Sample Category Title

USDJPY Trades Sideways Ahead of BoJ Meeting

- USDJPY consolidates near its almost 2-month high

- RSI and MACD lose ground but stay in positive zones

USDJPY has been in a steady advance since its five-month bottom of 140.24 registered in late December, posting consecutive higher highs. However, the rally seems to have taken a breather in the past few four-hour sessions as momentum indicators suggest that bullish pressures are fading.

Should the pair reverse lower, immediate support could be found at 147.44, which is the 61.8% Fibonacci retracement of the 151.89-140.24 downleg. Further retreats could then come to a halt at the 50.0% Fibo of 146.07. Even lower, the 38.2% Fibo of 144.69 may provide downside protection.

Alternatively, if buying pressures re-emerge, the price might revisit its recent peak of 148.78. Conquering this barricade, the bulls could attack the 78.6% Fibo of 149.40. A violation of that zone might pave the way for the October resistance of 150.76.

In brief, USDJPY appears to be in a consolidation mode ahead of the BoJ meeting on Tuesday. Any surprises there are likely to put an end to the rangebound pattern.

USD/JPY Flat Ahead of BoJ Announcement

- Bank of Japan to make announcement on Tuesday

The Japanese yen is in a holding pattern on Monday as the Bank of Japan holds a two-day meeting today and Tuesday. In the European session, EUR/USD is trading at 148.05, down 0.08%.

The yen has been on a rollercoaster in recent weeks. In December, the yen took advantage of a slumping US dollar and surged 4.85%. Those gains have been squandered as the dollar has rebounded in January and jumped 5.1%. On Friday, USD/JPY touched a high of 148.80, its highest level since November 28. The 150 level is not too far away and if the yen continues to lose ground, concerns will mount that the Ministry of Finance could intervene to prop up the yen.

Bank of Japan unlikely to make a move on Tuesday

The Bank of Japan will wrap up its policy meeting on Tuesday, and any hints of a shift in monetary policy would likely send the yen sharply higher. The markets aren’t expecting the central bank to change policy settings, although the BoJ, which isn’t known for transparency, has surprised the markets before.

The BoJ is expected to abandon negative rates, but Tuesday’s meeting doesn’t seem to be the right timing. Inflation has been easing and the economy remains fragile. The major earthquake on January 1 has contributed to the markets lowering expectations of a policy shift at this meeting. As well, the national wage negotiations take place in March and the BoJ would prefer to analyse the results of the wage talks before making any policy changes. This would point to the April meeting as being more ripe for a major announcement. Even if the BoJ stays on the sidelines tomorrow, investors will have plenty to digest, including updated inflation reports, quarterly economic projections and Governor Ueda’s follow-up press conference.

USD/JPY Technical

- USD/JPY tested resistance at 148.28 earlier. Above, there is support at 148.71

- There is support at 147.74 and 147.31

USD/JPY: Yen Pauses in Anticipation of Bank of Japan’s Decision

In 2024, the yen has significantly depreciated against other currencies. The USD/JPY chart indicates that since the first trading day of January, the exchange rate has risen by more than 5%. However, since the 18th, there has been a lull, and it may be disrupted today or tomorrow due to the Bank of Japan's meeting, during which comments on monetary policy will be provided.

According to Reuters, traders expect that interest rates will not be raised, remaining in the negative territory. This expectation is based on recent "peaceful" comments from the Bank of Japan, coupled with the country facing a serious test in the form of an earthquake on the west coast.

Today's technical analysis of USD/JPY suggests that buyers may have lost momentum as the price approached the psychological level of 150 yen per dollar. Judging by the long upper shadow (indicated by the arrow) on January 19, selling forces were activated. This could be attributed to either profit-taking by buyers after the rally in the first half of January or the opening of new short positions.

Pay attention to an important resistance zone (shown in blue). The bearish breakthrough occurred around the 149.3 level, confirming bearish dominance at the end of the previous year. It is possible that this dominance may persist, supporting the idea that the current calm may be disrupted in favour of the bears.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

New Year, Old Habits for the BoC?

- BoC meets on Wednesday; decision to be announced at 14.45 GMT

- Market wants a dovish show, but BoC might not be ready for such a shift

- Loonie could find its footing again against the US dollar

Bank of Canada meets on Wednesday

The week will be dominated by central bank meetings with the first BoC gathering for 2024 coming on Wednesday. The market does not expect any significant announcements but would clearly enjoy a dovish meeting that could open the door to rate cuts down the line. The BoC is seen cutting by around four times in 2024 with the first 25bps rate move fully priced in by June 5, 2024. It is worth noting that the BoC has amended its communication procedures with the decision being published 15 minutes earlier than usual i.e. at 14.45 GMT and a press conference held, 45 minutes after the decision, at every meeting.

