Sample Category Title

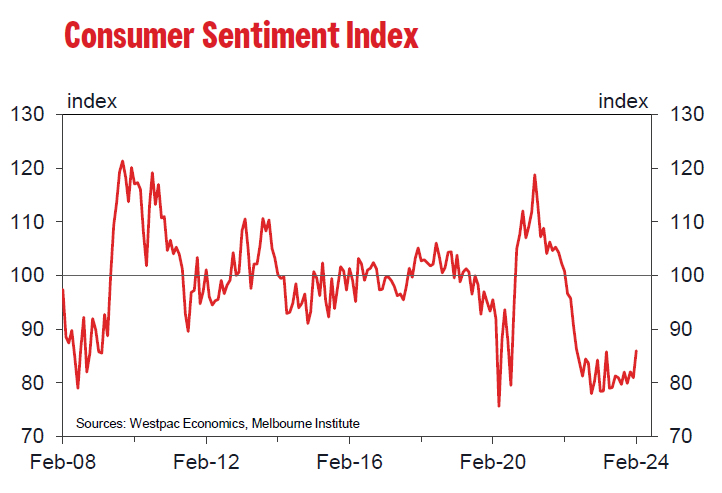

Australian Westpac consumer sentiment hits 20-Month high, but still pessimistic

Australia Westpac Consumer Sentiment Index surged by 6.2% mom to 86 in February, marking the highest level since June 2022. This increase also represents the largest monthly gain since April of the previous year, which conincided with a period when RBA temporarily halted its tightening cycle.

According to Westpac, the surge in consumer sentiment was notably propelled by improved sentiment towards major purchases, which climbed 11.3% to 86.8, and more optimistic outlook for the economy over the next year, rising 8.8% to 88.9—the highest since May 2022. Additionally, five-year economic outlook rose 4.4% to 93.

The cooling inflation and more favorable perspective on interest rates are believed to be the primary factors behind this uplift. However, despite the recent gains, consumer mood remains in the pessimistic territory.

A notable "sharp turnaround" in sentiment was observed following RBA's decision in February to maintain the cash rate steady, with sentiment dropping from 94.1 to just 80 post-meeting. While the decision to keep rates unchanged aligned with general expectations, the decline in sentiment suggests consumers were anticipating a "clearer indication" that interest rates might begin to decrease.

Looking forward, Westpac anticipates the RBA will maintain the current interest rate in March, contingent on inflation continuing to align with expectations.

RBA’s Kohler points to slightly faster than expected inflation decline

Marion Kohler, RBA's Head of Economic Analysis, noted in a speech that inflation is "still high" but acknowledged a welcome trend: it's decreasing "at a slightly faster rate" than what RBA had forecasted three months prior.

Looking ahead, RBA's expectation is for inflation to settle back into its 2-3% target range by 2025 and reach the midpoint by the following year. However, Kohler underscored the "substantial uncertainty" surrounding these long-term predictions.

A notable aspect of Australia's inflation dynamics, as Kohler pointed out, is the "divergence in the path of core goods and services price inflation."

The primary driver behind the recent dip in inflation rates is the decrease in goods price inflation, whereas services price inflation remains "high and broadly based." This sector's inflation is predicted to "only gradually" diminish as a more equitable demand-supply relationship is established and domestic cost pressures begin to ease.

Kohler also touched on labor costs, particularly significant in the labor-intensive services sector, as a crucial factor influencing the pricing strategies of businesses. RBA believes wage growth is "around its peak" and anticipates a gradual reduction in line with improvements in the labor market. Signs of "easing wage pressures" are already evident in specific industries, notably within business services.

ECB’s Cipollone: No further economic slack necessary

In a speech overnight, ECB Executive Board member Piero Cipollone suggested that additional tightening of monetary policy may not be necessary to rein in inflation. His remarks hint at a potentially less restrictive approach going forward, should inflationary pressures continue to subside.

Cipollone emphasized that the current economic conditions, "with demand still weak and inflation expectations anchored", arguing against the need for monetary policy to "generate further slack to keep inflation in check". This perspective underlines a significant shift from aggressive tightening to a more measured stance, possibly preparing the ground for a more accommodative monetary policy in the near future.

Unwinding of supply shocks offers room for demand to pick up "without fuelling inflation". Additionally, the downturn in energy prices could allow for "some wage catch-up, especially if profits normalize."

However, Cipollone also stressed the importance of a balanced approach to policy-making, pointing out that the path to the ECB's inflation target would depend on a complex interplay of economic factors. Consequently, he advocated for a "data-driven" approach to future monetary-policy decisions.

