Sample Category Title

Sunset Market Commentary

Markets

Both interest rate markets and the dollar held a wait-and-see mode this morning with EMU bonds slightly underperforming the US Treasuries. German ZEW investors sentiment again improved more than expected (expectations index from 42.9 to 47.1, the 10th consecutive improvement). This is not the most important input for the ECB, but it maybe marginally supported EMU yields. The focus of global markets however was on the first set US price data to be published this afternoon with the April producer prices. At 0.5% M/M for the headline figure and the measure excluding food and energy, monthly data were higher than expected, but the rise in the Y/Y-measure was slowed by a downward revision of the March data. Food price inflation was negative (-0.7% M/M), but services inflation (0.6% M/M) reaccelerated. US yields after the release briefly tried to reverse a small intraday decline, but soon relapsed, with markets looking forward to tomorrow’s CPI release. US yields currently decline 3-4 bps across the curve. German Bunds underperform with yields adding between 1-2 bps. ECB’s Wunsch in an interview with Handelsblatt was quoted that wage pressure persists, keeping services inflation high. In this context he wants the ECB to proceed gradually with rate cuts with no room for a back-to-back rate cut in July after a first step June. Equities show no clear trend. The rebound in the EuroStoxx 50 slows (-0.1% today) as the April top is again within reach. US indices also open marginally higher. Oil still struggles after recent losses (Brent $83 b/p).

The modest reaction of US interest rate markets to the PPI release is keeping the dollar in the defensive. The DXY trade-weighted index returned to the 105 area. EUR/USD tries a second consecutive attempt to regain the 1.0811 ST top. A gradual, but protracted further rise in Japanese long term yields amid speculation on some further BOJ policy normalization (lower amount of bond buying) isn’t enough to prevent further yen losses (USD/JPY 156.4). Sterling this morning initially didn’t know how to react to mixed UK labour market data (wage growth ex bonus still 6.0% Y/Y, but a further decline in April payrolls of 85k). Later in the session, BoE Chief economist Pill sounded rather soft as he indicated that the BoE can cut rates while staying restrictive as the BOE is making good progress in bringing inflation back to target. UK yields today decline 2-3 bps across the curve. EUR/GBP reversed tentative early weakness and again trades just north of the 0.86 big figure.

News & Views

After hitting the lowest since 2012 in March, US small business optimism unexpectedly recovered from 88.5 to 89.7 in April. It’s the first increase of the year but the headline figure remains well below the 50-yr average of 98, the National Federation of Independent Business said. 22% reported that cost pressures, including historically high levels of employee compensation, was the single most important problem in their business. Key findings of the April report include that 26% plan price hikes in April, down seven points to the lowest reading since April last year. A slightly bigger percentage of firms reported that they plan to hire in the next three months, though the subindex remains near its lowest since 2016 (excluding the pandemic period in 2020). 40% reported job openings they could not fill in the current period, up three points from March, which was then the lowest reading since January 2021. The net percent of owners who expect real sales to be higher rose six points from March to a net negative 12%. General uncertainty crept higher to 78.0 in April.

The Hungarian forint extends its recent strong performance today. EUR/HUF hits a three-month low around 386.4 in the wake of MNB Virag speaking. The deputy governor stressed the need for further efforts to maintain the disinflation trend. He said the current benchmark rate of 7.75% can be cut towards 6.5-7% by the middle of the year but room for further easing in 2024H2 is limited. Virag’s comments come after Hungarian inflation on Friday printed higher in April for the first time in more than a year. Central banks in the region turned more hawkish in general (eg. CNB) over the recent weeks as they reckon that the easy part of easing price pressures is over. Inflation is even expected to grind higher again in the second half of the year, joining the bumpy path that lies ahead for the likes of the ECB and the Fed as well. The latter’s forced delay to cut rates is a key consideration too for CE central banks looking to maintain a sufficiently attractive real rate differential for their respective currencies.

Graphs

EUR/HUF: forint extends rebound as MNB Virag indicates room for further cuts might be limited in H2 of this year

EUR/USD tries to regain 1.0811 short-term top as US yields fail to rise on higher than expected US PPI.