What has changed since early December 2023?

The December 6, 2023 gathering was a touch more dovish compared to the October 2023 meeting but far less than anticipated by certain market analysts. No press conference was hosted but both the Governor Macklem and the BoC member Gravelle were quite explicit in their post-meeting appearances that (1) the BoC wants to see a number of months of sustained downward momentum in core inflation, (2) it is too early to consider cutting rates and (3) the housing sector remains a big hurdle and plays a key role in the recently elevated inflation rates.

By examining the data flow since December, it is evident that no significant progress has been made on any front. Inflation for the month of December edged higher to a yearly increase of 3.4% with the prices subcomponent of the December Ivey PMI survey remaining north of 60. However, producer and raw material price indices continue to record negative yearly changes, thus setting the scene for possibly weaker price pressure down the line.

The housing sector remains a grave issue

On an equal footing, the housing sector remains a key input in the BoC’s deliberations. BoC member Gravelle devoted an entire speech in mid-December on the housing sector with the end-product being that the low supply of new homes is keeping shelter price inflation high and thus feeding through to national CPI.

Having said that, a central bank cannot directly affect the supply of new homes, but it could slow down the economy and reduce the demand for borrowing by keeping rates at current high levels for a considerable amount of time. That would probably be the outcome of Wednesday’s meeting i.e. no rate change and anticipation until inflation makes the BoC-desirable dip, barring a major surprise.

Quarterly projections matter

A small surprise could come at the quarterly Monetary Policy Report (MPR) and more specifically at the 2025 inflation projection. The October MPR had headline inflation dropping to 2.1% by the fourth quarter of 2025. Therefore, a downward revision to this figure would be the strongest signal yet that rate cuts are coming at some stage in 2024.

In addition, any BoC comments on the developments in the Middle East with its oil prices implication, could upset the market. A price war would be particularly bad for the oil-rich Canada but to a certain extent it might not displease the BoC, as lower growth would cool inflation, provided of course that such an event proves short-lived.

Could the loonie reverse its underperformance against the US dollar?

The aggressive correction recorded during the November-December 2023 period is a distant memory as in the past 20 days the US dollar has managed to rally around 2.5% against the loonie. It is currently trading below a busy area which is populated by the 50- and 200-day simple moving averages (SMAs).

A hawkish show on Wednesday could allow the loonie bulls to regain the market reins and aim for the next key support area at the 38.2% Fibonacci retracement of the April 5, 2022 – October 13, 2022 uptrend at 1.3375. On the flip side, should the BoC decide to make a dovish turn, then the US dollar-loonie pair could finally manage to overcome the busy 1.3482-1.3504 area.

