Sample Category Title

Fed’s Goolsbee forecasts three rate cuts amid rising real interest rate restrictiveness

Chicago Fed President Austan Goolsbee told Yahoo Finance that he aligned with the "median" projections regarding the monetary easing path forward, as anticipates three rate cuts within the year.

In this "murky period" of economic recovery as Goolsbee described, Fed has to "strike a balance of the dual mandate". He noted that with inflation rates on a downward path, the real cost of borrowing has inadvertently risen, positioning Fed in "historically pretty restrictive territory."

"So I think with that level of restrictiveness, you will have to start paying attention to the other side of the mandate, too, if it goes for too long," he added.

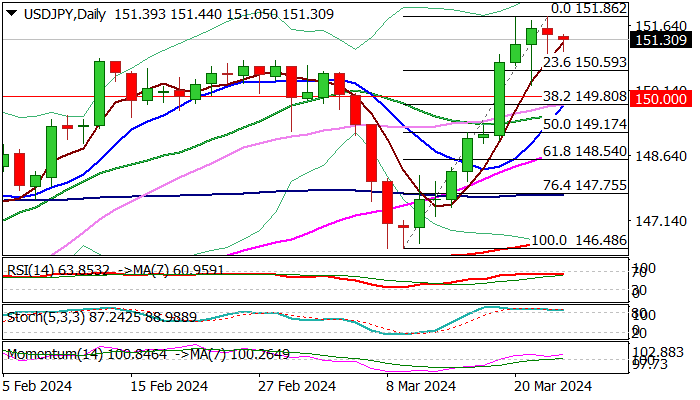

USDJPY- Bulls Hold Grip for Further Gains after Consolidation

Bulls are taking a breather and consolidating just under key barriers at 150.90/94 (2023/22 tops) after strong rally in past two weeks.

USDJPY was inflated by a wide gap between US and Japan’s interest rates, with no positive impact from BoJ’s rate hike last week, as investors do not expect the central bank to be aggressive with policy tightening.

However, traders remain cautious regarding the latest warning from Japan’s officials that yen is too weak, which keeps possibility of intervention on the table.

Technical studies on daily chart are firmly bullish and supportive for fresh gains, with consolidation / correction on overbought conditions, to precede fresh push higher.

Initial support lays at 150.59 (Fibo 23.6% of 146.48/151.86 upleg, ahead of more significant 150.00/149.80 (psychological / Fibo 38.2%, reinforced by rising 10DMA) where extended dips should find firm ground to keep larger bulls in play and mark a healthy correction ahead of renewed attack at 151.90/94.

Res: 151.90; 151.94; 152.56; 153.00

Sup: 151.00; 150.59; 150.00; 149.80

Sunset Market Commentary

Markets

The yuan’s sharp rebound this morning triggered some attention, if only because other news was so limited today. USD/CNY shot up last Friday on signals that Chinese authorities loosened their grip on the 7.2 handle it defended for several months. Clearly they weren’t expecting nor hoping for such an abrupt move. Such large fluctuations could pose threats to financial stability, tarnishing CNY reputation. The authorities including the PBOC send a clear message through a significantly stronger fixing. USD/CNY declined back to 7.2 before paring losses in European/US dealings again to 7.21. Sticking to the region, Japan’s vice finance minister for international affairs Kanda told reporters that the “current weakening of the yen is not in line with fundamentals and clearly driven by speculation.” Regarding direct interventions, Kanda said they are always prepared. USD/JPY eases to 151.15, but remains just inches away from the multidecade yen-lows of 151.95. It is also as much JPY appreciation as it is USD depreciation. DXY loses a few ticks but remains north of the 104 barrier. EUR/USD rebounded from the low 1.08 towards 1.0836. Sterling tries to build on Friday’s momentum, when a technical leap beyond 0.86 by EUR/GBP failed and triggered some return action lower instead. The currency pair currently eases to 0.8568. GBP/USD bounces of the 1.26 level to 1.264. Central European currencies are generally well bid though they are off their intraday highs. The forint takes center stage this week with the Hungarian central bank (MNB) meeting tomorrow. The Hungarian currency slid ever since the central bank jacked up the cutting pace from 75 to 100 bps and the feud between the government and the MNB escalated. On the latter, it became official today that the government will delay the hotly contested supervision law until the autumn. But with EUR/HUF (396.5) nonetheless moving dangerously close to the 400 symbolical level, we wouldn’t be surprised to see the MNB already revert to 75 bps of rate cuts. Off-bets for a 50 bps move circulate as well.

