Sample Category Title

Summary 2/19 – 2/23

Monday, Feb 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Jan | 48.8 | |

| 23:50 | JPY | Machinery Orders M/M Dec | 2.50% | -4.90% |

| 00:01 | GBP | Rightmove House Price Index M/M Feb | 1.30% | |

| 11:00 | EUR | German Buba Monthly Report | ||

| 13:30 | CAD | Industrial Product Price M/M Jan | 0.10% | -1.50% |

| 13:30 | CAD | Raw Material Price Index Jan | 0.80% | -4.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Jan | |

| Forecast: | Previous: 48.8 | ||

| 23:50 | JPY | Machinery Orders M/M Dec | |

| Forecast: 2.50% | Previous: -4.90% | ||

| 00:01 | GBP | Rightmove House Price Index M/M Feb | |

| Forecast: | Previous: 1.30% | ||

| 11:00 | EUR | German Buba Monthly Report | |

| Forecast: | Previous: | ||

| 13:30 | CAD | Industrial Product Price M/M Jan | |

| Forecast: 0.10% | Previous: -1.50% | ||

| 13:30 | CAD | Raw Material Price Index Jan | |

| Forecast: 0.80% | Previous: -4.90% | ||

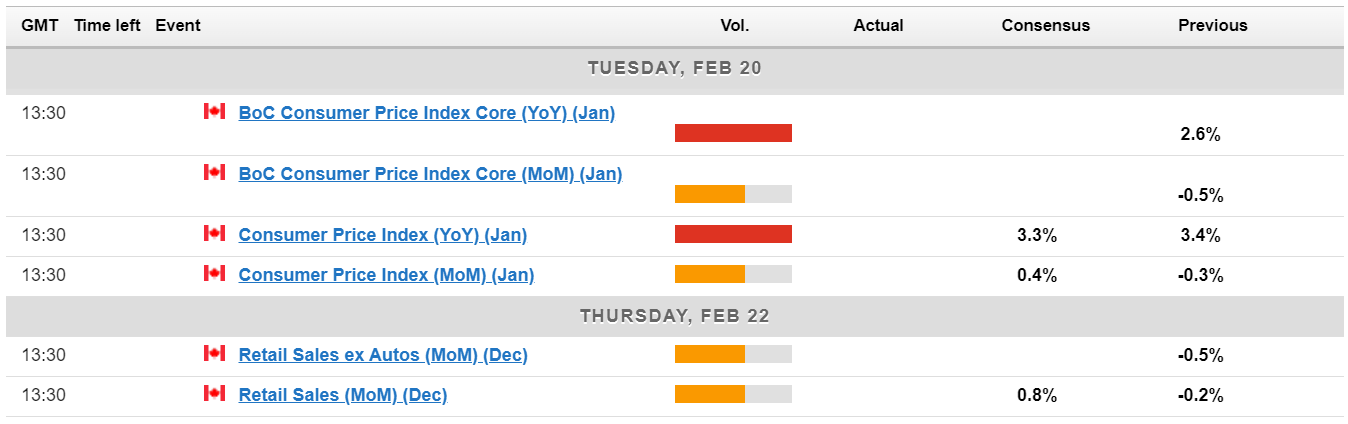

Tuesday, Feb 20, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | ||

| 01:15 | CNY | PBoC 1Y Loan Prime Rate | 3.45% | 3.45% |

| 01:15 | CNY | PBoC 5Y Loan Prime Rate | 4.10% | 4.20% |

| 07:00 | CHF | Trade Balance (CHF) Jan | 2.35B | 1.25B |

| 09:00 | EUR | Eurozone Current Account (EUR) Dec | 20.3B | 24.6B |

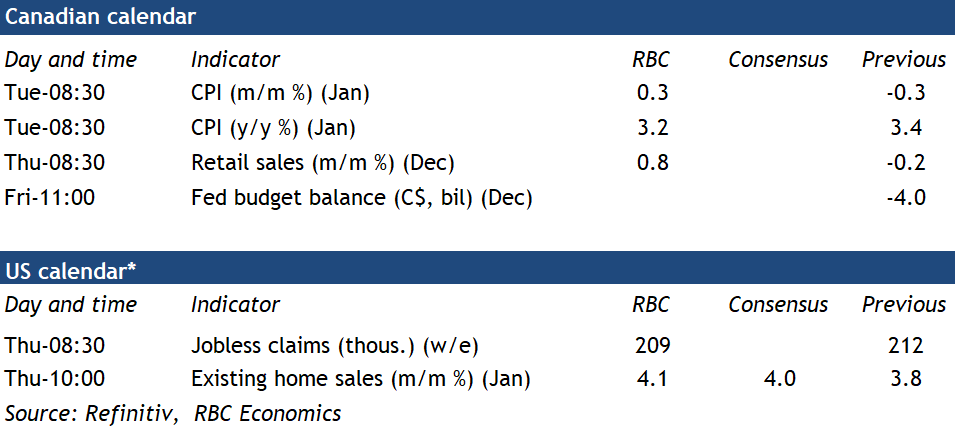

| 13:30 | CAD | CPI M/M Jan | 0.40% | -0.30% |

| 13:30 | CAD | CPI Y/Y Jan | 3.30% | 3.40% |

| 13:30 | CAD | CPI Median Y/Y Jan | 3.60% | 3.60% |

| 13:30 | CAD | CPI Trimmed Y/Y Jan | 3.60% | 3.70% |

| 13:30 | CAD | CPI Common Y/Y Jan | 3.80% | 3.90% |

| 21:45 | NZD | PPI Input Q/Q Q4 | 0.40% | 1.20% |

| 21:45 | NZD | PPI Output Q/Q Q4 | 0.40% | 0.80% |

| 23:50 | JPY | Trade Balance (JPY) Jan | -0.23T | -0.41T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | RBA Meeting Minutes | |

| Forecast: | Previous: | ||

| 01:15 | CNY | PBoC 1Y Loan Prime Rate | |

| Forecast: 3.45% | Previous: 3.45% | ||

| 01:15 | CNY | PBoC 5Y Loan Prime Rate | |

| Forecast: 4.10% | Previous: 4.20% | ||

| 07:00 | CHF | Trade Balance (CHF) Jan | |

| Forecast: 2.35B | Previous: 1.25B | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Dec | |

| Forecast: 20.3B | Previous: 24.6B | ||

| 13:30 | CAD | CPI M/M Jan | |

| Forecast: 0.40% | Previous: -0.30% | ||

| 13:30 | CAD | CPI Y/Y Jan | |

| Forecast: 3.30% | Previous: 3.40% | ||

| 13:30 | CAD | CPI Median Y/Y Jan | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Jan | |

