Sample Category Title

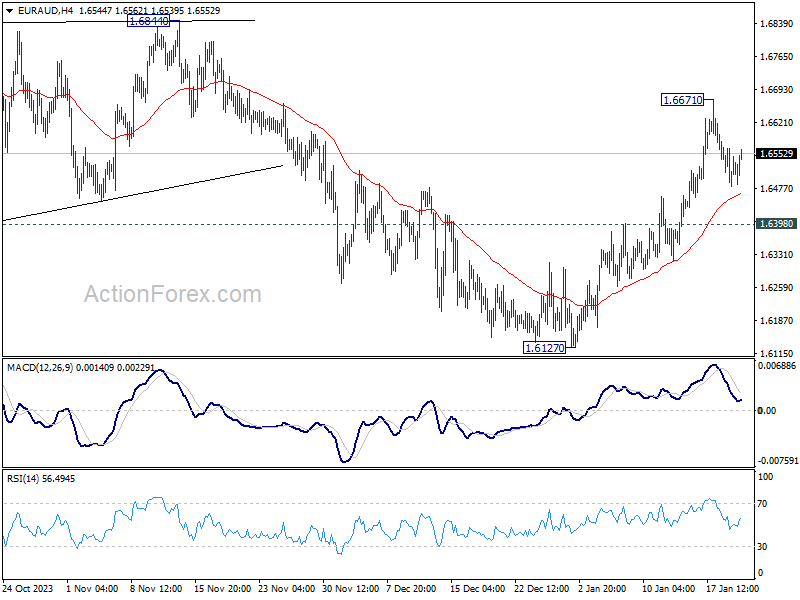

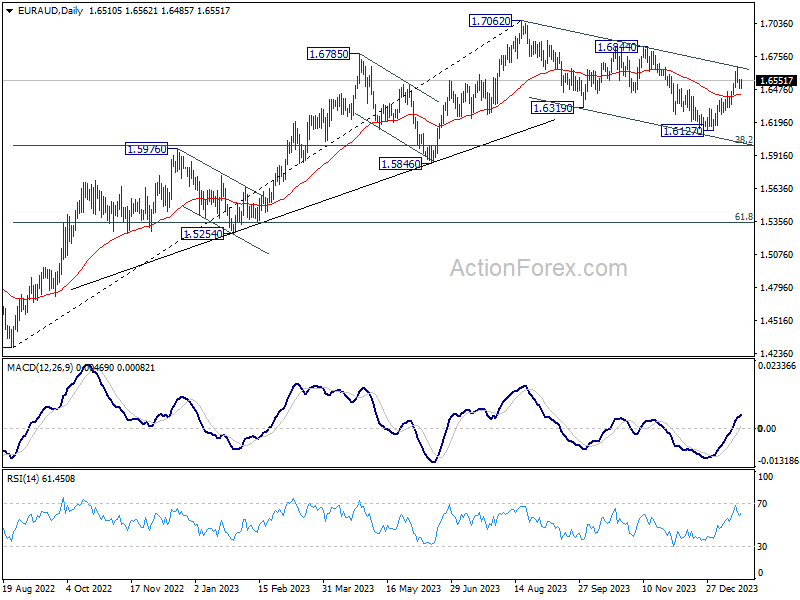

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6477; (P) 1.6523; (R1) 1.6564; More...

Intraday bias in EUR/AUD remains neutral for the moment, as consolidation from 1.6671 is extending. Further rise is expected as long as 1.6398 support holds. Corrective fall from 1.7062 should have completed with three waves down to 1.6127 already. Above 1.6671 will target 1.6844 resistance to confirm this bullish case.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Break of 1.6844 resistance will argue that this up trend is ready to resume through 1.7062 high. In case of another fall, strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound.

