Sample Category Title

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3808; (P) 1.3844; (R1) 1.3873; More...

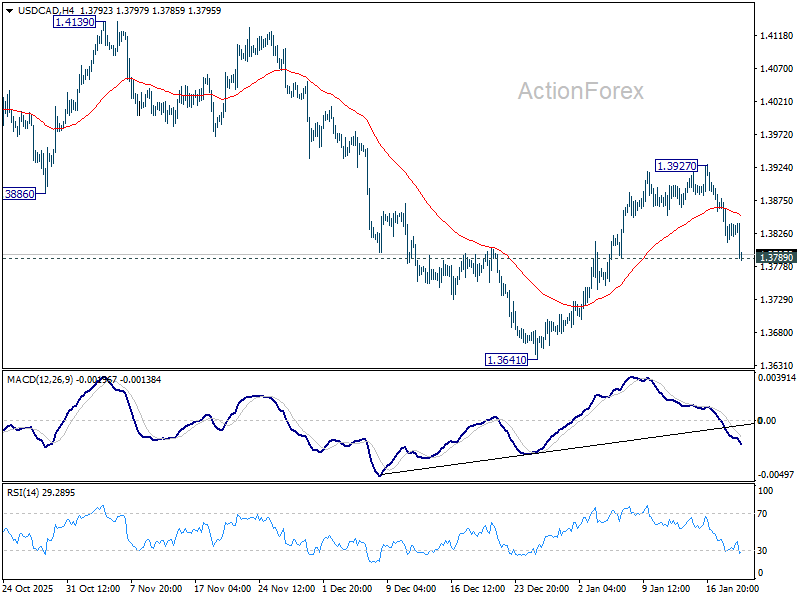

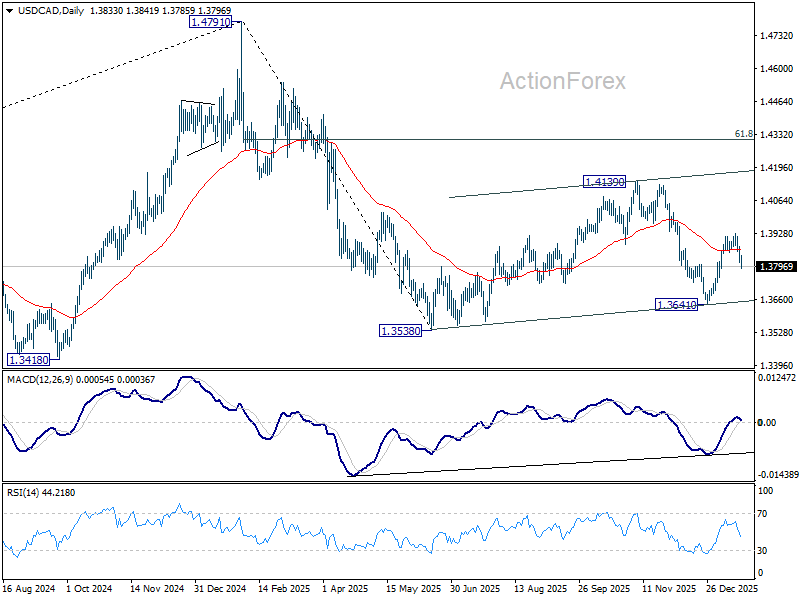

Immediate focus in on 1.3789 support as USD/CAD's fall from 1.3927 accelerates lower. Firm break there will argue that rebound from 1.3641 has completed. Deeper decline should be seen back to 1.3538/3641 support zone. ON the upside, above 1.3927 will resume the rebound towards 1.4139 resistance. Overall price actions from 1.3538 are seen as a consolidation to the fall from 1.4791, and might still extend.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, and break of 1.3538 will target 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral until there are signs that the correction has completed.

