Sample Category Title

Unideal Inflation Dynamics Explain Why Fed Won’t be in a Position to Cut Rates Soon

The FTSE 100 and the Stoxx 600 index closed at a fresh ATH on the back of rising dovish central bank expectations. The EURUSD bounced lower from the 50 and 200-DMA, while Cable tested its own 200-DMA to the upside on the back of strong GDP read last Friday, but the currency pairs need good news from the US inflation front to clear key resistances this week.

Released on Friday, the US Michigan sentiment and expectations numbers were a disaster. Not only the data showed that sentiment tanked in May, but the series of data also pointed at rising inflation expectations for the next year to 3.5%. That’s pretty much in line with where the US CPI has been stagnating since the end of last summer. Worse, the core CPI – which excludes useless stuff like food and energy that no one needs, is coming down slowly, but the index is sitting just a touch below the 4% level – that’s almost twice the Fed’s 2% inflation target. And the unideal inflation dynamics explain why the Federal Reserve (Fed) won’t be in a position to cut the rates soon.

So it’s in this tense and uncertain conditions that the US inflation data will land this week. A consensus of analyst estimates on Bloomberg survey points at a small improvement in both headline and core measures. If that’s the case, investors could breathe a sigh of relief and enjoy the dovish news from other central banks. We would then see the euro and sterling extend gains against the dollar, the yields ease and stock markets surf on a fresh wave of optimism. But if the numbers surprise to the upside for the 4th straight month, it will be hard to keep the Fed hawks contained. The dollar index kicks off the week a touch above the 105 level, the S&P500 is at a spitting distance from an ATH level, the US 2-year yield spiked to 4.87% on Friday, and activity on Fed funds futures gives around 60% chance for a September rate hike from the Fed. It will be interesting to see how the things will evolve from now to the end of the week. I am afraid there is a chance that we see another bad surprise given the surge in many regional Fed surveys.

Happily, the crude oil chart gives some hope regarding the energy inflation. The barrel of US crude fell 1.75% on Friday and slipped below the 100-DMA. The price of a barrel has been unable to make a move above the all-important $80pb level since it fell below this level at the start of May. Yet the geopolitical tensions remain high as Israel doesn’t listen to ceasefire calls from the US and the rest of the world. The US is in a tough position; it can’t really turn its back to its strongest ally, but the situation in Gaza and the rising protests against Biden’s ties with Israel give a very sour taste to Biden’s election campaign. So Biden – who is stuck between a rock and a hard place – vents his frustration on China; he is planning to double, triple or even quadruple levies on some Chinese goods.

China, on the other hand, continues to struggle with its own demons. Released during the weekend, the data showed that consumer inflation rose more than expected in April to 0.3% on a yearly basis, but producer price deflation continues with a 2.5% retreat in April. More disquietingly, the aggregate financing in China fell for the first time in history on the back of slower government bond issuance and a decline in shadow banking. The Chinese CSI 300 index is up by nearly 18% since the February dip. UBS and BNP upgraded their view on MSCI China recently, but the rally remains on a slippery path provided that the geopolitical challenges result in a deepening trade and technology war.

Elsewhere, the earnings calendar is busy with US big retailer earnings this week. The Chinese Alibaba will also report earnings, OpenAI is expected to announce some updates this Monday and Alphabet’s Google hosts its annual developer conference this week, which could bring plenty of AI news on the headlines.

EV Trade Spat Flares Up Amid US Tariff Hike

In focus today

Today will be quiet on the data front, with no major releases scheduled.

The focus for remainder of the week will primarily be on US inflation for April, due Wednesday. Tuesday sees the release of US April PPI, which could give hints on the forthcoming CPI report. In Europe, the German ZEW survey for May is published on Tuesday, followed by euro area industrial production on Wednesday. Friday brings final April inflation data for the euro area, where we especially look out for what drove the still strong service inflation. In Scandinavia, Swedish inflation for April will be the one to watch. Turning to Asia, we get the first estimate of Japanese Q1 national accounts, and Chinese policy rate announcements on Wednesday and the fresh batch of monthly economic data on Friday.

