Sample Category Title

Gold Hits Record as Net Long Positions Jump

The US economy added 275K new nonfarm jobs last month, significantly more than around 200K new job additions penciled in by analysts. But happily, the unemployment rate unexpectedly rose to 3.9% and wages grew slower than expected on a yearly basis and were almost flat on a monthly basis. The fact that another strong NFP read didn’t translate into higher wages gave a peace of mind to investors. US yields fell and the US dollar index tumbled in the immediate aftermath of the US jobs data, the EURUSD spiked to 1.0980.

While I found that the dollar selloff was a bit exaggerated – given that the US economy still added 275K new nonfarm jobs and wages grew 4.3% on yearly basis, more than twice the Fed’s inflation target - Friday’s reaction to the jobs data revealed an important information: investors don’t care about the strength of the US economy and the labour market, they only care about inflation. And because the wages data was lower than expected, Friday’s jobs day wasn’t a disaster for the Federal Reserve (Fed) doves. The market still gives around 74% chance for a 25bp cut from the Fed this June.

This week, attention shifts to the US CPI print, due tomorrow. The headline inflation is expected to steady near 3.1% on a yearly basis, core inflation is expected to have eased from 3.9% to 3.7%. But the monthly figures could print another strong month. If that’s the case, we shall see a softening in dovish Fed expectations. Remember, Fed Chair Powell said last week that the Fed ‘can and will’ start cutting the rates this year, but he also said that they are in no rush.

The US dollar begins the week on a negative note, the EURUSD gave back all post-US jobs data gains as the European Central Bank (ECB) Chief Lagarde gave a strong signal at her press conference last week that the ECB could take the first step as early as in June. Pricing in the market suggests that the ECB will cut the rates by 100bp this year – versus around 80bp cut from the Fed. The ECB’s dovish divergence could limit the euro’s upside potential against the dollar into the 1.10 psychological mark – unless the inflation numbers from the US comes in surprisingly strong.

The euro and sterling recorded their best performance against the US dollar in months on expectation that the first rate cut from the Fed won’t be delayed beyond June, and gold hit another record on Friday. The price of an ounce climbed to $2195 as the market found comfort in the idea that the Fed will cut in June. Released last Friday, the CFTC data showed that money managers boosted their long gold positions in the week through March 5th and the net long positions jumped 35% from a week earlier as they were looking to hedge against a potential post-jobs data market selloff. Also, data shows that China has been increasing its gold purchases since the beginning of last year; the central bank probably wants to diversify its dollar holdings and households certainly want to seek refuge amid the property meltdown. The question is, could the rally extend beyond $2200? Yes, it could. The inflation-adjusted gold price is below the 2020 peak – which would stand at $2323 if the price is adjusted to inflation of today. In 2011, gold traded at $2581 and back in 1980, the price of an ounce went past $3000 in inflation-adjusted terms. There is never an upper limit when people want to buy. But any retreat in Fed expectations could cool down the short term price surges.

In equities, the decline in US yields and the dollar didn’t boost appetite in major US indices. The S&P500 hit another record but closed the session 0.65% down, while Nasdaq 100 fell more than 1.50%. Tech stocks saw their largest weekly outflow on record.

Elsewhere, inflation in China rose for the first time in 6 months thanks to the Lunar New Year holiday boost in spending, but producer prices fell 2.7%. Nearby, the Japanese stocks fell as the USDJPY sank below 147 on rising speculation that the BoJ could exit the negative rates as soon as this month. I still think that there is more chance of a hint regarding the first rate hike than a concrete action on the rates front at this month’s BoJ meeting, but even a good hint could help investors rush into a long yen trade and pull the USDJPY toward the 140 mark. Finally, in energy, US crude slipped below the 200-DMA this Monday following last week’s failure to increase gains above the $80pb psychological level.

