Sample Category Title

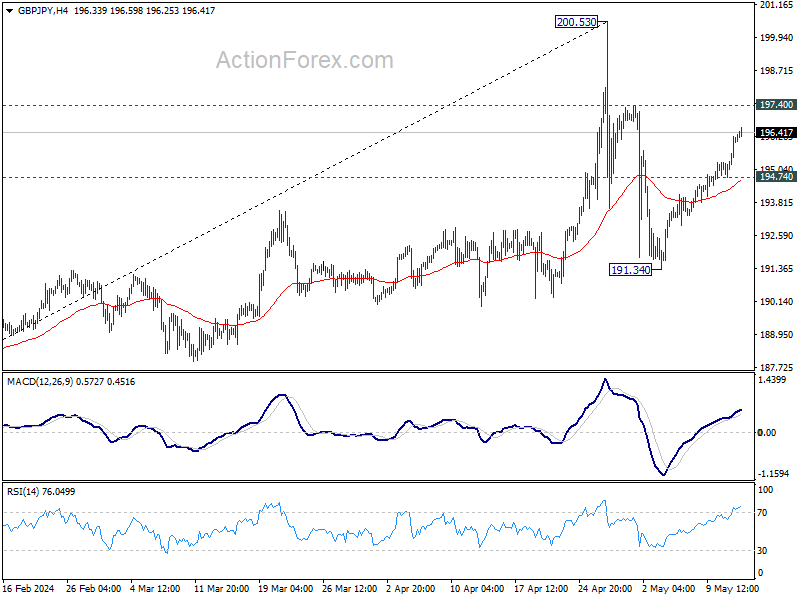

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.21; (P) 195.75; (R1) 196.74; More...

Intraday bias in GBP/JPY stays on the upside at this point. Rebound from 191.34 is seen as the second leg of the corrective pattern from 200.53, and could target 197.40 resistance. On the downside, break of 194.74 minor support will turn intraday bias neutral first.

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 183.41) holds, fall from there is seen as correcting the rise from 178.32 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