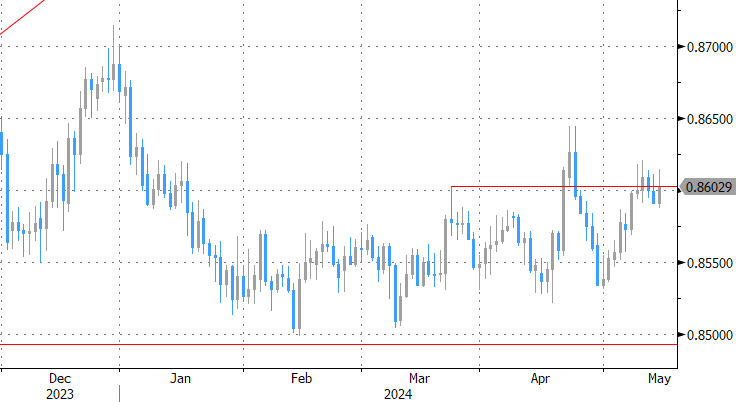

EUR/GBP: sterling losing modestly as BoE Chief economist Pill sounds rather optimistic on rate cuts in the near future.

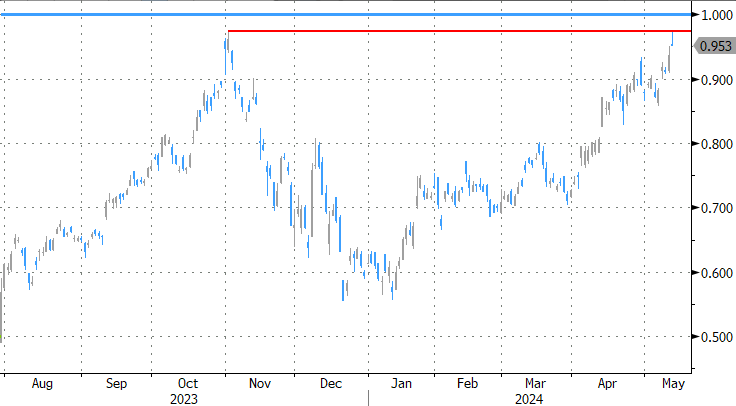

Japan 10-y yield near 1.0% barrier as markets ponder further BOJ policy normalisation.

US: Small Business Optimism Index Improves in April

NFIB's Small Business Optimism Index rose 1.2 points to 89.7 in April, beating market expectations for a 0.3-point decrease. This marked the first increase in the index in 2024.

Seven of the ten subcomponents improved on the month, two deteriorated and one remained unchanged. The improving categories included expectations for higher real sales in six months (up six points to -12%), higher reported earnings in the current quarter (up two points to -27%), and plans for capital expenditures in the next six months (up two points to 22%). The declining categories were expectations for credit conditions to ease and expectations for the economy to improve, both down one point to -9% and -37%, respectively.

The net share of businesses planning to increase employment rose for the first time in five months, up one point to 12%. The share of firms with unfilled job openings rose three points to 40%. Quality of labor concerns edged higher with 19% of business owners identifying this as their top business problem, but it continued to come second to inflation concerns which fell modestly in April.

The share of firms currently increasing or planning to increase compensation were unchanged relative to March at 38% and 21%, respectively. The share of businesses 'raising' average selling prices fell three points to 25% while the share of those 'planning’ to raise average selling prices fell by seven points to 26%.

Key Implications

After declining for the past three months, small business confidence improved in April. Most small businesses are planning to increase capital investments and headcounts over the coming months, with sales expectations improving gradually. However, high-level expectations for the economy were little changed on the month, with most small businesses continuing to expect the economy to weaken and credit conditions to remain tight moving forward.

Current wage and price increases on Main Street continue to ease gradually despite remaining above pre-pandemic trends. Moreover, plans for future increases in both have fallen after spiking late last year. Looking forward, easing labor market tightness and producer inflation pressures should help to gradually return consumer inflation closer to the Federal Reserve's 2% target.