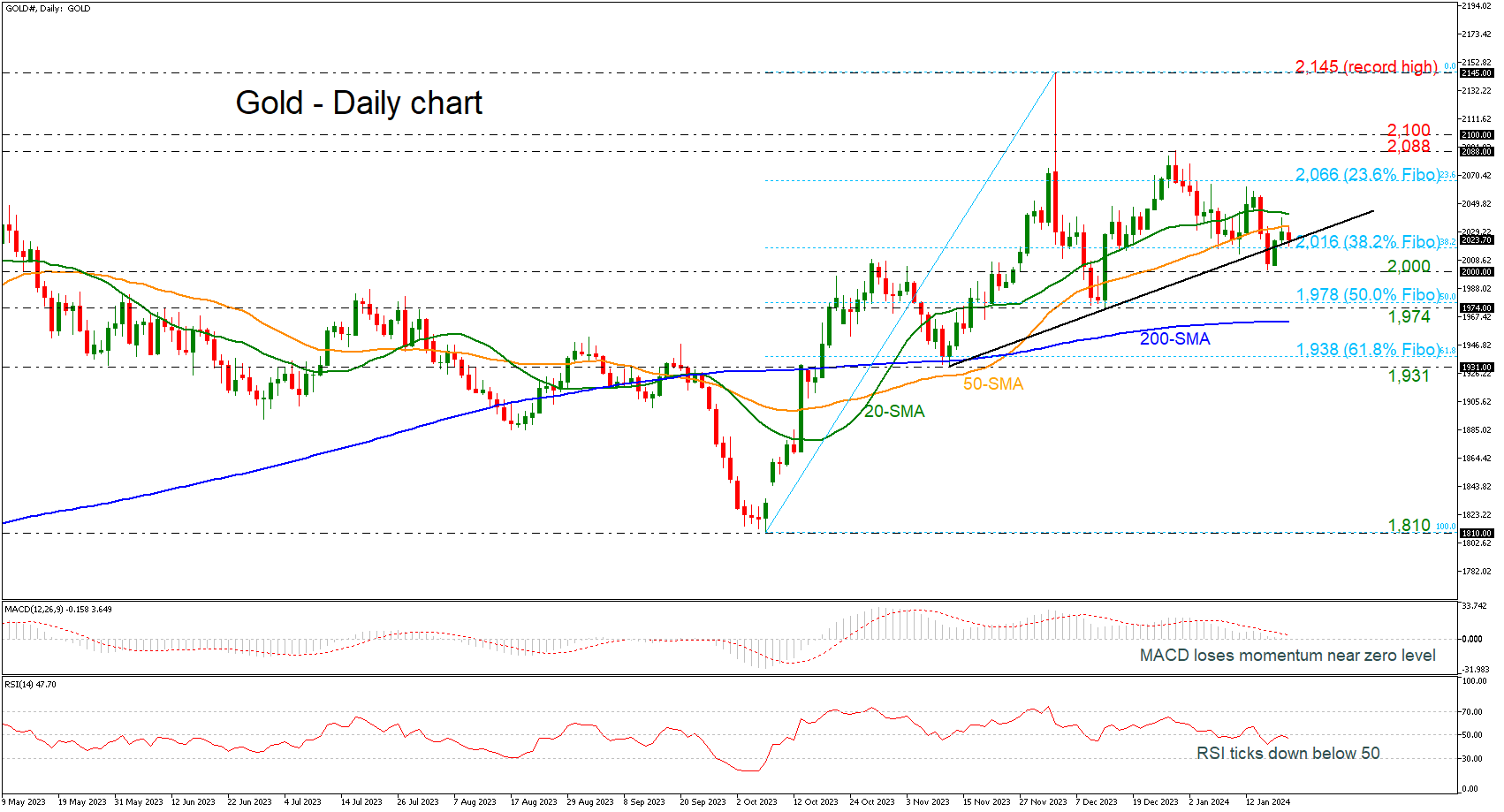

Gold Lower; Tests Key Trendline

- Gold is lower again today

- Holds beneath short-term SMAs

- Momentum indicators disappoint below mid-levels

Gold prices are fighting with the short-term uptrend line, which has been drawn since mid-November, and the 38.2% Fibonacci retracement level of the upward wave from 1,810 to 2,145 at 2,016.

Also, the market is failing to surpass above the 20- and the 50-day simple moving averages (SMAs), indicating weak momentum. The MACD oscillator is moving lower beneath its trigger line and near the zero level, while the RSI is pointing south after the pullback off the 50 zone.

Should the bulls thirst for more upside moves, they would try to overcome the short-term SMAs and then test the resistance set by the 23.6% Fibonacci of 2,066. If successful, they could then plan their course for the 2,088-2,100 restrictive region ahead of the record high of 2,145.

On the other hand, the bears are probably keen on retaking market control and defending November’s trendline. They could then face the significant 2,000 region before resting near the busy area of the 50.0% Fibonacci of 1,978, the 1,974 support and the 200-day SMA at 1,964.

To sum up, gold bulls are trying to cancel out the current bearish move that has been in place since the 2,088 high, but the path higher remains tricky, especially due to the weak support from the momentum indicators.

Focus Shifts to First Major Central Bank Gatherings of the Year

Markets

The goldilocks outcome of January University on Michigan consumer confidence ended a week of weakness in US Treasuries (and core bonds in general). The headline figure unexpectedly jumped from 69.7 to 78.8 (vs 70.1 expected; highest level since July 2021), backed by both better current conditions and a more rosy view for the next 12 months. Both short (1y) and long term (5-10y) inflation expectations declined, respectively from 3.1% to 2.9% (lowest since early 2021) and from 2.9% to 2.8%. Daily changes on the US curve varied between +3.2 bps (2-yr) and - 3.6 bps (30-yr). The front end of the curve still underperformed as more Fed governors pushed back against aggressive rate cut pricing. Atlanta Fed Goolsbee was the latest, suggesting that markets may have put the cart before the horse on cuts. SF Fed Daly added that monetary policy and the economy are in a good place so the Fed can be patient. She thinks that it’s far too early to declare victory on inflation. The market implied probability of a March Fed rate cut fell to 40%, coming from 80% at the start of the year. US equity markets rallied into the weekend following the Michigan release, gaining 1% (Dow) to 1.70% (Nasdaq). The S&P 500 added 1.23% to a fresh all-time high. The US dollar faded into the weekend with EUR/USD closing just below 1.09.