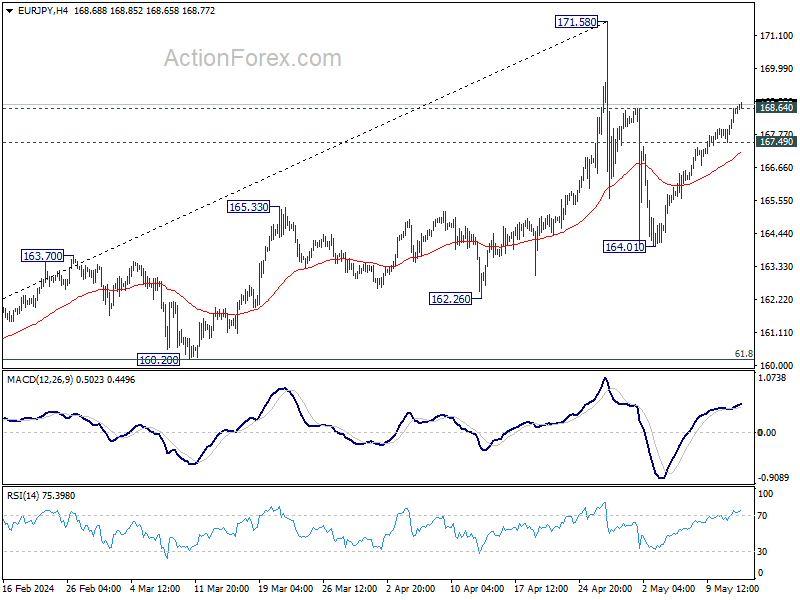

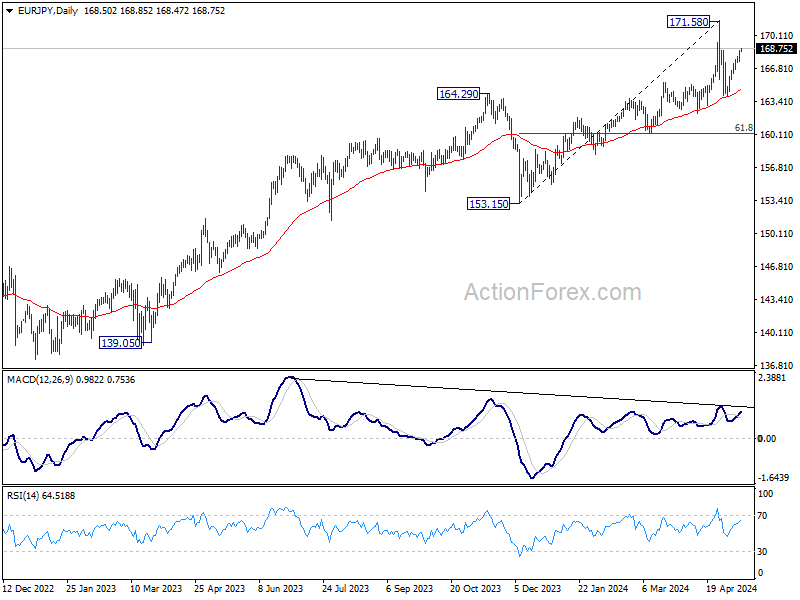

EUR/JPY Daily Outlook

Daily Pivots: (S1) 167.83; (P) 168.24; (R1) 168.98; More...

Intraday bias in EUR/JPY stays on the upside at this point. Rebound from 164.01 is seen as the second leg of the corrective pattern from 171.58. Firm break of 168.64 will target 171.58 high. On the downside, below 167.49 minor support will turn intraday bias neutral first.

In the bigger picture, a medium top could be formed at 171.58 after brief breach of 169.96 (2008 high). As long as 55 W EMA (now at 157.89) holds, fall from there is seen as correcting the rise from 153.15 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

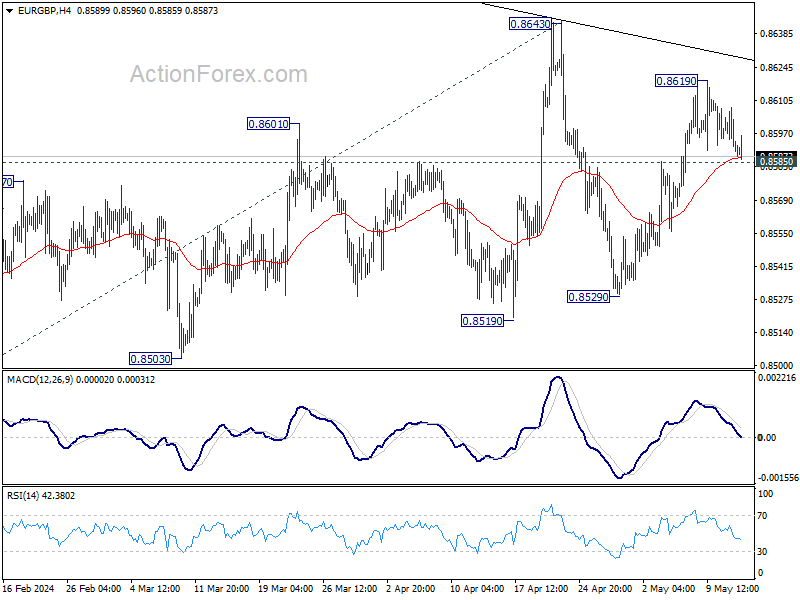

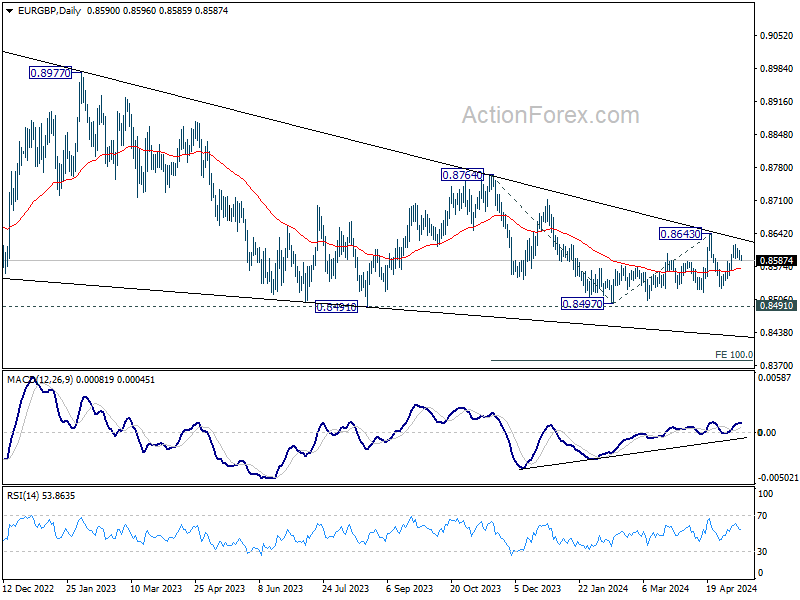

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8585; (P) 0.8597; (R1) 0.8603; More...

