Sample Category Title

USD/JPY Upside Resumes, Opening Door To Further Gains

Key Highlights

- USD/JPY started another increase from the 157.50 support.

- A major bullish trend line is forming with support at 158.00 on the 4-hour chart.

- AUD/USD and NZD/USD gained bullish momentum and outperformed other majors.

- Gold started a consolidation phase after trading to a new record high above $4,880.

USD/JPY Technical Analysis

The US Dollar remained stable near 157.50 against the Japanese Yen. USD/JPY formed a base and started a fresh increase above 158.00.

Looking at the 4-hour chart, the pair climbed above 158.20 and the 50% Fib retracement level of the downward move from the 159.45 swing high to the 157.42 low. The pair is now well above the 200 simple moving average (green, 4-hour) and the 100 simple moving average (red, 4-hour).

Immediate resistance sits near 159.00 and the 76.4% Fib retracement level of the downward move from the 159.45 swing high to the 157.42 low. A close above 159.00 could open the doors for a move toward 159.50. Any more gains could set the pace for a steady increase toward 150.00.

If there is no move above 149.00, there could be a fresh downside correction. On the downside, immediate support is near the 158.20 level. The first major area for the bulls might be near 158.00.

There is also a major bullish trend line forming with support at 158.00. A close below 158.00 might spark heavy bearish moves. The next support could be 157.50 or the 100 simple moving average (red, 4-hour), below which the bears might aim for a move toward the 200 simple moving average (green, 4-hour) at 156.80.

Looking at Gold, the price started a consolidation phase, but the bulls might soon aim for more gains above the $4,880 zone.

Upcoming Key Economic Events:

- US S&P Global Manufacturing PMI for Jan 2026 (Preliminary) – Forecast 52.1, versus 51.8 previous.

- US S&P Global Services PMI for Jan 2026 (Preliminary) – Forecast 52.8, versus 52.5 previous.

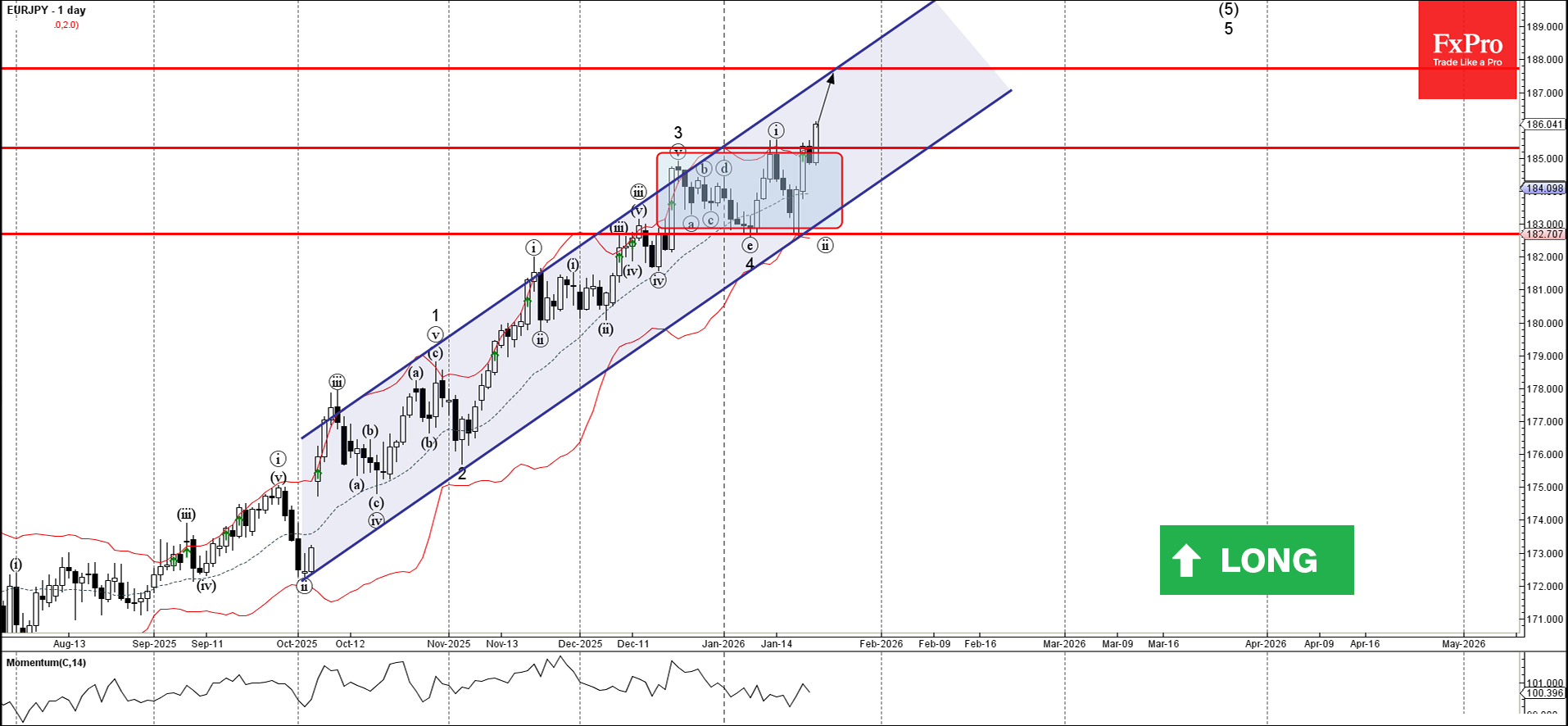

EURJPY Wave Analysis

EURJPY: ⬆️ Buy

- EURJPY broke resistance level 185.30

- Likely to rise to resistance level 188.00

EURJPY currency pair recently broke above the resistance level 185.30 (which is the upper border of the sideways price range inside which the price has been moving from December).

