Sample Category Title

Weak JPY Following Disappointing (But Outdated) November Labor Earnings Data

Markets

Bond supply stood in the center of attention yesterday. Belgium and Italy kicked off in Europe. Both received bumper investor interest, the former for a new 10-year OLO benchmark and the latter for a 7-year one as well as a tap of an existing 30-year BTP. The US started its monthly refinancing round with a $52bn 3-year auction stopping through the WI. With markets absorbing the load well, the impact on yields stayed modest. German Bunds underperformed Treasuries. Yields increased between 5 and 6.2 bps. This was, however, mainly a catch-up move with a late-session UST swoon on Monday. After yields gapped higher at yesterday’s open, they traded sideways. ECB’s Villeroy after European closing hours weighed in on the heated rate cut debate. But the nor-dove-nor-hawk was, well, neither dovish nor hawkish. While saying that 2024 would see the first rate cuts, he declined on giving a timing. The Frenchman said the ECB shouldn’t rush things but must not be too obstinate about it either. US yields eased a few bps (0.8-2.2), the belly outperforming the wings. The dollar held the upper hand in currency markets, supported in part by the fragile risk environment (equity markets closed up to 0.4% lower in Europe and the US). EUR/USD moved south to 1.093 in technically insignificant trading. USD/JPY bounced off the 200dMA to end at 144.48. The pound caught a breather following the surge so far this week. EUR/GBP rose from an intraday low around 0.858 to just north of 0.86. Even as GBP continues in Asian dealings this morning, the currency’s early 2024 track record is strong nonetheless. Other moves in FX include a weak JPY following disappointing (but outdated) November labor earnings data. The BoJ’s window of opportunity to ditch negative policy rates is closing rapidly. USD/JPY is testing the 145 big figure and equities in the country (up to +2%) greatly outperform regional peers. The Aussie dollar appreciates even as inflation eased slightly more than expected from 4.9% to 4.3% in November. The eco calendar is once again razor thin today, meaning technically inspired trading ahead of tomorrow’s US CPI numbers. Supply does remain in focus, this time with Spain (20-y syndication) and the US auctioning $37bn of 10-y bonds. Considering yesterday’s bond sales, we expect no major issues for the ones today. NY Fed president Williams’ speech on the 2024 eco and inflation outlook is worth listening to but comes only in late US dealings.

News & Views

The National Bank of Poland kept its policy rate unchanged at 5.75%. The central bank’s rate cut cycle is now on hold for a third meeting running after a cumulative 100 bps stealth easing around the time of tide-changing parliamentary elections in October. Polish data suggest that growth increased in Q4 2023, yet it remained relatively low. The labour market is still tight and the unemployment rate low. Polish inflation is expected to fall significantly in coming months (6.1% Y/Y in December) but the decline in core inflation will be slower with sticky wage inflation playing a key role. The NBP is happy with the support an appreciating zloty is providing in helping inflation lower as it is consistent with fundamentals of the Polish economy. NBP governor Glapinski will give more comments on the outcome of yesterday’s meeting and the path forward at this afternoon’s press conference. We think that an another unchanged decision will follow in February with the early March meeting being the important one when new projections will be released. The Polish zloty holds strong in the EUR/PLN 4.35-area.

The Fed’s vice chair for supervision, Michael Barr, signaled that the central bank’s Term Funding Program (BTFP) is set to expire on March 11. The BTFP offers loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging any collateral eligible for purchase by the Federal Reserve Banks in open market operations. The BTFP was set up for emergency purposes in the wake of the SVB collapse in March of last year with the aim of eliminating an institution’s need to quickly sell assets in times of stress. The BTFP was extensively used of late as institutions borrow at the one-year overnight index swap rate (which currently discounts rate cuts over the next 12 months) rather than at the 5.5% rate from the discount facility.

