Sample Category Title

ECB’s Villeroy advocates for caution over haste or rigidity

ECB Governing Council member Francois Villeroy de Galhau, in an address to France's financial sector overnight, stated, "We will cut rates this year when the inflation outlook is solidly anchored at 2% with effective and durable data."

However, Villeroy did not specify a timeline for these potential rate cuts, emphasizing instead the ECB's reliance on economic data to guide their decisions. He asserted, "Our decisions will not be guided by a calendar, but by data."

Villeroy's statement, "We must demonstrate neither obstinateness nor haste," further highlights the ECB's approach as the central bank is keen on avoiding premature actions that could destabilize the disinflation process.

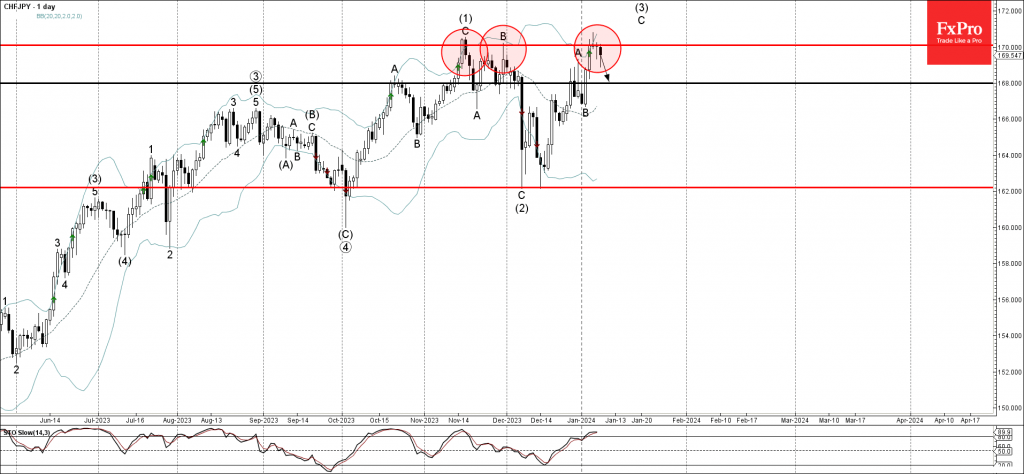

CHFJPY Wave Analysis

- CHFJPY reversed from resistance level 170.00

- Likely to fall to support level 168.00.

CHFJPY currency pair recently reversed down from the pivotal resistance level 170.00 (former Double Top from November) intersecting with the upper daily Bollinger Band.

The downward reversal from the resistance level 170.00 stopped the earlier impulse wave C from the start of this month.

Given the strength of the resistance level 170.00 and the overbought daily Stochastic, CHFJPY can be expected to fall further to the next support level 168.00.

