Sample Category Title

Morning Report

Key themes: Markets were in a holding pattern overnight as investors await key US inflation data later this week. US Fed Chair Powell is also due to speak, possibly providing further insights on future rate moves.

US equities were mixed and lack direction for most of the session. US bond yields were broadly unchanged, with stronger than expected consumer inflation expectations data driving yields higher late in the session. The US dollar was softer.

The local share market finished flat ahead of today’s 2024-25 federal budget. The government revealed overnight that it expects a $A9.3bn surplus this financial year. The key question for markets is whether the government can strike the right balance between providing cost-of-living support and continuing to take pressure off inflation.

Share markets: US equities drifted to a mixed finish. Investors are in a holding pattern ahead of key inflation data which includes the release of US producer price data on Tuesday, and the consumer price index on Wednesday.

The S&P 500 was broadly unchanged closing at 5,221.42 after flipping between small gains and losses through the session. The Dow Jones fell 0.2% to 39,431.51. The Nasdaq rose 0.3% to 16,338.24.

The ASX 200 was flat, closing at 7,750.0 ahead of the 2024-25 federal budget. Health and consumer equities advanced, while energy stocks declined in line with the fall in oil prices. Futures are pointing to a soft open today.

Interest rates: US bond yields were broadly unchanged. After falling in early trade, yields recovered on the back of stronger than expected consumer inflation expectations data released by the New York Fed.

The 2-year bond yield was unchanged at 4.86%, after reaching a low of 4.82%. The 10-year treasury yield declined by 1 basis point to 4.49%, after reaching a low of 4.46%.

Interest-rate markets continue to price a full rate cut by November. For 2024, the market is pricing in around 40 basis points of cuts – slightly less than two 25-basis-point moves.

Australian yields were also flat. The 3-year government bond yield (futures) was down by 1 basis point, at 3.95%. The 10-year government bond yield (futures) was up by 1 basis point, at 4.35%.

Foreign exchange: The US dollar was softer. The DXY index fell to a low of 105.06, before receiving yield support and staging a recovery late in the day to reach a high of 105.37. The DXY Index is trading at around 105.23.

The Aussie flipped between minor gains and losses, remaining around the 0.6600 level. Through the session, the AUD/USD moved from a low of 0.6586 to a high of 0.6629. The pair is currently trading at around 0.6606.

Commodities: Commodities were mixed. Oil and copper were higher. Gold and coal were lower. Iron ore was unchanged.

The West Texas Intermediate (WTI) futures is currently sitting at around US$79.12 per barrel.

Iron ore reached a high of almost US$118.0 per tonne following speculation the Chinese government will use capital, raised through the sovereign bond issuance program announced yesterday, to support the economy and property sector.

Australia: Business confidence and conditions were little changed in April. Conditions slipped 2 points to +7 index points. This is below the 10-year average but around the long-term average of the monthly series. Confidence was unchanged in the month, remaining just in positive territory, at +1 index points. Confidence among businesses has fluctuated around neutral levels for a little over 18 months, with occasional bumps higher or lower in certain months.

Quarterly measures of labour and purchase cost growth - key inputs for businesses - were both softer in the month, at 1.5% and 1.2%, respectively. Retail price growth slowed to the second slowest pace since January 2021, at 0.9% on a quarterly equivalent basis.

From a big picture perspective, little has changed in April. Conditions continue to gradually trend lower but remain around long-run average levels, while businesses are still cautious about the future. 2024 is expected to be a year of two halves. While conditions remain challenging in the first half of the year, a gradual recovery is expected to take place from the second half of 2024, before picking up more pace into 2025.

United States: The New York Fed consumer inflation expectations survey for April showed a sharp increase in expectations for the year ahead - 3.3% from 3.0% in March. Inflation expectations for five years ahead also increased, from 2.6% in March to 2.8% in April.