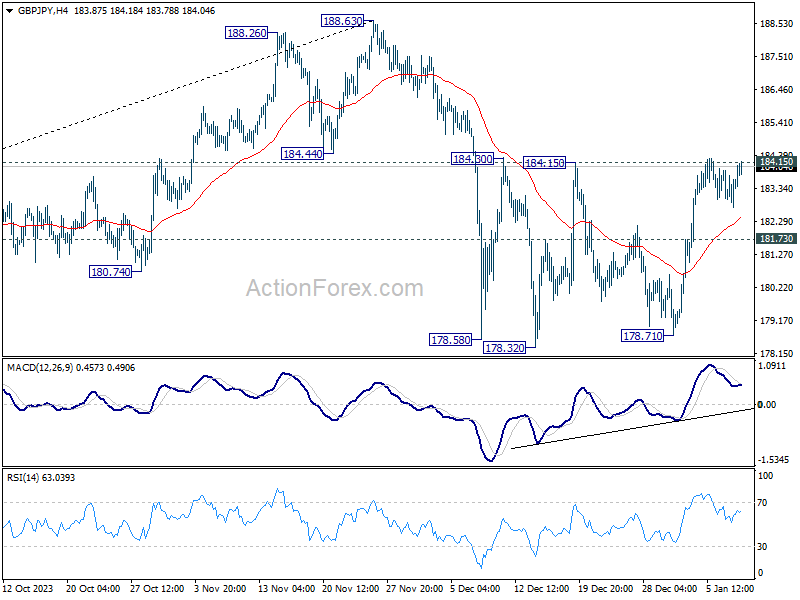

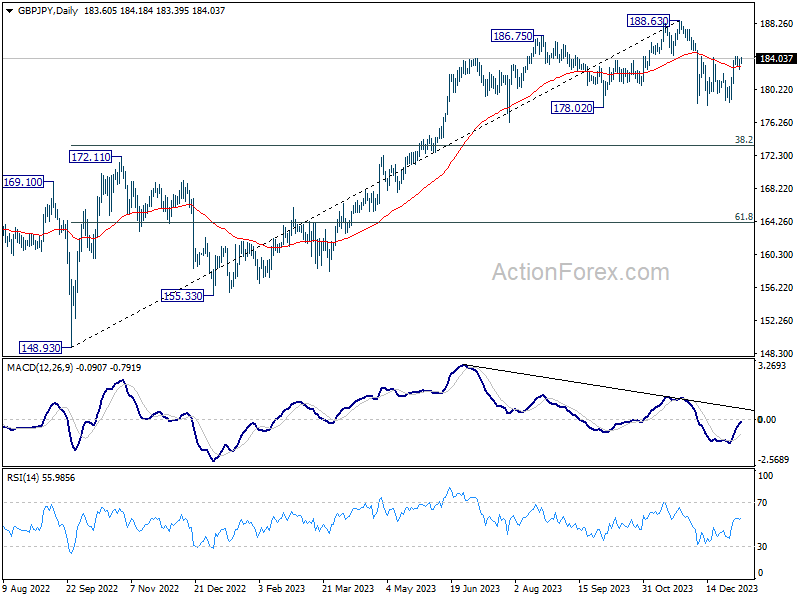

GBP/JPY Daily Outlook

Daily Pivots: (S1) 182.94; (P) 183.45; (R1) 184.15; More...

Intraday bias in GBP/JPY stays neutral this point. On the upside, sustained break of 184.15 resistance will argue that whole pull back from 188.63 has completed and bring further rally to retest this high. However, break of 181.73 minor support will indicate rejection by 184.15, and retain near term bearishness. Intraday bias will be back on the downside for 178.71 support instead.

In the bigger picture, price actions from 188.63 medium term top are seen as a correction to the up trend from 148.93 (2022 low) only. As long as 172.11 resistance turned support holds, larger up trend from 123.94 (2020 low) is still in favor to resume through 188.63 at a later stage.