Economic and market news

What happened overnight

The Bank of Japan sent a hawkish signal to markets by cutting the amount of Japanese government bonds it offered to buy in a routine operation. This marks the first cut since December. Specifically, the offer amounts for bonds maturing in 5-10 years was cut to 425 billion yen (USD 2.73 billion) from 475 billion yen at the previous operation on 24 April. The yen initially strengthened, but USD/JPY is currently trading around 155.78, while the 10-year JGB yield is up, hovering around 0.943%.

China's finance ministry reported this morning that it begins selling long-term treasury bonds worth 1 trillion yuan (USD 138.23 billion) this week, with tenors ranging from 20 to 50 years). The initiative was first introduced some weeks ago during China's parliamentary conference in March, and thus not surprising for markets. The funds raised through the issuance will support the rebuilding of disaster-hit areas and infrastructure improvement.

What happened over the weekend and Ascension Day

In the US on Friday, the Flash Michigan survey for May showed a weakening in consumer sentiment and higher inflation expectations. 1y inflation expectations climbed to 3.5%, the highest release since last November, and worryingly, it comes despite the recent downtick in oil prices. Additionally, on Thursday Atlanta Fed President Raphael Bostic (hawk and a voting member) stated that inflation would likely ease under the current monetary settings and allow the Fed to initiate its cutting cycle in 2024. On Friday, Fed official Lorie Logan (hawk and not a voting member) cautioned it is too early to think about rate cuts.

On the political front, the Biden administration intends to increase tariffs on Chinese vehicle imports from 25% to 100%. The initiative is part of an effort to safeguard American industry ahead of the US election and is expected to be announced tomorrow.

In Europe, the ECB minutes from last month's meeting showed increased confidence in reaching 2% inflation and hinted at a potential rate cut in June. For instance, some ECB members already felt confident in a reduction of the policy rates at the April meeting, while the following was phrased in the minutes from Friday: "It was seen as plausible that the Governing Council would be in a position to start easing monetary policy restriction at the June meeting if additional evidence received by then confirmed the medium-term inflation outlook embedded in the March projections".

In the UK, on Thursday, Bank of England (BoE) kept the Bank Rate at 5.25% as widely expected. Additionally, BoE delivered a dovish tweak to its communication, priming markets for an imminent start to a cutting cycle. We continue to pencil in the first 25bp cut in June.

In Sweden, on Wednesday the Riksbank delivered a 25bp cut in accordance with market expectations. Accordingly, the market reaction was muted. We had expected the Riksbank to wait until the June meeting before embarking on its cutting cycle. Thus, we remove our baseline forecast for 25bp in June, but maintain our profile for two 25bp cuts in September and December. For more information, please see Riksbank review - Start of a gradual cutting cycle, 8 May.

In Norway, inflation in April surprised somewhat to the upside, with headline inflation printing 3.5% y/y (0.9% m/m) and core inflation coming in at 4.4% y/y (0.9% m/m). That said, the underlying inflation, measured as a seasonally adjusted 3m moving average of the annualised m/m changes, stood unchanged at 2.8%, signalling that the disinflationary process clearly continues. Services prices excluding rent came in lower than expected, edging down to 4.5% y/y from 5.0% y/y, which should be positive news for Norges Bank, as the main risk currently is that higher wage growth will channel into higher service inflation.

In China, consumer inflation for April came in higher than expected at 0.3% y/y (cons: 0.2%) and 0.1% m/m (cons: -0.1%). The uptick was primarily attributed to price increases within energy, education, and tourism, neglecting the declining food prices. This marks the third consecutive month with prices increasing, indicating a slight recovery in domestic demand.

Market movements

Equities: Global equities ended higher on Friday, marking gains on four out of five days last week. After a nearly 2% gain last week, many of the major indices are now within a hair's breadth of all-time highs. This includes the MSCI World, which is now less than 1% away from its peak in late March. Last week's equities surge was based on a more benign yield environment. Although yields did not decrease, they stayed off their April highs, halting their one-way upward trajectory. Volatility and implied volatility steadily decreased last week, with VIX ending the week at 12.5. Hence, we now argue that the risk on volatility has now shifted to the upside. US markets on Friday were mixed: Dow +0.4%, S&P 500 +0.2%, Nasdaq -0.02%, and Russell 2000 -0.7%. Markets are mixed in Asia this morning, and European and US futures are similarly mixed.

