Sample Category Title

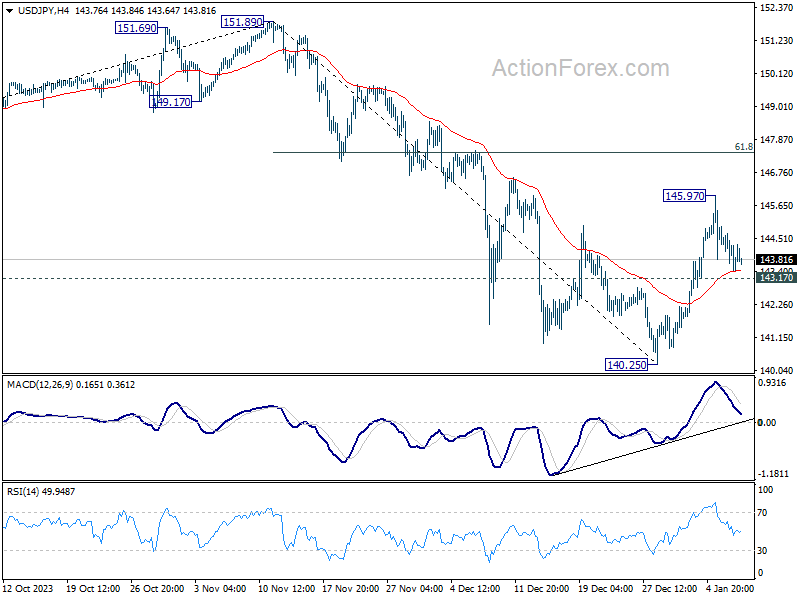

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.63; (P) 144.27; (R1) 144.89; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the upside, above 145.97 will resume the rebound from 140.25. But upside should be limited by 61.8% retracement of 151.89 to 140.25 at 147.44. On the downside, below 143.17 minor support will turn bias back to the downside for retesting 140.25 low.

In the bigger picture, for now, fall from 151.89 is still seen as the third leg of the corrective pattern from 151.89. Another decline through 140.25 will target 61.8% retracement of 127.20 to 151.89 at 136.63. Sustained break there will pave the way to 127.20 support (2022 low). However, firm break of 147.44 fibonacci resistance will dampen this view and bring retest of 151.89 instead.

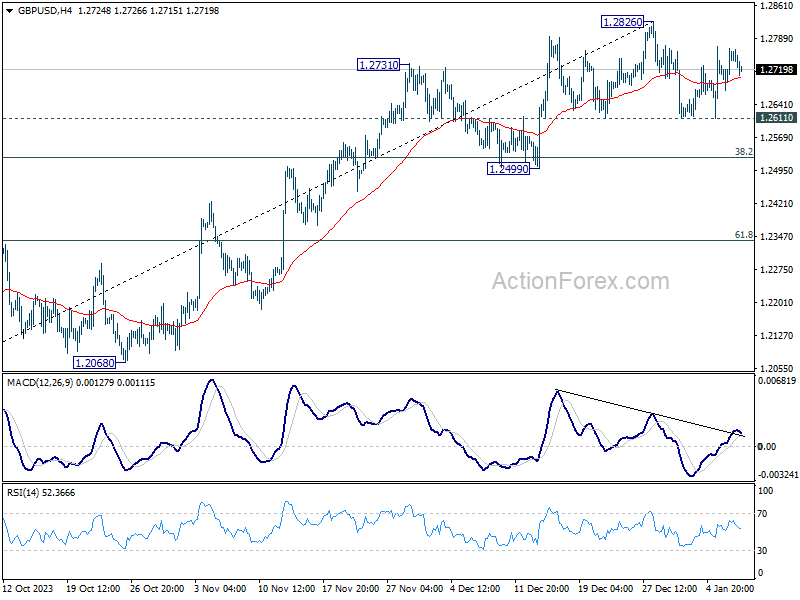

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2729; (R1) 1.2786; More...

GBP/USD is extending sideway trading below 1.2826 and intraday bias remains neutral. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Lackluster Trading in Forex as Economic Data Fails to Stir Major Movements

Currency trading today remained lackluster, characterized by limited movements across major pairs and crosses. Key economic data releases, ranging from Japan's Tokyo CPI, and retail sales figures from Australia and the Eurozone, to trade balance data from Canada and US, failed to significantly influence the markets.