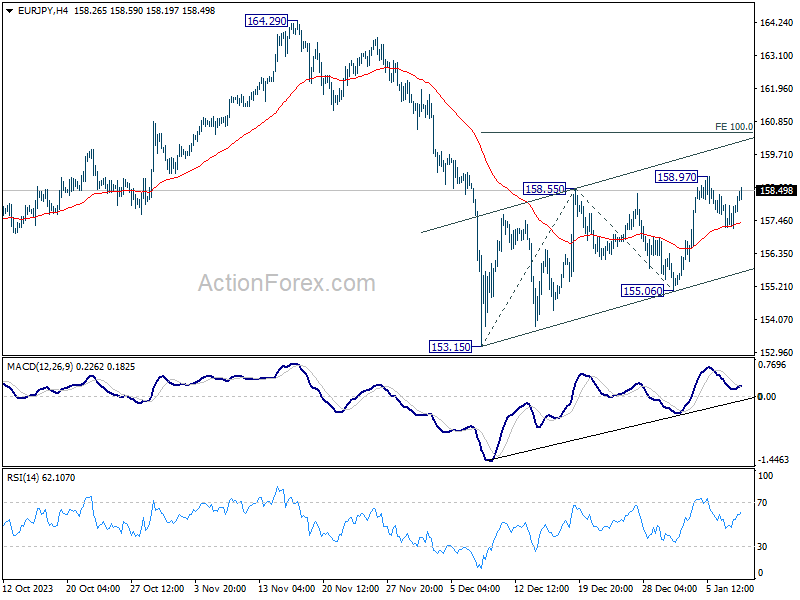

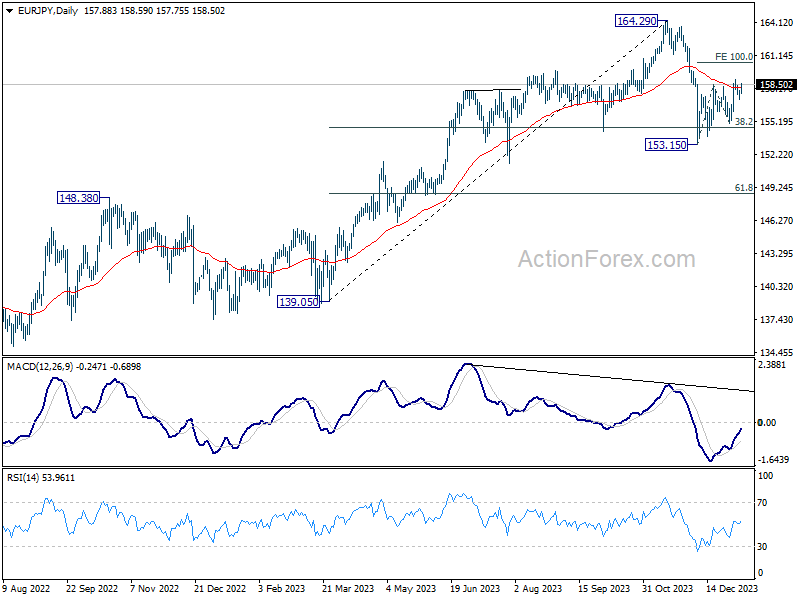

EUR/JPY Daily Outlook

Daily Pivots: (S1) 157.42; (P) 157.73; (R1) 158.24; More...

Intraday bias in EUR/JPY stays neutral at this point, and further rally is in favor with 155.06 support intact. On the upside, above 158.97 will resume the rebound from 153.15 to 100% projection of 153.15 to 158.55 from 155.06 at 160.46.

In the bigger picture, price actions from 164.29 medium term top are tentatively seen as a correction to rise from 139.05 for now. As long as 148.48 resistance turned support holds (2022 high), larger up trend from 114.42 (2020 low) could still resume through 164.29 at a later stage.

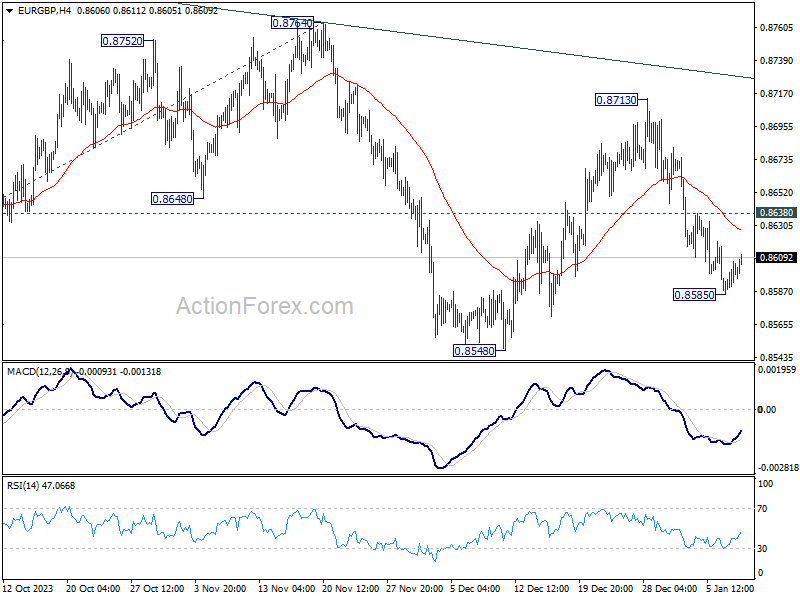

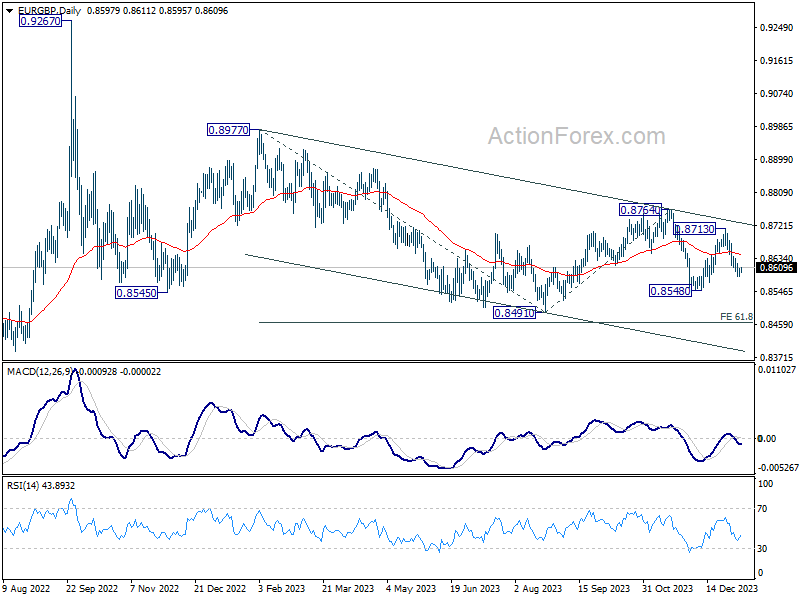

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8586; (P) 0.8597; (R1) 0.8612; More...