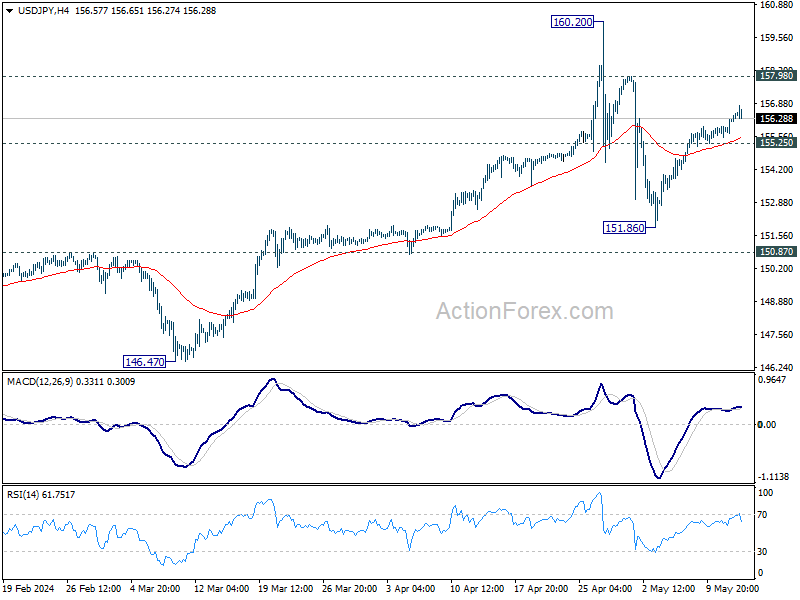

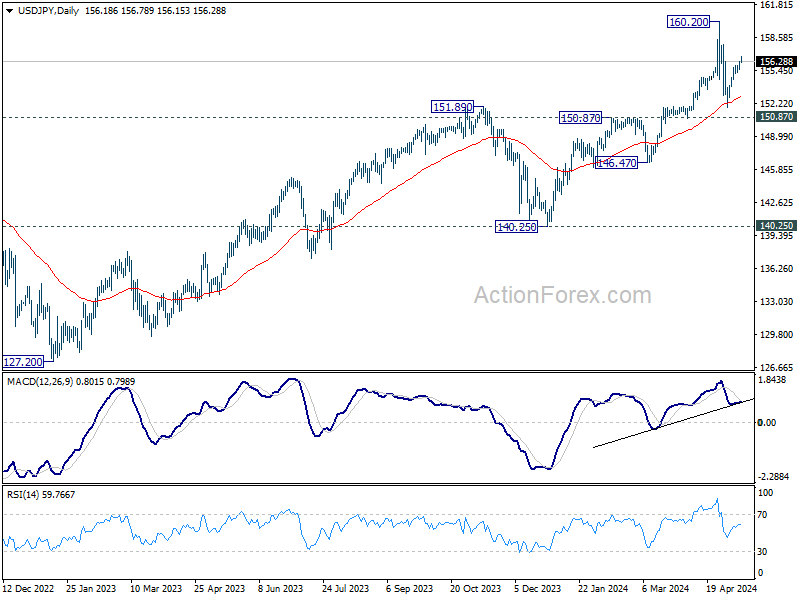

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.74; (P) 156.00; (R1) 156.47; More...

No change in USD/JPY's outlook and intraday bias stays mildly on the upside. Rebound from 151.86, as the second leg of the corrective pattern from 160.20, is in progress for 157.98 resistance. On the downside, break of 155.25 minor support will suggest that the third leg has started, and turn bias back to the downside for 151.86 support.

In the bigger picture, a medium term top might be formed at 160.20. But as long as 150.87 resistance turned support holds, fall from there is seen as correcting rise from 150.25 only. However, decisive break of 150.87 will argue that larger correction is possibly underway, and target 146.47 support next.