The breakout of this resistance level 185.30 accelerated the active impulse waves 5 and (5).

Given the strong daily uptrend, rising daily Momentum and the strongly bearish yen sentiment see across the FX markets today, EURJPY currency pair can be expected to rise to the next resistance level 188.00.

Eco Data 1/23/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.60% | 0.50% | 1.00% | |

| 21:45 | NZD | CPI Q/Q Q4 | 3.10% | 3.00% | 3.00% | |

| 22:00 | AUD | Manufacturing PMI Jan P | 52.4 | 51.6 | ||

| 22:00 | AUD | Services PMI Jan P | 56 | 51.1 | ||

| 23:30 | JPY | National CPI Y/Y Dec | 2.10% | 2.90% | ||

| 23:30 | JPY | National CPI Core Y/Y Dec | 2.40% | 2.40% | 3.00% | |

| 23:30 | JPY | National CPI Core-Core Y/Y Dec | 2.90% | 3.00% | ||

| 00:01 | GBP | GfK Consumer Confidence Jan | -16 | -16 | -17 | |

| 00:30 | JPY | Manufacturing PMI Jan P | 51.5 | 50.1 | 50 | |

| 00:30 | JPY | Services PMI Jan P | 53.4 | 51.6 | ||

| 03:07 | JPY | BoJ Interest Rate Decision | 0.75% | 0.75% | 0.75% | |

| 06:30 | JPY | BoJ Press Conference | ||||

| 07:00 | GBP | Retail Sales M/M Dec | 0.40% | 0.00% | -0.10% | |

| 08:15 | EUR | France Manufacturing PMI Jan P | 51 | 50.5 | 50.7 | |

| 08:15 | EUR | France Services PMI Jan P | 47.9 | 50.4 | 50.1 | |

| 08:30 | EUR | Germany Manufacturing PMI Jan P | 48.7 | 47.6 | 47 | |

| 08:30 | EUR | Germany Services PMI Jan P | 53.3 | 52.5 | 52.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan P | 49.4 | 49.3 | 48.8 | |