FI: Global rates range-traded in the second half of last week with long-end UST/Bund rates ending the week close to unchanged from their respective starting points last Monday. The US quarterly refunding auctions were well-bid in the 10Y and 30Y segments with bid-to-cover ratios slightly higher compared to the most recent auctions. Additionally, sentiment gained support from the dovish signals coming out from the BoE meeting. As a counterweight to these tailwinds, the Michigan survey released on Friday showed higher inflation expectations among US households in May, which comes despite the downtick in oil prices seen lately. The pricing of ECB rate cuts in 2024 is down to 67bp from 74bp last Monday. The Bund ASW spread is trading at 31.5bp, the lowest level since early April. We keep the view that the Bund ASW-spread should be trading around the 30bp level.

FX: EUR/USD still trades between the 1.07-1.08 mark. EUR/GBP remained close to the 0.86 mark despite stronger than expected GDP numbers and a push-back on imminent rate cuts from the Bo'’s Pill. The kneejerk sell-off in the SEK after the Riksbank cut the policy rate on Wednesday last week has fully reversed with EUR/SEK spot back below 11.70, while EUR/NOK hovers around 11.70.

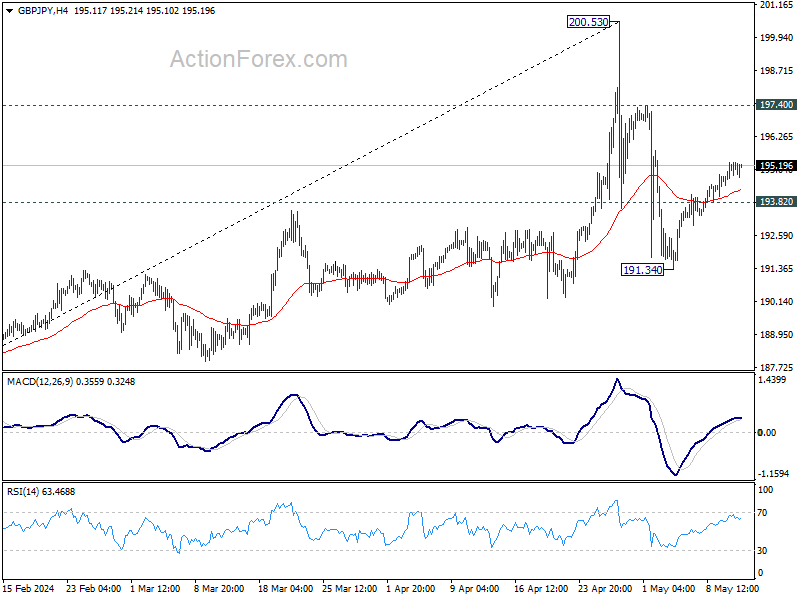

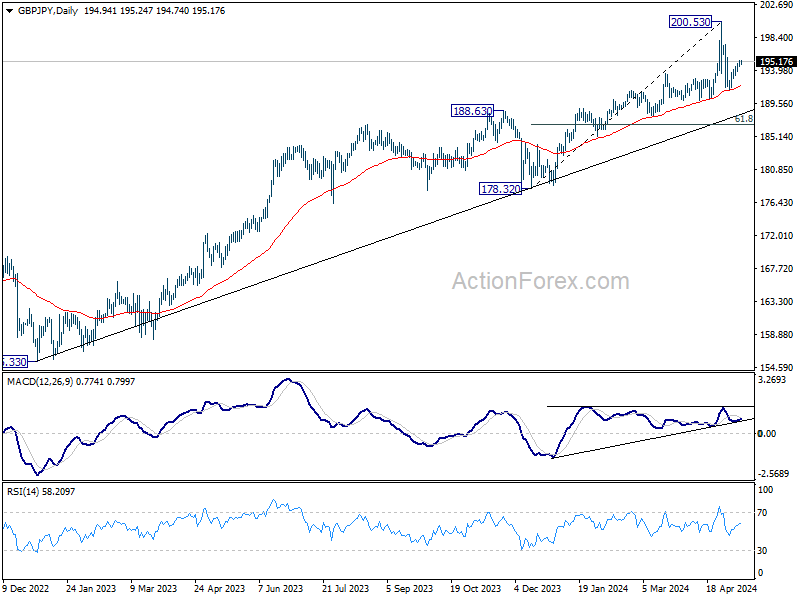

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.62; (P) 194.98; (R1) 195.48; More..