Intraday bias in EUR/GBP remains neutral at this point. On the downside, below 0.8585 minor support will argue that rebound from 0.8529 has completed, and larger fall might be ready to resume. Intraday bias will be back on the downside for 0.8529 support first.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

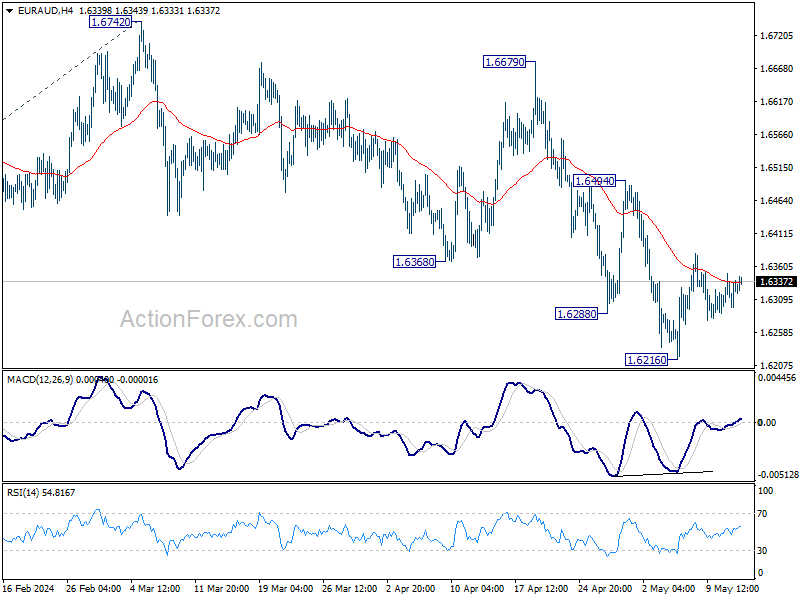

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6295; (P) 1.6324; (R1) 1.6357; More...

No change in EUR/AUD's outlook and intraday bias stays neutral. While stronger recovery might be seen, further decline is expected as long as 1.6494 resistance holds. Fall from 1.6742 is seen as the third leg of the corrective pattern from 1.7062. Break of 1.6216 will turn bias back to the downside to 1.6127 support, or further to 100% projection of 1.7062 to 1.6127 from 1.6742 at 1.5807.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

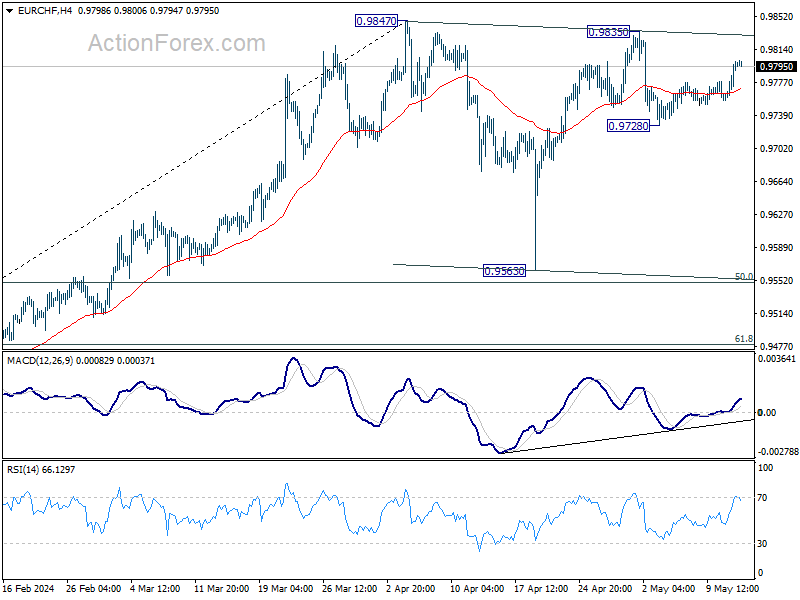

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9765; (P) 0.9784; (R1) 0.9819; More...