| 09:00 | EUR | Eurozone Services PMI Jan P | 51.9 | 52.6 | 52.4 | |

| 09:30 | GBP | Manufacturing PMI Jan P | 51.6 | 50.4 | 50.6 | |

| 09:30 | GBP | Services PMI Jan P | 54.3 | 51.7 | 51.4 | |

| 13:30 | CAD | Retail Sales M/M Nov | 1.30% | 1.20% | -0.20% | -0.30% |

| 13:30 | CAD | Retail Sales ex Autos M/M Nov | 1.70% | 1.10% | -0.60% | |

| 14:45 | USD | Manufacturing PMI Jan P | 51.9 | 52.1 | 51.8 | |

| 14:45 | USD | Services PMI Jan P | 52.5 | 52.8 | 52.5 | |

| 15:00 | USD | UoM Consumer Sentiment Jan F | 56.4 | 54 | 54 | |

| 15:00 | USD | UoM 1-Yr Inflation Expectations Jan F | 4.00% | 4.20% |

| 21:45 | NZD |

| CPI Q/Q Q4 | |

| Actual | 0.60% |

| Consensus | 0.50% |

| Previous | 1.00% |

| 21:45 | NZD |

| CPI Q/Q Q4 | |

| Actual | 3.10% |

| Consensus | 3.00% |

| Previous | 3.00% |

| 22:00 | AUD |

| Manufacturing PMI Jan P | |

| Actual | 52.4 |

| Consensus | |

| Previous | 51.6 |

| 22:00 | AUD |

| Services PMI Jan P | |

| Actual | 56 |

| Consensus | |

| Previous | 51.1 |

| 23:30 | JPY |

| National CPI Y/Y Dec | |

| Actual | 2.10% |

| Consensus | |

| Previous | 2.90% |

| 23:30 | JPY |

| National CPI Core Y/Y Dec | |

| Actual | 2.40% |

| Consensus | 2.40% |

| Previous | 3.00% |

| 23:30 | JPY |

| National CPI Core-Core Y/Y Dec | |

| Actual | 2.90% |

| Consensus | |

| Previous | 3.00% |

| 00:01 | GBP |

| GfK Consumer Confidence Jan | |

| Actual | -16 |

| Consensus | -16 |

| Previous | -17 |

| 00:30 | JPY |

| Manufacturing PMI Jan P | |

| Actual | 51.5 |

| Consensus | 50.1 |

| Previous | 50 |

| 00:30 | JPY |

| Services PMI Jan P | |

| Actual | 53.4 |

| Consensus | |

| Previous | 51.6 |

| 03:07 | JPY |

| BoJ Interest Rate Decision | |

| Actual | 0.75% |

| Consensus | 0.75% |

| Previous | 0.75% |

| 06:30 | JPY |

| BoJ Press Conference | |

| Actual | |

| Consensus | |

| Previous | |

| 07:00 | GBP |

| Retail Sales M/M Dec | |

| Actual | 0.40% |

| Consensus | 0.00% |

| Previous | -0.10% |

| 08:15 | EUR |

| France Manufacturing PMI Jan P | |

| Actual | 51 |

| Consensus | 50.5 |

| Previous | 50.7 |

| 08:15 | EUR |

| France Services PMI Jan P | |

| Actual | 47.9 |

| Consensus | 50.4 |

| Previous | 50.1 |

| 08:30 | EUR |

| Germany Manufacturing PMI Jan P | |

| Actual | 48.7 |

| Consensus | 47.6 |

| Previous | 47 |

| 08:30 | EUR |

| Germany Services PMI Jan P | |

| Actual | 53.3 |

| Consensus | 52.5 |

| Previous | 52.7 |

| 09:00 | EUR |

| Eurozone Manufacturing PMI Jan P | |

| Actual | 49.4 |

| Consensus | 49.3 |

| Previous | 48.8 |

| 09:00 | EUR |

| Eurozone Services PMI Jan P | |

| Actual | 51.9 |

| Consensus | 52.6 |

| Previous | 52.4 |

| 09:30 | GBP |

| Manufacturing PMI Jan P | |

| Actual | 51.6 |

| Consensus | 50.4 |

| Previous | 50.6 |

| 09:30 | GBP |

| Services PMI Jan P | |

| Actual | 54.3 |

| Consensus | 51.7 |

| Previous | 51.4 |

| 13:30 | CAD |

| Retail Sales M/M Nov | |

| Actual | 1.30% |

| Consensus | 1.20% |

| Previous | -0.20% |

| Revised | -0.30% |

| 13:30 | CAD |

| Retail Sales ex Autos M/M Nov | |

| Actual | 1.70% |

| Consensus | 1.10% |

| Previous | -0.60% |

| 14:45 | USD |

| Manufacturing PMI Jan P | |

| Actual | 51.9 |

| Consensus | 52.1 |

| Previous | 51.8 |

| 14:45 | USD |

| Services PMI Jan P | |

| Actual | 52.5 |

| Consensus | 52.8 |

| Previous | 52.5 |

| 15:00 | USD |

| UoM Consumer Sentiment Jan F | |

| Actual | 56.4 |

| Consensus | 54 |

| Previous | 54 |

| 15:00 | USD |

| UoM 1-Yr Inflation Expectations Jan F | |

| Actual | 4.00% |

| Consensus | |

| Previous | 4.20% |

Greenland Tensions Ease, But Forecasts for Gold Still Very Optimistic

- Gold prices steadied near $4 880 an ounce, just below record highs, after tensions over Greenland eased following a diplomatic breakthrough between Donald Trump, Europe, and NATO, temporarily cooling safe-haven demand.

- Geopolitical risk and concerns over U.S. monetary policy independence continue to support gold.

- Goldman Sachs Group Inc. raised its year-end gold price forecast to $5,400 an ounce, citing strong demand from private investors and central banks, while silver and other precious metals also extended gains.

