Sample Category Title

Why Silver Prices in the US and China Have Diverged So Sharply

- The price gap between silver in the US and in Shanghai has widened and is larger than normal.

- Western prices are driven mainly by futures and paper trading, while Chinese prices reflect physical supply and demand.

- Strong industrial and investment demand for physical silver in China supports a persistent price premium.

- Logistical and regulatory barriers limit arbitrage, allowing the divergence to last.

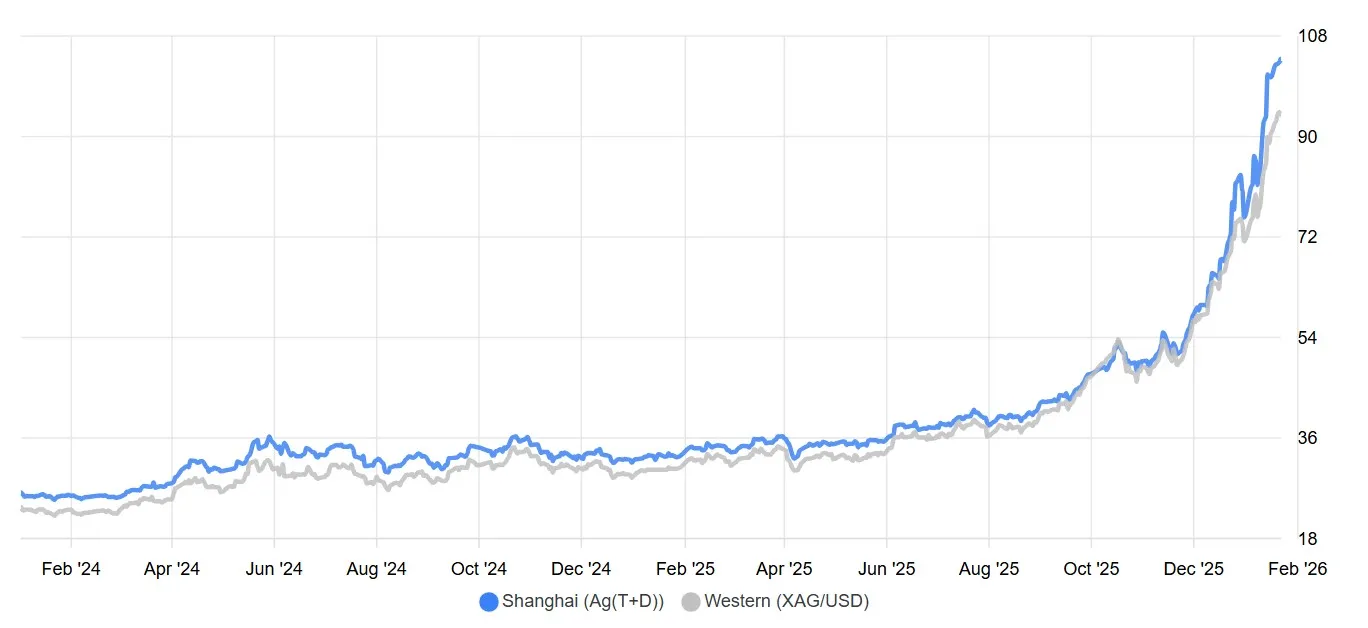

In recent weeks, the gap between silver prices in the United States and China has widened noticeably and is now larger than usual. According to the chart, silver is currently priced at around USD 94 per ounce in the US, while the equivalent price in Shanghai is roughly USD 104 per ounce after currency conversion. A spread of nearly USD 10 per ounce is not a minor discrepancy but a meaningful signal that the two markets are being driven by different forces.

This divergence is not primarily the result of exchange rates or transaction costs. Instead, it reflects fundamental differences in market structure, pricing mechanisms, and local supply and demand dynamics.

Chart compares daily silver prices from the Shanghai Gold Exchange with Western silver prices, converted to USD/oz using daily CNY/USD rates

Chart compares daily silver prices from the Shanghai Gold Exchange with Western silver prices, converted to USD/oz using daily CNY/USD rates

Paper pricing versus physical metal pricing

In the US and Europe, silver prices are largely determined on markets such as COMEX and in London, where futures contracts and financial instruments dominate trading activity. The vast majority of these contracts are settled financially rather than through physical delivery. As a result, prices tend to reflect liquidity conditions, speculative positioning, movements in the US dollar, and interest rate expectations more than the immediate availability of physical silver.

In China, pricing works differently. On the Shanghai Gold Exchange and the Shanghai Futures Exchange, physical delivery plays a far more important role. Prices in Shanghai are therefore much more closely tied to actual demand for metal that can be taken out of the exchange system. When demand for physical silver rises, this pressure is quickly reflected in higher local prices.

Strong physical demand in China

A key driver of the current premium in Shanghai is strong physical demand for silver in China. Silver is a strategically important industrial metal, used extensively in solar panels, electronics, and advanced manufacturing. In addition, Chinese investors tend to place greater emphasis on owning physical bullion rather than paper exposure.

