Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0737; (P) 1.0761; (R1) 1.0797; More...

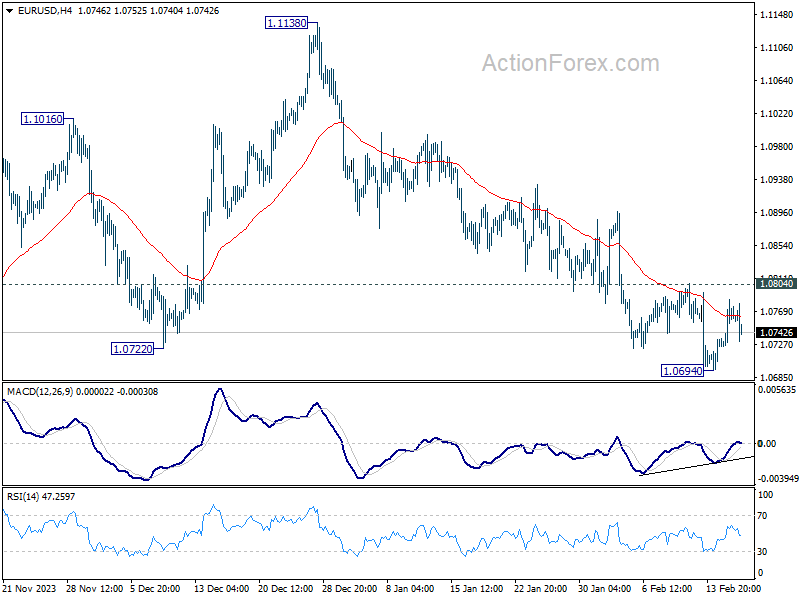

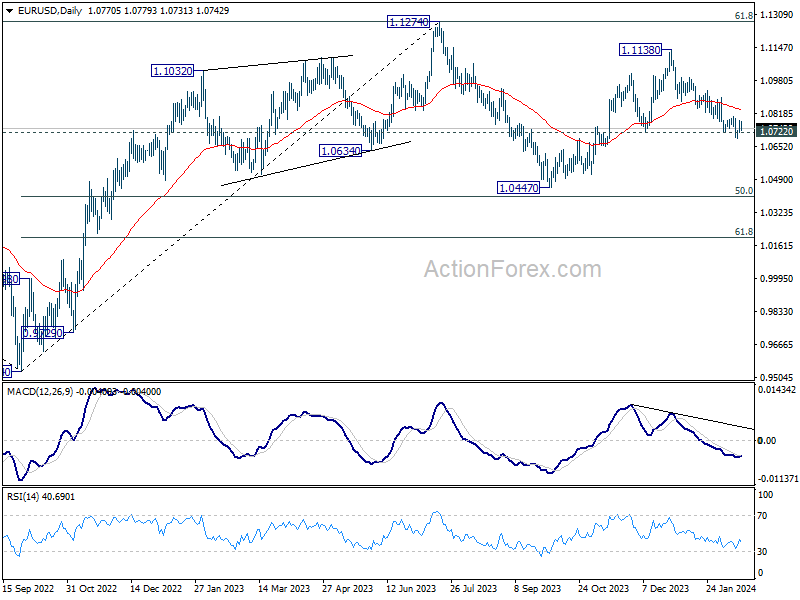

EUR/USD dips mildly in early US session as consolidation from 1.0694 extends. Intraday bias remains neutral and outlook stays bearish with 1.0804 resistance intact. Below 1.0694 will resume the fall from 1.1138 to retest 1.0447 support. Nevertheless, considering bullish convergence condition in 4H MACD, above 1.0804 will turn bias to the upside for stronger rebound.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