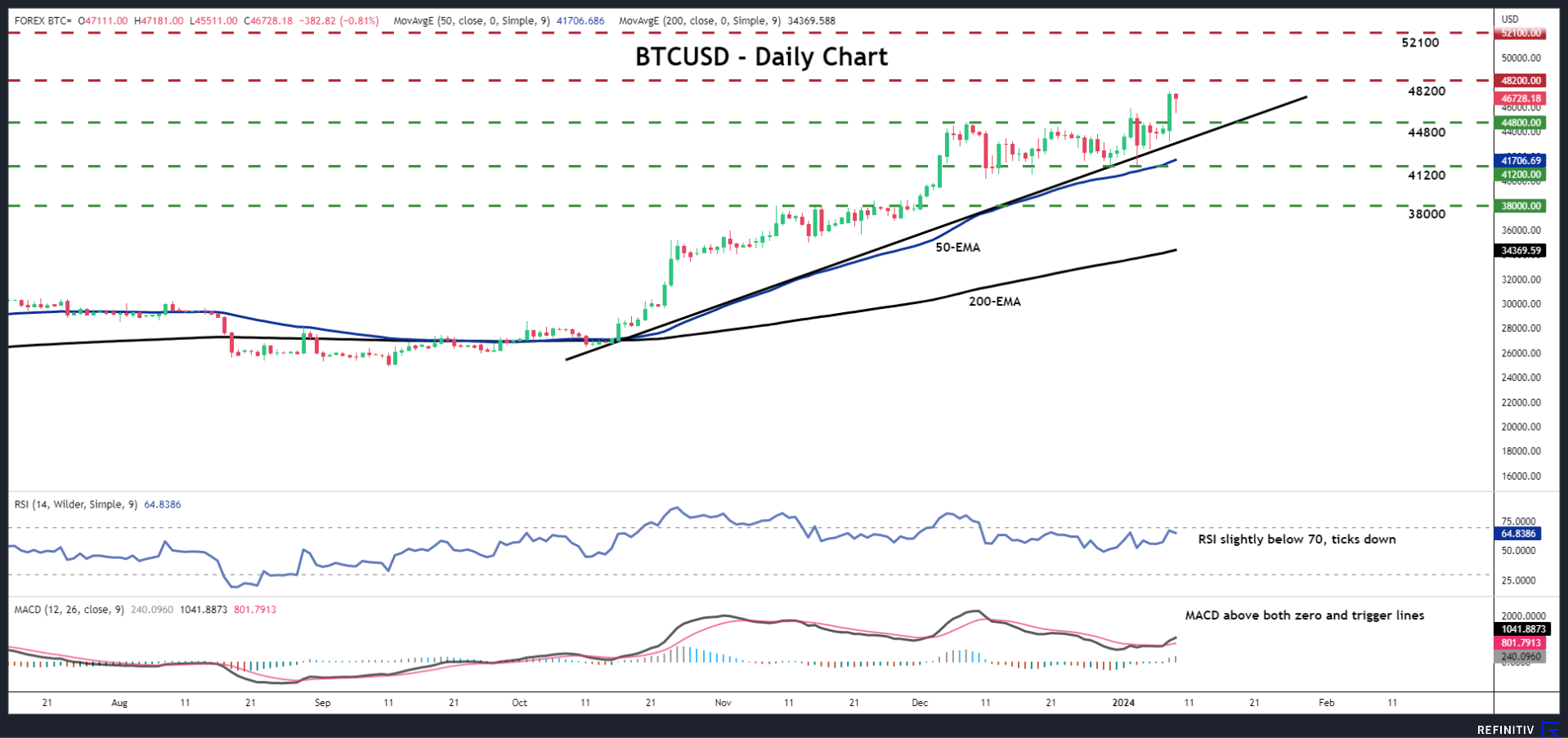

Bitcoin Climbs to New 21-month High Ahead of ETF Decision

- BTCUSD rallies and hits new 21-month high

- RSI and MACD detect positive momentum

- Bearish reversal to be considered upon dip below $41,200

BTCUSD surged yesterday, breaking back above $45,000 and hitting a new 21-month high at $47,282. It seems that the euphoria around the potential approval of a spot-Bitcoin ETF by the Securities and Exchange Commission (SEC) has been the main driver behind the current uptrend, increasing the chances for a sell-the-fact response at the time of the announcement.

That said, from a technical standpoint, even if the crypto king corrects lower, provided it stays above the uptrend line drawn from the low of October 13 and above the 50-day EMA, which has been tracking the advance well, the near-term outlook could still be considered positive. A break above the highs of March 2022 at around $48,200 could signal a trend continuation and perhaps pave the way towards the high of December 27, 2021, near $52,100.

The RSI and the MACD are both detecting positive momentum, with the former lying slightly below 70 and the latter running above both its zero and trigger lines. However, the RSI has ticked down after hitting resistance near its 70 line, which increases the likelihood of a small pullback before the next leg north.

For the outlook to start darkening, Bitcoin may need to dive below the $41,200 zone, which offered support several times since December 11. A break below that barrier may not only confirm the dip below the aforementioned uptrend line but also a violation of the 50-day EMA. The bears may then be encouraged to push the action down to the $38,000 area.

To recap, BTCUSD has been in uptrend mode since October in anticipation of a regulatory approval for Bitcoin-backed ETFs. The announcement of the approval may result in a corrective setback, but for a trend-reversal to start being discussed, a dip below $41,200 may be needed.