Gold stabilizes after a political storm

Daily timeframe of Gold, source: TradingView

Gold prices steadied near $4 880 an ounce, very close to yesterday's all-time high, after tensions surrounding Greenland eased. For several sessions, the metal had hovered close to record levels, fueled by demand for safe-haven assets amid escalating diplomatic strains.

Important was shift in tone from the White House. Donald Trump withdrew the threat of tariffs against Europe following an agreement with allies on a “framework for a future deal” concerning Greenland.

Greenland, NATO, and financial markets

The understanding announced after talks with NATO Secretary General Mark Rutte includes a strengthened NATO presence, the stationing of U.S. missile systems, and rules governing mining rights—aimed at limiting Chinese influence in the region. The meeting at the World Economic Forum in Davos “took some of the temperature out of U.S.–EU tensions,” although there are still “plenty of dip-buyers” supporting gold prices.

Goldman Sachs raises its forecast

Despite the near-term cooling, the outlook for gold remains robust. Goldman Sachs Group Inc. lifted its year-end gold price forecast to $5 400 an ounce, citing intensifying demand from private investors and central banks. Analysts emphasized that risks are “significantly skewed to the upside” amid lingering global policy uncertainty.

Silver and other metals also advance

Daily Timeframe of Silver, source: TradingView

Silver climbed as much as 2.8% and reach new all-time high at $96 an ounce and reversing earlier losses. Over the past year, prices have tripled, boosted by a historic short squeeze and heavy retail buying. Platinum and palladium also edged higher, while the Bloomberg Dollar Spot Index slipped slightly, offering additional support to precious metals.

What’s next?

Gold underlying fundamentals remain strong. Geopolitics, monetary policy, and structural investment demand continue to keep gold—and precious metals more broadly—firmly in the global market spotlight.

Natural Gas Explodes by 70% in Four Sessions: What’s Next?

- Natural Gas explodes to up 70% since the Friday close

- Supply bottlenecks, geopolitical tensions and oversold prices build a cocktail for price explosion

- Exploring Technical Levels for Natural Gas

Natural Gas, historically highly correlated with WTI Oil, has largely decoupled over the past four sessions.

While the weekly correlation ranged between 0.20 and 1.00 since 2020, it has turned close to negative in late 2025.

Since the Sunday open, US Natural Gas prices have exploded by approximately 60%.

While initially attributed to fears of European supply disruptions amid recent EU-US trade tensions, the reality is more complex.

US output sits at decade lows.

Persistently low prices have disincentivized production following the record output of 2023-2024, creating a supply bottleneck just as the Northern Hemisphere enters its coldest period.

This winter differs significantly from recent years. Previous warm seasons created storage gluts and led to assumptions that milder winters were the new norm. However, the current reality is harsh (This current winter is a cold one, based in Montreal I can only confirm), challenging those assumptions.

Simultaneously, power generation demand is surging.

The need to power AI data centers and metal smelting operations—sectors currently seeing high demand—is outpacing futures delivery schedules, fueling this price acceleration.

Stress on the system is amplified by the US's role as the world's leading LNG exporter, particularly to Europe following the closure of Russian supply routes.

Consequently, demand spikes or supply troughs in Europe now have immediate impacts on US spot prices.

The market is facing a perfect storm: a severe winter, rising global energy demand, and escalating tensions between key suppliers and constrained consumers.

Add to this the instability in Iran—holder of the second-largest proven gas reserves—and persistent global conflicts, and the result is an explosive mix for prices.

