Sample Category Title

Rising Oil About to Become An Issue

US crude jumped past the $79b level this morning on escalating tensions in the Red Sea. The European and American futures are slightly in the negative at the time of writing, and stocks in Hong Kong and China were better bid on Monday as China imposed ban on short sellers, but the gains remained short-lived after a HK court ordered Evergrande’s liquidation. Globally, we see a limited risk appetite at the start of a week packed with economic data, central bank decisions and corporate earnings.

In Europe

European stocks ended last week on a cheerful sentiment. The dovish European Central Bank (ECB) statement nourished appetite. LVMH jumped 9% on strong quarterly sales, and ASML soared after announcing that its orders tripled – as Chinese rushed in to order chips before the export ban became effective. The EURUSD consolidated in the bearish consolidation zone – below the major 38.2% retracement on its latest rebound, and is testing the 200-DMA to the downside. How far the weakness will continue depends on the US dollar. And the direction the dollar will take will depend on… the Federal Reserve (Fed).

In the US

US stocks traded mixed on Friday but ended last week on a positive note, with the S&P500 near a record, as many good news popped into the headlines throughout the week. The US growth numbers came to enchant investors while inflation numbers looked encouragingly set for further easing: The US economy grew more than 3% last quarter and the Fed’s favorite inflation gauge, the core PCE index fell below 3%.

Resilient growth and lower inflation mean the world to the Fed, a dream come true, the holy grail, the proof that Jay Powell and his team have beaten the economic theory and won over inflation without pushing the US economy into a recession.

And since the Fed signaled that there could be 6 rate cuts this year, which is a fair number of rate cuts to be squeezed into a year for an economy that does - pretty - well, all investors care about is: when will the first cut happen. The probability of a march cut is 50-50, a May cut is priced in at about 90%. The Fed will keep rates unchanged this week, and Powell will likely say the same thing than Lagarde last week: that inflation looks on path toward 2% goal, that soft landing is no longer a daydream and that the Fed will relax rates, but the timing will be data dependent. If that’s the case, the natural response of currency traders could be to sell the dollar.

Overall, note that because the Fed is insistently expected to cut the rates regardless of strong economic figures, the dollar bears resist to upside pressures. But any dovish euphoria is increasingly likely to hit a road bump with oil prices on the rise again.

While everyone expects the dollar to soften moving forward, there are a few scenarios that could lead to a stronger dollar.

1. If inflation numbers make a U-turn and interfere with the Fed’s plan to cut rates, the dollar would see higher demand. Note that among major central banks, the Fed is the one that could delay rate cuts thanks to its strong economic growth.

2. The US dollar could gain if other major economies perform even more poorly than they are expected to - because faltering economies would require faster rate cuts outside the US and lead to a stronger US dollar.

3. An economic shock in the US, or globally, could trigger a rush to the safe haven U.S. dollar and leave the dollar bears on the backfoot.

Elsewhere

The Bank of England (BoE) decision, euro area growth and inflation numbers, Australian inflation update, Canadian GDP and the US jobs numbers will be closely watched.

On the corporate calendar, Microsoft, Alphabet, Apple, AMD, and US big oil companies are among the names that are due to announce their latest earnings this week. A major part of the investor focus will be on Microsoft and its AI announcements. Any positive surprise should keep investors on their cloud.

But note that, overall, 25% of the companies in the S&P500 have reported results for Q4. Of these companies, 69% have reported actual EPS above estimates, yes but that’s below the 5-year average of 77%, according to FactSet.

Fed, Bank of England and Riksbank Policy Meetings This Week

In focus today

The week starts off with the publication of the Swedish preliminary GDP statistics for Q4 and the full GDP development of 2023. Strong GDP indicators in October and November (+1.0% and 0.2%) promise a relatively strong ending of 2023. We also receive data for Swedish retail sales for December. The sentiment in the retail sector is improving and may support Swedish growth.

The main event this week is the FOMC meeting on Wednesday. We expected the Fed to hold policy rates unchanged at this week's meeting but deliver its first interest rate cut of 25bp at the March meeting. Thursday, both the Bank of England and the Swedish Riksbank announce their rate decision, where we expect both to keep policy rates unchanged.

