Sample Category Title

Fed’s Collins explicitly endorses pause bias in FOMC guidance

Boston Fed President Susan Collins said she supported last week’s FOMC decision to lower the federal funds rate by 25 basis points, but emphasized that the decision was"a close call". Incoming information suggests the balance of risks has shifted modestly, with scenarios involving a notable further rise in inflation "seem somewhat less likely".

Nevertheless, Collins emphasized "it's important to me" that the updated language now echoes the December 2024 statement, which "preceded a pause in cutting rates".

Looking ahead, she said that with policy now at the lower end of a mildly restrictive range, she would want "greater clarity" on the inflation outlook before supporting further adjustments.

US Stock Index Outlook: Weak sentiment ahead of NFP

Friday provided a sharp shift in post-FOMC flows. The strong rallies in Equities—particularly in defensive sectors—turned sour as Fed members began to voice concerns regarding their recent decision.

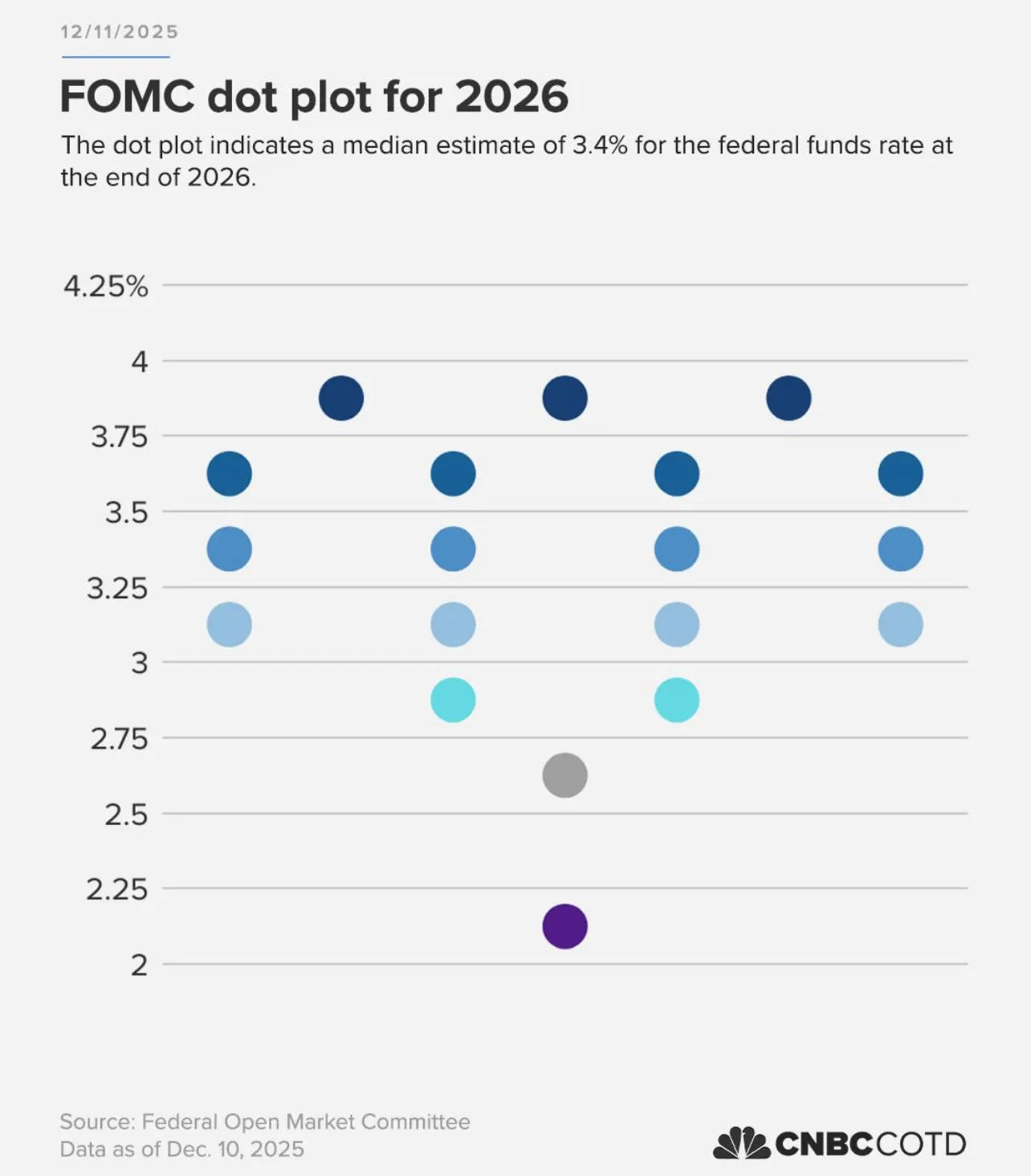

The bounce in the Debasement Trade following the Fed meeting came as a surprise, especially given that the cut and projections were more defensive than aggressive. Indeed, making a dovish case for 2026 is proving difficult, with the recent Dot Plot indicating only 1 to 2 cuts for the coming year.

Dot Plot for 2026 – Source: CNBC

Fed's Goolsbee, a dissenter of the recent cut (alongside Kansas Fed's Schmid), gave markets and risk assets a fresh reality check through multiple rounds of interviews. His stance is clear:

- The Fed was and still is in a "comfortable position to wait."

- The central bank is still blind on the inflation picture.

- Frontloading cuts now could carry significant risks.

Consequently, stocks printed a local top and have struggled to rebound since.

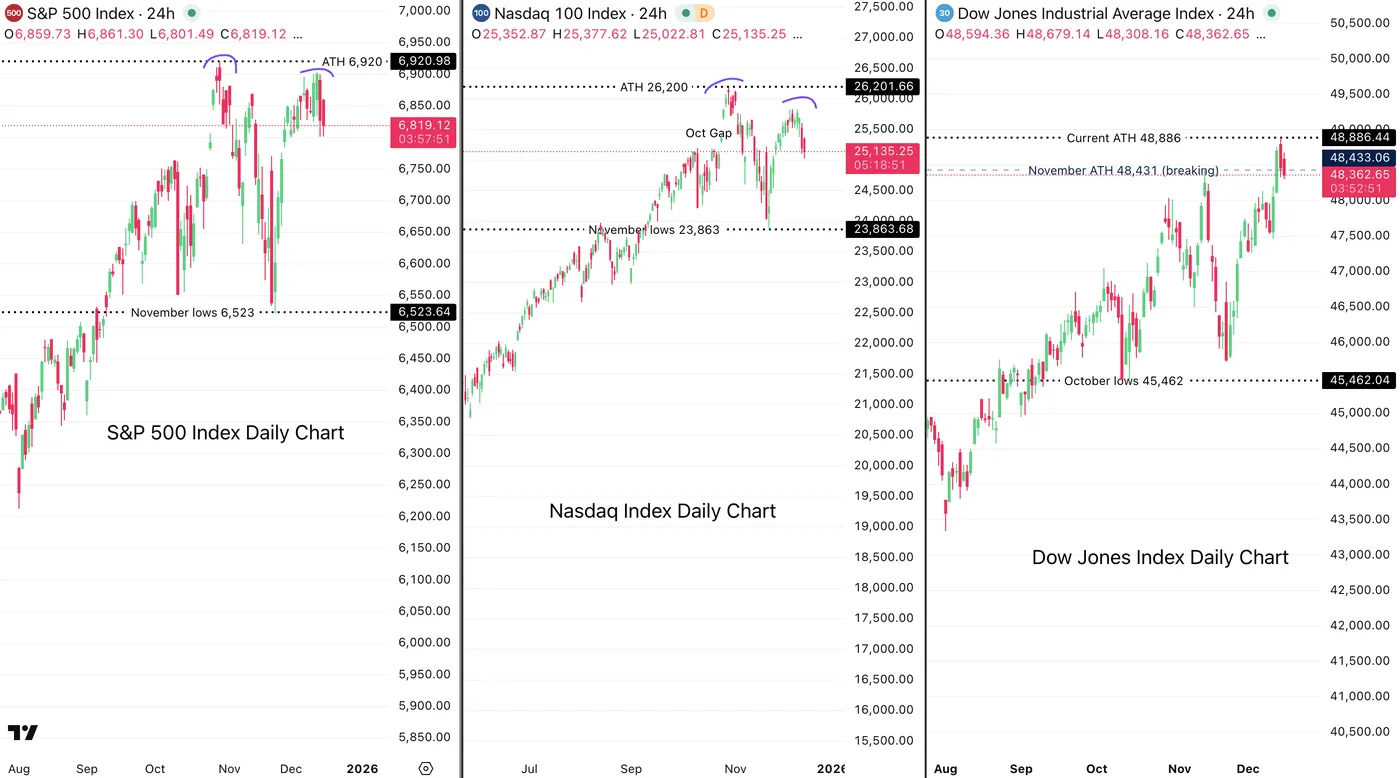

US Main Indexes Daily Outlook – Double tops in S&P 500 and Nasdaq? December 15, 2025 – Source: TradingView