Intraday bias in EUR/CHF remains neutral at this point. On the upside, decisive break of 0.9835/47 resistance will resume larger rally from 0.9252. On the downside, however, break of 0.9728 will extend the corrective pattern from 0.9847 with another fall, back to 0.9563 support.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Break of 0.9847 resistance will target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004.

UK Labour Market Data Mixed

Markets

Fed vice-chair Jefferson came with an important message to his colleagues. The current diversity of viewpoints among policymakers lends to stimulating debates and ultimately better policy. But… there’s a but… in such a situation, more communication could increase rather than reduce uncertainty about Fed policy. “The potential for misinterpretation is especially acute when many policymakers speak at the same time and disagree with each other”. Also the Summary of Economic Projections (including dot plot) serves as an additional source of volatility in uncertain, and rapidly changing, market conditions (rate outlook). Fed officials have been discussing alternative communication strategies after the previous meeting. An official strategic review including communication policy will start later this year. Earlier this month, the Bank of England received the results of a similar evaluation conducted by former Fed chair Bernanke. Jefferson confirmed the concerning lack of inflation progress in the first quarter, suggesting to keep the policy rate in restrictive territory awaiting that additional evidence. Unlike the FOMC statement, Jefferson didn’t specifically mention a policy rate cut. Fed Chair Powell speaks tonight at a special event organized by Netherlands’ foreign bankers’ association but its unclear if he’ll touch on monetary policy.

US April producer prices have the potential to move markets today. Another upward surprise would up the ante in the run-up to tomorrow’s CPI figures. Consensus expects 0.3% M/M and 0.2% M/M increases for headline and core PPI prints to day. The bar is higher tomorrow at 0.4% and 0.3% respectively. We have the feeling that especially tomorrow, even meeting this bar isn’t the hoped-for evidence that the disinflation process will continue. Therefore, and following the post-FOMC correction, we see asymmetric risks. US yields can then move again somewhat higher withing new trading ranges (4.75%-5.05% for 2-yr yield; 4.4%-4.75% for 10-yr). Such outcome should help the dollar holding above 105 support for the trade weighted greenback and below EUR/USD 1.0872 resistance.