Today’s eco calendar is completely empty. Focus shifts to first major central bank gatherings of the year. Chronologically, the Bank of Japan has a first go tomorrow. Rumours suggested downward revisions to the near term growth outlook and the near/medium term inflation outlook. Together with uncertainty related to external events like the severe earthquake, it suggests that the BoJ is in no hurry to implement a real policy U-turn (ending negative policy rates). The Japanese yen is the biggest victim of this continued soft stance in combination with new weakness in core bonds. The Bank of Canada convenes on Wednesday. December Canadian inflation data unexpectedly showed new momentum in underlying price trends, suggesting the BoC won’t be able to flag a rapid start to policy rates cuts. They could nevertheless turn somewhat more neutral as they still vowed to raise the policy rate (5%) further if needed. On Thursday, the duo of Norges Bank and ECB decide on monetary policy. A faster-thanhoped Norwegian disinflation process and a slightly stronger NOK could prompt the Norges Bank to pull its Dec 2024 first rate cut call forward in time. ECB President Lagarde pushed back against aggressive market expectations at the WEF in Davos. She suggested a first rate cut only in summer. Media concluded that European central bankers are preparing a June rate cut, with the jury still out whether June 6 can already be labelled “summer”. If not, our view, we’re talking about a July rate cut at the very earliest with markets still convinced about an April move. We expect Lagarde to hold this week’s line which should underpin this year’s trend (higher) on interest rate markets.

News and views

The European Commission will on Wednesday unveil a proposal with rules that aim boosting its power to screen and potentially block foreign investment in sensitive industries. The EC is also said considering the creation of a fund to increase development of technologies both for miliary and civil purposes. The proposal comes as the covid pandemic and geopolitical developments over the previous years highlighted Europe’s trade vulnerabilities and the region’s reliance of supplies from other countries.. According to Bloomberg, this week’s package will include five initiatives including strengthening of foreign direct investment regulation, coordination of export controls, options to support research of dual-use technologies, Ideas to improve research security and firs steps toward a new tool to control leaks of sensitive know-how to adversaries through European investments overseas.

Chinese Banks held their benchmark lending rates unchanged at 3.45% for the 1y loan prime rate and 4.20% for the 5y loan lending rate. The new pricing follows after the PBOC last week unexpectedly kept the rate on its medium term lending facility unchanged at 2.4%. This decision came even after recent data showed that the economic recovery struggles to gain further traction and as several indicators show deflationary tendencies. However, the PBOC apparently wants to avoid a further deprecation of the currency. The yuan eases marginally this morning to USD/CNY 7.1965. It finished 2023 at USD/CNY 7.10.

BoJ Poised to Offer Guidance on the Removal of Short-Term Negative Rates May Spark JPY Strength

- 10-year JGB implied volatility has tapered downwards since the implementation of flexible YCC in October 2023, lowering the odds of disorderly movements in the JGB

- Elevated demand-pull inflation (excluding fresh food & energy) in Japan may prompt BoJ to upgrade its inflation (excluding fresh food & energy) forecasts for FY 2024 & FY 2025.

- Technical analysis has detected bearish elements in USD/JPY where JPY may start to strengthen in the short term towards 146.25 and a break below it exposes 144.55 next.

Bank of Japan (BoJ) will conclude its first monetary policy meeting for 2024 tomorrow, 23 January. In the past three months, calls from the Japanese private and public sectors and even ex-BoJ officials have urged the Japanese central bank to ditch its current -0.1% short-term interest rate in place since 2016 as such a level is irrelevant and does not reflect the current fundamentals of the Japanese economy.

Since BoJ’s prior monetary policy meeting outcome on 31 October, the central bank has taken “baby steps” to guide market participants on the ending of its short-term negative interest rate policy and kickstart normalization of its current ultra-easy monetary policy stance.

BoJ has allowed more flexibility of its Yield Curve Control Programme on the 10-year Japanese Government Bond (JGB) yields as it scrapped the prior hard-capped upper limit of 1% to make it as a reference level now where BoJ’s will “nimbly conduct its market operations” around that 1% level.

Current flexible YCC model has lowered 10-year JGB implied volatility

Fig 1: 10-year JGB implied volatility with JGB futures & USD/JPY as of 19 Jan 2024 (Source: TradingView, click to enlarge chart)

This flexibility of allowing the 10-year JGB yield more breathing space to fluctuate on the upside has enabled BoJ not to be “boxed in” when it eventually removes the YCC programme as a non-committal stance to any perceived hard-capped upper limit is likely to reduce undesirable speculative activities in the JGB futures market that is likely to trigger adverse reflexive loops into other asset classes and the real economy.