Intraday bias in EUR/GBP is turned neutral with current recovery, but further decline is in favor with 0.8638 minor resistance intact. On the downside, break of 0.8585 will resume the fall from 0.8713 to 0.8548 support first. Break there will target 0.8491 low next. However, break of 0.8638 will turn bias to the upside for stronger rebound.

In the bigger picture, fall from 0.8764 is seen as another leg in the whole down trend from 0.9267 (2022 high). Outlook will stay bearish as long as 0.8764 resistance holds. Break of 0.8491 will target 61.8% projection of 0.8977 to 0.8491 from 0.8764 at 0.8464.

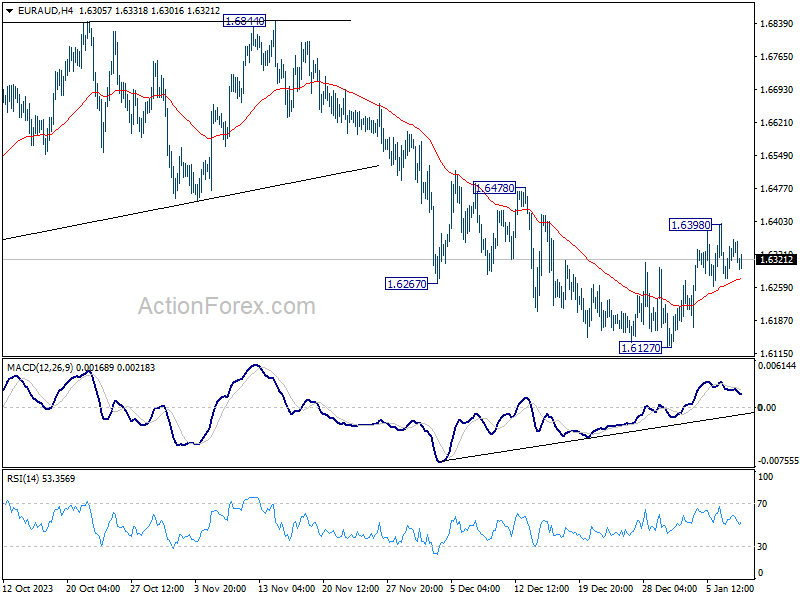

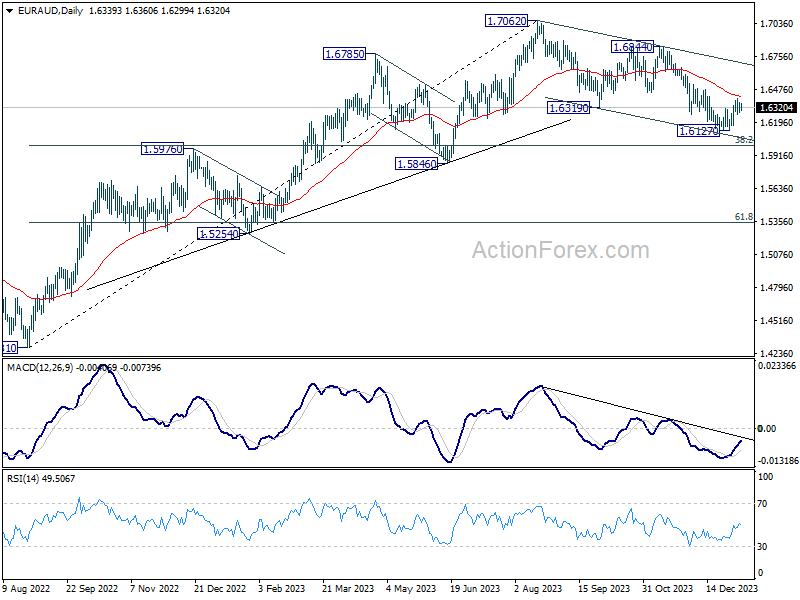

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6297; (P) 1.6331; (R1) 1.6382; More...