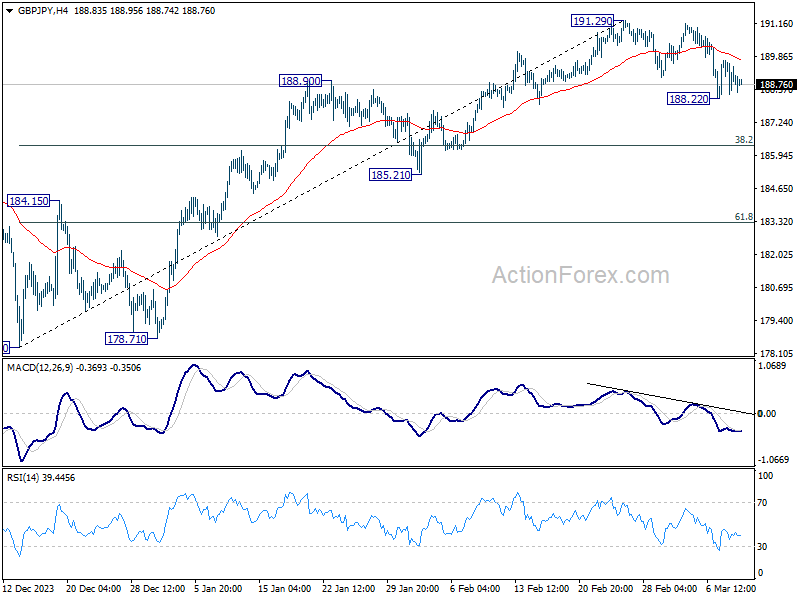

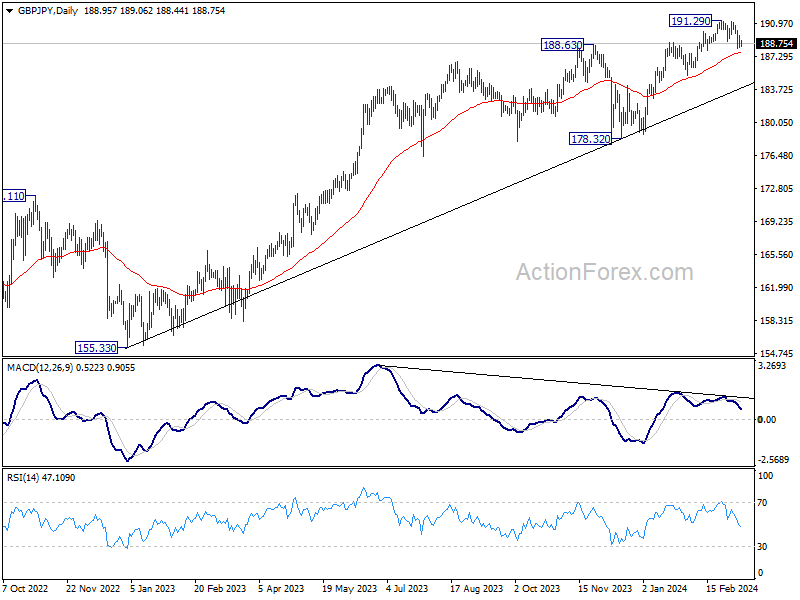

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.45; (P) 189.08; (R1) 189.78; More.....

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, below 188.22 will resume the decline from 191.29 to 38.2% retracement of 178.32 to 191.29 at 186.33. Sustained break there will raise the chance of larger scale correction and target 61.8% retracement at 183.27. On the upside, though, firm break of 55 4H EMA (now at 189.84) will retain near term bullishness and bring retest of 191.29 high.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