GBP/JPY – Testing Highs Ahead of Key UK Economic Data

- UK wage growth key to BoE sustainably hitting inflation target

- GBPJPY struggling near recent highs

- Divergence points to loss of momentum

The coming days offer several important data points for the UK that could help determine when the Bank of England starts cutting interest rates and, by extension, where the currency is headed in the coming months.

The jobs report on Tuesday is always widely followed but with the unemployment component less reliable than normal, it’s the average earnings that will matter most.

At 6.5% in November, it’s currently running far too high to enable inflation to fall to 2% on a sustainable basis and the BoE will be hoping that it will subside considerably in the coming months, as is expected to have started in December.

A double top at the November and January highs?

The pound has performed very well against the yen recently, as many currencies have, recouping all of December’s losses to surpass the November peak.

GBPJPY Daily

Source – OANDA

It is continuing to struggle near 189 where it has repeatedly now run into resistance. And on this occasion, it’s done so on much weaker momentum, with there being a notable divergence between the stochastic and MACD, and price.

This could potentially set up a double top in the short term, with the neckline falling at the 1 February low – around 185.23 – a break of which would be a bearish development.

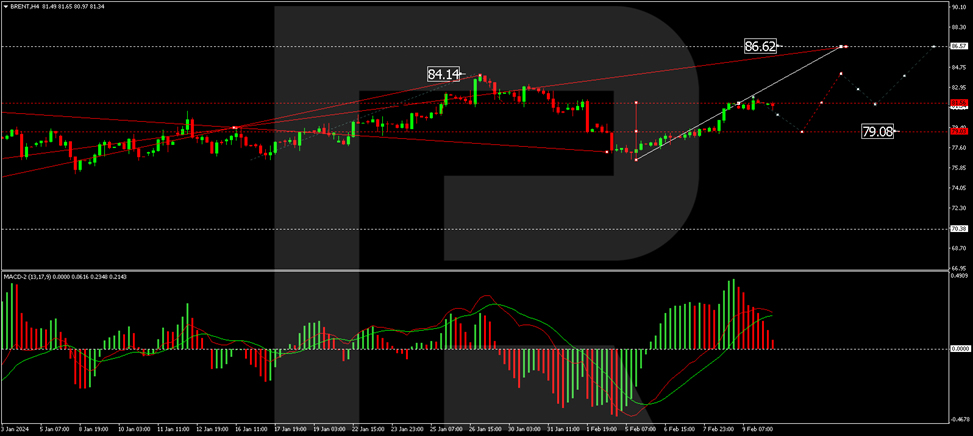

Brent Crude Prices Edge Higher Amid Middle East Tensions

Brent crude oil prices are currently hovering around $82.00 per barrel this Monday, with market sentiment influenced by recent developments in the Middle East. Although concerns over disruptions to energy supplies from the region have somewhat subsided, the possibility of supply disturbances continues to support oil prices.

The rejection of a ceasefire offer by Israel from Hamas last week led to a near 6% increase in oil prices, as the market remains sensitive to geopolitical tensions that could impact oil supply.

It's anticipated that trading activity in the oil market may be subdued this week due to holidays in much of the Asia-Pacific region, including China, Hong Kong, South Korea, Taiwan, and Japan.

Brent Technical Analysis

The H4 chart analysis for Brent indicates the formation of a new growth wave, with a recent structure completion at $82.12. The market is now forming a consolidation range below this level, and a correction down to $79.10 is not out of the question. Following this correction, a new upward trajectory towards $84.20 is expected, potentially extending to $86.68. The MACD indicator supports this view, with the signal line at the highs and anticipated to cycle back towards zero.