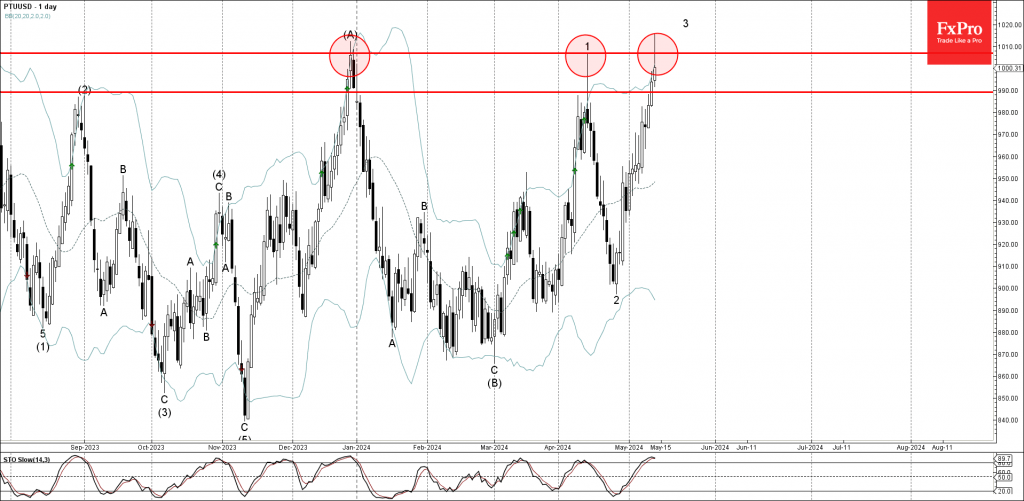

Platinum Wave Analysis

- Platinum reversed from resistance level 1010.00

- Likely to fall to support level 990.00

Platinum just reversed down from the major resistance level 1010.00, which has been reversing the price from the end of December.

The resistance level 1010.00 stands well above the upper daily Bollinger Band – increasing the possibility of the sharp correction in the near-term future.

Give the strength of the resistance level 1010.00, overbought daily Stochastic, Platinum can be expected to fall further toward the next support level 990.00.

Brent Crude Oil Faces Downward Pressure Amid Demand Uncertainties

The price of Brent crude oil is currently experiencing a downturn, trading around 82.55 USD per barrel this Monday. The primary concern affecting the market today is the uncertainty surrounding demand levels, exerting significant pressure on the commodity.

Recent statements from representatives of the US Federal Reserve have led to expectations that interest rates may remain elevated for an extended period. This prospect of sustained high rates is likely to dampen economic growth, which could, in turn, negatively impact fuel demand from American consumers. The likelihood that the Fed will maintain current lending rates throughout the year is considered relatively high.

Additionally, data released on Friday showed a marked decline in US consumer confidence, reinforcing concerns that the economy might be losing its growth momentum. As we approach the summer season, traditionally a peak period for fuel consumption, the latest reports indicate rising stocks of petrol and distillates in the US. However, demand appears lacklustre, contradicting typical seasonal trends.

The next OPEC meeting is scheduled for early June. The group is expected to extend its production quotas into the second half of the year, a decision that could further impact oil price movements.