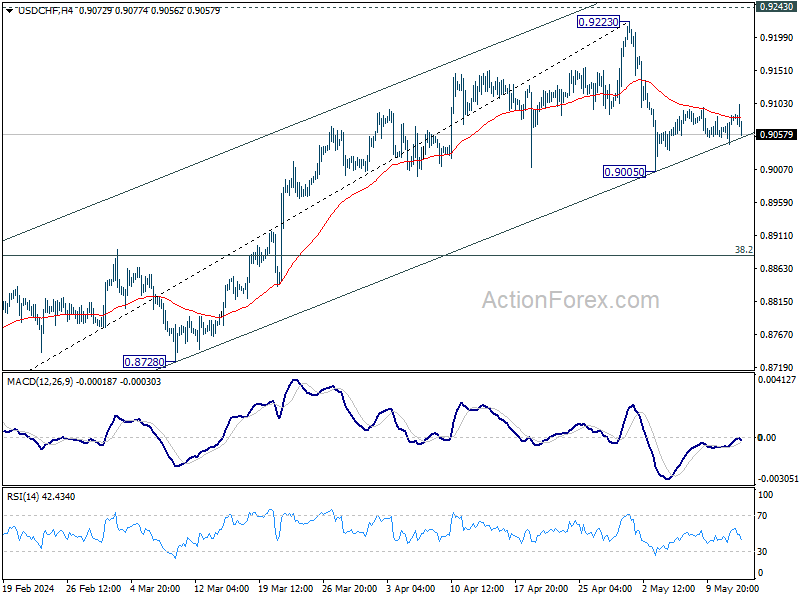

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9057; (P) 0.9072; (R1) 0.9099; More....

Intraday bias in USD/CHF stays neutral and further decline is in favor as long as 55 4H EMA (now at 0.9083) holds. On the downside, break of 0.9005 and sustained trading below 55 D EMA (now at 0.9010) will bring deeper fall to 38.2% retracement of 0.8332 to 0.9223 at 0.8883. However, firm break of 55 4H EMA will suggest that the pull back from 0.9223 has completed, and bring stronger rebound to retest 0.9223 high.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

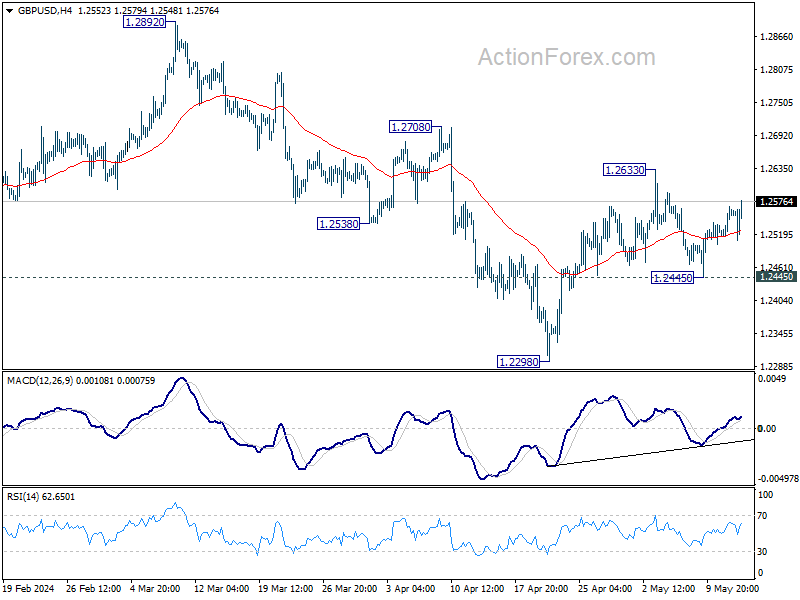

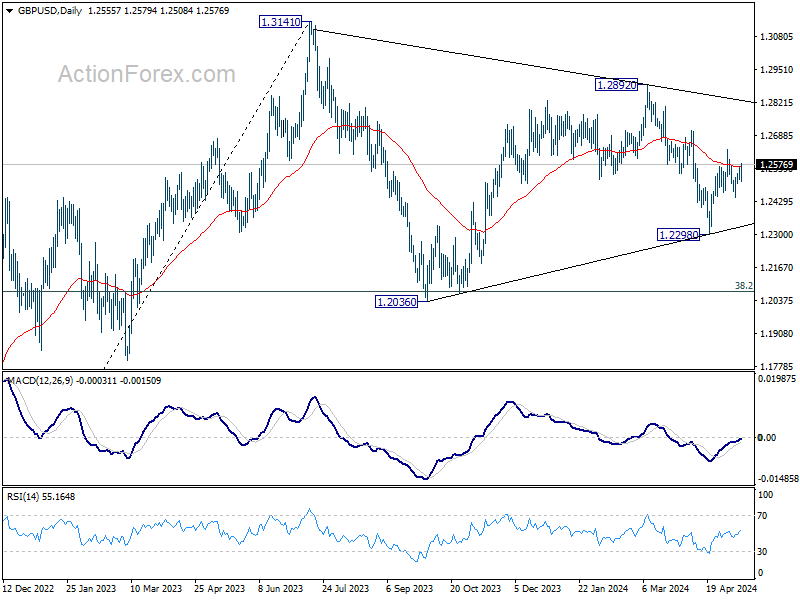

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2526; (P) 1.2547; (R1) 1.2581; More...