Japanese Yen is currently a marginally stronger currency, continuing its near-term recovery. Dollar follows closely, ranking as the second strongest . Conversely, Australian Dollar remains at the lower end of the performance chart, facing additional downward pressure due to selling against Canadian Dollar and New Zealand Dollar. Meanwhile, Euro experienced a mild uplift, primarily driven by its recovery against British Pound and Swiss Franc.

Looking ahead, the overall risk sentiment in the markets could become a key driver in forex, especially today, if there are sustainable movements in the stock markets. US futures are indicating lower open, with NASDAQ leading the decline. This is partly fueled by warnings from South Korea's tech giant Samsung, which projected a potential drop of up to 35% in its Q4 operating profit.

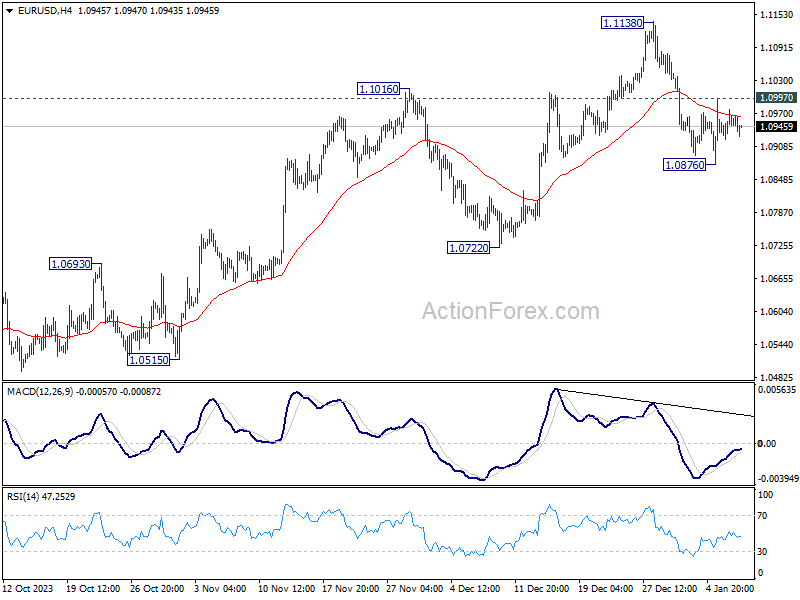

From a technical perspective, Dollar may have the potential to extend its near-term rebound against Euro and Australian Dollar, especially if the risk-off sentiment persists. For EUR/USD, a break below 1.0876 temporary low could resume the decline from 1.1138, targeting 1.0722 support level next.

In Europe, at the time of writing, FTSE is down -0.13%. DAX is down -0.60%. CAC is down -0.64%. Germany 10-year yield is up 0.053 at 2.188. UK 10-year yield is up 0.034 at 3.806. Earlier in Asia, Nikkei rose 1.16%. Hong Kong HSI fell -0.21%. China Shanghai SSE rose 0.20%. Singapore Strait Times rose 0.34%. Japan 10-year yield fell -0.0184 to 0.587.

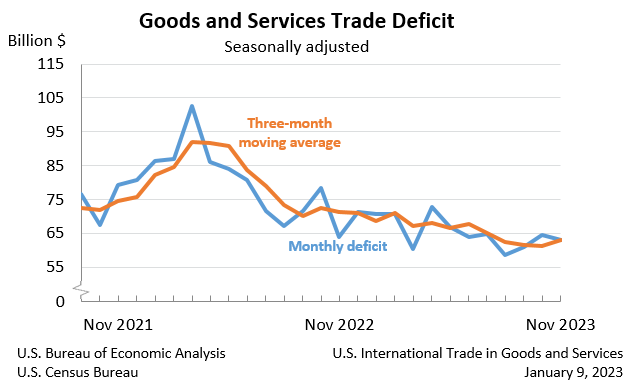

US goods and services exports down -1.9% mom in Nov, imports down -1.9% mom

US goods and services exports fell -1.9% mom to USD 253.7B in November. Imports fell -1.9% mom to USD 316.9B. Trade deficit narrowed slightly from USD -64.5B to USD -63.2B, smaller than expectation of USD -64.8B.