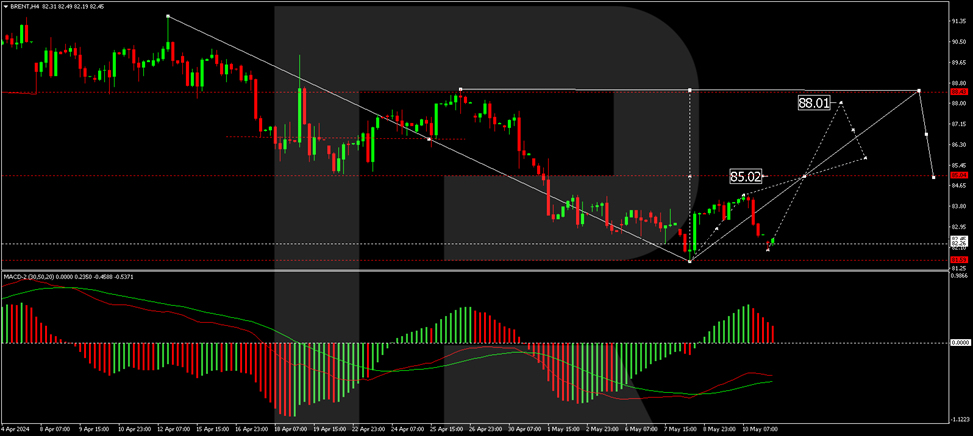

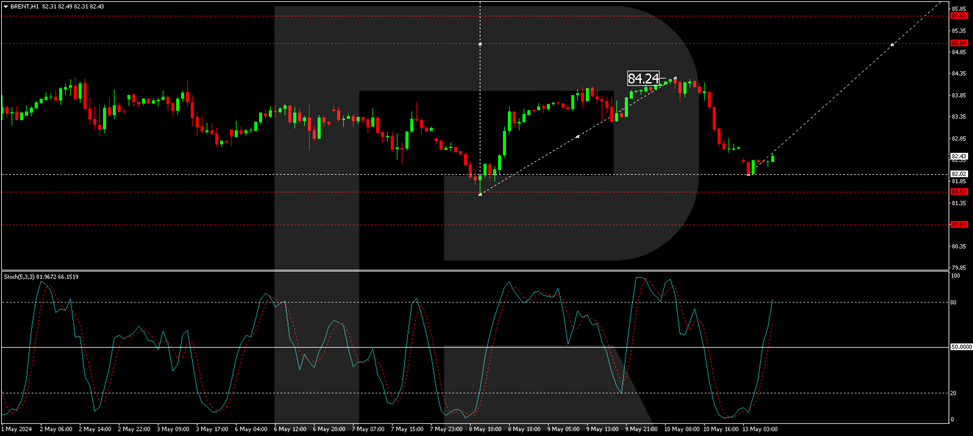

Brent technical analysis

The Brent H4 chart's initial growth impulse to 84.24 has been completed, and the subsequent correction wave nearing 82.02 is almost finished. We anticipate the formation of a consolidation range above this level. If the price breaks upwards from this range, a growth to the level of 85.00 is expected, potentially extending to 88.00. This bullish scenario is technically supported by the MACD indicator, whose signal line is below zero but pointing upwards from the lows.

On the H1 chart, after completing the growth structure to 84.24, the market has finalised its correction at 82.02. A consolidation range above this level is expected to form. A breakout upwards from this range could initiate a new growth wave towards 85.00. The Stochastic oscillator corroborates this potential upward movement, with its signal line currently above 20 and aiming towards 80, suggesting a bullish momentum could be building.

Sunset Market Commentary

Markets

All eyes are on Wednesday’s US CPI inflation print and to a lesser extent its PPI precursor tomorrow. That led to stoic, listless trading at the start of the new week. China announced during early Asian dealings that it will kick off its CNY 1tn stimulus plan on Friday with a CNY 40bn 30-yr auction of special bonds (of which the proceeds are used for predetermined investments). It’s the first round of the many that will stretch the year through November, with maturities ranging between 20 and 50 year. News of the rare event (China has issued special bonds on four occasions only, this one included) pulled Chinese equities from the intraday lows but had little impact on markets ex-China. European stocks lose some minor ground with the likes of the EuroStoxx50 shedding 0.2%. US stocks open with marginal gains of about 0.3%. Most commodities are well bid with oil seeking a gain to $83/b after a sharp drop earlier this month. Copper is on track for the highest close since April 2022. Core bonds gained some ground with a slight outperformance of US Treasuries vs German Bunds. US yields ease between 2.4 (30-yr) and 3.4 bps (2-yr). German rates give up 1.7-2.8 bps across the curve. Japanese yields are the odd one out today, having added up to 2.7 bps at the long end of the curve. This followed the Bank of Japan offering to purchase a smaller amount of government 5-to-10 year bonds in a regular operation than it did the previous time (April 24). While the amount was still within the planned range for the running quarter, it is seen as a baby step by the central bank to reduce its presence in the debt market and an attempt to support the ailing currency. The Japanese yen barely, if at all, profits though. USD/JPY holds steady around 155.7 even as the US dollar is suffering a bit from the Monday blues. DXY eases from 105.3 to 105.12 currently. EUR/USD is flirting with the 1.08 big figure compared to an 1.768 open. Technically, resistance is spotted at 1.0807, followed by 1.0885 (38.2% recovery on the December-April decline; April correction high). Sterling whipsawed within an extremely tight trading range between 0.8595 and 0.8611. The UK labour market is scheduled for release tomorrow. It’s one of the two reports that the Bank of England receives ahead of the June policy decision, along with two CPI prints. The data will be crucial with the central bank in last week’s meeting looking to cut rates sooner rather than later.