When this demand intensifies, local supply can become tight. In such an environment, the market clears not through higher trading volumes in derivatives, but through higher prices for immediately available metal, pushing Shanghai prices well above Western futures-based benchmarks.

Supply, inventories, and logistics

Differences in local inventories and logistics also matter. If physical silver stocks in China are relatively low while demand remains strong, prices must rise to balance the market. In the US and Europe, where inventories are larger and financial instruments dominate, similar demand pressures may not show up as quickly in prices.

At the same time, moving physical silver between regions is costly and complex. Transportation, certification, regulatory requirements, and capital constraints all limit how easily silver can flow from lower-priced markets to higher priced ones. These frictions allow price gaps to persist.

Why arbitrage does not eliminate the gap

In theory, a USD 10 per ounce price difference should invite arbitrage. In practice, arbitrage in the silver market is far from frictionless. Access to deliverable metal, export and import rules, and the time and cost involved in moving bullion across borders significantly weaken the arbitrage mechanism.

As a result, the price link between COMEX and Shanghai is looser than many investors assume, allowing China to trade at a sustained premium.

What the current 94 vs 104 USD spread is telling us

The current situation - around USD 94 per ounce in the US versus about USD 104 per ounce in Shanghai - suggests that:

- physical silver is relatively scarcer and more highly valued in China than in Western markets,

- Western “paper” prices may not fully reflect physical market tightness,

- the physical market is sending an early signal of supply-and-demand stress.

Historically, such sustained premiums on physical markets have often preceded either higher global prices or periods of increased volatility as Western markets eventually react.

Silver ETFs see heavy outflows despite firm prices

Since the start of the year, silver-focused exchange-traded funds have recorded substantial withdrawals. Data from Bloomberg show that ETF holdings of silver fell by around 528 tonnes within the first two weeks of the year. A significant share of this reduction came from the largest silver-backed ETF in the United States.

The rapid appreciation in silver prices appears to have prompted many ETF investors to lock in gains, although part of the decline in holdings may also be linked to physical metal being removed from ETF vaults. Notably, these outflows have not translated into downward pressure on prices, indicating that demand from other parts of the market has absorbed the metal.

A comparable dynamic was seen in the palladium market several years ago, when ETF inventories fell sharply even as prices continued to climb. At that time, ETF disinvestment contributed to alleviating tight physical supply conditions. That said, it remains premature to assume a similar outcome for silver, and the current developments should be interpreted cautiously.

Conclusion

The growing gap between silver prices in the US and in Shanghai highlights the contrast between a financially driven paper market and a physically driven commodity market. The unusually large premium in China indicates that real, deliverable silver is currently more valuable there than futures-based pricing in the West suggests. While this does not guarantee an immediate global repricing, it is a signal that the physical side of the silver market is under pressure and one that global investors would be wise to watch closely.

Dollar Played Out TACO Trade

- Trump’s retreat helped the EURUSD bears.

- USDJPY intends to resume its uptrend.

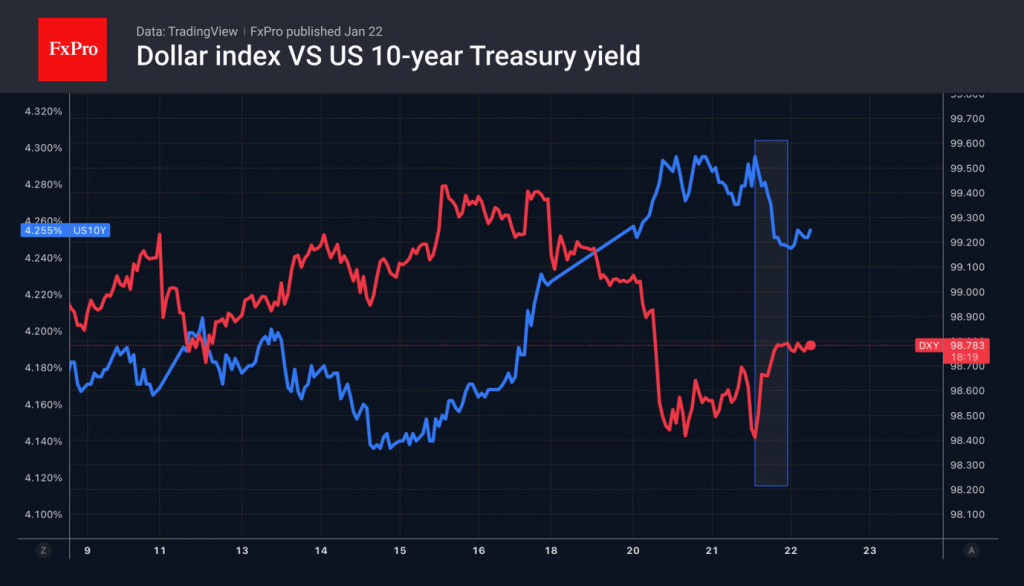

The US dollar got the upper hand after Donald Trump’s speech in Davos. The US president announced that there was some framework for a deal on Greenland and that he was abandoning his intention to impose additional tariffs on a number of European countries. The markets immediately switched from ‘sell America’ to TACO-trade or Trump-Always-Chickens-Out mode. Stock indices rose, Treasury yields fell, while EURUSD bears went on the counterattack.