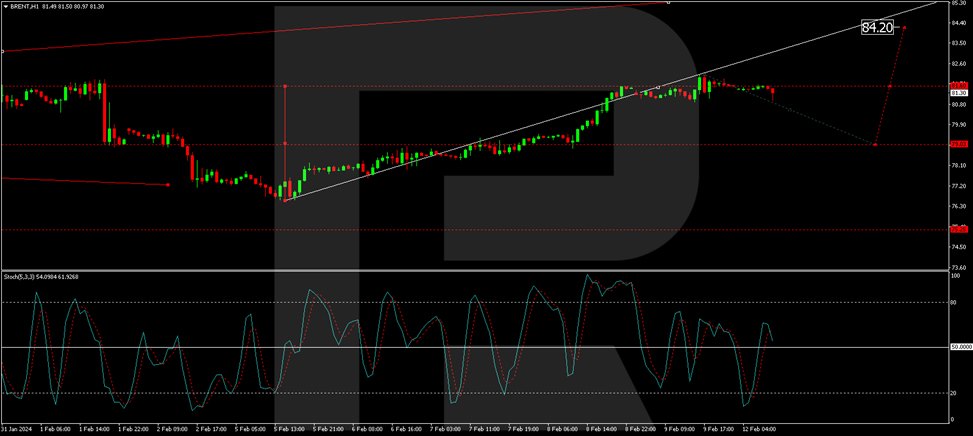

On the H1 Brent chart, a consolidation phase is observed under $82.12. A downward escape could lead to a correction towards $79.10, followed by an expected growth wave to $82.20. An upward breakout could set the stage for a movement towards $84.20. The Stochastic Oscillator, with its signal line above 50 and targeting 80, corroborates this growth potential.

Sunset Market Commentary

Markets

Core bonds marginally gained at the beginning of the new week. In super quiet trading (already starting in Asia as Japan and China kept their doors shut), US yields pared initial drops between 1.5 and 2.6 bps. German rates ease a little more, changes ranging between -0.6 and -2.4 bps. The European swap yield curve shifts lower similarly. Moves are technically inspired. Both US and German bond yields trade just shy of the first technical resistance zones (YtD highs) after recovering some ground last week. Investors took the opportunity of an empty economic calendar today to scoop up some of those beaten-up bonds. With important data scheduled for release later this week, they had an additional argument to do so today. The US and the UK take center stage, beginning with January inflation numbers in the former and the labour market report for the latter tomorrow. Equity markets took a guarded start. The EuroStoxx50 still ekes out a tiny gain, extending its recent winning streak. From a technical point of view, there are basically no resistance levels worth mentioning that lie between the current level (4723) and the nillies all-time high of 5522. Wall Street’s runner’s high is fading with the major indices treading water.

The dollar gains against most G10 peers, including the euro. EUR/USD snaps a four-day winning streak by testing but failing to overcome the 1.0793/1.08 big figure resistance. The pair is currently changing hands at 1.077. The trade-weighted dollar index (DXY) bounced off the 104 mirror support. Sterling holds steady against the euro and eases against an overall stronger USD. GBP/USD remains above 1.26 though – the level that marked the lower bound of a recent sideways trading range. The kiwi dollar underperforms despite the governor of the central bank saying before parliament that inflation remains too high. Deputy governor Hawkesby (what’s in a name) doesn’t seem to be in a hurry to cut rates, noting that the financial system can handle the current higher interest levels. It’s probably some profit-taking in NZD after a boost last week from an influential New Zealand bank airing expectations for the RBNZ to resume hiking. This compares to most, if not all, advanced central banks, be it slowly, pivoting towards monetary easing.

News & Views

The Chartered Institute of Personal and Development published its quarterly survey (winter 2023-24) today. There are signs that UK labour market tightness appears to be reducing and CIPD sees evidence there will be further easing in the coming months, as fewer employers are expecting significant problems filling vacancies. At the start of the new year, hiring freezes also seem more apparent, particularly among SMEs. The net employment balance, measuring the difference between employers expecting to increase staff levels in the next three months and those expecting to decrease staff levels – remains positive but has fallen from +26 last quarter to +22 this quarter. 9% of private sector employers plan to decrease staff levels in the next three months. In the public sector this even amounts to 18%. The expected basic pay increase has fallen from 5% last quarter to 4% this quarter, matching the December Y/Y CPI level. Expected pay awards in the public sector fell further than in the private sector from 5.0% to 3%. CIPD expects this to continue as inflation falls further. The CIPD survey evidence will meet a reality check of the official UK labour market data to be published tomorrow morning.

Price adjustments in the German property market continued in Q4 2023. Property prices were down by 2.2% Q/Q and 7.2% Y/Y, the VDP association of German Pfandbrief Banks revealed. The index dropped 10% off the peak level reached in Q2 2022. Residential property prices declined 1.6% Q/Q and 6.1% Y/Y. However, markets currently are in particular worried on potential impact of a further deterioration in the commercial property markets on banks’ balance sheets. In this respect, VDP saw the Q4 2023 decline in commercial property prices at 4.9% Q/Q and 12.1% Y/Y. This was especially due to office property prices. VDP doesn’t see a material improvement anytime soon as ‘their returns have thus far generally failed to meet investors’ expectations. On top of this, demand for offices remains subdued due to the uncertain economic growth in Germany and the still unclear impact of the working from home trend on office space needed, leading to further price decreases. VDP’s Jens Tolckmitt sees prices in residential property stabilizing summer, but not before the end of the year in the commercial segment.