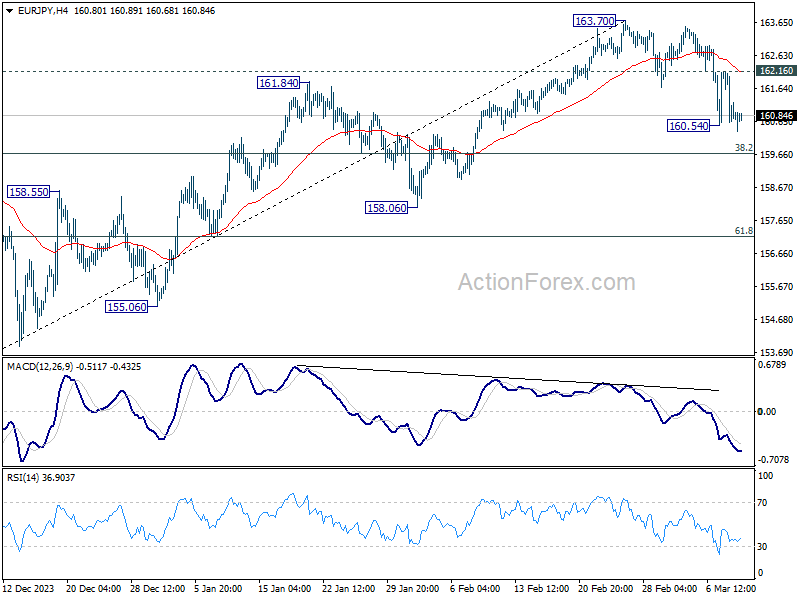

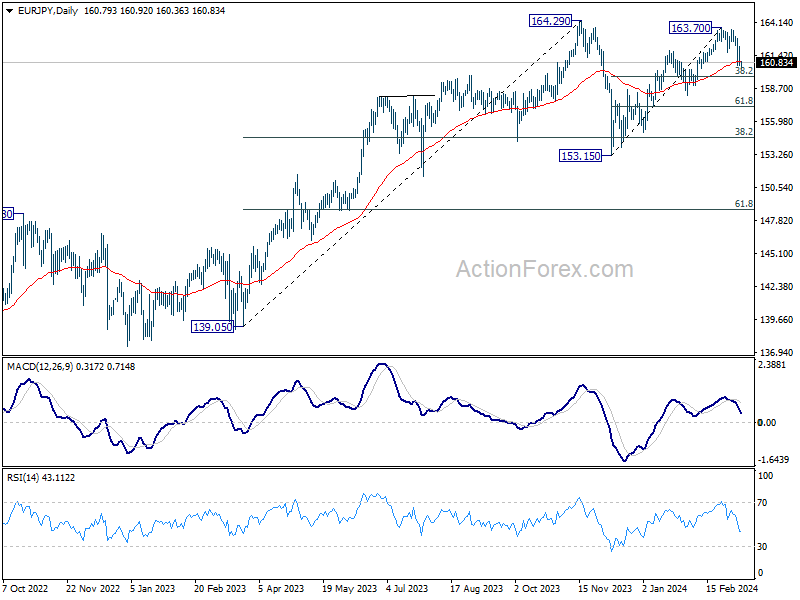

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.26; (P) 161.22; (R1) 161.82; More...

Intraday bias in EUR/JPY is back on the downside with breach of 160.54 temporary low. Fall from 163.70 is resuming to 38.2% retracement of 153.15 to 163.70 at 159.66. Sustained break there will indicate that fall from 163.70 is reversing whole rise from 153.13, and target 61.8% retracement at 157.18. On the upside, though, above 162.16 minor resistance will retain near term bullishness, and bring retest of 163.70.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 which could still be extending. As long as 148.38 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage. Next target would be 169.96 (2008 high).

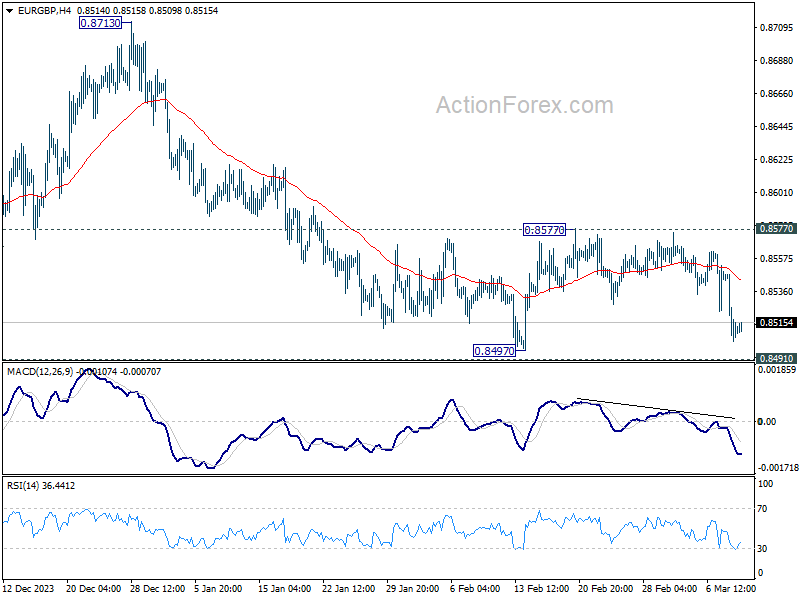

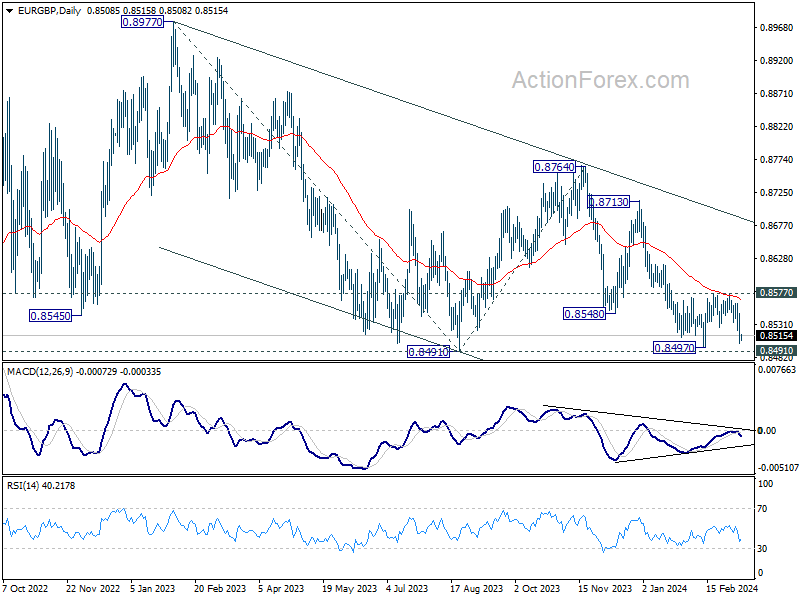

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8491; (P) 0.8520; (R1) 0.8536; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside decisive break of 0.8491/7 support zone will confirm larger down trend resumption and target 0.8464 projection level first. Nevertheless, firm break of 0.8577 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

