Sample Category Title

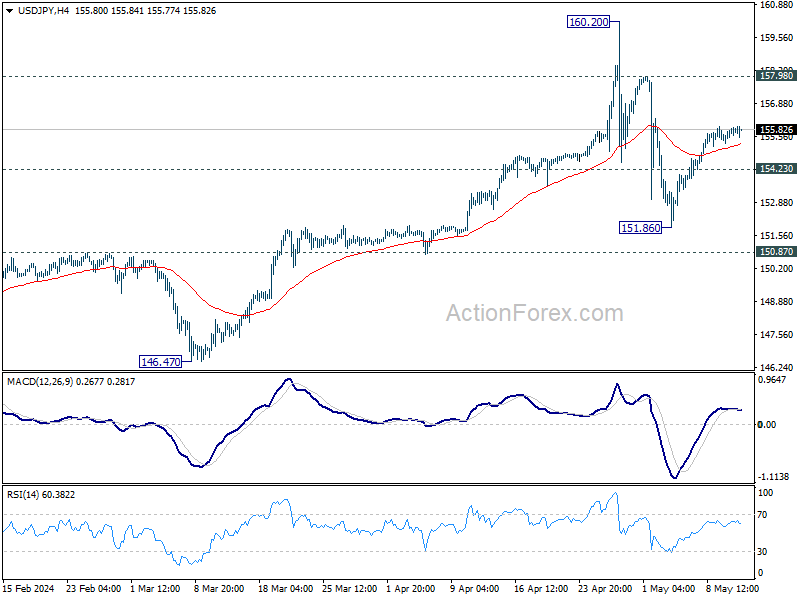

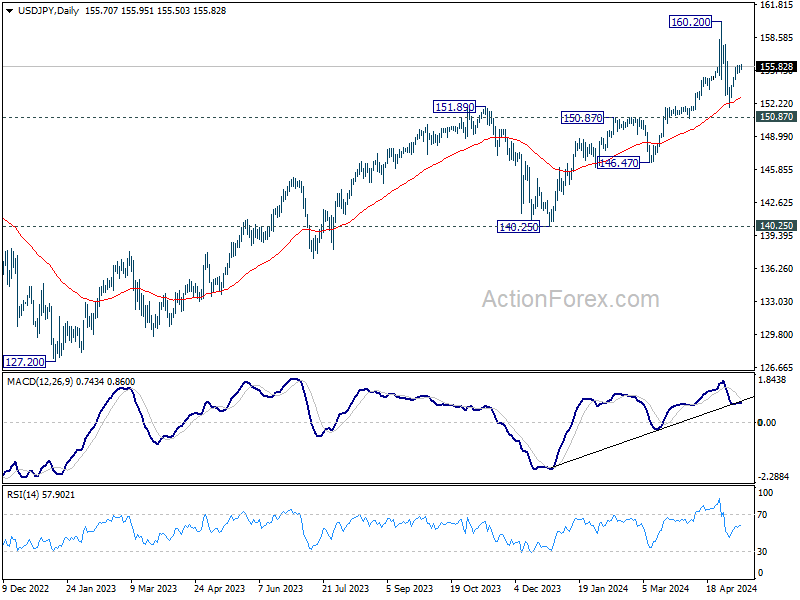

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.38; (P) 155.65; (R1) 156.02; More...

Further rise is mildly in favor in USD/JPY despite loss of upside momentum as seen in 4H MACD. Rebound from 151.86, as the second leg of the corrective pattern from 160.20, could extend towards 157.98 resistance. On the downside, break of 154.23 will suggest that the third leg has started, and turn bias back to the downside for 151.86 support.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

