Sample Category Title

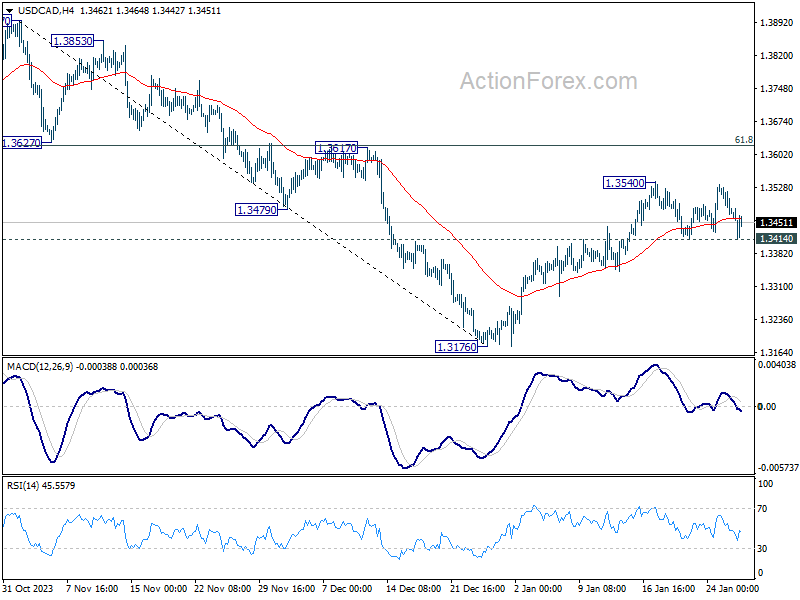

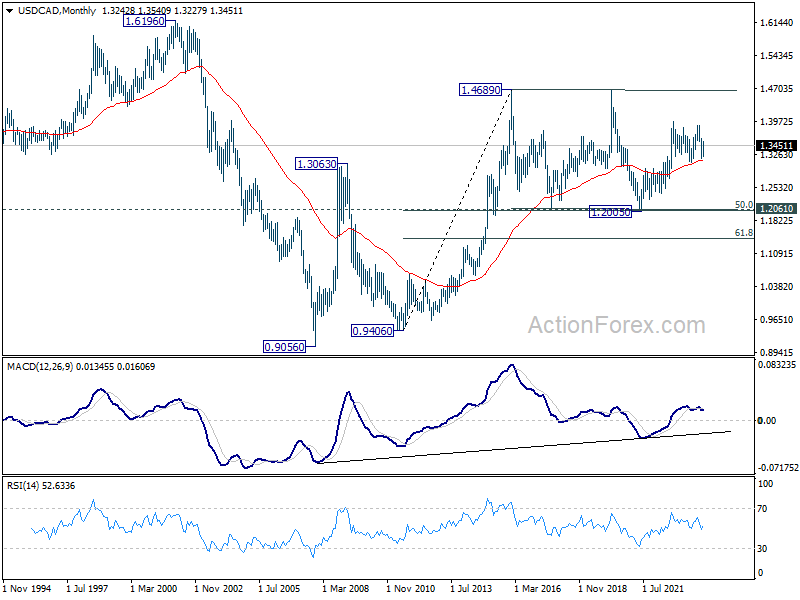

USD/CAD Weekly Outlook

USD/CAD stayed in consolidation below 1.3540 last week and outlook is unchanged. Initial bias stays neutral this week first, and further rally is in favor. Fall from 1.3897 should have completed at 1.3716. Break of 1.3540 will target 1.3617 cluster resistance (61.8% retracement of 1.3897 to 1.3176 at 1.3622). Decisive break there will pave the way to 1.3897/3976 key resistance zone. However, firm break of 1.3414 will dampen this view and turn bias back to the downside.

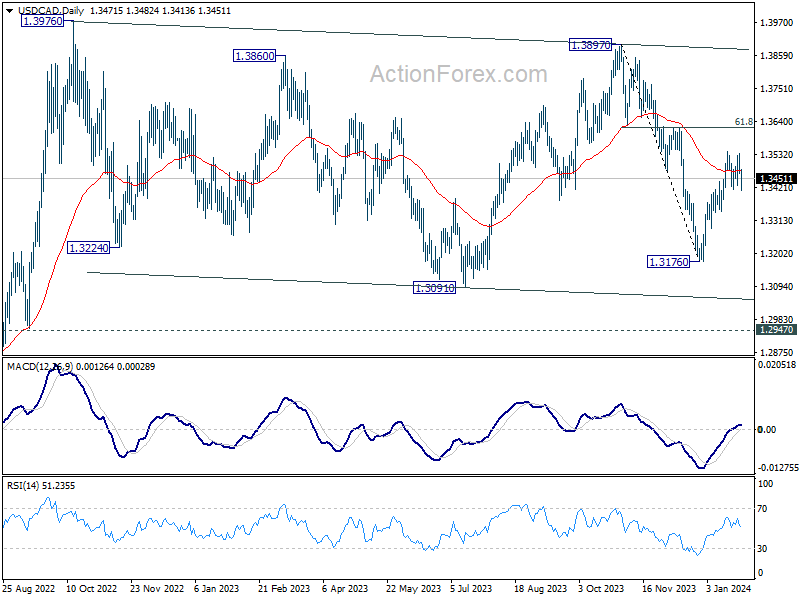

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

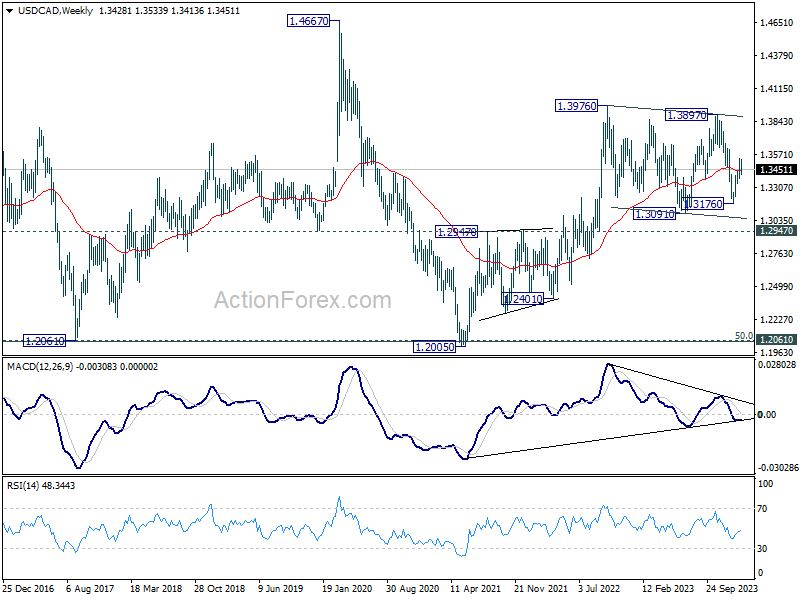

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as long as 1.2947 resistance turned support holds.

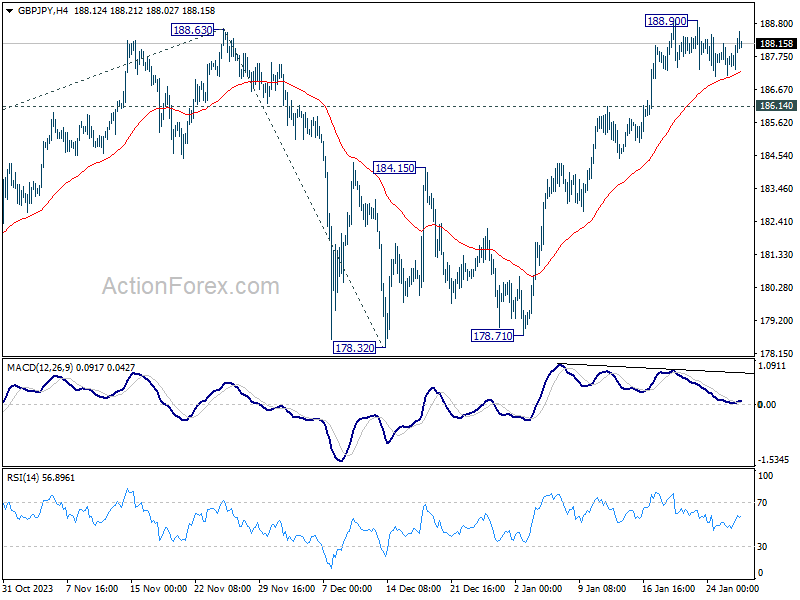

GBP/JPY Weekly Outlook

GBP/JPY edged higher to 188.90 last week but retreated since then. Initial bias remains neutral this week first. Further rally is expected as long as 186.14 support holds. Break of 188.90, and sustained trading above 188.63, will confirm up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04. However, break of 186.14 will turn bias to the downside for deeper pullback.