| Forecast: 3.60% | Previous: 3.70% | ||

| 13:30 | CAD | CPI Common Y/Y Jan | |

| Forecast: 3.80% | Previous: 3.90% | ||

| 21:45 | NZD | PPI Input Q/Q Q4 | |

| Forecast: 0.40% | Previous: 1.20% | ||

| 21:45 | NZD | PPI Output Q/Q Q4 | |

| Forecast: 0.40% | Previous: 0.80% | ||

| 23:50 | JPY | Trade Balance (JPY) Jan | |

| Forecast: -0.23T | Previous: -0.41T | ||

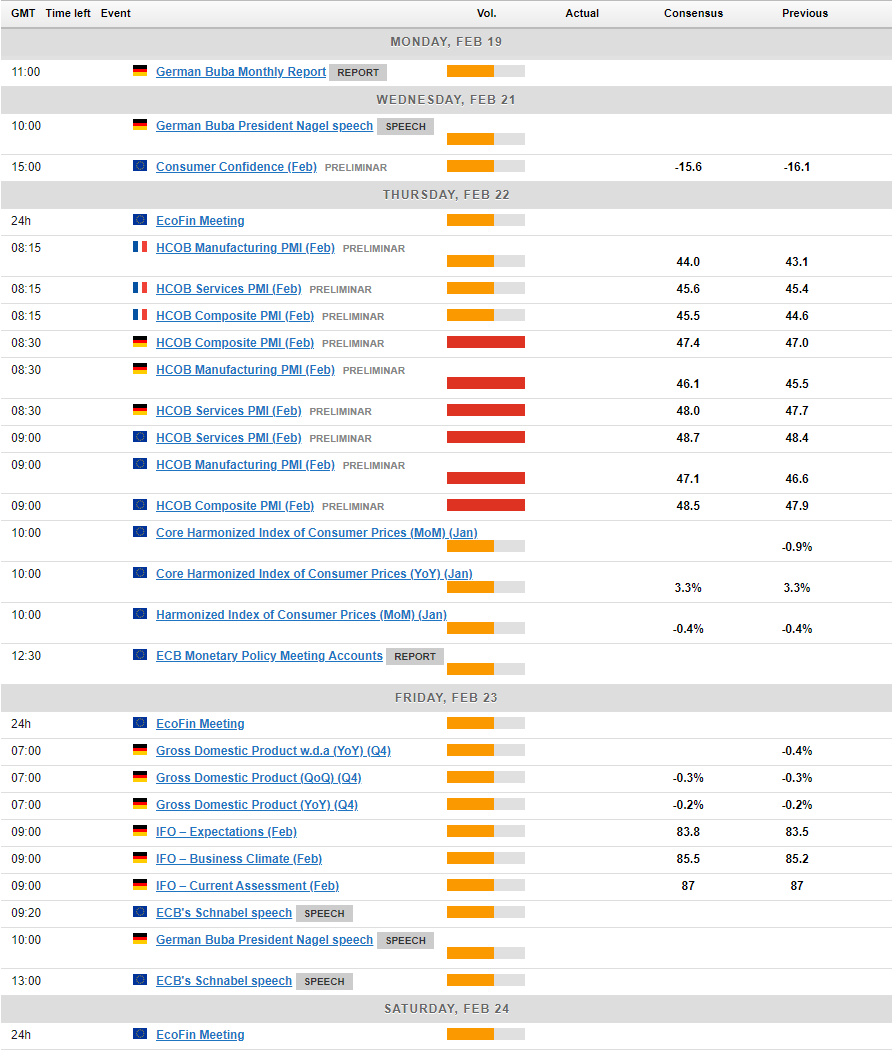

Wednesday, Feb 21, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Jan | -0.03% | |

| 00:30 | AUD | Wage Price Index Q/Q Q4 | 0.90% | 1.30% |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Jan | -18.4B | 6.8B |

| 13:30 | CAD | New Housing Price Index M/M Jan | 0.10% | 0.00% |

| 15:00 | EUR | Eurozone Consumer Confidence Feb P | -16 | -16 |

| 19:00 | USD | FOMC Minutes | ||

| 21:45 | NZD | Trade Balance (NZD) Jan | -200M | -323M |

| 22:00 | AUD | Manufacturing PMI Feb P | 50.1 | |

| 22:00 | AUD | Services PMI Feb P | 49.1 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Jan | |

| Forecast: | Previous: -0.03% | ||

| 00:30 | AUD | Wage Price Index Q/Q Q4 | |

| Forecast: 0.90% | Previous: 1.30% | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Jan | |

| Forecast: -18.4B | Previous: 6.8B | ||

| 13:30 | CAD | New Housing Price Index M/M Jan | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Feb P | |

| Forecast: -16 | Previous: -16 | ||

| 19:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Trade Balance (NZD) Jan | |

| Forecast: -200M | Previous: -323M | ||

| 22:00 | AUD | Manufacturing PMI Feb P | |

| Forecast: | Previous: 50.1 | ||

| 22:00 | AUD | Services PMI Feb P | |

| Forecast: | Previous: 49.1 | ||

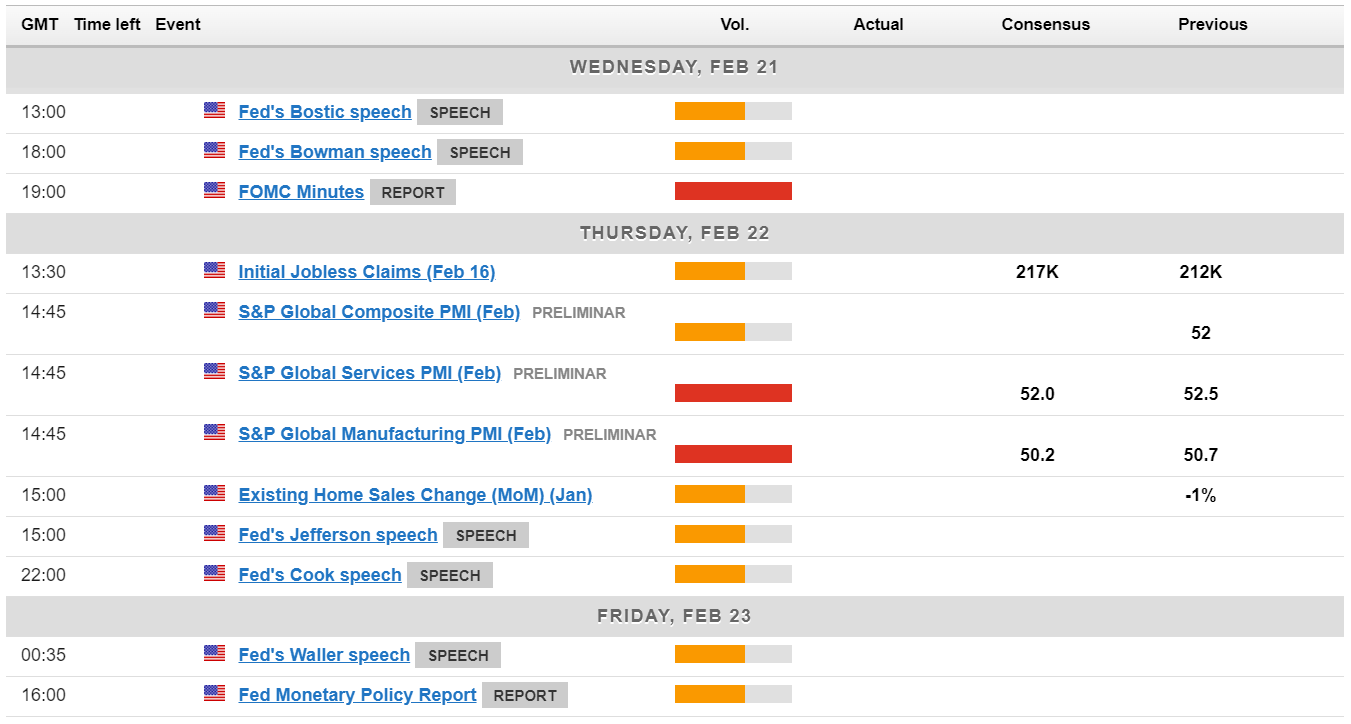

Thursday, Feb 22, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Feb P | 48.2 | 48.0 |

| 00:30 | JPY | Services PMI Feb P | 53.1 | |

| 08:15 | EUR | France Manufacturing PMI Feb P | 44.0 | 43.1 |

| 08:15 | EUR | France Services PMI Feb P | 45.6 | 45.4 |

| 08:30 | EUR | Germany Manufacturing PMI Feb P | 46.1 | 45.5 |

| 08:30 | EUR | Germany Services PMI Feb P | 48.0 | 47.7 |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | 47.1 | 46.6 |