The Supreme Court did not support the White House’s intention to dismiss Lisa Cook from her position as FOMC governor. The judges recognised that this could undermine the independence of the Fed. They are considering various options. The most conservative would be to keep the official in office while the lower courts discuss her mortgage case. The most radical would be to write a broad ruling on the extent of the president’s authority to remove members of the central bank.

The USD index received support from the SWIFT report, which showed that the share of the greenback in international transactions rose from 46.8% to 50.5% in December, reaching its highest level since 2023. De-dollarisation is not an urgent matter against the backdrop of a division between the West and the East. The US currency keeps its dominance and is still in demand.

The strengthening of the US dollar has been a tailwind for USDJPY. The pair risks quickly resuming its upward trend and coming under currency intervention due to large-scale sell-offs of Japanese bonds. The yield on 30-year bonds saw the biggest one-day jump in history, while yields on 10-year bonds reached their highest since 1999. Sanae Takaichi’s hints at abolishing the consumption tax on food products are forcing the Ministry of Finance to rack its brains over where to get the money.

Concerns about the financial stability of debt-ridden Japan are compounded by uncertainty over the outcome of the parliamentary elections scheduled for 8 February. The LDP’s long-time ally, Komeito, has joined the opposition, so Sanae Takaichi’s success is not guaranteed.