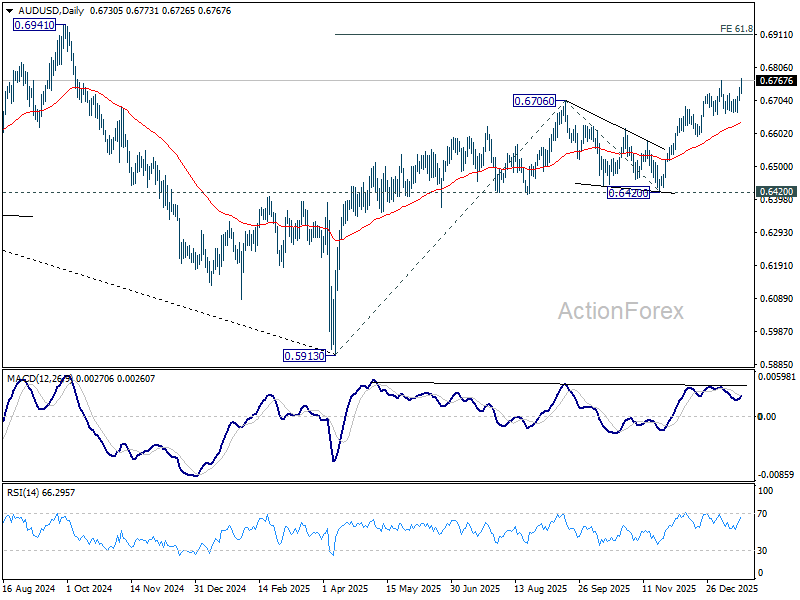

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6713; (P) 0.6730; (R1) 0.6753; More...

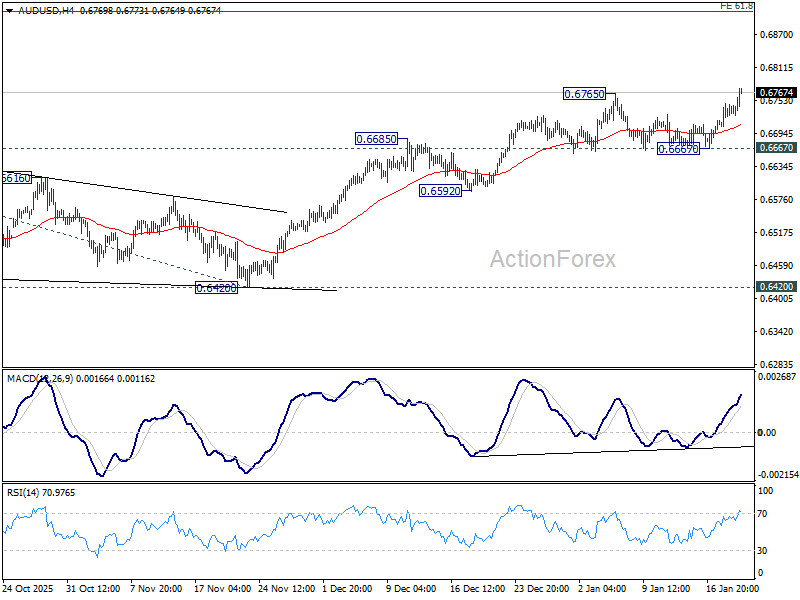

AUD/USD's rally from 0.5913 resumed by breaking through 0.6765 resistance today. Intraday bias is back on the upside. Further rise should be seen to 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910 next. For now, near term outlook will stay bullish as long as 0.6667 support holds, in case of retreat.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6420 support holds, even in case of deep pullback.

SNB Schlegel sees no issue with negative inflation prints if temporary

The SNB is not alarmed by recent soft inflation data, according to Chairman Martin Schlegel. He said inflation is expected to pick up, but the SNB is prepared to tolerate temporary negative readings, provided medium-term price stability remains intact.

"If we have some negative prints this year, for example, this is not a problem with the Swiss National Bank, because we look at the medium-term price stability," he added.

He also pointed to recent global political turbulence as a driver of Swiss Franc appreciation, reflecting its traditional safe-haven role. On reserve management, Schlegel declined to comment directly on whether the exchange-rate move would lead to changes in Dollar holdings, but reiterated the SNB’s commitment to diversification across currencies and asset classes, noting the bank continuously reviews its "investment universe" and stands ready to act if needed.

Bitcoin Falls Below $90k: Why Does It Matter?