News & Views

Czech inflation in April accelerated more than expected by 0.7% M/M with the Y/Y-figure approaching the upper band of the tolerance band around the Czech National Bank’s 2% inflation target (2.9% from 2% in March). The CNB in its spring monetary policy report (published early May) only expected a rebound to 2.5% Y/Y. The deviation was mainly due to food prices which rose 1% Y/Y instead of the projected -0.5% Y/Y decline. In line with expectations, core inflation slowed slightly further to 2.6% Y/Y. The CNB reacted that the qualitative message of the spring forecast remains valid with inflation moving back close to the 2% target throughout the year. The Czech koruna rallied after inflation numbers with EUR/CZK testing the 200-day moving average at 24.75 (strongest CZK-level since early February). CZK swap rates rose up to 9 bps at the front end of the curve. Today’s figures strengthen the case for a reduction in the CNB rate cut pace from the next meeting onwards (25 bps instead of 50 bps).

Polish Monetary Policy Council member Kotecki currently doesn’t see any room for interest rate cuts. Some room may come at the end of the year if wage growth slows. It doesn’t seem to be the base case and any potential rate cut will just be the minimal 25 bps. MPC Wnorowski also sees stable rates in 2024 as the base scenario and even thinks that the likelihood of a rate cut this year is smaller than a month ago. He also thinks that 2025 is too distant of a future to give already guidance on the scale of any potential cuts. The Polish zloty at EUR/PLN 4.30 holds strong against the euro.

Graphs

EUR/CZK: Czech crown rallies after CPI accelerates more than expected, bolstering case for slowdown the easing pace

Japanese 10-yr yield rises to new YtD high after BoJ cuts buying amount in regular bond auction

Copper prices on track for highest close since early 2022. Will Chinese stimulus boost demand further?

EUR/USD attacks 1.0805 in quiet trading and ahead of important US data tomorrow (PPI) and Wednesday (CPI)