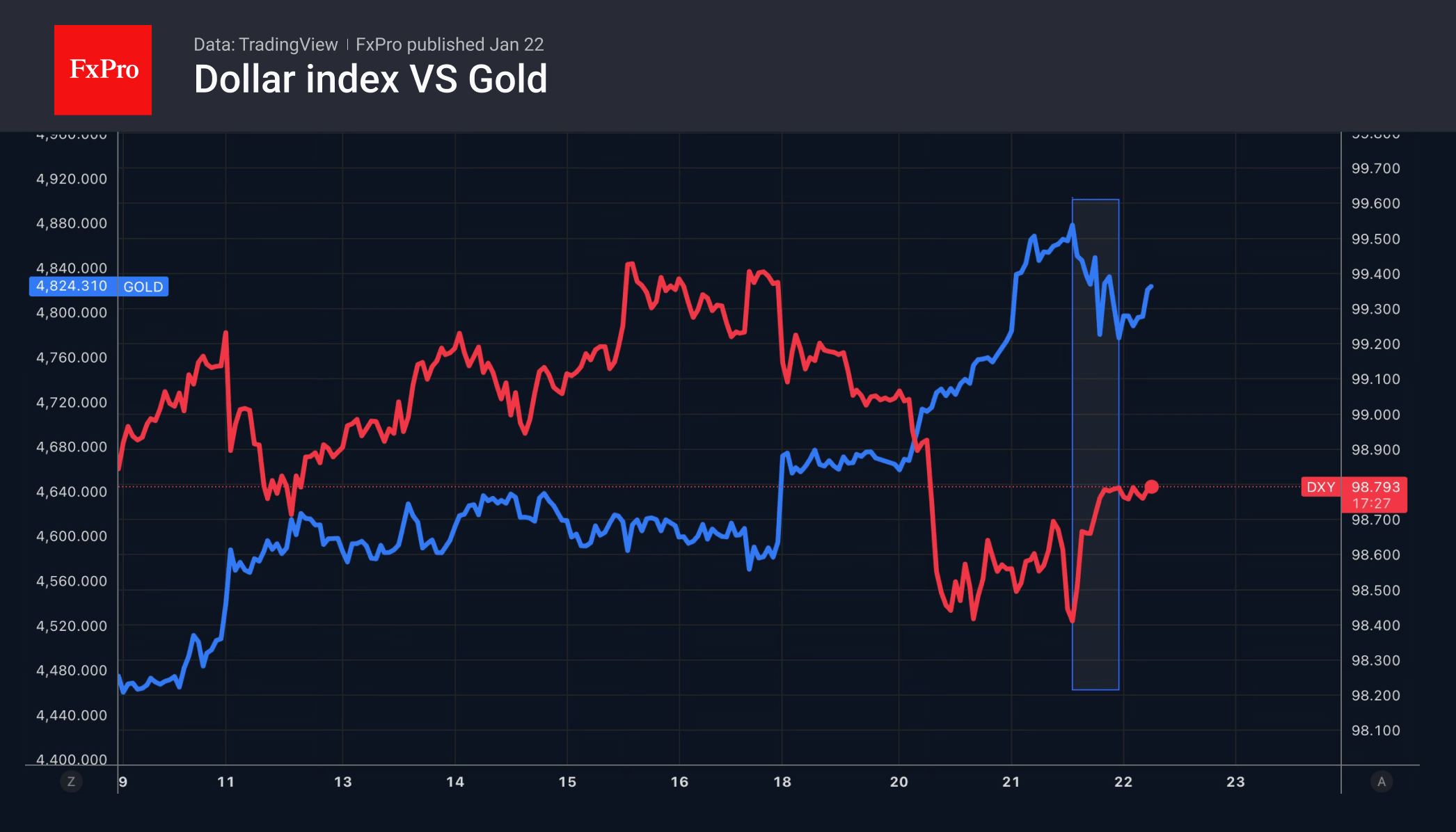

Donald Trump’s retreat, the Supreme Court’s defence of the Fed’s independence and the strengthening of the US dollar could have sent gold into a knockout. However, the precious metal took only a modest step back, and Goldman Sachs raised its forecast for the gold price from 4900 to 5400 per troy ounce by the end of 2026.

US Dollar Strengthens After Trump’s Statements on Greenland

During his visit to the World Economic Forum in Davos, Donald Trump softened his stance on claims over Greenland. According to media reports, the US President pledged not to use military force against NATO allies and also withdrew threats to impose tariffs on goods from several European countries. This eased geopolitical tensions, leading not only to a recovery in US equities but also to a strengthening of the US dollar.

The USD/JPY chart, for example, shows the US dollar gaining ground against the yen (marked by the orange arrow), which is under pressure ahead of the Bank of Japan’s interest rate decision scheduled for tomorrow.

Technical Analysis of the USD/JPY Chart

In late December, when analysing movements in the dollar–yen exchange rate, we identified a long-term ascending channel that remains valid (with a slight adjustment to reflect January data).

The lower boundary of this channel continues to act as solid support, but it is under threat because:

→ as indicated by the red arrow, bears are asserting control over the lower internal trendlines within the channel;

→ today’s peak (B) only marginally exceeds the high of 15 January (A). This resembles a bull trap, and a failed attempt to move higher could trigger renewed bearish pressure.

How the situation develops next will largely depend on a dense and rapidly changing news backdrop. In addition to the drivers already mentioned, attention should be paid to the release of US GDP data and initial jobless claims (scheduled for today at 16:30 GMT+3), which could have a significant impact on USD/JPY dynamics.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

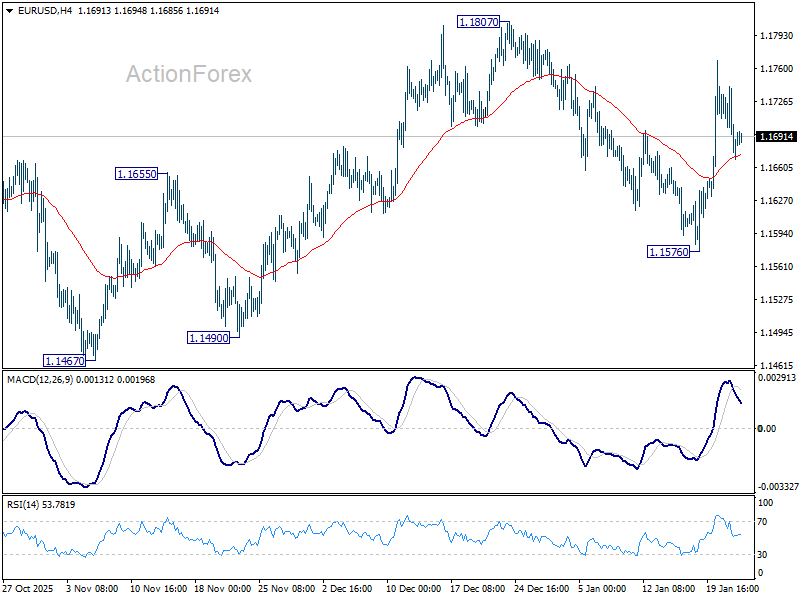

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1660; (P) 1.1701; (R1) 1.1727; More….

