Sample Category Title

BoJ holds steady, with CPI core-core projected at 1.9% in next two fiscal years

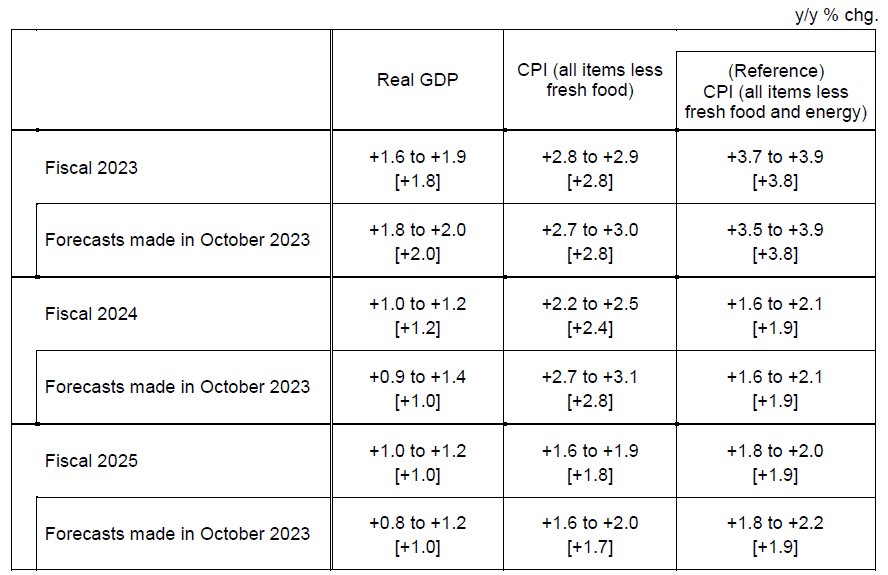

BoJ left monetary policy unchanged as widely expected. The forecast for fiscal 2024 CPI core was downgraded, whereas fiscal 2025 CPI core forecast saw a slight upgrade. Notably, CPI core-core forecasts for fiscal 2024 and 2025 were left unchanged at 1.9%, indicating a steady path towards achieving Japan's 2% inflation target sustainably.

Under Yield Curve Control, BoJ kept short-term policy interest rate unchanged at -0.1%. Additionally, target for 10-year JGB yield remains around 0%, with an allowance for fluctuation below 1.0% upper bound. These decisions were made by unanimous vote.

BoJ noted, "Consumer inflation is likely to increase gradually toward the BoJ's target as the output gap turns positive, and as medium- to long-term inflation expectations and wage growth heighten." The central bank also acknowledged the growing "likelihood" of realizing this outlook, albeit with an emphasis on the continued "high uncertainties" surrounding future developments.

In the median economic projections:

- Fiscal 2023 GDP growth at 1.8% (down from October's 2.0%).

- Fiscal 2024 GDP growth at 1.2% (up from 1.0%).

- Fiscal 2025 GDP growth at 1.0% (unchanged).

On the inflation front:

- Fiscal 2023 CPI core at 2.8% (unchanged).

- Fiscal 2024 CPI core at 2.4% (down from 2.8%).

- Fiscal 2025 CPI core at 1.8% (up from 1.7%).

- Fiscal 2023 CPI core-core at 3.8% (unchanged).

- Fiscal 2024 CPI core-core at 1.9% (unchanged).

- Fiscal 2025 CPI core-core at 1.9% (unchanged).

AUD/USD Faces Major Hurdle, Can It Recover?

Key Highlights

- AUD/USD declined below 0.6650 and tested the 0.6525 zone.

- A major bearish trend line is forming with resistance near 0.6610 on the 4-hour chart.

- EUR/USD is consolidating losses near the 1.0900 zone.

- Crude oil prices might start another increase above the $75.50 resistance.