| 09:00 | EUR | Eurozone Services PMI Feb P | 48.7 | 48.4 |

| 09:30 | GBP | Manufacturing PMI Feb P | 47.1 | 47 |

| 09:30 | GBP | Services PMI Feb P | 54.4 | 54.3 |

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 2.80% | 2.80% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 3.30% | 3.30% |

| 12:30 | EUR | ECB Meeting Accounts | ||

| 13:30 | CAD | Retail Sales M/M Dec | 0.80% | -0.20% |

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | 0.70% | -0.50% |

| 13:30 | USD | Initial Jobless Claims (Feb 16) | 217K | 212K |

| 14:45 | USD | Manufacturing PMI Feb P | 50.2 | 50.7 |

| 14:45 | USD | Services PMI Feb P | 52.0 | 52.5 |

| 15:00 | USD | Existing Home Sales Jan | 3.95M | 3.78M |

| 15:30 | USD | Natural Gas Storage | -49B | |

| 16:00 | USD | Crude Oil Inventories | 12.0M | |

| 21:45 | NZD | Retail Sales Q/Q Q4 | -0.20% | 0.00% |

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | -0.10% | 1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Feb P | |

| Forecast: 48.2 | Previous: 48.0 | ||

| 00:30 | JPY | Services PMI Feb P | |

| Forecast: | Previous: 53.1 | ||

| 08:15 | EUR | France Manufacturing PMI Feb P | |

| Forecast: 44.0 | Previous: 43.1 | ||

| 08:15 | EUR | France Services PMI Feb P | |

| Forecast: 45.6 | Previous: 45.4 | ||

| 08:30 | EUR | Germany Manufacturing PMI Feb P | |

| Forecast: 46.1 | Previous: 45.5 | ||

| 08:30 | EUR | Germany Services PMI Feb P | |

| Forecast: 48.0 | Previous: 47.7 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Feb P | |

| Forecast: 47.1 | Previous: 46.6 | ||

| 09:00 | EUR | Eurozone Services PMI Feb P | |

| Forecast: 48.7 | Previous: 48.4 | ||

| 09:30 | GBP | Manufacturing PMI Feb P | |

| Forecast: 47.1 | Previous: 47 | ||

| 09:30 | GBP | Services PMI Feb P | |

| Forecast: 54.4 | Previous: 54.3 | ||

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | |

| Forecast: 3.30% | Previous: 3.30% | ||

| 12:30 | EUR | ECB Meeting Accounts | |

| Forecast: | Previous: | ||

| 13:30 | CAD | Retail Sales M/M Dec | |

| Forecast: 0.80% | Previous: -0.20% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | |

| Forecast: 0.70% | Previous: -0.50% | ||

| 13:30 | USD | Initial Jobless Claims (Feb 16) | |

| Forecast: 217K | Previous: 212K | ||

| 14:45 | USD | Manufacturing PMI Feb P | |

| Forecast: 50.2 | Previous: 50.7 | ||

| 14:45 | USD | Services PMI Feb P | |

| Forecast: 52.0 | Previous: 52.5 | ||

| 15:00 | USD | Existing Home Sales Jan | |

| Forecast: 3.95M | Previous: 3.78M | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -49B | ||

| 16:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 12.0M | ||

| 21:45 | NZD | Retail Sales Q/Q Q4 | |

| Forecast: -0.20% | Previous: 0.00% | ||

| 21:45 | NZD | Retail Sales ex Autos Q/Q Q4 | |

| Forecast: -0.10% | Previous: 1.00% | ||

Friday, Feb 23, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Feb | -18 | -19 |

| 07:00 | EUR | Germany GDP Q/Q Q4 F | -0.30% | -0.30% |

| 09:00 | EUR | Germany IFO Business Climate Feb | 85.5 | 85.2 |

| 09:00 | EUR | Germany IFO Current Assessment Feb | 87.0 | 87.0 |

| 09:00 | EUR | Germany IFO Expectations Feb | 83.8 | 83.5 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | GfK Consumer Confidence Feb | |

| Forecast: -18 | Previous: -19 | ||

| 07:00 | EUR | Germany GDP Q/Q Q4 F | |

| Forecast: -0.30% | Previous: -0.30% | ||

| 09:00 | EUR | Germany IFO Business Climate Feb | |

| Forecast: 85.5 | Previous: 85.2 | ||

| 09:00 | EUR | Germany IFO Current Assessment Feb | |

| Forecast: 87.0 | Previous: 87.0 | ||

| 09:00 | EUR | Germany IFO Expectations Feb | |

| Forecast: 83.8 | Previous: 83.5 | ||

The Weekly Bottom Line: Inflation Progress Stalls and Spending Falls in January

U.S. Highlights

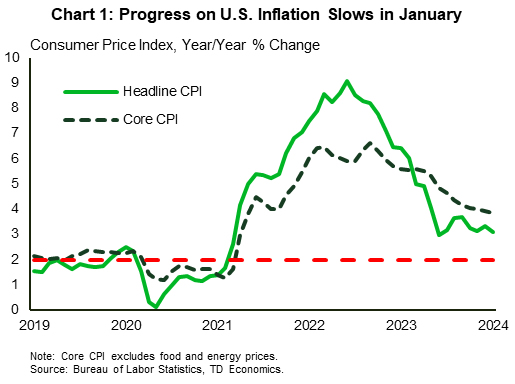

U.S. inflation rose more than anticipated to start the year, on a Consumer Price Index basis, largely due to greater price pressures within the services sector.

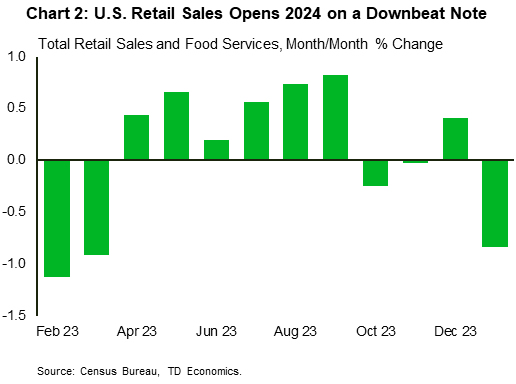

However, retail spending surprised to the downside in January, suggesting that consumer spending may be less vigorous than the stunning pace of last year.

A slowdown in housing starts and less optimistic small businesses also suggest that economic momentum may be cooling.

Canadian Highlights

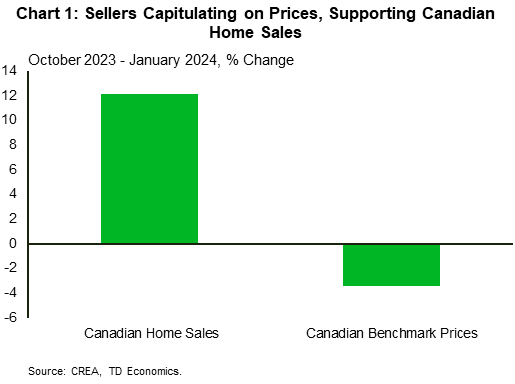

- Canadian home sales increased for the second straight month in January. However, price growth was soggy, with sellers lowering their price expectations. However, firmer price growth is likely moving forward.

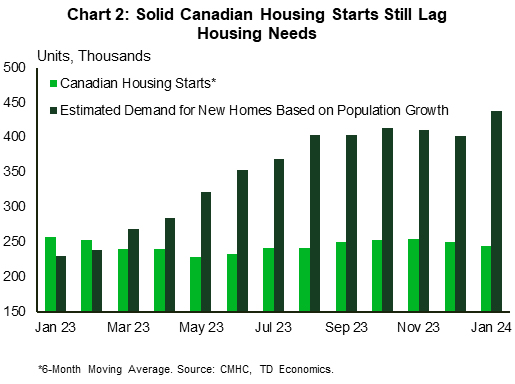

- Homebuilders continue to break ground on new homes at an impressive pace. However, starts still trail fundamental housing requirements flowing from Canada’s sizzling population growth.

