Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6586; (P) 0.6608; (R1) 0.6629; More...

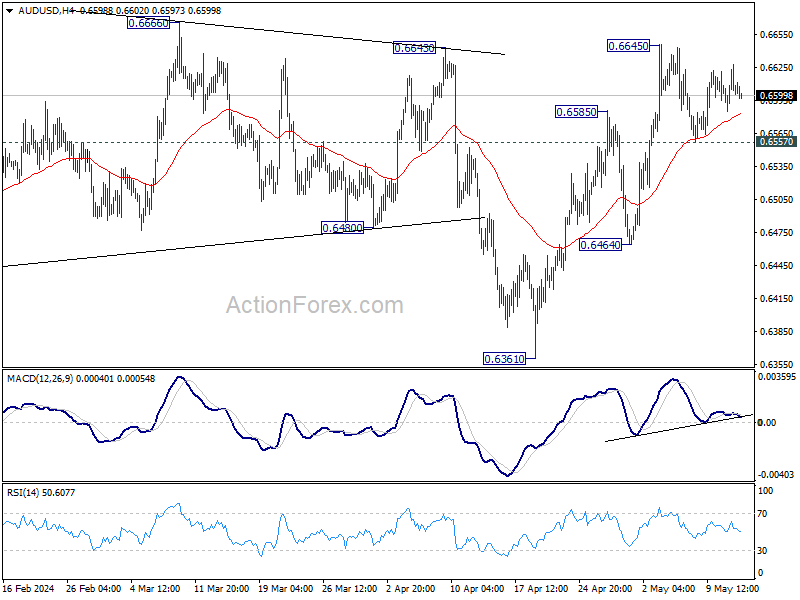

Intraday bias in AUD/USD stays neutral at this point. Further rally is expected as long as 0.6557 support holds. Break of 0.6645 will will resume the rebound from 0.6361. On the downside, however, firm break of 0.6557 will bring deeper fall back to 0.6464 support instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0788; (R1) 1.0809; More...

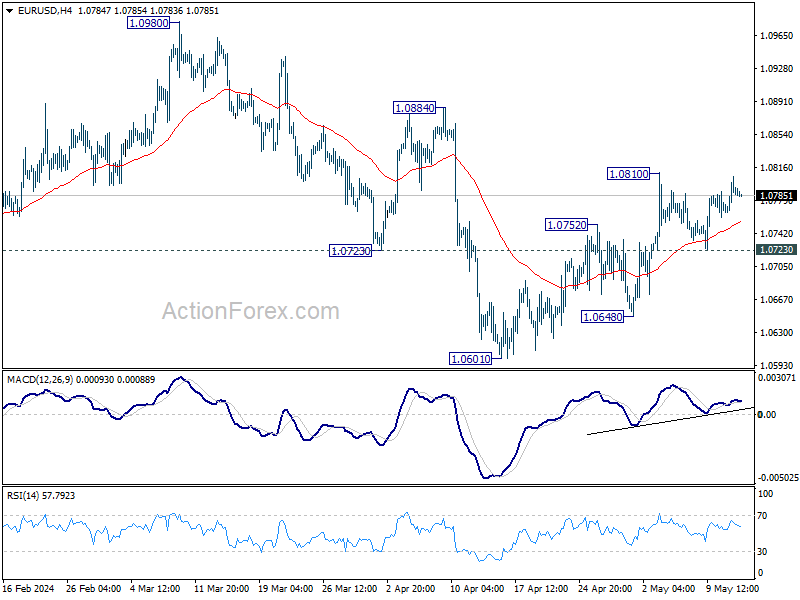

Intraday bias in EUR/USD remains neutral for the moment. Further rally is in favor as long as 1.0723 minor support holds. On the upside, break of 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 1.0723 will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