GBP/USD is staying in range below 1.2633 and intraday bias remains neutral. Further rise is mildly in favor with 1.2445 support intact. On the upside, break of 1.2633 will resume the rally from 1.2298 to 1.2708 resistance next. However, firm break of 1.2445 will indicate that this rebound has completed, and revive near term bearishness. Retest of 1.2298 should then be seen in this case.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern. Fall from 1.2892 is seen as the third leg which might have completed already. Break of 1.2892 resistance will argue that larger up trend from 1.0351(2022 low) is ready to resume through 1.3141. Meanwhile, break of 1.2298 support will extend the corrective pattern instead.

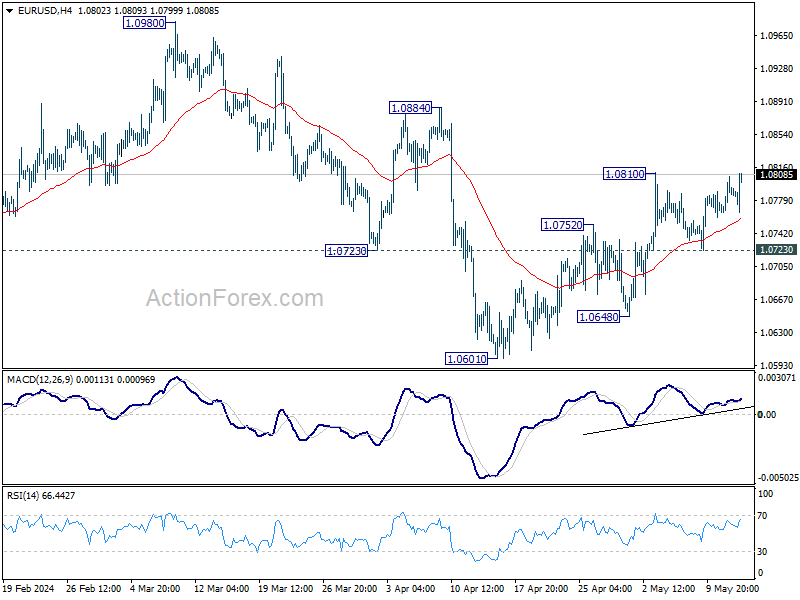

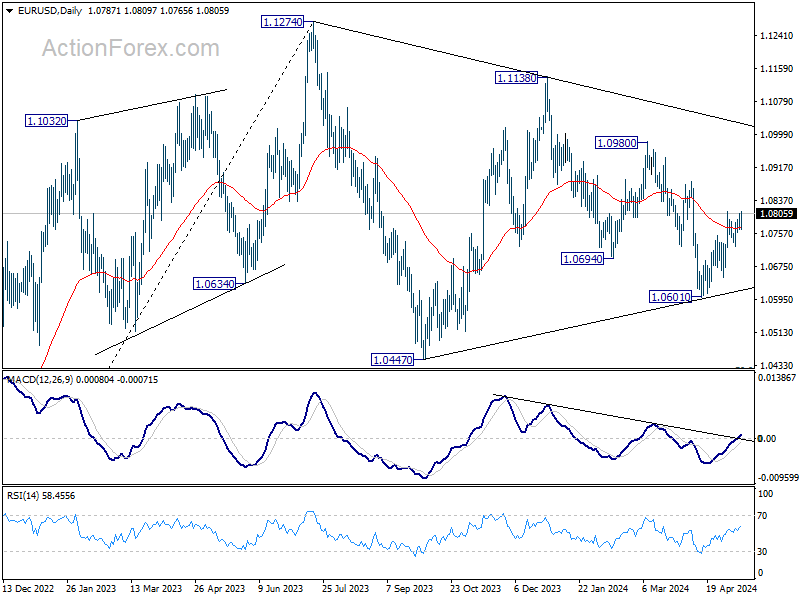

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0788; (R1) 1.0809; More...