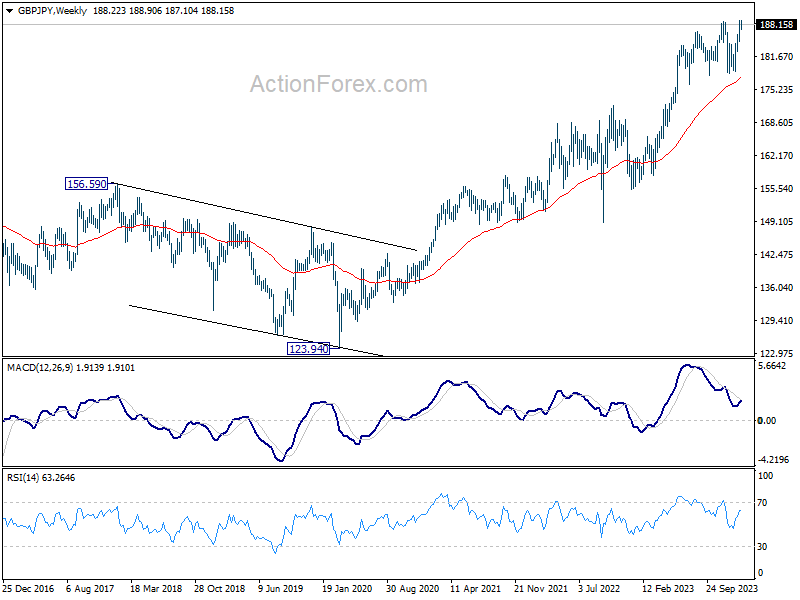

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

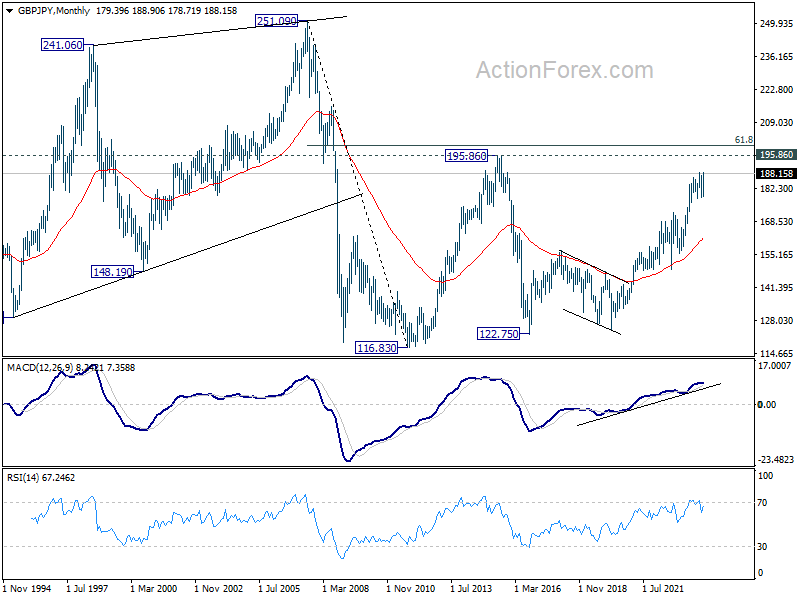

In the longer term picture, rise from 122.75 (2016 low) in still in progress despite loss of upside momentum as seen in W MACD. Further rise will remain in favor, as long as 172.11 support holds, to retest 195.86 (2015 high).

