Sample Category Title

US Payrolls Look a Little Different Today

Markets

Yesterday was your typical waiting game in the run-up to today much anticipated US payrolls report. Rotation forces remained at play on stock markets with the tech-heavy Nasdaq (-0.5%) underperforming against the industrial Dow Jones index (-0.1%), but also European equities (EuroStoxx50 +0.55%). Advanced peace talks in Germany resulted in cautious optimism both from the European (Merz) and the US (Trump) side: “a really far-reaching, substantive agreement that we have not had so far”. After Ukraine dropped its Nato membership demand over the weekend, yesterday saw progress in terms of European security guarantees, backed by the US. There’s still no breakthrough on the most thorniest issue though, territory concession. Moves on fixed income markets were small with a slight outperformance at the front end of the US yield curve. EUR/USD closed at 1.1769 from a start at 1.1735.

US payrolls look a little different today. In addition to the full November report, the Bureau of Labour Statistics will also release October payrolls data. The monthly survey of households, from which for example the unemployment rate is derived, will be released for November thanks to an extension of the collection period after the shutdown (which also cause today’s later-than-normal release) but such statistics couldn’t be retroactively collected for October so will be missing today. Consensus expects a combined job growth number of 50k for Oct-Nov today. Fed Chair Powell last week downplayed the number since he fears big downward revisions to numbers since April (average job losses of -20k instead of +40k; related to BLS’ companies birth-death model; final benchmark revisions come with Jan2026 payrolls report). Markets reacted to those dovish comments and suggest a preference to react on a weaker outcome, lifting odds of a continuation of the Fed’s normalization cycle in Q1 2026. The dollar is vulnerable for more losses (EUR/USD 1.1919 resistance) in case of an outperformance by short-term US Treasuries. For US equity markets, it could give some short term relief if the focus switches from potential data weakness to the prospect of a more accommodative Fed stance. We keep a close eye on the unemployment rate as well. It has been steadily rising from 4.1% in June to 4.4% in September. A new uptick to 4.5% or even 4.6% won’t go unnoticed and implies that the SAHM recession indicator (3-month moving average of unemployment rate more than 0.5 ppt above low-point of the past 12 months) could be triggered soon. Apart from Oct-Nov payrolls, today’s agenda also features October retail sales and global December PMI surveys. The impact of EMU (& UK) numbers will be overshadowed by the US agenda from a market perspective. After today, November US CPI numbers (Thursday) and Q3 GDP data (Dec 23) are the ones to watch from a US perspective.

News & Views

December Indian PMI surveys showed growth easing to a 10-month low even as output level continued to rise sharply. The composite out index slowed to 58.9 from 59.7, with both activity in the services sector (59.1 from 59.8) and the manufacturing output index (58.4 from 59.6) easing. Growth of new orders slowed at the end of the year, but remained noticeable. Growth in new export orders improved. At the same time, companies kept their staffing levels broadly unchanged amid a further easing of business confidence. Inflationary pressures were again muted. Input costs increased modestly, and at a pace that was only slightly faster than the near five-and-a-half-year low posted in November. Output prices also increased modestly, and at the second-slowest pace in the past nine months. The rate of inflation seen in December was weaker than the average across 2025 as a whole. The India rupee this morning continues to set record lows levels with the USD/INR cross rate surpassing the 91 big figure.

National Bank of Poland policy maker Henryk Wnorowski gave a rather mild assessment yesterday on NBP policy going forward. He indicated that it was unlikely that anything will change in monetary policy before March. However, for the rest of 2026 it didn’t rule out anything, but suggested the possibility of further rate cuts, perhaps even several steps. He deemed it very unlikely that the policy rate will decline below 3%. Other NBP members, including governor Glapinski, recently suggested a higher level for the bottom of the NBP easing cycle (3.5% area). The National Bank of Poland since May reduced the policy rate from 5.75% to 4%. The zloty remains well bid with EUR/PLN testing the bottom of the 4.22/4.31 trading range.

All Eyes on US Data

Stocks in Europe and the UK benefited from rotation flows yesterday, while tech-heavy US peers remained under pressure, with the Nasdaq 100 leading losses among the major indices. This morning, futures on both sides of the Atlantic are pointing lower.

In Asia, the Nikkei is down more than 1.2%, slipping below its 50-day moving average. The move comes after a recent spike in Japanese long-term yields — which look more stable today — and a stronger yen ahead of Thursday’s Bank of Japan (BoJ) decision, where the BoJ is expected to announce a rate hike.