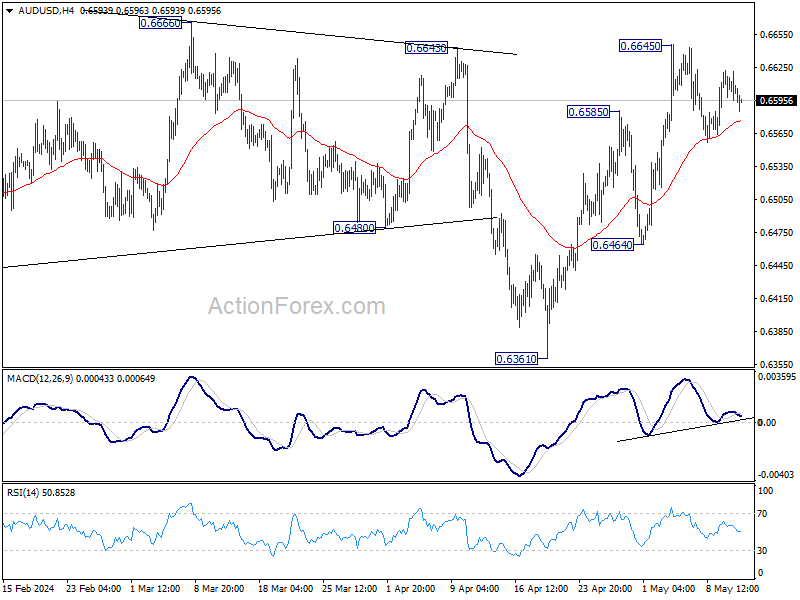

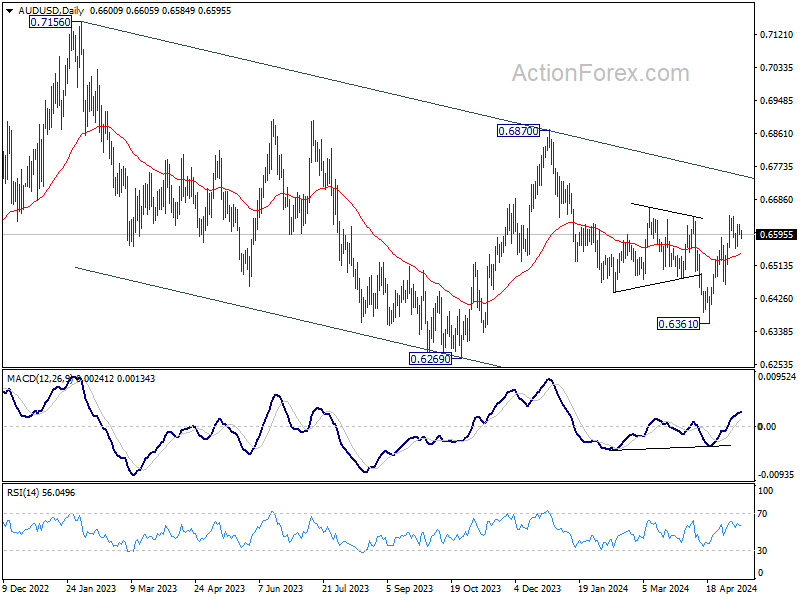

AUD/USD Daily Report

Daily Pivots: (S1) 0.6591; (P) 0.6608; (R1) 0.6620; More...

Intraday bias in AUD/USD remains neutral for the moment. Further rally is in favor as long as 55 4H EMA (now at 0.6577) holds. Above 0.6645 will resume the rebound from 0.6361. On the downside, however, firm break of 55 4H EMA will bring deeper fall back to 0.6464 support instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

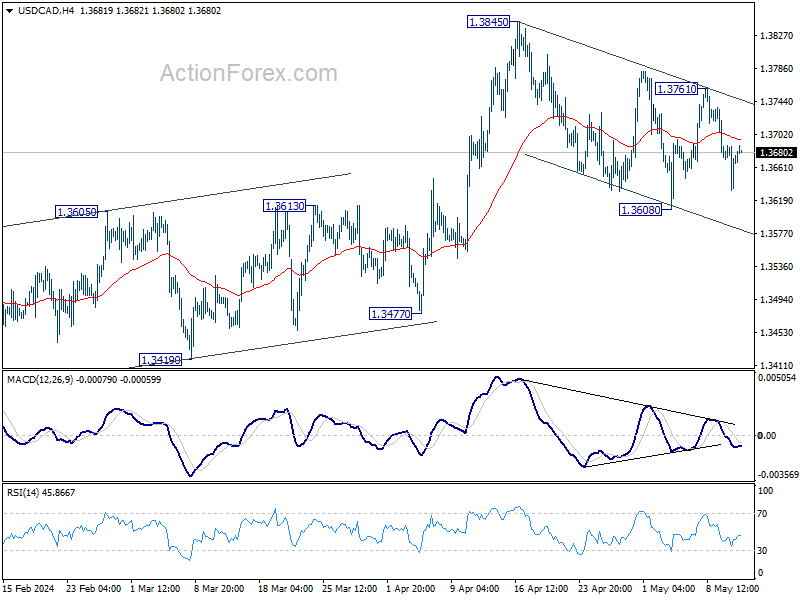

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3641; (P) 1.3667; (R1) 1.3698; More...

Intraday bias in USD/CAD remains neutral for the moment. On the upside, break of 1.3761 resistance will argue that correction from 1.3845 has already completed. Intraday bias will be back to the upside to resume larger rally from 1.3176 through 1.3845. However, sustained trading below 55 D EMA (now at 1.3630) will argue that whole rise from 1.3176 has completed already, and bring deeper fall to 1.3477 support next.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Lower Inflation Expectations Weigh on NZD, Anticipation Builds for US CPI Release

New Zealand Dollar dips mildly as the new week began on a quiet note. This comes in wake of New Zealand weaker services data and the decline in short-term inflation expectations, which may provide some relief to RBNZ about the persistence of high inflation. However, the key question remains on the pace at which inflation will decline. Slower-than-expected disinflation ahead would still limited scope for RBNZ to initiate rate cuts within this year.

Elsewhere in the currency markets, Australian and Canadian Dollars also softened, trailing Kiwi as the next weakest. In contrast, Euro and Sterling appeared stronger, followed by relatively steady Dollar, while Swiss Franc is mixed. But as side from the Aussie and Kiwi, most major currencies remained within Friday's range against each other.

Today's economic calendar appears light, suggesting that trading might remain quiet. However, upcoming reports such as tomorrow's UK employment data and Wednesday's US retail sales and CPI could significantly increase market volatility.