Core bonds lose some ground at the start of the new week, returning some of Friday’s (outsized) gains. US yields add between 3.6 and 4.4 bps. Atlanta Fed Bostic in a speech today repeated he expects just one rate cut if the economy evolves as expected. Goolsbee from Chicago said he needed to see more progress in inflation coming down. According to him, the main puzzle is in housing. He added that the current dot plot’s suggestion of three cuts this year was in line with his thinking. German Bunds marginally underperform with yields strengthening 3 (30-y) to 5 bps (5-y).

News & Views

The Dutch government this morning announced that last year’s budget deficit was only 0.3% of GDP, in line with the 0.1% of GDP shortfall in 2022. That’s significantly below the 1.8% deficit estimated in November. The government debt ratio declined from 50.1% of GDP to 46.5% which is the lowest level of the past 30 years apart from 2006 (45.2%) and 2007 (43%). On both metrics, the Netherlands easily beat the Maastricht criteria (<3% and <60%), significantly outperforming other EMU countries and bucking the global trend of huge fiscal stimulus. Government spending and government income respectively increased by 8% (to €449.5bn) and 7% (to €445.9bn) in 2023.

The composite Czech consumer & business confidence indicator rose from 90.6 to 94.2 in March, its highest level since May of last year. Both consumer confidence (99.9 from 94; best since October 2021) and business confidence (93 from 89.9) improved. Amongst entrepreneurs, confidence only deteriorated in the construction sector. Consumers sounded less pessimistic on the economy in the next 12 months while the number fearing a deterioration in their financial situation over the same time period did increase significantly. The share of consumers who believe that the current time is not suitable for making major purchases has not changed compared to the previous month.

USD/JPY Drifting at Start of Week

The Japanese yen is showing limited movement on Monday. In the North American session, USD/JPY is trading at 151.25, down 0.13%.

Yen can’t find its footing

Last week’s Bank of Japan was dramatic as the central bank raised interest rates for the first time since 2007. The move did not catch the markets completely by surprise, as some media reports ahead of the meeting said the BoJ would raise rates and investors were looking at both the March and April meetings as strong possibilities for a rate hike.

The yen did not respond to the rate hike with gains, as might have been expected. There are several reasons for this. First, the actual tightening was limited, with rates rising from -0.10% to 0.10%. This means that although the BoJ rate is now in positive territory, the move had little impact on the wide USD/JPY rate differential. BoJ Governor Ueda said after the meeting that despite the hike, monetary policy would remain accommodative, saying that there was “some distance to go” until inflation climbs to the 2% target.

As well, many investors approached the BoJ meeting with a “buy the rumour, sell the fact” approach and this resulted in heavy selling of the yen after the rate announcement. The yen slipped 1.60% last week and dropped as low as 151.86, its lowest level since November 2023.

The Japanese yen has dropped to levels that could invite intervention – the Ministry of Finance intervened last September and October when the yen dropped to around the 152 line. If the yen continues to lose ground, the threat of intervention will become greater.

In the US, the markets have priced in three rate cuts this year, and the Fed also projected three cuts this year at last week’s meeting. However, Atlanta Federal Reserve President Raphael Bostic sounded hawkish on Friday when he said that he expects only one quarter-point cut this year.