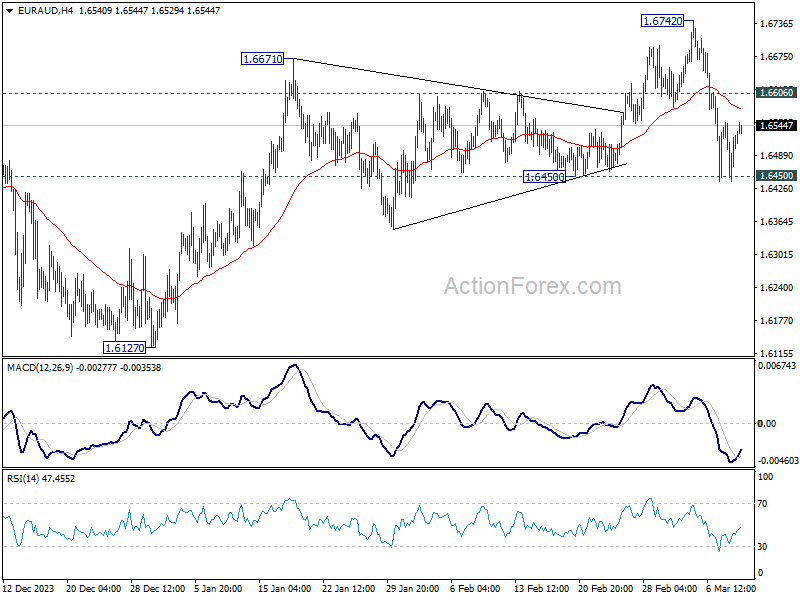

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6451; (P) 1.6502; (R1) 1.6562; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the downside, decisive break of 1.6450 support will argue that whole rebound from 1.6127 has completed with three waves up to 1.6742 already. Near term outlook will be turned bearish for 1.6127 again, to extend the whole corrective pattern from 1.7062. Nevertheless, strong rebound from current level, followed by break of 1.6606 minor resistance, will retain near term bullishness and bring retest of 1.6742.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