What’s interesting is that this hawkish divergence from the BoJ has not translated into a stronger yen against majors since the start of the year. On the contrary, the currency has remained under pressure, weighed down by still significantly lower yields compared to other major economies.

The recent move of the Japanese 10-year yield above the 1.70% mark — often cited as the level at which foreign investments become less attractive for Japanese investors once hedging costs are considered — has created some stress among global risk investors. However, some market participants point out that Fed liquidity conditions remain ample, and may even become more supportive under the Reserve Management Purchases (RMP) programme, which is expected to inject around $40bn per month into the system. For context, that is roughly half the monthly pace of QE following the global financial crisis. In that sense, the Fed’s liquidity stance may help temper concerns linked to rising Japanese yields and the behaviour of large Treasury buyers.

That said, overall market sentiment is not particularly strong at the start of the week. Investors are focused on upcoming US jobs, retail sales and inflation data. Jobs and retail sales are due today and are expected to confirm a softer labour market alongside resilient consumer spending.

There are lingering questions around data quality following recent shutdown-related disruptions to data collection, with some arguing that December figures may offer a clearer picture of labour-market conditions. Still, today’s data should provide an early indication of how markets react.

For jobs and sales, the familiar dynamic applies: “good news is bad news, bad news is good news.” Strong data reduce the case for Federal Reserve (Fed) rate cuts — bearish for stocks and bonds, supportive for the US dollar. Softer data increase the likelihood of cuts, supporting bonds and equities while weighing on the dollar. But data that are too weak would also hurt earnings expectations, making the market reaction a delicate balancing act.

There is an additional nuance. The prevailing narrative matters — and sentiment in tech, which has driven markets since early 2023, has deteriorated. Investors increasingly focus on the risks — heavy investment, rising debt and uncertain paths to monetisation — rather than the growth and productivity upside. As a result, even a data mix supportive of Fed easing may fail to lift tech sentiment and instead reinforce the rotation trade. If so, gains in the tech-heavy S&P 500 and Nasdaq 100 may continue to lag those of the Dow Jones Industrial Average and small- and mid-cap indices.

In FX markets, the US dollar remains broadly under pressure — slightly steadier this morning, partly offset by yen strength — but the broader outlook for the dollar remains negative. That said, one chart stands out: markets are pricing roughly two Fed cuts next year versus one implied by the Fed’s latest dot plot. Given the wide divergence of views within the Fed, the median forecast may not offer reliable guidance. Still, with positioning heavily skewed against the dollar, it raises the question of whether the greenback is due for a short-term rebound.

Dollar weakness continues to support gold, silver and copper, and the outlook for metals remains constructive as confidence in fiat currencies erodes amid rising developed-market debt levels.

Oil prices continue to fall despite a softer US dollar and last week’s tensions around the seizure of a sanctioned Venezuelan vessel. The prevailing view is that sanctions-related events primarily affect sanctioned barrels themselves, with limited spill-over to WTI and Brent unless they materially alter long-term global supply. With non-sanctioned supply currently ample, geopolitical headlines are having little impact on benchmark crude prices.

By contrast, a potential peace agreement involving Russia — which could bring Russian oil back into the non-sanctioned market — would add to global supply and weigh on prices. It is possible that markets are increasingly pricing such a scenario, which could help explain why US crude is testing the lower end of this year’s range despite last week’s Fed cut and a cheaper US dollar. WTI is trading near $56 per barrel this morning. I would expect solid support around $55 and a potential rebound from that area.

US Nonfarm Payrolls Back With a Double Release

In focus this week

In the US, the delayed October nonfarm payrolls (NFP) and full November jobs report are both due for release at 14:30 CET. We expect that delayed seasonal hiring will weigh on October NFP and forecast job growth at only 20k. Reversal of this effect likely supported November NFP growth to +50k. Both estimates are below the September pace, which is driven by a further slowdown in labour supply growth. We forecast November unemployment rate steady at 4.4%. October retail sales data and December flash PMIs are also due for release.

In the euro area, the flash PMI report for December is released. Activity in the final quarter of the year has been decent according to the latest two PMI reports that surpassed expectations. We expect the manufacturing PMI to rise slightly to 49.9 from 49.6 while we expect services to fall marginally to 53.3 from 53.6, thereby showing broadly the same picture of decent activity as in November and supporting the ECB's "good place" assessment of the euro area economy.