NY Fed President John Williams just issued a counter-narrative, warning that the labor market poses new risks while noting that inflation has eased—effectively mirroring Goolsbee's comments but from a different angle of concern.

But dip-buyers haven't showed as much conviction this time around.

As markets wiggle around in this conflicting narrative, all eyes are on tomorrow's NFP report (preview coming up soon).

Let's dive into the intraday timeframe charts for all major US stock indexes to see where we stand.

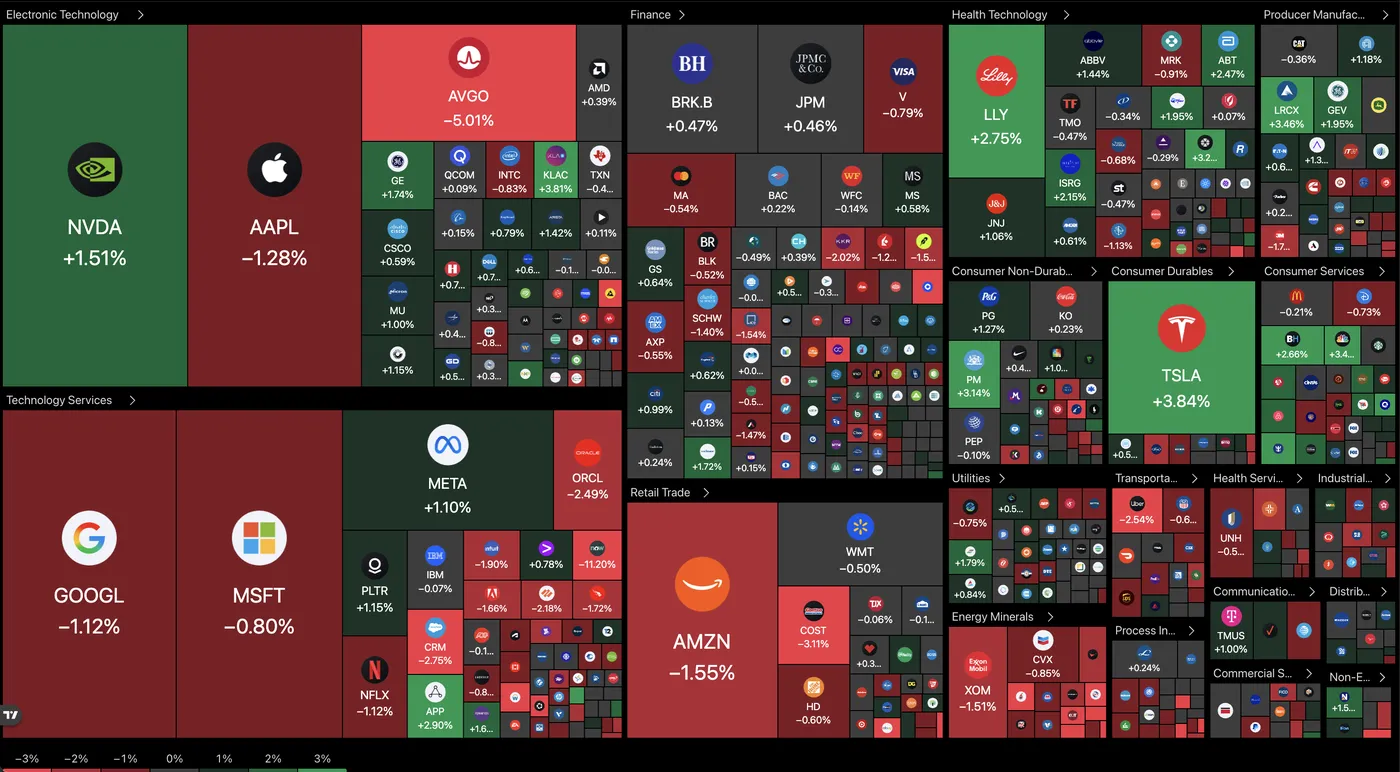

A mixed picture across sectors – Typical pre-NFP trading

Current picture for the Stock Market (12:50 A.M. ET) – Source: TradingView – December 15, 2025

Dow Jones – Buyers are not following through

Dow Jones (CFD) 4H Chart – December 15, 2025 – Source: TradingView

The Dow Jones, bellwether of the post-FOMC bullish sentiment, has just rejected to its higher timeframe upward channel (formed since May 2025).