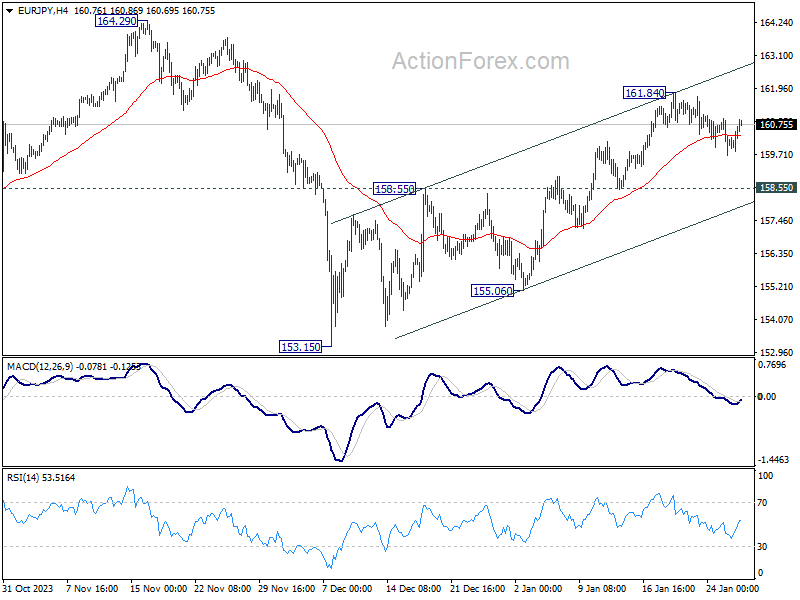

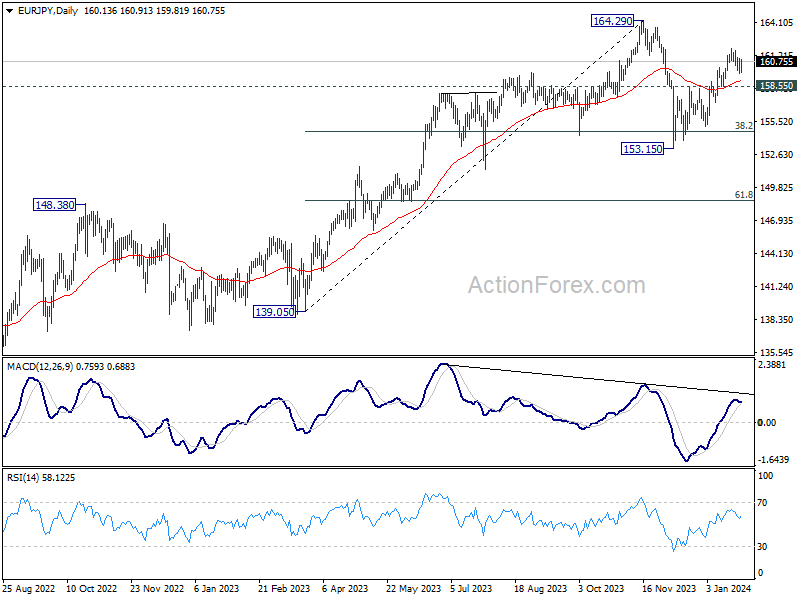

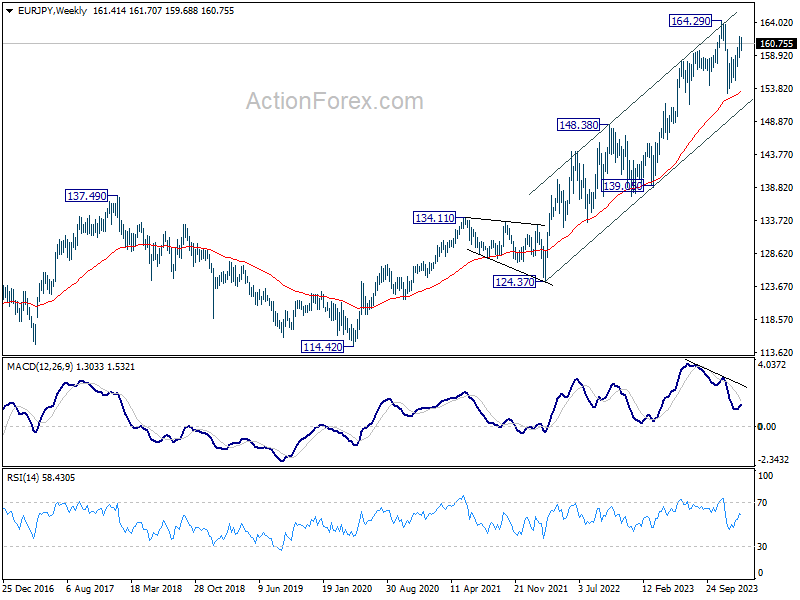

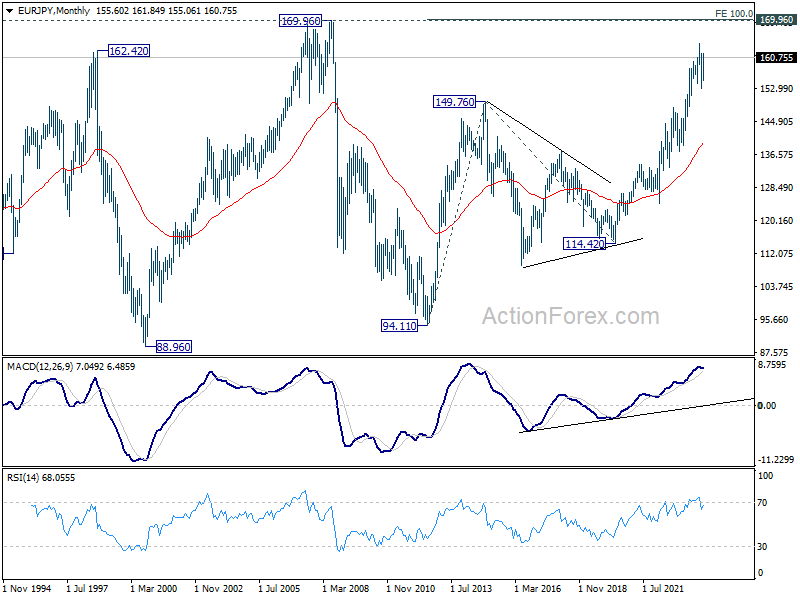

EUR/JPY Weekly Outlook

EUR/JPY turned into consolidation below 161.84 last week. Initial bias remains neutral this week first. While another dip cannot be ruled out, further rally is expected as long as 158.55 resistance turned support holds. Break of 161.84 will resume the rebound from 153.15 to retest 164.29 high.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

In the long term picture, rise from 114.42 (2020 low) is seen as the third leg of the whole up trend from 94.11 (2012 low). Next target is 100% projection of 94.11 to 149.76 from 114.42 at 170.07 which is close to 169.96 (2008 high). This will remain the favored case as long as 148.48 resistance turned support holds.