Further rise is mildly in favor in GBP/JPY. Rebound from 191.34 is seen as the second leg of the corrective pattern from 200.53, and could target 197.40 resistance. On the downside, break of 193.82 minor support will argue that the third leg as started, and turn bias back to the downside for 191.34 support.

In the bigger picture, a medium term top could be in place at 200.53 after breaching 199.80 long term fibonacci level. As long as 55 W EMA (now at 183.41) holds, fall from there is seen as correcting the rise from 178.32 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 178.32 support.

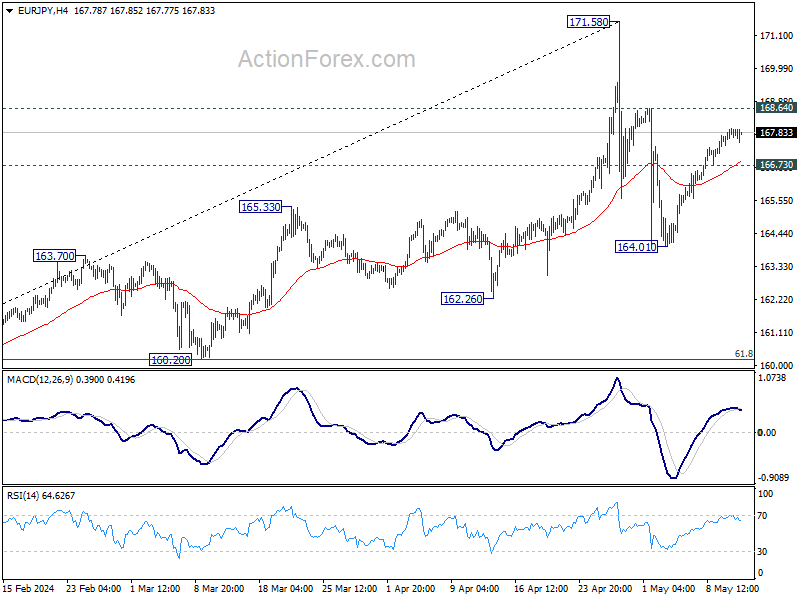

EUR/JPY Daily Outlook

Daily Pivots: (S1) 167.48; (P) 167.72; (R1) 168.03; More...

Further rise is mildly in favor in EUR/JPY despite loss of momentum as seen in 4H MACD. Rebound from 164.01 is seen as the second leg of the corrective pattern from 171.58, and would target 168.64 resistance. On the downside, break of 166.73 minor support will argue that the third leg has started, and turn bias back to the downside for 164.01.

In the bigger picture, a medium top could be formed at 171.58 after brief breach of 169.96 (2008 high). As long as 55 W EMA (now at 157.89) holds, fall from there is seen as correcting the rise from 153.15 only. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