Canada's merchandise exports down -0.6% mom in Nov, imports up 1.9% mom

In November, Canada's merchandise exports fell -0.6% mom to CAD 65.74B. This decrease occurred despite increases in 7 of the 11 product sections. Merchandise imports rose 1.9% mom to CAD 64.17B, with increases in 8 of the 11 product sections.

Merchandise trade surplus narrowed from CAD 3.2B to CAD 1.6B, smaller than expectation of CAD 2.5B.

Services exports rose 1.0% mom to CAD 16.6B. Services imports fell -0.1% mom to CAD 17.6B.

Combining goods and services, exports decreased -0.3% mom to CAD 82.4B. Imports rose 1.5% mom to CAD 81.8B. Trade surplus fell from CAD 2.0B to CAD 594m.

Eurozone unemployment rate falls to 6.4% in Nov, EU down to 5.9%

Eurozone unemployment rate fell from 6.5% to 6.4% in November, below expectation of 6.5%. EU unemployment rate fell from 6.0% to 5.9%.

According to Eurostat, total number of unemployed individuals in EU stood at approximately 12.954m, with around 10.970m of in Eurozone. This figure represents a decrease of -144k unemployed persons in EU and -99k in Eurozone compared to October.

Japan's Tokyo CPI core down for the second month to 2.1%

Japan's Tokyo CPI core, which excludes fresh food, slowed from 2.3% yoy to 2.1% yoy in December, aligning with market expectations. This figure represents the lowest reading since June 2022 and marks the second consecutive month of decline.

Additionally, CPI core-core, which excludes both food and energy, also slipped from 3.6% yoy to 3.5% yoy. This marks the fourth consecutive month of cooling in this measure. Headline CPI, similarly fell from 2.6% yoy to 2.4% yoy. T

Tokyo's CPI figures are often regarded as precursors to the national data, suggesting that a similar trend might be observed in the broader Japanese economy.

In separate report, households reduced their spending in November -by 2.9% yoy, worst than expectation of -2.3% yoy. This decrease in consumer spending is attributed to the rising costs of living, which have led to more selective purchasing behaviors among shoppers.

Australia's retails sales rises 2.0% mom in Nov on Black Friday boost

Australia retail sales rose 2.0% mom to AUD 36.5B in November, above expectation of 1.2% mom. That followed a fell of -0.4% mom in October.

Robert Ewing, ABS head of business statistics, attributed this surge to the impact of Black Friday sales. He noted, "Black Friday sales were again a big hit this year, with retailers starting promotional periods earlier and running them for longer, compared to previous years."

Ewing further explained: "The strong rise suggests that consumers held back on discretionary spending in October to take advantage of discounts in November." Additionally, he observed that shoppers might have advanced some of their Christmas shopping to November, which typically occurs in December.

Looking ahead

Swiss unemployment rate and foreign currency reserves, Germany industrial production, France trade balance, and Eurozone unemployment rate will be released in European session. Later in the day, US will release trade balance. Canada will release trade balance and building permits.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2692; (P) 1.2729; (R1) 1.2786; More...

GBP/USD is extending sideway trading below 1.2826 and intraday bias remains neutral. On the upside, decisive break of 1.2826 high will resume whole rally from 1.2036. Nevertheless, another fall and break of 1.2611 will bring deeper correction to 1.2499 support instead.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Dec | 2.40% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI ex Fresh Food Y/Y Dec | 2.10% | 2.10% | 2.30% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | 3.50% | 3.60% | ||

| 00:30 | AUD | Retail Sales M/M Nov | 2.00% | 1.20% | -0.20% | -0.40% |

| 00:30 | AUD | Building Permits M/M Nov | 1.60% | -2.00% | 7.50% | 7.20% |

| 06:45 | CHF | Unemployment Rate M/M Dec | 2.20% | 2.20% | 2.10% | |

| 07:00 | EUR | Germany Industrial Production M/M Nov | -0.70% | 0.40% | -0.40% | -0.30% |