As the BTC/USD chart shows, the price of the leading cryptocurrency slipped below the psychological $90k level earlier this morning. This downward move provides grounds for several important observations.

→ First, bitcoin is performing poorly as a defensive asset. At a time when global markets are assessing risks linked to US ambitions regarding Greenland, gold is once again proving its well-established safe-haven status, having climbed above $4,700 yesterday. By contrast, bitcoin is tracking technology stocks — with the Nasdaq 100 currently at its lowest levels since the start of the year.

→ Second, the price is moving towards a key support area, increasing the risk of a much deeper decline if that support is breached.

Technical Analysis of the BTC/USD Chart

On 8 January, we discussed bitcoin’s price action within a system of two channels, both of which remain relevant. At the time, we noted that a sharp rebound from the $90k level (marked by a black arrow) signalled renewed bullish activity.

Since then:

→ bullish efforts pushed the price into the upper half of the red channel and led to a break above local resistance; however, bitcoin failed to hold at these higher levels, forming a bull trap (indicated by the red arrow);

→ bears subsequently regained control and drove BTC/USD back below the psychological $90k mark.

This behaviour highlights the persistence of selling pressure and increases the risk of a break below support that has been in place throughout 2025.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service (additional fees may apply). Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

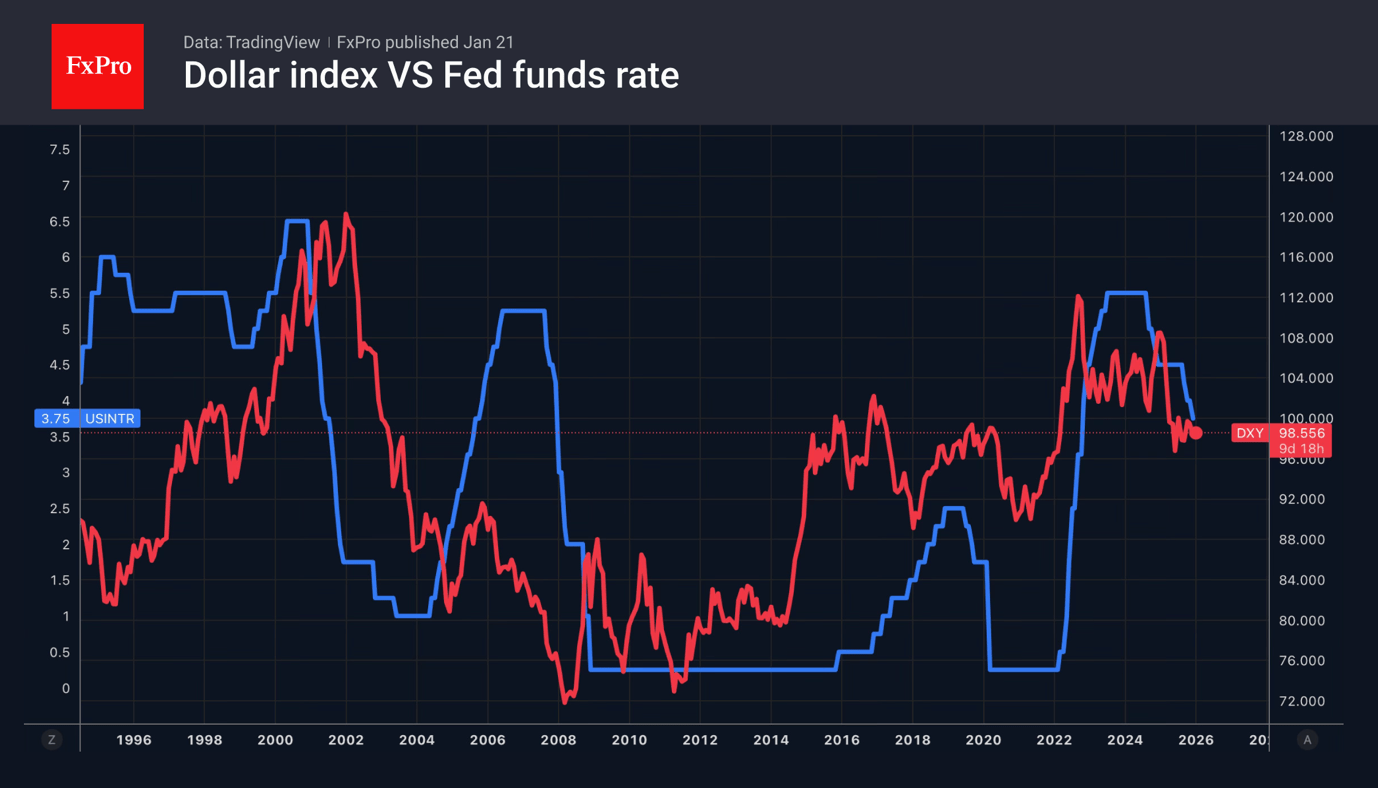

To Sell America is Great Again

- The dollar is under pressure due to threats to the Fed’s independence.

- The yen has weakened due to the government’s political adventurism.

What is happening now is reminiscent of the hysteria that followed America’s Liberation Day. Take a deep breath, exhale, and let events unfold. This is how Scott Bessent tried to calm the financial markets and the US’s European partners. He urged them not to retaliate. However, another parallel with the events of April accelerated the sell-off of everything American. Stocks, bonds and the dollar all collapsed. Admittedly, to a lesser extent compared to the announcement of global tariffs back then.

Pressure on the greenback was created by criticism of the Fed chairman from the Treasury and the Lisa Cook hearing. The court will decide whether the protection of the central bank from political interference, created by Congress 90 years ago, will stand or not. If Donald Trump is able to dismiss and appoint FOMC members at will, the federal funds rate will fall to 1%, and with it, the US dollar will collapse.