Still evolving within the uptrend, the indication is more one of a slowdown in buyers' strength, for now, but things are still subject to change after tomorrow's release.

Having formed a Head and Shoulders on its 4H RSI, momentum is facing a wall.

Sellers have held prices at the past week lows throughout the entire morning session, so look at whether buyers manage to rebound from here.

Failing to do so opens the door for sellers to take the short-term control.

The hourly bull channel has its lower bound at around 47,850. Watch the reactions when and if prices get there.

Dow Jones technical levels of interest:

Resistance Levels

- All-time High resistance between 48,400 to 48,886 (rejecting)

- 48,700 session highs

- Potential Fib Target 2 49,526

- 50,000 Psychological Level and Potential Fib Target 3 (50,159)

Support Levels

- 50-period MA at 48,000

- Short-term Channel lows 47,850

- Key Support 47,000 (+/- 150) and MA 200

- August highs and November Lows 45,715

- 45,000 psychological level (next support and main for higher timeframe)

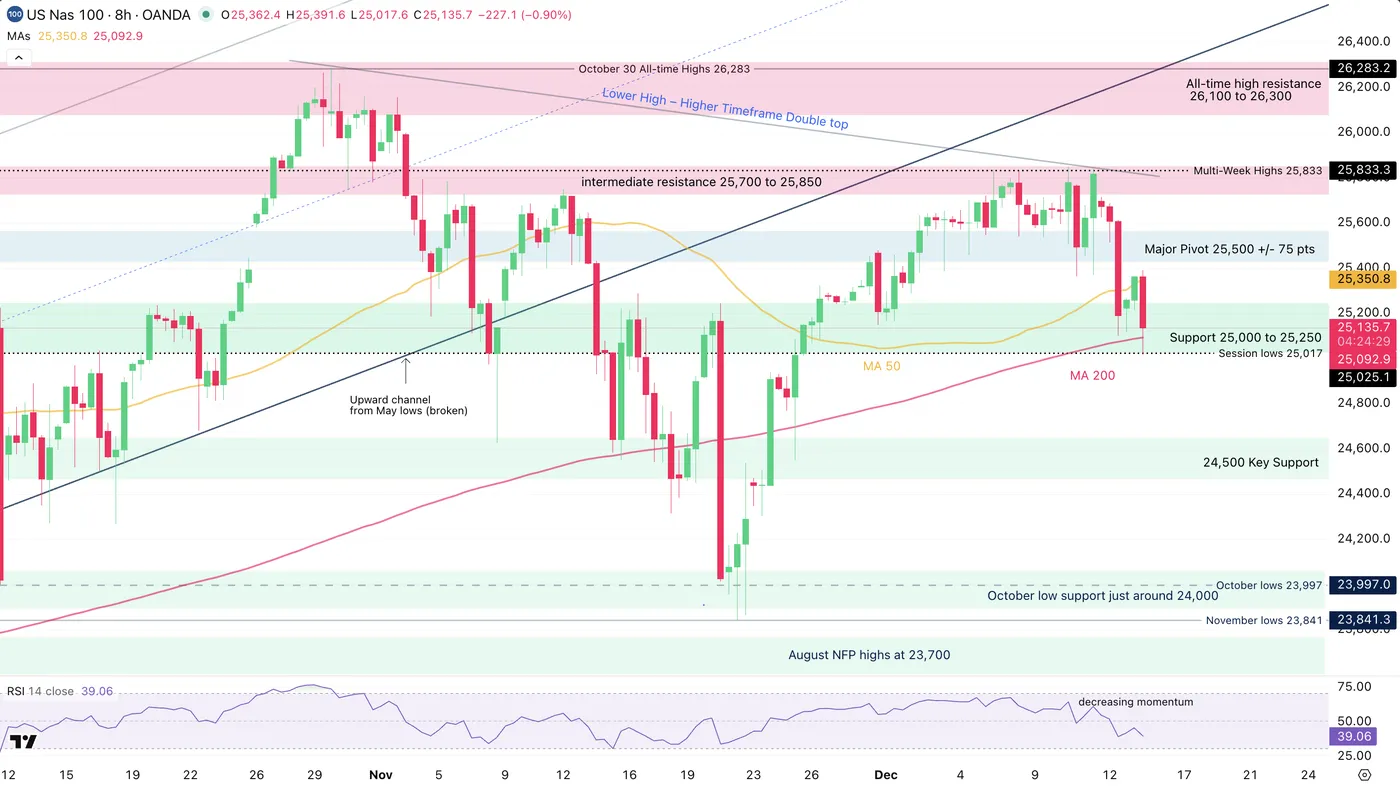

Nasdaq – Higher timeframe warning

Nasdaq (CFD) 4H Chart – December 15, 2025 – Source: TradingView

Nasdaq is sending scary signs for tech and AI bulls.

After a solid rebound ahead of the FOMC, the index hasn't been able to show any form of strength since the cut, even forming a double-top/lower high with the past week's bullish impulse.

The 25,000 level, acting as immediate support, will be one of its decisive support, supported by the 4H MA 200 for the bulls to maintain the mid-term bullish outlook.

Nasdaq technical levels of interest:

Resistance Levels

- Major Pivot 25,500 +/- 75 pts

- intermediate resistance 25,700 to 25,850 (recent highs)

- All-time high resistance zone 26,100 to 26,300

- Current ATH 26,283 (CFD)

Support Levels

- Support 25,000 to 25,250 (current lows, testing)

- 24,500 Main support and Pivot (recent rebound)

- October and November lows just below 24,000

- Early 2025 ATH at 22,000 to 22,229 Support

S&P 500 – A fragile range

S&P 500 (CFD) 4H Chart – December 15, 2025 – Source: TradingView

The S&P is still holding the 6,800 to 6,900 range indicated in our latest Index analysis but is now testing its support.