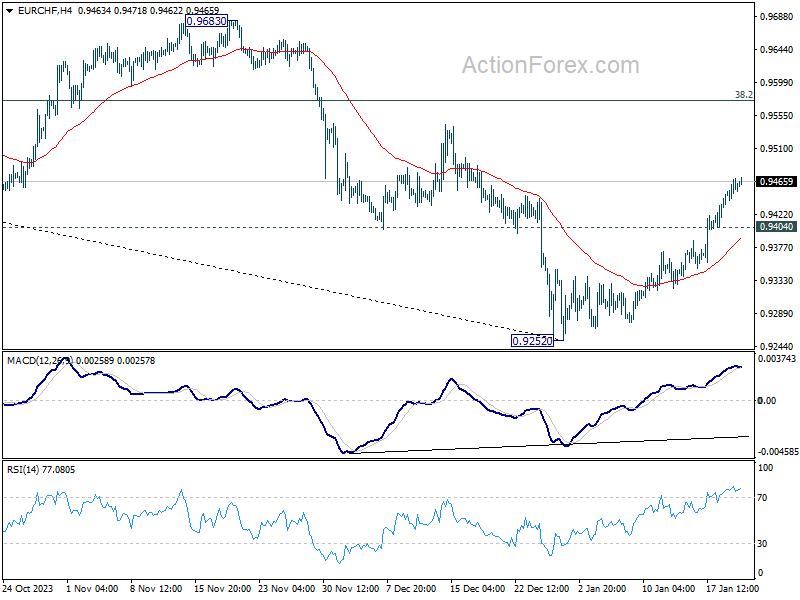

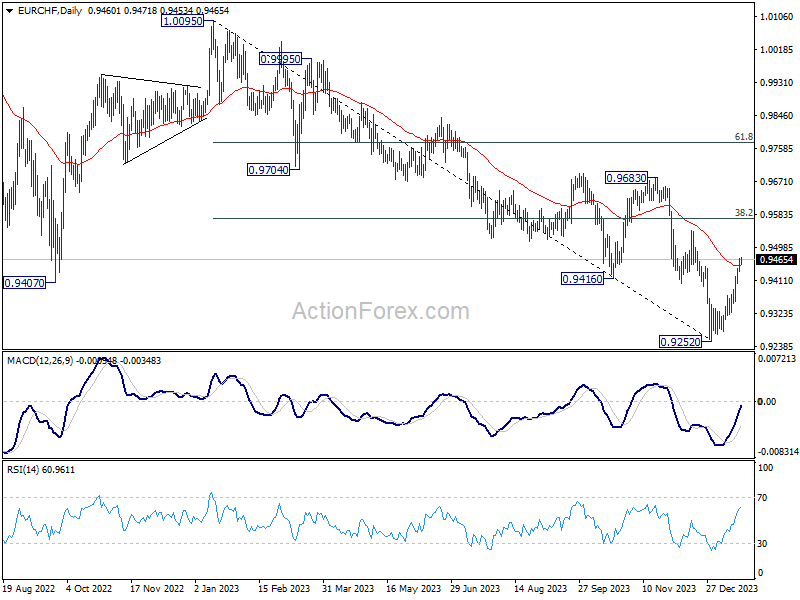

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9440; (P) 0.9456; (R1) 0.9475; More...

Intraday bias in EUR/CHF stays on the upside for the moment. Rebound from 0.9252 is seen as correcting whole down trend from 1.0095. Further rally should be seen to 38.2% retracement of 1.0095 to 0.9252 at 0.9574. On the downside, below 0.9404 minor support will turn intraday bias neutral first.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Another decline is in favor after rebound from 0.9252 completes. However, firm break of 0.9683, and sustained trading above 55 W EMA (now at 0.9659) will argue that EUR/CHF is already in a medium term rally, even as a corrective move.