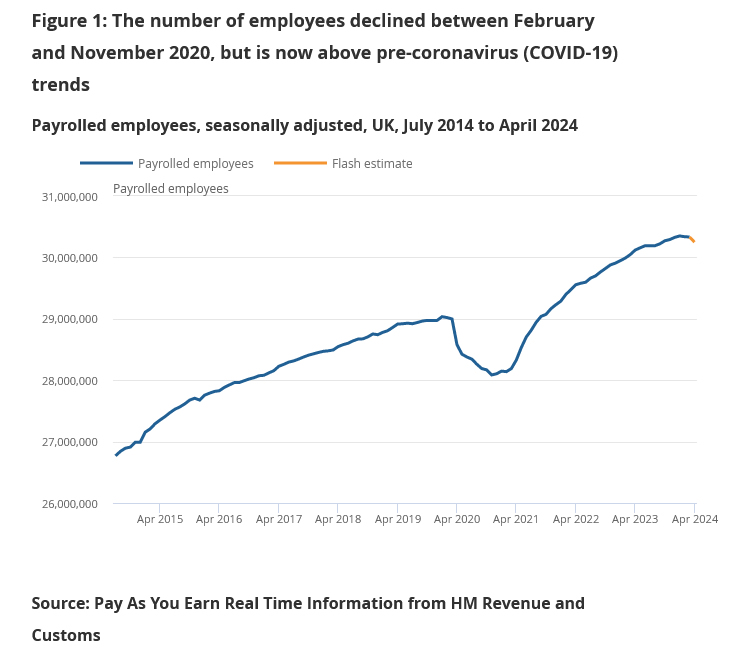

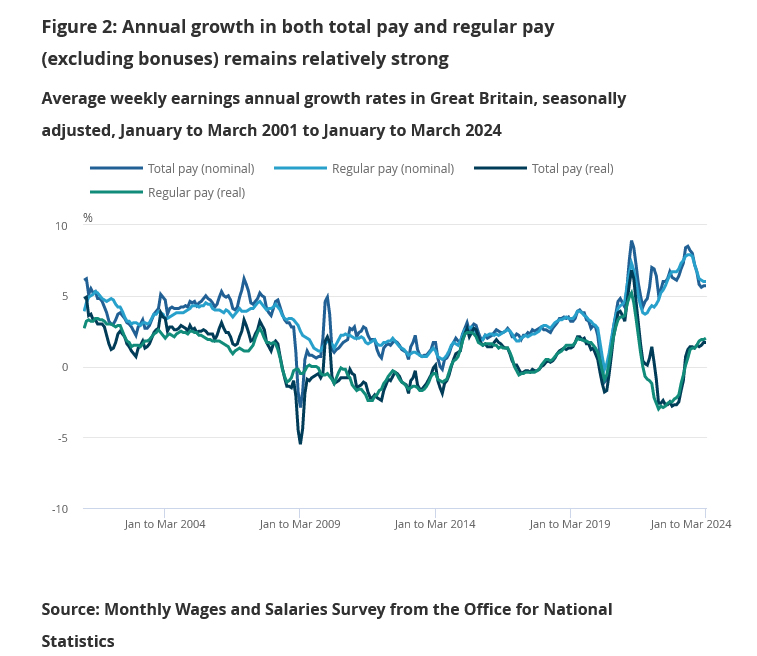

UK labour market data were mixed this morning. April payrolls fell by 85k (vs +20k expected) but the March figure was upwardly revised from 67k job losses to only 5k. The unemployment rate ticked up from 4.2% to 4.3% in the three months to March. Wages rose slightly more than expected over that period (5.7% 3M/YoY). Sterling trades volatile not knowing to choose the weaker employment or the stickier wage inflation side.

News & Views

The NY Fed’s April survey of consumer expectations showed one-year ahead inflation expectations increasing to 3.3% from 3% in March. They also increased to 2.8% from 2.6% at a five year ahead horizon, but eased slightly to 2.8% from 2.9% at a three year horizon. Higher inflation expectations in the New-York Fed survey follow a rise in both one-year and longer time expectations in the consumer sentiment report of the University of Michigan published last week. Home price expectations in the NY-Fed survey also ticked up to 3.3% after seven consecutive months at 3%, reaching their highest level since July 2022. However, answers on the labour market, income and spending showed a more mixed picture. Spending growth expectations also increased (0.2% to 5.2%). Median expected household income eased slightly (0.1%) to 3%. The average perceived likelihood of voluntary and involuntary job separation declined, as did the perceived likelihood of finding a job in the event of a job loss.

Indian inflation eased only slightly in April to 4.83% from 4.85% in March. A further/faster decline in inflation was hampered by elevated food price inflation. Food price inflation (about half of the country’s inflation basket) rose 8.70% Y/Y in April up from 8.52 Y/Y in March. Inflation of most other components continues to ease. Fuel and power prices even were 4.24% lower. The Reserve Bank of India aims to bring inflation back to its 4% target. The April data suggest that it will keep its policy rate on hold at 6.5% at the next policy meeting early June. As is the case for several emerging market currencies, the Indian Rupee is trading in the defensive against a broadly strong dollar. At USD/INR 83.51, the Indian currency trades very close to the all-time lows reached last month (83.57).

Graphs

GE 10y yield

ECB President Lagarde clearly hinted at a summer (June) rate cut which has broad backing. EMU disinflation continued in April and brought headline CPI closer to the 2% target. Together with weak growth momentum, this gives backing to deliver a first 25 bps rate cut. A more bumpy inflation path in H2 2024 and the Fed’s higher for longer strategy make follow-up moves difficult. Markets have come to terms with that.

US 10y yield

The Fed in May acknowledged the lack of progress towards the 2% inflation objective, but Fed’s Powell left the door open for rate cuts later this year. Soft US ISM’s and weaker than expected payrolls supported markets’ hope on a first cut post summer, triggering a correction off YTD peak levels. Sticky inflation suggests any rate cut will be a tough balancing act. 4.37% (38% retracement Dec/April) already might prove strong support for the US 10-y yield.

EUR/USD

Economic divergence, a likely desynchronized rate cut cycle with the ECB exceptionally taking the lead and higher than expected US CPI data pushed EUR/USD to the 1.06 area. From there, better EMU data gave the euro some breathing space. The dollar lost further momentum on softer than expected early May US data. Some further consolidation in the 1.07/1.09 are might be on the cards short-term.

EUR/GBP

Debate at the Bank of England is focused at the timing of rate cuts. Most BoE members align with the ECB rather than with Fed view, suggesting that the disinflation process provides a window of opportunity to make policy less restrictive (in the near term). Sterling’s downside turned more vulnerable with the topside of the sideways EUR/GBP 0.8493 - 0.8768 trading range serving as the first real technical reference.