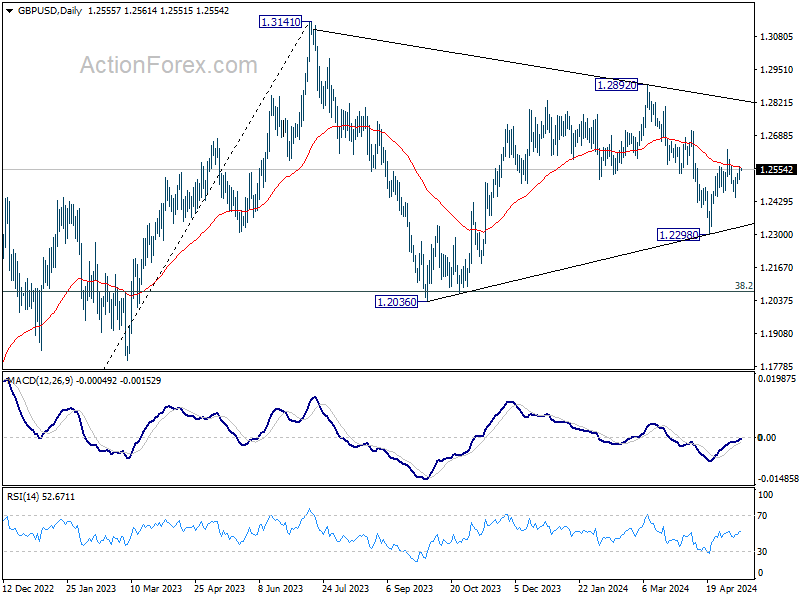

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2547; (R1) 1.2581; More...

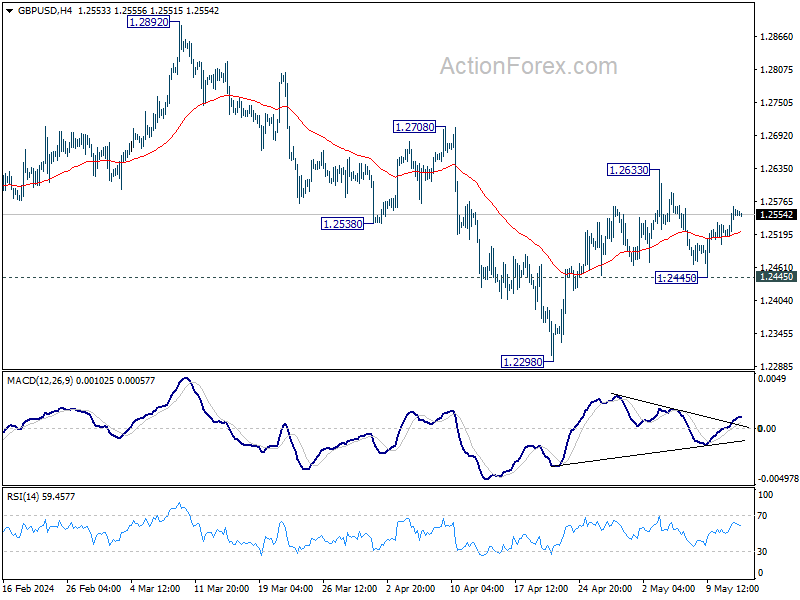

Intraday bias in GBP/USD remains neutral for the moment. Further rise is mildly in favor with 1.2445 support intact. On the upside, break of 1.2633 will resume the rally from 1.2298 to 1.2708 resistance next. However, firm break of 1.2445 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

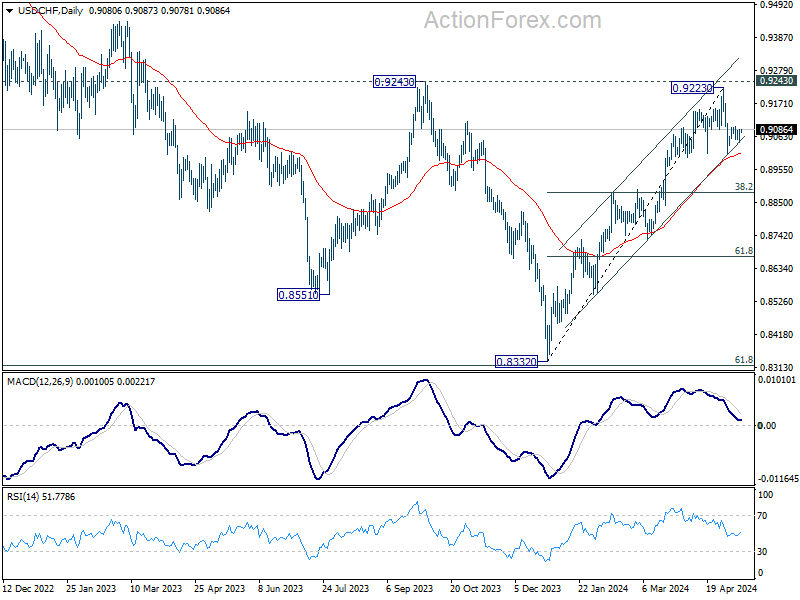

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9057; (P) 0.9072; (R1) 0.9099; More....