Intraday bias in EUR/AUD is turned neutral first. But risk will stay on the upside as long as 1.6127 support holds. Above 1.6398 will resume the rebound to 1.6478 resistance. Firm break there will argue that whole correction from 1.7062 has completed, and target 1.6844 resistance for confirmation. Nevertheless, break of 1.6127 will resume the corrective fall to 1.6000 fibonacci level.

In the bigger picture, fall from 1.7062 medium term top is seen as correction to the up trend from 1.4281 (2022 low). Strong support should be seen around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 bring rebound. Break of 1.6844 will argue that this up trend is ready to resume through 1.7062 high.

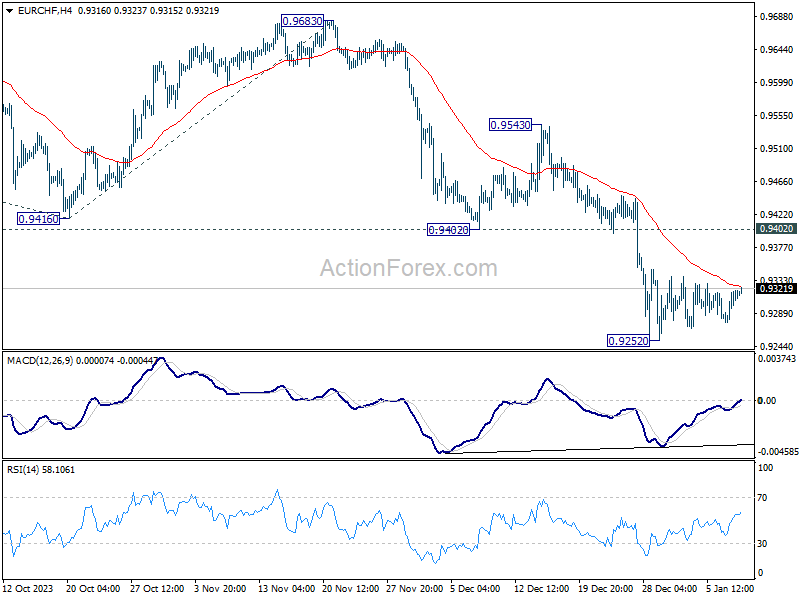

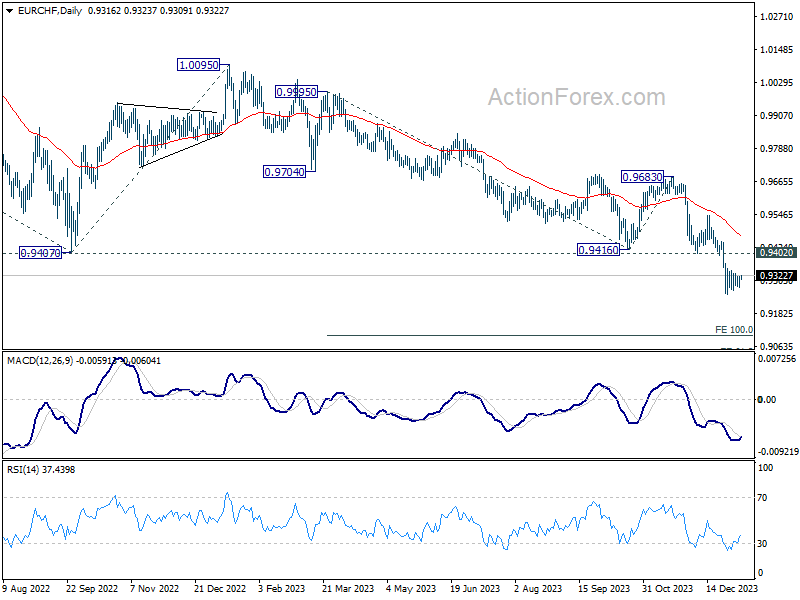

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9290; (P) 0.9306; (R1) 0.9332; More...

Intraday bias in EUR/CHF stays neutral as consolidation from 0.9252 is still extending. While another recovery cannot be ruled out, outlook will stay bearish as long as 0.9402 support turned resistance holds. On the downside, break of 0.9252 will resume larger down trend to 100% projection of 0.9995 to 0.9416 from 0.9683 at 0.9104 next.

In the bigger picture, medium term outlook remains bearish as long as 0.9683 resistance holds. Current fall from 1.2004 (2018 high) is part of the multi-decade down trend. Next target is 61.8% projection of 1.1149 (2020 high) to 0.9407 from 1.0095 at 0.9018.