Economic and market news

What happened overnight

Iran backed militants performed a drone attack against a US military base in northeastern Jordan, the White House announced late Sunday. The attack killed three US servicemen. President Joe Biden said that the US will "hold all those responsible to account at a time and in a manner of our choosing." On the back of this, oil futures rose with brent crude rising as much as 1.5% in the early hours of Monday, hitting 84.80 USD/barrel.

A Hong Kong court has ordered China Evergrande to be wound up. The liquidation order came after the developer was not able to come up with a restructuring plan that would satisfy international creditors.

What happened the weekend

In the US, core PCE index rose 2.9% y/y, down from a 3.2% pace in November just slightly below expectations. Real spending remained very strong with November revised higher. On headline level, all the figures were fairly well in line with expectations, and hence the market reaction was muted. That said, they still underscore how US economy remains solid.

In the euro area, monetary aggregate statistics showed that M3 rose 0.1% in December (from -0.9% in November). Importantly, loans to households were 0.3% (down from 0.5% in November) and to non-financial corporations 0.4% (up from 0% in November). The credit growth numbers coupled with the BLS out last week point to the credit impulse having bottomed. In Germany, consumer confidence declined to -29.7 in February (cons: -24.6, prior: -25.1). The past months, consumer confidence has declined in tandem with the service PMIs from Germany, which means we are likely in for another weak quarter or two in Germany before rising real wages, a strong labour market, and a possible rebound in the manufacturing sector should increase private consumption and service sector growth.

In Norway, retail sales dropped 0.9 % m/m in December, as Christmas shopping was worse than signalled by short-term card data, which could be a seasonal adjustment problem. Note that service consumption is currently slowing, so overall consumption will be weak.

In Israel, prime minister Benjamin Netanyahu said that Israel vows to continue the war on Hamas after the UN's International Court of Justice ordered Israel to take steps to safeguard Palestinians.

In the Red Sea the Houthi rebels on Friday hit a British oil carrier transporting products for Trafigura.

In China, restrictions were made to effectively limit shorts selling. Starting from Monday, investors who buy shares will not be allowed to lend them out for short selling within an agreed lock-up period, the Shenzhen and Shanghai stock exchanges said on Sunday. It is seen as an attempt to try to stop the stock sell-out fuelled by uncertainty over China's economic growth prospects.

Equities: Global equities were higher for the seventh consecutive day on Friday. Once again, the reason was the combination of decent inflation data and strong macroeconomic indicators, with the positive data emerging from the US. However, on Friday, defensives outperformed on the sector side, while Europe continued to outperform within the regions. As mentioned last week, this is the peak of earnings season, and some disappointing guidance from US tech companies was the reason behind the US cyclicals' underperformance on Friday. In the US, Dow rose by 0.2%, S&P 500 dropped by 0.1%, Nasdaq declined by 0.4%, and Russell 2000 increased by 0.1%. Asian markets are mostly higher this morning though with China going against the trend. US and European futures are lower.

FI: Global yields started Friday's session 5bp lower than Thursday's close, however by the end of Friday it was broadly unchanged as the enthusiasm of the UST overnight rally faded. The ECB speak on Friday saw a broad consensus and reflected the ECB's guidance on Thursday. This weekend, Villeroy said that ECB will cut the rates this year at that 'the exact date, not one is excluded, and everything will be open at our next meetings.' This will keep markets zooming in on the April meeting as a live meeting, with 22bp priced (cumulative). We currently still like our call for the first cut in June. Markets are pricing 143bp of rate cuts by year end.

FX: USD was in for a whirlwind of a week, as US macro data came in to the strong side, with EUR/USD ending the week around the 1.0850 mark. Last week saw NOK gain on relative rate differentials with the market perception that NB is set to deliver rate cuts among the last central banks and also deliver fewer rate cuts than peers in the coming years. This week focus turns to European inflation data and further central bank meeting from the Fed, Riksbanken and the Bank of England.