We will now dive into the Natural Gas charts, ranging from daily to intraday timeframes, to identify the trajectory of this squeeze, potential retracement levels, and historical context.

Natural Gas Multi-Timeframe Technical Analysis

Weekly Chart

Natural Gas (ETF) Weekly Chart – January 22, 2026 – Source: TradingView

Natural Gas is posting a gigantic Bullish Marabozu candle (which doesn't show any wicks) indicating high pressure to the current Market.

Now breaking outside of its 2024 Upward Channel, further upside could easily be warranted.

The RSI is quickly moving to overbought levels and the daily action faces a short-term challenge at the 2022 Pivotal Resistance ($5.25 to $5.50).

Current prices remain about 40% to the 20-Week MA highs (which got up to $7.194)!

To trade Natural gas with close precision and further clues on physical supply/demand balances, keep a close eye on the EIA's daily reports – Today In Energy.

Moving averages will be long to catch up to such a squeeze and won't serve as ideal technical indicators on higher timeframes (Weekly, Daily).

One may rather look for support and resistance levels and Fibonacci-retracements for entries and exits.

Daily Chart and Technical Levels

Natural Gas (ETF) Daily Chart – January 22, 2026 – Source: TradingView

The 75% rise since Friday close is a frightening picture – This weekly close will be very key for upcoming action. See why on the intraday timeframe just below.

Levels of interest for Natural Gas trading

Resistance Levels

- $5.30 to $5.50 Immediate Resistance

- $5.68 Session and Weekly Highs

- 2022 Key Pivot (As Resistance) $6.00 to $6.20

- December 2022 Resistance level $6.60 to $6.95

- August 2022 Record $10.15

- ATH in 2005 at $15.51

Support Levels

- $5.00 to $5.20 Break-Retest support

- $5.00 Psychological mini-support

- $4.60 to $4.75 Major Momentum Pivot (61.8% Fib)

- $4.20 Pivotal Support ($4.10 4H MA 50)

- $3.60 Monday Support and 200-Day MA

- $3.00 August 2025 Support

2H Chart

Natural Gas (ETF) 2H Chart – January 22, 2026 – Source: TradingView

Despite the extreme squeeze throughout the past few days, the action is reacting to some overbought levels and marking intermediate tops.

With the current $5.67 Wick being rejected, Nat Gas is reacting well to the $5.30 to $5.50 Resistance Zone, which will act as key barometer for bull/bear strength:

- Breaking above on the Daily hints at a quick test of the $6.00 Resistance

- Remaining here indicates a short-term pullback to the $5.00-$5.20 Break-Retest support – Look at the 2H 20-period MA.

- Correcting then bouncing from there would be the most sustainable bull-path for the commodity

- Breaking the $5.00 Support however should see a calmer price-action, extending the potential correction to $4.60 which will be an interesting Pivotal Support area.

Safe Trades!

US: Consumer Spending Remains Resilient, Outpacing Income

Personal income rose 0.3% month-over-month (m/m) in November, up from 0.1% m/m in October (also released today) and slightly below expectations. On an inflation adjusted basis, personal income was up just 0.1% m/m in November, and down 0.1% in October.

Consumer spending grew by 0.5% month-over-month in nominal terms, matching the pace seen in October and aligning with market expectations. After adjusting for inflation, the real spending rose by 0.3% m/m in both October and November.

Examining the broad categories, spending on both goods and services rose in real terms in both October and November. Spending on goods rose by 0.6% in November, following a 0.4% m/m gain in October. Spending on services increased by 0.3% in November, following a 0.2% gain in the prior month.

With spending outpacing income, the personal saving rate declined to 3.5% in November, down from 3.7% in the prior month and 4.9% a year ago. This marks the first time saving rate dipped below 4% since 2022.

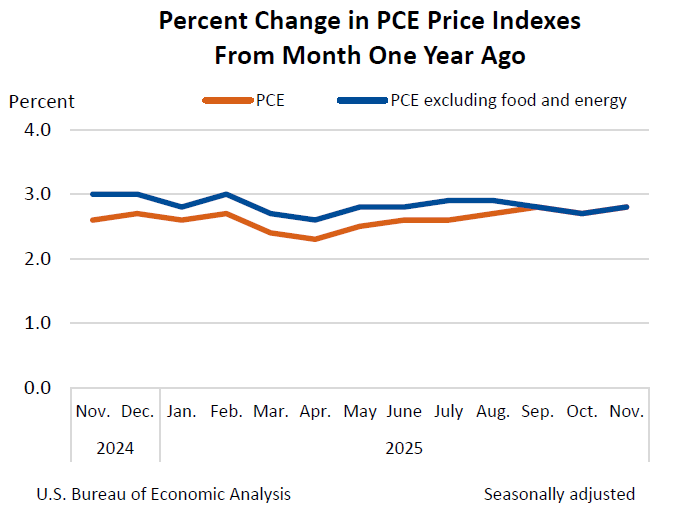

Inflation remains persistently elevated above the Fed's 2% target. Core PCE – the Fed's preferred inflation gauge – rose by 0.2% in both October and November, on par with the pace seen prior to the shutdown. In annual terms, core PCE inflation was up 2.8% year-over-year in November, up slightly from 2.7% pace seen in October.

Key Implications

Personal spending was robust through the first two months of Q4 2025, echoing other indicators, such as retail sales, and suggesting that consumer spending remained more resilient throughout the lengthy government shutdown than expected. In volume terms, consumer spending was up 0.6% from September, putting our estimate of Q4 2025 PCE growth at 3.0% (annualized) – not much slower than the 3.5% pace seen in Q3 but considerably higher than originally projected. It was also notable that spending continued to outpace income, with saving rate falling to levels not seen since late-2022 when core measures of inflation were around their peak. Evidently, households are saving less or dipping into their savings to maintain the spending momentum, particularly during the period where some payments were disrupted by the government shutdown.