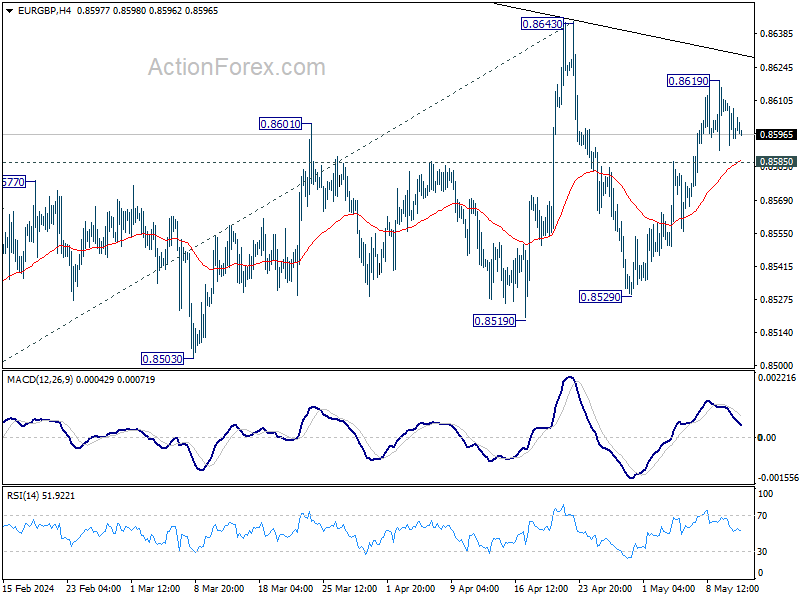

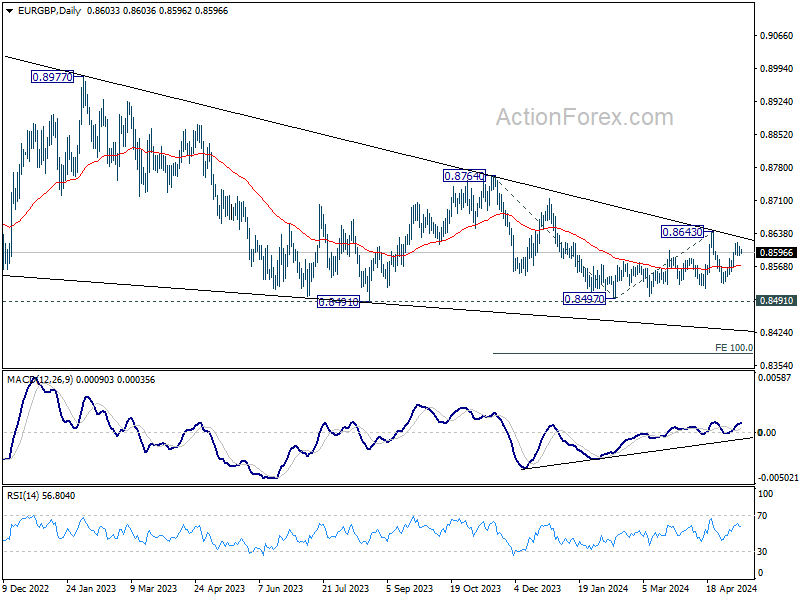

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8592; (P) 0.8602; (R1) 0.8609; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, below 0.8585 minor support will argue that rebound from 0.8529 has completed, and larger fall might be ready to resume. Intraday bias will be back on the downside for 0.8529 support first.

In the bigger picture, outlook remains bearish as EUR/GBP is capped below medium term falling trendline. That is, down trend from 0.9267 (2022 high) is still in progress. Firm break of 0.8491/7 will target 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376.