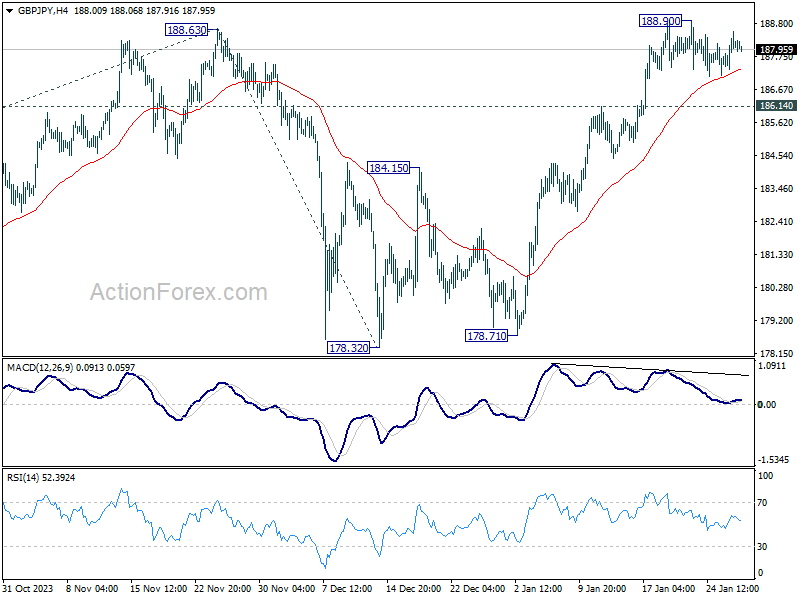

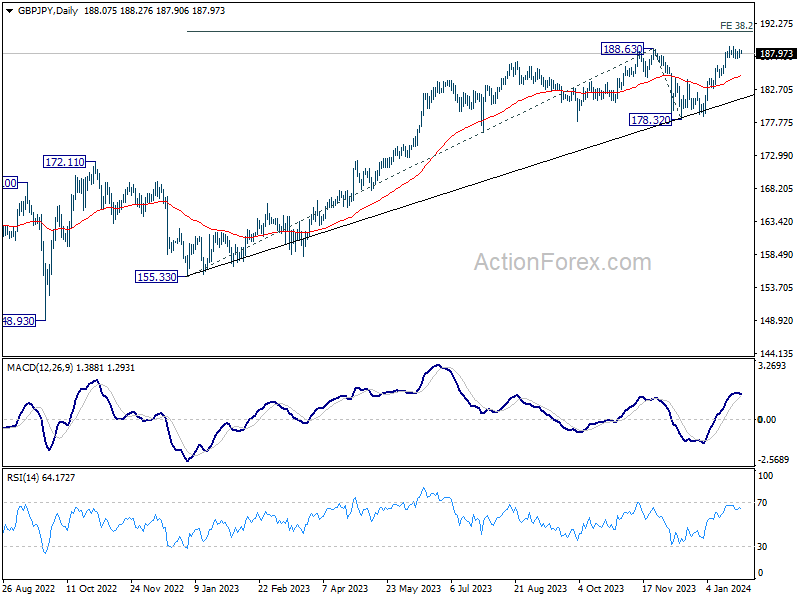

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.50; (P) 188.04; (R1) 188.73; More...

Intraday bias in GBP/JPY remains neutral at this point. Further rally is expected as long as 186.14 support holds. Break of 188.90, and sustained trading above 188.63, will confirm up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04. However, break of 186.14 will turn bias to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