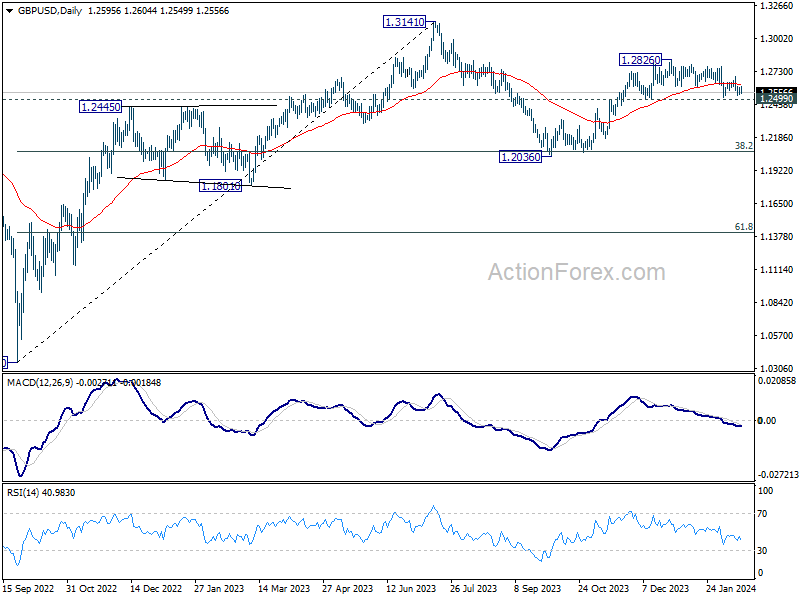

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2561; (P) 1.2581; (R1) 1.2621; More...

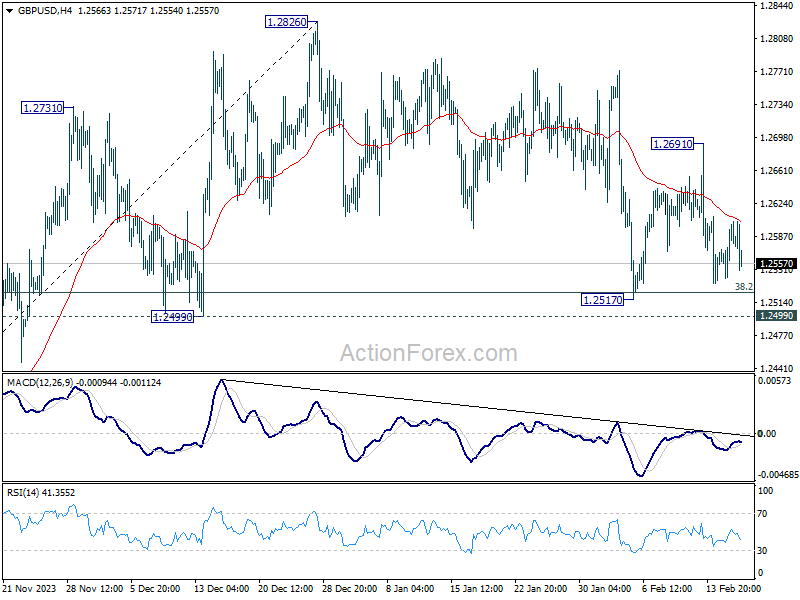

Range trading continues in GBP/USD and intraday bias stays neutral. On the upside, break of 1.2691 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