EUR/USD is still staying in range below 1.0810 and intraday bias remains neutral at this point. Further rally is in favor as long as 1.0723 minor support holds. On the upside, break of 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 1.0723 will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

Dollar Spikes on Strong PPI Data, Reverses as Bears Maintain Control

Dollar spiked higher after US PPI reported stronger-than-expected monthly rise. However, this upward movement was quickly reversed within minutes, indicating that bearish sentiment continues to dominate the greenback. The key question now is whether Dollar will see downside breakouts before tomorrow's crucial CPI release.

Sterling's movements have also been indecisive. The Pound initially recovered following stronger-than-expected UK wage growth data but upside was capped by a rise in unemployment rate. It softened again after BoE Chief Economist Huw Pill affirmed that a summer rate cut is "not unreasonable." Despite these fluctuations, Sterling remains within yesterday's range, except against Yen.

In the broader forex market, Euro is currently the strongest performer for the day, followed by Canadian Dollar and Aussie. Yen is the weakest, followed by Sterling and Swiss Franc, with Dollar and Kiwi position in the middle.

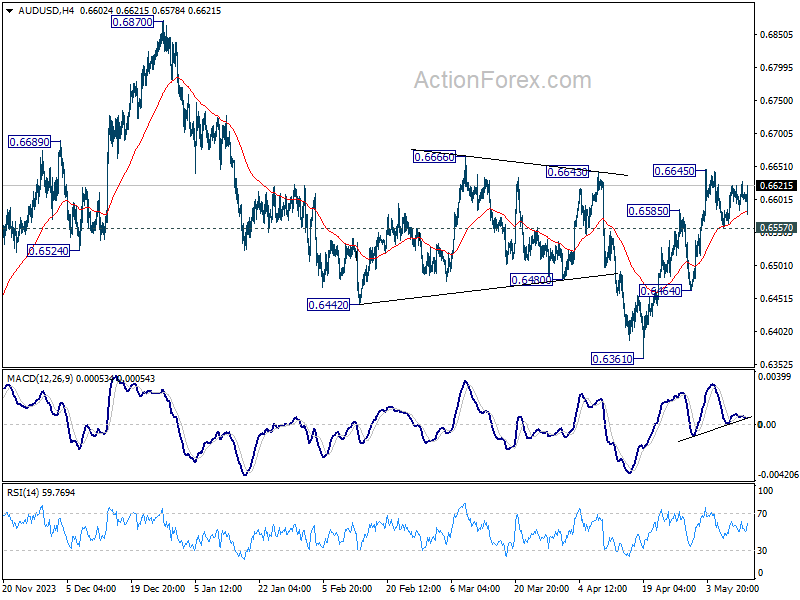

Technically, AUD/USD is staying bullish with 0.6557 support intact. Break of 0.6645 will resume rise from 0.6361. Further break of 0.6666 resistance should confirm the whole fall from 0.6870 has completed and target this resistance next. Australia's wage price index data in the upcoming Asian session is a potential trigger for the move.

In Europe, at the time of writing, FTSE is up 0.33%. DAX is down -0.21%. CAC is up 0.10%. UK 10-year yield is down -0.055 at 4.166. Germany 10-year yield is up 0.028 at 2.540. Earlier in Asia, Nikkei rose 0.46%. Hong Kong HSI fell -0.22%. China Shanghai SSE fell -0.07%. Singapore Strait Times rose 0.29%. Japan 10-year JGB yield rose 0.0246 to 0.966.

US PPI rises 0.5% mom, 2.2% yoy in Apr, highest since Apr 2022

US PPI for final demand rose 0.5% mom in April, above expectation of 0.2% mom. Nearly three-quarters of the April advance in final demand prices is attributable to a 0.6% mom increase in the index for final demand services. Prices for final demand goods moved up 0.4% mom. PPI less foods, energy and trade services rose 0.4% mom.

For the 12 months period, PPI rose 2.2% yoy, highest since April 2023. Prices for final demand less foods, energy, and trade services increased 3.1% yoy, the largest advance since April 2023.

German ZEW rises to 47.1, signs of recovery growing

German ZEW Economic Sentiment jumped from 42.9 to 47.1 in May, above expectation of 44.9. Current Situation Index also rose from -79.2 to -72.3, above expectation of -75.0.

Eurozone ZEW Economic Sentiment rose from 43.9 to 47.0, above expectation of 46.1. Current Situation Index jumped by 10.2 pts to -38.6.