UK labour market data is released ahead of the Bank of England meeting on Thursday. Recent data has been soft with accelerating job loss and unemployment edging higher. This report will be key in combination with tomorrow's CPI data for the Bank of England to weigh the pros and cons for cutting the Bank Rate on Thursday.

Economic and market news

What happened overnight

In Japan, the manufacturing PMI remained in contractionary territory despite the increase to 49.7 from 48.7 in November. However, the increase was above market consensus of 48.8 and was the highest reading in three months. Demand conditions improved, however new export orders declined.

What happened over the weekend

In the Ukraine war, Ukrainian President Zelenskyy offered to drop demands of NATO membership and cede territory to Russia during talks in Berlin. US officials offered security guarantees as Zelenskyy said he would require "Article 5-like guarantees" from the US, Europe and other countries. A draft peace agreement was said to be close by US officials, although territorial issues remain. Over the weekend Russia appeared ready to reject all proposals from Ukraine and Europe throwing doubt on whether a ceasefire is reachable within the foreseeable future.

In France, the Senate approved a reworked 2026 budget bill. The bill is expected by the French government to push the public deficit to 5.3% of GDP and above the government's 4.7-5.0% target. The National Assembly overwhelmingly rejected the bill last month and a joint committee of seven lawmakers and seven senators will meet on Friday to attempt a compromise. If they fail to reach an agreement, the National Assembly will have the final say on the 2026 budget.

In the US, New York Fed President Williams said he sees interest rates as modestly restrictive, downside risks to employment and expects inflation to return to 2% by 2027. Fed Governor Miran held a speech offering insight into his diverging view on Fed policy rates. Miran argued that current empirical Fed models overvalue the neutral interest rate and due to rapid changes in immigration, tariffs and tax law, the real neutral rate is at 0%.

Equities: Global equity markets appeared broadly unchanged on the surface yesterday, but beneath the headline performance a clear rotation continued to unfold. The healthcare versus technology rotation persisted, with tech acting as the key drag: the sector ended the day around 1% lower, while healthcare outperformed, rising 1.3%. Overall, the S&P 500 closed down -0.2%, while the NASDAQ underperformed, ending the session -0.6%. In contrast, European equities delivered a positive performance, with the STOXX 600 finishing the day +0.7%. Overnight, most Asian equity indices are trading weaker.

FI and FX: There was modest movement in both US and European bond yields/interest rates ahead of the US labour market data today and the ECB, BoE and BoJ meetings on Thursday. We are still looking forward to the German funding requirement on Thursday and more details on France during the week.

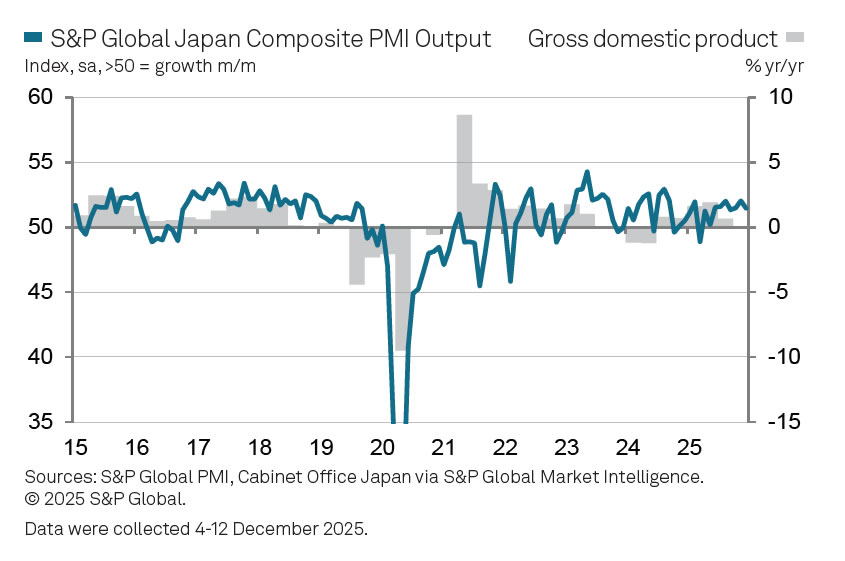

Japan’s PMI composite falls to 51.5, slowing momentum but manufacturing nears expansion

Japan’s December PMI data pointed to a modest cooling in overall momentum, while offering tentative signs of stabilization in manufacturing. PMI Manufacturing rose from 48.7 to 49.7. PMI Services eased from 53.2 to 52.5, while PMI Composite slipped from 52.0 to 51.5, indicating slower but still positive private-sector growth.