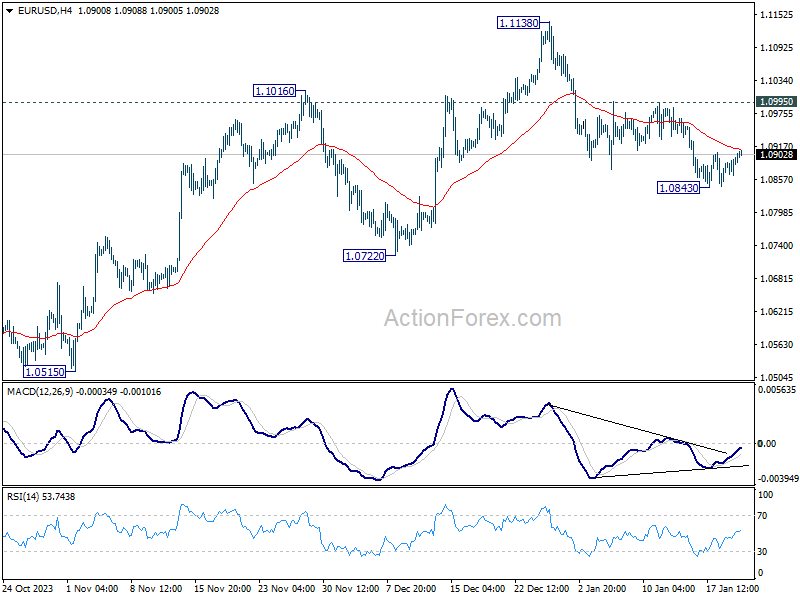

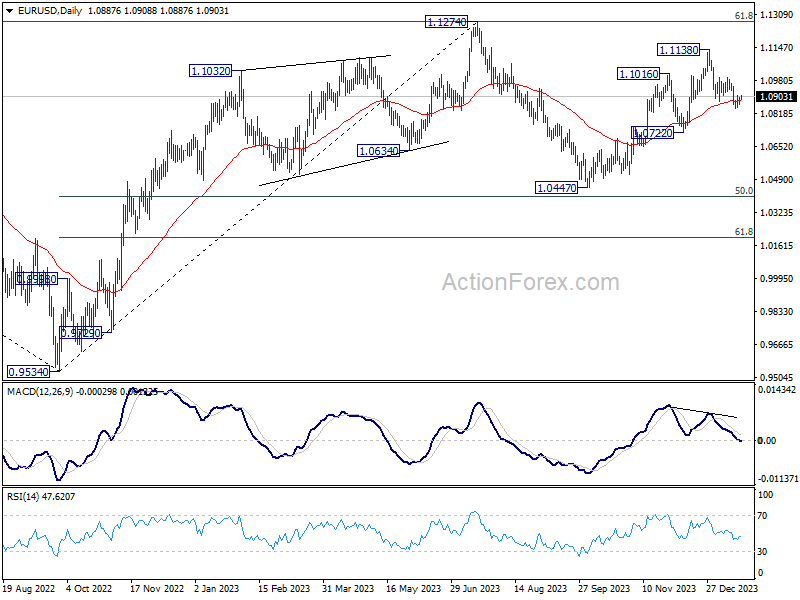

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0877; (P) 1.0888; (R1) 1.0908; More...

Intraday bias in EUR/USD remains neutral for consolidation above 1.0843 temporary low. But further decline is expected as long as 1.0995 resistance holds. Below 1.0843 will target 1.0722 support next. Decisive break there will argue that whole rise from 1.0447 has completed, and target this low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

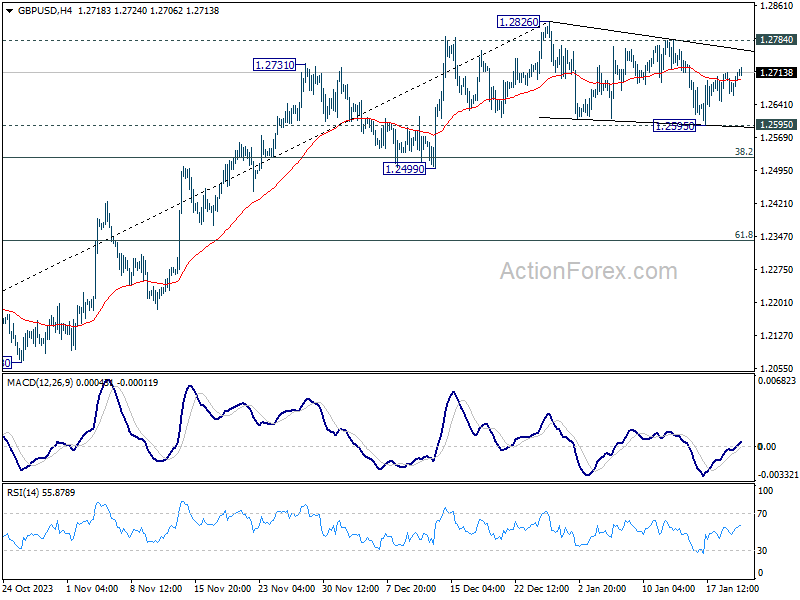

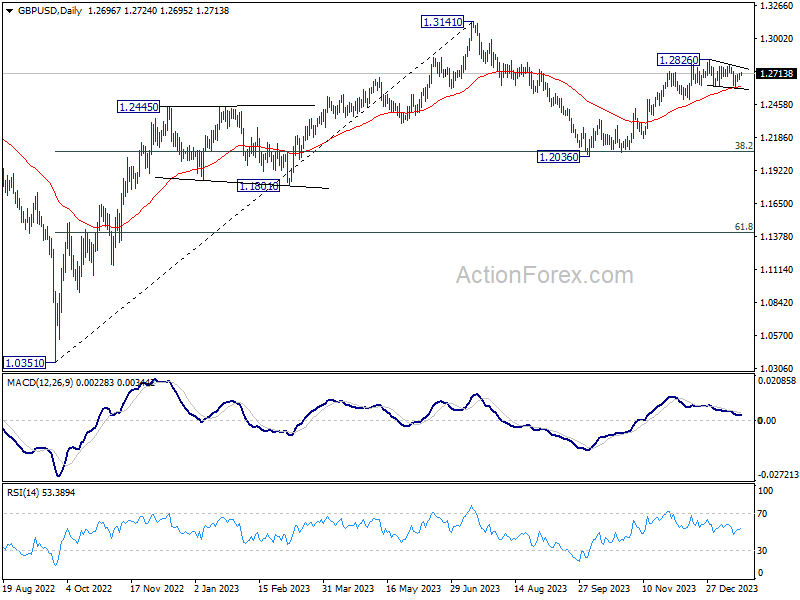

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2672; (P) 1.2694; (R1) 1.2725; More...