Intraday bias in USD/CHF remains neutral at this point. Further decline is in favor as long as 55 4H EMA (now at 0.9083) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9010) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back from 0.9223 has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

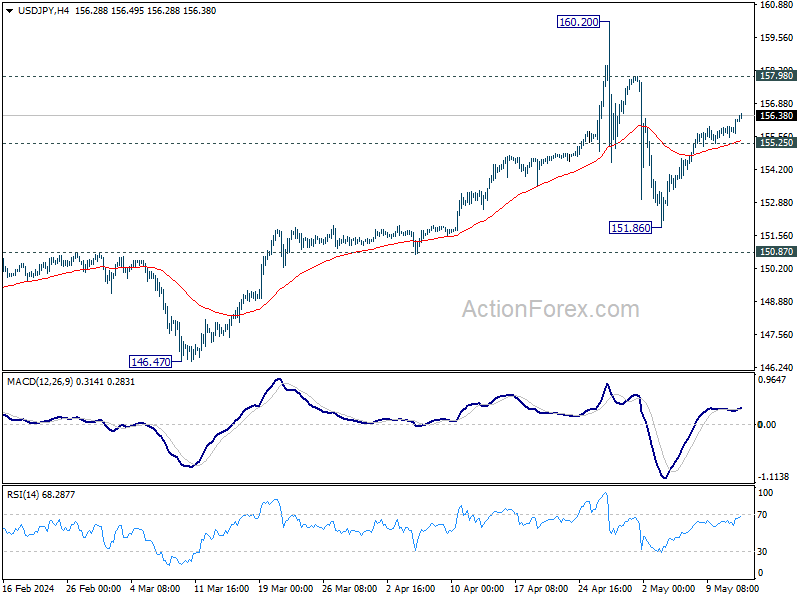

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.74; (P) 156.00; (R1) 156.47; More...

Intraday bias in USD/JPY stays mildly on the upside at this point. Rebound from 151.86, as the second leg of the corrective pattern from 160.20, is in progress for 157.98 resistance. On the downside, break of 155.25 minor support will suggest that the third leg has started, and turn bias back to the downside for 151.86 support.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Yen Decline Persists, Pound Eyes UK Wage Data

Yen's decline persisted in Asian session, continuing to reverse its strong gains from earlier in the month. Traders seem confident that Japan will not intervene as long as Yen remains above 160 level against Dollar, with no apparent determination to push it through 150. This range appears to be set for the near term.

Japan's response to Yen's selloff has been restrained. Finance Minister Shunichi Suzuki reiterated his commitment to closely monitoring the currency markets and taking all possible measures against excessive, speculative moves. He emphasized the importance of close communication and coordination BoJ.

Elsewhere in the currency markets, Sterling ranks as the second strongest currency of the day after Dollar. The Pound is anticipating today's UK employment data, with particular attention on wage growth. BoE Governor Andrew Bailey has left the door open for a June rate cut, but some economists believe the central bank will not rush into a decision until the risk of wage-driven inflation resurgence is mitigated. Currently, Aussie follows Yen as the second weakest currency, with Loonie trailing behind. Euro and Swiss Franc are positioned in the middle.

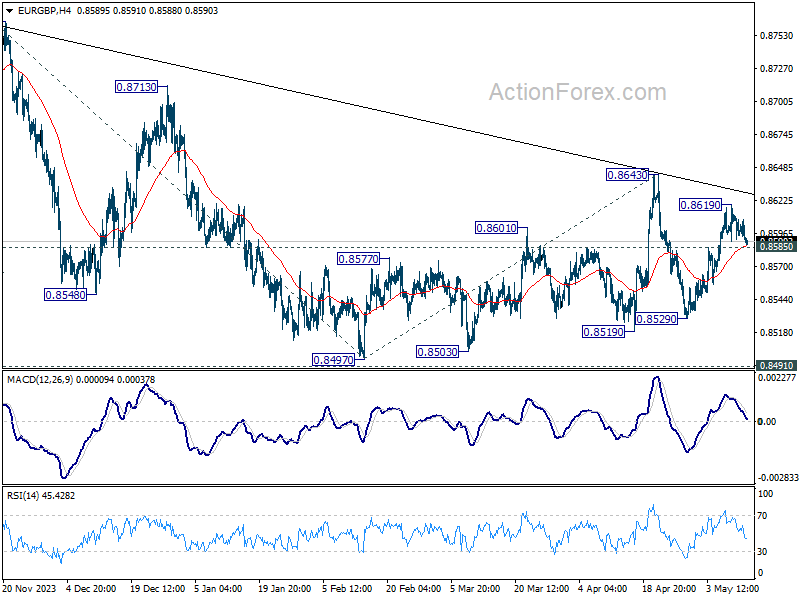

Technically, EUR/GBP's rebound from 0.8529 stalled ahead of 0.8643 resistance as well as medium term falling trend line. Price actions from 0.8497 are seen as a corrective pattern. Break of 0.8585 support will add to the case that larger down trend is ready to resume and target 0.8529 support first.