According to S&P Global, Japan’s private sector ended the year on a relatively strong footing, with output continuing to expand and new business rising further. Firms responded by stepping up hiring, with employment growth accelerating to its fastest pace in more than a year and a half. Growth remained concentrated in services, though the decline in manufacturing output and sales softened noticeable.

Forward-looking signals were more cautious. Business confidence weakened, particularly among manufacturers, reflecting subdued foreign demand and concerns about the outlook for 2026. At the same time, cost pressures intensified, with input prices rising at the fastest pace since April. Firms responded by raising output charges "at a solid pace".

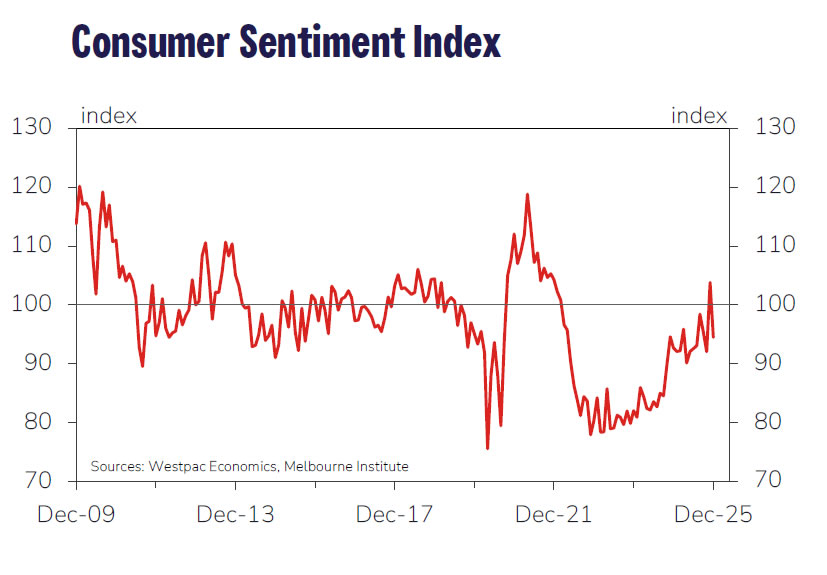

Australia Westpac consumer sentiment falls back to 94.5, bounce proves short-lived

Australian consumer confidence fell sharply in December, reversing November’s brief improvement. The Westpac Consumer Sentiment Index dropped -9.0% mom to 94.5, slipping back toward levels seen prior to last month’s surprise bounce. The pullback leaves sentiment only in “cautiously pessimistic” territory as the year comes to a close.

Westpac noted that while confidence has improved meaningfully from the deep and prolonged pessimism that dominated much of 2024, households remain reluctant to shift into outright optimism. The November rebound marked the first net positive reading since the economy reopened after the pandemic, but the latest data suggests that underlying confidence remains fragile and easily unsettled.

The survey reinforces a cautious backdrop for the RBA ahead of its February 2–3 meeting. While inflation has picked up recently, there are few signs that tight labor markets or strong consumer demand are driving the move. Instead, administered prices outside the reach of monetary policy have been a key factor. As those pressures fade, inflation is expected to resume its path toward the midpoint of the target range, though policymakers have warned that if normalization proves slow, rates may need to stay on hold for longer, with hikes still a live contingency.

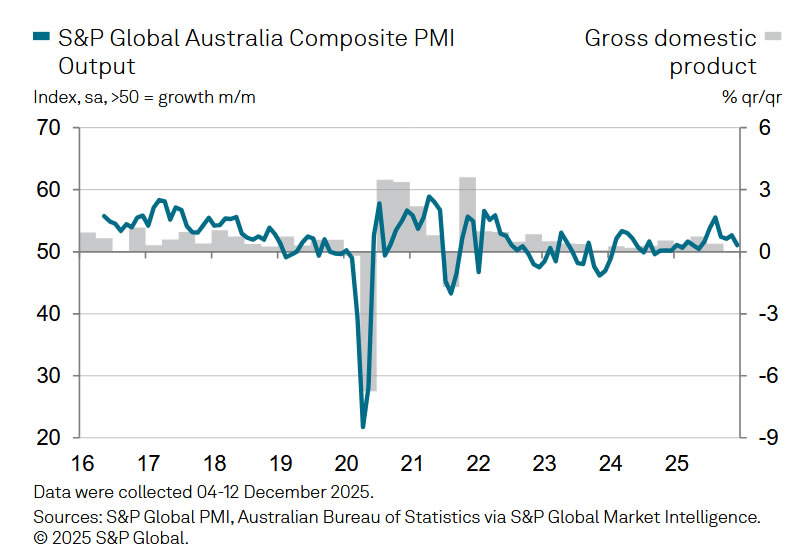

Australia PM composite falls to 51.1, growth cooling but persistent price pressures