Holding 6,800 will be key for bulls to withhold their current strength, particularly as the higher timeframe is also sending signs of a double top – however not as scary as the one in Nasdaq.

Keep a close eye on the psychological support.

- Closing above would maintain the rangebound/bullish picture.

- Closing below opens the door to some downside all the way to November lows around 6,600.

S&P 500 technical levels of interest:

Resistance Levels

- 6,930 (current All Time-Highs)

- Weekly highs 6,896

- Resistance 6,850 to 6,880 (testing)

- ATH Resistance 6,900 to 6,930

Support Levels

- 6,800 Psychological Pivot

- Support 6,720 to 6,750 and 8H MA 50

- 6,490 to 6,512 Previous ATH October lows (recent lows)

- 6,400 psychological support

Safe Trades!

Fed’s Williams sees cooling jobs market, tariff risks contained

New York Fed President John Williams said monetary policy is “well positioned” heading into 2026, as the Fed has moved from a modestly restrictive stance toward neutral. He emphasized the need to return inflation to the 2% target without creating "undue risks" to the labor market, framing current policy as appropriately balanced after recent cuts.

Williams noted a shift in the risk profile. "the downside risks to employment have increased as the labor market has cooled, while the upside risks to inflation have lessened somewhat," he noted.

On tariffs, Williams said their impact on prices has been smaller than initially expected. Import levies appear to have caused one-off price increases rather than persistent inflation pressures. He expects tariff-related effects to be fully realized in 2026, with inflation moderating to around 2.5% next year before easing back to 2% in 2027.

Turning to the labor outlook, Williams sees the unemployment rate ticking up to 4.5% this year, but expects it to gradually decline over the following years alongside forecast growth of 2.25% in 2026. He stressed that the cooling in the labor market has been gradual, "without signs of a sharp rise in layoffs or other indications of rapid deterioration".

Fed’s Miran presses case for faster easing, shelter disinflation will offset sticky goods prices

Fed Governor Stephen Miran, who dissented at the last FOMC meeting in favor of a larger 50bps cut, reinforced his dovish stance in a speech today, arguing that inflation risks are being overstated.