In Asia, at the time of writing, Nikkei is up 0.09%. Hong Kong HSI is down -0.13%. China Shanghai SSE is down -0.12%. Singapore Strait Times is down -0.06%. Japan 10-year JGB yield is up 0.0176 at 0.959. Overnight, DOW fell -0.21%. S&P 500 fell -0.02%. NASDAQ rose 0.29%. 10-year yield fell -0.023 to 4.481.

Fed's Jefferson: Restrictive rates necessary amid slow disinflation progress

Fed Vice Chair Philip Jefferson indicated that with the economy showing robust job growth, Fedcan focus "even more so" on ensuring that inflation returns to its 2% target. Jefferson acknowledged the slow progress in reducing inflation, asserting that it justifies keeping the policy rate elevated.

"In light of the attenuation in progress, in terms of getting inflation down to our target, it is appropriate that we maintain the policy rate in restrictive territory," Jefferson noted.

He reiterated that the Fed is vigilant in seeking clear evidence of inflation decreasing to the desired level before considering any policy rate adjustments.

Fed's approach is influenced by the varied perspectives among policymakers, which Jefferson believes enriches policy discussions. However, he cautioned that increased communication from Fed might sometimes lead to greater uncertainty about its policies, rather than clarity.

IMF recommends gradual approach for future BoJ rate hikes

IMF projects Japan's economic growth to continue, with a noticeable increase in consumption anticipated later this year. According to a report, Japan's growth rate is expected to decelerate to 0.9% in 2024, largely due to the fading impact of one-off factors that boosted growth in 2023.

The report highlights that consumption will pick up in the latter half of 2024 and into 2025, driven by rising nominal wages following a strong Shunto settlement in 2024 and a decrease in headline inflation that will boost real wages.

IMF foresees core inflation gradually declining as the impact of higher import prices diminishes. However, core inflation is expected to remain above BoJ's 2% target until the second half of 2025.

In light of these developments, IMF suggests that further increases in BoJ's short-term policy rate should "proceed at a gradual pace" and be "datadependent", considering the balanced risks to inflation and the mixed signals from recent economic data.

IMF emphasizes the importance of Japan's adherence to a "flexible exchange rate regime", which will play a crucial role in absorbing economic shocks and supporting the central bank's focus on maintaining price stability.

Looking ahead

UK employment data is a major focus in European session. Swiss PPI, Germany ZEW economic sentiment and CPI final, will be released too. Later in the day, US PPI will be the highlight.

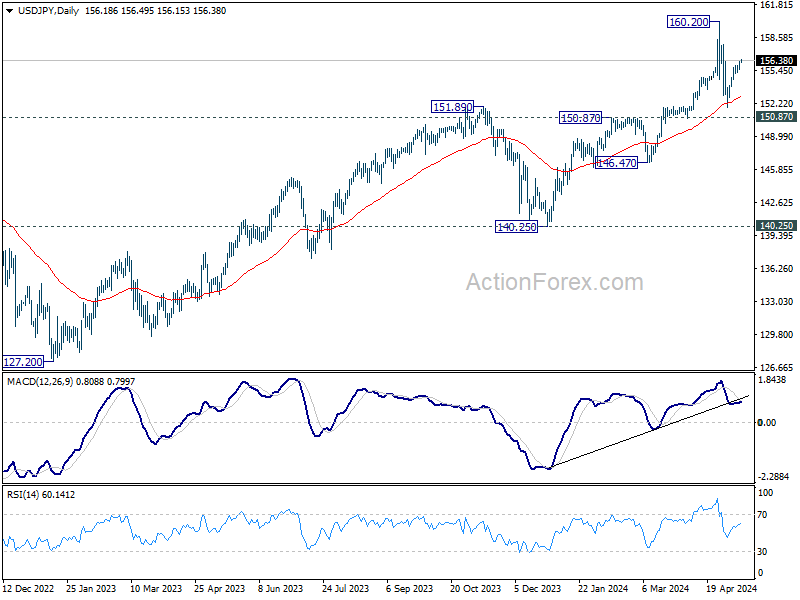

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.74; (P) 156.00; (R1) 156.47; More...