Bostic said that he was “definitely less confident than I was in December” that inflation will continue to drop towards the 2% target, as he noted that inflation remains stubbornly high and the US economy has been more resilient than he expected.

USD/JPY Technical

- USD/JPY is putting pressure on resistance at 151.44. Above, there is resistance at 151.88

- 151.02 and 15058 are providing support

Gold’s Prospects Look Promising

Gold prices have stabilized around $2170.00 per troy ounce after two days of decline. Investors are taking a pause ahead of an important US inflation indicator report due this week, which could provide insights into the future direction of the Federal Reserve's monetary policy.

The Core PCE index data, an inflation measure closely watched by the Federal Reserve, will be released this Friday. This week, several Federal Reserve officials, including Chair Jerome Powell, will speak at various events, potentially influencing market reactions. Additionally, most markets in Catholic countries will be closed on Good Friday at the week's end, possibly delaying market reactions.

Strategically, gold has gained solid support after the Federal Reserve's March meeting outlined three interest rate cuts for the current year. Support also came from the Swiss National Bank, which unexpectedly reduced its lending rate, sparking discussions that other major central banks might ease monetary policy sooner than expected - even before the Fed. For gold, this is a positive signal: lower interest rates reduce the opportunity cost of holding bullion.

The probability of the Fed starting to cut rates in June is estimated at 74%.

COMEX data shows that net long positions in gold have decreased by 2,093 contracts to 157,467 contracts, which is not critical for the precious metal's trend.