Australia’s PMI readings for December pointed to moderating growth momentum toward year-end. PMI Manufacturing rose from 51.6 to 52.2, signaling a stronger expansion in factory activity. PMI Services slipped from 52.8 to 51.0. As a result, PMI Composite eased from 52.6 to 51.1, the lowest level in seven months.

The slowdown in overall activity was accompanied by more encouraging details beneath the surface. According to S&P Global, new orders continued to rise at a solid pace, while business confidence improved in December. Employment growth also remained robust, with job creation sustained at faster rates across both manufacturing and services, suggesting firms remain confident enough in demand to continue hiring.

Inflation signals, however, firmed again. Cost pressures intensified for Australian businesses, prompting companies to raise output prices more quickly in an effort to "defend their margins". As a result, output price inflation returned to its long-run average after two months of subdued increases.

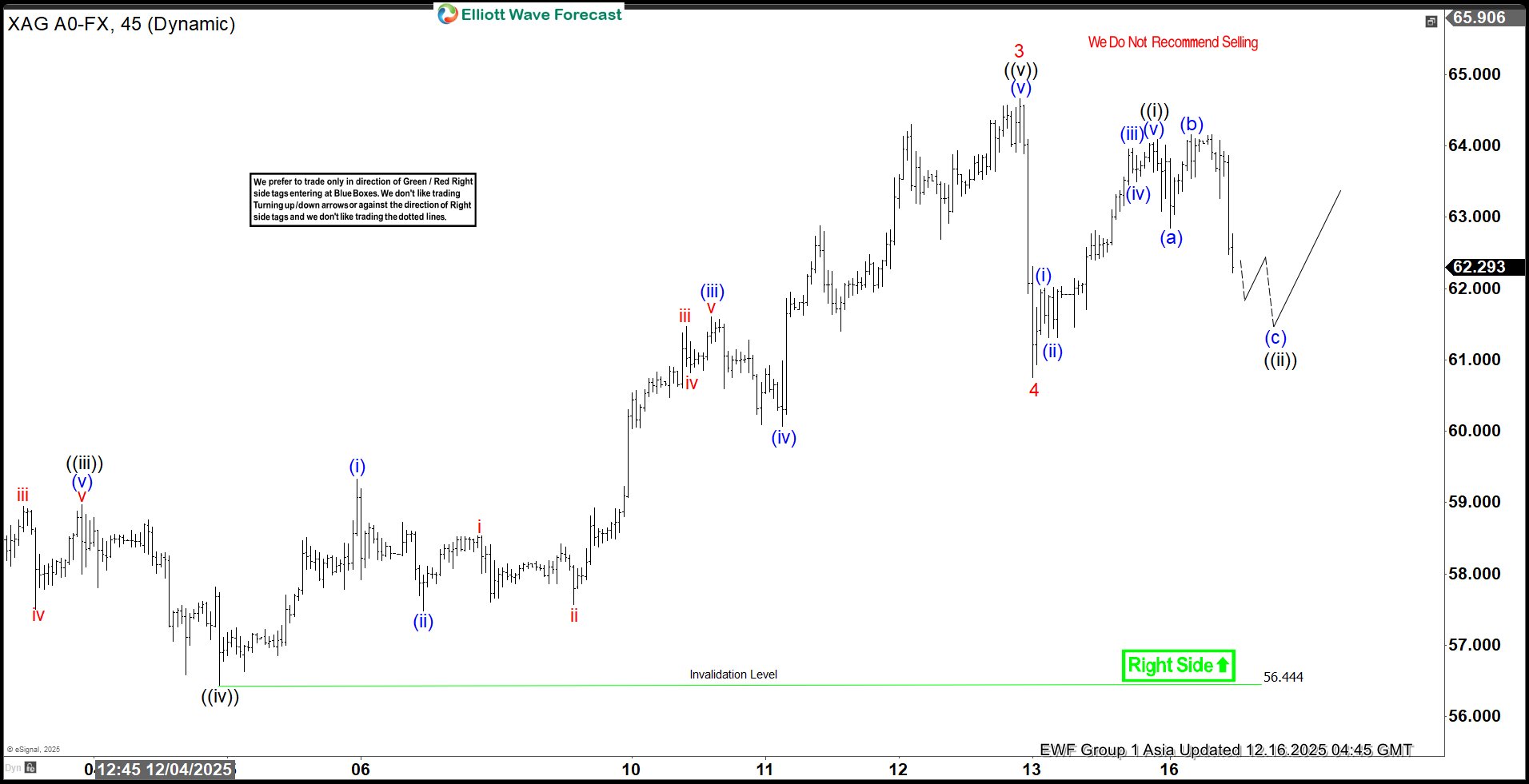

Silver (XAGUSD) Pullback Seen as Buying Opportunity Amid Record Breaking Rally

The cycle in Silver (XAGUSD) from the October 28, 2025 low remains in progress as a clear five‑wave impulse Elliott Wave sequence. From that low, wave 1 advanced to $49.36 before a corrective decline in wave 2 concluded at $46.88. This initial correction set the stage for a stronger rally. The metal then entered wave 3, which unfolded with internal subdivision into five smaller waves, reflecting the classic structure of an impulsive advance.