Jerome Powell’s intention to attend the Lisa Cook trial outraged Scott Bessent. He accused the Fed chairman of causing huge losses to the central bank due to large-scale monetary stimulus during the pandemic. Everything is bad for the executive branch: both when the Fed keeps rates unchanged and when it lowers them.

The noise and dust surrounding White House politics is causing investors to flee the dollar and other American assets. The surge in Treasury bond yields is the result of a ‘sell America’ attitude. Events in Japan are adding fuel to the fire in global debt markets. There, long-term bond yields have reached record levels on fears that early elections to the lower house of parliament are a political gamble by Sanae Takaichi.

The Liberal Democratic Party’s long-time ally, Komeito, has joined the opposition, and the policy of fiscal stimulus and low interest rates risks fuelling inflation. The associated decline in real household income will lead to discontent with the current government. As a result, the yen feels out of place even against the backdrop of a frankly weak US dollar. USDJPY cannot decide on the direction of further movement and is stuck in indecision.

Gold is another matter. Its new record high is due, among other things, to the Supreme Court’s reluctance to rule on the legality of US tariffs. This could drag on until June.

GBP/USD Growth Driven by Weakening US Dollar

On Wednesday, GBP/USD remained stable at 1.3436. The British pound was supported by a sell-off in the US dollar following increased trade tensions between the US and Europe over Greenland.

US President Donald Trump has threatened to impose tariffs on imports from the UK, Denmark, Norway, Finland, France, Germany, and the Netherlands if these countries do not agree to transfer control of Greenland to the US. In response, investors began pulling back from American assets, including the dollar, and reallocating funds into European currencies and gold.

While recent UK labour market data showed weakness, with unemployment rates near five-year highs and the largest drop in payrolls since November 2020, there are some positive developments. These include a reduction in layoffs, stabilisation in job vacancies and unemployment, and a slowdown in wage growth that aligns with the Bank of England’s inflation target.

This backdrop sets the stage for further interest rate cuts by the Bank of England. The central bank’s baseline scenario suggests a final reduction to 3.50% in April, with market expectations for one more cut by mid-year and a 60% probability of a second cut by December.

