvement it’s still showing poorer liquidity than during the September 2022 gilt crash. Some BoE watchers as a result expect the central bank to actually raise the annual QT target.

The European Commission is mulling sanctions on Robert Fico’s Slovakian government over rule of law concerns. At stake for Slovakia are some of the €12.8bn of allocated European funds and the €2.7bn of EUNextGen grants, officials said. The EU is worried about some recent judicial changes, including a revision to the criminal code that reduces sentences for crimes such as fraud and the decision to scrap an anti-corruption office. The latter was one of the conditions for receiving pandemic-related grants. EU executives are drafting a letter to let Slovakia know it faces punishment. Commission president von der Leyen is said she has yet to decide whether the letter will be sent and when.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU activity data rolled in, dragging the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is moving to a better in to balance. The pivot weakened the technical picture in US yields. A string of weak eco data and a risk-off market climate pushed and kept the 10-yr sub 4%. We think we could be up to three 50 bps rate cuts this year.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1276 (2023 top) serves as next technical references.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Recent better UK activity data and a cautious assessment of BoE’s Bailey at Jackson Hole are pushing EUR/GBP lower in the 0.84/0.086 range.