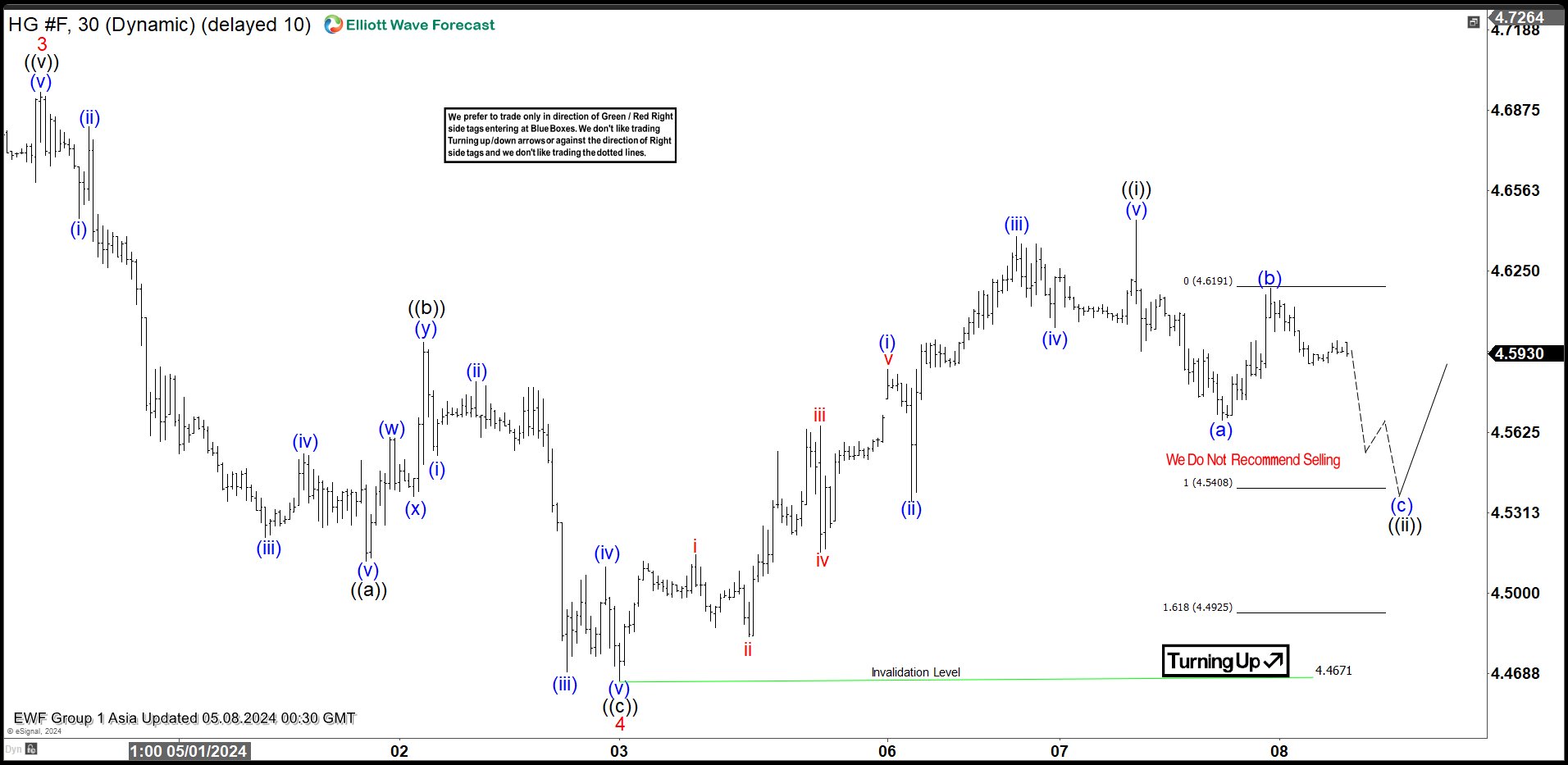

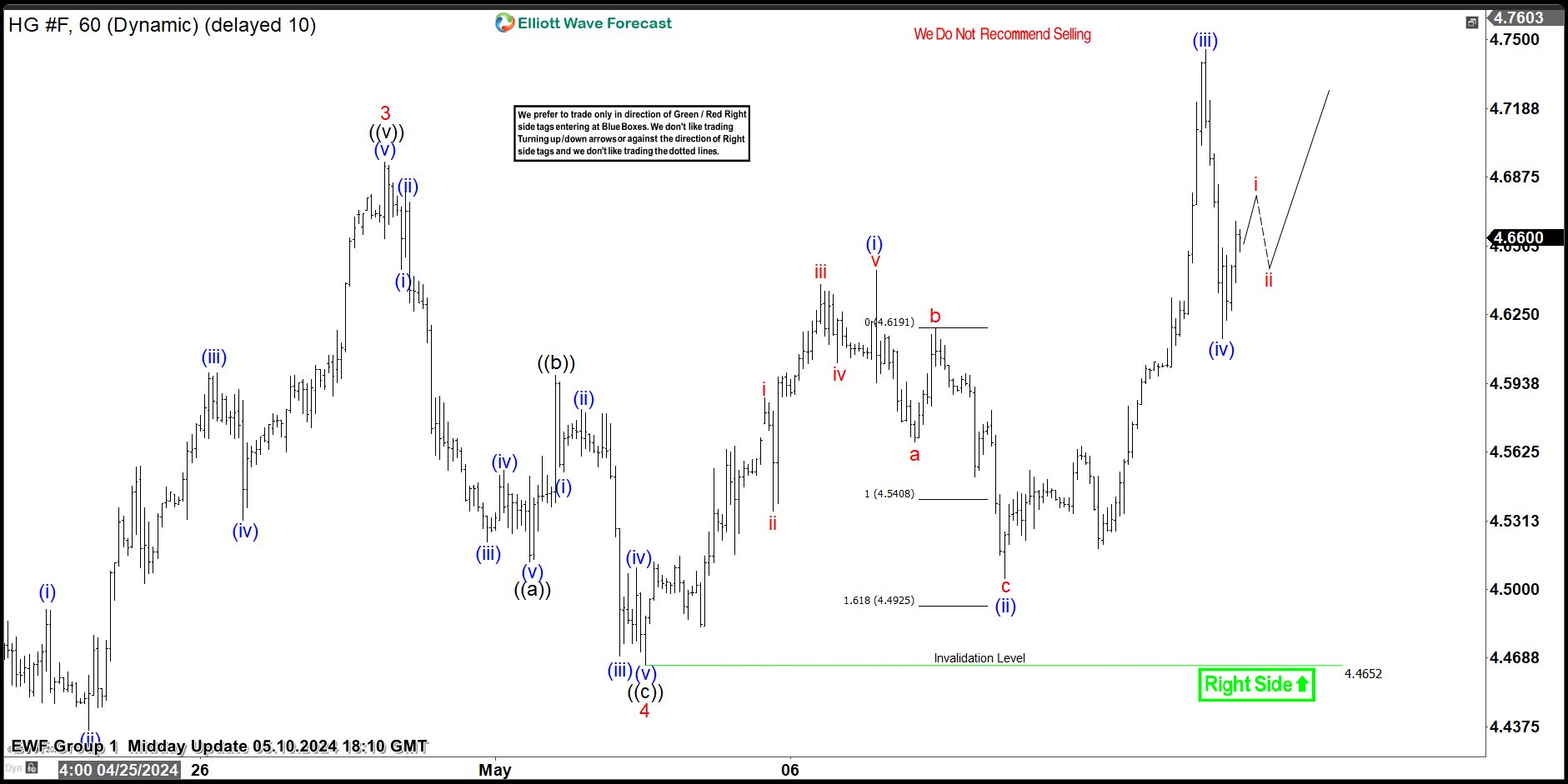

Copper (HG_F) Elliott Wave : Forecasting the Rally from the Equal Legs Zone

In this technical article we’re going to take a quick look at the Elliott Wave charts of Copper Futures HG_F, published in members area of the website. As our members know, Copper is showing impulsive bullish sequences in the cycle from the 3.6592 low. Consequently we are favoring the long positions at this stage. The commodity has recently given us a 3-wave pattern, when buyers appeared right at the equal legs zone. We are going to explain Elliott Wave forecast further in this article.

Copper H1 Asia Update 05.08.2024

The current view suggests that the Copper commodity is doing a ((ii)) black pullback, which is correcting the cycle from the 4.4671 low. So far pullback has given us 5 waves from the peak, suggesting structure is still incomplete. We expect to see another leg down toward equal legs : 4.5408-4.4925 ( buying area). Once extreme zone is reached , we expect potential buyers to appear in that area, which could lead to a further rally towards new high or a three-wave bounce at least.

Copper H1 Midday Update 05.10.2024

The commodity made another leg down as we expected. The price has reached the extreme zone at 4.5408-4.4925 area and made a nice rally from the Equal Legs-Buyers zone, as anticipated.The commodity remains bullish against the 4.4652 pivot. We expect Copper to keep finding buyers in 3,7,11 swings as far as the mentioned pivot holds.