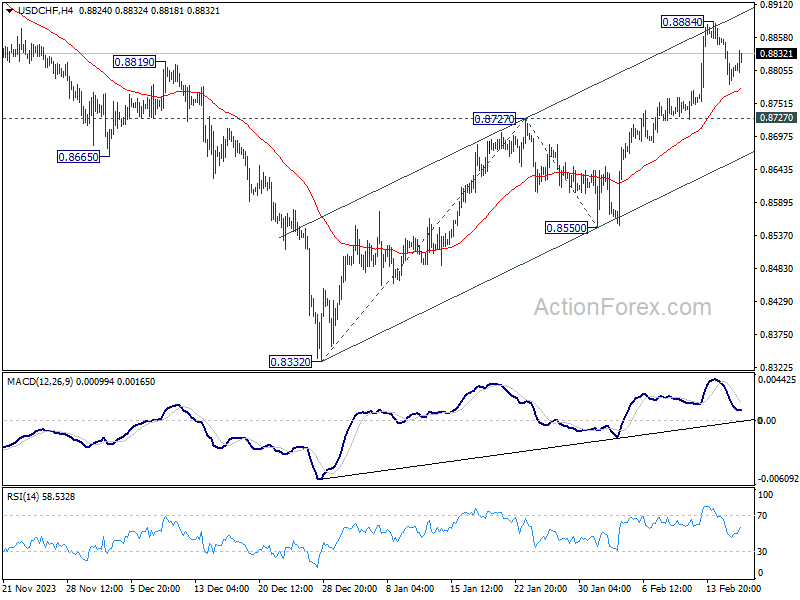

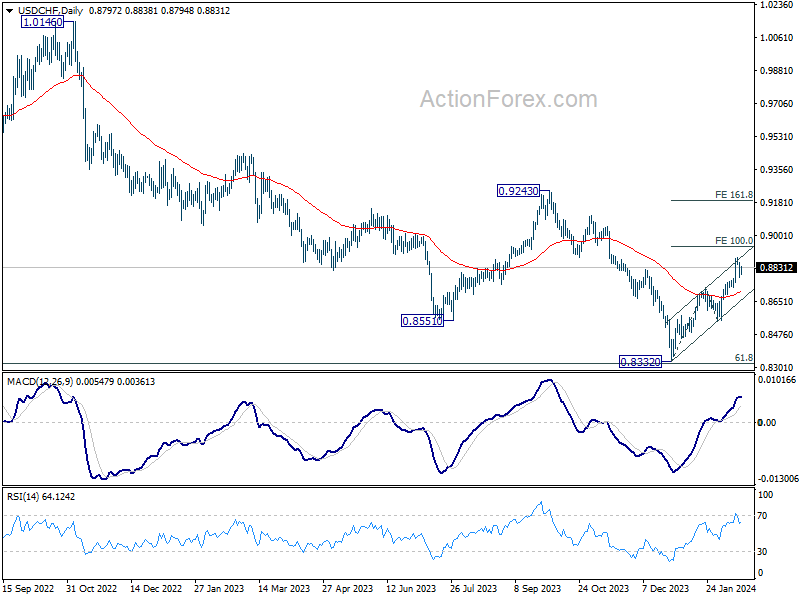

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8767; (P) 0.8816; (R1) 0.8850; More....

USD/CHF recovers mildly in early US session as consolidation from 0.8885 continues. Intraday bias remains neutral first. Downside of retreat should be contained by 0.8727 resistance turned support to bring another rally. On the upside, above 0.8884 will resume the rise from 0.8332 to 100% projection of 0.8332 to 0.8727 from 0.8550 at 0.8954. Firm break there will pave the way to 161.8% projection at 0.9189. However, sustained break of 0.8727 will dampen this bullish view, and turn bias back to the downside for 0.8550 support instead.

In the bigger picture, a medium term bottom should be formed at 0.8332, on bullish convergence condition in W MACD, just ahead of 0.8317 long term fibonacci support, on bullish convergence condition in W MACD. It's still early to decide if the larger down trend from 1.0146 (2022 high) is reversing. But further rise should be seen to 0.9243 resistance even as a correction.