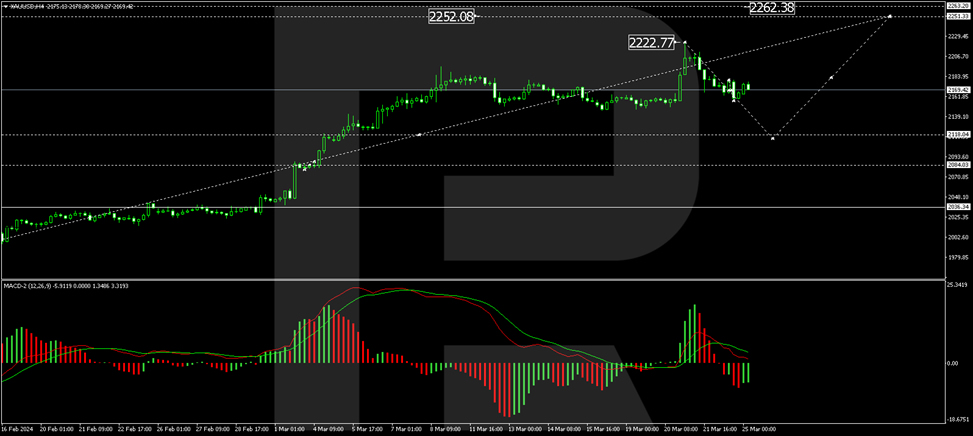

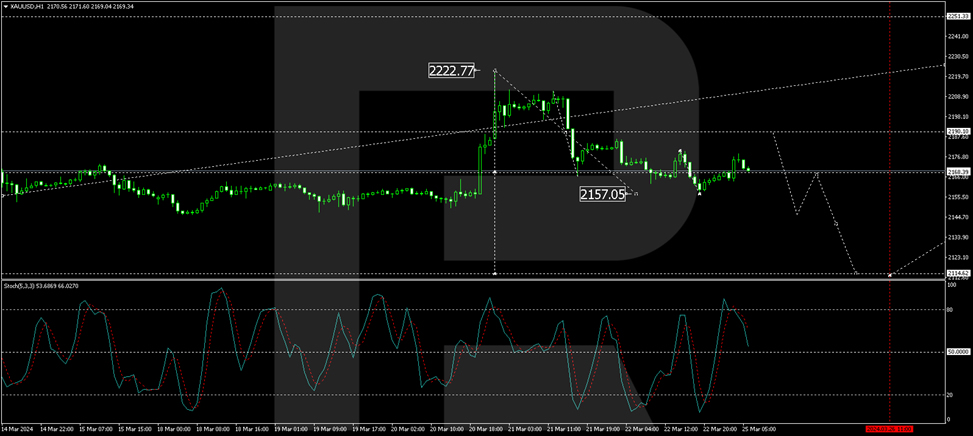

Technical analysis of XAU/USD

On the H4 chart, XAU/USD reached a local target of 2222.77. A correction to the level of 2157.05 has been executed today. Currently, the market is forming a consolidation range around 2168.40. A downward breakout is expected, followed by a continuation of the correction to 2114.60. After completing this correction, a growth wave to 2251.33 is anticipated. This scenario is supported by the MACD indicator, with its signal line above zero and sharply directed downwards.

On the H1 chart, XAU/USD has formed a consolidation range around 2168.40. An upward exit from this range could lead to a correction towards 2188.77. After reaching this level, a decline to 2146.66 will be considered, followed by the possibility of rising back to 2168.40 (testing from below) and then a decline to 2114.60. This scenario is confirmed by the Stochastic oscillator, with its signal line below 80 and heading straight down to 20.

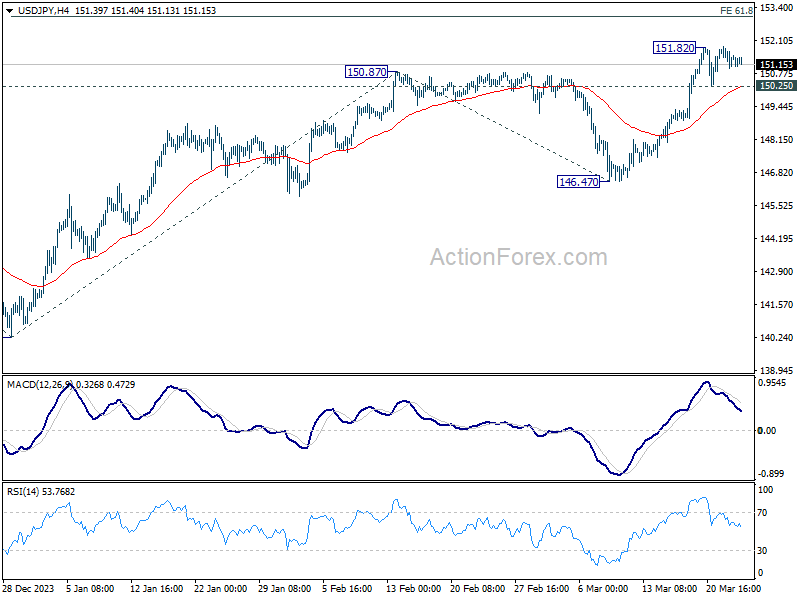

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.02; (P) 151.44; (R1) 151.88; More...