Intraday bias in GBP/USD stays neutral for the moment. Consolidation pattern from 1.2826 could extend further. Break of 1.2595 support will target 1.2499 support. On the upside, however, firm break of 1.2784 resistance will suggest that the consolidation pattern has completed. Further rally should then resume through 1.2826 towards 1.3141 high.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

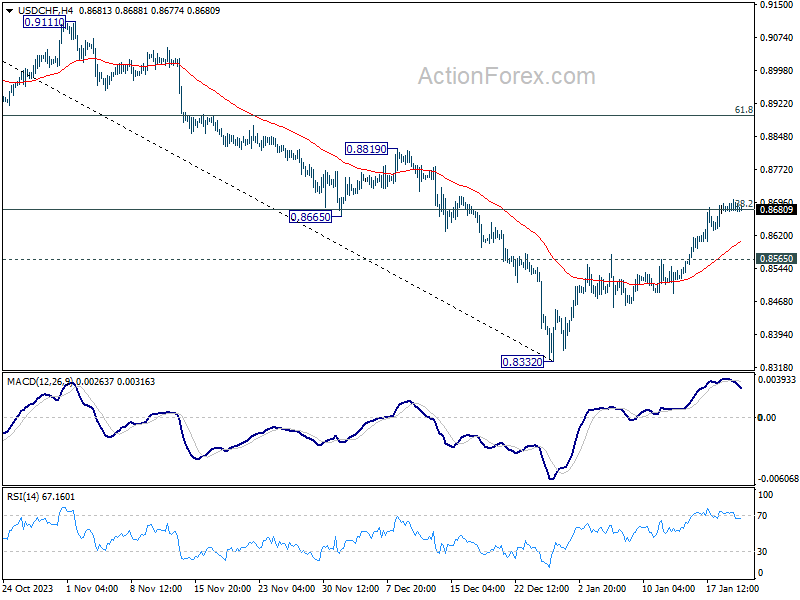

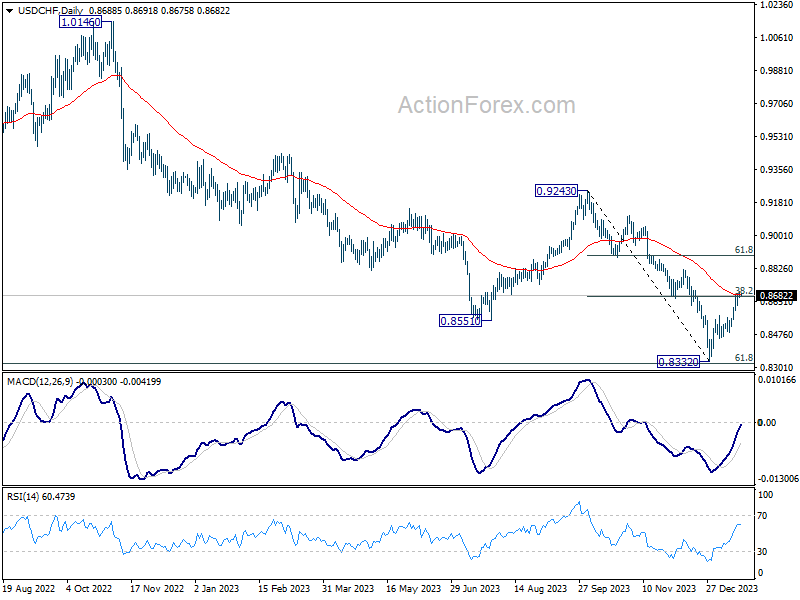

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8666; (P) 0.8685; (R1) 0.8700; More....

Outlook in USD/CHF remains unchanged, with focus on 38.2% retracement of 0.9243 to 0.8332 at 0.8680, which coincides 55 D EMA (now at 0.8687). Decisive break there will turn near term outlook bullish for 61.8% retracement 0.8995. Nevertheless, break of 0.8565 minor support will turn intraday bias back to the downside for retesting 0.8332 low.