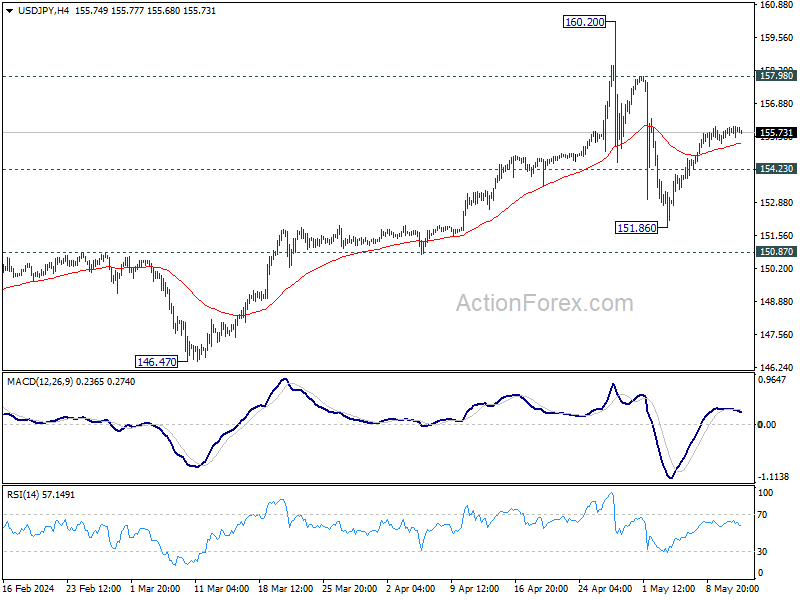

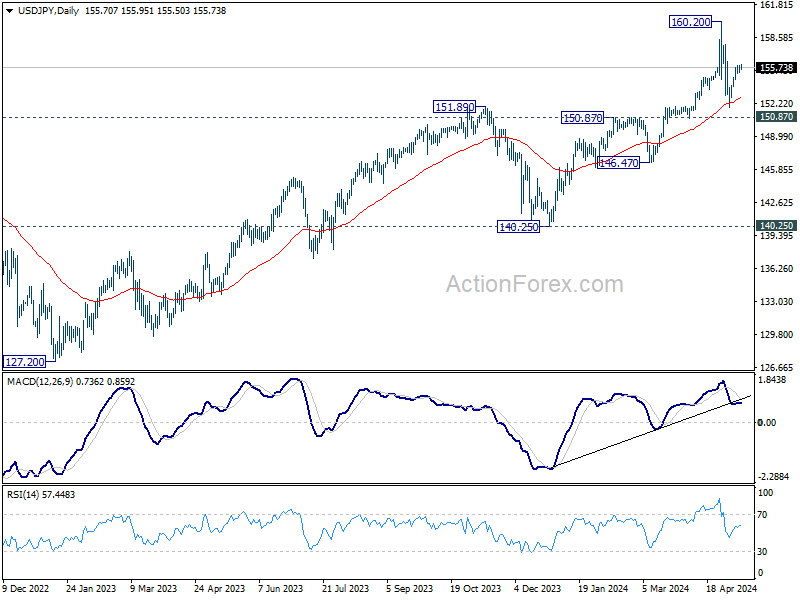

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.38; (P) 155.65; (R1) 156.02; More...

USD/JPY continues to lose upside momentum as seen in 4H MACD, but further rise is still mildly in favor. Rebound from 151.86, as the second leg of the corrective pattern from 160.20, could extend towards 157.98 resistance. On the downside, break of 154.23 will suggest that the third leg has started, and turn bias back to the downside for 151.86 support.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

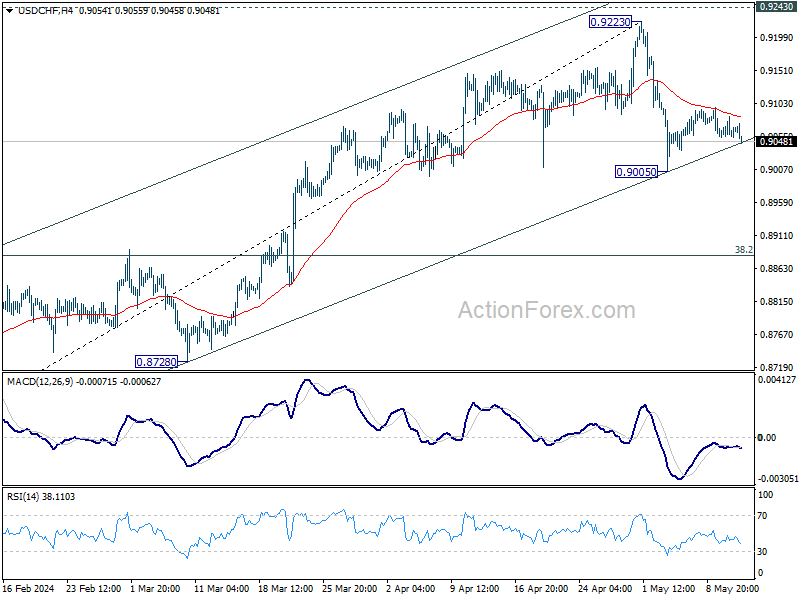

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9048; (P) 0.9066; (R1) 0.9084; More....

USD/CHF is staying above 0.9005 support despite today's dip and intraday bias remains neutral. Further decline is in favor as long as 55 4H EMA (now at 0.9082) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9006) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