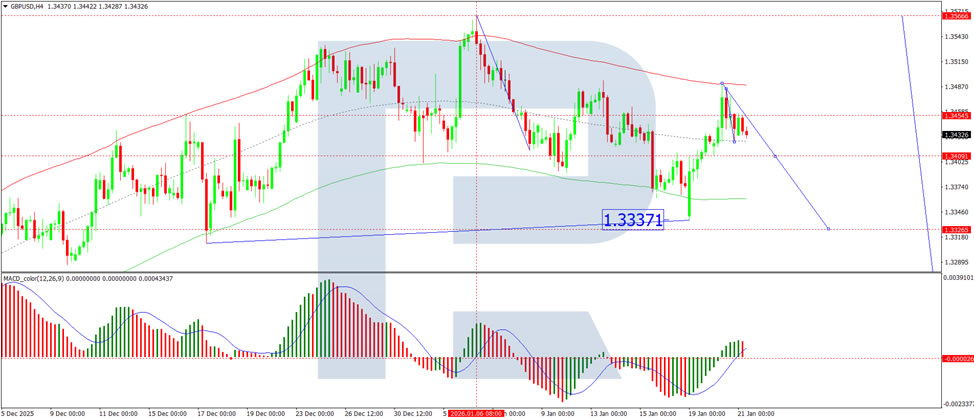

Technical Analysis

On the H4 GBP/USD chart, the market is forming a broad consolidation range around the 1.3455 level. Today, we expect the range to extend to 1.3395. A correction to 1.3450 is likely, followed by a continuation of the downward trend toward 1.3326, with a potential drop to 1.3220. This scenario is supported by the MACD indicator, with its signal line above zero and pointing downward.

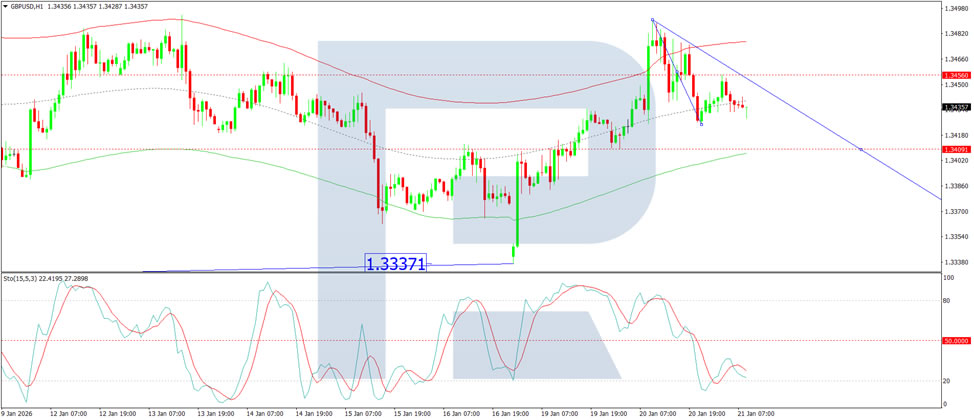

On the H1 chart, the market is consolidating around 1.3450, with a potential decline towards 1.3400. If this level breaks, the downward trend could extend to 1.3326. The Stochastic oscillator confirms this bearish outlook, as its signal line remains below the 50 level and continues pointing downward.

Conclusion

GBP/USD growth is closely linked to the weakening US dollar, primarily driven by geopolitical tensions and shifting market sentiment. The UK’s labour market data and the BoE’s expected rate cuts further support the pound’s position. Technically, GBPUSD may continue its downward correction in the near term, with key support levels at 1.3395 and 1.3326.