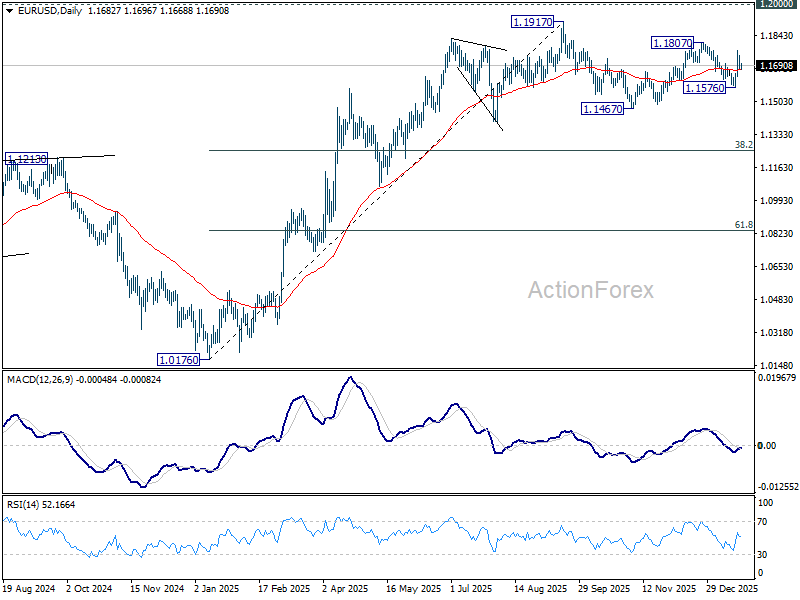

EUR/USD retreated well ahead of 1.1807 resistance and intraday bias is turned neutral. Risk will stay on the upside as long as 55 4H EMA (now at 1.1672) holds. Break of 1.1807 will will resume whole rally from 1.1467, and target a retest on 1.1917 key resistance level. However, sustained trading below 55 4H EMA will bring deeper fall back to 1.1576 support instead.

In the bigger picture, as long as 55 W EMA (now at 1.1413) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

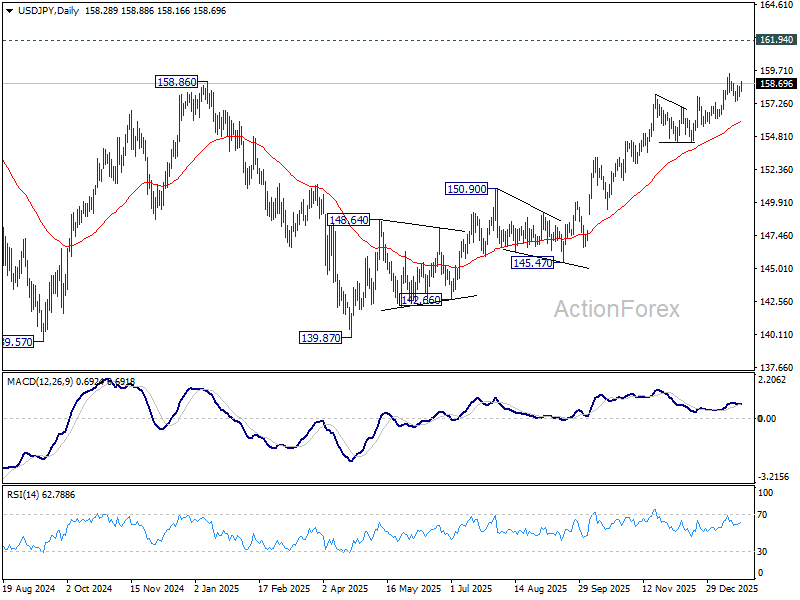

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.86; (P) 158.19; (R1) 158.64; More...

USD/JPY is still bounded in consolidations below 159.44 and intraday bias stays neutral. With 156.10 support intact, outlook remains bullish. On the upside, break of 159.44 will resume the rise from 139.87 towards 161.94 high. However, firm break of 156.10 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.86 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