ZEW President Professor Achim Wambach said: " Signs of an economic recovery are growing, bolstered by better assessments of the overall eurozone and of China as a key export market. The increased optimism is reflected in particular in the sharp rise in expectations for domestic consumption, followed by the construction and machinery sectors."

BoE's Pill: Summer rate cut not unreasonable

BoE's Chief Economist Huw Pill suggested today that it is "not unreasonable" for central bank to consider rate cuts over the summer. However, he emphasized the critical need for to maintain a "restrictive stance" on monetary policy to address persistent domestic inflation pressures.

Pill's comments come against the backdrop of newly released data, which he referenced in his remarks. "We actually got some additional data this morning that would be consistent with a small additional decline in the first quarter," he said, pointing to the latest figures on private sector regular pay growth.

This data indicates a slight cooling in the labor market, although Pill noted that it "still remains pretty tight by historical standards." He emphasized that "rates of pay growth remain quite well above what would be consistent for meeting the 2% inflation target sustainably."

UK payrolled employment down -85k in Apr, but wages growth steady in Mar

UK payrolled employment fell -85k or -0.3% mom in April. This is a rise of 129,000 people over the 12-month period. Median monthly pay growth was 6.9% yoy, accelerated from March's 6.4% yoy. Claimant count rose 8.9k, below expectation of 13.9k.

In the three months to March, unemployment rate rose from 4.2% to 4.3%, matched expectations. Average earnings including bonus rose 5.7% yoy. Average earnings excluding bonus rose 6.0% yoy. Both were unchanged from February's figures.

IMF recommends gradual approach for future BoJ rate hikes

IMF projects Japan's economic growth to continue, with a noticeable increase in consumption anticipated later this year. According to a report, Japan's growth rate is expected to decelerate to 0.9% in 2024, largely due to the fading impact of one-off factors that boosted growth in 2023.

The report highlights that consumption will pick up in the latter half of 2024 and into 2025, driven by rising nominal wages following a strong Shunto settlement in 2024 and a decrease in headline inflation that will boost real wages.

IMF foresees core inflation gradually declining as the impact of higher import prices diminishes. However, core inflation is expected to remain above BoJ's 2% target until the second half of 2025.

In light of these developments, IMF suggests that further increases in BoJ's short-term policy rate should "proceed at a gradual pace" and be "datadependent", considering the balanced risks to inflation and the mixed signals from recent economic data.

IMF emphasizes the importance of Japan's adherence to a "flexible exchange rate regime", which will play a crucial role in absorbing economic shocks and supporting the central bank's focus on maintaining price stability.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0768; (P) 1.0788; (R1) 1.0809; More...

EUR/USD is still staying in range below 1.0810 and intraday bias remains neutral at this point. Further rally is in favor as long as 1.0723 minor support holds. On the upside, break of 1.0810 will resume the rebound from 1.0601 to 1.0884 resistance next. However, firm break of 1.0723 will argue that the rebound has completed, and turn bias to the downside for 1.0648 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern. Fall from 1.1138 is seen as the third leg and could have completed. Firm break of 1.1138 will argue that larger up trend from 0.9534 (2022 low) is ready to resume through 1.1274 high. On the downside, break of 1.0601 will extend the corrective pattern instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Apr | 0.90% | 0.90% | 0.80% | 0.90% |

| 06:00 | JPY | Machine Tool Orders Y/Y Apr | -11.60% | -3.80% | ||

| 06:00 | EUR | Germany CPI M/M Apr F | 0.50% | 0.50% | 0.50% | |

| 06:00 | EUR | Germany CPI Y/Y Apr F | 2.20% | 2.20% | 2.20% | |

| 06:00 | GBP | Claimant Count Change Apr | 8.9K | 13.9K | 10.9K | -2.4K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Mar | 4.30% | 4.30% | 4.20% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Mar | 5.70% | 5.30% | 5.60% | 5.70% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Mar | 6.00% | 6.00% | ||

| 06:30 | CHF | Producer and Import Prices M/M Apr | 0.60% | 0.20% | 0.10% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Apr | -1.80% | -2.10% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment May | 47.1 | 44.9 | 42.9 | |

| 09:00 | EUR | Germany ZEW Current Situation May | -72.3 | -75 | -79.2 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | 47 | 46.1 | 43.9 | |