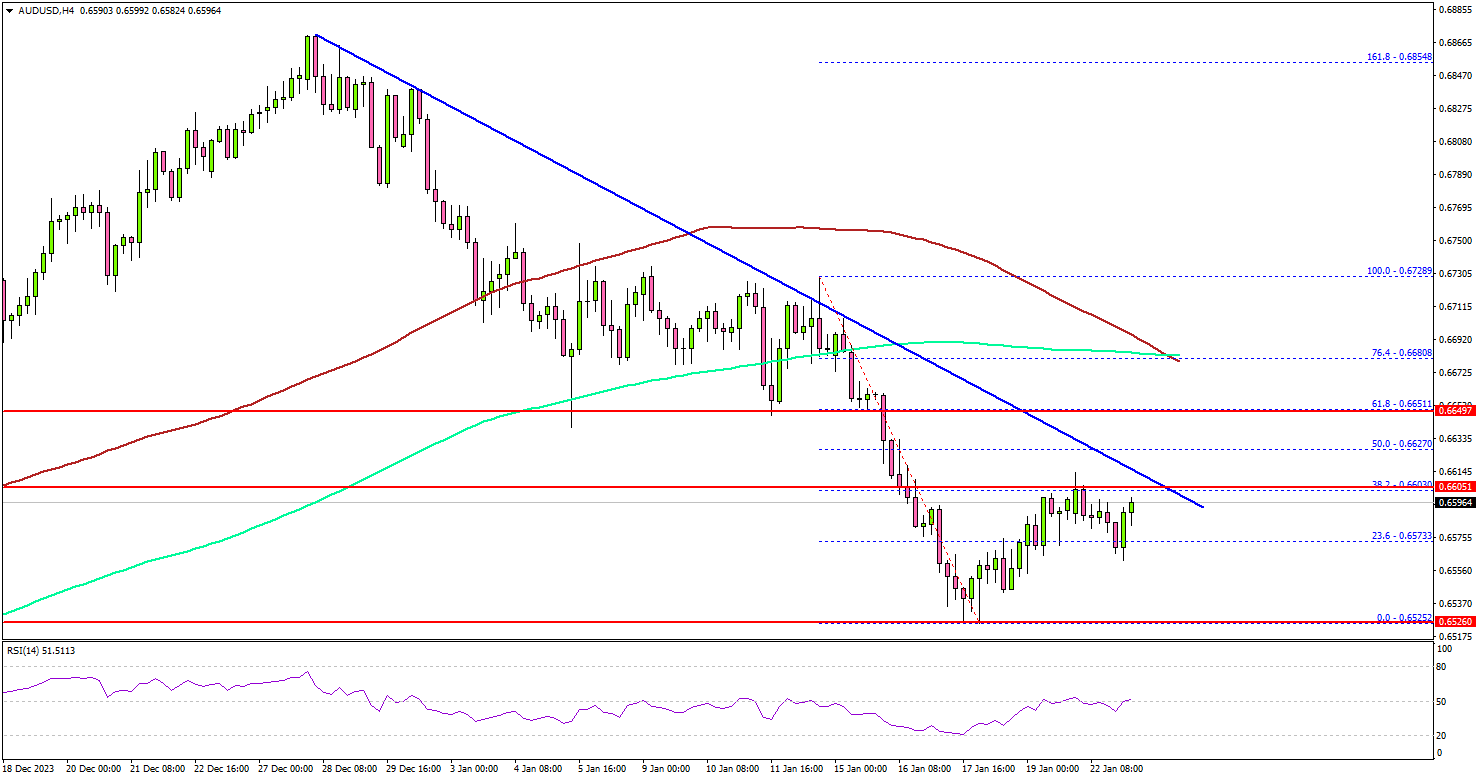

AUD/USD Technical Analysis

The Aussie Dollar started a major decline from well above 0.6800 against the US Dollar. AUD/USD dropped below the 0.6650 and 1.0920 levels to enter a bearish zone.

Looking at the 4-hour chart, the pair settled below the 0.6620 level, the 100 simple moving average (red, 4 hours), and the 200 simple moving average (green, 4 hours). Finally, the bulls appeared near the 0.6525 level.

A low was formed near 0.6525 and the pair is now attempting a recovery wave. There was an increase above the 0.6575 resistance. It cleared the 23.6% Fib retracement level of the downward move from the 0.6728 swing high to the 0.6525 low.

On the upside, the pair is facing resistance near the 0.6610 level. There is also a major bearish trend line forming with resistance near 0.6610 on the same chart.