- Next week’s inflation report is likely to show little change in overall inflation and sticky core measures, keeping policymakers vigilant on rates.

U.S. – Inflation Progress Stalls and Spending Falls in January

This week saw some key data releases to help gauge the state of the U.S. economy at the start of 2024, and the likely timing of a Fed rate cut. Among them were the CPI inflation and retail sales reports for January. While inflation was higher than expected, retail spending came in notably lower. Markets reacted strongly to the inflation data with stocks falling sharply and treasury yields rising.

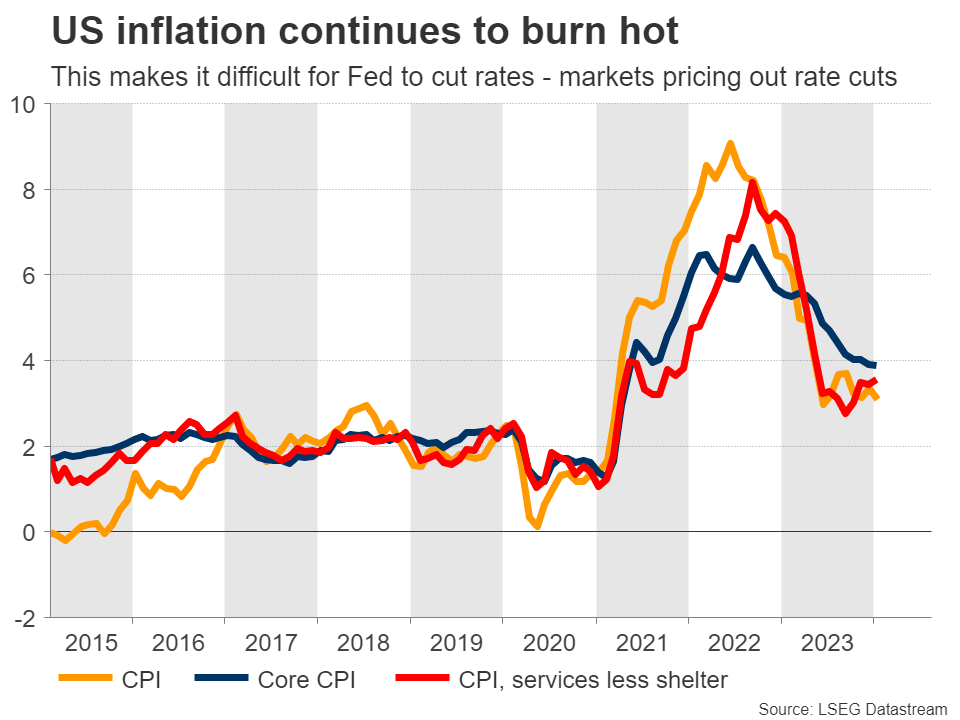

Taking a closer looker at CPI, the headline figure came in at 3.1% year-on-year (Chart 1). While this was lower than December’s 3.4%, it was higher than market expectations for 2.9%. The core measure matched December’s pace at 3.9%, but again was higher than expectations (3.7%). The near-term movements showed that progress on the disinflation front stalled a bit, largely due to services. Both monthly headline and core inflation accelerated relative to December. Also, both the 3-month and 6-month annualized growth for core CPI accelerated, suggesting that the process to tame inflation is likely to progress in uneven spurts. The producer price index corroborated the stalled CPI signal, with the PPI rising by 0.3% m/m in January (markets expected 0.1%) relative to -0.1% in December.

Turning to retail spending, consumers were a lot less jolly coming off the holiday season. Retail sales declined by 0.8% m/m in January (Chart 2). The sizeable decline was much larger than market expectations, however severe winter weather during January likely played a part in keeping consumers on the sidelines. Technical aspects of how the seasonally adjusted data is calculated may also have contributed to the relatively large decline. Nonetheless, the pullback suggests that consumer spending may be less of tailwind to U.S. economic resilience than it was last year.

Signals from the small business sector also suggest that economic activity might be slower in 2024. The NFIB’s small business optimism index declined to 89.9 from 91.1 in December, marking the biggest monthly decline since late-2022. On balance, small firms were generally less upbeat about their economic prospects, with the net percent of firms anticipating a better economy falling by 2 points. Given the higher exposure of small businesses to domestic economic conditions compared to larger firms, their downbeat mood points to headwinds ahead for the economy.

On the housing front, starts also disappointed expectations falling 14.8% to a five-month low (1.33 million) in January. The decline was in both the single and multi-family segments. Permits for future construction also fell on the month, implying that recovery in the housing market will be slow as buyers await lower mortgage rates.

Overall, data for January largely came in below expectations. This has left many market participants wondering what it all means for the timing of rate cuts. FOMC members have repeatedly stated that they need to see steady evidence that inflation is on a consistent path back to 2%. While the CPI and PPI data suggest that progress may be slow going for a bit, the pullback in other indicators point to an economy that is cooling. As such, Fed members may soon have the evidence that they need to begin the cutting cycle – it may just be later than markets desire.

Canada – Housing to Offer Little Shelter from Inflation

Canada's economic calendar was relatively light this week, so markets took their cue from developments south of the border. A hotter-than-expected U.S. inflation report reminded markets that the fight is not over, prompting a re-pricing of rate cut expectations. The prospect of delayed fed rate cuts pushed U.S. yields higher, dragging their Canadian counterparts along with them, while also weighing on the loonie. The Canadian 10-year yield hit 3.67% early in the week – the highest since November, before it retreated into week's end on softer U.S. consumer spending data.

Although the Canadian data slate was light this week, it certainly wasn’t barren. Housing took centre stage, thanks to reports on home sales and prices, alongside the latest data on homebuilding. Home sales increased for the second straight month in January, benefitting from lower borrowing costs in recent months, favourable weather conditions, and ample pent-up demand. The signal from home prices was much softer, with average home prices up only modestly while quality-adjusted benchmark prices declined.

Looking at the big picture, home sales have surged since rates broke meaningfully lower in October, while price growth has lagged (Chart 1). Our view on this dichotomy is that sellers have lowered the price expectations in order to move their homes, especially in Ontario and B.C., where conditions have recently favoured buyers. However, with supply/demand conditions now much more balanced in these markets, weak price performances are likely in the rear view.

This is not just a story for the short-term, either, as Canadian housing shortages should support higher prices over the longer-term. This week, we received homebuilding data which showed a January decline, but that starts are still elevated on a trend basis. However, the rate at which builders are breaking ground continues to lag fundamental requirements from tremendously strong population growth which has persisted into this year (Chart 2).

Resurgent housing demand, alongside tighter markets, is sure to raise some eyebrows at the Bank of Canada. Rising housing market activity supports GDP growth through a direct boost to residential investment and can stoke consumer spending as well. Meanwhile, home prices feed directly into the CPI through the shelter component, which accounts for nearly 30% of the index. We agree with the Bank of Canada that inflation can hit its 2% target, despite only gradual improvements in the shelter component. However, if the housing market heats up by more than policymakers expect, this could delay rate cuts and/or alter the speed at which they're delivered.

We won't have to wait long to observe the impacts of housing market activity on consumer costs, as the January CPI report is on tap next week. The consensus expectation is that overall inflation was little changed last month, while the Bank's preferred core measures are likely to remain sticky at above 3.5%. The Canadian inflation battle clearly still has legs, which will keep the Bank vigilant on rates.

Week Ahead North America – FOMC Minutes Key, Canadian Inflation in Focus

- Is March a live meeting for the Fed?