Everybody is Fed-Dependent

The major indices in Europe and the US across traded rangebound near their ATH levels and the US dollar index fluctuated a touch above the 105 level ahead of the US and European inflation updates that will start flowing in today.

The major story of Monday was a renewed rally in Gamestop and AMC shares after Keith Gill, aka, Roaring Kitty, posted on X for the first time since 2021. The moves revived the 2021’s meme nostalgia, but the meme stocks will unlikely see their original glory. First, the macroeconomic setting is different: we are in a period of higher interest rates and tight monetary policies where the Federal Reserve (Fed) and other central banks are no longer pumping pandemic-rescue cash into the system. 2. People are not stuck home and savings have melted since the pandemic pile-up. 3. The trading volumes are nowhere close to 2021: around 700’000 options changed hands yesterday, while this number was around 8.5 mio back in 2021. And last but not least, most of the retail traders know that if they are the last the come in, they will lose it all. Of course, because the meme story is irrational, we can’t predict what’s next. But thank you, Roaring Kitty, for spicing up a day that would’ve otherwise been long hours of waiting for the US and European inflation numbers.

Let’s go back to our beans. The US will release the PPI figures for April today. The core PPI is seen stable at 2.4% on a yearly basis, while headline PPI may have ticked slightly higher, from 2.1% to 2.2% last month. A figure in line, or ideally below expectation, should give a sigh of relief to the Fed doves, let the US dollar soften against major peers and help lift appetite in risk assets, while a figure above expectations will further dampen the Fed cut expectations, give a boost to the US dollar and weigh on stock and bond valuations.

Across the Atlantic Ocean, headline inflation in the Eurozone may have stabilized near 2.4% and core inflation may have eased further to 2.7% from 2.9% printed a month ago.

This week’s inflation updates should maintain the ‘diverging inflation dynamics’ narrative live. The US inflation is seen heating up whereas inflation in the Eurozone and the UK are forecasted to continue their journey to the south – toward the central banks’ 2% inflation target. The latter divergence obliges the Fed to postpone its rate cut plans, but keeps the European Central Bank (ECB) and the Bank of England (BoE) on track to cut their rates this summer.

Both the ECB and the BoE say that they are ‘data dependent and not Fed dependent’. But that’s true under one condition: the euro and sterling should not depreciate significantly against the USD. So far, both the euro and sterling resist surprisingly well to the divergence between the hawkish Fed versus dovish ECB and BoE.

- Slight improvement in EZ growth numbers versus a significant slide in the latest growth data partly explain the tempered USD appreciation.

- The idea that the Fed’s next move is a rate cut – even if it comes a bit later than many have hoped at the start of the year – prevents the USD bulls from coming back forcefully in charge. The Fed also announced to slow QT at the March meeting.

Yet, note that the US dollar index advanced up to 5% since the start of this year and risks are tilted to the upside as long as we don’t see the US inflation return to the falling path.

And the reality is that we are all Fed dependent. No matter what the ECB and the BoE say, they can’t walk it alone if the US dollar appreciates due to a U-turn in the US inflation. A significant dollar appreciation would boost inflation in the Eurozone and the UK, and bring the ECB and the BoE to review their rate cutting plans beyond summer.

UK payrolled employment down -85k in Apr, but wages growth steady in Mar

UK payrolled employment fell -85k or -0.3% mom in April. This is a rise of 129,000 people over the 12-month period. Median monthly pay growth was 6.9% yoy, accelerated from March's 6.4% yoy. Claimant count rose 8.9k, below expectation of 13.9k.

In the three months to March, unemployment rate rose from 4.2% to 4.3%, matched expectations. Average earnings including bonus rose 5.7% yoy. Average earnings excluding bonus rose 6.0% yoy. Both were unchanged from February's figures.

US Consumers Anticipate Sticky Inflation Ahead

In focus today

In the US, April PPI is due for release this afternoon, unusually ahead of the CPI release tomorrow. This means markets could pay even more attention to it than usual, not least after the upside surprises seen in the March inflation data.

In Germany, we receive the ZEW survey for May. The assessment of the current economic situation has been flat for the past six months while expectations have risen greatly. Hence, it will be interesting to see if we finally get an improvement in the assessment of the economic situation.