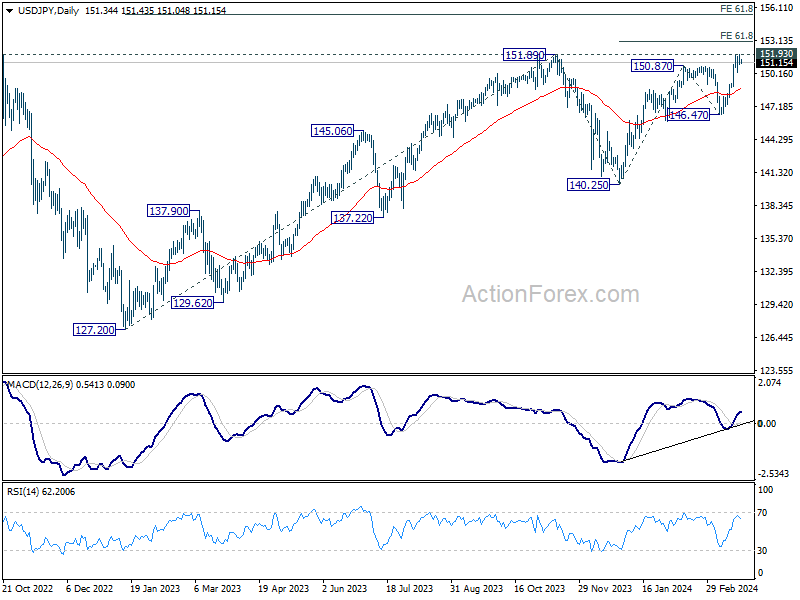

USD/JPY is still extending the consolidation from 151.92 and intraday bias stays neutral. Further rally is expected as long as 150.25 support holds. On the upside, decisive break of 151.93 key resistance will confirm long term up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. However, firm break of 150.25 will turn bias back to the downside for deeper pullback.

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Next medium term target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.20. This will remain the favored case as long as 146.47 support holds, in case of another pullback.

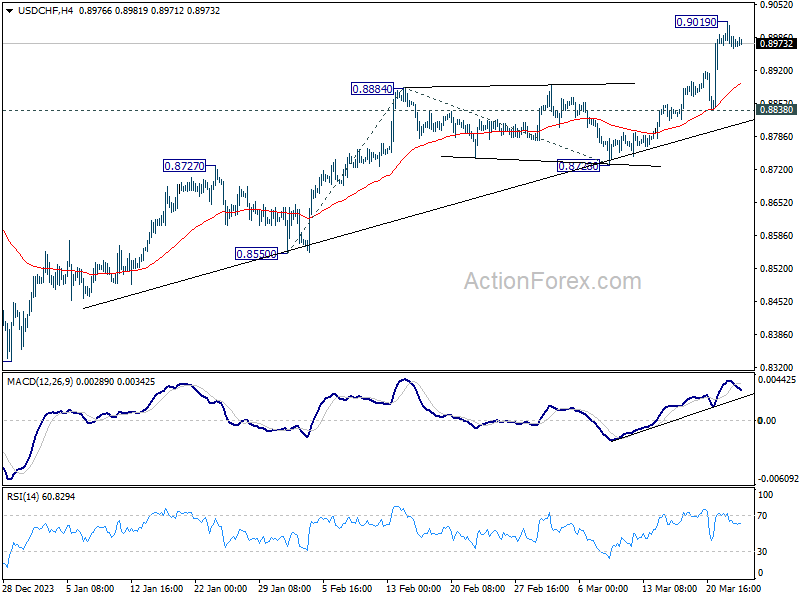

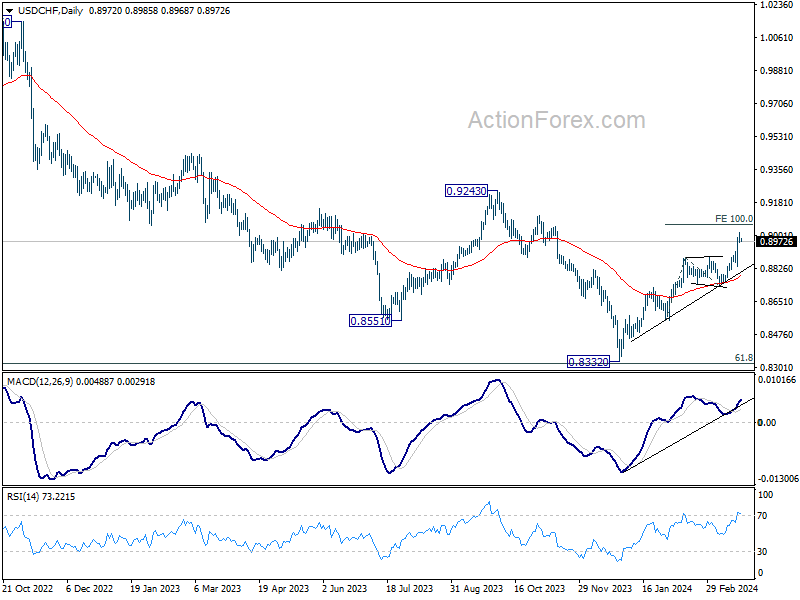

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8953; (P) 0.8987; (R1) 0.9009; More....