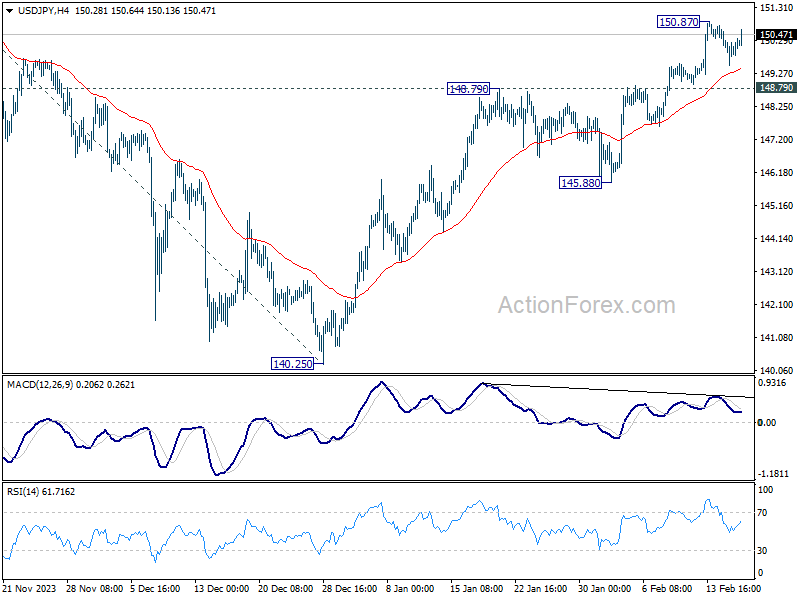

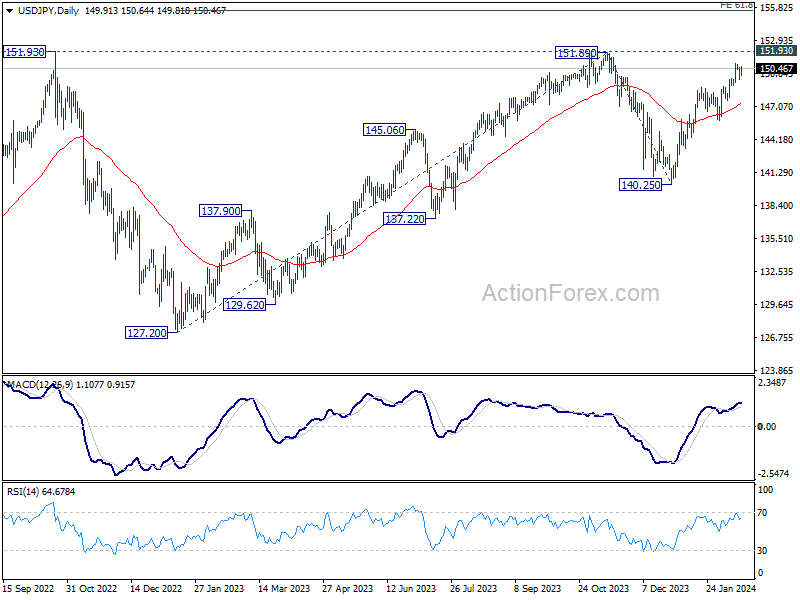

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.47; (P) 150.02; (R1) 150.50; More...

USD/JPY recovers in early US sessions but stays in range below 150.87. Intraday bias remains neutral and more consolidation would be seen. But in case of another retreat, downside should be contained by 148.79 resistance turned support to bring another rally. Above 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. However, firm break of 148.79 will turn bias to the downside for 145.88 support.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

Dollar Finds Footing on Strong PPI Data

Dollar stages a notable recovery in the early US session, buoyed by stronger than expected January PPI figures. The highlight was PPI excluding foods, energy, and trade services, which saw its largest monthly increase in a year, hinting at persistent underlying inflationary pressures upstream. Despite the current rebound rebound, Dollar has yet to surpass the highs against major currencies seen earlier this week. Nevertheless, the current development at least indicates that the selloff triggered by the previous day's retail sales data should have run its course.

Also, Dollar's resurgence should be able to cement its position as the top performer for the week. Canadian and Australian Dollars are trailing behind in strength. Meanwhile, Swiss Franc, Japanese Yen, and New Zealand Dollar languish at the lower end of the performance spectrum, with the Euro and Sterling showing mixed results. The Pound, despite an initial surge from unexpectedly robust retail sales figures earlier today, saw its momentum wane swiftly.

In Europe, at the time of writing, FTSE is up 1.30%. DAX is up 0.46%. CAC is up 0.33%. UK 10-year yield is up 0.0644 at 4.122. Germany 10-year yield is up 0.049 at 2.414. Earlier in Asian, Nikkei rose 0.86%. Hong Kong HSI rose 2.48%. Singapore Strait Times rose 1.42%. Japan 10-year yield fell -0.0001 to 0.730.