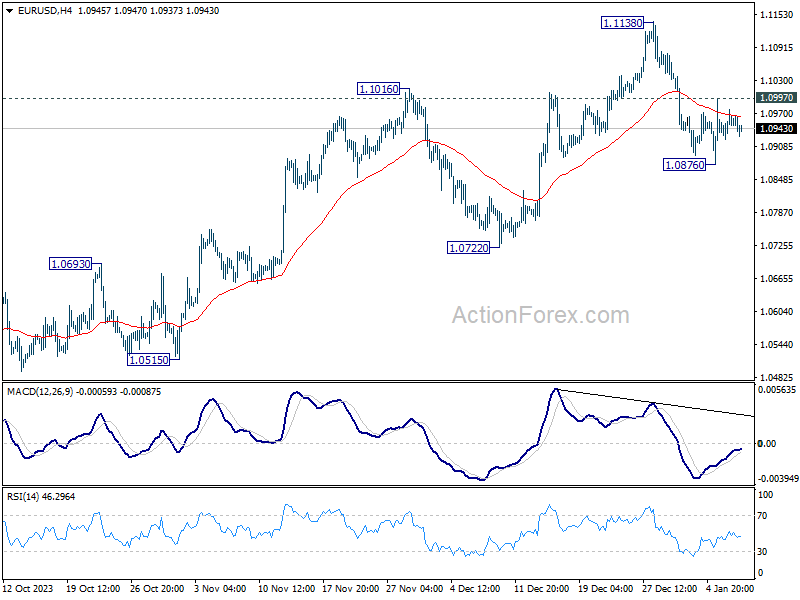

EUR/USD Price Action – Technical Analysis

EURUSD continues its attempt to reverse back above the 1.1000 level but has been unsuccessful so far, the current trading range is critical, and any real breakout may help in forecasting future price action, we will go over a long-term as well as a short-term timeframe reflecting the current price action.

Talking Points

- Weekly Chart – Longer Term Patterns overview

- 1-Hour Chart – Short Term and current price action

Weekly Chart

- Price continues to trade below its ascending channel as identified on the chart, Price action broke below the lower trendline in August 2023 and so far, 2 pullbacks have taken place where both times price found resistance and was unable to reenter the channel again.

- The two pullbacks are currently in a double-top formation and the connecting baseline is marked on the chart.

- A confluence of support is represented by the baseline, Monthly pivot point, and EMA9.

1-Hour Chart

- EURUSD price action continues to trade within the range of 1.0920 – 1.0980, a confluence zone of support and resistance levels represented by monthly and annual calculations.

- Last month, December 2023, the price broke and closed above its annual pivot point of 1.0920, a critical level where the price spent an extended time trading around, the most recent EURUSD price decline in January 2024, took the rate back to 1.0920 where it is so far finding support.

- Price action broke out and closed above the upper resistance line of the descending channel (Green line), a throwback to the line took place on Friday with the Non-Farm Payroll release, however, price action found support above the green line and reversed back up.

- A triple bottom formation developed above the breakout and the price broke out again above the resistance line connecting the inverted bases for the bottoms. (Dotted black line)

- Price action is currently attempting an inverted Head and Shoulder formation, which is yet to materialize in full, the neckline lies at the 1.0980 – 1.0990 area which is the high end of the extended trading range, as well as the psychological level of 1.1000, which if penetrated along with price move following the pattern, may lead price action to the upcoming resistance levels. It is also important to remember that pattern failures can be an indication of a potential change in direction.