Intraday bias in USD/CHF remains neutral for consolidations below 0.9019 temporary top first. Downside of retreat should be contained above 0.8838 support to bring rebound. Break of 0.9019 will resume larger rally from 0.8332. Next target is 100% projection projection of 0.8550 to 0.8884 from 0.8728 at 0.9062.

In the bigger picture, price actions from 0.8332 medium term bottom as tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8728 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.

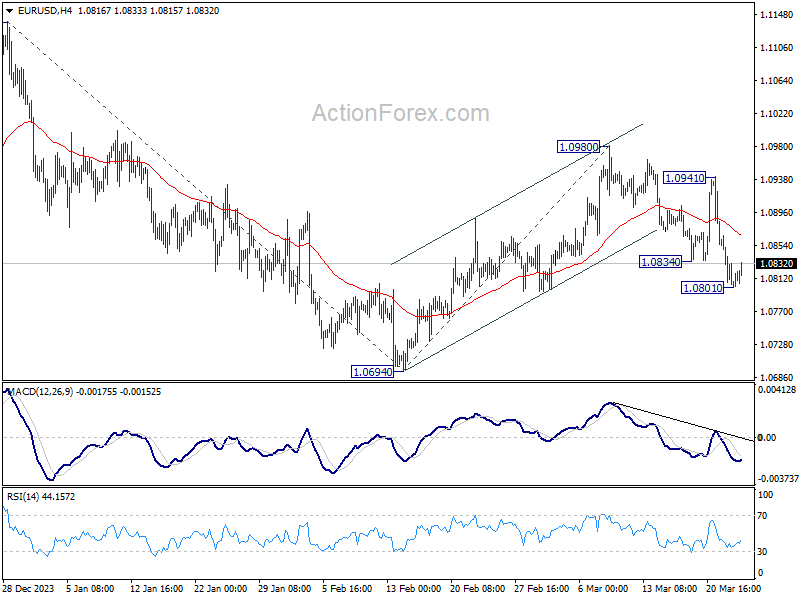

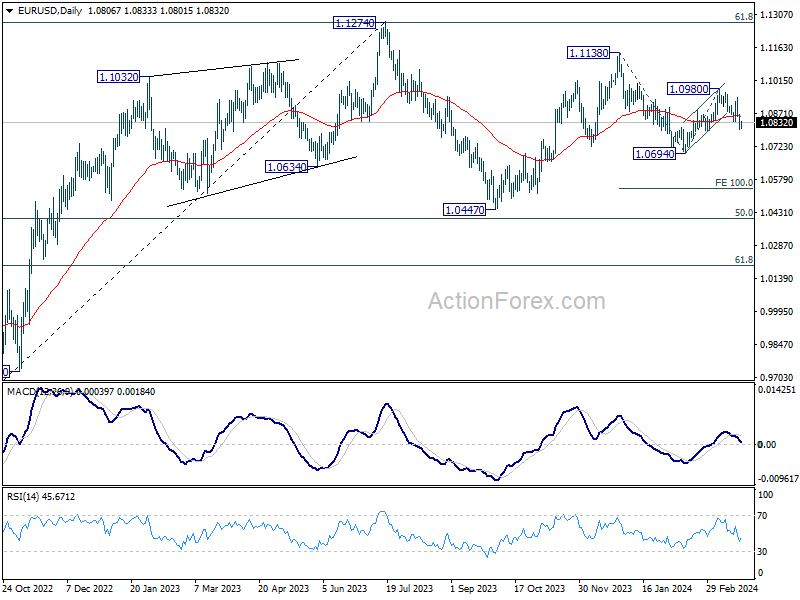

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0784; (P) 1.0826; (R1) 1.0850; More...