We expect consumer spending to remain robust at the start of 2026. Consumers should benefit from past interest rate cuts, some stabilization in the labor market, and ongoing accumulation in wealth. The fiscal boost from higher OBBBA-linked tax refunds—which are expected to arrive between February and April—should also provide another tailwind to household income and spending. This robust spending momentum and steady inflationary backdrop provide the FOMC with reasons to remain patient regarding further rate cuts when its members meet next week.

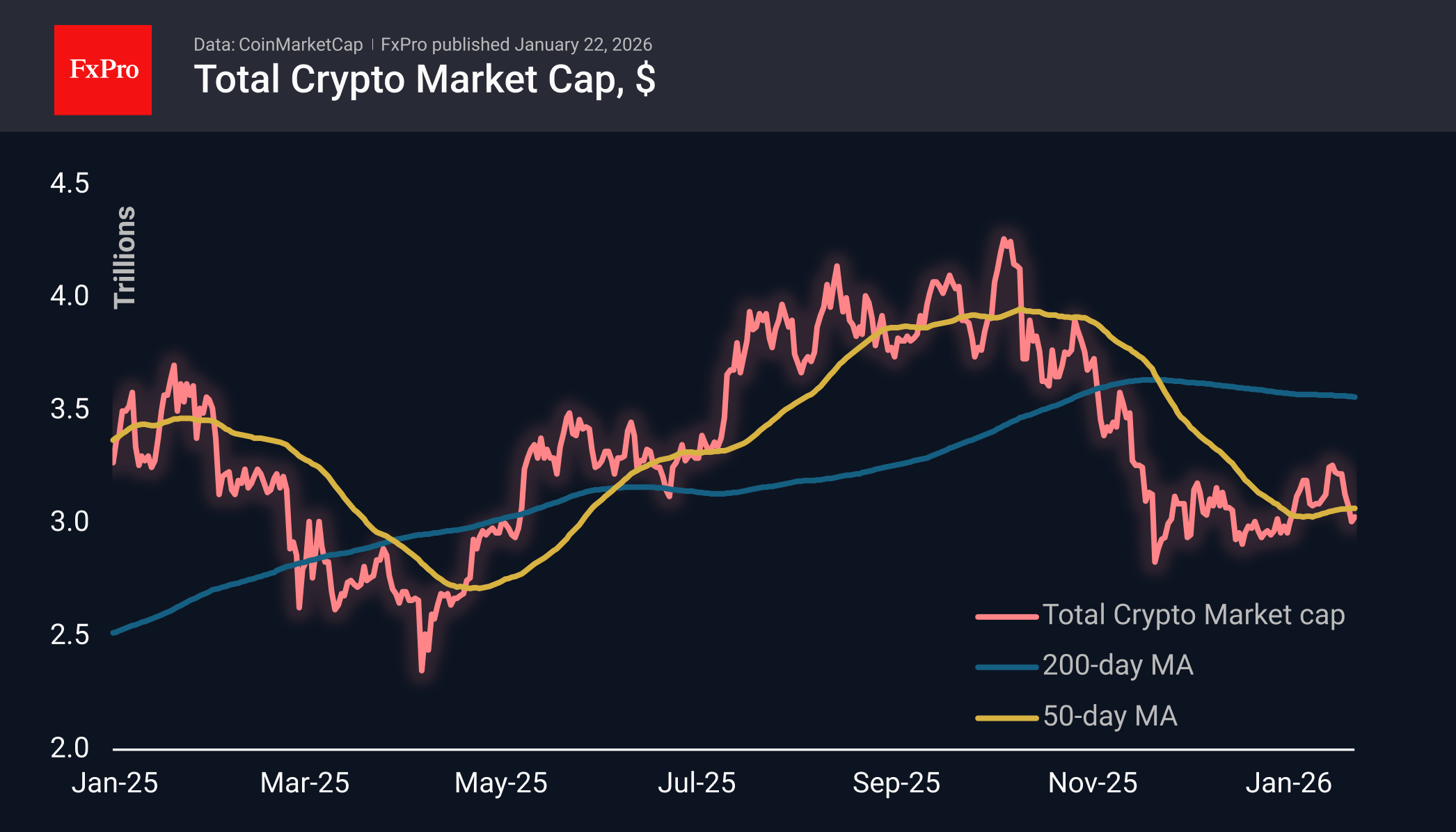

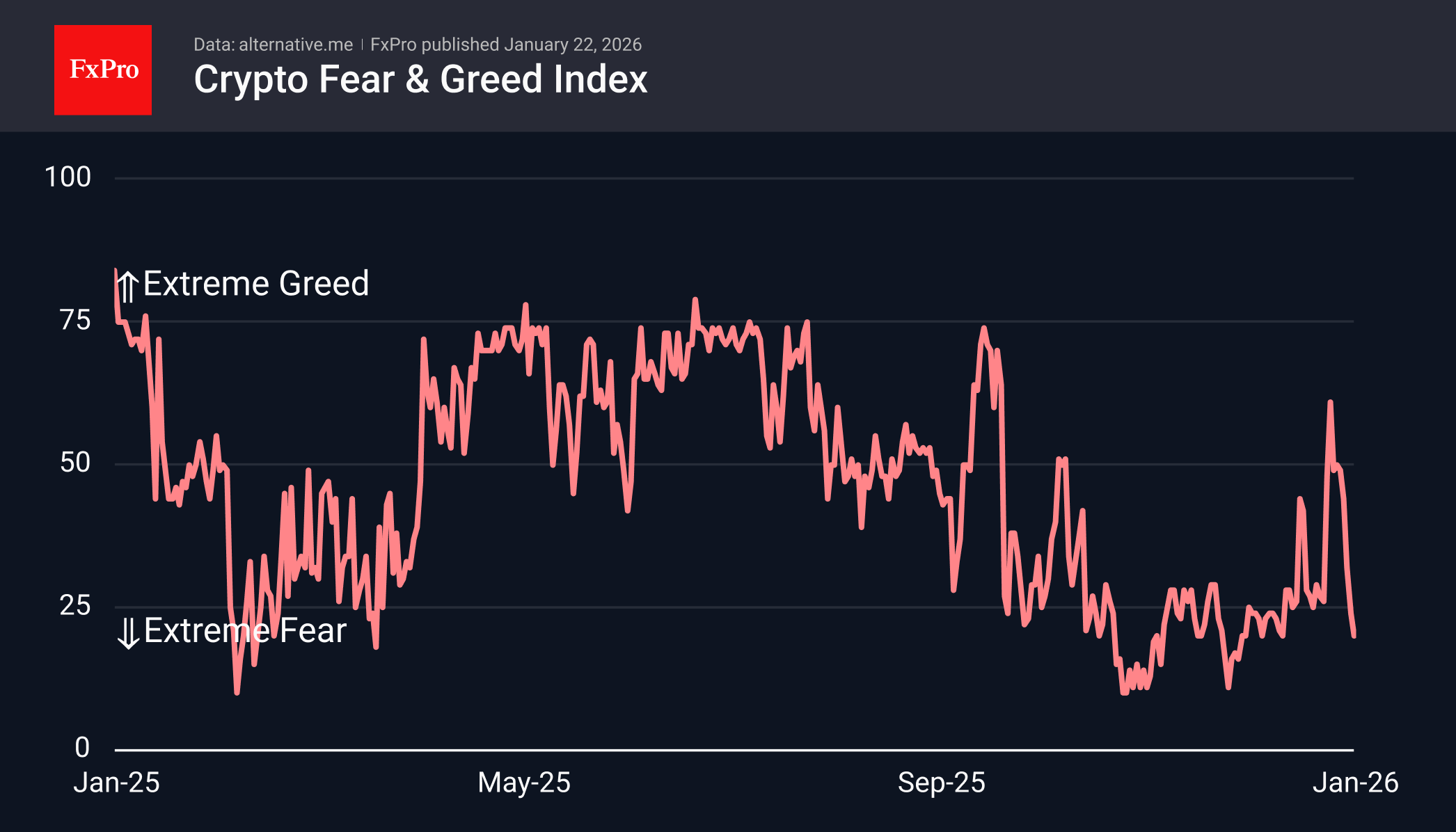

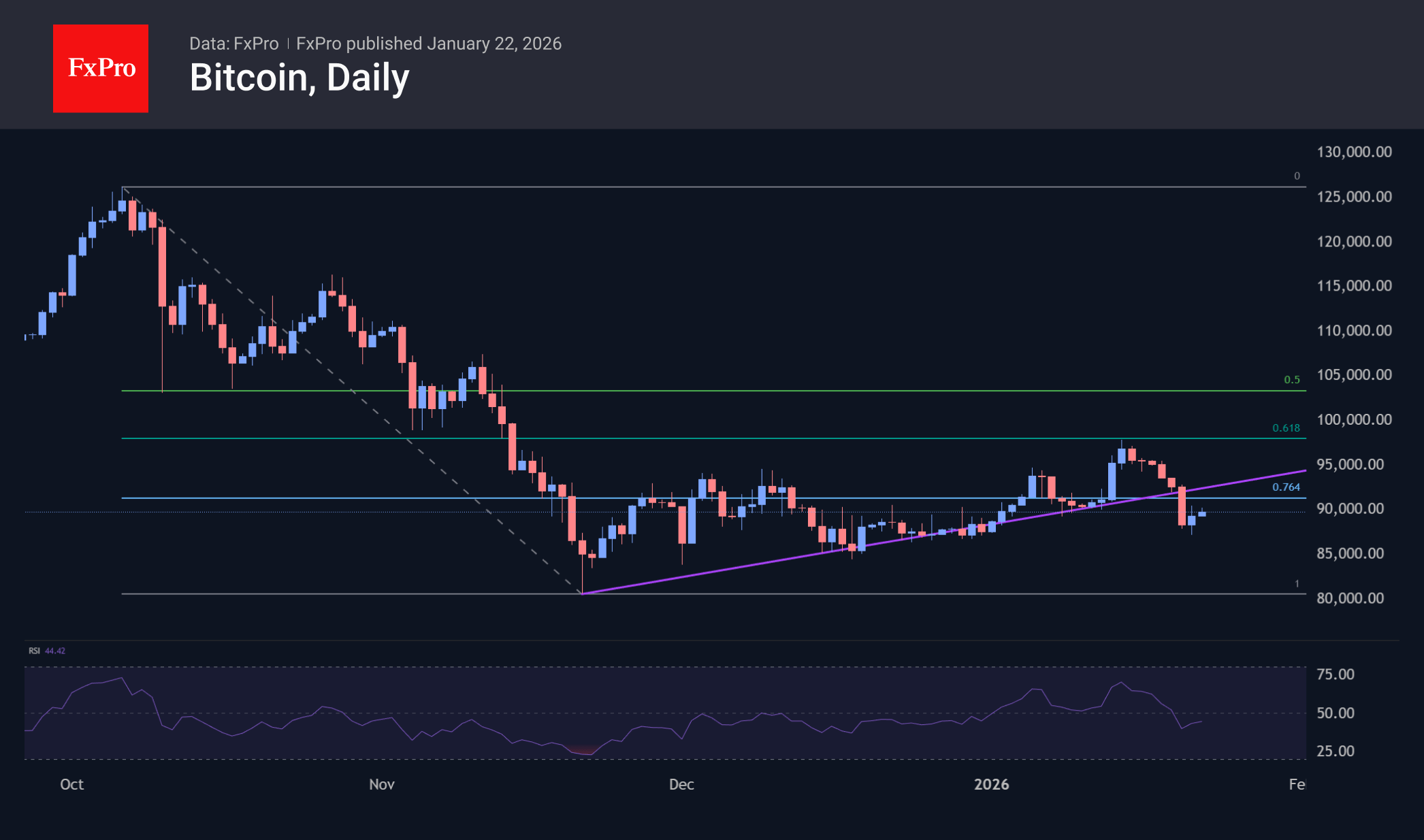

Cryptos Remain Laggards With Weak Rebound

Market Overview

The crypto market cap grew by less than 1% to $3.04 trillion. Since October, it has become the norm for cryptocurrencies to pay particular attention to negative news and react weakly to positive news. This time, the impressive rebound in stock markets only helped stop the sell-off in the crypto market and led to a modest rebound in cryptocurrencies from local lows. The momentum of the rebound was not even enough to overcome the 50-day moving average, underscoring the current dominance of bearish sentiment in the crypto market.

The sentiment index further highlights the extreme fear, losing 41 points over the last seven days of decline. After touching the greed zone last week, profit-taking emerged. While risk sentiment improved following developments in Davos yesterday, it was not strong enough to trigger a sustainable rebound in crypto.

Bitcoin jumped from $87K to above $90K at the end of the day on Wednesday, but has since faced active selling as it approaches the round level, although it has not experienced significant declines due to increased risk appetite. Technically, BTC remains just below its 50-day moving average and below the former support line of the uptrend. Despite yesterday’s retreat from local lows in Bitcoin, the picture remains bearish with a higher chance of a resumption of the decline, at least to $84K, and to $80K with a more extreme downward momentum.