The next key resistance is near the 0.6650 zone or the 61.8% Fib retracement level of the downward move from the 0.6728 swing high to the 0.6525 low. A close above the 0.6650 zone could open the doors for more upsides. The next stop for the bulls might be 0.6685.

If there is no move above 0.6610, the pair might continue to move down. Immediate support is seen near the 0.6575 level. The first major support is near the 0.6650 level.

The next major support sits near the 0.6525 region. A downside break below the 0.6525 zone could spark another sharp decline. The next major support is 0.6465 below which the pair might decline and test 0.6420.

Looking at EUR/USD, the pair is consolidating losses near 1.0900 and might attempt a recovery wave in the near term.

Economic Releases

- Euro Zone Consumer Confidence for Jan 2023 (Preliminary) – Forecast -14.3, versus -15 previous.

Australia’s NAB business confidence rises to -1 amidst slowing price growth

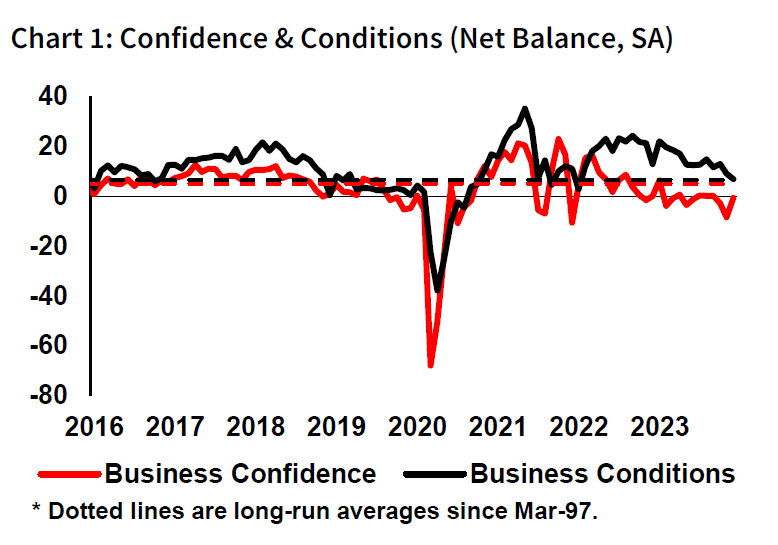

Australia NAB Business Confidence fell rose from -8 to -1 in December. However, Business Conditions fell from 9 to 7. The decline was observed across several key areas: Trading conditions dropped from 13 to 10, while Employment conditions also decreased slightly from 8 to 7. Profitability conditions remained steady at 6.

NAB Chief Economist Alan Oster noted that "confidence and conditions are softest in manufacturing, retail and wholesale," attributing this to consumers cutting back on spending over time. Although there was a pickup in confidence within the retail sector in December, Oster expressed caution, stating that "it remains to be seen if this will be maintained."

Another significant development was the sharp decline in price and cost growth. Labor cost growth eased to 1.8% in quarterly equivalent terms, down from 2.3%. Purchase cost growth also declined from 2.5% to 1.6%. Overall price growth slowed from 1.2% to 0.9%, with notable decrease in retail price growth from 1.8% to 0.6%.

Oster highlighted the significance of this decline in retail price growth, attributing it in part to the sales periods around Black Friday and Christmas. He remarked, "The marked fall in retail price growth in December... is nonetheless an encouraging sign that inflation may have eased at the end of the quarter."