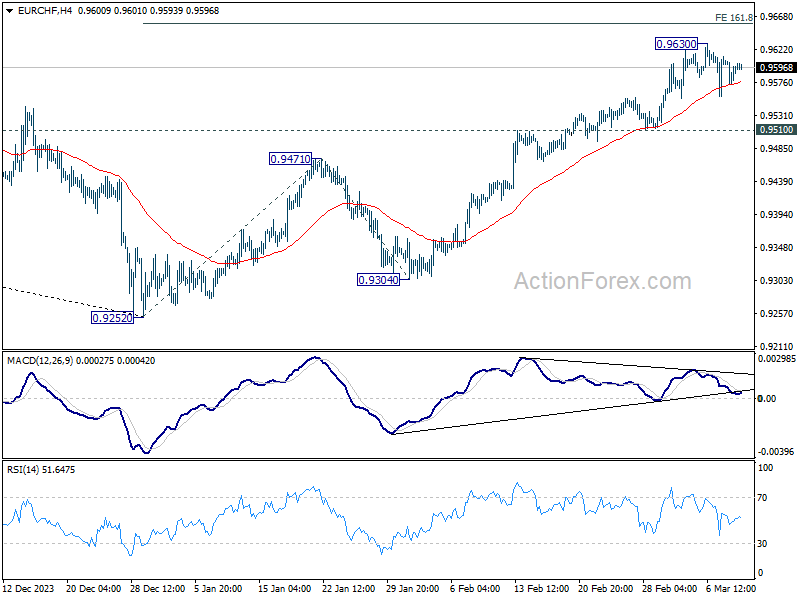

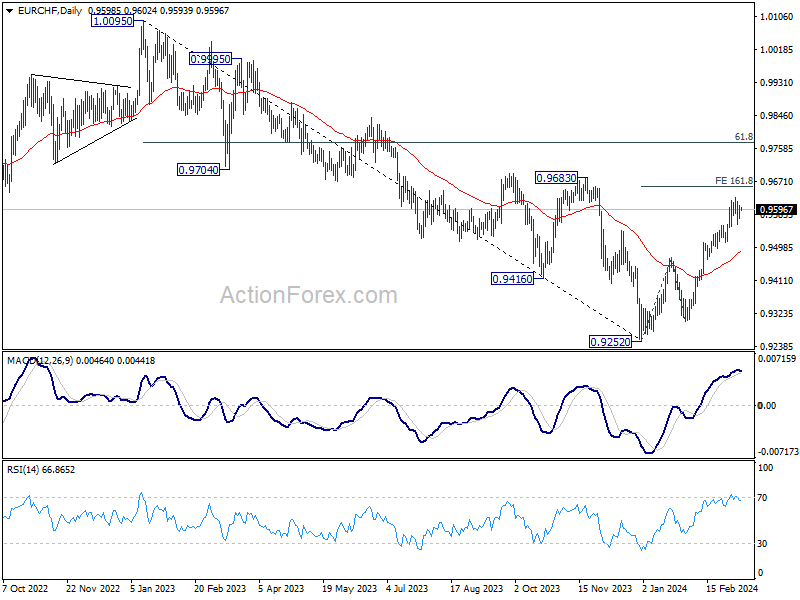

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9581; (P) 0.9596; (R1) 0.9615; More...

Intraday bias in EUR/CHF remains neutral as consolidation from 0.9630 is extending. As long as 0.9510 support holds, further rally is still expected. On the upside, break of 0.9630 will resume the rise from 0.9252 and target 161.8% projection of 0.9252 to 0.9471 from 0.9304 at 0.9658 next. However, considering bearish divergence condition in 4H MACD, firm break of 0.9510 will turn bias back to the downside for deeper fall.

In the bigger picture, as long as 0.9683 resistance holds, rebound from 0.9252 are seen as a corrective move only. Larger down trend is expected to resume through 0.9252 after the correction completes. However, firm break of 0.9683 and sustained trading above 55 W EMA (now at 0.9620) will argue that 0.9252 is already a medium term bottom. Stronger rise would then be seen 61.8% retracement of 1.0095 to 0.9252 at 0.9773 and above.

Big Inflation Week Kicks Off

In focus today

Today is a relatively quiet day on the global data front.

In Denmark, CPI inflation is released for February. We expect that inflation decreased to 1.0% y/y in February from 1.2% y/y in January, largely driven by food prices as the February price surge from last year no longer features in the measure. Additionally, Danish foreign trade and current account data for January is also scheduled for release.

In Norway, February inflation figures are released. We expect Norwegian core inflation to remain unchanged at 5.3%, as import prices are likely to have risen again and will counteract somewhat lower food prices. If proven right, this would be 0.2 pp. lower than Norges Bank expected in the December MPR and in isolation should be an argument for a less hawkish Norges Bank in March, but far from a game changer.

Focus this week will be on inflation releases, with the star of the show being the US CPI inflation release on Tuesday. January's surprisingly strong print dampened rate cut expectations for 2024 in tandem with other strong macro data. Hence, February figures coming in hotter than expected could send rate cut expectations further south. Our call is for the first Fed cut at the May meeting. Furthermore, in China we get credit and money growth between 9 and 15 March but there is no fixed date or time. The credit data is very volatile from month to month, but the trend has been relatively robust in recent months reflecting the stimulus by the government.

Economic and market news

What happened overnight

In Japan, the final Q4 2023 GDP print was released. The print was revised up to 0.1% q/q from -0.1% q/q, indicating that the Japanese economy averted a technical recession in Q4. Moreover, speculations regarding the Bank of Japan hiking rates in March flared up slightly amid expectations of robust pay increases in this year's annual wage negotiations. This led to the Japanese yen moving somewhat higher.

In China, Chinese regulators engaged in talks with financial institutions and private debt to bolster financing support and extend debt maturity for Vanke, a state-backed developer. Recently, the property developer has faced pressure as investors have sold shares and bonds due to liquidity concerns, prompted by reports of the state-owned entity seeking debt maturity extension with some insurers.

What happened over the weekend and on Friday

In the US, on Friday, the February Jobs Report sent mixed signals. Non-farm payrolls (NFP) came in higher than expected at +275k (cons: 200k). However, at the same time, past months' figures were revised down by a cumulative 167k, offsetting the upside surprise in February. In contrast to the NFP, the household survey (which counts the number of employed workers) was markedly weaker at -184k (Jan: -31k). Coupled with the labour force growing by +150k, the unemployment rate climbed higher to 3.9% from 3.7%, indicating that some slack is slowly building in the labour markets, which is good news for the Fed. On the wage front, average hourly earnings growth declined considerably to 0.1% m/m SA, mainly reflecting a rise in the average hours worked, with wage sum growth continuing its declining trend seen recently.