News Background

Markets have gone into ‘defensive mode’ due to economic turmoil in Japan and political tensions, according to QCP Capital. Instead of acting as a hedge, the first cryptocurrency is behaving like a risky asset, sensitive to interest rates and macroeconomics.

For the first time in history, control of the market has shifted from long-term holders to ‘new’ whales who entered the market in the late stages of the cycle, CryptoQuant points out. The average purchase price for this group is around $98K. And until the market absorbs their loss-making supply, sales will prevail in BTC.

In the first half of the year, the crypto market may fall by 15-20%, and its recovery will begin in the fourth quarter, said BitMine CEO Tom Lee. In his opinion, Bitcoin will retain its status as digital gold and could reach $250,000 in the long term.

Ripple President Monica Long said that the coming year will be a turning point for the industry — cryptocurrencies will finally become integrated into the global financial system and will no longer be perceived as an alternative to traditional finance.

US personal consumption resilient as core PCE inflation firm at 2.8%

U.S. personal income and spending data pointed to steady demand momentum into late 2025, according to figures released by the Bureau of Economic Analysis. Personal income rose 0.1% mom in October and 0.3% mom in November, while personal consumption expenditures increased a firm 0.5% mom in both months.

Inflation readings remained firm but controlled. The headline PCE price index rose 0.2% mom in both October and November, with the core PCE measure also increasing 0.2% mom in each month. On a year-over-year basis, headline and core PCE inflation ticked up from 2.7% in October to 2.8% in November, suggesting inflation pressures are easing only gradually.

The data, released together due to the recent government shutdown, replace reports originally scheduled for late November and December. Taken together, the figures reinforce the view that consumer demand remains robust while disinflation progress is slow.