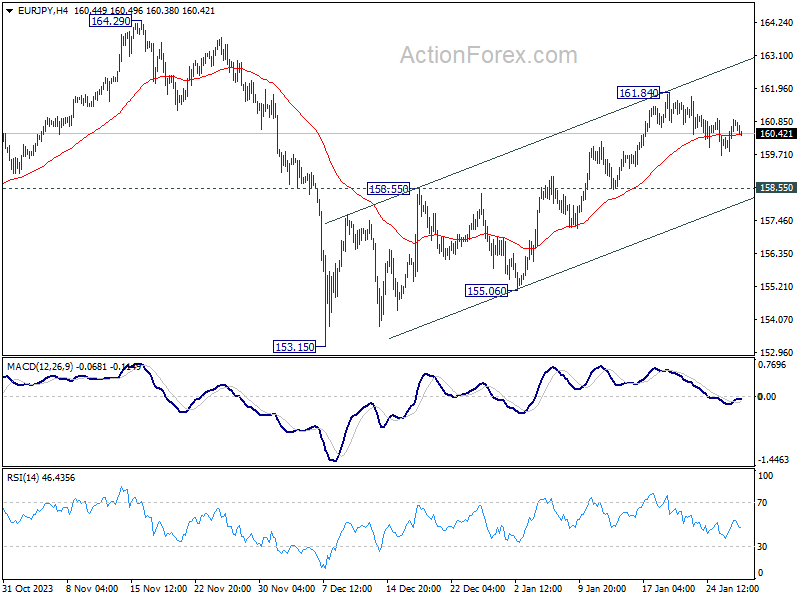

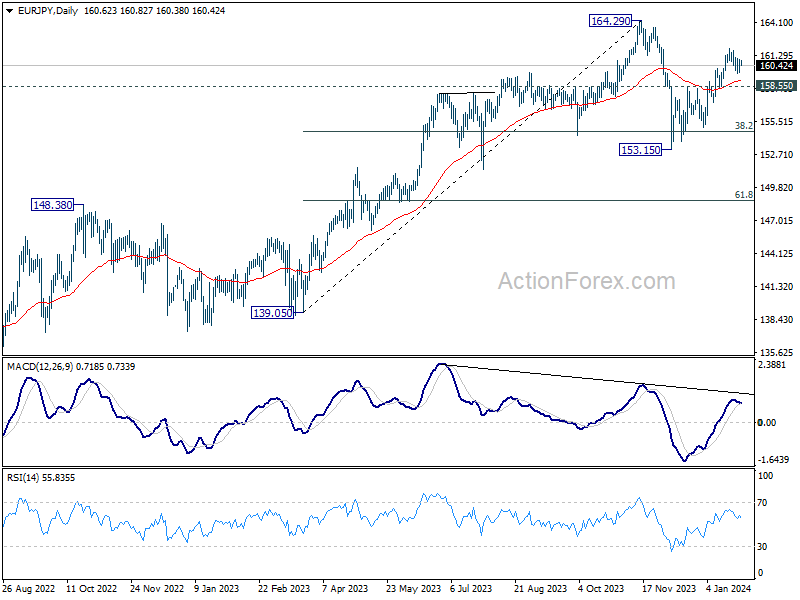

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.12; (P) 160.52; (R1) 161.22; More...

Intraday bias in EUR/JPY remains neutral as consolidation from 161.84 is extending. While another dip cannot be ruled out, further rally is expected as long as 158.55 resistance turned support holds. Break of 161.84 will resume the rebound from 153.15 to retest 164.29 high.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

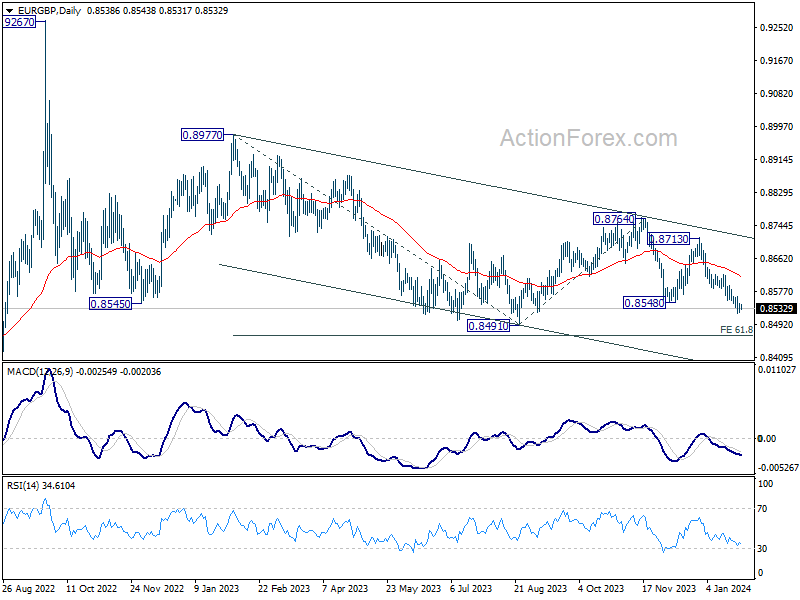

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8531; (P) 0.8540; (R1) 0.8554; More...