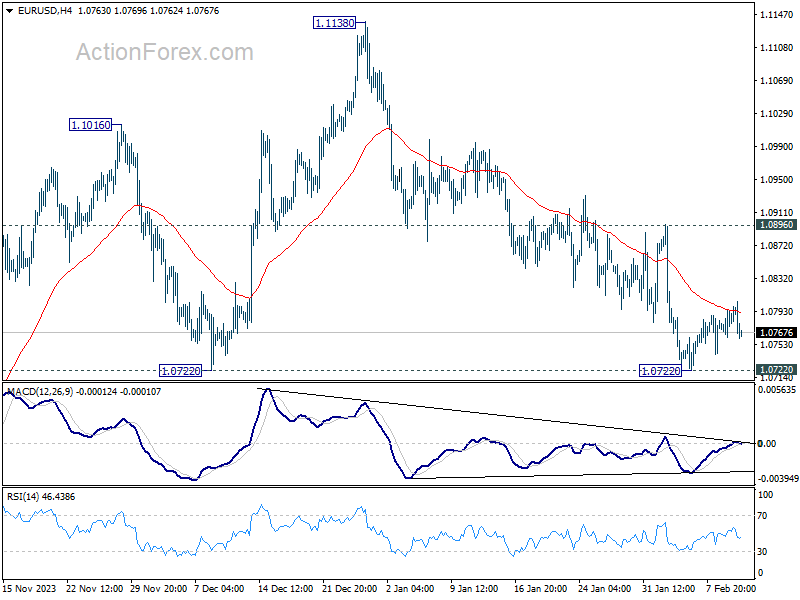

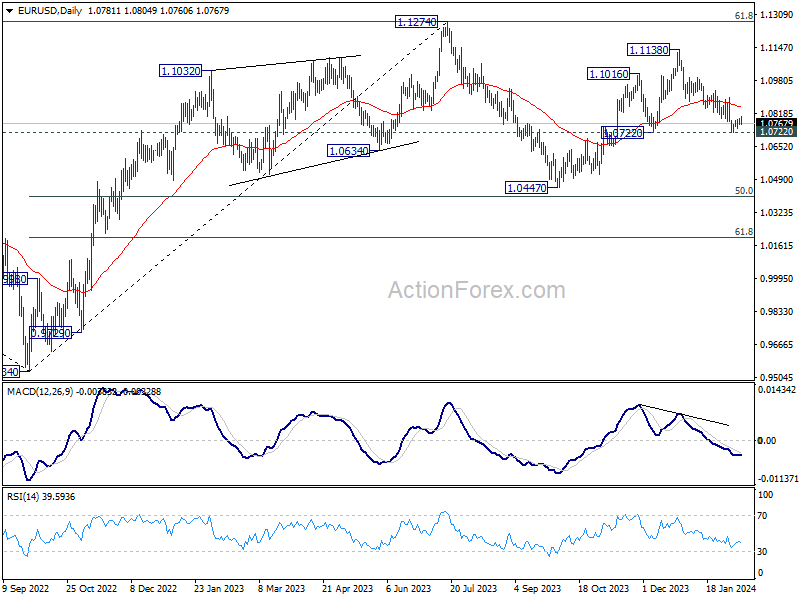

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0766; (P) 1.0781; (R1) 1.0799; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. While stronger recovery cannot be ruled out, outlook will stay bearish as long as 1.0896 resistance holds. On the downside, sustained break of 1.0722 will argue that whole rise from 1.0447 has completed. Deeper fall would then be seen to target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and possibly below.