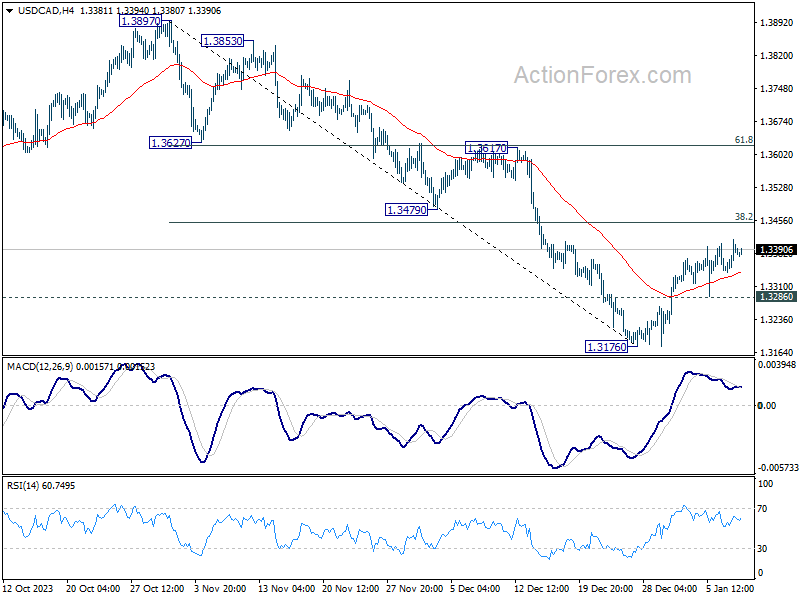

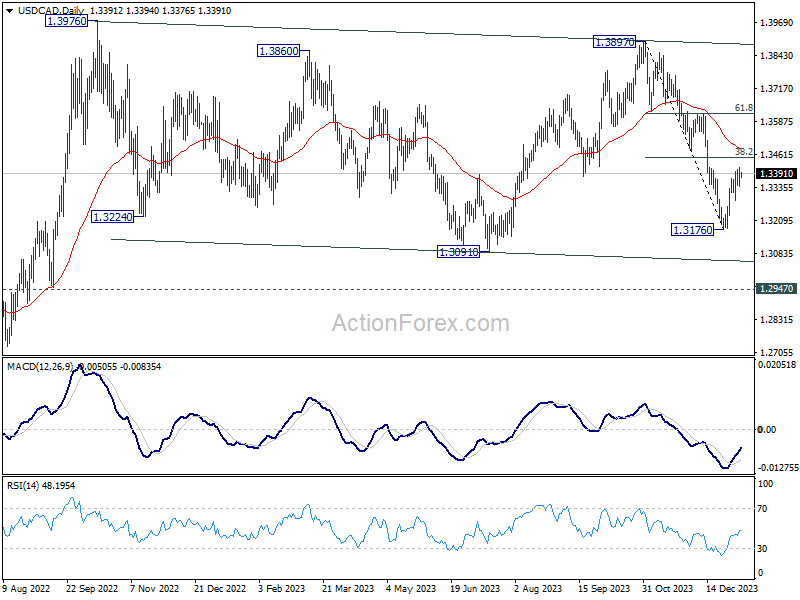

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3349; (P) 1.3382; (R1) 1.3423; More...

Further rise remains in favor in USD/CAD, and rebound from 1.3176 would target 38.2% retracement of 1.3897 to 1.3176 at 1.3451. Firm break there will pave the way to 61.8% retracement at 1.3622. On the downside, however, break of 1.3286 will turn bias back to the downside for 1.3176 low instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern only. While fall from 1.3897 could still extend through 1.3091, strong support should emerge above 1.2947 resistance turned support to bring rebound. Overall, larger up trend from 1.2005 (2021 low) is still expected to resume at a later stage.