Technically, NZD/USD's rebound from 0.5851 is still in favor to continue as long as 55 4H EMA (now at 0.5984) holds. Break of 0.6044 will target near term channel resistance. Sustained break there will argue that whole fall from 0.6368 has completed with three waves down to 0.5851, and turn near term outlook bullish. However, firm break of 55 4H EMA will argue that rebound from 0.5851 has completed, and retain near term bearishness instead.

In Asia, at the time of writing, Nikkei is down -0.43%. Hong Kong HSI is up 0.47%. China Shanghai SSE is down -0.08%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is up 0.038 at 0.947.

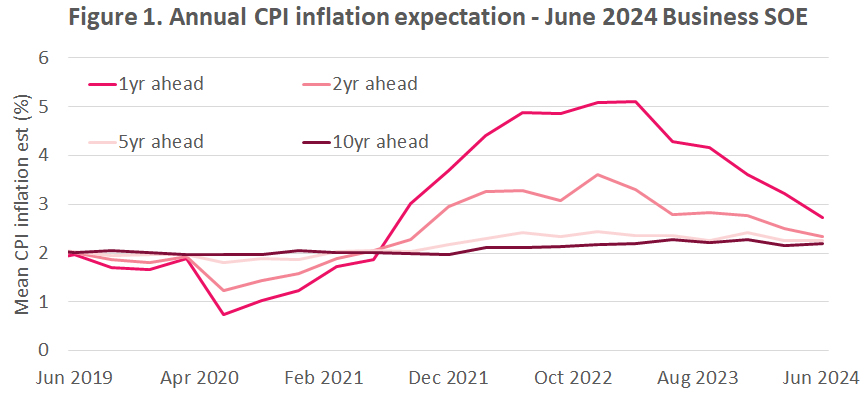

RBNZ survey shows moderating short-term inflation expectations

According to RBNZ Business Expectations Survey for Q2, respondents have lowered their expectations for CPI inflation in both the short-term and medium-term, while their long-term CPI inflation expectations have remained stable.

Specifically, one-year-ahead annual inflation expectations have notably decreased by 49 bps, moving from 3.22% to 2.73%. Two-year-ahead inflation expectations also saw a decline from 2.50% to 2.33%. Five-year-ahead inflation expectations are holding steady at 2.25%. Ten-year-ahead expectations edged up slightly by 3bps, from 2.16% to 2.19%.

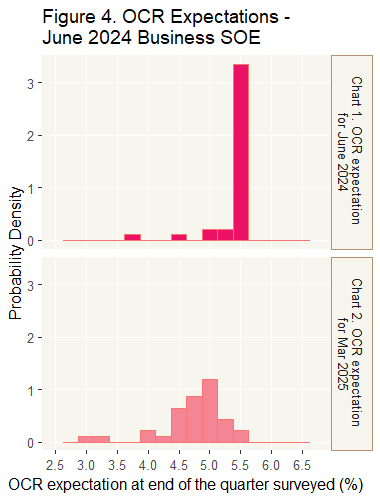

Regarding the Official Cash Rate, survey respondents anticipate that it to 5.46% by the end Q2, similar to current rate at 5.50%. Looking further ahead, they forecast a reduction in OCR to 4.79% by the end of Q1 2025, marking a slight increase from last quarter's prediction of 4.74%. These expectations align with anticipation of approximately three rate cuts by the end of Q1 next year.

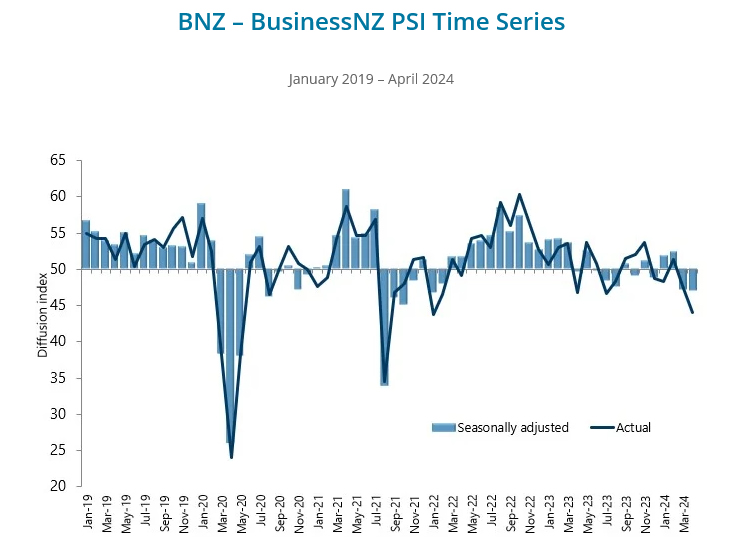

NZ BNZ services dips to 47.1, lowest since early 2022

New Zealand's BusinessNZ Performance of Services Index ticked down from 47.2 to 47.1 in April, marking the lowest level since January 2022.