Intraday bias in USD/JPY stays mildly on the upside at this point. Rebound from 151.86, as the second leg of the corrective pattern from 160.20, is in progress for 157.98 resistance. On the downside, break of 155.25 minor support will suggest that the third leg has started, and turn bias back to the downside for 151.86 support.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Apr | 0.90% | 0.90% | 0.80% | 0.90% |

| 06:00 | GBP | Claimant Count Change Apr | 13.9K | 10.9K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | 4.30% | 4.20% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 5.30% | 5.60% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 6.00% | |||

| 06:00 | EUR | Germany CPI M/M Apr F | 0.50% | 0.50% | ||

| 06:00 | EUR | Germany CPI Y/Y Apr F | 2.20% | 2.20% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Apr | -3.80% | |||

| 06:30 | CHF | Producer and Import Prices M/M Apr | 0.20% | 0.10% | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | -2.10% | |||

| 09:00 | EUR | Germany ZEW Economic Sentiment May | 44.9 | 42.9 | ||

| 09:00 | EUR | Germany ZEW Current Situation May | -75 | -79.2 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | 46.1 | 43.9 | ||

| 10:00 | USD | NFIB Business Optimism Index Apr | 88.1 | 88.5 | ||

| 12:30 | USD | PPI M/M Apr | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Y/Y Apr | 2.20% | 2.10% | ||

| 12:30 | USD | PPI Core M/M Apr | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Core Y/Y Apr | 2.40% | 2.40% | ||