The current YCC modus operandi to deter rampant speculation activities in the JGB futures market seems to be working as the implied volatility of the 10-year JGB has dropped from a high of 7.98 before the 31 October 2023’s new YCC flexible implementation to 3.79 as of last Friday, 19 January (see Fig1).

Forward guidance will be key for tomorrow as demand-pull inflation remains elevated

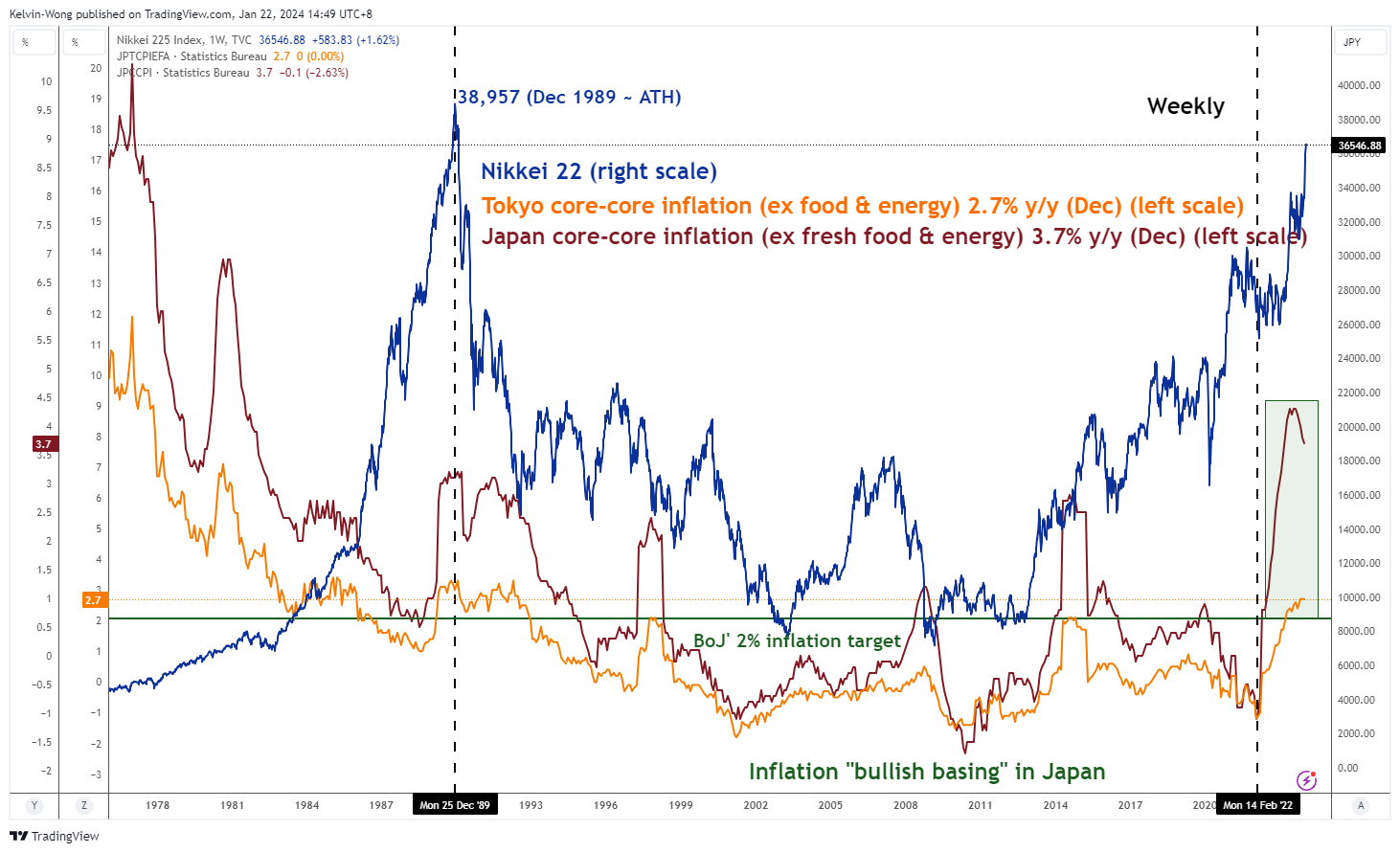

Fig 2: Tokyo & Japan core-core inflation trends with Nikkei 225 as of 22 Jan 2024 (Source: TradingView, click to enlarge chart)

In the run-up to tomorrow’s BoJ monetary policy decision outcome, market participants have toned down significantly the expectations of the removal of short-term negative interest rates due to the recent Japan’s Noto earthquake that occurred at the start of the new year. Right now, expectations on BoJ’s stance to scrap short-term negative interest rates have shifted down the calendar to the next meeting in April where BoJ will also have the release of preliminary results of annual wage negotiations between unions and companies that are still ongoing till the end of March. Stable and rising wages are key criteria for Japan to enable a forceful and sustainable exit from its decade-plus of deflationary spiral according to BoJ Governor Ueda.