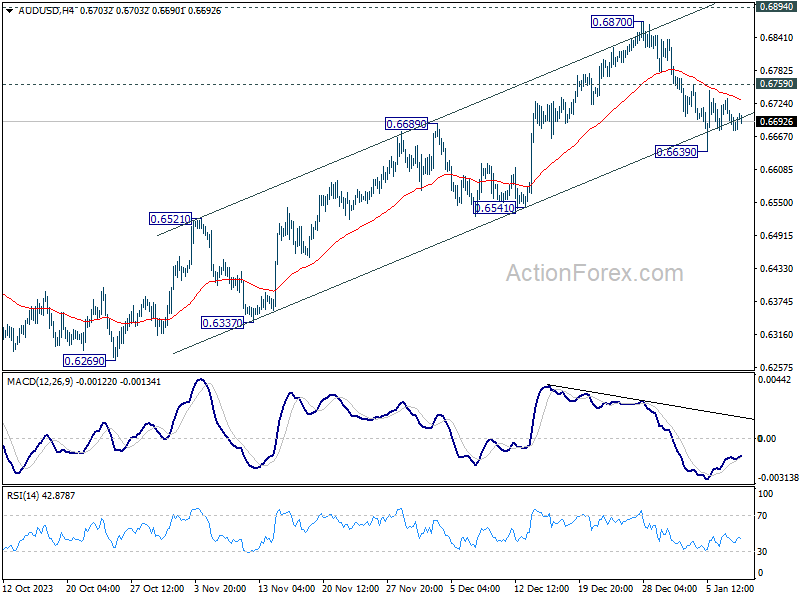

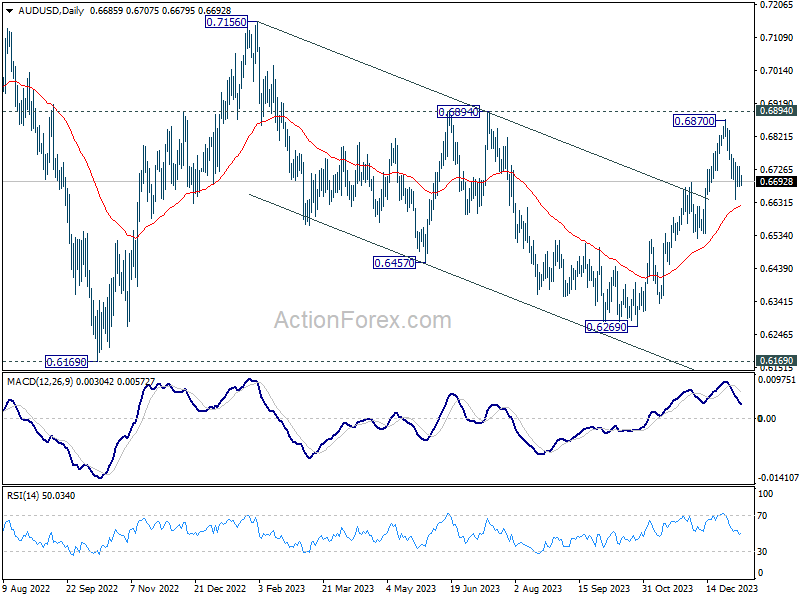

AUD/USD Daily Report

Daily Pivots: (S1) 0.6664; (P) 0.6700; (R1) 0.6722; More...

Intraday bias in AUD/USD is neutral as sideway trading continues. On the downside, break of 0.6639 will resume the fall from 0.6870 short term top to 0.6541 support next. On the downside, though, break of 0.6759 minor resistance will suggest that the pull back has completed already. Intraday bias will be turned back to the upside for 0.6870 resistance.

In the bigger picture, price actions from 0.6169 (2022 low) could be just a medium term corrective pattern to the down trend from 0.8006 (2021 high). Rise from 0.6269 is seen as the third leg of the pattern that could target 0.7156 on break of 0.6894 resistance. For now, range trading should be seen between 0.6169 and 0.7156 (2023 high), until further developments.