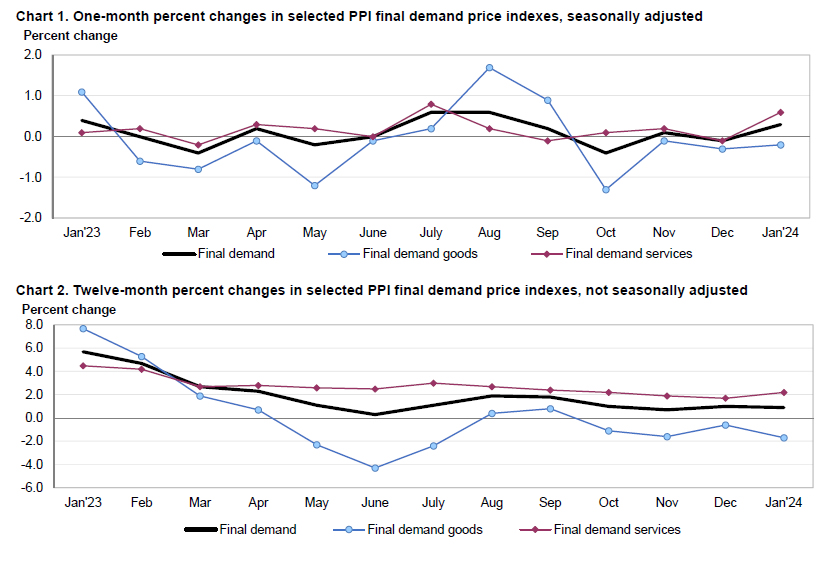

US PPI up 0.3% mom, 0.9% yoy in Jan

US PPI rose 0.3% mom in January above expectation of 0.1% mom. PPI goods declined -0.2% mom while PPI services rose 0.6% mom. PPI less foods, energy, and trade services rose 0.6% mom, the largest advance since January 2023.

For the 12-month period, PPI slowed from 1.0% yoy to 0.9% yoy, above expectation of 0.7% yoy. PPI less foods, energy, and trade services was unchanged at 2.6% yoy.

ECB's Schnabel warns of premature policy ease amid wage-driven inflation pressures

In a speech today, ECB Executive Board member Isabel Schnabel noted the role of "persistently low, and recently even negative, productivity growth" in exacerbating the inflationary pressures from the current strong growth in nominal wages.

She pointed out that this scenario increases the likelihood of firms passing higher wage costs onto consumers, thus "delaying inflation returning to our 2% target."

With the backdrop of a prolonged period of high inflation, Schnabel argued for the necessity of maintaining restrictive monetary policy stance until there is clear confidence that inflation will sustainably return to ECB's medium-term objective.

She warned against premature policy adjustments, suggesting that to avoid a "stop-and-go policy" reminiscent of the 1970s, a cautious approach is essential.

"We must be cautious not to adjust our policy stance prematurely," she said.

UK retail sales rises 3.4.% mom in Jan, largest since April 2021

UK retail sales volume rose 3.4% mom in January, well above expectation of 1.5% mom. That was the largest monthly rise since April 2021, reversing the deep decline of -3.3% mom in December.

Sales volumes in all subsectors except clothing stores increased over the month, with food stores such as supermarkets contributing most to the increase.

Sales value rose 3.9% mom, largest rise since January 2021. Sales volume rose 0.7%

RBNZ's Orr stresses continued effort needed to anchor inflation expectations

In a forum today, RBNZ Governor Adrian Orr indicated that the central bank's primary challenge lies in firmly anchoring inflation expectations around the 2% target, a goal that remains elusive despite significant progress.

This "tail end" of the inflation fight, as Orr describes, requires meticulous attention to both "capacity pressures" within the economy and the public's "inflation expectation"s.

"We've got more work to do to have inflation expectations truly anchored at that 2% level, he added.

"We observe headline but we are targeting in a large sense core inflation," Orr stated, emphasizing the importance of these metrics in shaping the central bank's policy decisions.

NZ BNZ manufacturing rises to 47.3, still someway off to expansion

New Zealand BusinessNZ Performance of Manufacturing Index rose from 43.4 to 47.3 in January, hitting the highest level since June last year. Despite this uptick, it's important to note that the manufacturing sector remained in contraction for eleven straight months.

BusinessNZ's Director of Advocacy, Catherine Beard noted that while there are signs of improvement, "the sector is still someway off returning to expansion."