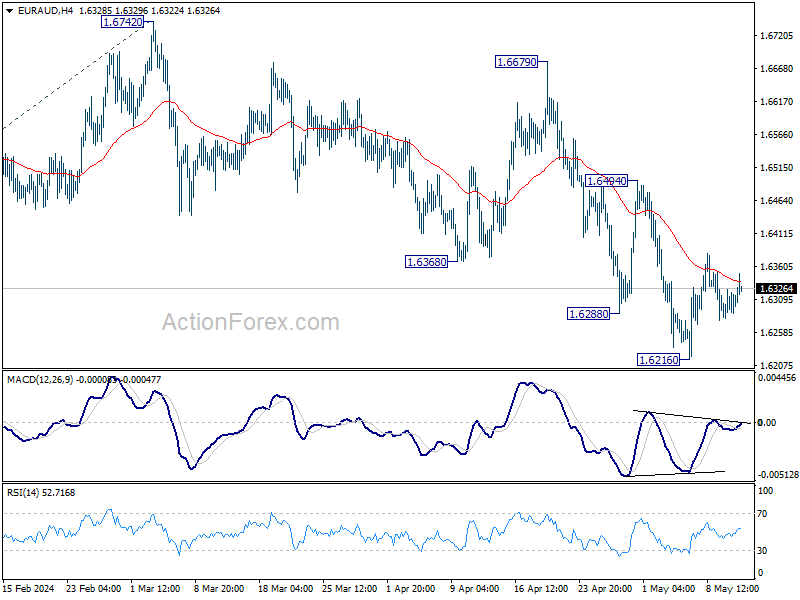

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6287; (P) 1.6307; (R1) 1.6330; More...

Intraday bias in EUR/AUD remains neutral for the moment. While stronger recovery might be seen, further decline is expected as long as 1.6494 resistance holds. Fall from 1.6742 is seen as the third leg of the corrective pattern from 1.7062. Break of 1.6216 will turn bias back to the downside to 1.6127 support, or further to 100% projection of 1.7062 to 1.6127 from 1.6742 at 1.5807.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

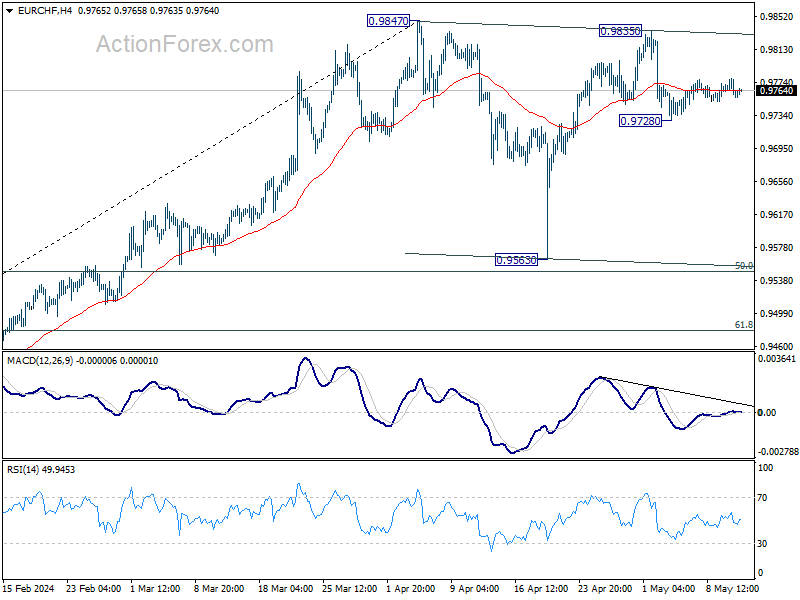

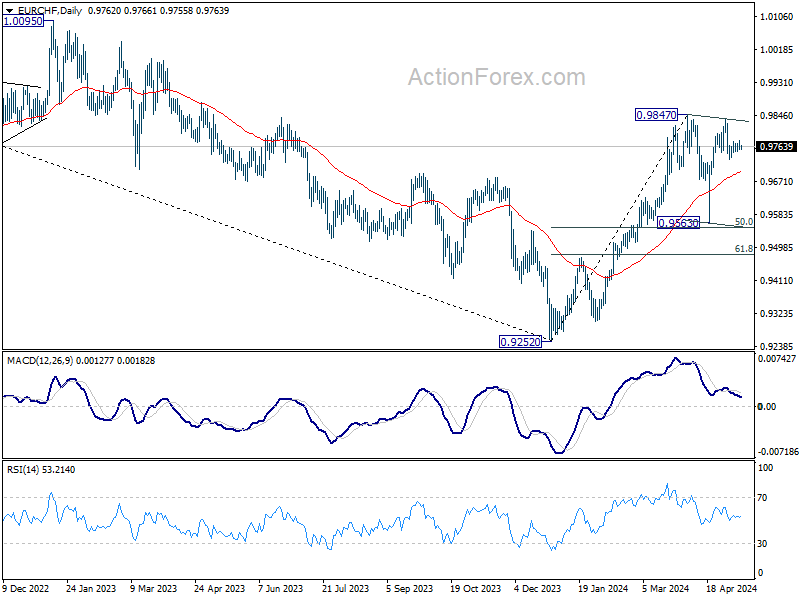

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9755; (P) 0.9767; (R1) 0.9777; More...