Even though inflation growth has eased off in December due to cost-push factors such as lower oil prices as indicated by the Tokyo and nationwide Japan CPI data, demand-pull related inflation excluding fresh food and energy in Japan has remained elevated at 3.7% y/y, a 42-year high, and above BoJ’s 2% target for the 15th consecutive month. Services inflation in Japan also grew by 2.3%y/y for the second consecutive month in December, its fastest pace in three decades.

Therefore, market participants will be scrutinizing the BoJ’s monetary policy statement, its latest inflation projections in its updated quarterly outlook report as well as BoJ Ueda’s press conference for hints of “comfortability” to finally set the stage for the removal of short-term negative interest rates.

In the previous quarterly outlook released in October, BoJ upgraded its inflation forecasts (excluding fresh food & energy) to 1.9% y/y for fiscal years 2024 and 2025 from 1.7% y/y and 1.8% y/y respectively. A further potential upgrade on inflation (excluding fresh food & energy) towards 2% y/y for 2024 and 2025 suggests a potential signal to the market that the end of short-term negative interest rate is imminent and baby steps are in the pipeline for the normalization of ultra-easy monetary policy.

Watch the 149.30 key short-term resistance on USD/JPY

Fig 3: USD/JPY short-term minor trend as of 22 Jan 2024 (Source: TradingView, click to enlarge chart)

The recent 5-day rally of USD/JPY from 12 January to 19 January 2024 intraday high of 148.81 has started to show signs of exhaustion ahead of tomorrow’s risk event (BoJ’s monetary policy decision outcome).

The hourly RSI momentum indicator has flashed out a bearish divergence signal at its overbought region while its daily price actions as of the close of last Friday, 19 January have formed a bearish daily “Spinning Top” candlestick pattern after prior three consecutive appearances of bullish candlesticks right below a key short-term pivotal resistance at 149.30.

The intermediate support zone will be at 147.30/146.25 and a break below 146.25 may trigger a potential impulsive down move sequence to expose the next support at 144.55 (also 50-day and 200-day moving averages) in the first step.

On the other hand, a clearance above 149.30 invalidates the bearish tone to see the next intermediate resistance coming in at 150.20/70.