Looking at some details, production rose from 40.5 to 42.1. Employment rose from 47.0 to 51.3. New orders rose from 44.0 to 47.7. Finished stocks rose from 45.9 to 47.3. Deliveries rose from 43.7 to 49.3.

However, the persistence of negative sentiment among businesses cannot be overlooked. The proportion of negative comments in January rose to 63.2%, up from 61% in December and 58.7% in November, reflecting concerns over seasonal factors such as holiday disruptions and a sustained lack of demand or orders.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.47; (P) 150.02; (R1) 150.50; More...

USD/JPY recovers in early US sessions but stays in range below 150.87. Intraday bias remains neutral and more consolidation would be seen. But in case of another retreat, downside should be contained by 148.79 resistance turned support to bring another rally. Above 150.87 will resume the rise from 140.25 to 151.89/93 key resistance zone. Decisive break there will confirm larger up trend resumption of 155.50 projection level next. However, firm break of 148.79 will turn bias to the downside for 145.88 support.

In the bigger picture, fall from 151.89 is seen as a correction to the rally from 127.20, which might have completed at 140.25 already. Firm break of 151.89/93 resistance zone will confirm up trend resumption, and next target will be 61.8% projection of 127.20 to 151.89 from 140.25 at 155.50. This will now remain the favored case as long as 140.25 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Jan | 47.3 | 43.1 | 43.4 | |

| 04:30 | JPY | Tertiary Industry Index M/M Dec | 0.70% | 0.20% | -0.70% | -1.40% |

| 07:00 | GBP | Retail Sales M/M Jan | 3.40% | 1.50% | -3.20% | -3.30% |

| 13:30 | CAD | Wholesale Sales M/M Dec | 0.30% | 0.70% | 0.90% | |

| 13:30 | USD | Building Permits Jan | 1.47M | 1.52M | 1.49M | |

| 13:30 | USD | Housing Starts Jan | 1.33M | 1.47M | 1.46M | |

| 13:30 | USD | PPI M/M Jan | 0.30% | 0.10% | -0.10% | |

| 13:30 | USD | PPI Y/Y Jan | 0.90% | 0.70% | 1.00% | |

| 13:30 | USD | PPI Core M/M Jan | 0.50% | 0.10% | 0.00% | -0.10% |

| 13:30 | USD | PPI Core Y/Y Jan | 2.00% | 1.70% | 1.80% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Feb P | 80 | 79 |

RBNZ’s Orr – Inflation Expectations Still Too High

The New Zealand dollar is drifting on Friday. In the European session, NZD/USD is trading at 0.6110, up 0.08%.

Orr pushes back against rate cut expectations

The Reserve Bank of New Zealand has made inflation its top priority and the Bank’s steep rate-hiking cycle has brought inflation lower. Still, at the current clip of 4.7%, inflation is more than double the 2% midpoint of the target band of one to three percent. Earlier this week, New Zealand released inflation expectations, which eased to 2.5% in the first quarter, down from 2.7% in Q4 2023 and lower than the forecast of 2.6%. This was the lowest level since Q3 2021.

If anyone thought that the drop in inflation expectations might prod the RBNZ to be more dovish, they were no doubt disappointed. Governor Adrian Orr responded to the release by saying that inflation is moving in the right direction but there is “more work to do to have inflation expectations truly anchored at that 2% level”. In other words, there has been good progress but the battle with inflation continues.

The RBNZ has paused rates at 5.5% for four straight times and the markets have priced in a rate cut May. The central bank has pushed back against these expectations and Orr’s comments about inflation expectations was the latest instance of the central bank pouring cold water on rate-cut expectations.

At the last meeting in late November, the RBZN said that a rate hike could not be ruled out and projected that there would not be any rate cuts before mid-2025. The RBNZ remains in a hawkish mood and is unlikely to consider rate cuts anytime soon.

NZD/USD Technical

- NZD/USD is putting pressure on resistance at 0.6116. Above, there is resistance at 0.6193

- 0.6072 and 0.5995 are providing support

US PPI up 0.3% mom, 0.9% yoy in Jan

US PPI rose 0.3% mom in January above expectation of 0.1% mom. PPI goods declined -0.2% mom while PPI services rose 0.6% mom. PPI less foods, energy, and trade services rose 0.6% mom, the largest advance since January 2023.