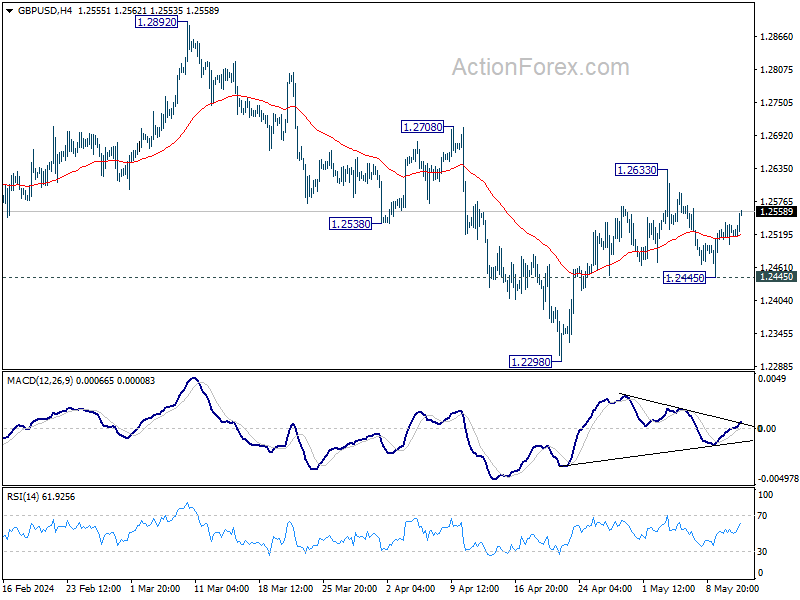

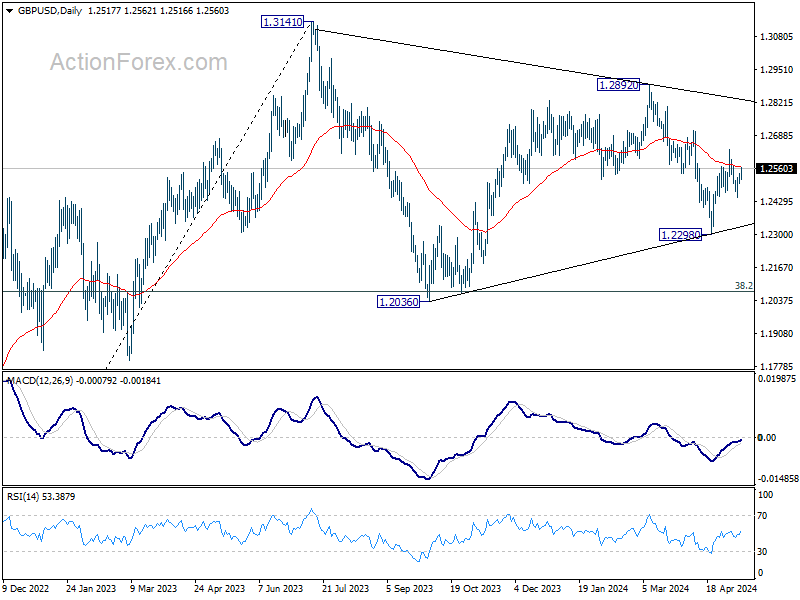

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2504; (P) 1.2523; (R1) 1.2543; More...

GBP/USD is staying below 1.2633 resistance despite today's rally. Intraday bias remains neutral for the moment. Further rise is mildly in favor with 1.2445 support intact. On the upside, break of 1.2633 will resume the rally from 1.2298 to 1.2708 resistance next. However, firm break of 1.2445 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

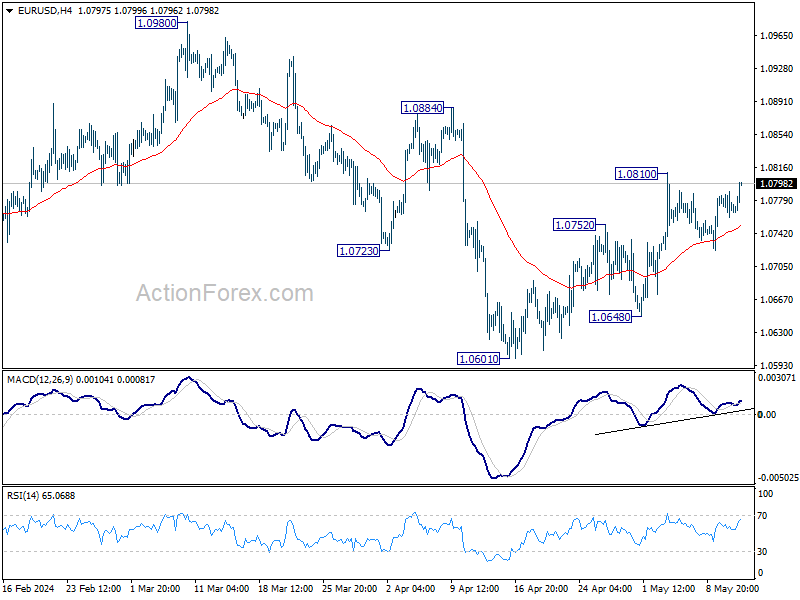

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0757; (P) 1.0773; (R1) 1.0787; More...

EUR/USD is staying below 1.0810 resistance despite today's rise. Intraday bias remains neutral at this point. Further rally is expected as long as 55 4H EMA (now at 1.0751) holds. On the upside, above 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 55 4H EMA will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.