Intraday bias in EUR/USD is turned neutral with current recovery and some consolidations would be seen. But risk will stay on the downside as long as 55 4H EMA (now at 1.0868) holds. Below 1.0801 will resume the fall from 1.0980 to retest 1.0694 first. Break there will resume the decline from 1.1138 and target 100% projection of 1.1138 to 1.0694 from 1.0980 at 1.0536.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

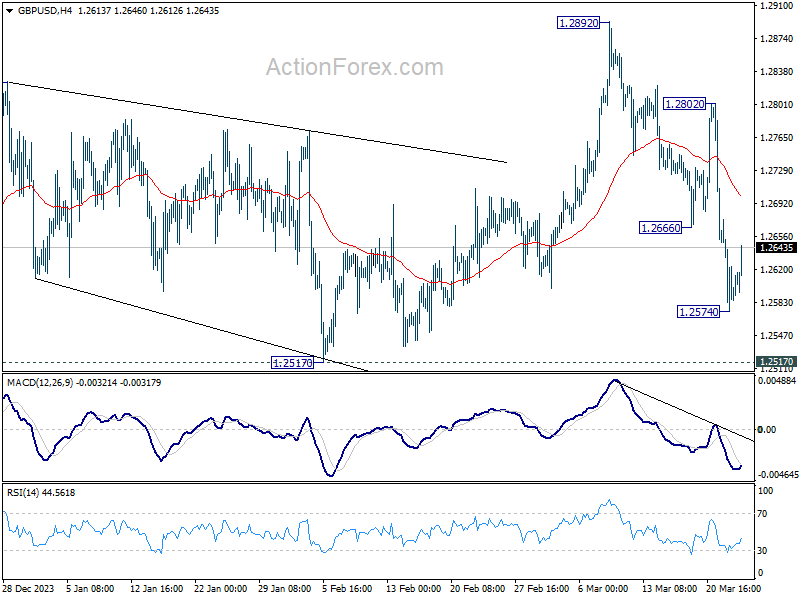

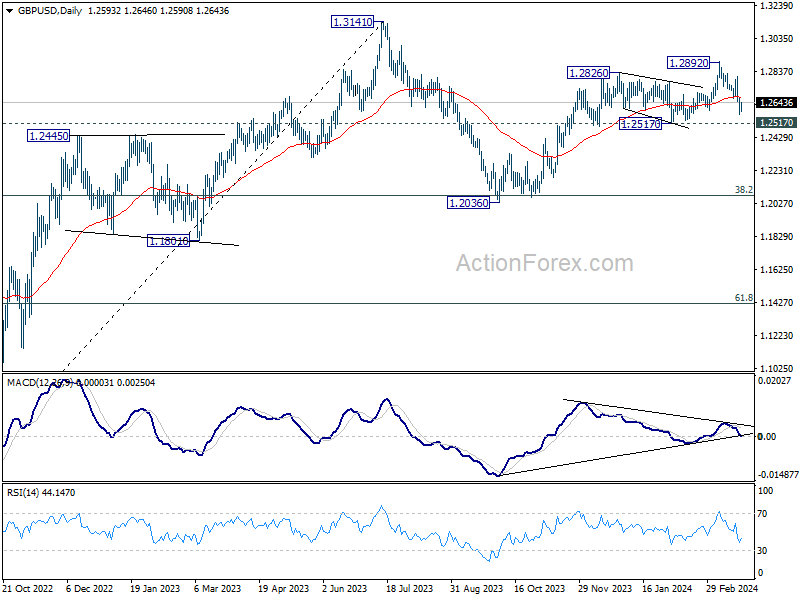

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2558; (P) 1.2617; (R1) 1.2658; More...