Sunset Market Commentary

Markets

Economic data were few today. Still core bond yields continued the bottoming out process that started last week, with Europe this time taking the lead. German yields are rising between 5-6 bps across the curve. Supply obviously was the name of the game today. According to Bloomberg analyses, a record of at least (probably more) than €43 bln of bonds (financials corporates and government related paper) was to be priced today. The sale of a dual Italian 7-y (€10 bln, new syndication 2031 bond) and 30-y tap (€5 bln) enjoyed ample investor buying interest, with books of the 30-y sale reported at a record of over €91 bln. The spread on the 10-y BTP even eased marginally in a daily perspective (-2 bps). Belgium also successfully launched the new 10-y October 2034 OLO 100 bond. The Belgian debt agency sold €7 bln at MS +24 bps with investor demand said to have been in excess of €72 bln. US yields for now outperform Bunds with yields easing between 1.5 bps (2-y) and 2.5 bps (30-y) The US Treasury will start its monthly refinancing with the sale $52 bln of 3-y notes later today. For now, investors apparently didn’t ask big price concessions going into the sale. Market resilience, amongst others, probably suggests that investors prepare for rather soft US December CPI data, to be published on Thursday. Even so, investors’ appetite for credit didn’t positively inspire broader risk sentiment. On the contrary, European equities failed to build on yesterday’s quite impressive US tech rally. The EuroStoxx 50 is ceding 0.75%. US indices also open up to 0.70% at the open (Nasdaq) as investors take a more cautious approach going into the start of the earnings season. Yesterday’s setback in the oil price is partially reversed with Brent oil again trading north of $77 p/b.

On FX markets, the dollar wins in on points (DXY 102.38), but the picture remains unchanged/indecisive. EUR/USD also declines marginally (1.094), but even first minor support (1.0877) stays out of reach. The yen slightly outperforms (USD/JPY 143.85). EUR/GBP after yesterday’s decline tried to sustain below the 0.86 big figure, but further sterling gains for now are running into resistance. Poor BRC retail sales data this morning questioned more positive news from the December PMI’s.

News & Views

French President Macron named Gabriel Attal, currently education minister, as new Prime Minister in a high profile government reshuffle to boost his party’s dwindling support ratings ahead of European elections later this year. A 10-point polling gap recently opened up with Marine Le Pen’s far-right party (RN). Macron’s government was also dealt a humiliating defeat back in December on long-promised immigration reforms. Lacking a parliamentary majority since 2022 elections, opposition parties initially united to block the reforms. Macron had to toughen his proposal to eventually win the backing of Le Pen’s RN. Gabriel Attal will be the youngest French PM (34y), replacing Elisabeth Borne. He is widely considered to be Macron’s heir in 2027 presidential elections when Macron hits his term limit.

Hungary’s full-year budget deficit was 4.59tn forint in 2023. The Finance Ministry initially targeted 2.28tn HUF, but the Orban government gradually raised the target from 3.9% of GDP via 5.2% of GDP to eventually 5.9%. Economy minister Nagy already questioned whether this year’s deficit target of 2.9% of GDP was reasonable given the size of the adjustment it would require. Rating agency Fitch in December suggested that a deficit narrowing up to 4.2% of GDP was a more likely scenario given that the Ministry of National Economy plans to keep the investment rate above 25% of GDP and wants to increase the employment rate to 85% via direct government programs. The Hungarian forint trades in the defensive today with EUR/HUF rising from 377.50 to 379. Separately, the Hungarian statistical office announced that industrial production declined by 5.6% Y/Y in November. In the first eleven months of the year industrial production was 4.8% lower than in the same period of 2022.

Canada’s Trade Accounts Register a $1.6 Billion Surplus in November

Canada’s merchandise trade surplus notched its fourth consecutive month in black ink. However, November's surplus narrowed to $1.6 billion as imports rose and exports edged lower. This comes after October's surplus was revised upward to $3.2 billion.

Exports fell slightly by 0.6% month-on-month (m/m) in November, the first decline in four months. The contribution to the drag was narrowly-based, driven by a -16.8% decrease in aircraft and other transportation equipment exports. In fact, 7 of 11 sectors posted a rise in exports, including a 1.3% m/m increase in energy product exports and a 4.4% m/m increase in industrial machinery exports.

Meanwhile, total imports increased by 1.9% m/m in November, with 8 of 11 sectors rising on the month. Imports of energy products (11.6% m/m) posted its first increase after two consecutive monthly declines. Meanwhile, imports of machinery and equipment were up by 4.9% m/m and imports of electronic and electrical equipment rose by 4.7% m/m.

In volume terms, overall imports increased by 1.6% m/m in November (after a large 3.5% m/m drop the month prior), while exports edged down slightly by 0.1% m/m.