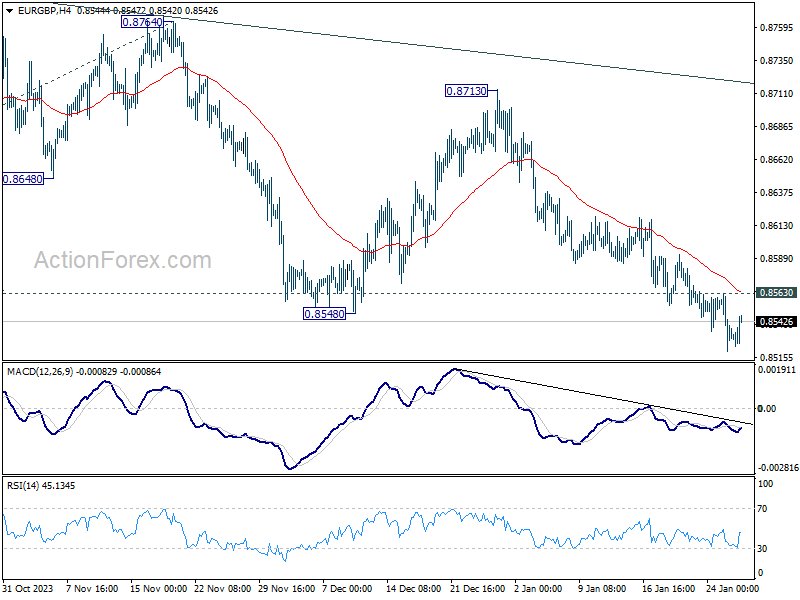

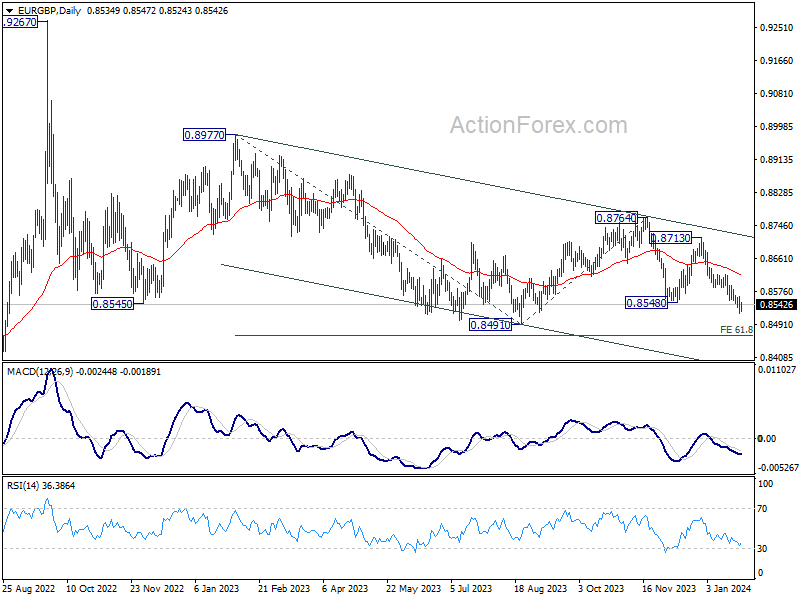

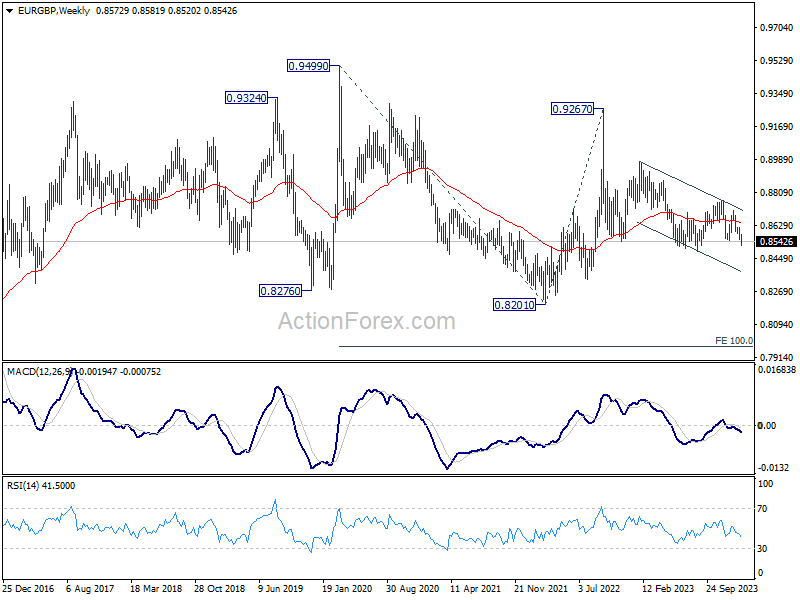

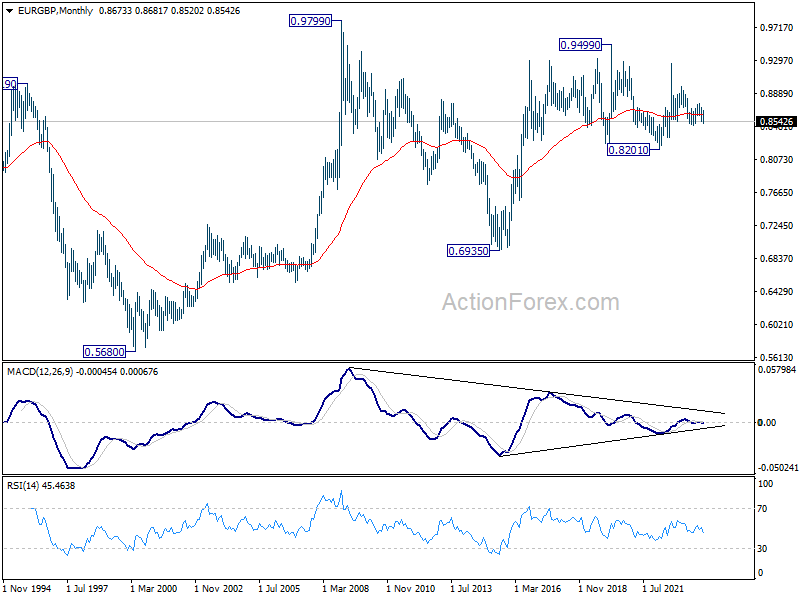

EUR/GBP Weekly Outlook

EUR/GBP's fall from 0.8764 resumed through 0.8548 last week. While downside momentum is a bit unconvincing, further decline is expected with 0.8563 resistance intact. Next target is 0.8491 low and break will resume larger down trend to 0.8464 projection level. On the upside, above 0.8563 minor resistance will turn intraday bias neutral and bring consolidations again.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Fall from 0.9267 is the third leg of the pattern from 0.9499. Break of 0.8201 (2022 low) will target 100% projection of 0.9499 to 0.8201 from 0.9267 at 0.7969.

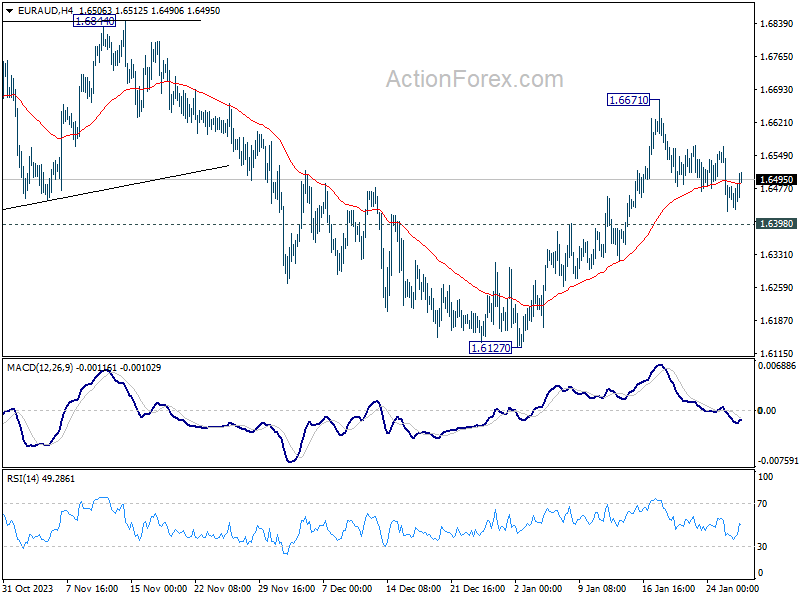

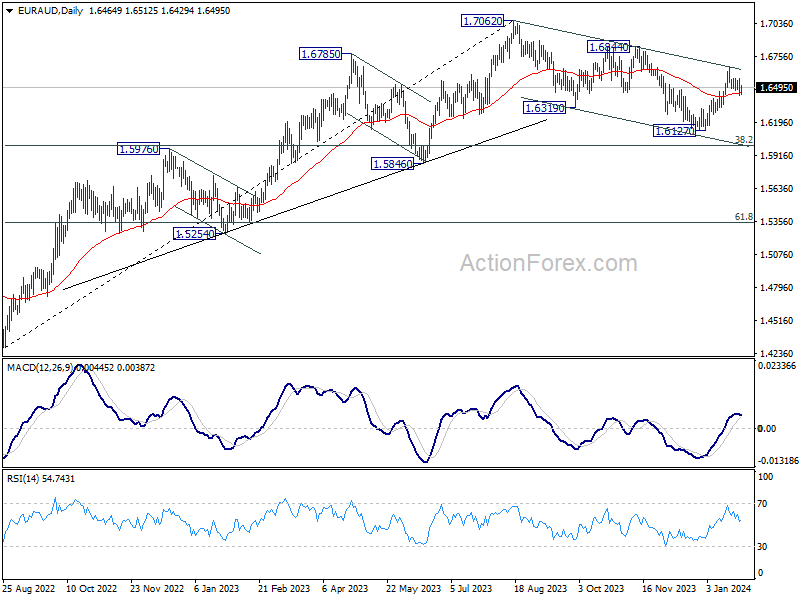

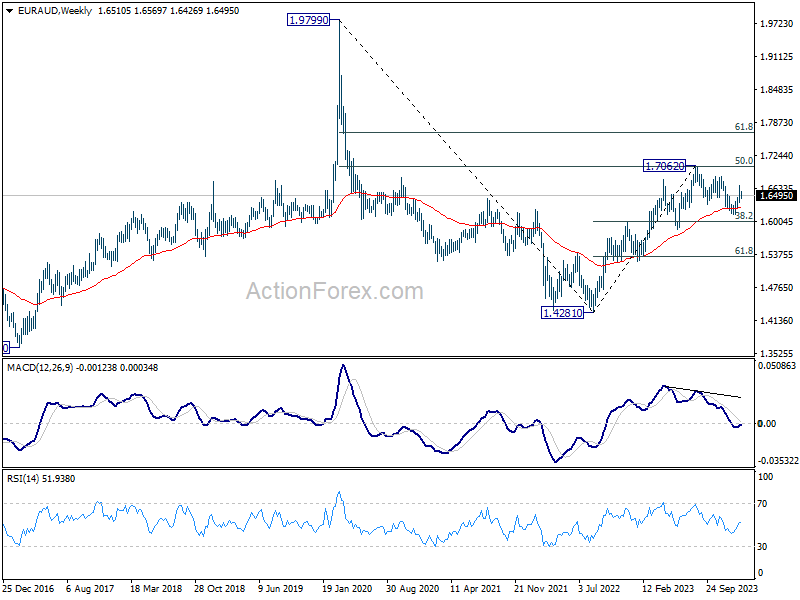

EUR/AUD Weekly Outlook

EUR/AUD's corrective pull back continued last week and outlook is unchanged. Initial bias remains neutral this week first. Further rally is expected as long as 1.6398 support holds. Corrective fall from 1.7062 should have completed with three waves down to 1.6127 already. Above 1.6671 will target 1.6844 resistance to confirm this bullish case. However, break of 1.6398 will dampen this view and bring retest of 1.6127 low instead.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