While downside momentum in EUR/GBP isn't too convincing, further decline is still expected with 0.8563 resistance intact. Next target is 0.8491 low and break will resume larger down trend to 0.8464 projection level. On the upside, above 0.8563 minor resistance will turn intraday bias neutral and bring consolidations again.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

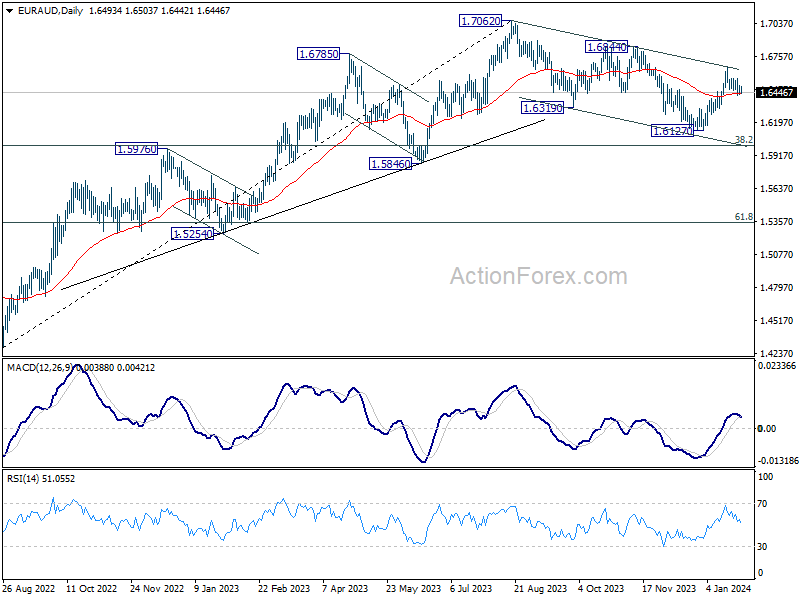

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6454; (P) 1.6484; (R1) 1.6536; More...

Intraday bias in EUR/AUD remains neutral at this point. Further rally is expected as long as 1.6398 support holds. Corrective fall from 1.7062 should have completed with three waves down to 1.6127 already. Above 1.6671 will target 1.6844 resistance to confirm this bullish case. However, break of 1.6398 will dampen this view and bring retest of 1.6127 low instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

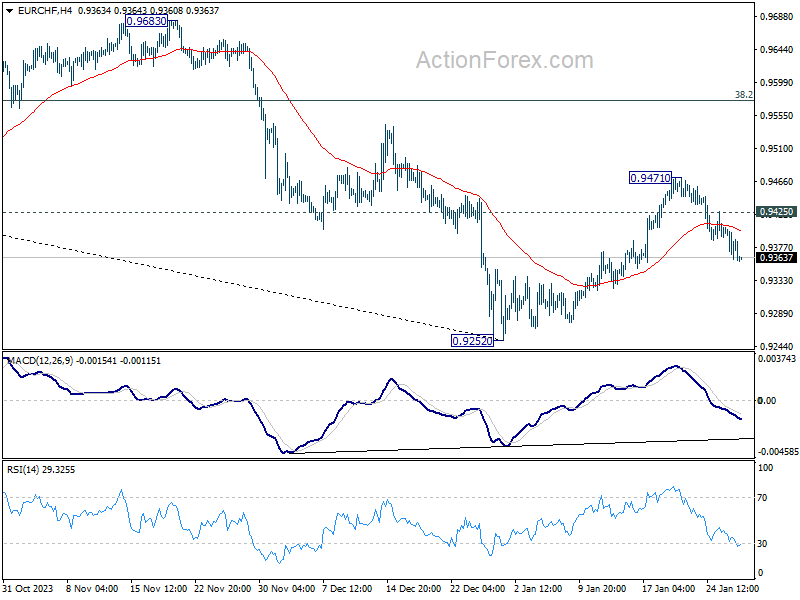

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9358; (P) 0.9382; (R1) 0.9402; More...

Intraday bias in EUR/CHF stays mildly on the downside at this point. Deeper pull back could be seen but downside should be contained above 0.9252 low to bring rebound. On the upside, above 0.9425 minor resistance will turn bias back to the upside. Further break of 0.9471 will resume the rebound from 0.9252 to 38.2% retracement of 1.0095 to 0.9252 at 0.9574.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9638) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