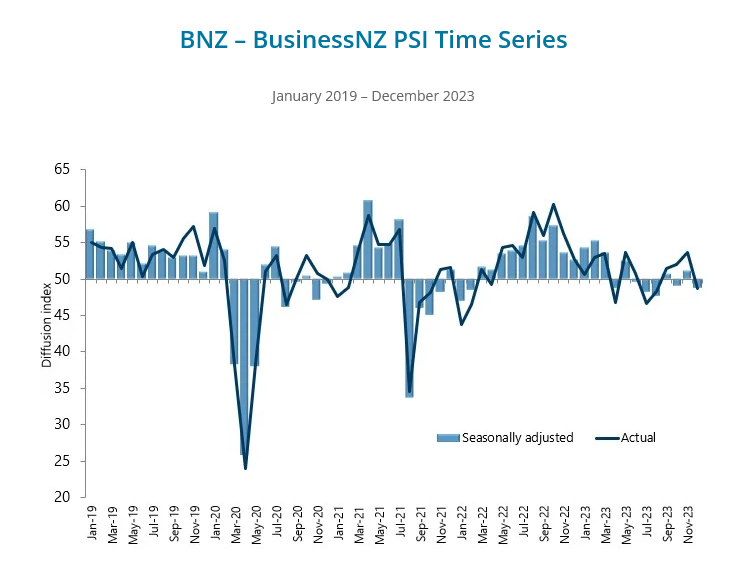

New Zealand BNZ services falls to 48.8, back in contraction

New Zealand BusinessNZ Performance of Services Index fell from 51.1 to 48.8 in December, back into contraction territory. This downturn also brings the index below long-term average of 53.4. The increase in negative sentiment is evident, with the proportion of negative comments rising from 54.0% to 58.7%. The primary concerns expressed by businesses revolve around seasonal factors, increasing costs of living, and an overall economic slowdown.

Breaking down the PSI, several key components showed declines. Activity and sales dropped from 48.7 to 47.1, employment fell from 50.6 to 47.5, and new orders/business dipped from 52.2 to 51.2. Additionally, stocks and inventories decreased from 55.0 to 51.5, while supplier deliveries also saw a reduction from 52.8 to 50.5.

Stephen Toplis, BNZ's Head of Research noted that the softening in PSI, combined with the previously reported weakness in Performance of Manufacturing Index, paints a concerning picture for New Zealand's near-term economic growth and employment. While tourism has been a critical driver for the services sector and is expected to continue supporting the economy, Toplis emphasized that it cannot solely bear the burden of economic revitalization.

JPY: Bulls Eagerly Await the BOJ’s Move

The yen has experienced significant fluctuations in recent weeks, initially gaining ground against the weakening US dollar in December but subsequently losing those gains as the dollar rebounded in January. USD/JPY reached 148.80 on Friday, the highest level since November 28, prompting concerns that if the yen continues to depreciate, the Ministry of Finance might intervene to support it, especially if it breaches the 150 level.

The upcoming policy meeting of the Bank of Japan (BoJ) on Tuesday adds a layer of uncertainty. While the market does not anticipate a change in policy settings, surprises from the BoJ are not unprecedented. Although expectations are for the BoJ to eventually move away from negative interest rates, the prevailing economic conditions, recent earthquake impacts, and upcoming national wage negotiations in March suggest that the April meeting might be more conducive for significant policy announcements. Even if the BoJ maintains its current stance in the upcoming meeting, investors will closely analyze various factors, including updated inflation reports and quarterly economic projections.

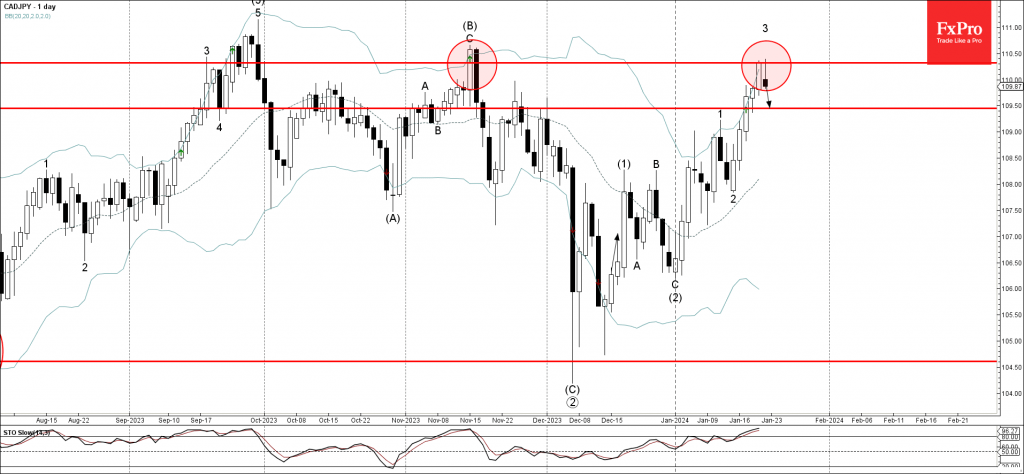

CADJPY - D1 Timeframe

CADJPY on the Daily timeframe seems to be setting up for a reversal in the trend. From the price action on the chart, it is evident that price is currently trading within a supply zone, with a likely QMR (Quasimodo Reversal) being formed. The presence of a trendline that overlaps the supply zone serves as an extra confirmation of the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: 108.631