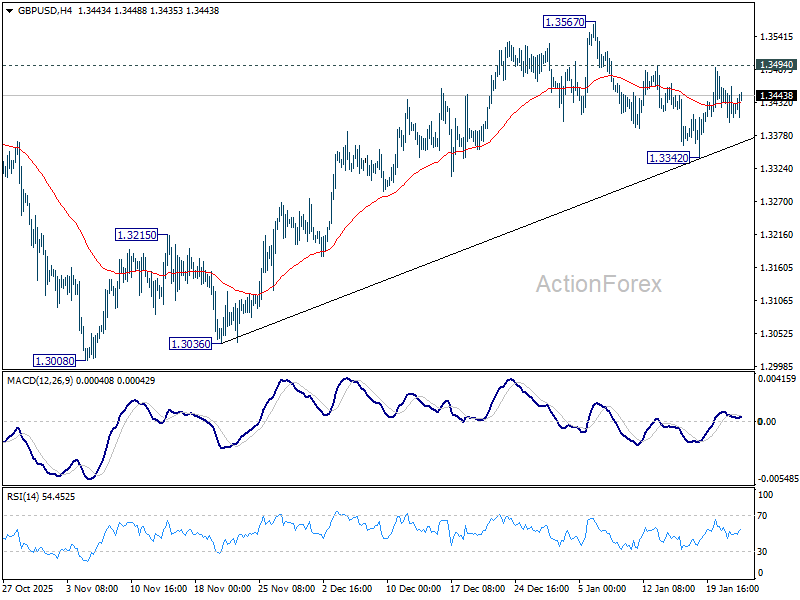

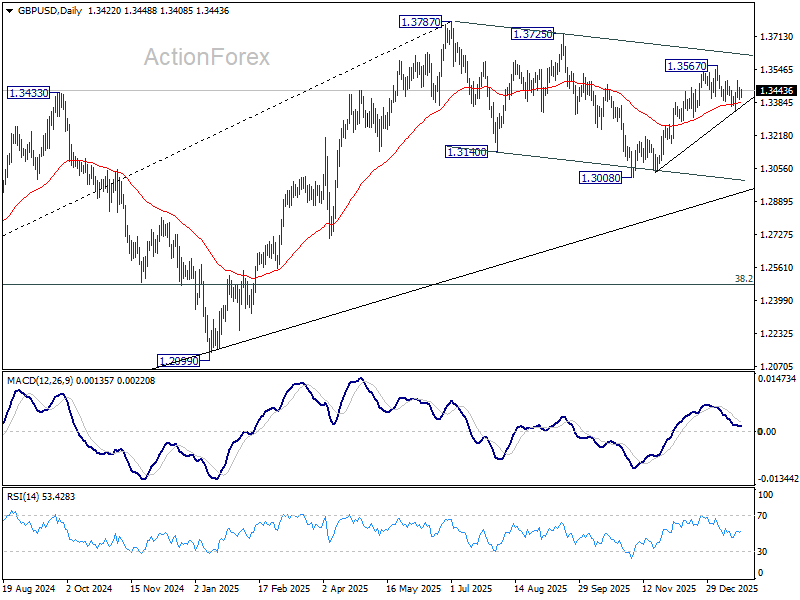

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3400; (P) 1.3430; (R1) 1.3458; More...

Range trading continues in GBP/USD and intraday bias stays neutral. On the upside, firm break of 1.3494 will suggest that pullback from 1.3567 has completed at 1.3342, after drawing support from 55 D EMA (now at 1.3382). Intraday bias will be back on the upside for 1.3567 first. Break there will resume the rally from 1.3008 to retest 1.3787 high. On the downside, sustained trading below 55 D EMA will argue that the decline is another falling leg in the corrective pattern from 1.3787.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

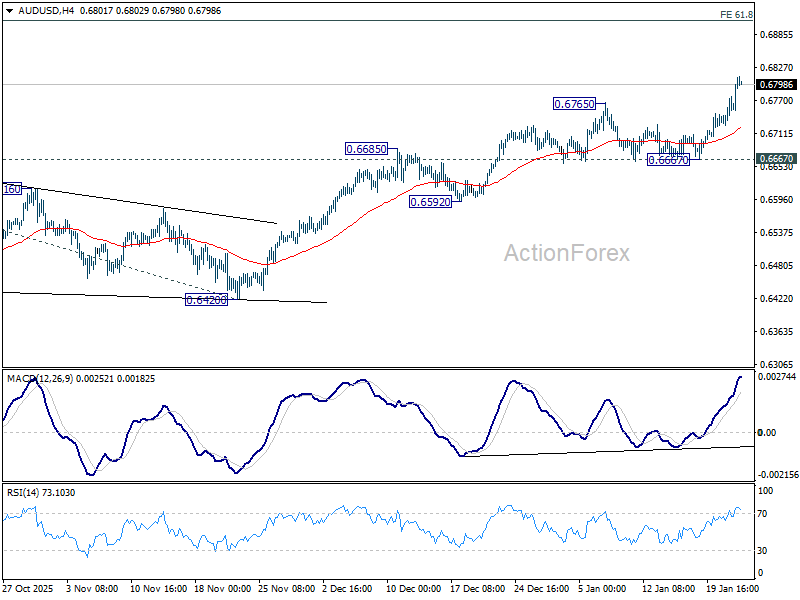

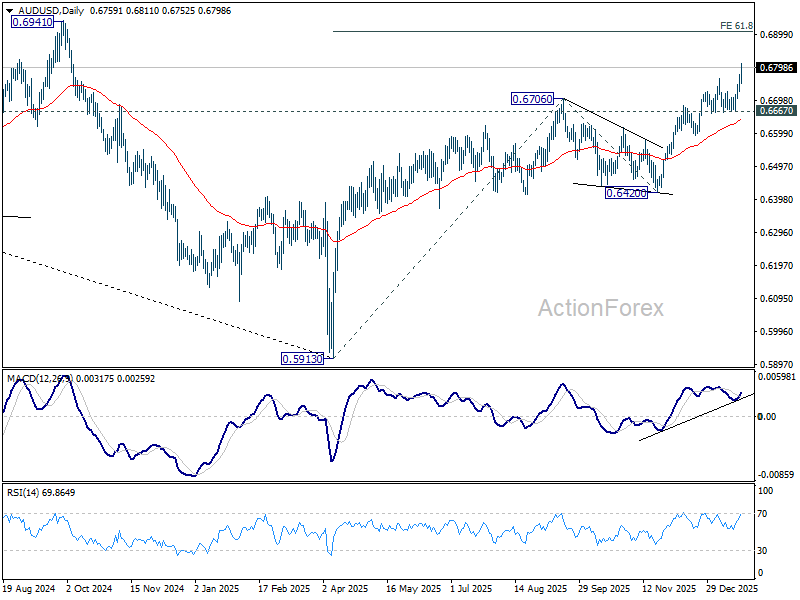

AUD/USD Daily Report

Daily Pivots: (S1) 0.6734; (P) 0.6756; (R1) 0.6784; More...

Intraday bias in AUD/USD remains on the upside for the moment. Current rise is part of the whole rally from 0.5913. Next target is 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. For now, near term outlook will stay bullish as long as 0.6667 support holds, in case of retreat.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6420 support holds, even in case of deep pullback.