| 07:45 | EUR | France Trade Balance (EUR) Nov | -5.9B | -7.9B | -8.6B | |

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 6.40% | 6.50% | 6.50% | |

| 11:00 | USD | NFIB Business Optimism Index Dec | 91.9 | 90.9 | 90.6 | |

| 13:30 | USD | Trade Balance (USD) Nov | -63.2B | -64.8B | -64.3B | -64.5B |

| 13:30 | CAD | Trade Balance (CAD) Nov | 1.6B | 2.5B | 3.0B | 3.2B |

| 13:30 | CAD | Building Permits M/M Nov | -3.90% | 2.00% | 2.30% |

US goods and services exports down -1.9% mom in Nov, imports down -1.9% mom

US goods and services exports fell -1.9% mom to USD 253.7B in November. Imports fell -1.9% mom to USD 316.9B. Trade deficit narrowed slightly from USD -64.5B to USD -63.2B, smaller than expectation of USD -64.8B.

Canada’s merchandise exports down -0.6% mom in Nov, imports up 1.9% mom

In November, Canada's merchandise exports fell -0.6% mom to CAD 65.74B. This decrease occurred despite increases in 7 of the 11 product sections. Merchandise imports rose 1.9% mom to CAD 64.17B, with increases in 8 of the 11 product sections.

Merchandise trade surplus narrowed from CAD 3.2B to CAD 1.6B, smaller than expectation of CAD 2.5B.

Services exports rose 1.0% mom to CAD 16.6B. Services imports fell -0.1% mom to CAD 17.6B.

Combining goods and services, exports decreased -0.3% mom to CAD 82.4B. Imports rose 1.5% mom to CAD 81.8B. Trade surplus fell from CAD 2.0B to CAD 594m.

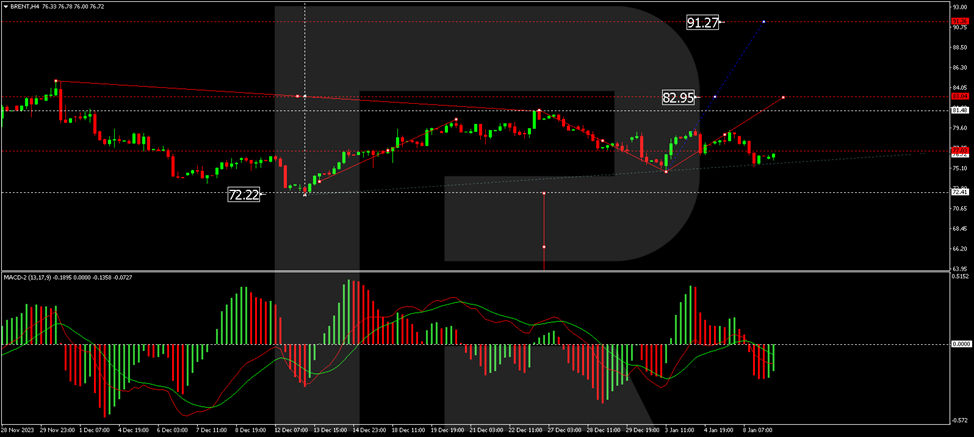

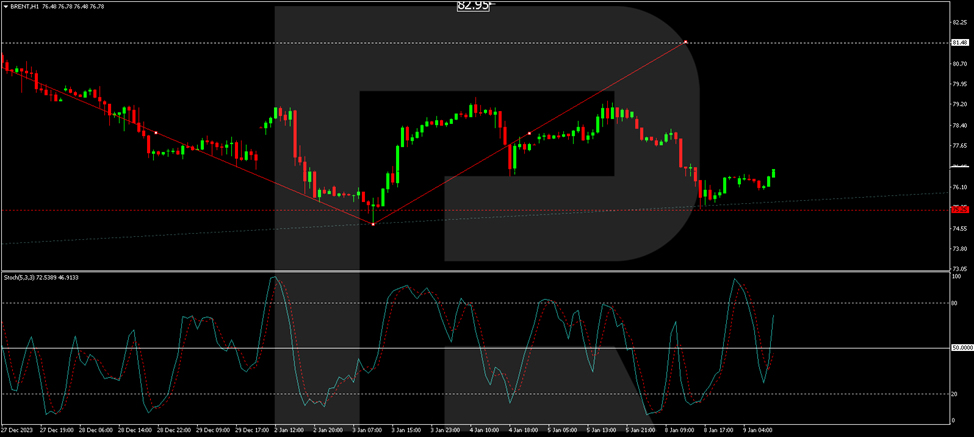

Brent is Stressed Again

For the last month and a half, the crude oil market has been under a constant stress. Sentiment changes mostly because of the supply and demand forecasts. A Brent barrel price dropped to 75.65 USD yesterday.