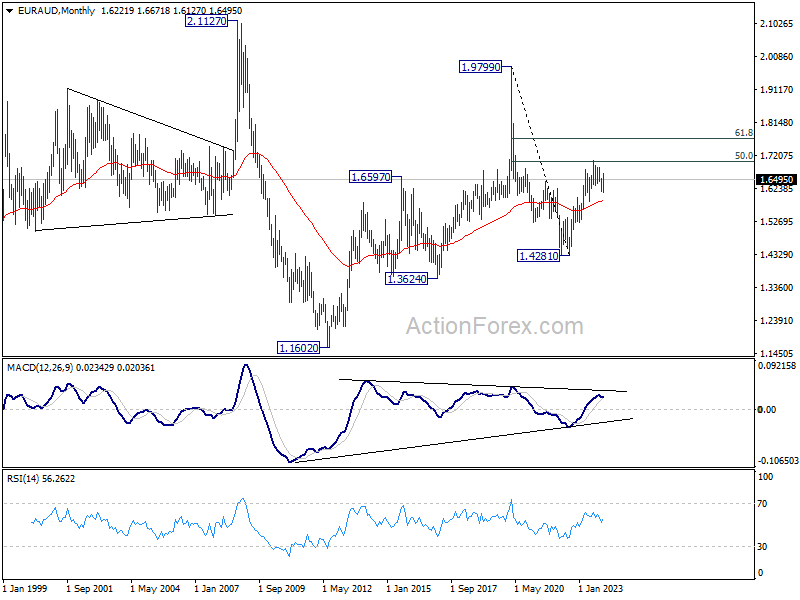

In the longer term picture, price actions from 1.9799 (2020 high) is seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5881) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

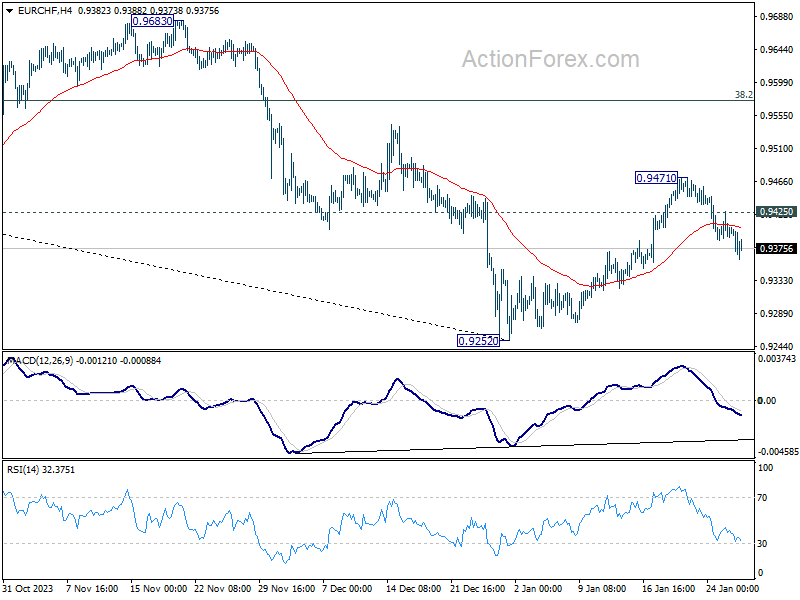

EUR/CHF Weekly Outlook

EUR/CHF failed to sustain above 55 D EMA (now at 0.9443) last week, and reversed from there. Initial bias stays mildly on the downside this week for deeper pull back. But downside should be contained above 0.9252 low to bring rebound. On the upside, above 0.9425 minor resistance will turn bias back to the upside. Further break of 0.9471 will resume the rebound to 38.2% retracement of 1.0095 to 0.9252 at 0.9574.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9659) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

In the long term picture, outlook remains bearish as it's staying well below 55 M EMA (now at 1.0265). Larger down trend from 1.2004 (2018 high) is in progress.

Summary 1/29 – 2/2

Monday, Jan 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | -975M | -1234M |

| 23:30 | JPY | Unemployment Rate Dec | 2.50% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | |

| Forecast: -975M | Previous: -1234M | ||

| 23:30 | JPY | Unemployment Rate Dec | |

| Forecast: 2.50% | Previous: 2.50% | ||

Tuesday, Jan 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Dec | -1.90% | 2.00% |

| 06:30 | EUR | France Consumer Spending M/M Dec | 0.00% | 0.70% |

| 06:30 | EUR | France GDP Q/Q Q4 P | 0.00% | -0.10% |

| 07:00 | CHF | Trade Balance (CHF) Dec | 2.55B | 3.71B |

| 08:00 | CHF | KOF Leading Indicator Jan | 98.2 | 97.8 |

| 09:00 | EUR | Italy GDP Q/Q Q4 P | 0.00% | 0.10% |

| 09:00 | EUR | Germany GDP Q/Q Q4 P | -0.30% | -0.10% |

| 09:30 | GBP | M4 Money Supply M/M Dec | 0.20% | -0.10% |

| 09:30 | GBP | Mortgage Approvals Dec | 53K | 50K |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | -0.10% | -0.10% |

| 10:00 | EUR | Eurozone Economic Sentiment Jan | 96.2 | 96.4 |

| 10:00 | EUR | Eurozone Industrial Confidence Jan | -9 | -9.2 |

| 10:00 | EUR | Eurozone Services Sentiment Jan | 8 | 8.4 |

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | 4.80% | 4.90% |

| 14:00 | USD | Housing Price Index M/M Nov | 0.20% | 0.30% |

| 15:00 | USD | Consumer Confidence Jan | 113.2 | 110.7 |

| 23:50 | JPY | BoJ Summary of Opinions | ||

| 23:50 | JPY | Industrial Production M/M Dec P | 2.40% | -0.90% |

| 23:50 | JPY | Retail Trade Y/Y Dec | 5.00% | 5.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Dec | |

| Forecast: -1.90% | Previous: 2.00% | ||

| 06:30 | EUR | France Consumer Spending M/M Dec | |

| Forecast: 0.00% | Previous: 0.70% | ||

| 06:30 | EUR | France GDP Q/Q Q4 P | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 07:00 | CHF | Trade Balance (CHF) Dec | |

| Forecast: 2.55B | Previous: 3.71B | ||

| 08:00 | CHF | KOF Leading Indicator Jan | |

| Forecast: 98.2 | Previous: 97.8 | ||

| 09:00 | EUR | Italy GDP Q/Q Q4 P | |

| Forecast: 0.00% | Previous: 0.10% | ||

| 09:00 | EUR | Germany GDP Q/Q Q4 P | |

| Forecast: -0.30% | Previous: -0.10% | ||

| 09:30 | GBP | M4 Money Supply M/M Dec | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 09:30 | GBP | Mortgage Approvals Dec | |

| Forecast: 53K | Previous: 50K | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Jan | |

| Forecast: 96.2 | Previous: 96.4 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Jan | |

| Forecast: -9 | Previous: -9.2 | ||

| 10:00 | EUR | Eurozone Services Sentiment Jan | |

| Forecast: 8 | Previous: 8.4 | ||

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Nov | |

| Forecast: 4.80% | Previous: 4.90% | ||

| 14:00 | USD | Housing Price Index M/M Nov | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 15:00 | USD | Consumer Confidence Jan | |

| Forecast: 113.2 | Previous: 110.7 | ||

| 23:50 | JPY | BoJ Summary of Opinions | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Industrial Production M/M Dec P | |

| Forecast: 2.40% | Previous: -0.90% | ||

| 23:50 | JPY | Retail Trade Y/Y Dec | |

| Forecast: 5.00% | Previous: 5.30% | ||

Wednesday, Jan 31, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Jan | 33.2 | |

| 00:30 | AUD | CPI Q/Q Q4 | 0.80% | 1.20% |

| 00:30 | AUD | CPI Y/Y Q4 | 4.30% | 5.40% |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | 0.90% | 1.20% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | 4.40% | 5.20% |