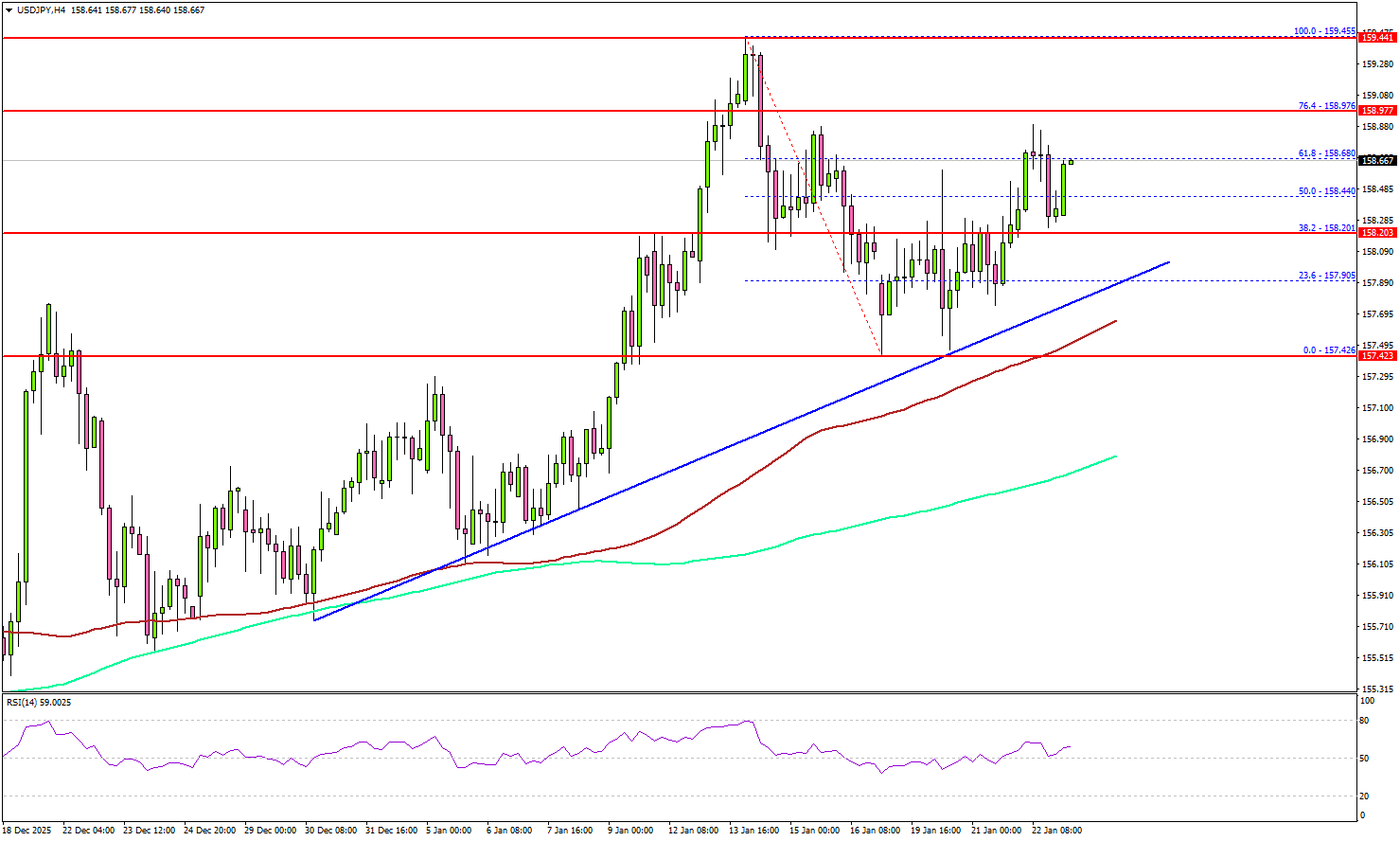

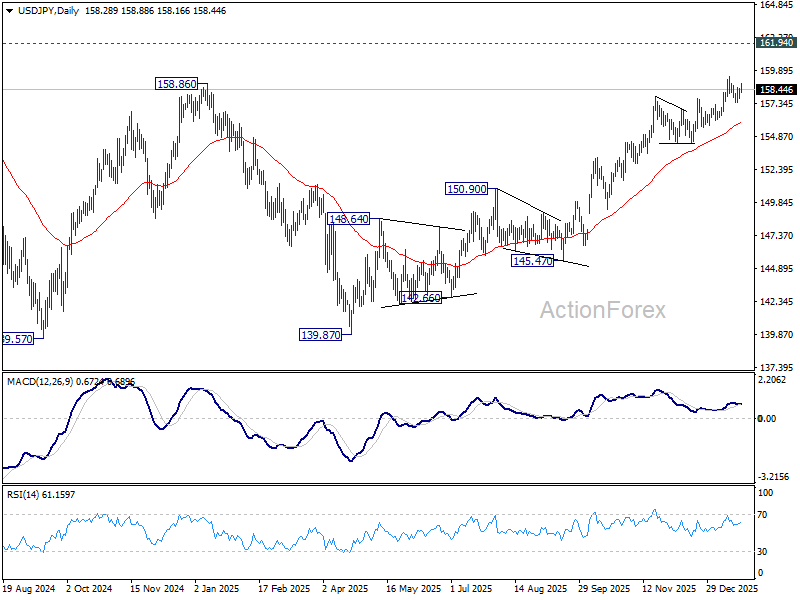

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.86; (P) 158.19; (R1) 158.64; More...

USD/JPY is staying in consolidation from 159.44. Intraday bias remains neutral at this point. With 156.10 support intact, outlook remains bullish. On the upside, break of 159.44 will resume the rise from 139.87 towards 161.94 high. However, firm break of 156.10 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.86 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

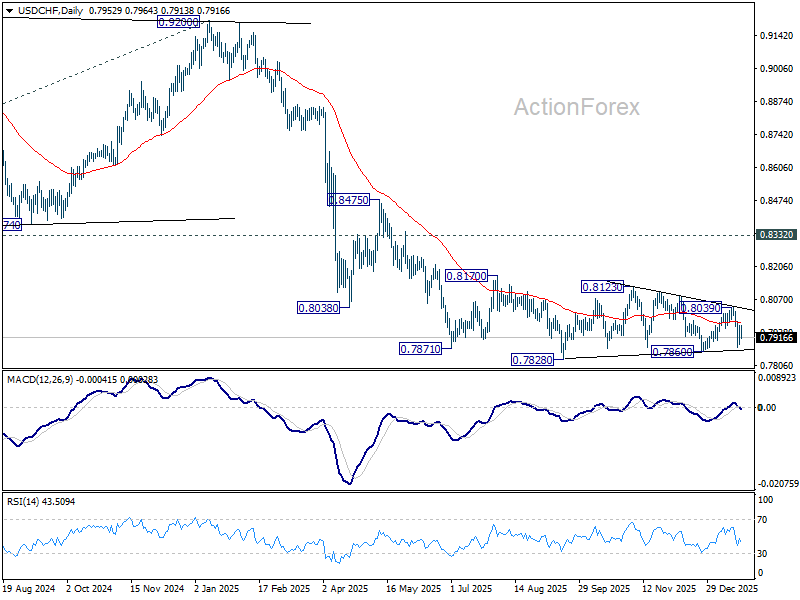

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7903; (P) 0.7936; (R1) 0.7989; More….

Intraday bias in USD/CHF remains neutral, and risk stays on the downside with 55 4H EMA (now at 0.7958) intact. Firm break of 0.7860 support argue that larger down trend is ready to resume through 0.7828 low. Nevertheless, sustained break of 55 4H EMA will bring stronger rebound towards 0.8039 resistance. Overall, price actions from 0.7828 are seen as a corrective pattern, which could still extend.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).