The decline was triggered by the decision of Saudi Arabia to decrease prices for its buyers starting February, regardless of the region. The discount will amount to 2 USD, which is quite a lot.

The market thinks that the Saudis have either noticed a demand slump and are now trying to run ahead of it, or they have decided to shove away the competitors, such as the US crude oil producers.

Brent technical analysis

On the H4 Brent chart, the quotes have corrected to 74.74. A consolidation range is now forming around the 78.15 level. An escape from the range upwards might open the potential for a growth wave to 81.50. This is a local target. With an escape from the range downwards, the correction could continue to 70.00. Technically, this scenario is confirmed by the MACD, whose signal line is under zero, preparing to start growing.

On the H1 Brent chart, the quotes have completed a growth wave to 79.45 and a correction to 75.25. Today a growth link to 80.00 is expected to develop. If this level breaks, the wave could continue to 81.50. Technically, this scenario is confirmed by the Stochastic oscillator: its signal line is under 50, aimed strictly upwards to 80.

Swiss National Bank Suffered Losses of 3 Billion Francs in 2023

The Swiss National Bank (SNB) reported an annual loss of 3 billion Swiss francs (USD 3.54 billion) in 2023 and said it would not make payments to Switzerland's central or local government or pay dividends to investors.

The loss is believed to have occurred as a result of interest rate hikes aimed at fighting inflation.

Although in Switzerland, perhaps, inflation is at the lowest level: according to yesterday's Core Price Index data, the actual value is = 0.0% (expected = 0.1%, a year ago = -0.2%, the highest actual value in 2023 was = +0.7 %). However, the SNB raised the rate to 1.75% twice in 2023, and this led to it making more payments to deposit account holders.

Note that the loss for 2023 is much less than the record minus 133 billion for 2022. Reuters writes that the losses will not affect the bank's current monetary policy, and interest rates could be cut during 2024.

On November 2, we wrote that the franc could continue to strengthen. Since then, USD/CHF has fallen about 6%, setting its 2023 low on December 28 at 0.83327.

The graph shows that:

→ during 2023, the price moved within the descending channel;

→ at the 2023 low, the price was unable to reach its lower limit — a sign of a lack of selling pressure;

→ the median line of the channel still serves as resistance (as shown by the arrow);

→ level 0.845 changed its role from resistance to support;

→ in the area of the 2023 lows, long lower shadows were formed on the candles (a sign of aggressive demand). At the same time, the RSI indicator showed that the market was strongly oversold.

Taking into account the above arguments, it can be assumed that the USD will be able to strengthen against the franc, stopping the pace of the downward trend in 2023. A bullish breakdown of the median line (or failure of the price to consolidate below the 0.845 level) will provide more arguments in favor of the presence of demand in the market in question.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Japanese Yen Shrugs as Tokyo Core CPI Slows

- Tokyo Core CPI eases to 2.1%

The Japanese yen has posted slight gains for a second straight day. In the European session, USD/JPY is trading at 144.10, down 0.09%.

Tokyo Core CPI dips to 2.1%

Tokyo Core CPI rose 2.1% y/y in December, down from 2.3% in November and matching the estimate of 2.1%. This marked the lowest reading since June 2022. At the same time, the indicator has exceeded the Bank of Japan’s target of 2% for 19 straight months.

There has been speculation that persistent inflation the BoJ will tighten policy and BoJ meetings have become closely-watched events, with investors on the alert for a shift in the BoJ’s ultra-loose policy. The BoJ meets next on Jan. 22-23. BoJ Governor Ueda has hinted at a change in policy but has stressed that wages must first rise if the BoJ is to achieve its goal of sustainable inflation at 2%.

The BoJ’s ultra-loose policy took a massive toll on the yen in 2023. The yen plunged 15% between January and October but managed to recover about half of those losses by the end of the year, as the US dollar retreated on expectations that the Federal Reserve would lower rates in 2024.