Intraday bias in EUR/CHF remains neutral for the moment. Outlook is unchanged that fall from 0.9835 is the third leg of the corrective pattern from 0.9847. Risk will stay on the downside as long as 0.9835 resistance holds. Below 0.9728 will target 0.9563. But strong support is expected from 50% retracement of 0.9252 to 0.9847 at 0.9550 to complete the pattern.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Break of 0.9847 resistance will target 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a correction to the down trend from 1.2004.

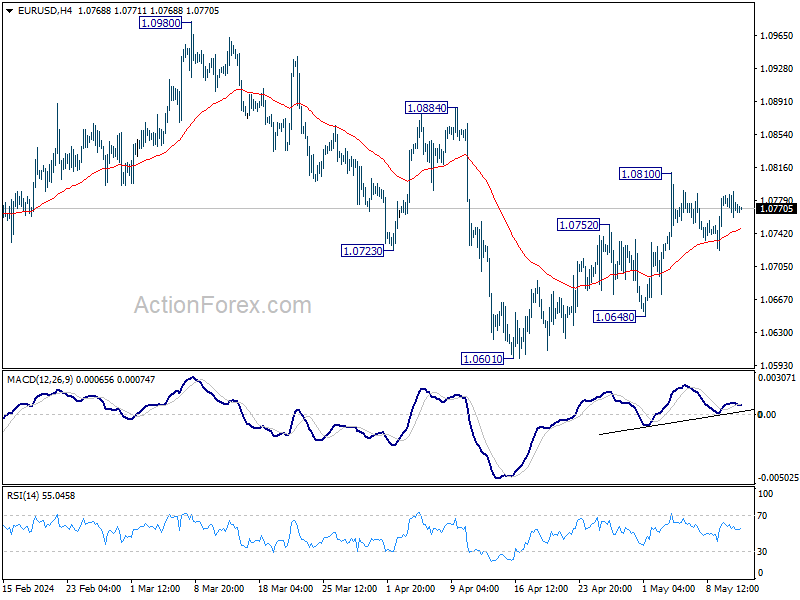

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0757; (P) 1.0773; (R1) 1.0787; More...

Intraday bias in EUR/USD remains neutral for the moment. Further rally is expected as long as 55 4H EMA (now at 1.0747) holds. On the upside, above 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 55 4H EMA will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