- Inflation data in focus as markets eye July BoC rate cut

FOMC minutes could tell us how close they are to rate cuts

It’s been a turbulent start to the year, one in which we’ve seen significant shifts in expectations for the economy, interest rates, and the markets.

This past week was evidence of that with inflation exceeding expectations while retail sales dived at the start of the year. That’s not made the Federal Reserve’s job of determining when the correct time to start cutting rates any easier.

The mixed data since the last meeting though makes the FOMC minutes – released on Wednesday – all the more interesting. March appears unlikely for the first cut but the minutes could tell us how close policymakers think they are.

Is inflation set to fall again in Canada?

There’s a lot of economic data being released next week which will be of keen interest to traders, particularly in light of what we’ve seen elsewhere recently.

USDCAD Daily

Week Ahead Europe – Eurozone Inflation and PMI Surveys Eyed

- Is a March rate cut from the ECB still possible?

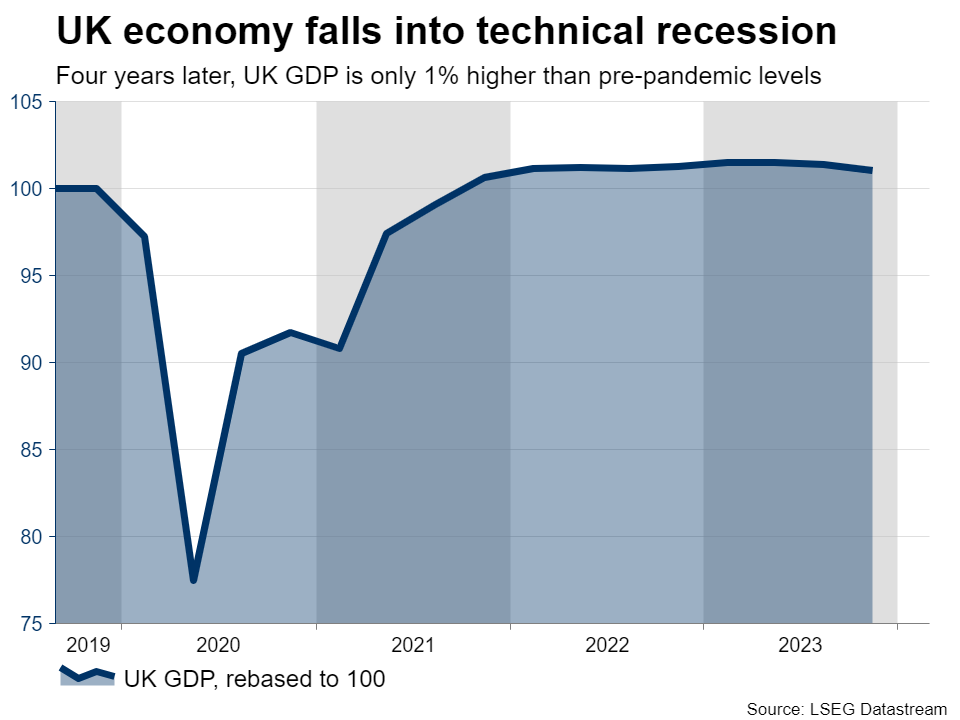

- UK surveys eyed as the economy falls into recession

Could eurozone inflation figures reignite the rate cut debate next month?

March has widely been written off as the likely moment that some major central banks will start cutting interest rates but data next week may change that for one.

The European Central Bank is arguably closer than any other at this point to pulling the trigger on an easing cycle and while the odds of a cut, in the markets, are still low, they could improve if we see a significant revision to the January inflation data on Thursday.

With the bloc flirting with recession, it won’t take much of a downward revision for the ECB to have to consider rate cuts, with the current rate of headline and core CPI within touching distance of the 2% target.

Also on Thursday, we’ll get PMI figures for the eurozone, Germany, and France which could offer an up-to-date view on the economic situation and prospects for the euro area. The surveys are currently deep in negative territory so any improvement, even one that leaves it in contraction territory will be welcome.

EURUSD Daily

Source – OANDA

EURUSD has continued to trend lower this week but it may be running into some support. The latest rotation off the 61.8% Fibonacci retracement level came amid weaker momentum and a divergence between the price and the MACD.

Perhaps this is a sign of exhaustion in the decline since the turn of the year and that it occurs around a key Fib level may be considered a further bullish indicator.

PMIs eyed after the UK fell into recession at the end 2023

We’ve had a lot of data from the UK over the last week which left us with a much better idea of where things stand going into a big election year.

The economy fell into recession at the end of 2023, albeit a very mild one, while inflation didn’t rise last month as it was expected to, and retail sales roared back at the start of the year. While there’s plenty of room for improvement, the UK is in a good position to see rates falling soon and the BoE is confident that the economy will quickly bounce back too.

It’s much quieter next week on the data front, with manufacturing and services PMIs on Thursday the only notable releases. The services component has rebounded strongly over the last couple of months and another good reading could back up the BoE view on the economy this year.

GBPUSD Daily

Source – OANDA

It’s been quite a choppy week for cable after some bearish developments earlier this month. The move below the topping formation neckline, around 1.26, appeared to be quite bearish, as did the following rebound off a key Fib level after rebounding this week, but it’s lost some momentum already before reaching the February lows.

NZD: The Week Ahead

Commerzbank's analysis suggests a brighter outlook for the New Zealand Dollar (NZD) in the coming months despite recent downward pressure. Factors like broader U.S. Dollar strength and domestic issues have kept the NZD below last year's highs. However, robust labor markets in both New Zealand and Australia and an expected stabilization of Chinese economic growth offer reasons for optimism. While economic growth in New Zealand is projected to stabilize slowly, persistent inflation prompts cautious actions from the Reserve Bank of New Zealand (RBNZ). Despite challenges, Commerzbank anticipates a moderate appreciation of the NZD due to the relatively hawkish stance of its central bank compared to other G10 counterparts.

GBPNZD - H4 Timeframe

The 4-hour timeframe chart of GBPNZD as attached above shows price currently retesting the 88% region of the Fibonacci retracement tool. This, combined with the trendline support, and 200-period moving average, indicates the likelihood of price to bounce off the current region to approach the 23% of the Fibonacci retracement as a target level.

Analyst’s Expectations:

- Direction: Bullish

- Target: 2.07402

- Invalidation: 2.04964

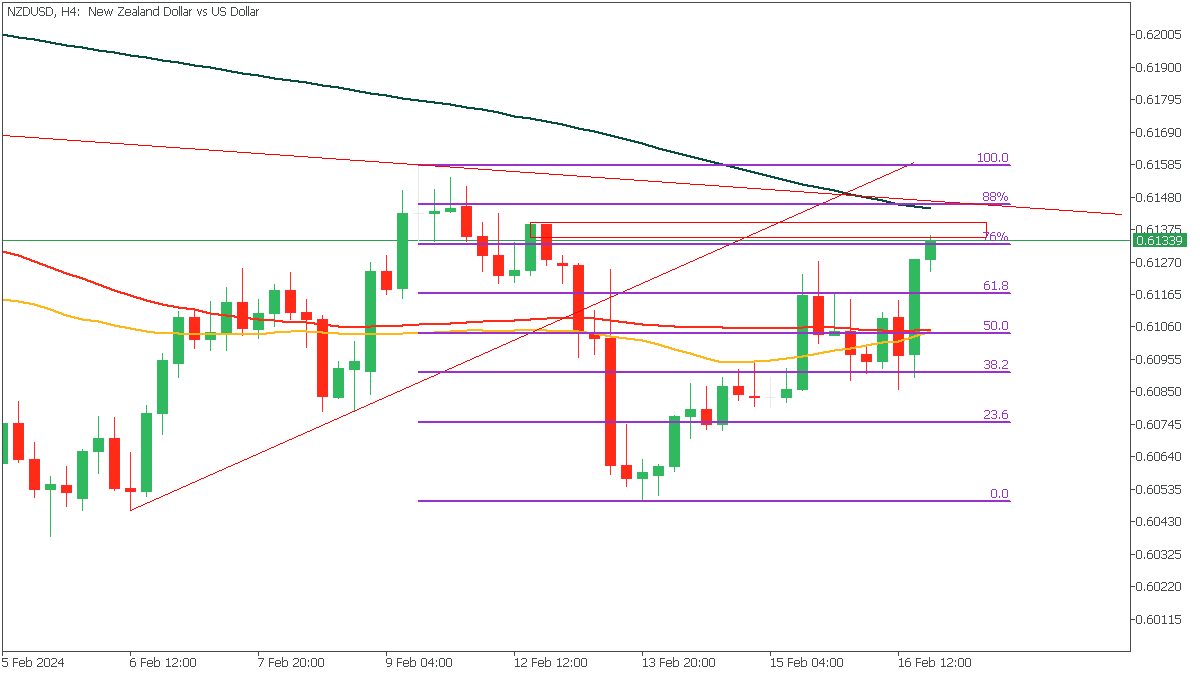

NZDUSD - H4 Timeframe

NZDUSD is currently trading between 76% and 88% of the Fibonacci retracement after having broken structure and trendline support. This means that the current price action is likely to reverse once price retests the trendline. Other confirmations include the confluence of two resistance trendlines, the 200-period moving average resistance, the Fibonacci retracement levels, and also, the supply zone.

Analyst’s Expectations:

- Direction: Bearish

- Target: 0.60761

- Invalidation: 0.61595

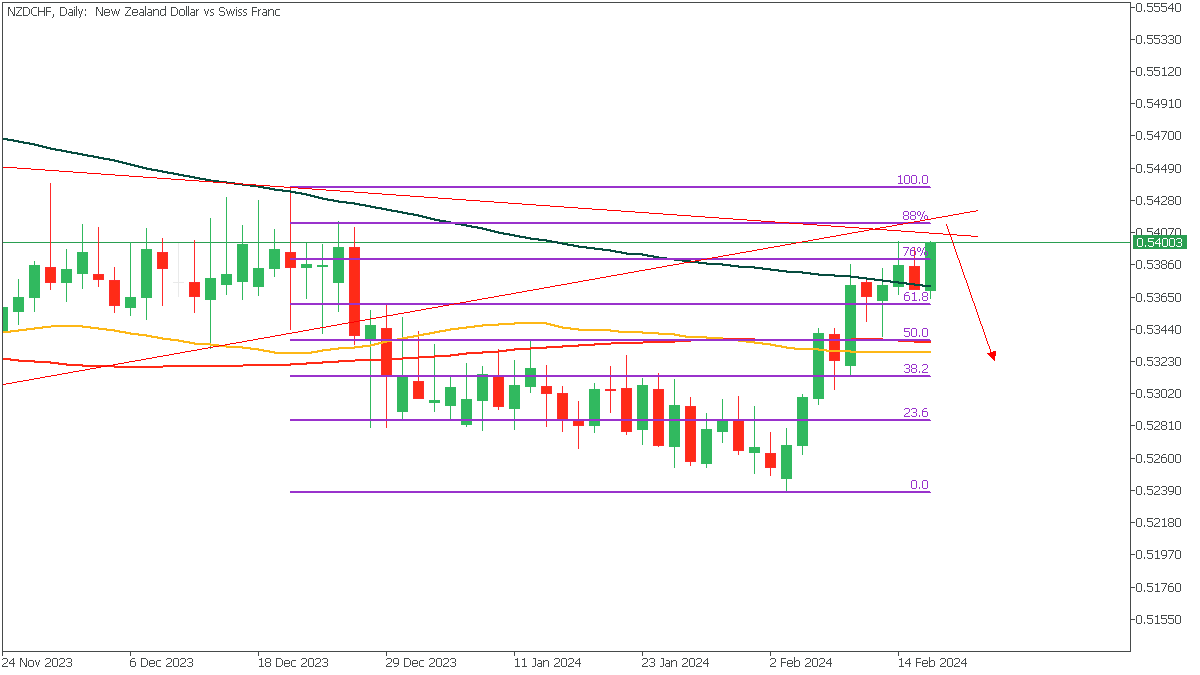

NZDCHF - D1 Timeframe

The price action on the daily timeframe of NZDCHF is very akin to what we saw earlier on the 4-hour timeframe of NZDUSD. Here, we see a similar break of structure and trendline support, with price currently making a move to retest these resistance trendlines, as well as the supply zone and the Fibonacci retracement levels. I expect to see a rejection from the supply zone.

Analyst’s Expectations:

- Direction: Bearish

- Target: 0.52863

- Invalidation: 0.54377

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

Weekly Economic & Financial Commentary: Central Banks on Hold for Longer?

Summary

United States: Little Love in January Data

- Economic data were stuck in the doldrums this week, highlighted by a hot January CPI print. The out-of-consensus start to the year for economic data continued with a slip in retail sales and industrial production followed by a startling 14.8% drop in housing starts during January.

- Next week: LEI (Tue.), Existing Home Sales (Thu.)

International: International Data Deliver Downside Surprises

- This week in international data, U.K. Q4 GDP fell 0.3% quarter-over-quarter, and January inflation was slower than forecasted, holding steady at 4.0%. Japan's GDP was also weak, reporting an unexpected decline. Australia's January labor market report was disappointing, with employment virtually unchanged, while the jobless rate rose more than forecast to 4.1%.

- Next week: Canada CPI (Tue.), Eurozone PMIs (Thu.)

Interest Rate Watch: Central Banks on Hold for Longer?

- We explain why we think the FOMC is still on pace to cut rates by 25 bps at its May 1 meeting despite this week's higher-than-expected print on CPI inflation in January. We look for the European Central Bank to reduce its policy rate by 25 bps on April 11. That said, we readily acknowledge that both central banks could wait longer to ease policy than we currently anticipate.

Credit Market Insights: Housing Affordability Update

- The affordability of the U.S. housing market continues to be bifurcated across prospective and existing homeowners as the differential between rates for new mortgages and the average existing mortgage widens. Purchase affordability has reached its lowest level in close to 40 years. Meantime, existing homeowners have yet to directly feel the pinch of higher mortgage rates.

Topic of the Week: Slow to Find Shelter from Inflation

- The strengthening in January's CPI for owners' equivalent rent (OER) stood in contrast to leading measures of shelter inflation and moderation in rent of primary residences (RPR). We expect to see some payback next month, but January's gap between OER and RPR growth hints at a firmer path for OER ahead as the single-family rental market remains tight amid low purchase affordability.

Week Ahead – Fed Minutes Headline a Data-Heavy Week

- Dollar shines after inflation surprise, awaits latest Fed minutes

- In Europe, business surveys will be crucial for euro and sterling

- Canadian and Australian data releases also on the agenda

Fired up dollar turns to FOMC minutes

It was a beneficial week for the US dollar, which charged higher after data revealed US inflation is not cooling down as quickly as investors had hoped. Traders were forced to unwind bets of imminent Fed rate cuts in the aftermath, lending the dollar strength through the interest rate channel.

Solid economic growth, a tight labor market, and persistently high inflation are a cocktail that makes it very difficult for the Fed to cut interest rates. Markets have finally gotten the message. The timing of the first rate cut has been pushed out to June, while the market is now pricing in less than four cuts in total for 2024, down from six earlier.