From the wave 2 low, wave ((i)) reached $54.39, followed by a pullback in wave ((ii)) that ended at $48.60. Momentum resumed in wave ((iii)), which carried prices to $58.94, as confirmed by the 45‑minute chart. A modest retracement in wave ((iv)) found support at $56.44, and the subsequent rise in wave ((v)) extended sharply to $64.65. This completed wave 3 at a higher degree, reinforcing the bullish sequence.

Afterward, the market experienced a corrective phase in wave 4, which is proposed to have ended at $60.74. This decline appears orderly and consistent with the broader impulsive framework. In the near term, as long as the pivot at $56.44 remains intact, the expectation is for Silver to continue its upward trajectory. The structure suggests further extension higher, with buyers likely to re‑emerge on any pullback.

Silver (XAGUSD) 60-Minute Elliott Wave Chart From 12.16.2025

XAGUSD Elliott Wave Video:

https://www.youtube.com/watch?v=jKh8qsyi10Y

Gold Jumps and Holds—Are Bulls Targeting Fresh Highs?

Key Highlights

- Gold started a fresh surge above the $4,200 resistance.

- The bulls could now aim for a move above $4,365.

- WTI Crude Oil prices remained in the red zone and declined below $58.00.

- EUR/USD is holding gains and might climb above 1.1800.