- Invalidation: 110.732

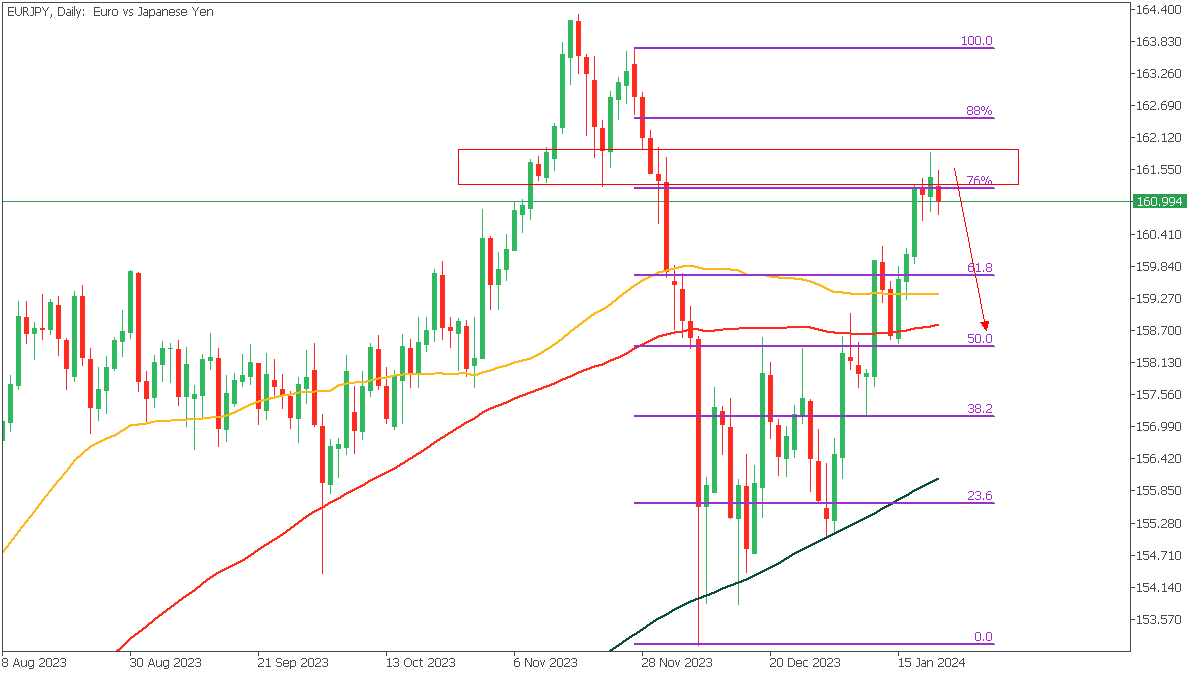

EURJPY - D1 Timeframe

EURJPY is currently trading around 76% of the Fibonacci retracement and can be seen to be under a lot of bearish pressure from the supply zone. On the lower timeframes, I would prefer to see a clear break of structure in order to confirm the validity of my sentiment - remember that.

Analyst’s Expectations:

- Direction: Bearish

- Target: 158.762

- Invalidation: 161.976

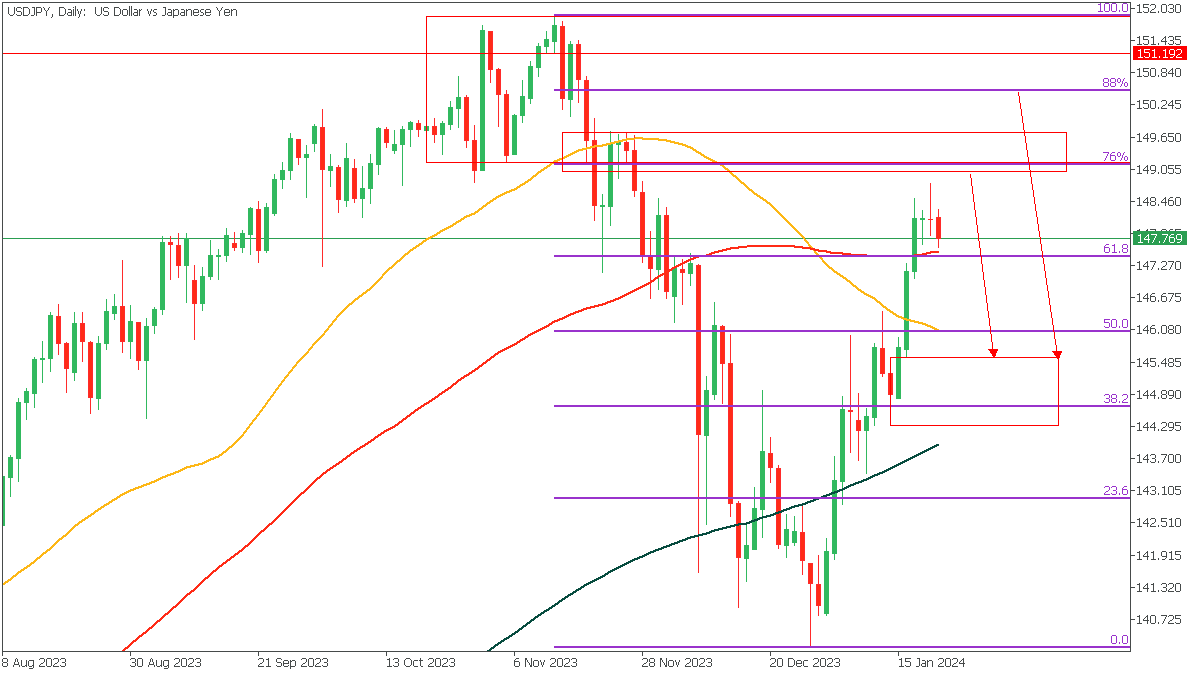

USDJPY - D1 Timeframe

As for USDJPY, I have two key areas of interest that I will be watching keenly. I want to patiently watch for the reaction that price ends up making at either of these levels before taking my entry. As you can tell, both areas sync well with the 76% and 88% of the Fibonacci retracement level, so we can wait to confirm which of the two presents a stronger case.

Analyst’s Expectations:

- Direction: Bearish

- Target: 145.662

- Invalidation: 149.832

CONCLUSION

The trading of CFDs comes at a risk. Thus, to succeed, you have to manage risks properly. To avoid costly mistakes while you look to trade these opportunities, be sure to do your due diligence and manage your risk appropriately.

CADJPY Wave Analysis

- CADJPY reversed from key resistance level 110.00

- Likely to fall to support level 109.50

CADJPY currency pair recently reversed down from the key resistance level 110.00, which stopped the previous wave (B) in the middle of November, as can be seen below.

The resistance level 110.00 was strengthened by the upper daily Bollinger Band. The pair is currently forming the daily Shooting Star.

Given the strength of the resistance level 110.00 and the overbought daily Stochastic, CADJPY can be expected to fall further to the next support level 109.50.