Miran acknowledged that the lack of a clear downward trend in core goods prices could argue for keeping rates elevated, but said he expects disinflation in housing services to "counterbalance that possibility". The key risk, in his view, would be a renewed pickup in shelter inflation or a sustained overshoot in core goods prices. He judged both outcomes as unlikely, adding that if shelter inflation slows as expected while tariff effects disappoint, inflation could "undershoot our inflation target".

He also pushed back against reliance on backward-looking inflation measures. Shelter inflation, Miran argued, reflects supply-demand imbalances from "two to four years ago" rather than current conditions. Given long and variable policy lags, he said monetary policy should be calibrated for 2027, not anchored to inflation dynamics from 2022.

On the employment side of the mandate, Miran warned that labor market deterioration can occur quickly and nonlinearly, and can be difficult to reverse. Keeping policy unnecessarily restrictive risks avoidable job losses, particularly when prices have stabilized, even if at higher levels. He reiterated that a quicker pace of easing would better move policy toward a neutral stance and reflect the current balance of risks.

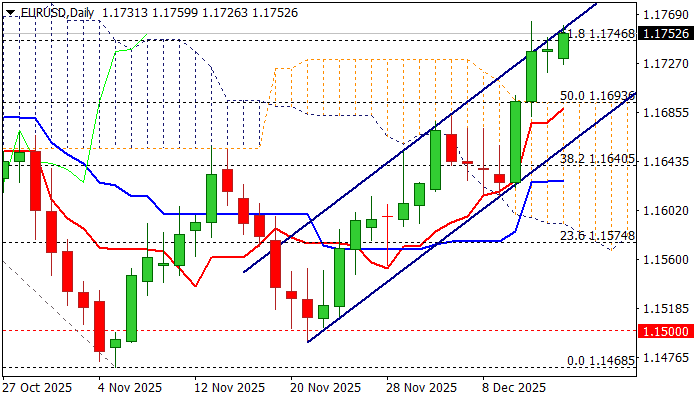

EURUSD: Bulls Hold Grip and Extend Gains Above Thick Daily Cloud

The Euro maintains firm tone at the start of the week and holds near new multi-week high, posted last Thursday (1.1762).

Bulls hold grip and probe again through cracked Fibo barrier at 1.1746 (61.8% of 1.1918/1.1468), also being on track for the third consecutive daily close above broken top of thick daily Ichimoku cloud (1.1693).

However, the near-term action continues to face headwinds from the upper boundary of bull-channel (bull-leg from 1.1490), with overbought daily studies adding to signals that the price may hold in a sideways mode and wait for fresh signals.

A batch of delayed economic data from the US will be released on Tuesday (NFP is the top event) and expected to provide more information to the Fed in shaping their monetary policy outlook, which would generate stronger direction signals.

Daily close above cracked Fibo level at 1.1746 to confirm fresh positive signals for probe through channel upper trendline and open way for acceleration above 1.18 mark.

Friday’s low (1.1750) offers immediate support, with near-term action to remain biased higher while holding above daily cloud.

Res: 1.1760; 1.1778; 1.1812; 1.1848

Sup: 1.1750; 1.1693; 1.1673; 1.1640

Sunset Market Commentary

Markets

Yields in core markets mostly were driven by technical considerations today. Investors were cautious to engage in outright positions as they await a huge batch of key economic data that will be released both in the US and EMU, starting tomorrow. Especially US payrolls and PMI’s published tomorrow might help markets to make up their mind on the amount and/or the pace of further Fed rate cuts in 2026. The European PMI’s will be read against recent indications from ECB policymakers that growth has been more resilient than expected, rekindling the debate on timing of a future ECB rate hike, potentially at the turn of 2026/27. The only relevant US data release today, the NY Fed Empire manufacturing survey showed an unexpected sharp drop from +18.7 to -3.9, but the negative reading on the current situation was counterbalanced by a substantial improvement in the forward-looking 6 months ahead index, improving to a solid 37.5 (best level since January). The market reaction to this (mixed) release was limited. US yields are ceding between 3.5 bps (5-y) and 2.5 bps (30-y). German Bund yields are easing -0.8 bps (2-y) to -2.8 bps (30-y). Equity markets try to find their composure after mainly US tech stocks again felt some shivers from headlines questioning the amount and the efficacy of AI spending by some tech bellwethers last week. The EuroStoxx 50 adds 0.7%. The all-time record high is less than 1.5% away. US equities try to recoup part of Friday’s setback (S&P +0.3%), but the move lacks conviction. For now, moves like the one end last week remain corrections including some rotation into less AI-related sectors. Key support levels stay out of reach, for now. The price of crude oil remains under pressure, amongst others driven by headlines that global cure oil stocks and stocks of oil products remain above seasonal averages.