Gold Price Technical Analysis

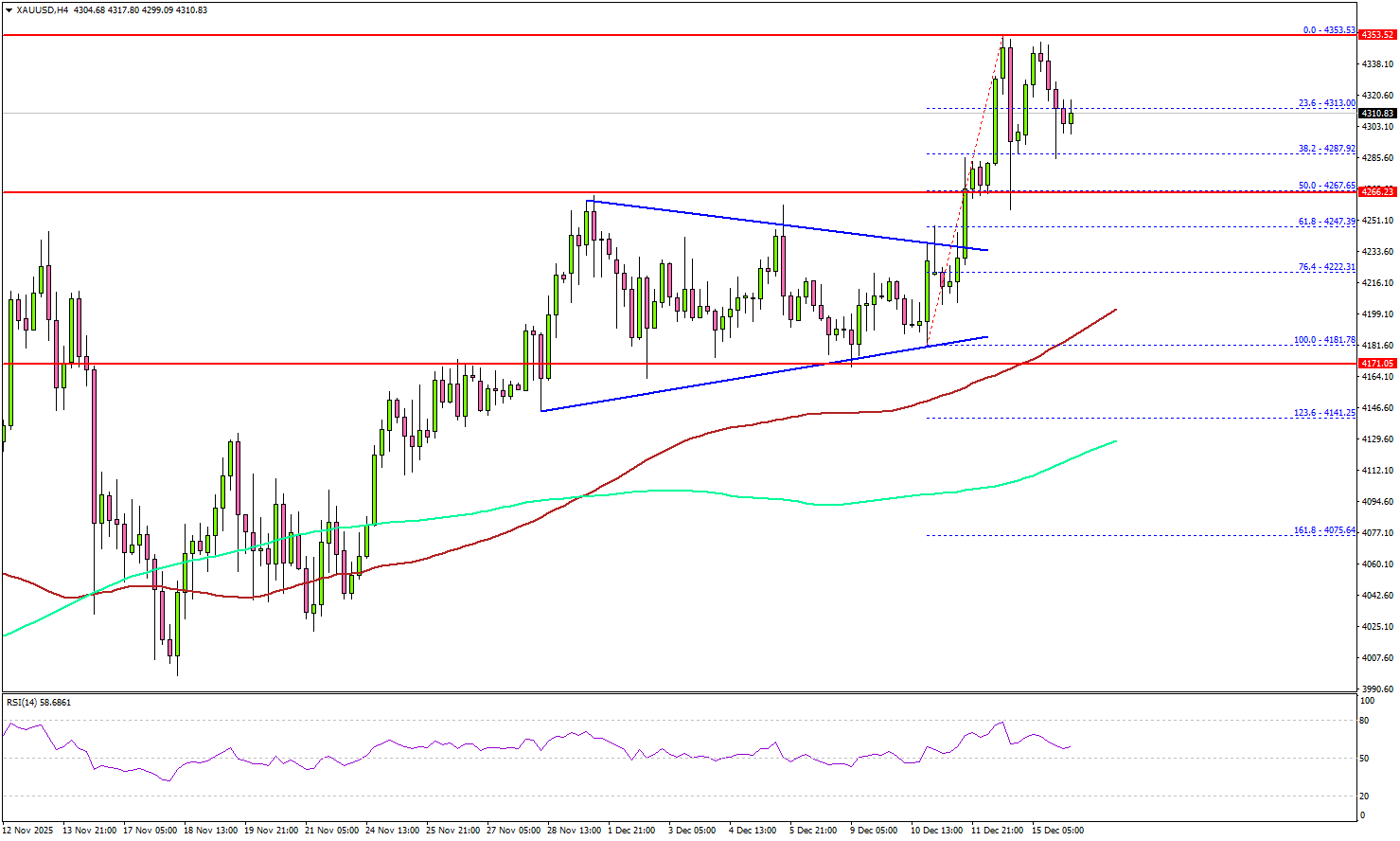

Gold prices started a fresh surge above $4,200 and $4,220 against the US Dollar. It settled above $4,300 to enter a bullish zone.

The 4-hour chart of XAU/USD indicates that the price cleared a key contracting triangle with resistance at $4,230 to enter a positive zone. The bulls even pumped the price above $4,320. The price tested $4,350 before there was a consolidation phase.

On the upside, immediate resistance is near the $4,350 level. The next major resistance sits near the $4,365 level. A clear move above $4,365 could open the doors for more upside. In the stated case, the bulls could aim for a move toward $4,400.

If there is a pullback, Gold might find bids near the $4,300 level. The first major support sits at $4,285, below which the price might slide to $4,265.

The main support sits at $4,250. Any more losses might call for a test of the 100 Simple Moving Average (red, 4 hours) or even the 200 Simple Moving Average (green, 4 hours).

Looking at WTI Crude Oil, the price attempted a decent recovery wave, but the bears remained active below the $60.00 level.

Economic Releases to Watch Today

- US nonfarm payrolls for Nov 2025 – Forecast 40K, versus 119K previous.

- US Unemployment Rate for Nov 2025 - Forecast 4.4%, versus 4.4% previous.

- US Retail Sales for Oct 2025 (MoM) – Forecast +0.2%, versus +0.2% previous.

NFP Preview: Rate Path Divergence & Implications for the DXY, Gold (XAU/USD)

The Non-Farm Payrolls (NFP) report, which comes out on December 16, 2025, is the first full look at the US job market since September, and it will be a crucial factor in determining the Federal Reserve's (Fed) strategy for interest rates throughout 2026.

This jobs data will either prove that the Fed was right to implement the controversial rate cuts of 75 basis points since September, or it will suggest that the central bank was too aggressive in cutting rates.

The report is complicated because it includes both October and November job numbers and is slightly skewed by issues like the recent government shutdown and delayed resignations of federal workers.

For this reason, experts suggest ignoring the main unemployment rate and focusing instead on the number of new jobs added in November and the changes in Average Hourly Earnings (AHE), which track how much wages are rising.