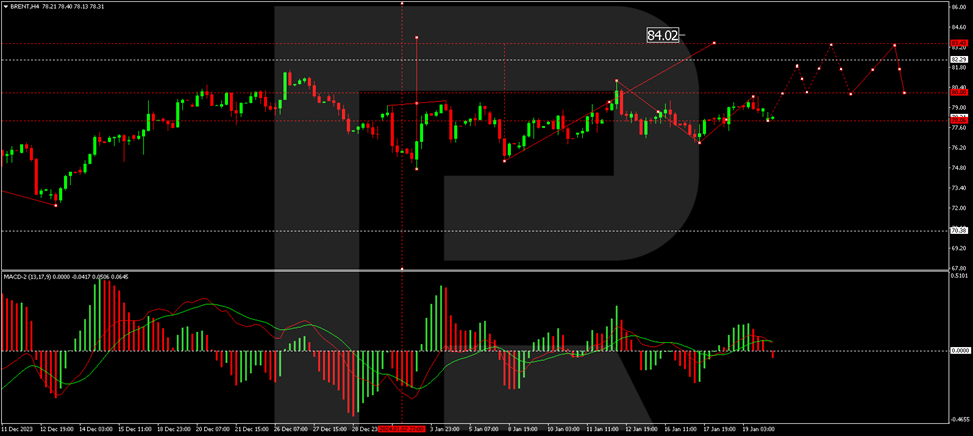

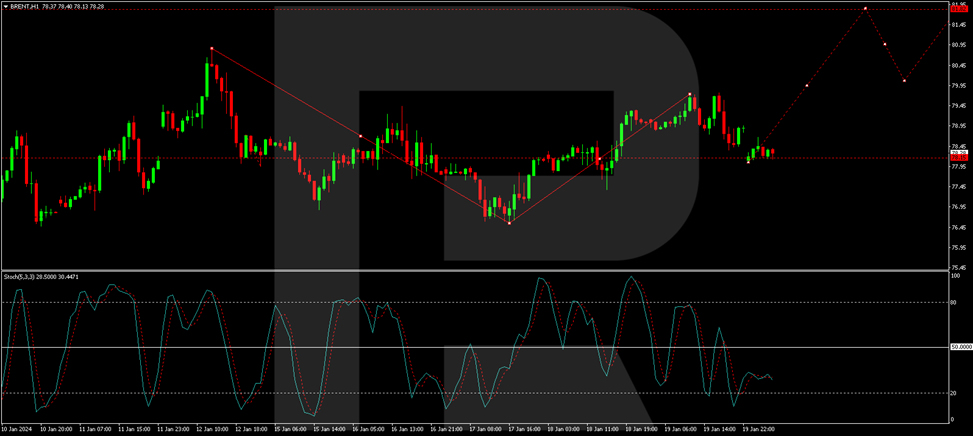

Brent Crude Oil Prices Inch Upwards Amid Demand Speculations

Brent crude oil prices are witnessing a moderate rise as the week begins, with the cost per barrel currently near $78.40. This upward trend is primarily influenced by the evolving outlook on energy demand. Recent macroeconomic data have cast some doubts on future demand, somewhat offsetting factors previously buoying prices, such as tensions in the Middle East.

Currently, Brent crude seems poised for a phase of consolidation within a specific price range. Despite some existing downward pressures, the ongoing geopolitical tensions in the Red Sea and the Gulf of Aden are maintaining a significant risk premium in crude oil prices. Market dynamics are also reflected in the backwardation between the current Brent price and its six-month futures, suggesting an anticipation of potential future oil supply limitations.

Brent Crude Oil Technical Analysis

The H4 chart for Brent indicates a recent rise to $79.74, followed by a correction to $78.06. It's likely that a tight consolidation range will form above this level today. A break above this range could signal a growth trajectory towards $80.00, and potentially higher to $81.84 as a local target. The MACD indicator, with its signal line positioned above zero, supports the likelihood of continued growth.

On the H1 chart, a correction phase appears to have concluded. The price may start ascending towards $79.79. Following this, a new consolidation phase around this level is anticipated. An upward breakout from this range could propel the price further to $81.84. This outlook is reinforced by the Stochastic oscillator, indicating a signal line trajectory from above 20, aiming towards 80.