Canada's trade surplus with the United States narrowed from $12.1 billion in October to $11.7 billion in November.

Key Implications

October and November trade data suggests that net trade may shape up to be a tailwind for fourth quarter growth. This would mark a reversal from last quarter's significant growth revisions that hit net trade more than any other GDP component. The solid performance of the Canadian dollar at the end of 2023 (up over 2% versus the USD in December), may potentially dampen export activity in next month's trade reading.

Despite the potential positive effects from trade in the fourth quarter, overall Canadian economic growth is expected to be weak as domestic and international activity slows. Imports, a barometer for domestic demand, have been effectively flat (in real terms) over 2023.

U.S. Small Business Optimism Improved Moderately at End of 2023

NFIB's Small Business Optimism Index rose 1.3 points to 91.9 in December, coming in above market expectations for a modest increase. Despite the increase, the index was still 6 points below its historical average of 98 points.

Five of the ten subcomponents improved on the month, three deteriorated, and two remained unchanged. Leading the gains were earning trends (up 7 points to -25%), along with expectations about an improvement in the economy (up 6 points to -36%) and higher real sales (up 4 points to -4%). On the other hand, current inventory took a notable step back, falling 5 points to -5%.

The share of businesses planning to increase employment fell 2 points to a still-decent 16%, while the share of firms with unfilled job openings held steady for the second consecutive month at 40%. Of note, quality of labor concerns fell 4 points, with 20% of business owners identifying this as their top business problem. Given the sharp drop in the latter, inflation replaced labor quality as the top concern among small business owners (up 1 point to 23%).

The share of firms increasing compensation was unchanged at 36%, the same as in the pre-pandemic period. Meanwhile, the share of firms planning to raise compensation over the next three months fell one point to 29%, which is not far off the 32% historical high set earlier in the pandemic. The share of businesses 'raising' average selling prices was unchanged at 25%, while the share of firms planning price hikes in the next three months fell 2 points to a still elevated 32%.

Key Implications

The improvement in small business confidence at the end last year – albeit from low levels – is encouraging, especially since it was accompanied by enhanced outlooks on the economy, earnings trends and sales. What's more, labor market indicators continue to show resilience, with job opening still plentiful and businesses continuing to place a focus on hiring workers. Nonetheless, it's worth noting that this latter theme is gradually losing some of its luster. This is evidenced by a gradual easing in plans to boost employment, and the fact that quality of labor concerns pulled back notably in December.

With the labor market still tight, the share of businesses planning to raise compensation in order to retain and attract new workers remains elevated. The share of businesses planning to raise average selling prices has also trended higher, which points to some upside risk for inflation over the near-term – a factor that would work in favor of the Fed showing some patience before it begins to lower interest rates later this year.

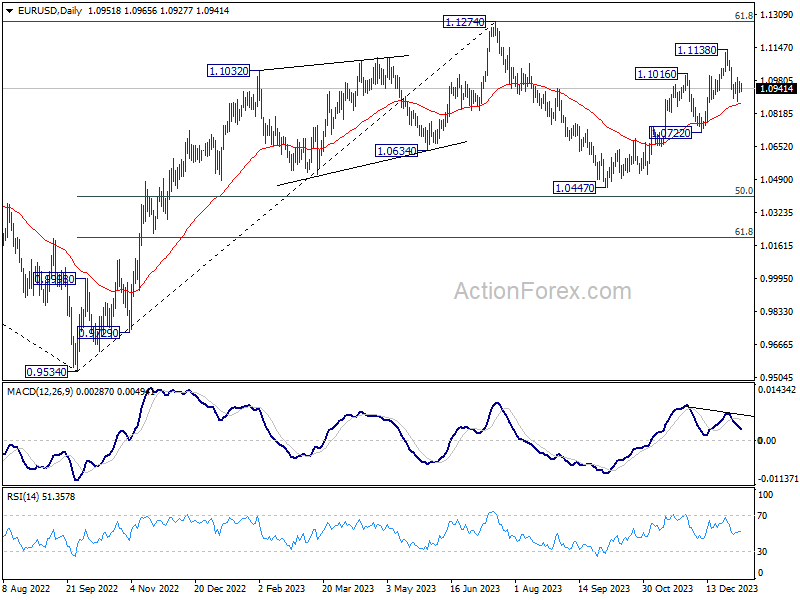

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0922; (P) 1.0951; (R1) 1.0978; More...