Breaking down the components of the index reveals mixed signals: Activity and sales saw a modest improvement, rising from 44.8 to 46.5. However, employment took a downturn, dropping from 49.9 to 47.1, recording its lowest level since February 2022. New orders and business also declined slightly to 47.1, from 47.9. Stocks and inventories remained unchanged at 46.6, while supplier deliveries worsened, falling from 48.6 to 47.6—the lowest since November 2022.

The feedback from businesses has increasingly skewed negative, with 66.3% of comments in April being pessimistic, up from 63.0% in March and 57.3% in February. Many respondents highlighted the difficult economic environment and persistent inflationary pressures as significant concerns.

Doug Steel, a senior economist at BNZ, commented on the broader implications of these figures, stating, "combining today's weak PSI with last week's PMI yields a composite reading that would be consistent with GDP tracking below year earlier levels into the middle of this year." He further noted that the combined index suggests there could be "some downside risk" to their current economic forecasts.

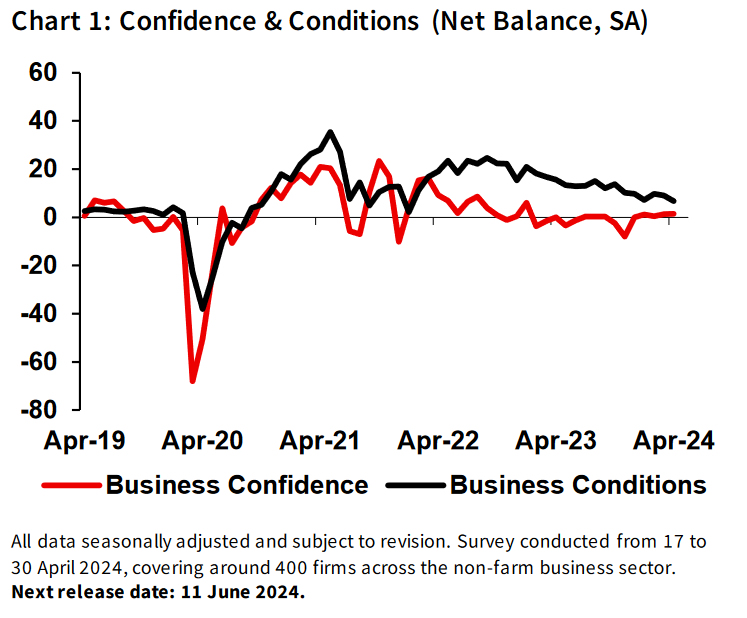

Australia's NAB business confidence steady at 1, conditions normalize with slowing cost growth

Australia's NAB Business Confidence held steady at 1 in April. Business Conditions index fell from from 9 to 7. Notably, trading conditions declined from 15 to 12, while profitability was unchanged at 6. A significant reduction was observed in employment conditions, which dropped from 6 to 2.

NAB Chief Economist Alan Oster reflected on these figures: "All three components of business conditions were back at their long-run averages in April." He described this as a milestone, marking a normalization after the unusually high levels of 2022, "reflecting slowing economic growth."

Labour cost growth decreased to 1.5% from 1.7%, and purchase cost growth slowed to 1.2% from 1.5%. Meanwhile, product price growth rose slightly to 0.9% from 0.7%. Retail price growth moderated significantly to 0.9% from 1.4%.

Oster noted, "There was some further improvement in the pace of cost growth in April, and a step down in the pace of retail price growth." He suggested these changes could indicate easing in inflation in the second quarter, though further observation is needed to confirm this trend.

US CPI and retail sales, UK jobs, and more

US CPI is a major highlight of the week while retail sales will also be released on the same day. Expectations are set for the headline CPI to fall back 3.5% to 3.4% in April. Core CPI is expected to resume its down trend and decrease from 3.8% to 3.6%.

If realized, these anticipated declines do represent modest progress. However, the broader concern remains that momentum in disinflation that was evident last year has largely diminished. This is attributed to a robust labor market that continues to fuel strong consumer spending despite elevated prices and borrowing costs.