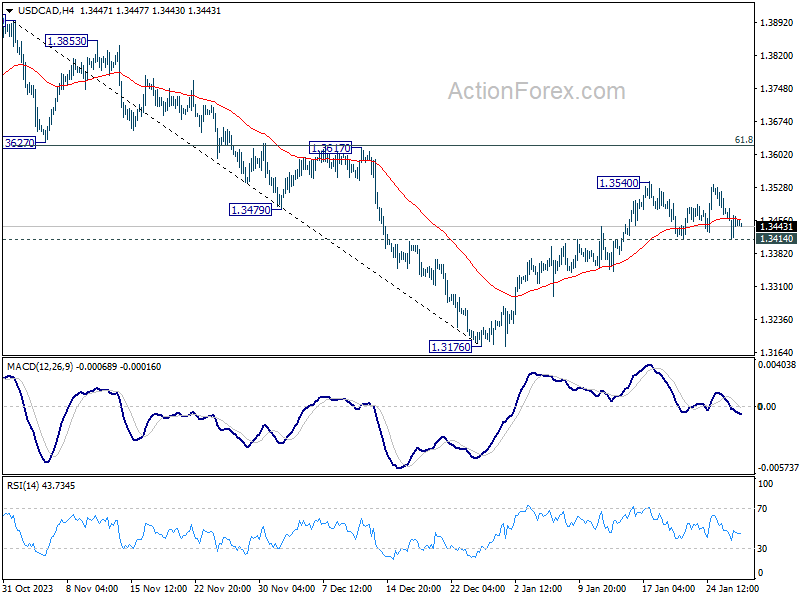

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3417; (P) 1.3450; (R1) 1.3486; More...

Intraday bias in USD/CAD remains neutral for consolidations below 1.3540. Further rally is in favor as long as 1.3414 support holds. Fall from 1.3897 should have completed at 1.3716. Break of 1.3540 will target 1.3617 cluster resistance (61.8% retracement of 1.3897 to 1.3176 at 1.3622). Decisive break there will pave the way to 1.3897/3976 key resistance zone. However, firm break of 1.3414 will dampen this view and turn bias back to the downside.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

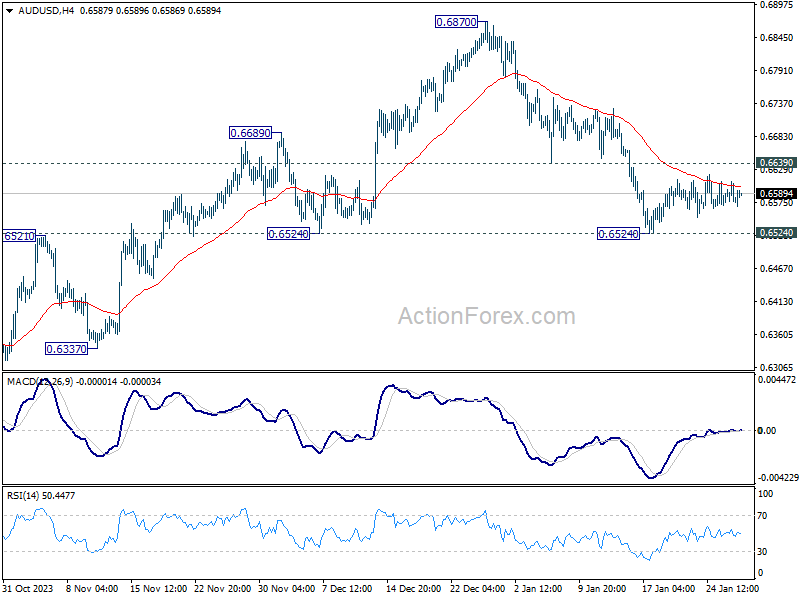

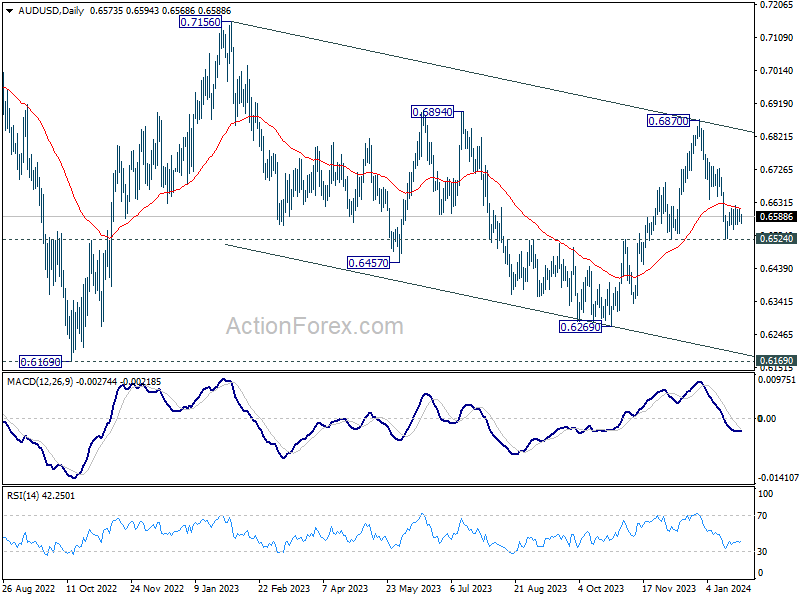

AUD/USD Daily Report

Daily Pivots: (S1) 0.6563; (P) 0.6586; (R1) 0.6599; More...