Intraday bias in GBP/USD is turned neutral with current recovery and some consolidations would be seen first. But risk will stay on the downside as long as 55 4H EMA (now at 1.2700) holds. Below 1.2574 will resume the fall from 1.2892 to 1.2517 structural support first. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Subdued Currency Movements, Cautious Stocks, Range Trading Gold

Mild risk-off mood is seen in the global financial markets today, starting from the the noticeable retreat in Japan's Nikkei, then the marginal declines across European stock indices, alongside soft US futures. However, this sense of caution has not significantly rippled through the currency markets, where activity remains largely subdued. Notably, most major currency pairs and crosses have maintained tight ranges, except for a few Sterling crosses which have shown more activity.

British Pound is currently the stronger one, alongside Australian Dollar and New Zealand Dollar, Conversely, Swiss Franc, Dollar, and Japanese Yen are registering softer performances. This paints a picture typically associated with risk-on market behavior, rather than risk-off. Euro and Canadian Dollar find themselves positioned in the the middle. Market activity is expected to remain muted throughout the session, particularly given the sparse US economic calendar.

Technically, a short term top has likely formed at 2222.66 in Gold, with D MACD crossed below signal line. Some consolidations would be seen first. But downside should be contained by 38.2% retracement of 1984.05 to 2222.66 at 2131.51 to bring another rally. Above 2222.66 will resume the long term up trend to 100% projection of 1614.60 to 2062.95 from 1810.26 at 2259.15. However, sustained break of 2131.51 fibonacci support will bring deeper pull back to 55 D EMA (now at 2085.37).

In Europe at the time of writing, FTSE is down -0.42%. DAX is up 0.02%. CAC is down -0.38%. UK 10-year yield is down -0.0747 at 3.962. Germany 10-year yield is up 0.025 at 2.350. Earlier in Asia, Nikkei fell -1.16%. Hong Kong HSI fell -0.16%. China Shanghai SSE fell -0.71%. Singapore Strait Times fell -0.62%. Japan 10-year JGB yield fell -0.0078 to 0.736.

ECB's Lane confident that wages growth is on track to normalize

ECB Chief Economist Philip Lane, in a podcast published today, conveyed a sense of confidence among policymakers regarding wage growth trends. Lane articulated that policymakers are "confident" that wages growth is "on track" to return to normal.

"If this assessment is confirmed, then we will start looking more closely at reversing some of the rate increases we've made," he added.

Adding to the conversation, Governing Council member Fabio Panetta addressed an audience at a separate event, underscoring the feasibility of a rate cut given the current inflation trend.

"The consensus emerging - especially in recent weeks - within the ECB governing council points in this direction," Panetta noted.

BoJ Jan minutes: No need for aggressive tightening like Western counterparts

BoJ's minutes from January meeting, ahead of the landmark March decision to end negative interest rates, reveal a cautious approach towards monetary policy adjustments. Members highlighted the Japan's economic conditions "differed significantly" to those of US and Europe when they initiated interest rate hikes a few years ago. The consensus was clear: it was "not required in Japan to conduct rapid monetary tightening" as seen in Western economies.

Further discussions underscored three primary risks to Japan's economic activity: shifts in global economic performance and financial markets, fluctuations in commodity and grain import prices, and future growth expectations of firms and households.

Members agreed these factors could significantly influence economic outcomes and emphasized the need for vigilance towards price-setting behaviors within the economy, as well as the impact of currency and commodity price movements on domestic inflation.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2558; (P) 1.2617; (R1) 1.2658; More...

Intraday bias in GBP/USD is turned neutral with current recovery and some consolidations would be seen first. But risk will stay on the downside as long as 55 4H EMA (now at 1.2700) holds. Below 1.2574 will resume the fall from 1.2892 to 1.2517 structural support first. Decisive break there will suggest that rise from 1.2036 has completed at 1.2892 already, and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which might still be in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 14:00 | USD | New Home Sales Feb | 675K | 661K |