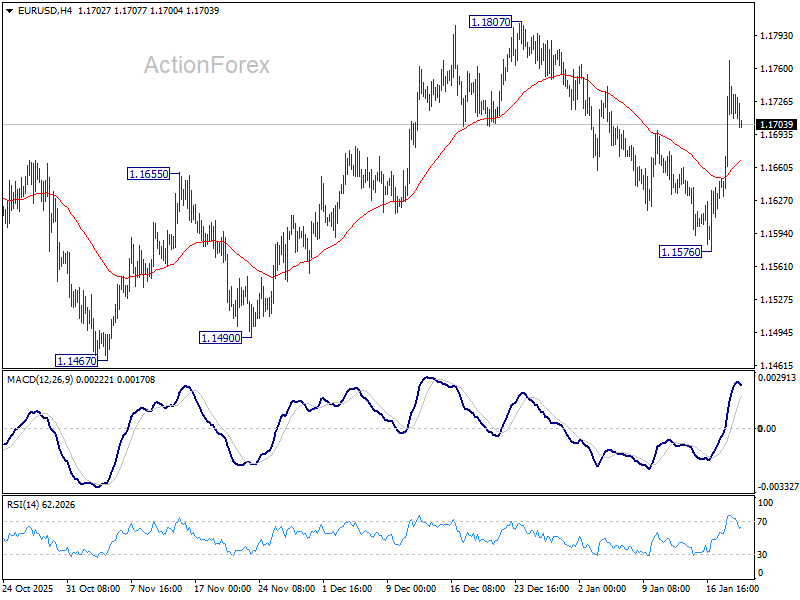

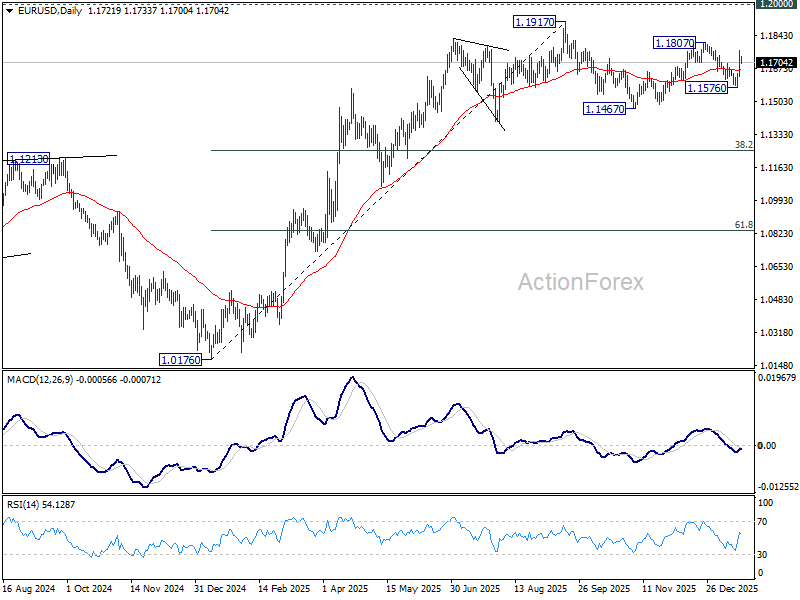

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1649; (P) 1.1709; (R1) 1.1785; More….

EUR/USD's rise from 1.1576 should still be in progress and intraday bias remains on the upside for 1.1807. Firm break there will resume whole rally from 1.1467, and target a retest on 1.1917 key resistance level. For now, risk will stay on the upside as long as 55 4H EMA (now at 1.1666) holds, in case of retreat.

In the bigger picture, as long as 55 W EMA (now at 1.1413) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