Range trading continues in EUR/USD and intraday bias remains neutral at this point. On the downside break of 1.0876 will resume the fall from 1.1138 short term top to 1.0722 support next. However, break of 1.0997 will turn bias back to the upside for retesting 1.1138 high instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

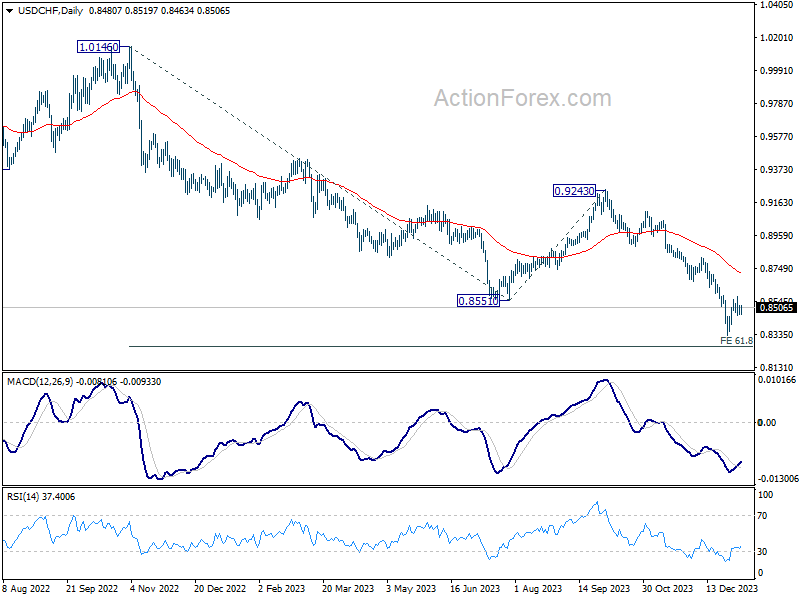

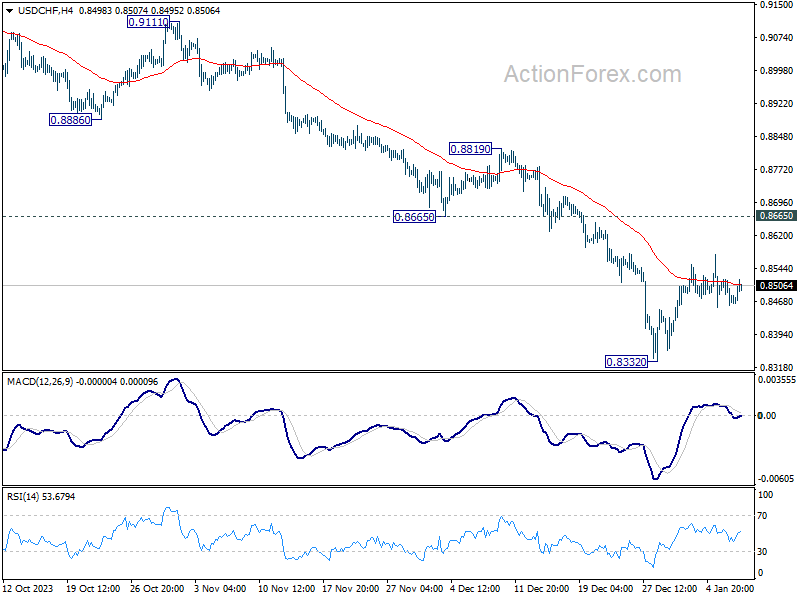

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8453; (P) 0.8488; (R1) 0.8516; More....

USD/CHF is extending the consolidation from 0.8332 and intraday bias stays neutral. While recovery could extend higher, outlook will stay bearish as long as 0.8665 support turned resistance holds. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, the down trend from 1.0146 (2022 high) is in progress. Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.