| 12:30 | CAD | Wholesale Sales M/M Mar | -0.90% | 0.00% |

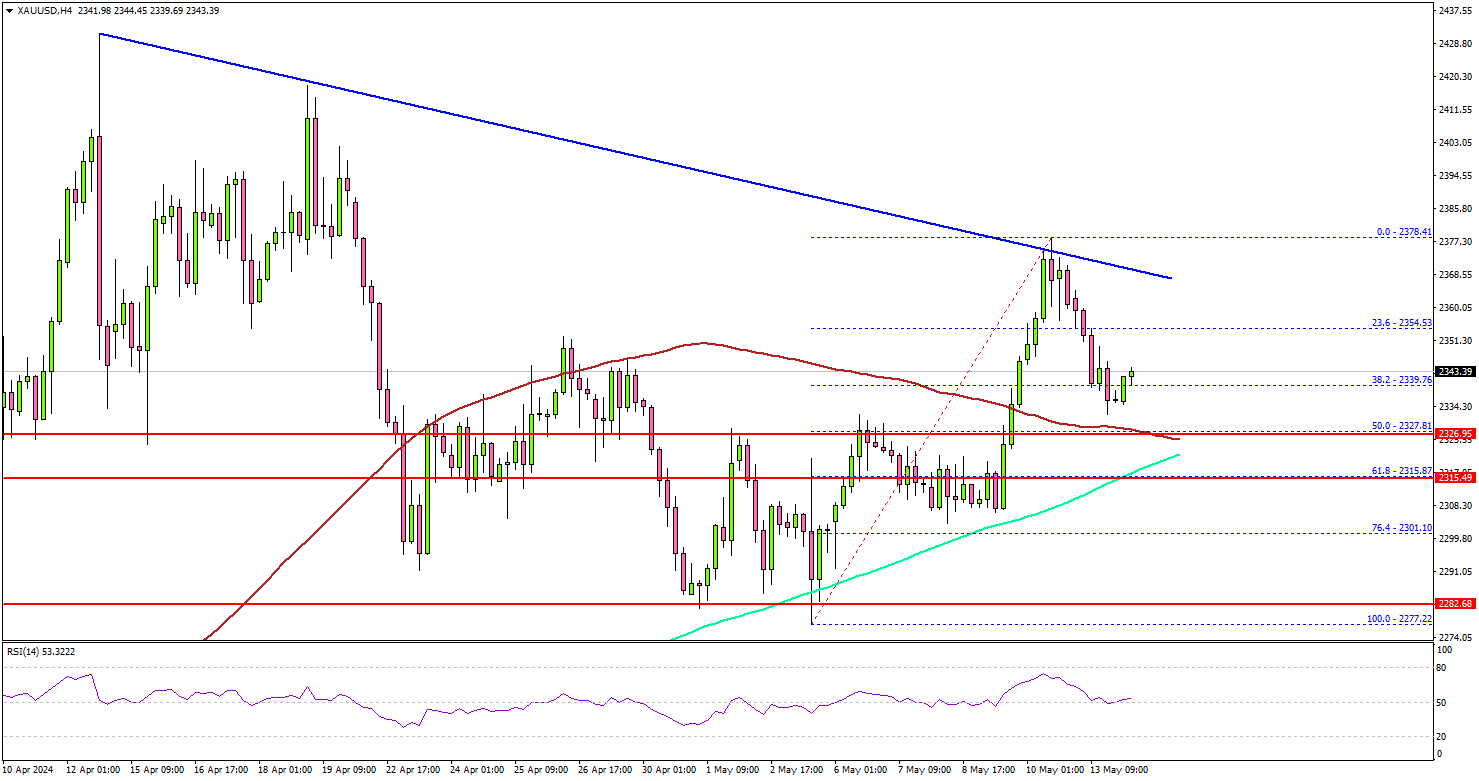

Gold Price Could Resume Upside, This Support Is The Key

Key Highlights

- Gold started a downside correction from the $2,380 zone.

- A key bearish trend line is forming with resistance at $2,370 on the 4-hour chart.

- Oil prices are showing bearish signs below $80.00.

- Bitcoin price is still consolidating above the $60,000 support zone.

Gold Price Technical Analysis

Gold prices started a fresh increase above the $2,335 resistance against the US Dollar. It traded above the $2,350 zone before the bears appeared.

The 4-hour chart of XAU/USD indicates that the price traded as high as $2,378 and settled above the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

Recently, there was a downside correction from the $2,378 level and the price declined below $2,355. The price dipped below the 23.6% Fib retracement level of the upward move from the $2,277 swing low to the $2,378 high.

On the downside, the 100 Simple Moving Average (red, 4 hours) is the key at $2,328. It is close to the 50% Fib retracement level of the upward move from the $2,277 swing low to the $2,378 high.

The next support sits at the 200 Simple Moving Average (green, 4 hours) and $2,315. A downside break below the $2,315 support might call for more downsides. The next major support is near the $2,280 level. Any more losses might send Gold prices toward $2,265.

On the upside, immediate resistance is at $2,355. The first major resistance is now forming near a key bearish trend line at $2,375, above which the price could accelerate higher toward $2,395.

Looking at Bitcoin, the bulls are still active above the $60,000 support and they might aim for a steady increase in the near term.

Economic Releases to Watch Today

- UK Claimant Count Change for April 2024 – Forecast 13.9K, versus 10.9K previous.

- UK ILO Unemployment Rate Feb 2024 (3M) – Forecast 4.3%, versus 4.2% previous.

- US Producer Price Index for April 2024 (YoY) – Forecast +2.2%, versus +2.1% previous.

IMF recommends gradual approach for future BoJ rate hikes

IMF projects Japan's economic growth to continue, with a noticeable increase in consumption anticipated later this year. According to a report, Japan's growth rate is expected to decelerate to 0.9% in 2024, largely due to the fading impact of one-off factors that boosted growth in 2023.

The report highlights that consumption will pick up in the latter half of 2024 and into 2025, driven by rising nominal wages following a strong Shunto settlement in 2024 and a decrease in headline inflation that will boost real wages.

IMF foresees core inflation gradually declining as the impact of higher import prices diminishes. However, core inflation is expected to remain above BoJ's 2% target until the second half of 2025.

In light of these developments, IMF suggests that further increases in BoJ's short-term policy rate should "proceed at a gradual pace" and be "datadependent", considering the balanced risks to inflation and the mixed signals from recent economic data.

IMF emphasizes the importance of Japan's adherence to a "flexible exchange rate regime", which will play a crucial role in absorbing economic shocks and supporting the central bank's focus on maintaining price stability.

Fed’s Jefferson: Restrictive rates necessary amid slow disinflation progress

Fed Vice Chair Philip Jefferson indicated that with the economy showing robust job growth, Fed can focus "even more so" on ensuring that inflation returns to its 2% target. Jefferson acknowledged the slow progress in reducing inflation, asserting that it justifies keeping the policy rate elevated.

"In light of the attenuation in progress, in terms of getting inflation down to our target, it is appropriate that we maintain the policy rate in restrictive territory," Jefferson noted.

He reiterated that the Fed is vigilant in seeking clear evidence of inflation decreasing to the desired level before considering any policy rate adjustments.

Fed's approach is influenced by the varied perspectives among policymakers, which Jefferson believes enriches policy discussions. However, he cautioned that increased communication from Fed might sometimes lead to greater uncertainty about its policies, rather than clarity.