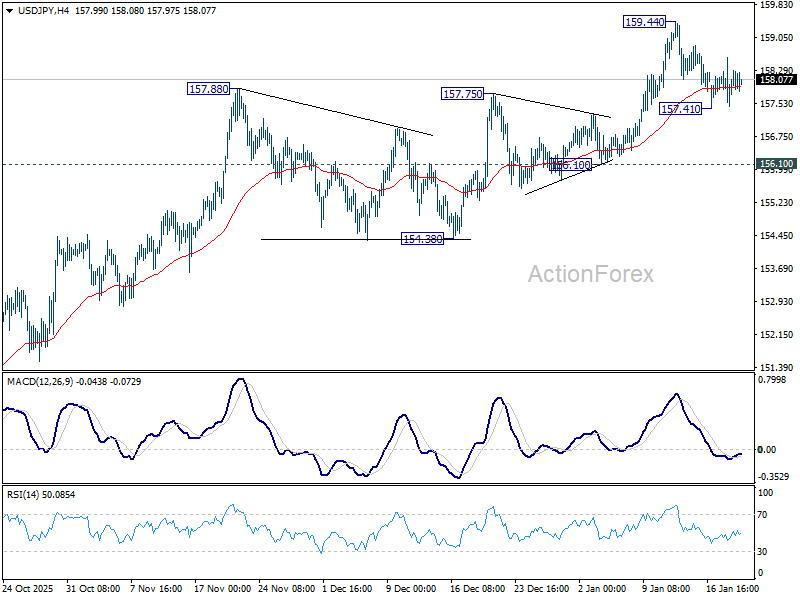

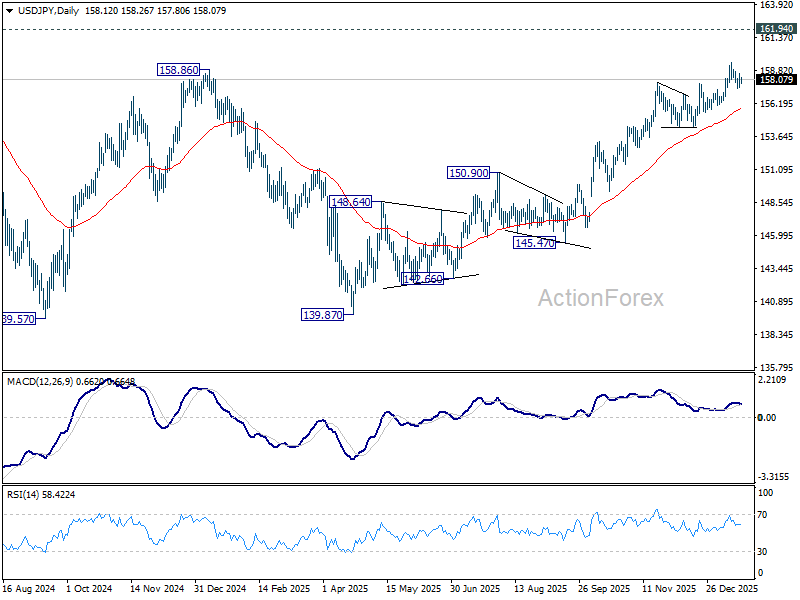

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.55; (P) 158.07; (R1) 158.68; More...

No change in USD/JPY's outlook as consolidation continues below 159.44. Intraday bias remains neutral for the moment. With 156.10 support intact, outlook remains bullish. On the upside, break of 159.44 will resume the rise from 139.87 towards 161.94 high. However, firm break of 156.10 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.86 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