| 10:00 | USD | NFIB Business Optimism Index Apr | 89.7 | 88.1 | 88.5 | |

| 12:30 | USD | PPI M/M Apr | 0.50% | 0.20% | 0.20% | -0.10% |

| 12:30 | USD | PPI Y/Y Apr | 2.20% | 2.20% | 2.10% | 1.80% |

| 12:30 | USD | PPI Core M/M Apr | 0.50% | 0.20% | 0.20% | -0.10% |

| 12:30 | USD | PPI Core Y/Y Apr | 2.40% | 2.40% | 2.40% | |

| 12:30 | CAD | Wholesale Sales M/M Mar | -1.10% | -0.90% | 0.00% | 0.20% |

US PPI rises 0.5% mom, 2.2% yoy in Apr, highest since Apr 2022

US PPI for final demand rose 0.5% mom in April, above expectation of 0.2% mom. Nearly three-quarters of the April advance in final demand prices is attributable to a 0.6% mom increase in the index for final demand services. Prices for final demand goods moved up 0.4% mom. PPI less foods, energy and trade services rose 0.4% mom.

For the 12 months period, PPI rose 2.2% yoy, highest since April 2023. Prices for final demand less foods, energy, and trade services increased 3.1% yoy, the largest advance since April 2023.

Ethereum (ETHUSD): Incomplete Sequences Calling the Decline

In this technical article we’re going to take a quick look at the Elliott Wave charts of Ethereum ETHUSD , published in members area of the website. As our members know, ETHUSD is showing incomplete sequences in the cycle from the March peak. Consequently we expect more weakness in short term. Ethereum is targeting 2700.3-2057.9 area , where we would like to be buyers again. Recently the crypto made 3 waves bounce and found sellers as expected. In further text we are going to explain Wave forecast.

ETHUSD H1 London Update 05.06.2024

ETHUSD is doing a ((iv)) recovery, which is correcting the cycle from the 3352.618 peak. Proposed recovery can be unfolding as a Elliott Wave Double Three pattern .The price has already reached extreme zone from the lows and we expect sellers to appear soon. We are aware that short term recovery can complete any moment. We advise members not to entry long positions at this stage, while still favoring the short side.

ETHUSD H1 London Update 05.06.2024

Ethereum found sellers as expected and made a nice decline after completing wave ((iv)) recovery. We consider the wave ((iv)) correction completed at the 3220 high. We expect short term bounces to keep finding sellers in 3,7,11 swings as far as the pivot at 3355.46 high holds. Right way to trade the crypto is waiting for extreme zone to be reached at 2700.3-2057.9 area, before buying the dips again.

EUR/USD Steady as German Confidence Index Rises

The euro is drifting on Tuesday. EUR/USD is up 0.07% on Tuesday, trading at 1.0798 in the European session at the time of writing.

German inflation steady, confidence higher

Germany’s inflation rate remained unchanged in April at 2.2% y/y, matching the market consensus. Services inflation slowed but this was offset by higher food prices. Monthly, inflation rose by 0.5%, up from 0.4% in March and matched the market consensus of 0.4%. This marked the highest monthly gain in 14 months.

The German ZEW economic sentiment indicator climbed to 47.1 in May, up sharply from 42.9 in April and above the market consensus of 46.0. This was its highest level since February 2022 and marked a 10th straight rise in confidence among financial experts. The stronger German data helped push up eurozone ZEW economic sentiment, which rose from 43.9 to 47.0 in April, above the market estimate of 46.1.

Germany’s economy is showing signs of recovery, such as GDP in the first quarter which was stronger than expected. Domestic activity is expected to increase as is the demand for German exports, with the eurozone and China showing stronger growth.

Federal Reserve Chair Powell speaks at an event in Amsterdam later today and the markets will be looking for hints regarding a rate cut. The Fed has delayed plans to cut rates as the US economy remains resilient and inflation has unexpectedly accelerated. A drop in this week’s inflation releases would boost the likelihood of a rate cut in September. The US releases PPI is expected to remain unchanged at 2.4% in April while CPI is projected to ease to 3.6%, down from 3.8% in April.

EUR/USD Technical

- EUR/USD is putting pressure on resistance at 1.0809. Above, there is resistance at 1.0829

- There is support at 1.0788 and 1.0768