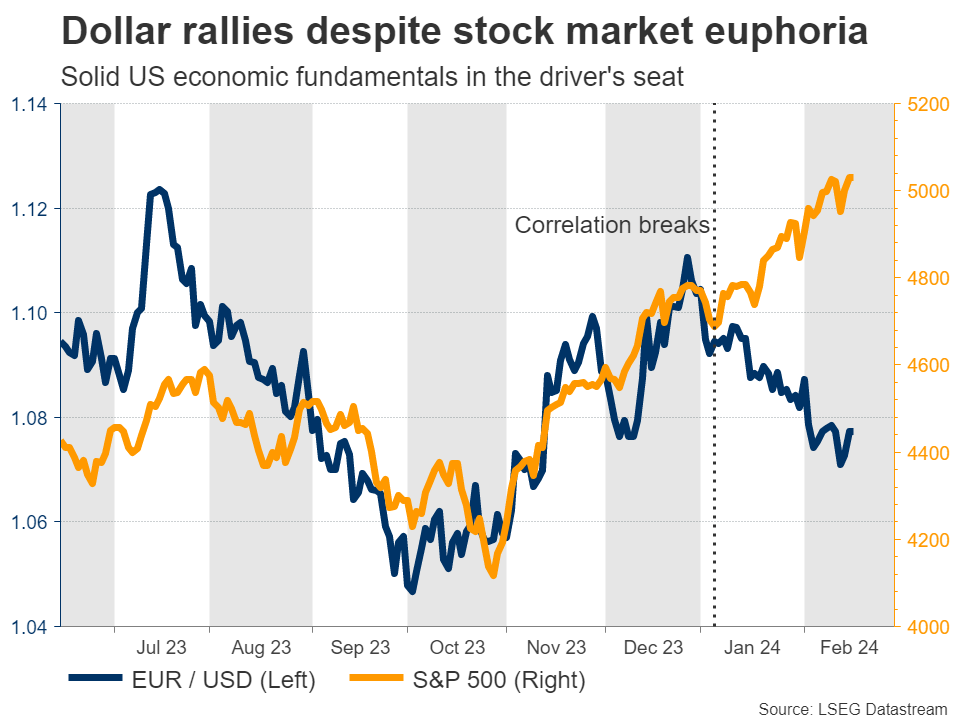

With rate cuts getting priced out, the dollar has started to shine once again, gaining 3% already this year against a basket of currencies. It’s crucial to note that this is happening even despite the euphoria in the stock market. Positive risk sentiment is generally bad news for the dollar, which is considered a safe haven asset.

This makes the dollar’s recent rally even more impressive. The reserve currency has started to realign itself with its robust economic fundamentals, and this process might have scope to continue since the market is still pricing in four rate cuts for this year, whereas the Fed has only signaled three.

Minutes of the latest Fed meeting will be released on Wednesday and will be the next piece in this puzzle. Investors will search for any clues on the potential timing of the first rate cut. We’ve heard from several Fed officials since this meeting, and most have preached patience on rates, warning against premature cuts given the strength of the US economy.

If the minutes echo a similar tone, the dollar could gain more momentum.

Eurozone and UK business surveys on tap

Crossing into Europe, the latest round of PMI business surveys will be released on Thursday in both the Eurozone and the United Kingdom. Both economies have been haunted by stagnant growth for some time now, with the UK even falling into a technical recession late last year.

Investors will dissect these business surveys for signals on whether the situation is improving or worsening in order to gain insights on how quickly these central banks might cut interest rates. Since UK inflation is still very hot, markets think the Bank of England will be among the last central banks to cut in this cycle.

This notion has helped support the British pound, which is currently the second-best performing major currency this year, behind the US dollar. The cheerful tone in global markets played a role too, as the pound is highly correlated with stock market performance, thanks to the UK’s twin deficits.

Of course, this is a dynamic that cuts both ways. If stock markets suffer a correction or if UK data continues to deteriorate, the pound would be left vulnerable to a selloff, especially with political uncertainty brewing ahead of a general election.

As for the Eurozone, even though it narrowly dodged a recession, the outlook is equally grim. New business orders have declined for seven months in a row, which is bad news for future growth. If the upcoming surveys show that this trend persists, the euro could receive another blow as traders become more confident the ECB will cut rates in April.

The minutes of the latest ECB meeting will also be published on Thursday, although this release usually does not have a significant market impact.

Canadian and Australian releases

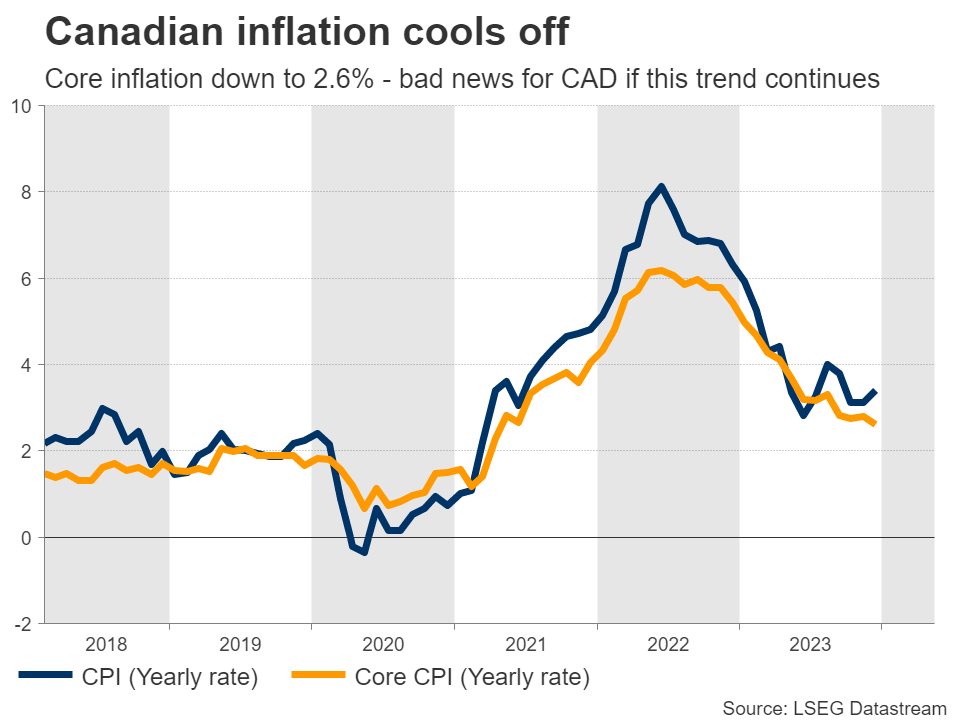

Turning to the commodity-linked currencies, the ball will get rolling on Tuesday with Canada’s inflation stats for January. Inflation has cooled dramatically in recent months, with the core CPI rate falling to just 2.6% in December, leading the Bank of Canada to abandon its tightening bias.

Another cooldown in inflation could raise the likelihood of a rate cut in the spring, keeping the Canadian dollar under pressure. The nation’s retail sales for December will also be released on Thursday.

Finally in Australia, minutes from the latest RBA meeting will see the light on Tuesday, ahead of wage growth data for Q4 on Wednesday.

Canadian Inflation in January Likely Eased as BoC Contemplates Interest Rate Cut Timing

The first Canadian inflation reading of 2024 out next Tuesday should edge lower on falling energy prices and slower food price growth.

We expect the consumer price index to rise 3.2% year-over-year, lower than 3.4% in December. But the underlying details will be closely watched for signs on whether inflation pressures are continuing to trend— albeit gradually—towards the Bank of Canada’s 2% target. Most of the deceleration we expect in price growth comes from lower energy prices, which the central bank has little to no control over. Gasoline prices were little changed from December to January and residential natural gas prices fell in Alberta. Food price growth also looks likely to ease as a large month-over-month surge in January 2023 (+1.7%) falls outside of the year-over-year growth rate.