| 00:30 | AUD | Private Sector Credit M/M Dec | 0.40% | 0.40% |

| 01:00 | CNY | NBS Non-Manufacturing PMI Jan | 50.4 | |

| 01:00 | CNY | NBS Manufacturing PMI Jan | 49.3 | 49 |

| 05:00 | JPY | Housing Starts Y/Y Dec | -6.20% | -8.50% |

| 05:00 | JPY | Consumer Confidence Jan | 37.6 | 37.2 |

| 07:00 | EUR | Germany Import Price Index M/M Dec | -0.50% | -0.10% |

| 07:00 | EUR | Germany Retail Sales M/M Dec | 0.60% | -2.50% |

| 07:30 | CHF | Real Retail Sales Y/Y Dec | 0.90% | 0.70% |

| 08:55 | EUR | Germany Unemployment Change Jan | 10K | 5K |

| 08:55 | EUR | Germany Unemployment Rate Jan | 5.90% | 5.90% |

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | -23.7 | |

| 09:00 | EUR | Italy Unemployment Dec | 7.50% | 7.50% |

| 13:00 | EUR | Germany CPI M/M Jan P | 0.20% | 0.10% |

| 13:00 | EUR | Germany CPI Y/Y Jan P | 3.40% | 3.70% |

| 13:15 | USD | ADP Employment Change Jan | 143K | 164K |

| 13:30 | CAD | GDP M/M Nov | 0.10% | 0.00% |

| 13:30 | USD | Employment Cost Index Q4 | 1.00% | 1.10% |

| 14:45 | USD | Chicago PMI Jan | 48.2 | 46.9 |

| 15:30 | USD | Crude Oil Inventories | -9.2M | |

| 19:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% |

| 19:30 | USD | FOMC Press Conference |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | NZD | ANZ Business Confidence Jan | |

| Forecast: | Previous: 33.2 | ||

| 00:30 | AUD | CPI Q/Q Q4 | |

| Forecast: 0.80% | Previous: 1.20% | ||

| 00:30 | AUD | CPI Y/Y Q4 | |

| Forecast: 4.30% | Previous: 5.40% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q4 | |

| Forecast: 0.90% | Previous: 1.20% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q4 | |

| Forecast: 4.40% | Previous: 5.20% | ||

| 00:30 | AUD | Private Sector Credit M/M Dec | |

| Forecast: 0.40% | Previous: 0.40% | ||

| 01:00 | CNY | NBS Non-Manufacturing PMI Jan | |

| Forecast: | Previous: 50.4 | ||

| 01:00 | CNY | NBS Manufacturing PMI Jan | |

| Forecast: 49.3 | Previous: 49 | ||

| 05:00 | JPY | Housing Starts Y/Y Dec | |

| Forecast: -6.20% | Previous: -8.50% | ||

| 05:00 | JPY | Consumer Confidence Jan | |

| Forecast: 37.6 | Previous: 37.2 | ||

| 07:00 | EUR | Germany Import Price Index M/M Dec | |

| Forecast: -0.50% | Previous: -0.10% | ||

| 07:00 | EUR | Germany Retail Sales M/M Dec | |

| Forecast: 0.60% | Previous: -2.50% | ||

| 07:30 | CHF | Real Retail Sales Y/Y Dec | |

| Forecast: 0.90% | Previous: 0.70% | ||

| 08:55 | EUR | Germany Unemployment Change Jan | |

| Forecast: 10K | Previous: 5K | ||

| 08:55 | EUR | Germany Unemployment Rate Jan | |

| Forecast: 5.90% | Previous: 5.90% | ||

| 09:00 | CHF | Credit Suisse Economic Expectations Jan | |

| Forecast: | Previous: -23.7 | ||

| 09:00 | EUR | Italy Unemployment Dec | |

| Forecast: 7.50% | Previous: 7.50% | ||

| 13:00 | EUR | Germany CPI M/M Jan P | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 13:00 | EUR | Germany CPI Y/Y Jan P | |

| Forecast: 3.40% | Previous: 3.70% | ||

| 13:15 | USD | ADP Employment Change Jan | |

| Forecast: 143K | Previous: 164K | ||

| 13:30 | CAD | GDP M/M Nov | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 13:30 | USD | Employment Cost Index Q4 | |

| Forecast: 1.00% | Previous: 1.10% | ||

| 14:45 | USD | Chicago PMI Jan | |

| Forecast: 48.2 | Previous: 46.9 | ||

| 15:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -9.2M | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

Thursday, Feb 1, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | -1 | |

| 00:30 | AUD | Building Permits M/M Dec | 0.10% | 1.60% |

| 00:30 | AUD | Import Price Index Q/Q Q4 | 0.60% | 0.80% |

| 00:30 | JPY | Manufacturing PMI Jan F | 48.0 | 48.0 |

| 01:45 | CNY | Caixin Manufacturing PMI Jan | 50.9 | 50.8 |

| 08:30 | CHF | Manufacturing PMI Jan | 44.5 | 43.0 |

| 08:45 | EUR | Italy Manufacturing PMI Jan | 47.3 | 45.3 |

| 08:50 | EUR | France Manufacturing PMI Jan F | 43.2 | 43.2 |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 45.4 | 45.4 |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 46.6 | 46.6 |

| 09:30 | GBP | Manufacturing PMI Jan F | 46.9 | 47.3 |

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 6.40% | 6.40% |

| 10:00 | EUR | Eurozone CPI Y/Y P | 2.70% | 2.90% |

| 10:00 | EUR | Eurozone CPI Core Y/Y P | 3.20% | 3.40% |

| 12:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.25% |

| 12:00 | GBP | MPC Official Bank Rate Votes | 2--0--7 | 3--0--6 |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -20.20% | |

| 13:30 | USD | Initial Jobless Claims (Jan 26) | 211K | 214K |

| 13:30 | USD | Nonfarm Productivity Q4 P | 2.40% | 5.20% |

| 13:30 | USD | Unit Labor Costs Q4 P | 2.10% | -1.20% |

| 14:30 | CAD | Manufacturing PMI Jan | 45.4 | |

| 14:45 | USD | Manufacturing PMI Jan F | 50.3 | 50.3 |

| 15:00 | USD | ISM Manufacturing PMI Jan | 47.7 | 47.4 |

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | 45.6 | 45.2 |

| 15:00 | USD | ISM Manufacturing Employment Index Jan | 48.1 | |

| 15:00 | USD | Construction Spending M/M Dec | 0.50% | 0.40% |

| 15:30 | USD | Natural Gas Storage | -326B | |

| 21:45 | NZD | Building Permits M/M Dec | -10.60% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | 7.50% | 7.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q4 | |

| Forecast: | Previous: -1 | ||

| 00:30 | AUD | Building Permits M/M Dec | |

| Forecast: 0.10% | Previous: 1.60% | ||

| 00:30 | AUD | Import Price Index Q/Q Q4 | |

| Forecast: 0.60% | Previous: 0.80% | ||

| 00:30 | JPY | Manufacturing PMI Jan F | |

| Forecast: 48.0 | Previous: 48.0 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jan | |

| Forecast: 50.9 | Previous: 50.8 | ||

| 08:30 | CHF | Manufacturing PMI Jan | |

| Forecast: 44.5 | Previous: 43.0 | ||

| 08:45 | EUR | Italy Manufacturing PMI Jan | |

| Forecast: 47.3 | Previous: 45.3 | ||

| 08:50 | EUR | France Manufacturing PMI Jan F | |

| Forecast: 43.2 | Previous: 43.2 | ||

| 08:55 | EUR | Germany Manufacturing PMI Jan F | |

| Forecast: 45.4 | Previous: 45.4 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | |

| Forecast: 46.6 | Previous: 46.6 | ||

| 09:30 | GBP | Manufacturing PMI Jan F | |

| Forecast: 46.9 | Previous: 47.3 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Dec | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 10:00 | EUR | Eurozone CPI Y/Y P | |

| Forecast: 2.70% | Previous: 2.90% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y P | |

| Forecast: 3.20% | Previous: 3.40% | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.25% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 2--0--7 | Previous: 3--0--6 | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | |

| Forecast: | Previous: -20.20% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 26) | |

| Forecast: 211K | Previous: 214K | ||

| 13:30 | USD | Nonfarm Productivity Q4 P | |

| Forecast: 2.40% | Previous: 5.20% | ||

| 13:30 | USD | Unit Labor Costs Q4 P | |

| Forecast: 2.10% | Previous: -1.20% | ||

| 14:30 | CAD | Manufacturing PMI Jan | |

| Forecast: | Previous: 45.4 | ||

| 14:45 | USD | Manufacturing PMI Jan F | |

| Forecast: 50.3 | Previous: 50.3 | ||

| 15:00 | USD | ISM Manufacturing PMI Jan | |

| Forecast: 47.7 | Previous: 47.4 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Jan | |

| Forecast: 45.6 | Previous: 45.2 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Jan | |

| Forecast: | Previous: 48.1 | ||

| 15:00 | USD | Construction Spending M/M Dec | |

| Forecast: 0.50% | Previous: 0.40% | ||

| 15:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: -326B | ||

| 21:45 | NZD | Building Permits M/M Dec | |

| Forecast: | Previous: -10.60% | ||

| 23:50 | JPY | Monetary Base Y/Y Jan | |

| Forecast: 7.50% | Previous: 7.80% | ||

Friday, Feb 2, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q4 | 1.90% | 1.80% |

| 00:30 | AUD | PPI Y/Y Q4 | 3.80% | |

| 07:45 | EUR | France Industrial Output M/M Dec | 0.20% | 0.50% |

| 13:30 | USD | Nonfarm Payrolls Jan | 178K | 216K |

| 13:30 | USD | Unemployment Rate Jan | 3.80% | 3.70% |

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.40% |

| 15:00 | USD | Factory Orders M/M Dec | 0.50% | 2.60% |

| 15:00 | USD | Michigan Consumer Sentiment Index Jan F | 78.8 | 78.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q4 | |

| Forecast: 1.90% | Previous: 1.80% | ||

| 00:30 | AUD | PPI Y/Y Q4 | |

| Forecast: | Previous: 3.80% | ||

| 07:45 | EUR | France Industrial Output M/M Dec | |

| Forecast: 0.20% | Previous: 0.50% | ||

| 13:30 | USD | Nonfarm Payrolls Jan | |

| Forecast: 178K | Previous: 216K | ||

| 13:30 | USD | Unemployment Rate Jan | |

| Forecast: 3.80% | Previous: 3.70% | ||

| 13:30 | USD | Average Hourly Earnings M/M Jan | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 15:00 | USD | Factory Orders M/M Dec | |

| Forecast: 0.50% | Previous: 2.60% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Jan F | |

| Forecast: 78.8 | Previous: 78.8 | ||

The Weekly Bottom Line: Feds, BoC Steal This Show This Week

U.S. Highlights

- The U.S. economy ended 2023 on a solid note, with GDP rising 3.3% quarter-over-quarter (annualized) – smashing expectations for a more moderate gain of 2%.

- The consumer remained a key factor underpinning last quarter’s strength, with spending accelerating sharply through the holiday shopping season.

- Inflation continued to drift lower in December, with the 12-month change on core PCE – the Fed’s preferred inflation measure – slipping below 3%.

Canadian Highlights

- The Bank of Canada held their policy rate at 5% this week, while making minor tweaks to their forecasts. Messaging accompanying the decision pointed to no change in rates for the time being.

- Markets have priced in a rate cut in June. Our own call sees rates beginning to move lower in the second quarter.

- The federal government announced a cap on international student visas this week. This will weigh on consumption and offer some relief to Canada’s rental market.

U.S. – The Final Approach

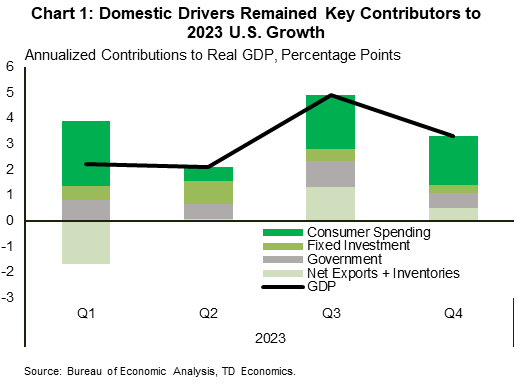

The latest data has shown the U.S. economy had all the markings of a soft landing as 2023 drew to a close. Economic growth held up better than expected, the labor market is coming back into better balance, and price pressures are quickly abating. Market pricing on the timing of the first Fed rate cut has seesawed between March and May in recent months, with March currently priced as a coin-toss. But with progress on the inflation front showing no signs of stalling, market sentiment remained in risk-on mode this week, with the S&P 500 edging up 1% for the week, reaching yet another all-time high. Shorter-term yields drifted a bit lower, leading to a further flattening in the yield curve. At the time of writing, the inversion of the 10Y-2Y spread had narrowed to just -20bps – well off the peak inversion of -110bps seen back in July.

The Bureau of Economic Analysis’ advance estimate of fourth quarter real GDP came in at 3.3%, a downshift from Q3’s blistering 4.9%, but well above the consensus forecast calling for a more moderate gain of 2%. Economic resilience remained on full display, with the consumer, private investment, and government spending accounting for the lion’s share of last quarter’s gain (Chart 1). While the rearview mirror isn’t always the best guide to the road ahead, the solid end to last year provides a more favorable starting point heading into 2024.

This is especially true for the consumer. The monthly income and spend figures for December – released a day after the GDP report – showed consumer spending accelerated sharply through the holiday shopping season. This was happening even though the tailwinds from excess savings had slowed from the gale force gust felt at the beginning of the tightening cycle to just a gentle breeze by the end of last year. At the same time, 27 million student loan borrowers were faced with the harsh reality of having to restart regular loan repayments in October following the expiration of the three-year student loan moratorium. But neither of these factors appear to have phased the consumer, as a still sturdy labor market has continued to support meaningful gains in real income and help to sustain a healthy pace of consumer spending.

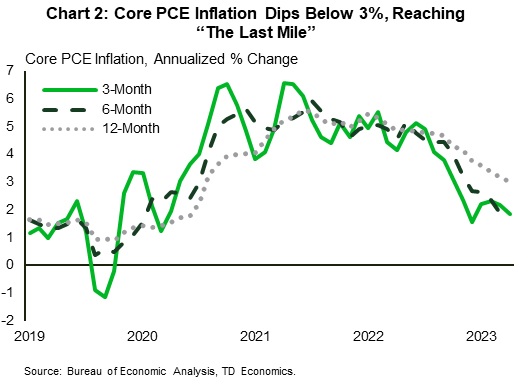

The puzzle has been on the inflation front. Despite the economy continuing to run well above its long-run potential through H2’2023, inflation has still made incredible progress. As of December, the 12-month rate of change on core PCE fell to 2.9%, while the annualized 3-and-6-month rates slipped to 1.5% and 1.9%, respectively (Chart 2). Falling goods prices and some cooling in non-housing services have both been the key contributors to the recent downward pressure on inflation.

From the Fed’s perspective, time (and the economic data) remain on their side. With the economy showing no signs of keeling over, and the labor market still relatively tight, policymakers can afford to be patient. Fed officials will want to see at least a few more ‘soft’ readings on inflation and a bit more easing in the labor market before pulling the trigger on rate cuts.