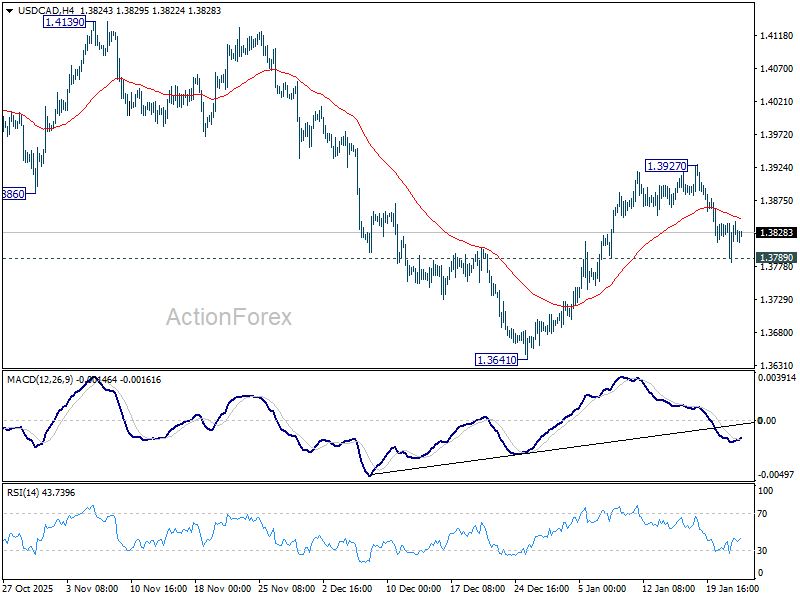

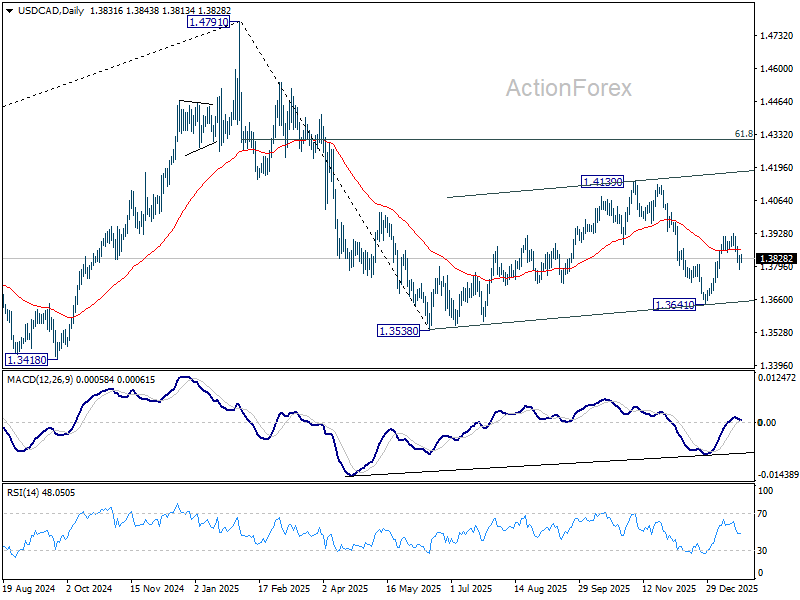

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3800; (P) 1.3821; (R1) 1.3857; More...

Intraday bias in USD/CAD stays neutral and further rise is still mildly in favor with 1.3789 support intact. Break of 1.3927 will resume the rebound from 1.3641, as part of the corrective pattern from 1.3538, towards 1.4139. However, firm break of 1.3789 will bring deeper fall back to 1.3538/3641 support zone.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral until there are signs that the correction has completed.