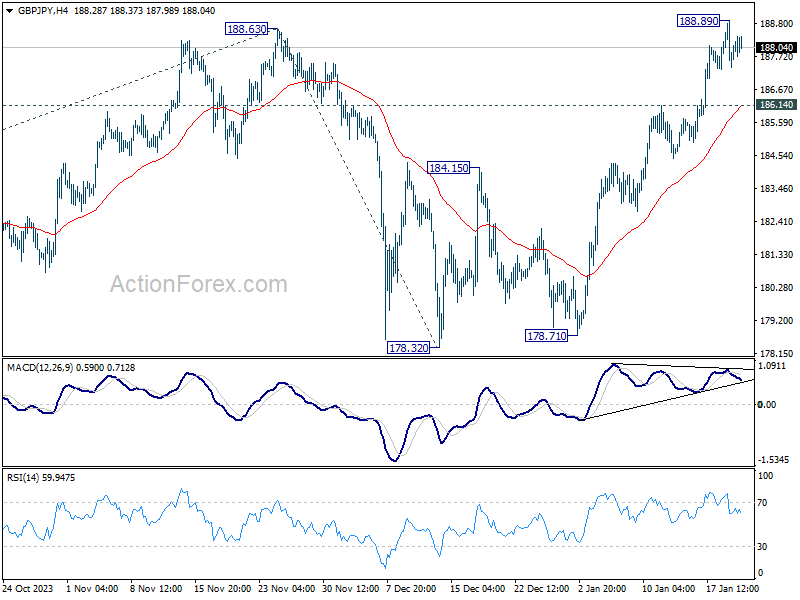

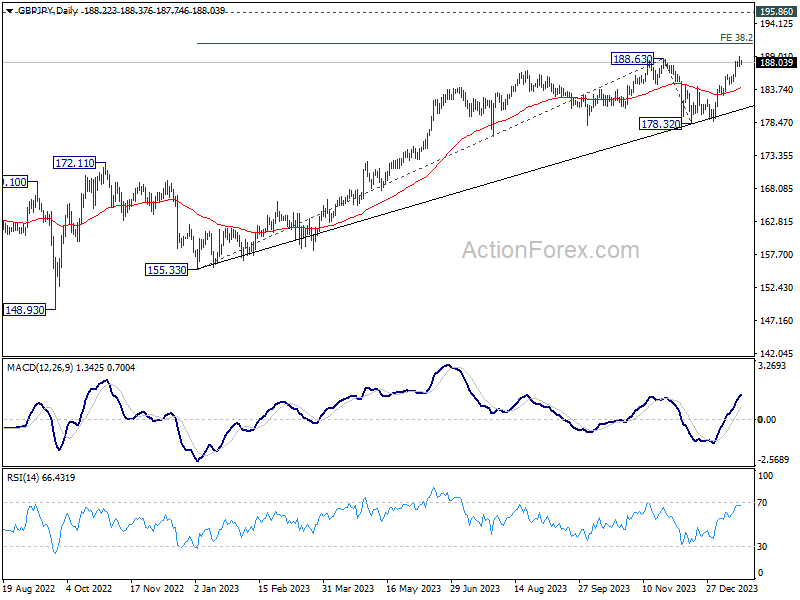

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.63; (P) 187.94; (R1) 188.57; More...

Intraday bias in GBP/JPY is turned neutral first with a temporary top formed at 188.89. Further rally is expected as long as 186.14 resistance turned support holds. ON the upside, break of 188.89, and sustained trading above 188.63 will confirm up trend resumption. Next target is 38.2% projection of 155.33 to 188.63 from 178.32 at 191.04.

In the bigger picture, up trend from 123.94 (2020 low) in in progress. Medium term outlook will stay bullish as long as 178.32 support holds. Next target is 195.86 long term resistance (2015 high).

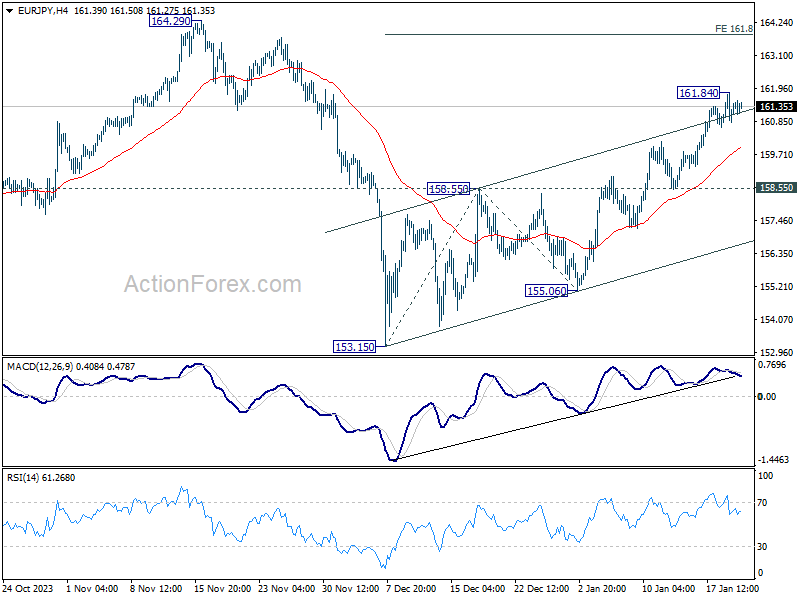

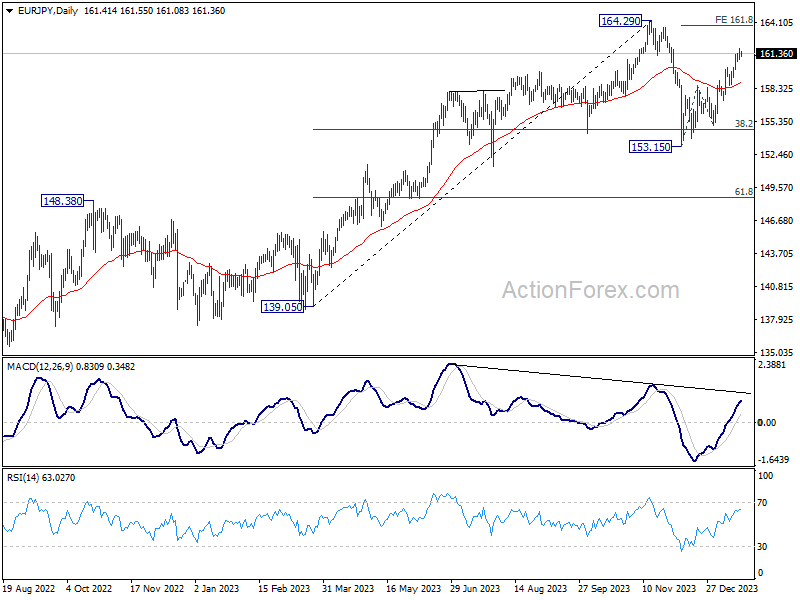

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.90; (P) 161.38; (R1) 161.95; More...