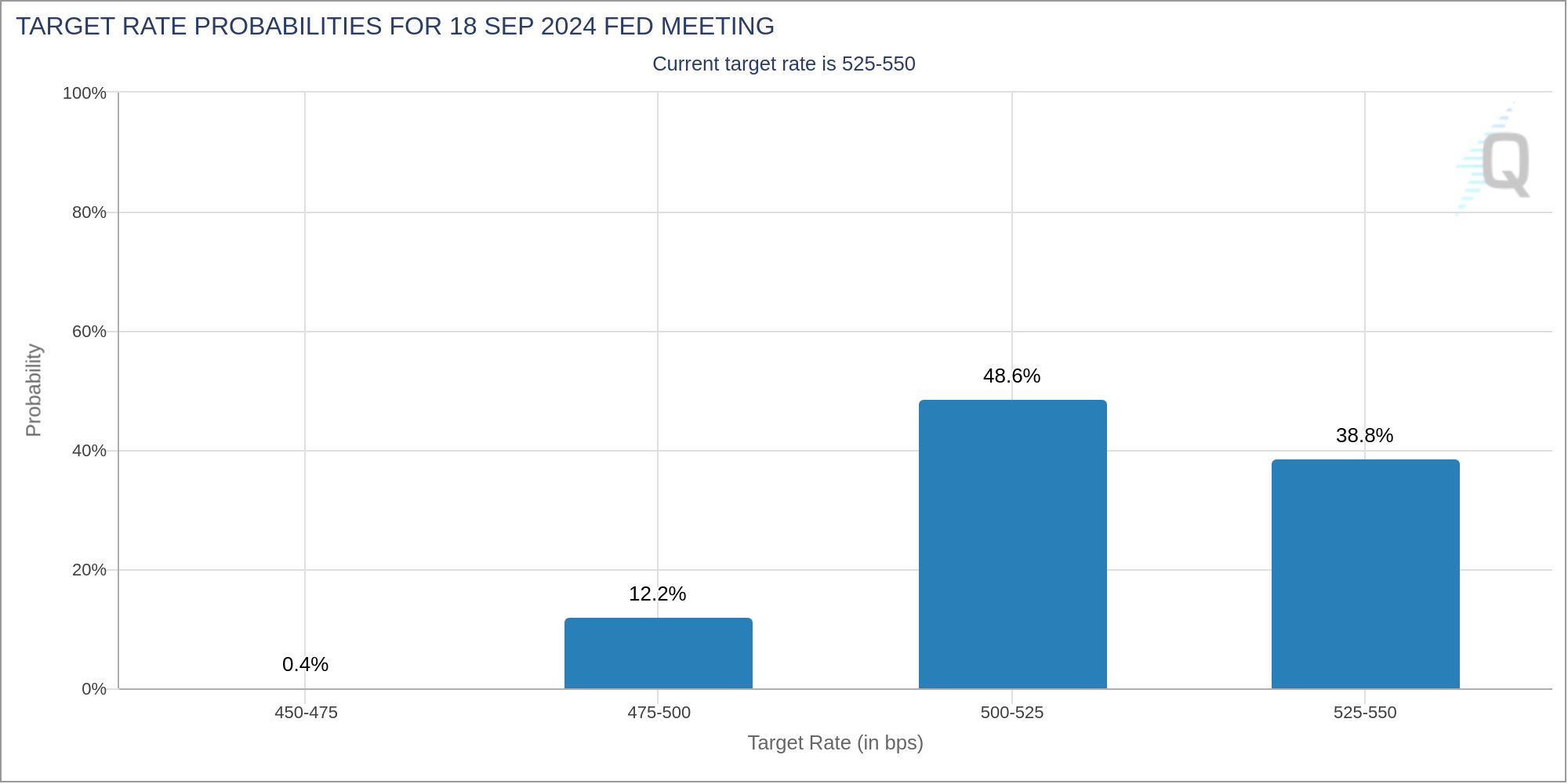

Any upside surprises in inflation figures could revive speculations around the necessity for further rate hikes by Fed, with the current rate level of 5.25-5.50% deemed insufficiently restrictive. Currently, Fed funds futures indicate 61.2% probability of a rate cut in September, with 52.6% chance of two rate cuts within the year. These expectations could shift dramatically following the CPI release.

In the UK, job data will also be closely watched. BoE Governor Andrew Bailey has stated clearly that a June rate cut is "neither ruled out nor a fait accompli." For BoE to consider starting monetary easing, there will need to be additional loosening in the job market, and more substantial slowing in wage growth.

Additionally, other significant economic indicators due this week include Germany's ZEW economic sentiment, Japan's GDP, Australia's wage price index and employment figures, and a series of reports from China, including industrial production, retail sales, and fixed asset investment.

Here are some highlights for the week:

- Monday: New Zealand BNZ services, inflation expectations; Australia NAB business confidence; Swiss SECO consumer climate; Canada building permits.

- Tuesday: Japan PPI; UK employment; Swiss PPI; Germany CPI final, ZEW economic sentiment; Canada wholesale sales; US PPI.

- Wednesday: Australia wage price index; Eurozone GDP revision, industrial production; Canada housing starts, Manufacturing sales; US CPI, retail sales, Empire state manufacturing, business inventories, NAHB housing index.

- Thursday: Japan GDP; Australia employment; US jobless claims, building permits and housing starts, industrial production.

- Friday: New Zealand PPI; China industrial production, retail sales, fixed asset investment; Eurozone CPI final; US leading index.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3641; (P) 1.3667; (R1) 1.3698; More...

Intraday bias in USD/CAD remains neutral for the moment. On the upside, break of 1.3761 resistance will argue that correction from 1.3845 has already completed. Intraday bias will be back to the upside to resume larger rally from 1.3176 through 1.3845. However, sustained trading below 55 D EMA (now at 1.3630) will argue that whole rise from 1.3176 has completed already, and bring deeper fall to 1.3477 support next.