Overnight, China will announce policy rates (Medium Lending Facility) but a rate cut is unlikely at this stage as China is likely waiting for the Fed to ease before cutting rates further.

Economic and market news

What happened yesterday

In the US, the Survey of Consumer Expectations from the New York Fed echoed the University of Michigan sentiment survey. 1y inflation expectations rose to 3.3% from 3.0%, the highest print since November 2023, while the 5y figure increased to 2.8% from 2.6%. Conversely, the 3y measure decreased to 2.8% from 2.9%. The elevated inflation expectations are largely attributed to anticipated rises in home prices, food, fuel, and medical costs.

Moreover, Fed vice-chair Philip Jefferson (voting member) was on the wire stating that the Fed should maintain interest rates at restrictive levels until it has further evidence that inflation is reaching its 2% target.

Market movements

Equities: Global equities saw a marginal increase yesterday, characterised by low trading volume and what felt like a snoozefest. In other words, it was a wait-and-see game in anticipation of the Wednesday data release, particularly the US CPI numbers. Tech and growth sectors, along with small caps, outperformed slightly. Of more concern is the resurgence of the meme stock frenzy, with a few names showing remarkable gains and Bitcoin's value on the rise. This indicates a return of complacency and exuberance in the markets following a downturn in volatility and a perceived lack of clear market threats. In the US yesterday, the Dow was down by 0.2%, the S&P 500 by 0.02%, while the Nasdaq rose 0.3% and the Russell 2000 increased 0.1%. Asian markets are mixed or marginally lower this morning, a trend mirrored by futures in Europe and the US.

FI: There were modest movements in global bond yields yesterday with both US Treasuries and Bunds range trading ahead of the US inflation data released on Wednesday. Yesterday, a survey by the New York Federal Reserve showed that consumers expect prices to rise to 3.3% for 2024 relative to the consensus forecast of 3.1% for 2024. Today, we have US Producer prices for April as well as the ZEW indicator from Germany.

FX: EUR/USD trended slightly higher, trading just below 1.08 in a rather uneventful session. USD/JPY has continued to climb, surpassing the 156-mark. EUR/NOK and EUR/SEK still trade around 11.70, with the former slightly below, benefiting from higher oil prices. EUR/GBP continues to hover just below 0.8600, ahead of today's UK labour market report.

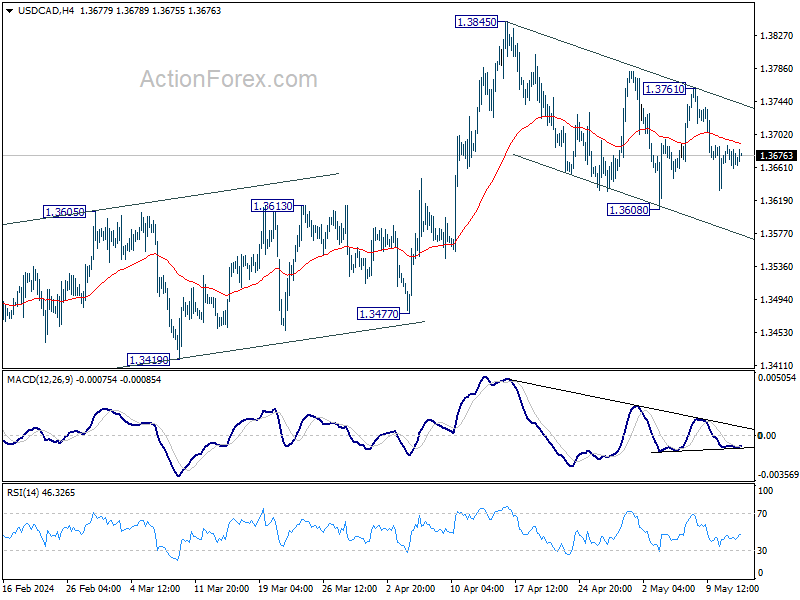

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3655; (P) 1.3673; (R1) 1.3684; More...

Intraday bias in USD/CAD stays neutral and outlook is unchanged. On the upside, break of 1.3761 resistance will argue that correction from 1.3845 has already completed. Intraday bias will be back to the upside to resume larger rally from 1.3176 through 1.3845. However, sustained trading below 55 D EMA (now at 1.3630) will argue that whole rise from 1.3176 has completed already, and bring deeper fall to 1.3477 support next.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.