In the bigger picture, while rebound from 0.8332 could be strong, there is no clear sign of medium term bottoming yet. This rebound is tentatively seen as a corrective move for now. Also, outlook will stay bearish as long as 0.9243 resistance holds. Larger down trend from 1.0146 (2022 high) should resume through 0.8332 low at a later stage.

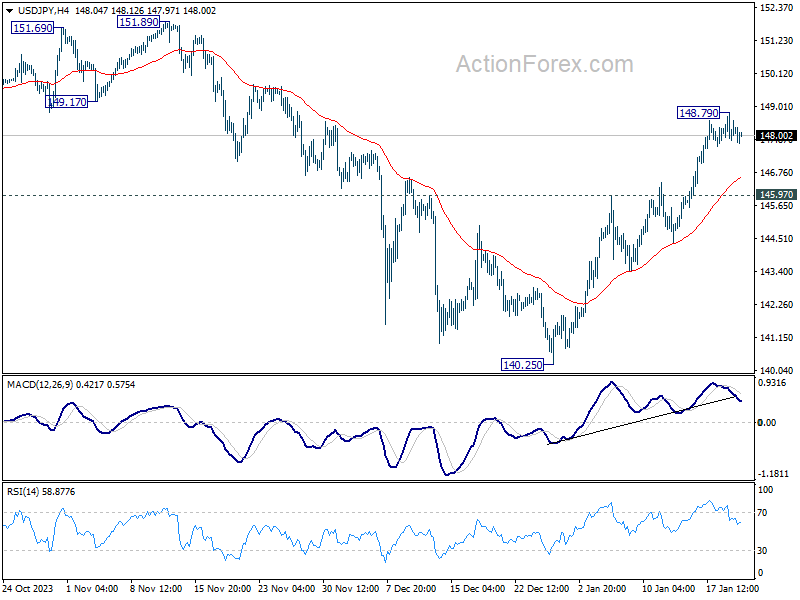

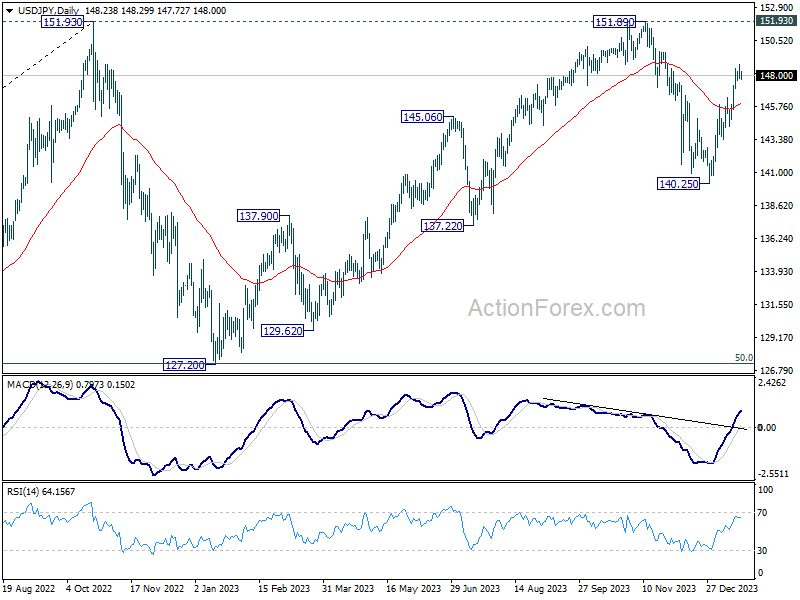

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.74; (P) 148.28; (R1) 148.71; More...

Intraday bias in USD/JPY remains neutral for consolidation below 148.79 temporary top. Further rally is expected as long as 145.97 resistance turned support holds. Corrective all from 151.89 should have completed at 140.25 already. Break of 148.79 will resume the rise from there for retesting 151.89/93 key resistance zone.

In the bigger picture, stronger than expected rebound from 140.25 dampened the original bearish review. Strong support from 55 W EMA (now at 141.89) is also a medium term bullish sign. Fall from 151.89 could be a correction to rise from 127.20 only. Decisive break of 151.89/93 will confirm resumption of long term up trend. This will now be the favored case as long as 140.25 support holds.