On the political front, the US government avoided a partial shutdown as six out of 12 individual appropriations bills were signed into law by President Biden. However, with the deadline for the remaining funding bills set for 22 March, a partial shutdown is still possible.

In Europe, euro area wage growth for Q4 2023 was released on Friday. The figure came in at 4.5% y/y down from 5.1% y/y in Q3. Overall wage growth remains too elevated for a 2% inflation target. Hence, we believe that the ECB most likely awaits Q1 2024 data to become confident that wage growth is consistently decreasing, which serves as a key reason why we expect the ECB to start lowering rates at the June meeting.

In China, the February CPI was released on Saturday. The print surprised to the upside, with Chinese consumer prices ticking higher for the first time in six months, coming in at 1.0% m/m and 0.7% y/y (cons: 0.7% m/m, 0.3% y/y). The positive figures are strongly attributed to a spending boom following the Lunar New Year.

In Saudi Arabia, state-owned Saudi Aramco raised its dividend to nearly USD 100bn amid reporting its second-highest annual profit ever despite lower oil prices. The payout stands as the primary revenue source for the Saudi government, which seeks to fund its ambitious modernization plans via the generated profits.

In the geopolitical space, US, French, and British forces retaliated against a Houthi attack on a bulk carrier and destroyer by striking dozens of drones in the Red Sea area. Additionally, the European Commission announced on Friday that a maritime aid corridor could commence operations between Cyprus and Gaza over the weekend, in a project financed by the UAE. However, as of early this morning, the vessel remains docked in Cyprus.

Equities: Global equities were lower Friday, dragged down by US and long duration growth stocks. The pullback in some the best performing names over the last year came despite a day with solid macro figures basically confirming the current investment narrative of a soft landing. Please note both small caps and banks were outperforming and 15 out of 25 industries in the US were higher, highlighting that the sell-off was being macro related. In US on Friday, Dow -0.2%, S&P 500 +0.7%, Nasdaq -1.2% and Russell 2000 -0.10%. Japanese equities are sharply lower this morning as Bank of Japan is increasingly expected to tighten policies soon. US and European futures are lower as well.

FI: US Treasury yields continued to decline last week as 10Y US treasury yields declined some 12-13bp during the week. We have seen a similar move in the 10Y German government bond, where the yield has declined some 13-14bp.

Furthermore, the spread compression in both the German ASW-spreads and the BTPS-Bund spread has been relentless. The Bund ASW-spread is slowly moving towards 30bp and the 10Y BTPS-Bund is gradually tightening towards 125bp. Short-term the momentum seems to be for a tighter as there is plenty of supply from Germany also relative to Italy. This week Germany will tap EUR 9bn in the 2Y and 10Y segments, while Italy will tap EUR 8.5bn in the 7Y to 15Y segments.

FX: The USD had its worst week since December losing out vs the rest of G10, with JPY as the winner with a 2% appreciation. The SEK also had a strong week, with EUR/SEK once more challenging the lower bound of the recent range (11.20). This week brings a lot of interesting macro data, which are bound to influence FX trading.