Canada – Feds, BoC Steal This Show This Week

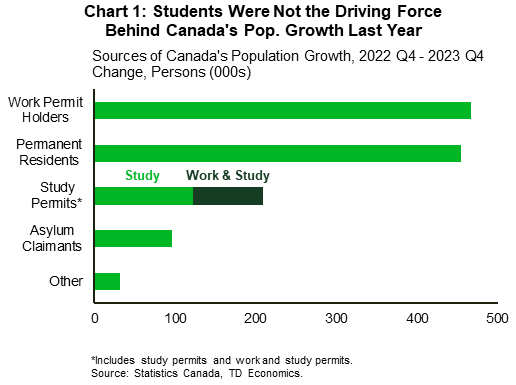

Multigenerational highs in Canada's population growth have strained the country's social systems and inflamed the country's housing crisis. In view of these challenges (and others), the federal government announced a cap on international students. The idea is that in the fall of this year, the number of student visas will be rolled back to 2022 levels, and some estimates suggest that this could lower the student intake by at least 200k spots over time. To put this figure in perspective, it would amount to roughly 20% of Canada's massive population inflow in 2023.

This will undoubtedly sap some steam from Canada's frothy population growth. This weaker growth will then weigh on consumption and housing. On the latter, the policy should slow down rent growth relative to its prior trajectory. However, it's tough to envision a large-scale cool down in rents this year. Note that even if this policy begins to weigh on population growth this year, it was newcomers with work permits (not students) who were largely responsible for Canada's population surge last year (Chart 1). What's more, immigration levels (untouched by the policy) remain robust.

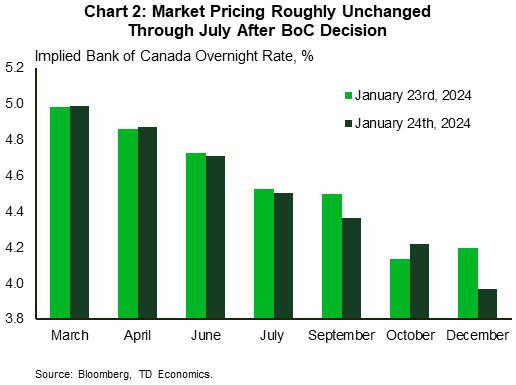

The even bigger news this week for financial markets was the Bank of Canada's interest rate decision. There are a handful of important takeaways. First, the Bank of Canada left their policy rate on hold, as expected. Second, their inflation and economic growth forecasts were little changed from the prior report. Notably, the Bank still sees headline inflation falling to 2.4% by the end of this year and 2.1% by the final quarter of 2025. These projections match our own. However, we see the economy posting weaker growth in 2024 and 2025, with rising debt service costs keeping the pressure on Canada's highly indebted households. Third, the statement accompanying the decision was a touch more dovish than October, and Governor Macklem's opening remarks after the decision noted that no further tightening will be required if their forecast evolves as expected. Fourth, the Bank took great pains to acknowledge that shelter costs will be a "material headwind" against the return of inflation to its target. These costs do complicate the Bank's inflation fight, as they are partly due to factors beyond the Bank's control, and policymakers will seemingly not "look through" them when setting policy. Fifth, Governor Macklem acknowledged the broad range of inflation indicators that the Bank is looking at to get a sense of underlying inflation, even if the preferred measures are CPI-trim and CPI-median. This could offer the Bank some degree of optionality on how they frame the trend in inflation moving forward.

The Bank's interest rate decision didn't meaningfully sway the markets' rate expectations, at least over the next few meetings (Chart 2). June remains the likeliest month for the first rate cut, in the mind of markets. Our own expectation is that policymakers will be in position to cut their policy rate sometime in the second quarter of this year.

Weekly Economic & Financial Commentary: Almost Everything Coming Up Roses

Summary

United States: Almost Everything Coming Up Roses

- Data released this week garnered further optimism that the economy can power through the Federal Reserve's efforts to corral inflation—an endeavor the Fed could increasingly be construed as achieving. Economic activity ended the year on better footing than expected, and inflation continued its deceleration.

- Next week: Construction Spending (Thu.), ISM Manufacturing (Thu.), Employment (Fri.)

International: Foreign Central Banks at the Forefront

- It was a busy week for foreign central banks. The Bank of Japan appears to be on course for an April rate hike, while a dovish Bank of Canada announcement suggested the risks are tilted toward an earlier initial rate cut than our June base case. We still forecast an initial rate cut from the European Central Bank in April, though we acknowledge that risks for a later June move do exist.

- Next week: China PMIs (Wed.), Bank of England Policy Rate (Thu.), Eurozone CPI (Thu.)

Interest Rate Watch: In a Holding Pattern

- As discussed in our Fed Flashlight report released this week, we share the near-universally held view that the FOMC will leave the fed funds rate and pace of quantitative tightening (QT) unchanged at its upcoming meeting on January 31.

Credit Market Insights: Increased Borrowing in the Beige Book

- In the most recent Beige Book released by the Fed, a majority of the 12 Federal Reserve Districts reported little or no change in economic activity, reflecting the continuing resilience of the economy. However, closer examination of this month’s Beige Book reveals the cracks that are beginning to emerge in the economy, particularly for household borrowing.

Topic of the Week: Sea of Red

- The recent Houthi militant attacks in the Red Sea have thrown a wrench in global supply chains. Container ship spot rates have jumped as capacity is stretched and popular trade routes are diverted around the southern tip of Africa. For the U.S., the impact may be more muted as businesses look to be in far better shape to weather any potential supply disruption today.

Canada’s November GDP to Edge Higher for First Time Since May But Economy Still Looks Weak

The November Canadian gross domestic product (GDP) estimate released on Wednesday will probably tick higher for the first time in six months, but the economic backdrop to end 2023 still looks soft.

We expect a 0.1% increase in GDP from October, which would be in line with Statistics Canada’s early estimate a month ago. These advance estimates have been prone to revisions. Still, data released since for November has largely been consistent with a tick higher in output. Retail sale volumes edged lower in November, but manufacturing and wholesale sale volumes rose (by 1.6% and 0.6% month-over-month, respectively) and oil production in Alberta increased.

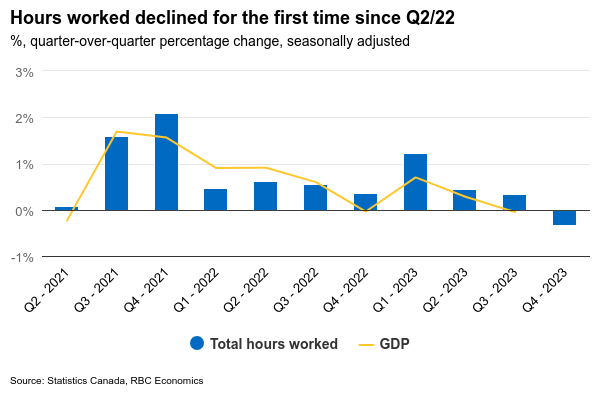

Still, other indicators have been softer. Employment continued to rise through the end of last year, but actual hours worked declined for the first time in Q4 since the early days of the pandemic (Q2/2020). The early estimate of December manufacturing sales was down 0.6%.

The economic growth data looks substantially weaker on a per-capita basis after controlling for still rapid population growth. We continue to expect a small decline in Q4 GDP once all the numbers have been counted, but even a small increase would leave output per person down for a sixth consecutive quarter.

The labour market also still looks substantially softer with the unemployment rate up 0.8 percentage points since spring 2023. The Bank of Canada has referenced the softer economic backdrop as the reason additional interest rate hikes this year are unlikely and we continue to expect a pivot to gradual cuts by mid-year.

Week ahead data watch

The U.S. Federal Reserve is widely expected to hold the fed funds target range unchanged for a fourth consecutive meeting on Wednesday. Attention will be focused on any hints on the potential timing of a pivot to cuts. Another round of strong GDP data in Q4 showed that the economy is still weathering higher interest rates better than expected. But slowing price growth is leaving the Fed with flexibility to hold the line on interest rates for now – and to respond with lower rates later this year (we expect before mid-year) once the economy starts to soften more significantly.

Next Friday, we will get the first U.S. jobs report for 2024. Payroll employment is likely up by 195K in January, slightly below the 216K in December. The unemployment rate should continue to edge up to 3.8% from 3.7% in December, reflecting some easing conditions in the labour market.