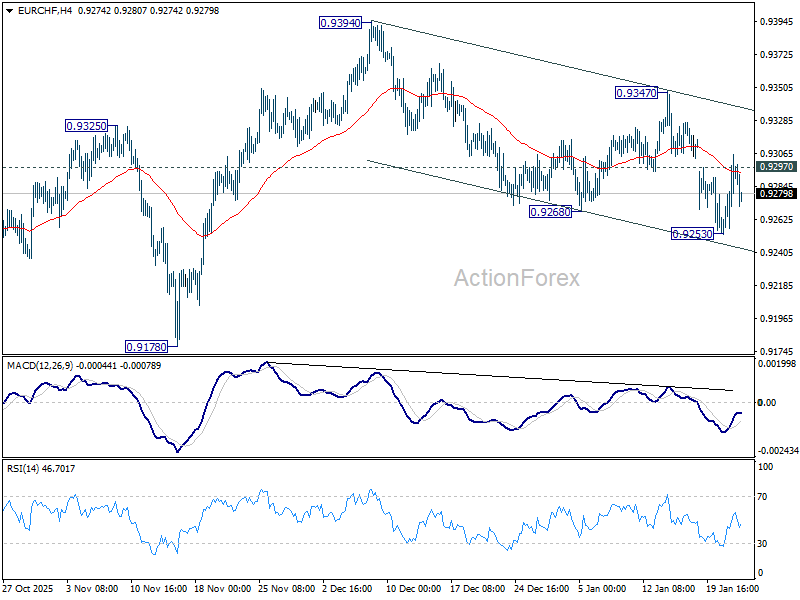

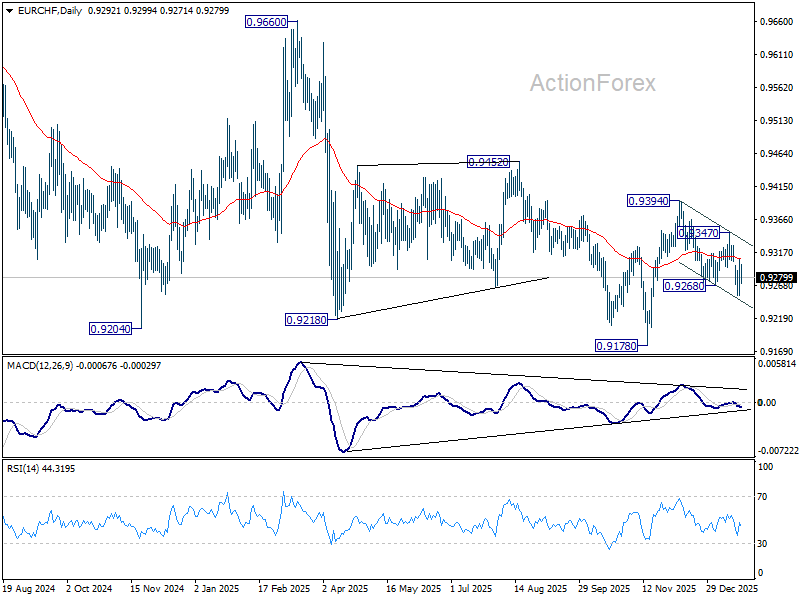

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9255; (P) 0.9282; (R1) 0.9322; More....

Intraday bias in EUR/HF is turned neutral first with breach of 0.9297 minor resistance. Another fall will remain mildly in favor as long as 0.9347 resistance holds. Below 0.9253 will extend the decline from 0.9394 towards 0.9178 low. Nevertheless, firm break of 0.9347 will indicate that fall from 0.9394 has completed as a correction, and bring stronger rally to retest this resistance.

In the bigger picture, persistent bullish convergence condition in W MACD is a medium term bullish sign. Firm break of 0.9394 resistance should bring sustained trading above 55 W EMA (now at 0.9360). That should indicate medium term bottoming at 0.9178. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9928 resistance next, even still as a corrective bounce. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9178 at a later stage.

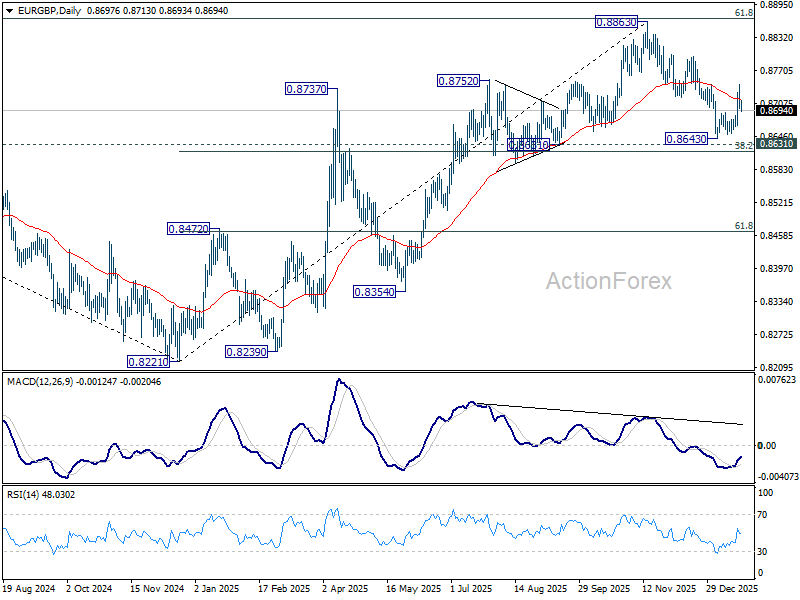

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8686; (P) 0.8716; (R1) 0.8733; More…

Intraday bias in EUR/GBP is turned neutral first with current retreat. On the downside, firm break of 0.8691 resistance turned support will suggest that rebound form 0.8643 has completed as a corrective bounce. Rejection by 55 D EMA (now at 0.8717) will keep the fall from 0.8863 intact. Intraday bias will be back on the downside for 0.8643 low first, and then 0.8631 cluster support (38.2% retracement of 0.8221 to 0.8663 at 0.8618).

In the bigger picture, rise from 0.8221 medium term bottom (2024 low) is seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8623) should confirm that this corrective bounce has completed. In this case, deeper fall would be seen back to 0.8201/21 key support zone. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.