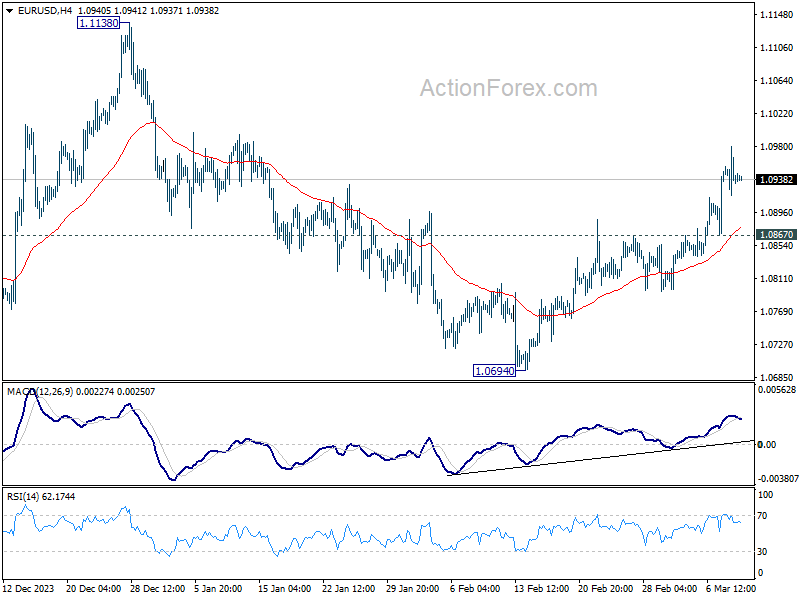

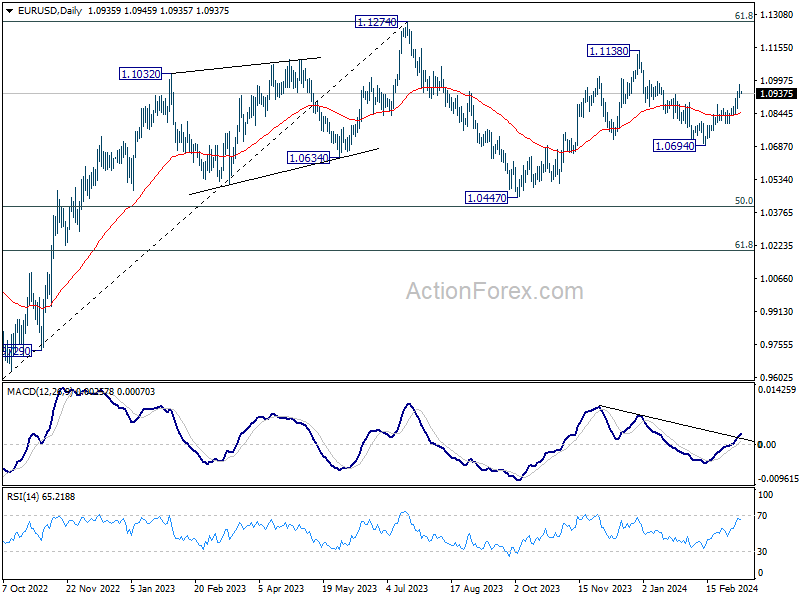

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0911; (P) 1.0946; (R1) 1.0974; More...

Intraday bias is EUR/USD remains on the upside at this point. Fall from 1.1138 could have completed at 1.0694, as a correction to rise from 1.0447. Further rally would be seen to retest 1.1138 next. On the downside, below 1.0867 minor support will turn intraday bias neutral and bring consolidations.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0694 support will argue that the third leg has already started for 1.0447 and possibly below.

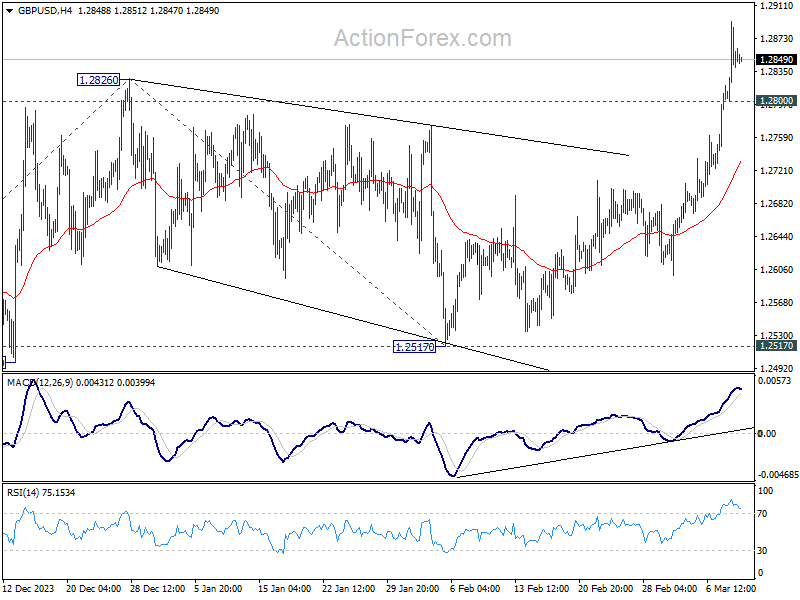

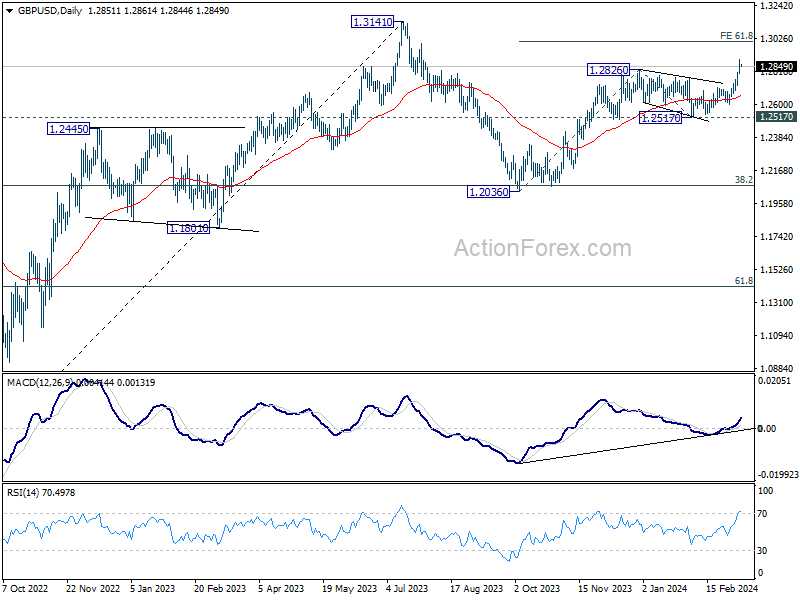

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2809; (P) 1.2852; (R1) 1.2902; More...