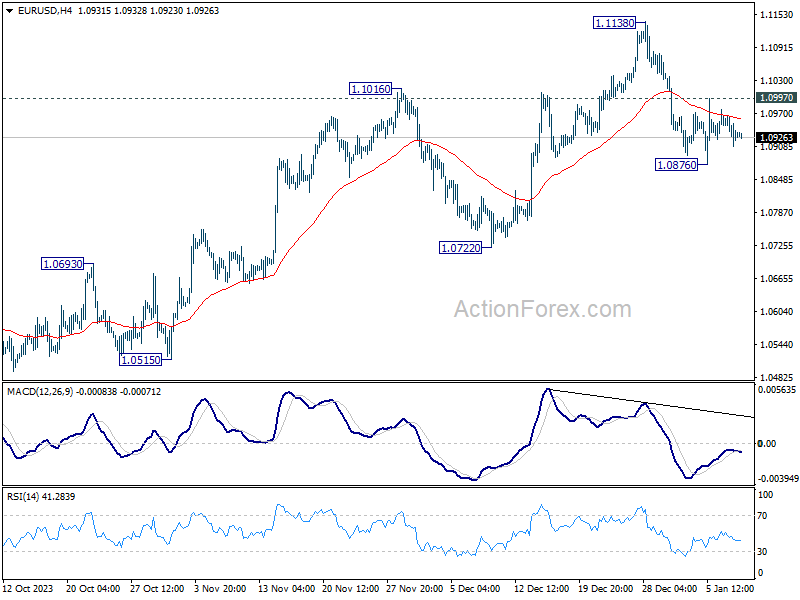

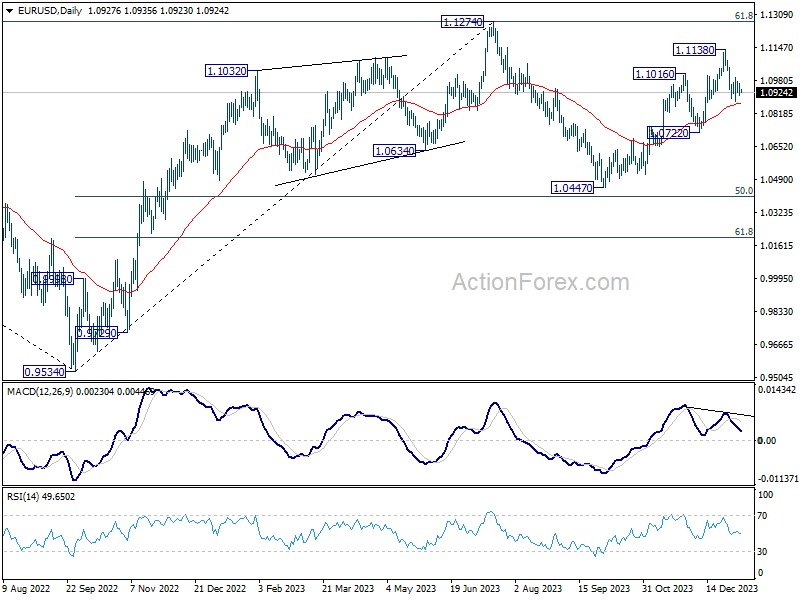

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0906; (P) 1.0936; (R1) 1.0961; More...

Intraday bias in EUR/USD remains neutral as range trading continues. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

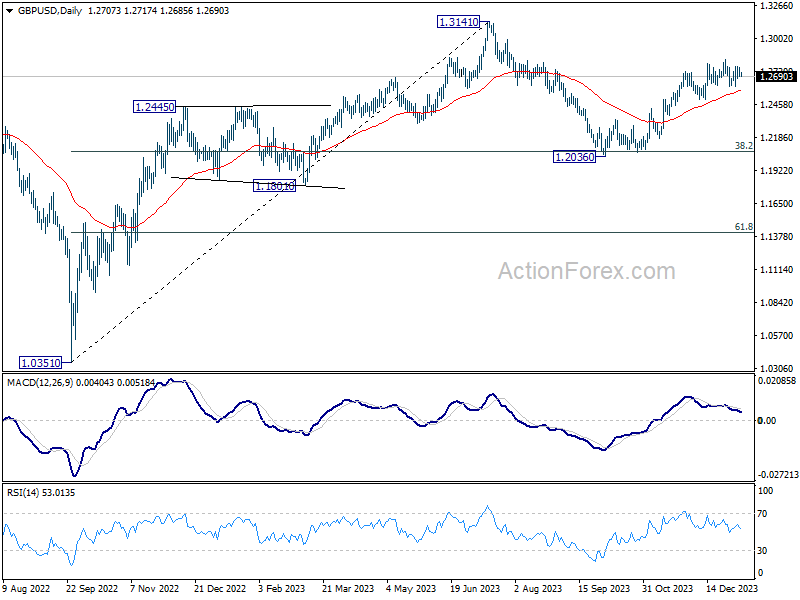

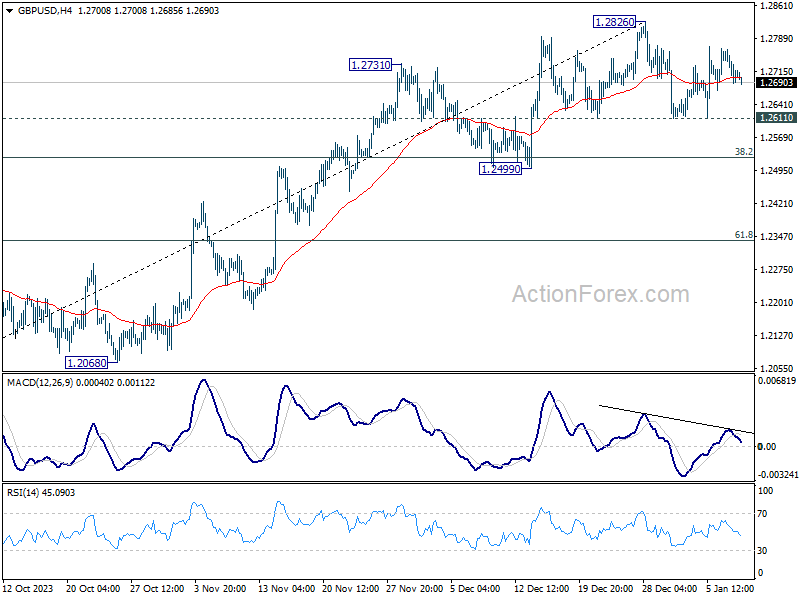

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2678; (P) 1.2722; (R1) 1.2753; More...

Intraday bias in GBP/USD remains neutral as range trading continues. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.