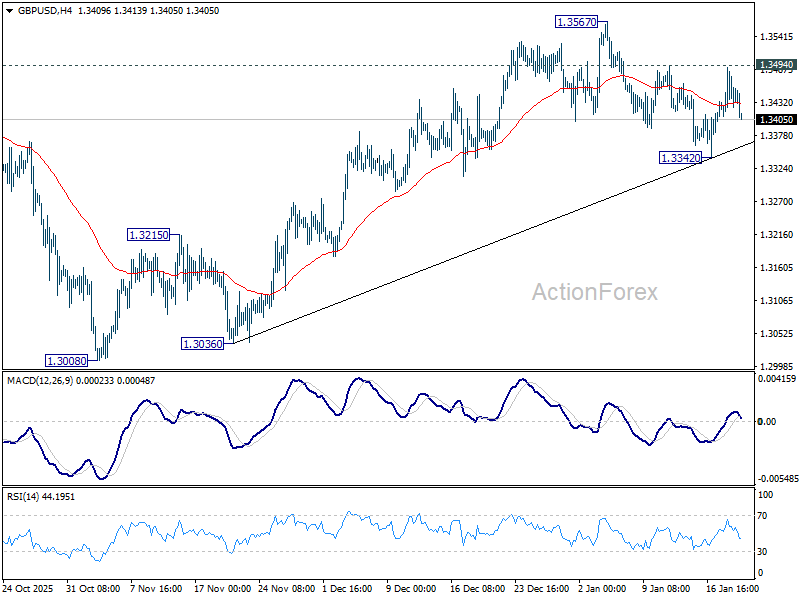

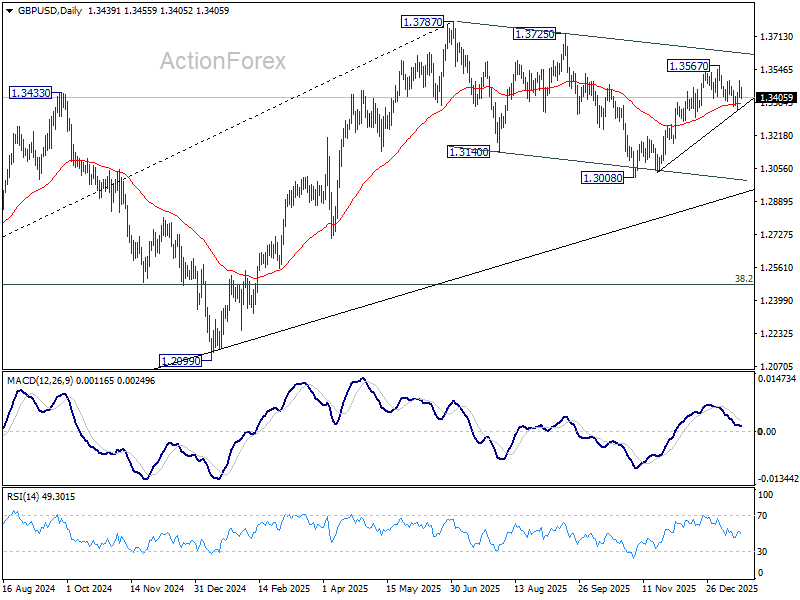

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3398; (P) 1.3445; (R1) 1.3488; More...

GBP/USD failed to break through 1.3494 resistance and retreated, and intraday bias remains neutral. On the upside, firm break of 1.3494 will suggest that pullback from 1.3567 has completed at 1.3342, after drawing support from 55 D EMA (now at 1.3379). Intraday bias will be back on the upside for 1.3567 first. Break there will resume the rally from 1.3008 to retest 1.3787 high. On the downside, sustained trading below 55 D EMA will argue that the decline is another falling leg in the corrective pattern from 1.3787.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

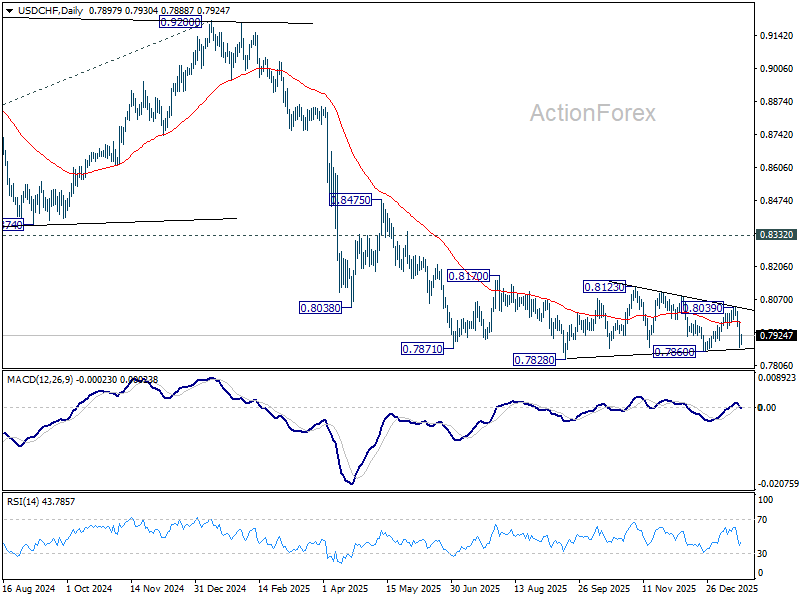

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7858; (P) 0.7921; (R1) 0.964; More….

No change in USD/CHF's outlook as intraday bias stays on the downside at this point. Firm break of 0.7860 support will argue that larger down trend is ready to resume through 0.7828 low. Next target will be 0.7382 projection level. For now, risk will stay on the downside as long as 55 4H EMA (now at 0.7967) holds, in case of recovery.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).