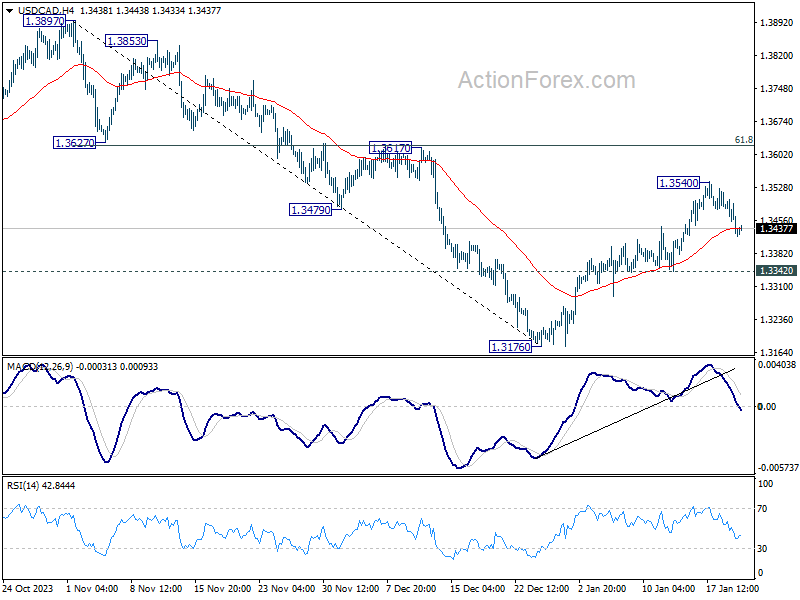

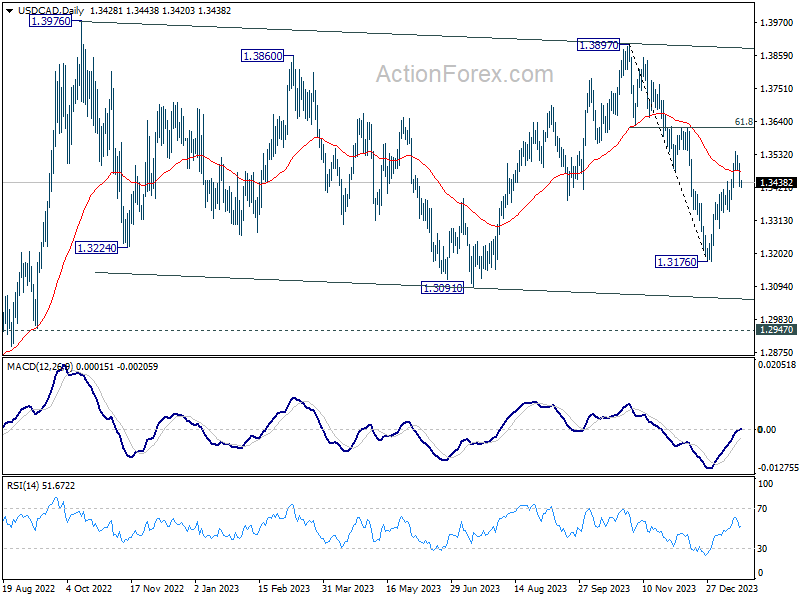

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3403; (P) 1.3453; (R1) 1.3478; More...

Intraday bias in USD/CAD remains neutral at this point, and some more consolidations could be seen below 1.3540. But further rally is expected as long as 1.3342 minor support holds. Fall from 1.3897 should have completed at 1.3716. Break of 1.3540w ill target 1.3617 cluster resistance (61.8% retracement of 1.3897 to 1.3176 at 1.3622). Decisive break there will pave the way to 1.3897/3976 key resistance zone.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume through 1.3976 at a later stage.

Busy Week Ahead: Tech Earnings and Central Bank Meetings

Friday’s economic data was yet another proof of the diverging fortunes between the US economy and the rest of the developed world. In the morning, the UK announced that its retail sales slumped for the second straight year, fueling the worries of a mild recession in the UK this year. But in the afternoon, Michigan’s consumer sentiment index showed an advance to a more than two year high, the expectations improved more than expected, with falling inflation expectations as a cherry on top. Remember, the US retail sales also showed a shiny number for the past holidays season.

The prospects of Federal Reserve (Fed) rate cuts and the likely scenario of soft landing hint that there is a growing chance that we see the US 10-year yield go back to where it belongs – above the 2-year yield. Right now, the US 2-year yield stands near 4.40%, the 10-year yield advanced past the 4.10%, the US dollar has been unable to clear the 200-DMA last week, but the strong US data versus weak data from the rest of the world would justify a swift move above this 200-DMA and the US stocks – especially the US technology stocks continue to fly high in the first month of this new year. The S&P500 finally hit an ATH level last Friday. Nvidia extended its gains to a fresh record as well, thanks to Meta’s announcement that it will be buying 350’000 cutting-edge chips from Nvidia to power its AI systems. Some estimate that Meta’s purchases will ensure around $10bn revenue this year for Nvidia from Meta alone.