For the 12-month period, PPI slowed from 1.0% yoy to 0.9% yoy, above expectation of 0.7% yoy. PPI less foods, energy, and trade services was unchanged at 2.6% yoy.

ECB’s Schnabel warns of premature policy ease amid wage-driven inflation pressures

In a speech today, ECB Executive Board member Isabel Schnabel noted the role of "persistently low, and recently even negative, productivity growth" in exacerbating the inflationary pressures from the current strong growth in nominal wages.

She pointed out that this scenario increases the likelihood of firms passing higher wage costs onto consumers, thus "delaying inflation returning to our 2% target."

With the backdrop of a prolonged period of high inflation, Schnabel argued for the necessity of maintaining restrictive monetary policy stance until there is clear confidence that inflation will sustainably return to ECB's medium-term objective.

She warned against premature policy adjustments, suggesting that to avoid a "stop-and-go policy" reminiscent of the 1970s, a cautious approach is essential.

"We must be cautious not to adjust our policy stance prematurely," she said.

GBP/USD Yawns as UK Retail Sales Soar

The British pound has edged lower on Friday. In the European session, GBP/USD is trading at 1.2578, down 0.17%.

UK retail sales rebound with 3.4% gain

UK retail sales were more than impressive, surging 3.4% m/m in January. This crushed the market estimate of 1.5% and followed a 3.3% decline in December. The reading was the largest monthly gain since April 2021. The sharp gain was driven by increased sales of food and fuel. On an annualized basis, retail sales rebounded with a 0.7% gain, compared to a 2.4% decline in December and well above the market estimate of -1.4%.

Will the real UK economy please stand up?

Traders can be forgiven for scratching their head after the latest retail sales report, which points to consumers spending with gusto. Just a day earlier, the markets were digesting the news that the UK economy had entered a recession late in 2024, after recording back-to-back quarters of negative growth. GDP fell 0.3% in the fourth quarter and 0.1% in the third quarter. What gives?

The answer could well be that the UK economy, although hurting, may be turning a corner. The sharp rise in interest rates has cooled down the economy and lowered inflation dramatically, but this effect appears to be fading fast. The “R” word (recession) may be making headlines but it is a shallow recession and the economy could quickly return to growth mode with some decent economic data.

The Bank of England meets on March 21th and will try to make sense of where the UK economy is headed. The BoE has kept rates unchanged since August and there is pressure on the central bank to provide some relief to households and businesses and lower rates. At the same time, inflation remains sticky and the BoE is determined to stamp out high inflation and bring it closer to the 2% target before it lowers rates.