Japan’s economy remains weak, which is another reason that the BoJ is hesitant to tighten policy. Household spending, released earlier today, declined 1% in November, compared to -0.1% in October and lower than the estimate of 0.2%. On a yearly basis, household spending fell 2.9% in November, down from -2.5% in October and shy of the estimate of -2.3%. Since November 2022, household spending has posted only one gain as consumers continue to hold tight to the purse strings due to the difficult economic conditions.

USD/JPY Technical

- USD/JPY tested resistance at 144.27 earlier. Above, there is resistance at 144.89

- There is support at 143.63 and 143.01

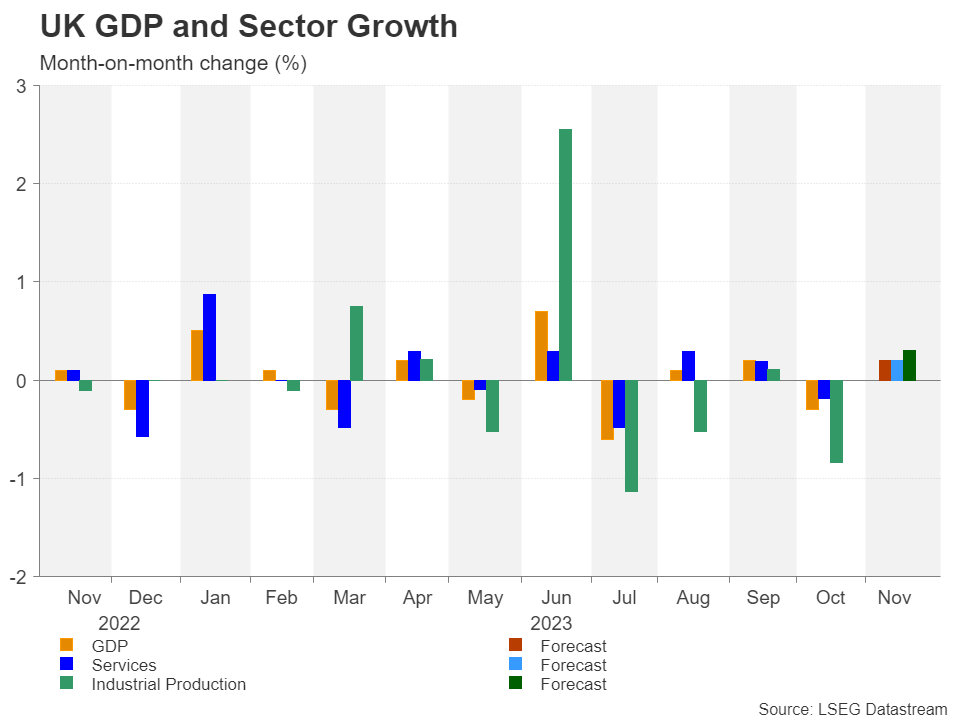

Pound Looks to UK GDP Rebound to Keep Bears at Bay

- UK GDP likely expanded in November, potentially dashing hopes for early rate cut

- But any disappointment would increase the odds of a technical recession

- Data due at 07:00 GMT, Friday, will be key to sustaining pound’s uptrend

Confounding expectations

The British pound was the second best performing major currency of 2023, ending the year with gains of 5.2% against the US dollar. Unfortunately, the pound’s bullish streak had more to do with out-of-control inflation than an exceptionally strong economy, but nevertheless, the Bank of England looks set to be one of the least dovish central banks in 2024.

On the bright side, the UK economy has been able to withstand several major headwinds far better than anyone anticipated. So although growth has been near stagnant for the past two years, it’s steered clear of a recession. But the risk of one is rising and the fourth quarter of 2023 could be when the economy succumbs to the pain of high interest rates and weak global demand and slips into recession.

On the brink of a recession

Revised data for the third quarter showed that GDP contracted by 0.1% q/q, while in the first month of the fourth quarter, output declined by 0.3% m/m. However, it appears that the economy started regaining some momentum towards the end of the year, driven primarily by a rebound in the services sector, as indicated by the S&P Global PMI surveys. Thus, the British economy may narrowly avoid a recession if the actual data follows in the PMIs’ footsteps.