Overall, strong US economic data has been tempering the expectation of a March rate cut from the Fed. But the Fed is still broadly expected to cut in May, if it doesn’t in March. The US yields are drifting gently higher from last year’s end levels. The rebounding yields weigh heavier on the S&P493; the equal weighted index continues to underperform the Magnificent 7.

The earnings season continues full swing with Netflix and Tesla due to announce their latest quarterly results this week.

The week’s economic calendar is also busy with major central bank meetings including the Bank of Japan (BoJ), the European Central Bank (ECB) and the Bank of Canada (BoC).

The BoJ will not normalize rates this week. In the best-case scenario, it will give further hints regarding the timing of the first rate hike – perhaps April. More realistically, the Japanese policymakers will push back on the normalization expectations and say that the monetary policy in Japan will remain supportive for as long as needed. The USDJPY opened the week near the 148 level. The risks are tilted to the downside as the risk of a verbal intervention increases into the 150 level.

The ECB and the BoC will certainly keep their rates unchanged, but the nuance in their accompanying statement will be closely watched for any hints regarding the first rate cut. ECB Chief Lagarde said last week in Davos that the ECB could lower rates by or in summer. The EURUSD is flirting with the 1.09 level this morning. Any hint that the ECB is ready to cut rates will weaken the euro bulls’ hands for a sustainable rise above the 1.10 level.

We Expect BoJ to Stay on Hold

In focus today

We start off the week with low activity on the data release front.

In Denmark the monthly employment statistics for November is released Monday morning.

Early Tuesday we await the rate decision from the first policy meeting from Bank of Japan in 2024. We expect the Bank of Japan to stay on hold. Wage growth remains the key missing piece of the puzzle before they can raise the policy rate out of negative and let go of the yield curve. We expect they will be ready to do that once we have hard evidence that the Shunto (spring wage negotiations) results in wage acceleration.

This week's main event is the ECB meeting on Thursday, where we expect rates to stay on hold for now, but signal that the next rate change most likely is a cut, which may happen in the summer. We also look out for Thursday's rate decision from Norges Bank, January PMIs on Wednesday and Tokyo January CPI print from Japan on Friday. Focus will also be on the US earnings season, where companies from a broader selection of sectors (including IT) will report.

Economic and market news

What happened overnight

In China the People's Bank of China kept its loan prime rates unchanged. This means that the one-year and five-year loan Prime Rates will remain at 3.45% and 4.2%, respectively. The move was in line with expectations, after the People's Bank surprisingly kept the medium-term lending facility unchanged last week, despite the consensus of a cut.

In the Republican primary election, Ron DeSantis suspended his campaign and endorsed Donald Trump becoming the republican nominee for the 2024 US presidential election, leaving Nikki Haley as Trump's sole competitor in the race. The decision was made in the aftermath of last week's first round Iowa election where Ron DeSantis gained 21% of votes compared to Donald Trump's 51%. Tomorrow, the primary election heads to New Hampshire for the second round.

What happened over the weekend

In the US, the University of Michigan's consumer sentiment survey showed that the consumer sentiment improved markedly from 70.1 to 78.8 (consensus: 69.7) as current conditions and expectations improved. This is the highest level since July 2021. 5-10Y inflation expectations fell from 2.9% to 2.8% in January (consensus: 3.0%), though still close to the 3% average over the past year. Short-term inflation expectations (1Y) declined to 2.9% from 3.1% in December.

In the UK, December retail sales dropped more than expected, at the fastest pace since early 2021, raising concerns over the health of the economy in late 2023.

Equities: Global equities were higher on Friday with S&P 500 reaching a new all-time high. This will of course happen from time to time but it was the first time in more than two years for the big refence index to set a new high. Our benchmark index, the MSCI world local currency index also made a new high. Just as interesting, the index is almost 35% higher since October 2022 and based investor surveys a period of historical underweights among profession investors. This should serve as a lesson on risk of being underweight and too defensive. Very often we meet investors seeing the risk in being overweight risk but not so much vice versa. On Friday there was big appetite for cyclical, large cap growth stocks. Global big tech outperformed consumer staples by 2.5% although yields continued to push higher. However, as emphasised several times in our Espresso, as long as yields are higher for the right reasons it is not a problem. On Friday, US consumer confidence increased significantly while inflation expectations dropped further. In US on Friday, Dow +1.1%, S&P 500 +1.2%, Nasdaq +1.7%, Russell 2000 +1.1%.