.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Apr | 47.1 | 47.5 | 47.2 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Apr | 2.20% | 2.50% | ||

| 01:30 | AUD | NAB Business Confidence Apr | 1 | 1 | ||

| 01:30 | AUD | NAB Business Conditions Apr | 7 | 9 | ||

| 03:00 | NZD | RBNZ Inflation Expectations Q/Q Q2 | 2.33% | 2.50% | ||

| 07:00 | CHF | SECO Consumer Climate Q2 | -40 | -38 | ||

| 12:30 | CAD | Building Permits M/M Mar | -4.60% | 9.30% |

RBNZ survey shows moderating short-term inflation expectations

According to RBNZ Business Expectations Survey for Q2, respondents have lowered their expectations for CPI inflation in both the short-term and medium-term, while their long-term CPI inflation expectations have remained stable.

Specifically, one-year-ahead annual inflation expectations have notably decreased by 49 bps, moving from 3.22% to 2.73%. Two-year-ahead inflation expectations also saw a decline from 2.50% to 2.33%. Five-year-ahead inflation expectations are holding steady at 2.25%. Ten-year-ahead expectations edged up slightly by 3bps, from 2.16% to 2.19%.

Regarding the Official Cash Rate, survey respondents anticipate that it to 5.46% by the end Q2, similar to current rate at 5.50%. Looking further ahead, they forecast a reduction in OCR to 4.79% by the end of Q1 2025, marking a slight increase from last quarter's prediction of 4.74%. These expectations align with anticipation of approximately three rate cuts by the end of Q1 next year.

NZ First Impressions: RBNZ Survey of Expectations, Q2 2024

Inflation expectations have continued to fall. That will help to quell the RBNZ concerns about the longer-term inflation outlook.

Inflation expectations

- One year ahead: 2.73% (Prev: 3.22%, down 49 points)

- Two years ahead: 2.33% (Prev: 2.50%, down 17 points)

- Five years ahead: 2.25% (Prev: 2.25%, unchanged)

- Ten years ahead: 2.19% (Prev: 2.16%%, up 3 points)

Expectations for inflation over the next few years have continued to drop back in the RBNZ’s latest Survey of Expectations. That follows the fall in actual inflation in recent months.

Looking at the detail of the June quarter report:

- Expectations for inflation one year ahead have fallen sharply for a second quarter, dropping to 2.7%, down from 3.2% in the previous survey.

- Similarly, the closely-watched 2 years ahead measure dropped to 2.33%, down from 2.50% last quarter. This measure is now back around the average seen since 2002 (when we shifted to a 1 to 3% target range for inflation).

- Expectations for inflation 5 and 10 years ahead held broadly steady a little above 2%.

The importance of this survey in the RBNZ’s policy deliberations has fallen over time, with the RBNZ instead preferring to look at a range of different measures of inflation pressures. Even so, today’s result will be welcome news for the RBNZ, and will help to reinforce expectations that inflation will continue to drop back over the course of this year.

The big question for the RBNZ is “how fast will inflation decline?” Over the past year we’ve seen that domestic inflation pressures are proving to be ‘sticky’ – lingering at higher levels than the RBNZ and other forecasters (including ourselves) have expected. Consistent with that, this morning’s monthly price update from Stats NZ pointed to continued upside pressure. While today’s fall in inflation expectations will help to quell concerns about the persistence of domestic inflation, we still think that inflation will fall more gradually than the RBNZ has assumed. Consistent with that, we’re not forecasting rate cuts until early next year.