Analysts expect GDP to have grown by 0.2% m/m in November. This would put the 3-month average at -0.1% so a positive figure is also needed for December to dodge a negative print for the full quarter. But it seems that the recent sharp drop in inflation combined with the BoE putting the brakes on further rate hikes have lifted optimism among UK businesses, raising hopes that GDP eked out modest growth in the final three months of 2023.

Looking at the breakdown of the GDP components, the services sector is expected to have expanded by 0.2% m/m, and manufacturing by 0.3%, while broader industrial output is forecast to have risen by 0.3%.

Can the pound stay on an uptrend?

If the economy fails to expand in November, or even contracts, there would be little chance of any pickup in December being substantial enough to turn quarterly GDP growth positive. The pound is therefore likely to come under pressure from any disappointing figures.

Having bounced off the ascending trendline only last week, cable could again test this crucial support line in such a scenario, putting strain on the $1.26 handle. A break below the trendline would turn the attention on the 50- and 200-day moving averages, which just achieved a golden cross in the $1.2540 region. A steeper selloff could see cable tumbling all the way to the historically congested $1.2375 zone.

However, if the November GDP estimate exceeds expectations, the timing of any recession is bound to be pushed back again along with that of the first rate cut. The pound could extend its latest upswing towards the December high of $1.2827. A successful break above it would quickly bring the $1.3000 mark into scope, which would then raise the prospect of cable surpassing the July peak of $1.3144.

Politics and inflation path will be key for sterling

Investors have pared back some of their dovish expectations for the Bank of England in January following a similar shift in Fed rate cut bets. Nonetheless, a 25-basis-point cut is nearly fully priced in for May, with further similar-sized reductions seen in almost all the remaining meetings of the year.

This would likely keep GBP bulls in check as cumulative rate cut bets for the Fed aren’t significantly higher, although even if UK CPI does fall in line with market expectations, looser fiscal policy domestically is one factor that could compromise the BoE’s fight against inflation.

With a general election likely to take place sometime in the second half of the year, there is speculation the ruling Conservative party will announce fresh tax cuts in the government’s March 6 budget, in addition to those announced in the Autumn Statement. But a Labour win in the election wouldn’t necessarily mean tighter fiscal policy as any reversal in tax cuts would probably be replaced by higher spending.

So to sum up, although the pound’s uptrend lost some steam at the start of the year, the risks in the medium term remain tilted to the upside.

EUR/GBP Technical: Short-Term Relative Weakness of EUR Reasserts Against GBP

- Persistent underperformance of the EUR against GBP as the EUR/GBP cross pair reintegrated below the 200-day moving average.

- The hourly RSI momentum indicator of EUR/GBP has flashed out a bearish momentum condition.

- Watch the 0.8615 key short-term resistance with intermediate supports coming in at 0.8550 and 0.8500.

In the long term, the EUR/GBP cross pair is still evolving within a major downtrend phase as depicted by its price actions’ oscillations within a descending channel in place since the 3 February 2023 swing high of 0.8979 (see Fig 1)

The major downtrend phase has remained intact since 3 February 2023

Fig 1: EUR/GBP medium-term trend as of 9 Jan 2024 (Source: TradingView, click to enlarge chart)

Short-term downside momentum has resurfaced

Fig 2: EUR/GBP minor short-term trend as of 9 Jan 2024 (Source: TradingView, click to enlarge chart)

Recent price actions have staged a bearish breakdown below its 200-day moving average at the start of 2024 on 3 January.

On the hourly chart, the price actions have taken the form of a minor descending channel with a bearish momentum reading seen in the hourly RSI momentum indicator as it staged a bearish reaction right below its parallel resistance at the 50 level.

These observations suggest that the EUR/GBP is likely to be staging a potential bearish impulsive downmove sequence within its major descending channel.

Watch the 0.8615 key short-term pivotal resistance with the next intermediate supports coming in at 0.8550 and 0.8500 (psychological & the swing low areas of 11 July/23 August 2023) next.

On the other hand, a clearance above 0.8615 negates the bearish tone for a minor corrective bounce to see the next intermediate resistance coming in at 0.8650 (also the 200-day moving average).