Intraday bias in AUD/USD remains neutral for the moment, as consolidation continues above 0.6524. Further fall is expected with 0.6639 minor resistance intact. On the downside, firm break of 0.6524 support will argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support. On the upside, break of 0.6639 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

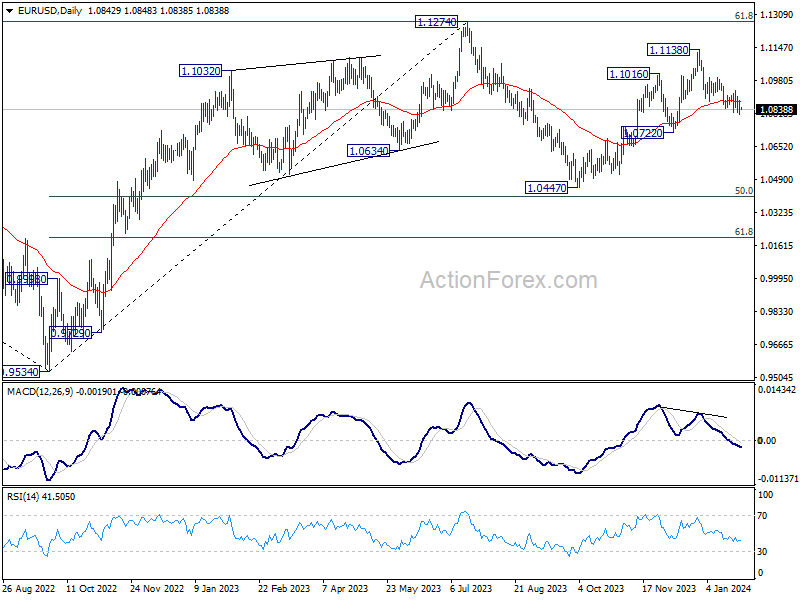

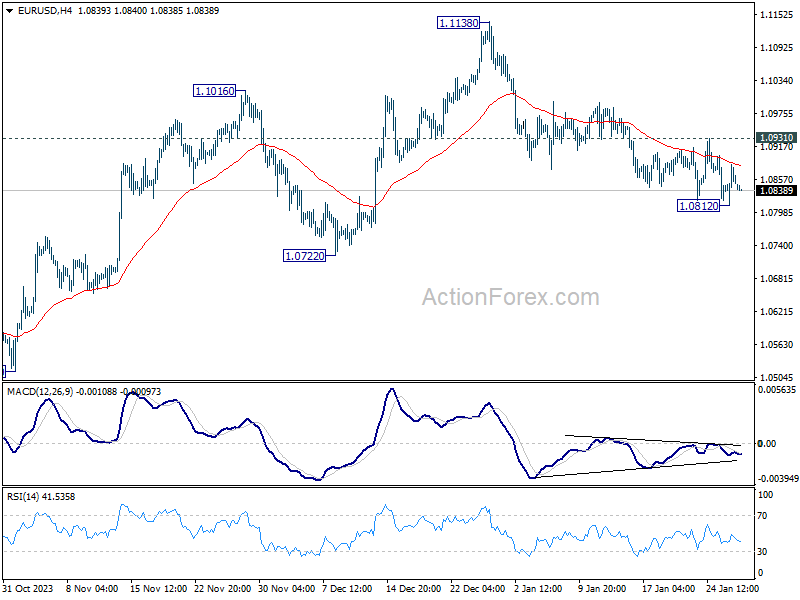

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0816; (P) 1.0851; (R1) 1.0889; More...

Intraday bias in EUR/USD remains neutral and more consolidations could be seen above 1.0812. Further decline is mildly in favor as long as 1.0931 resistance holds. On the downside, break of 1.0812 will resume the fall from 1.1138 to 1.0722 support. On the upside, above 1.0931 will turn bias to the upside for stronger rebound towards 1.1138 resistance.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.