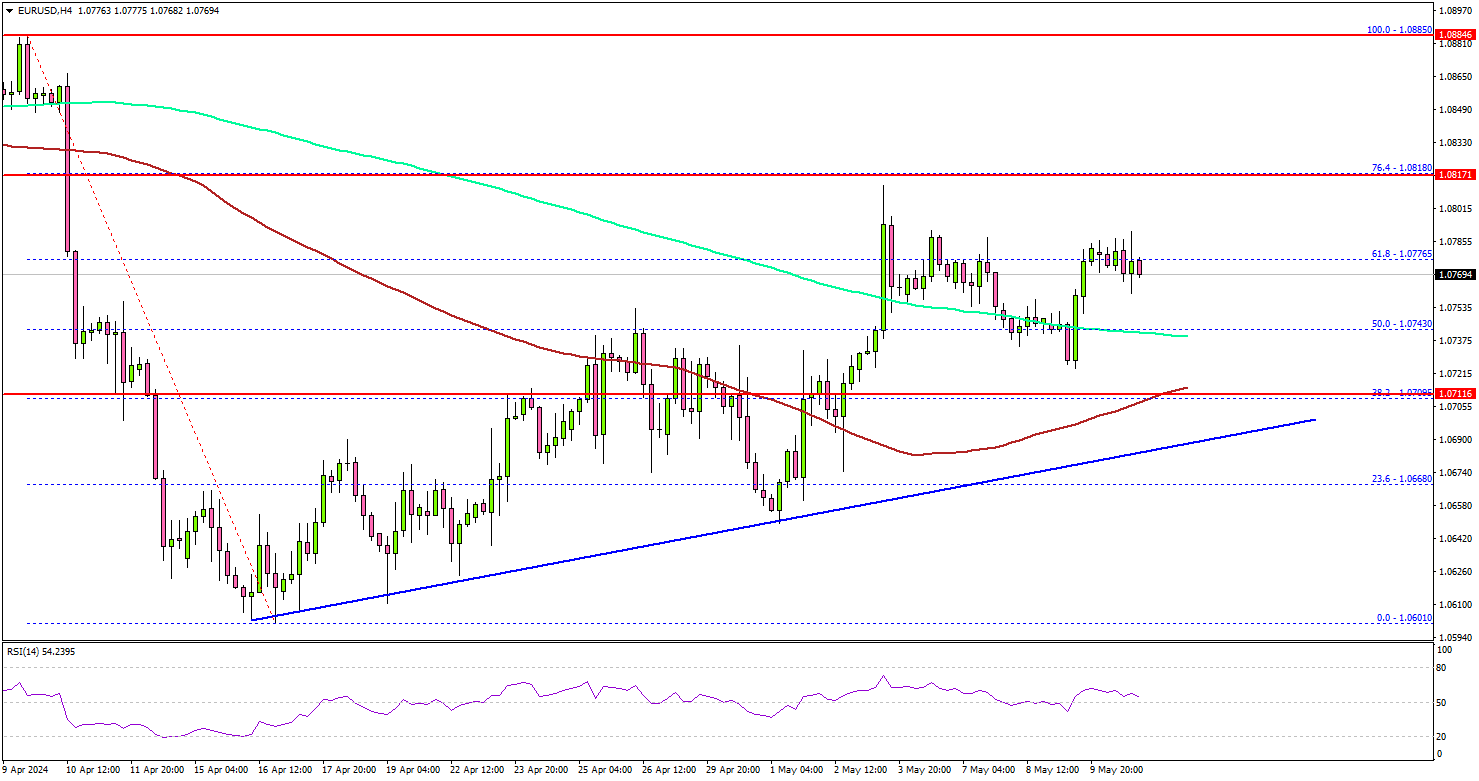

EUR/USD Could Extend Gains Unless This Support Fails

Key Highlights

- EUR/USD started a decent increase and climbed above 1.0750.

- A key bullish trend line is forming with support at 1.0700 on the 4-hour chart.

- Gold prices cleared the $2,335 resistance to move into a positive zone.

- Oil prices are showing bearish signs below the $80.00 region.

EUR/USD Technical Analysis

The Euro started a decent increase above the 1.0685 resistance against the US Dollar. EUR/USD cleared the 1.0720 resistance to move into a positive zone.

Looking at the 4-hour chart, the pair surpassed the 50% Fib retracement level of the downward move from the 1.0885 swing high to the 1.0601 low. It also settled above the 100 simple moving average (red, 4-hour) and tested the 200 simple moving average (green, 4-hour).

The bears are now active near the 1.0800 level. The first major resistance is near 1.0820 or the 76.4% Fib retracement level of the downward move from the 1.0885 swing high to the 1.0601 low.

A clear move above the 1.0820 resistance might send it toward the 1.0865 level. Any more gains might call for a move toward the 1.0920 level in the near term.

Immediate support is near the 1.0740 level and the 200 simple moving average (green, 4-hour). The next major support is at 1.0720. There is also a key bullish trend line forming with support at 1.0700 on the same chart.

If there is a downside break below the 1.0720 support, the pair might test 1.0665. Any more losses might send the pair toward 1.0600.

Looking at Oil, the bears are active below the $80.00 resistance zone and they might aim for more losses in the near term.

Economic Releases

- Eurogroup Meeting.

- Fed's Jefferson speech.

Australia’s NAB business confidence steady at 1, conditions normalize with slowing cost growth

Australia's NAB Business Confidence held steady at 1 in April. Business Conditions index fell from from 9 to 7. Notably, trading conditions declined from 15 to 12, while profitability was unchanged at 6. A significant reduction was observed in employment conditions, which dropped from 6 to 2.

NAB Chief Economist Alan Oster reflected on these figures: "All three components of business conditions were back at their long-run averages in April." He described this as a milestone, marking a normalization after the unusually high levels of 2022, "reflecting slowing economic growth."

Labour cost growth decreased to 1.5% from 1.7%, and purchase cost growth slowed to 1.2% from 1.5%. Meanwhile, product price growth rose slightly to 0.9% from 0.7%. Retail price growth moderated significantly to 0.9% from 1.4%.

Oster noted, "There was some further improvement in the pace of cost growth in April, and a step down in the pace of retail price growth." He suggested these changes could indicate easing in inflation in the second quarter, though further observation is needed to confirm this trend.

NZ BNZ services dips to 47.1, lowest since early 2022

New Zealand's BusinessNZ Performance of Services Index ticked down from 47.2 to 47.1 in April, marking the lowest level since January 2022.

Breaking down the components of the index reveals mixed signals: Activity and sales saw a modest improvement, rising from 44.8 to 46.5. However, employment took a downturn, dropping from 49.9 to 47.1, recording its lowest level since February 2022. New orders and business also declined slightly to 47.1, from 47.9. Stocks and inventories remained unchanged at 46.6, while supplier deliveries worsened, falling from 48.6 to 47.6—the lowest since November 2022.