Significant market swings are expected because market participants are betting on much deeper rate cuts in 2026 than the Fed has officially planned. This creates a unique situation where Gold could rise strongly regardless of the outcome, while the currently low US Dollar has a greater potential to suddenly jump in value.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Complex Expectations: Analyzing the Dual-Month Release and Distortion

The upcoming NFP report will release two months of jobs data simultaneously, though the most important figure is for November. The jobs number for October is expected to be a loss of about 10,000 jobs, but this is largely ignored because it's due to a technical issue: many federal workers who resigned had their departure dates delayed, resulting in a temporary, one-time drop in the count.

The crucial expectation for November NFP is a modest recovery, adding about 50,000 jobs, which is a major slowdown from the 119,000 jobs gained in September. This expected number is uncertain, with forecasts ranging widely, and the risk is tilted toward a lower number, especially after a separate report (the ADP) unexpectedly showed a loss of 32,000 private sector jobs.

A key concern for the Fed is inflation, which they measure through Average Hourly Earnings (AHE), or wage growth. This is expected to rise by 0.3% from the previous month, translating to an annual growth of 3.7%. Since the main unemployment rate is unreliable right now, AHE is the clearest signal the Fed has to judge how tight the job market is and how high the risk of inflation is.

Finally, the official Unemployment Rate for October will not be released at all because the government shutdown prevented the necessary data from being collected. The rate for November is expected to suddenly spike to around 4.5% to 4.7%.

However, this sharp increase is not considered a true sign of economic weakness but rather a temporary glitch: federal employees who were temporarily sent home (furloughed) during the reference week of the government shutdown will be mistakenly counted as unemployed. Because of this issue, the market is expected to largely ignore the high unemployment rate and focus primarily on the raw payrolls number and the wage inflation figures.

Policy Crossroads: The Federal Reserve’s 2026 Rate Path Divergence

The market currently has a very different view from the Fed on interest rates for 2026, which is expected to create high market volatility. Traders are betting that the Fed will cut rates two more times by September 2026. However, the Fed's own latest forecast (Dot Plot) suggests they only expect one cut for the entire year of 2026.

If the November jobs report is stronger than expected, the market will be forced to quickly reduce its bets on those extra rate cuts and move closer to the Fed's more cautious projection. This would strengthen the argument from some Fed members who believed the central bank was in a "comfortable position to wait" before cutting rates.

This risk of the market having to "reprice" its expectations is why the NFP report is considered the single most important event for setting the tone of monetary policy in the first part of 2026.

Potential implications for the US Dollar Index (DXY) & Gold

The market's reaction to the NFP report will not be uniform, but rather dependent on the deviation from consensus forecasts. These are the potential reactions we could see depending on how the data comes out and is received.

Source: Table Created by Zain Vawda

US Dollar (DXY) Strategy: Asymmetric Upside Risk

The US Dollar Index (DXY) is currently in a near-term downtrend and is technically oversold due to aggressive market pricing of future rate cuts. This technical positioning creates an asymmetric risk profile:

- Weak Data Scenario: A weak NFP print (e.g., net job losses) validates the dovish market stance. Downside momentum would accelerate, targeting the "measured move" objective near prior support at 97.60.

- Strong Data Scenario: A stronger-than-expected November payrolls report (e.g., above 75k) would trigger a rapid unwinding of dovish expectations. This necessitates a violent short-covering bounce for the USD, potentially driving DXY back toward the 200-day Simple Moving Average (SMA) at 99.30.

US Dollar Index (DXY) Daily Chart, December 15, 2025

Source: TradingView (click to enlarge)

Gold (XAU/USD) Strategy: The Dual Bullish Catalyst

Gold exhibits the potential for a rally regardless of the NFP outcome due to the unique policy environment. A strong Dollar traditionally controls Gold prices, while a weaker Dollar pushes them up. However, the current political and policy uncertainty provides two avenues for gains:

- Dovish Catalyst (Weak NFP): Weak employment figures lead to lower interest rates and a weaker dollar, diminishing the opportunity cost of holding the non-yielding metal.

- Policy Error Catalyst (Strong NFP): If the data is surprisingly strong, it suggests the Fed may have cut rates "too far too fast". This shift in narrative from a controlled slowdown to policy error ignites fears of future inflationary acceleration. Gold then trades as an inflation hedge and an asset favored when confidence in financial assets or prudent policymaking declines, which could boost prices toward October’s record high. This structural bid under Gold suggests continuation toward resistance zones (e.g., 4380)

Gold Four-Hour Chart, December 15, 2025

Source: TradingView (click to enlarge)