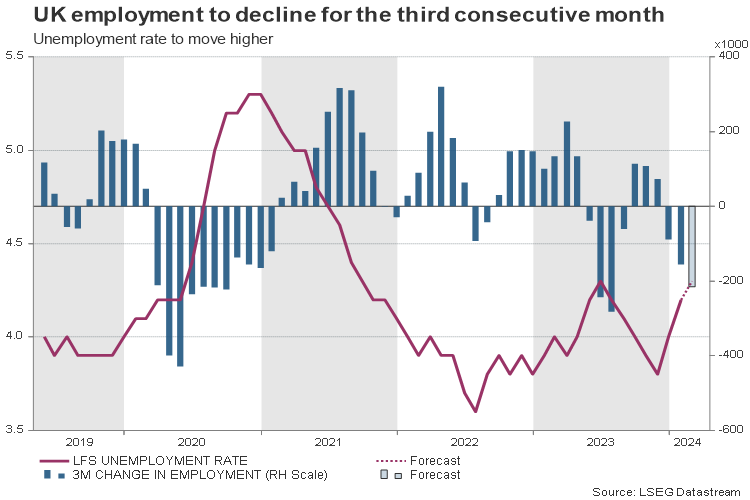

Will UK Jobs Data Give Any Meaningful Signal?

- UK set to report further softening in employment conditions

- Data accuracy issues persist, but wage growth could still move the pound

- GBPUSD needs to gain buying confidence above 1.2700

BoE leans towards a rate cut

The Bank of England (BoE) left interest rates steady at a 16-year high of 5.25% last Thursday as widely expected, and although it did not pre-commit its future policy path, it telegraphed that a summer rate cut is on the cards. While the majority of the board members voted to keep rates steady, Deputy Governor Dave Ramsden joined Shati Dhingra to advocate for an immediate quarter-point reduction.

A downward revision in the central bank’s inflation projections to 1.9% in two years and 1.6% in three years added to the signs that the central bank is likely feeling more confident to shift to the dovish side despite highlighting near-term upside risks in the face of geopolitical factors and persisting upside pressures in the services costs.

Nevertheless, the dovish tilt did not signal the need for an immediate rate cut at the next policy meeting in June. Analysts are still split between a rate cut next month or at some point in the third quarter despite the odds of a June cut increasing to 54% according to futures markets. Moreover, with BoE chief Andrew Bailey requesting a close monitoring of the tight labor market, wage trends, and upside price pressures in the services sector, the central bank might remain data-dependent in the coming months.

Jobs data to soften further; real wages to hold positive

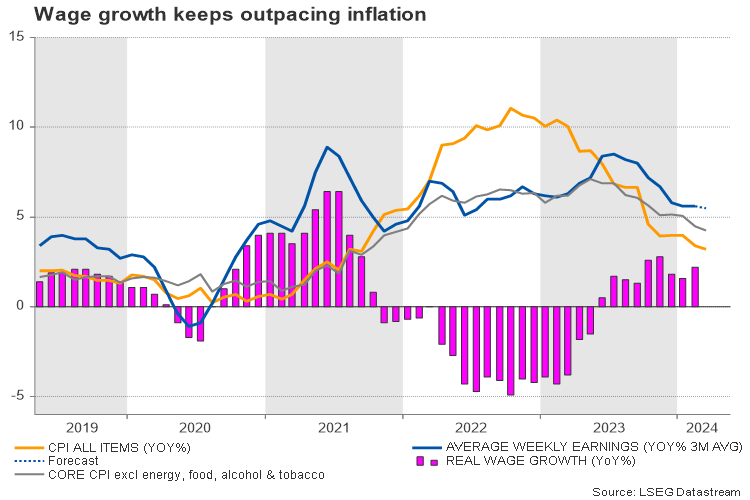

Tuesday’s jobs data is the next key event on the UK calendar and might attract special attention, although the labor survey has lost value after regional stats showed an unexplained variability. Analysts foresee a soft release, with employment falling more aggressively for the third consecutive month by 216k on average over the three months to March compared to a decline of 156k in February. Consequently, the unemployment rate could tick up to 4.3% from 4.2% previously – the highest since September 2023 and March 2018 excluding the pandemic period–, while average hourly earnings could slip from 5.6% to 5.5% but still hold comfortably above the headline inflation rate of 3.2% y/y.

Data accuracy concerns and the fact that there are two more inflation report releases before June’s gathering could mute any market reaction. However, any unexpected changes to wages will not go unnoticed, especially considering that British employers are projected to increase wages by 4.0% in the coming year, as per the recent survey by the Chartered Institute of Personnel and Development.