FI: Friday was a relatively volatile session in bond markets as investors continued to digest the hawkish signals from central banks during the week. Initially, long government bond yields dipped early in the session, but the move was swiftly reversed in the afternoon following the release of a stronger-than-expected US Michigan Consumer Survey for January. Meanwhile, 2Y Bund yields climbed by 5bp, reflecting ongoing adjustments to ECB expectations. Ahead of this week's meeting, the pricing of ECB rate cuts for the year stands at 130bp vs. 150bp last Monday. The Bund ASW-spread widened after consequent tightening for most of the week. The issuance pressure in the coming weeks will continue to be significant.

FX: USD/Scandies have started 2024 on a strong note, though last week was one where the USD consolidated vs most G10 peers. EUR/USD closed Friday a notch below 1.09, USD/JPY close to 148, USD/SEK in the mid-10.40s and USD/NOK just below 10.50. Meanwhile, NOK/SEK is again closing in on parity. This week offers a lot of important macro events to digest for FX, fixed income and equities including the ECB meeting on Thursday and US PCE data on Friday.

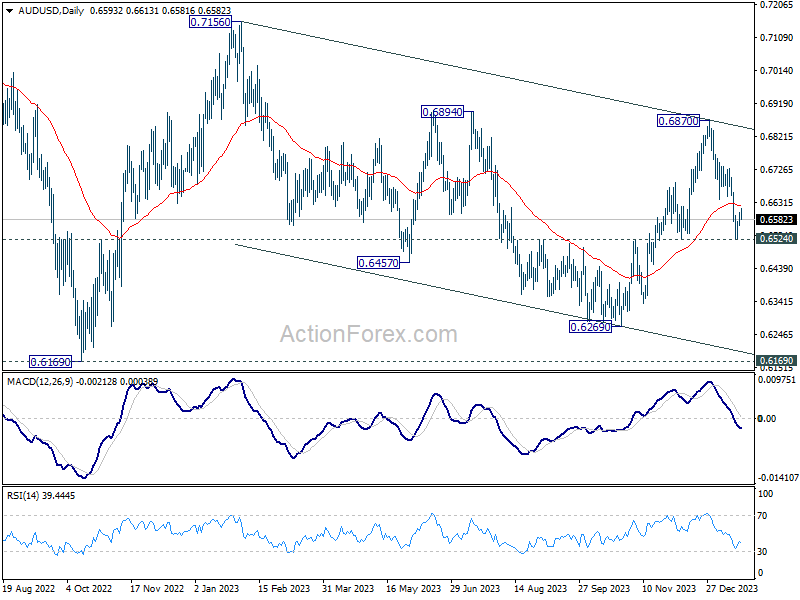

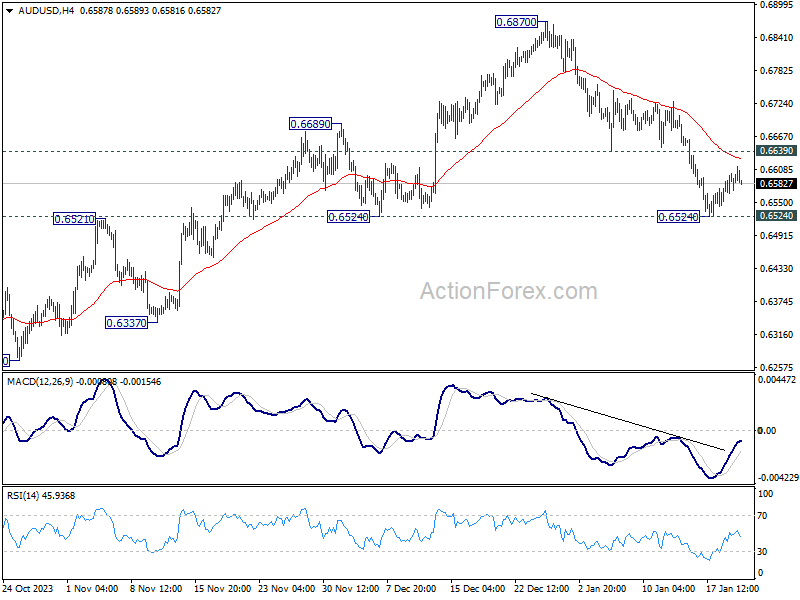

AUD/USD Daily Report

Daily Pivots: (S1) 0.6575; (P) 0.6588; (R1) 0.6611; More...

Intraday bias in AUD/USD remains neutral at this point. Some more consolidations could be seen above 0.6524 temporary low. But further decline is expected as long as 0.6639 support turned resistance holds. Firm break of 0.6524 support will argue that whole rebound from 0.6269 has completed, and bring deeper fall to this support.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.