The feedback from businesses has increasingly skewed negative, with 66.3% of comments in April being pessimistic, up from 63.0% in March and 57.3% in February. Many respondents highlighted the difficult economic environment and persistent inflationary pressures as significant concerns.

Doug Steel, a senior economist at BNZ, commented on the broader implications of these figures, stating, "combining today's weak PSI with last week's PMI yields a composite reading that would be consistent with GDP tracking below year earlier levels into the middle of this year." He further noted that the combined index suggests there could be "some downside risk" to their current economic forecasts.

Morning Report

Key themes: A sharp fall US consumer confidence added to evidence that the US economy is losing some momentum. However, an uptick in consumer inflation expectations complicated the picture, prompting suggestions of the risk of stagflation. A flurry of Fed speakers reinforced higher for longer messaging but backed up Jerome Powell in watering down the risk of further rate hikes.

US equities unwound early gains but finished in the green, posting a third consecutive weekly rise.

Treasury yields rose across the curve but remained broadly within the last week’s trading range.

The higher yield structure supported the US dollar which gained against the Yen, the euro, the Pound and the Aussie.

Share markets: US equities started strongly on Friday night but lost ground following the consumer sentiment report which showed expectations soured and inflation expectations rose. The S&P 500 rose 0.2% to close the week up 1.9%, the third consecutive weekly gain. The NASDAQ was flat on Friday but ended the week 1.1% higher.

The ASX 200 rose 0.4% on Friday. Futures traded lower, pointing to a soft start to the week.

Interest rates: US treasury yields rose across the curve, supported by higher consumer inflation expectations and further comments from Fed officials reinforcing higher for longer interest rates. The 2-year yield rose 5 basis points to 4.87%, while the 10-year yield increased 4 basis points to 4.50%. There remains one 25-basis point Fed rate cut fully priced by the end of the year. The implied probability of a second has pulled back to around 60%.

The Aussie 3-year futures yield rose 3 basis points to 3.99%, while the 10-year yield rose 4 basis points to 4.37%. Market pricing for interest rates suggests the RBA will leave rates unchanged for the remainder of 2024, with a very slight risk of a rate hike priced in.

Foreign exchange: The higher rates structure provided the US dollar with a mild tailwind. The DXY rose from a low of 105.14 to a high of 105.40 and is currently trading around 105.30. However, a clear downtrend since mid-April remains in-tact alongside increasing signs economic growth is fatiguing.

The Aussie dollar slipped from a high of 0.6623 to a low of 0.6596 but managed to regain some ground to finish above the 66-cent handle. The euro, Japanese Yen and British Pound all. The USD/JPY tested and failed resistence at the 156 level for a second consecutive session.

Commodities: The West Texas Intermediate (WTI) price of oil fell 1.3% to US$78.26 per barrel. Copper (1.2%) and gold (0.6%) both gained while iron ore (-0.3%) slipped.

Australia: There were no major economic data releases on Friday.

China: The consumer price index (CPI) rose just 0.3% over the year to April suggesting sluggish demand continues to weigh on the economy. However, the slim price increase was slightly stronger than expected and marked an improvement on March’s reading which narrowly skirted deflation.

The producer price index (PPI), which measures prices faced by businesses, recorded an annual fall for a 19th consecutive month, dropping 2.5% over the year to April. The weak PPI is a sign that deflationary risks remain and that the economy likely requires further policy support for the tentative economic recovery to gain additional momentum.

The current account surplus narrowed to US$39.2bn in the March quarter, down from a $56.2bn surplus in the December quarter.

Japan: The current account surplus widened to a record ¥3.4tr in March from ¥2.6tr in February.

United Kingdom: Activity bounced back solidly from a shallow recession at the end of last year. GDP rose 0.6% in the March quarter, beating expectations for a 0.4% quarterly gain and marking the strongest quarter gain in over two years. In annual terms, GDP growth swung form a 0.2% decline to a 0.2% increase.

Business investment and industrial production surprised to the upside, while there was a smaller than expected drag from imports. This helped offset weakness in private consumption, government spending and in construction activity.

United States: Consumer sentiment soured in March falling to its weakest level in six months. The University of Michigan consumer sentiment index fell to 67.4 in May, falling short of expectations of 76.2 and representing a sharp fall on April’s reading of 77.2. Perceptions of both current future economic conditions deteriorated, while both short and long-term inflation expectations ticked up marginally to 3.5% and 3.1%, respectively. The rise in inflation expectations likely reflects stalling disinflation progress and will do little to help cool price pressures.

Several Fed members spoke on Friday, echoing the higher-for-longer messaging from Jerome Powell and reinforcing the expectations that further rate hikes are unlikely to be necessary.

Chicago Fed President Austan Goolsbee said he doesn’t see much evidence inflation I stuck above the Fed’s target but was reluctant to say when rate cuts might be appropriate. Lorie Logan, Dallas Fed Chief, said “it’s just too early to think about cutting rates” while Fed Governor Michelle Bowman said she doesn’t expect it will be appropriate for the Fed to cut interest rates in 2024, pointing to persistent inflation in the first several month of the year.