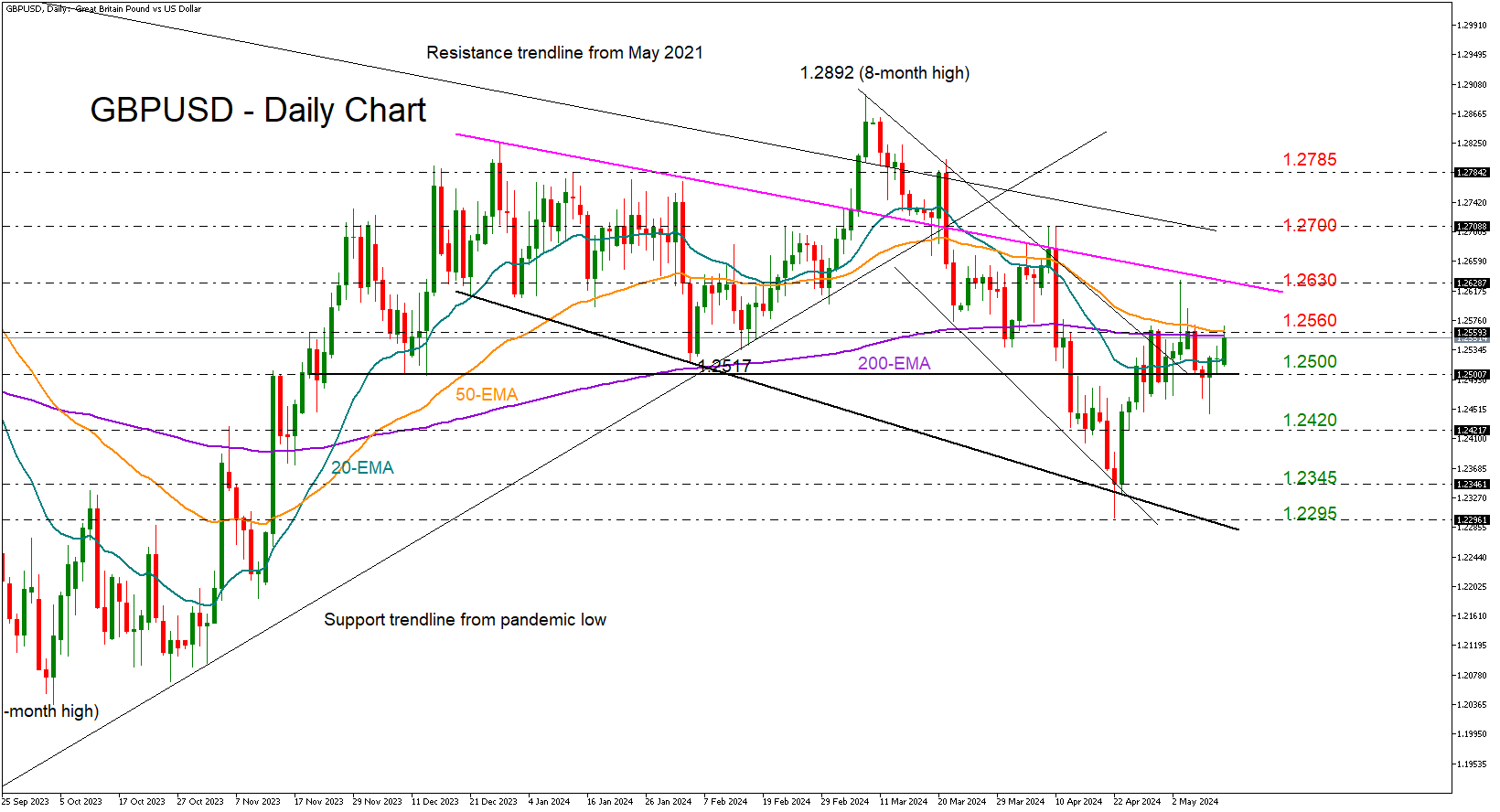

GBP/USD levels to watch

If wage growth exceeds expectations, pushing the rate cut timeline to August, GBPUSD could rise above the resistance zone of 1.2560 and surpass the flattening 50- and 200-day exponential moving averages (EMAs). Still, an extension above the 1.2630-1.2700 trendline territory could be more meaningful.

In the event of a negative surprise, analysts might evaluate how fast or far the central bank might loosen monetary policy after the BoE Governor said that policy might get less restrictive than markets are currently thinking. If the data miss forecasts by a large margin, analysts could bet on a pre-Fed rate cut action in June, causing a downside reversal in GBPUSD. Specifically, a step below 1.2500 could confirm a continuation towards the 1.2420 barrier and then down to the 1.2295-1.2345 restrictive region.