Sunset Market Commentary

Markets

European stocks were off for a blazing start in the wake of new record highs on Wall Street (S&P 500, Down Jones) end last week. The EuroStoxx50 gapped >1% higher at the open before losing some momentum. US equities open higher as well, resulting in new highs for the major indices but the Nasdaq. Risk assets are still buoyed by market believe of economies slowing down enough to cool inflation while avoiding a painful recession. Such a scenario gives central banks all the reasons to kick off the monetary easing cycle. Core bond yields indeed slip several basis points today. German bonds outperform US Treasuries. Yields on the former had some minor catching up to do with a late-session swoon in US yields last Friday. Net daily changes currently vary between -4.2 bps (30-y) to -6.9 bps (-5y). The 10-year’s break above the 38.2% resistance level (2.32%) last week therefore doesn’t receive technical confirmation just yet. US yields are down 0.8 bps (2-y) to -3.8 bps (10-y). Using a magnifying glass, we spot some JPY outperformance on currency markets. Tomorrow morning’s BoJ meeting could upend that soon if governor Ueda keeps postponing (hints on) policy normalization. The main reason is that the central bank is not yet seeing enough signs of inflation getting anchored around the 2% target as long as there’s no virtuous cycle between wage and price growth. Prime minister Kishida today called upon companies for larger wage hikes, saying the country is at a critical point for escaping from deflation. USD/JPY eases to 147.47 after a blistering rally last week and, more broadly, all off 2024. EUR/JPY loses some ground to 160.88. Other cross rates including EUR/USD barely budge. EUR/GBP is back towards testing the 0.856 support area (December lows). A break would pave the way towards the August low of 0.849. This is not our preferred scenario

The European Union will tap the bond market tomorrow. It announced a dual tranche transaction comprising an increase of the EU 3.125% December 2030 and of the EU 3% March 2053 benchmark lines. The syndicated transaction is one of the six planned for the first half of 2024 along with seven bond auctions. The EU seeks to issue €75bn of long-term bonds during this period while setting the annual limit for all of 2024 at €160bn. The proceeds will be used to meet payments primarily related to NextGenerationEU (including possible payments under REPowerEU).

News & Views

Belgian consumer confidence fell from 0 to -2 in December, posting a first monthly decline since May. After last month’s rebound, household expectations for the general economic situation in Belgium deteriorated significantly (-14 from -9). On the other hand, consumers’ opinion on the trend in unemployment over the next twelve months remains unchanged (14). On a personal level, they expressed a bit more caution about their future financial situation (-1 from 1). Moreover, they revised their saving intentions very slightly upwards (21 from 20). Consumer confidence remains above its long term average of around -6. Belgian business confidence will be published on Thursday.

Polish retail sales (constant prices) rose by 11% M/M in December (vs 14.8% consensus). Compared with a year earlier, sales are down 2.3% (vs consensus +1.9% forecast). The decline was driven by an 11% decline in the sales of household goods, an 8.3% drop in newspapers, books and other sales in specialized stores, as well as a 6.4% fall in the sales of fuel. Average gross wages increased by 4.7% M/M & 9.6%Y/Y (vs 7.1% M/M & 12.1% Y/Y expected).

New Zealand Dollar Eyes Services PSI

- New Zealand releases Performance of Services Index on Tuesday

The New Zealand dollar is flat at the start of the week. In the European session, NZD/USD is trading at 0.6116, up 0.01%. It was a rough week for the New Zealand dollar, which declined 2% and fell to a five-week low.

New Zealand’s economy has struggled in the fourth quarter and the gauge of services activity, the Performance of Services Index (PSI) posted three contractions in the second half of 2023. The PSI improved to 51.2 in November, up from 49.2 in October, indicating weak growth. We’ll get a look at the December report on Tuesday.

China maintains benchmark lending rates

With global inflation on the decline, major central banks have likely ended their rate-tightening cycles and are looking to lower interest rates. In China, the central bank (PBOC) has been under pressure to lower rates due to the economic slowdown and deflationary pressures which have pushed up real borrowing costs. The PBOC has stood pat, not wanting to put further pressure on the yuan, which has fallen 1.4% in January against the dollar. The PBOC kept the one-year loan prime rate (LPR) at 3.45% and the five-year LPR at 4.20% on Monday, as expected. The decrease in economic activity is bad news for New Zealand, as China is its largest trading partner.

What a difference a week can make. In the case of Fed rate odds, the markets have become less confident that the Fed will press the rate-cut trigger in March. Just one week ago, the probability stood at 78% but that has fallen to 48% at present, according to the CME’s FedWatch tool. The Fed has pushed back against market expectations of six rate cuts this year, starting in March. Last week, Atlanta Fed President Bostic said he did not expect rate cuts until the third quarter and San Francisco Fed President Daly said the Fed would have to be “patient” about rate cuts.

NZD/USD Technical

- 0.6150 and 0.6211 and are the next resistance lines

- There is support at 0.6054 and 0.5993