Intraday bias in EUR/JPY is turned neutral with a temporary top formed at 161.84. Some consolidations could be seen first. But even in case of deep retreat, further rally is expected as long as 158.55 resistance turned support holds. On the upside, break of 161.84 will resume whole rally from 153.15 to 161.8% projection of 153.15 to 158.55 from 155.06 at 163.79, which is close to 164.29 high.

In the bigger picture, price actions from 164.29 medium term top are seen as a correction to rise from 139.05 only. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) is expected to resume through 164.29 at a later stage.

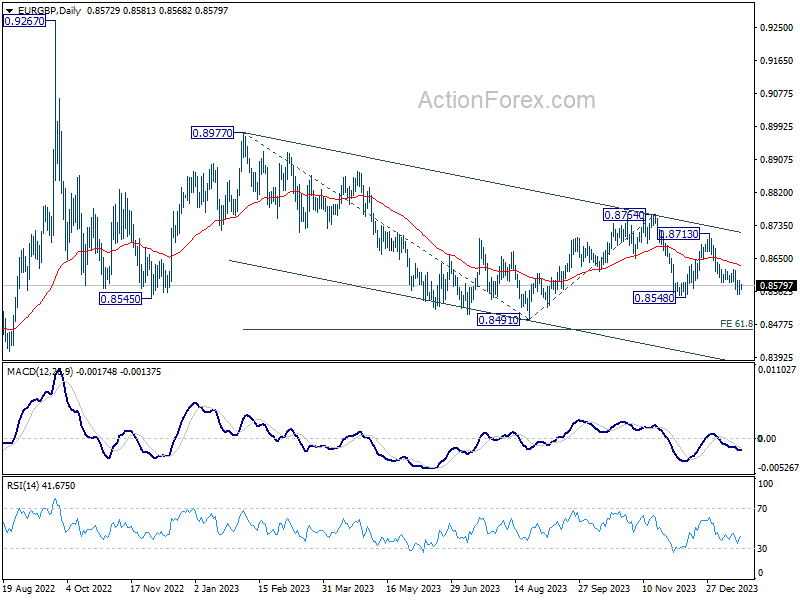

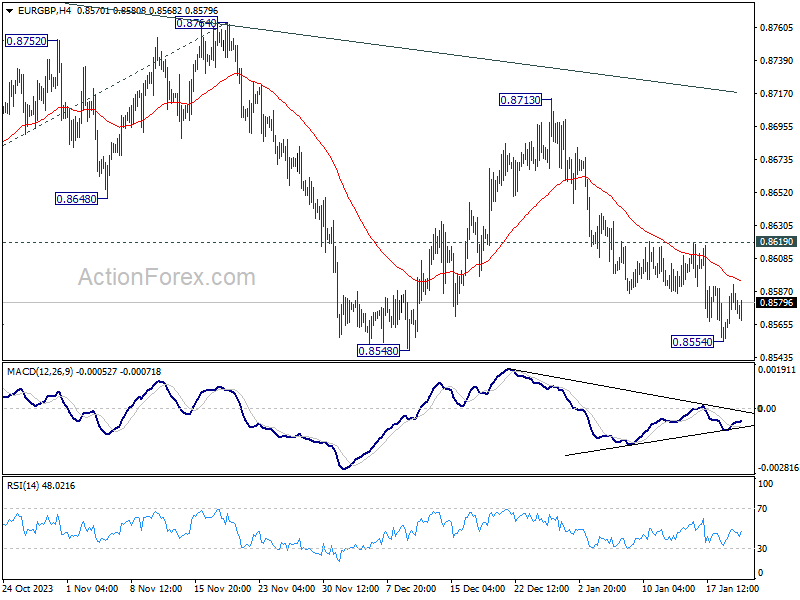

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8555; (P) 0.8574; (R1) 0.8597; More...

Intraday bias in EUR/GBP remains neutral at this point. Further decline is expected as long as 0.8619 resistance holds. On the downside, decisive break of 0.8548 will indicate that larger down trend is ready to resume through 0.8491 low. However, break of 0.8619 will dampen this bearish view and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8713 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.