GBP/USD Technical

- GBP/USD is testing support at 1.2597. Below, there is support at 1.2550

- There is resistance at 1.2676 and 1.2723

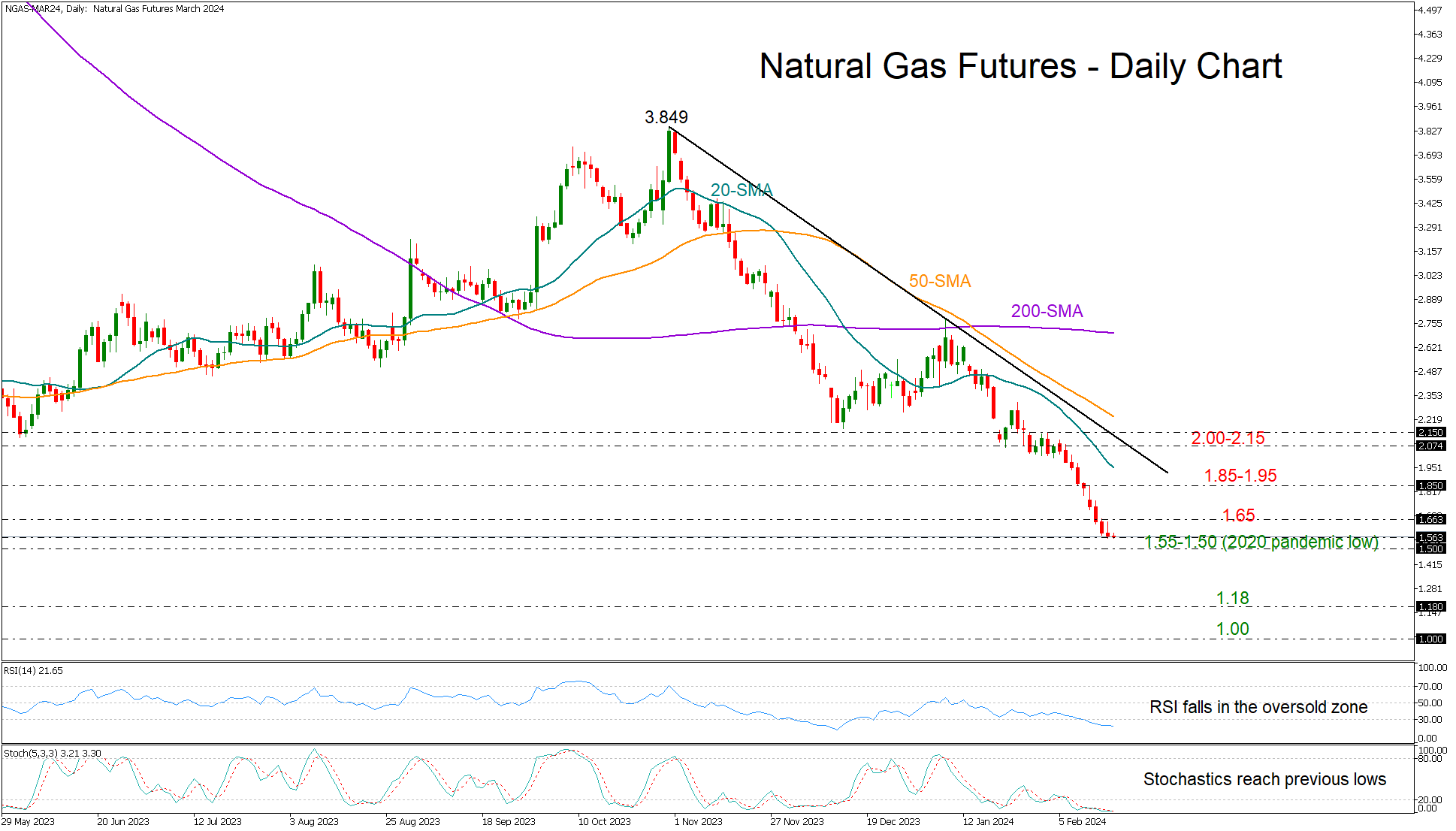

Natural Gas Dives to Pandemic Lows; Near-Term Oversold

- Natural gas futures reach pandemic lows

- Oversold signals present; confirmation above 1.65

Natural gas futures (March delivery) experienced another painful week, plummeting towards the pandemic floor of 1.50, which halted the 2014-2016 downtrend too.

The RSI and the stochastics have detected oversold conditions, while Thursday’s candlestick, which seems to have the shape of an inverse hammer, is adding to the optimism that the price could soon change direction to the upside.

Yet, a clear extension below the 1.50 threshold could cancel this bullish scenario, activating a new bearish wave towards the 1.18 level, which coincides with the 261.8% Fibonacci extension of the December-January upleg. Failure to pivot there could bring the case of parity under the spotlight.

Should selling forces fade out, the price may reverse up to test the nearby resistance zone of 1.65. A break higher would validate the bullish hammer candlestick pattern, bolstering buying appetite towards the 1.85 territory. A steeper increase above the 20-day simple moving average (SMA) and the 2.00 round level might provide direct access to the tentative resistance trendline from November’s high at 2.07. However, buyers may not gain confidence unless the recovery continues sustainably above the 2023 constraining region, around 2.16.

In short, natural gas futures have been sold aggressively, reaching attractive levels for a bullish reversal. For that to happen, though, the price will have to set a strong foothold within the 1.50 area.