Intraday bias in GBP/USD remains on the upside at tis point. Current rise is part of the rally from 1.2063, and should target 61.8% projection of 1.2036 to 1.2826 from 1.2517 at 1.3005. On the downside, below 1.2800 minor support will turn intraday bias neutral first. But further rise will remain in favor as long as 55 4H EMA (now at 1.2732) holds.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

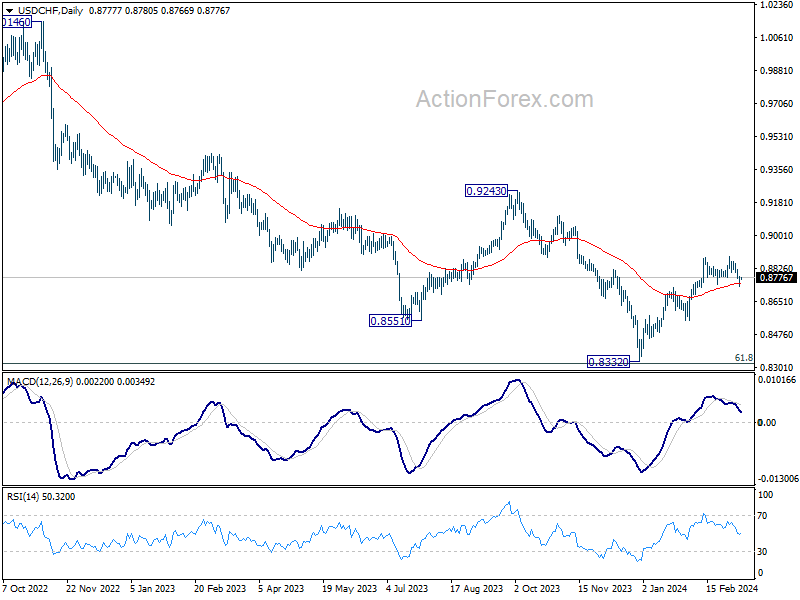

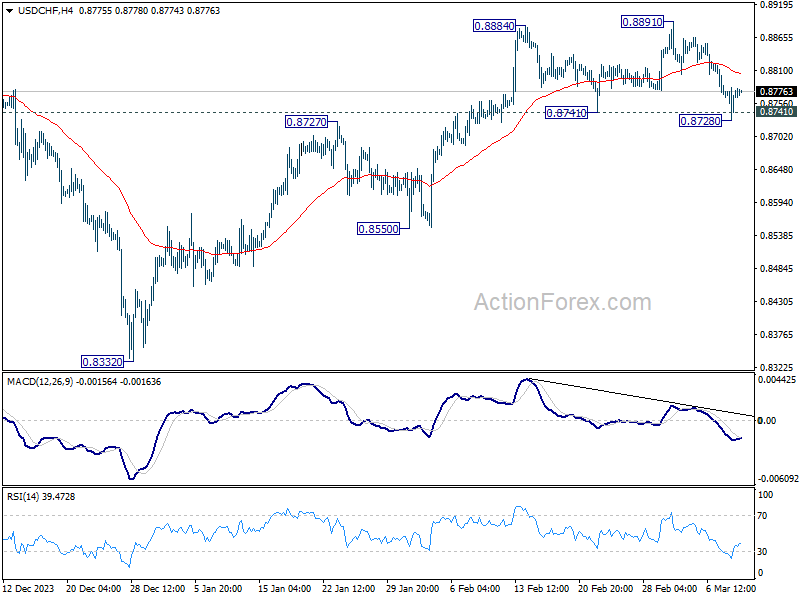

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8743; (P) 0.8764; (R1) 0.8797; More....

Intraday bias in USD/CHF remains neutral for the moment. On the downside, sustained break of 0.8741 will argue that the whole rebound from 0.8332 might have completed, and bring deeper fall to 0.8550 support. Nevertheless, strong bounce from current level will retain near term bullishness. Further break of 0.8891 will resume the rise from 0.8332.

In the bigger picture, price actions from 0.8332 medium term bottom as seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Further rise would be seen as long as 0.8555 support holds. But upside should be limited by 0.9243 resistance, at least on first attempt.