Stripping out volatile components like food and energy, we expect price growth to hold at 3.4% year-over-year with the recent months’ mixed underlying drivers continuing. More than a quarter of price growth overall is still coming from higher mortgage interest costs that are a direct result of earlier BoC interest rate increases. If we exclude that component, price growth would already be back within the BoC’s 1% to 3% inflation target range.

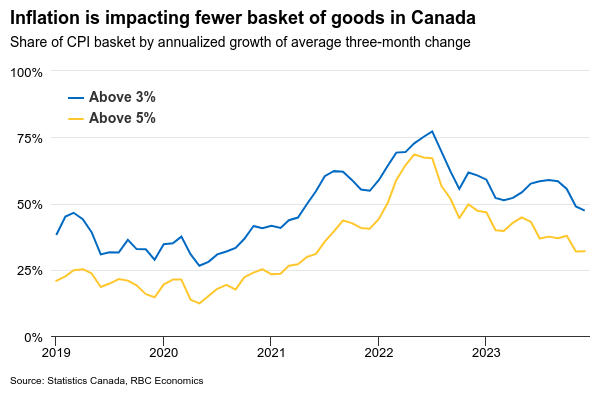

The share of the CPI basket seeing abnormally high inflation has also been declining. Roughly 51% of the consumer basket was growing at more than 3% over the last three months, down from a peak of 77% of the basket in July 2022. But we also look for year-over-year growth in the BoC’s preferred broader trim and median measures of underlying price growth to hold steady at 3.7% and 3.6%, respectively, in December.

Substantially stronger-than-expected January labour market data and a bounce back in home resales have raised fears that the Bank of Canada will need to leave interest rates higher for longer (again) to get inflation sustainably back to target. But, consumer demand has continued to soften on a per-capita basis.

We expect December retail sales data on Thursday to show an increase close to the 0.8% advance estimate from Statistics Canada a month ago, but that likely implies lower spending outside of a monthly jump in vehicle sales and higher gasoline prices. Our tracking of spending in January has been softer.

Weekly Focus – Data Dampens Rate Cut Expectations

The overall theme for markets this week continued to be the scaling back of expectations of rate cuts especially in the US as the economy looks stronger, and inflation higher, than expected. However, the change should not be exaggerated. Inflation expectations are well in line with targets and indicators for banking activity in both the US and Europe confirm that the current stance of monetary policy is having a dampening effect on economies.

The latest significant upside surprise to US data was the January CPI. The core price index rose 0.4% m/m, so clearly more than what is compatible with 2% annual inflation. The increase was driven by a broad-based increase in service prices. The so-called "super core" index of services excluding shelter rose 0.85% m/m. This likely reflected higher than normal January price adjustments to make up for past cost increases in businesses and so is not likely to be repeated to the same extent in coming months, but nevertheless feeds into concerns in the Fed and elsewhere that a tight labour market and high wage growth could make it difficult to get service inflation down far enough.

On the negative side, US retail sales declined 0.8% in January and were revised down for December, and industrial production declined 0.5%. Especially retail sales is a highly volatile data series though, and these numbers do not really change the view on the US economy.

In Europe, the economic news has been slightly more positive this week. Employment growth in the euro area actually accelerated in Q4 to 0.3% q/q. The labour market usually reacts with a lack to the economy, so it is perhaps not surprising that the stagnating European economy has not yet produced a decline in jobs, but accelerating outright growth in employment is harder to explain. Surveys continue to show a large, unmet demand for labour among euro area companies. The strong labour market reduces pressure on the ECB to cut rates and adds to concerns about a potential rebound in inflation from high wage growth. The German ZEW index showed a new increase in business expectations in February consistent with the view of a more positive global situation for manufacturing, although assessment of current conditions actually worsened.

Unlike in the US, UK inflation was lower than expected in January, which helped dampen market worries globally. Core CPI increased just 0.16% m/m seasonally adjusted, and service prices dragged down. On the other hand, wage growth declined less than expected in December and stands at 6.2% y/y, while the unemployment rate declined from 4.0% to 3.8%. With core inflation still as high as 5.1% y/y, we still expect the Bank of England to be cautious in cutting rates.

Next week, on Thursday, we will get February PMI data for most major economies. They could show a renewed strengthening in global manufacturing. Regional PMIs published this week in the US point in that direction, as does indicators from several Asian countries that are normally leading in the manufacturing cycle. However, PMIs might also point to continued weakness in services which at least in the euro area seem to be stagnating or contracting, albeit with rising prices.

Sunset Market Commentary

Markets

This week’s market story was all about US price data which dashed investors hope on a May Fed policy rate cut. January CPI delivered the first and biggest blow on Tuesday by unexpectedly accelerating on a monthly basis and keeping Y/Y-equations more sticky than hoped (3.1% headline & 3.9% core) with a special mention to services and housing related costs. Less important, but again consensus-overtaking import and export prices yesterday neutralized an attempt by US Treasuries to rally on disappointing retail sales. Third time’s usually the charm, though not this time around. January producer prices accelerated by 0.3% M/M (headline) and 0.5% M/M (core) while consensus forecasted only 0.1% for both. The January price update (with only PCE deflators missing; Feb 29 release) highlights the bumpy path ahead, both for markets and for the Fed. The former now even doubt whether the Fed will be able to pull the trigger in June (80% probability)!! The data amplify overnight comments by Atlanta Fed governor Bostic who defended a view consisting of only two rate cuts this year with a first one only in July. US Treasuries sold off in the wake of PPI data with US yields currently rising by 6 bps (30-yr) to 9 bps (2-yr). The US 2-yr yield set a new YTD high at 4.72%. The US 10-yr yield tested the similar reference at 4.33% which also coincides with the 100 day moving average. The dollar profited from the interest rate support, but the move lacked technical relevance. EUR/USD is currently changing hands around 1.0750. ECB comments (see News & Views) failed to impact the pair. We don’t expect any additional follow-up technical action during today US trading session given the upcoming long week. US markets are closed on Monday for President’s day. EUR/GBP trades close to opening levels around 0.8550, with the UK currency failing to profit from strong UK retail sales. Following this week’s economic update, we believe that the EUR/GBP 0.85 support zone is once again stronger.

Next week’s eco calendar is far less enticing that this week’s jam-packed US agenda. On Tuesday, the ECB publishes an in-house, forward-looking, indicator of negotiated wage rates. The day after, the FOMC publishes Minutes of the January policy meeting. On Thursday, it’s the ECB’s turn with global PMI’s on the agenda as well. It’s next week’s main dish with EMU consumer inflation expectations rounding off on Friday.

News & Views

Mario Draghi said central banks should give European sovereigns the space to invest in the green transition and robust supply chains, adding governments need sufficiently low borrowing costs to finance the shift. The former ECB president made the comments in the context of being mandated by the European Commission to seek ways to revitalize the European economy in the face of increased Chinese and US competition. Draghi has never been shy of airing controversial proposals, including during his tenor as head of the ECB. This time around, his call could be seen as a contentious one because it would risk creating the perception of (some form of) monetary financing. The ECB currently keeps policy rates at an elevated level to fight inflation that’s still above target. Draghi said, however, that central banks should focus on keeping inflation expectations anchored and look through “temporary upward price shocks”.

ECB’s Schnabel again warned for caution against calling victory over inflation. Challenging French governor Villeroy’s quote this morning that “the last mile of taming prices is not harder by nature”, the German board member noted that Europe’s sluggish productivity growth may slow the fall in inflation to the 2% target. She explained that "Persistently low, and recently even negative, productivity growth exacerbates the effects that the current strong growth in nominal wages has on unit labour costs for firms" which may eventually get passed on to consumers. Factors behind this underperformance vs the US include lower investment in technology, more red tape and more expensive energy, she noted.