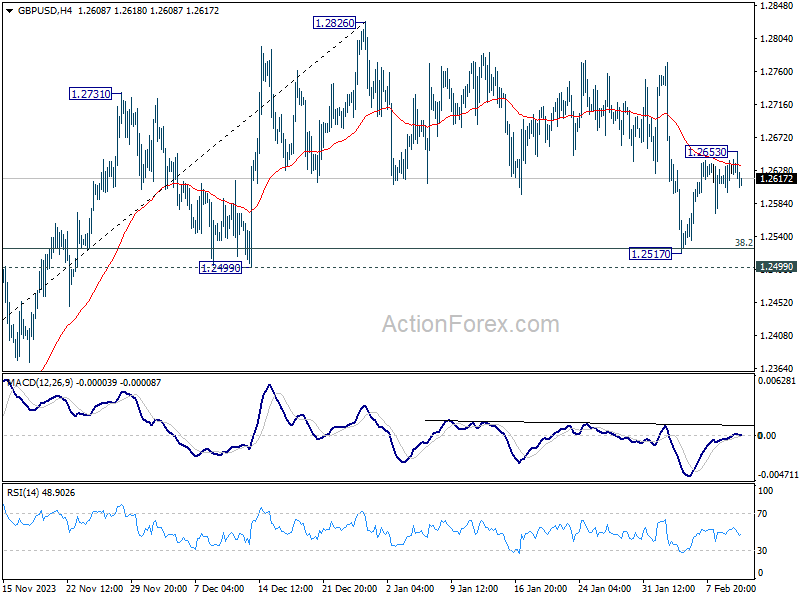

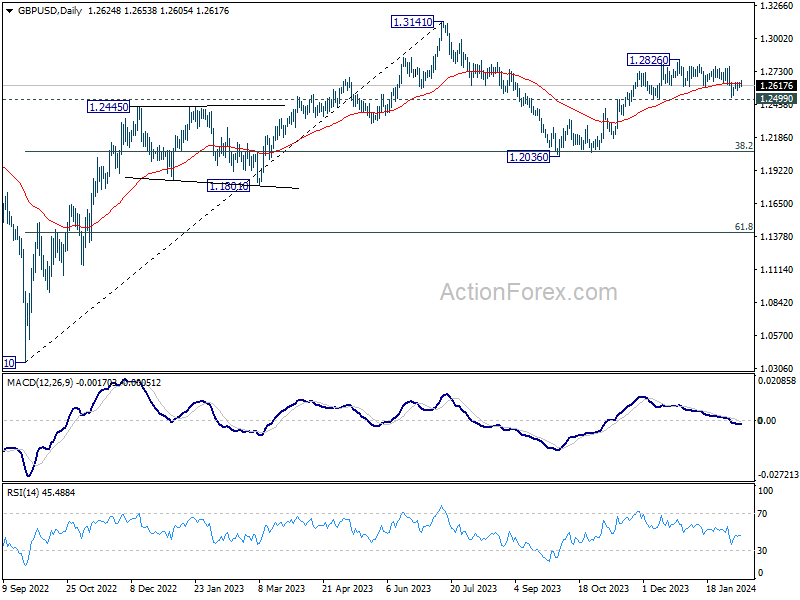

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2604; (P) 1.2624; (R1) 1.2648; More...

GBP/USD edged higher to 1.2653 today but failed to sustain above 55 4H EMA again. Intraday bias remains neutral for the moment. On the upside, firm break of 1.2653 resistance will affirm the case that correction from 1.2826 has completed at 1.2517, after drawing support from 1.2499. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, would could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

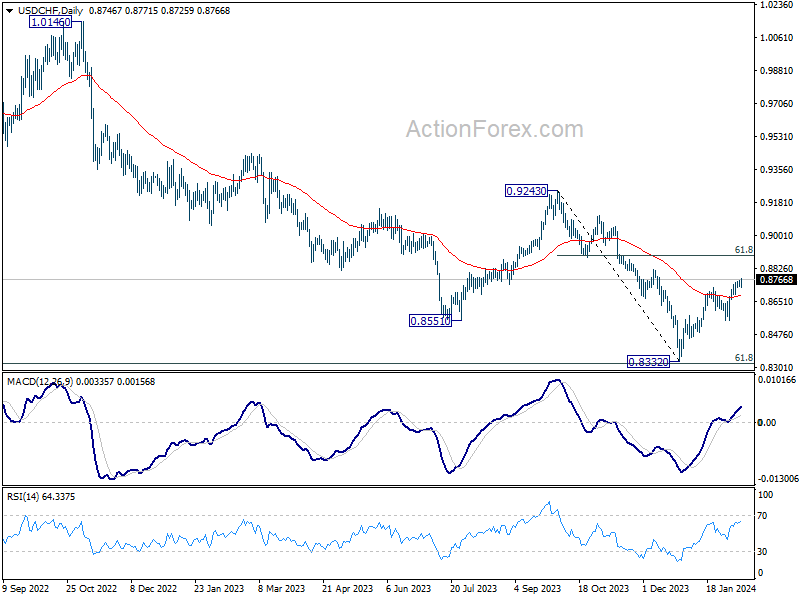

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8733; (P) 0.8747; (R1) 0.8763; More....

USD/CHF's rally continues today and intraday bias stays on the upside. Current rise from 0.8332 should target 61.8% retracement of 0.9243 to 0.8332 at 0.8995. On the downside, below 0.8725 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

In the bigger picture, there is prospect of medium term bottoming at 0.8332 considering possible bullish convergence condition in W MACD, and the support from 0.8317 long term fibonacci support. Sustained trading above 55 D EMA (now at 0.8681) will affirm this case, and bring stronger rise back towards 0.9243 resistance, even as a corrective move.