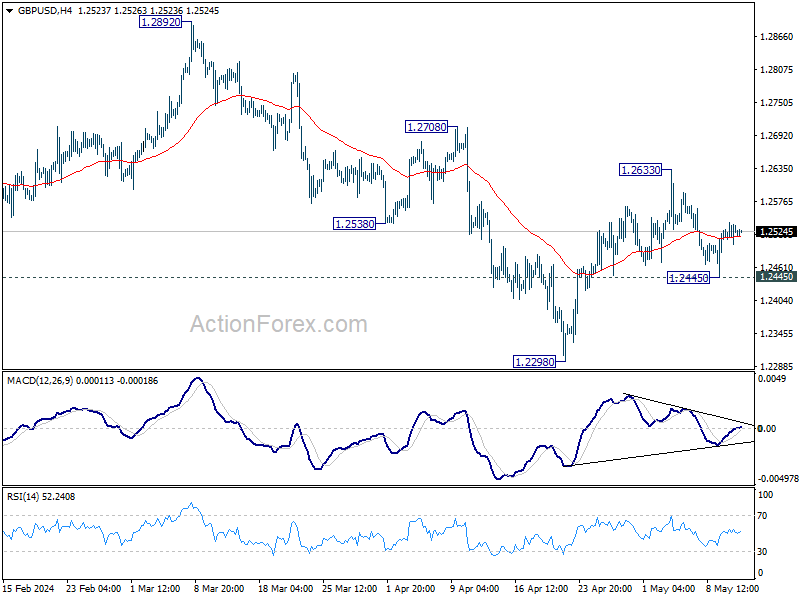

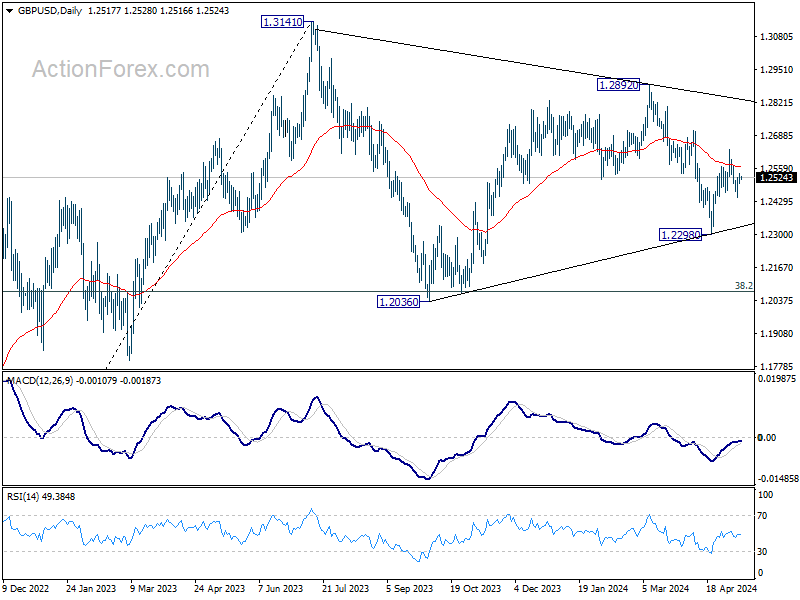

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2504; (P) 1.2523; (R1) 1.2543; More...

Intraday bias in GBP/USD remains neutral for the moment. Further rise is mildly in favor with 1.2445 support intact. On the upside, break of 1.2633 will resume the rally from 1.2298 to 1.2708 resistance next. However, firm break of 1.2445 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

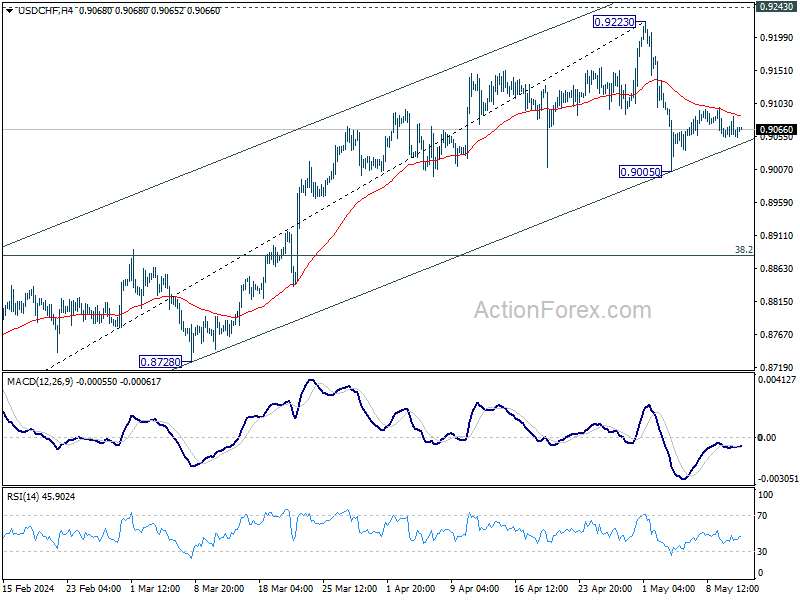

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9048; (P) 0.9066; (R1) 0.9084; More....

Intraday bias in USD/CHF remains neutral for the moment. Further decline is in favor as long as 55 4H EMA (now at 0.9085) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9006) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.