On FX markets, the dollar struggles to avoid further losses. The narrative from this week’s data and CB meetings might favor the likes of the euro (better growth prospects) or the yen (BoJ rate hike, further policy normalization). DXY trades near 98.2 nearing a first support area at 98.13/03 (last week post-Fed low/mid-October low). EUR/USD at 1.1755 is holding near last week’s post-Fed top (1.1763). The yen this morning ‘rallied’ as a solid quarterly BoJ Tankan report gave a nihil obstat for the central bank to take a next step in its (admittedly very gradual) process of policy normalization. USD/JPY eases from 155.8 to 155.14. That said, the picture for the Japanese currency still looks unconvincing. A break below USD/JPY 154.35 could signal the yen gaining some traction. EUR/JPY also eases slightly (182.2) but stays withing reach of its all-time record since the introduction of the euro. EUR/GBP is holding stable (0.8775 area) with tomorrow’s labour market report and December PMI’s next data references for GBP trading.

News & Views

The Swiss State Secretariat for Economic Affairs has slightly revised upwards its forecast for economic growth in 2025 (adjusted for sporting events: 1.4% from 1.3%) and 2026 (1.1% from 0.9% in October) as the reduction in US tariffs have improved prospects for the sectors concerned. In 2027, Swiss growth is expected to normalize at 1.7% as the global economy gradually recovers. The KOF Swiss Economic Institute in its Winter forecast, also released today, plots a similar growth path. Domestic demand remains the main driver of growth with low inflation supporting real incomes: inflation is forecast to average 0.2% in both 2025 and 2026 (October forecast: 0.2% in 2025, 0.5% in 2026) before rising slightly to 0.5% in 2027. The outlook remains surrounded by a lot of mainly downside risks including lingering trade uncertainty, lofty valuations, debt-related problems (sovereign, balance sheet risks at FI’s, real estate markets) and geopolitics. Should any of these risks materialize, further upward pressure on the Swiss franc would be expected.

Reserve Bank of New Zealand governor Breman this morning observed that financial markets conditions have tightened since the November decision, beyond what is implied by the central projection for the OCR. It were her first public comments since taking the helm at the RBNZ earlier this month. With the remark, she pushed back against NZ money market expectations that the central bank in H2 of this year will turn back to hiking its policy rate. It was the natural reflex after the RBNZ suggested last month that it was likely done easing. The kiwi dollar initially lost ground, with NZD/USD dipping from 0.5810 to 0.5770, but most of the move was erased later on.

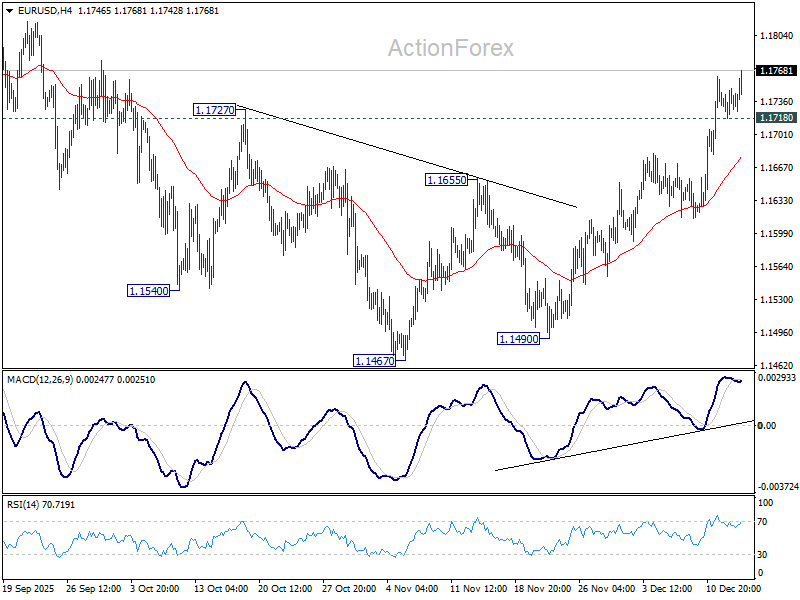

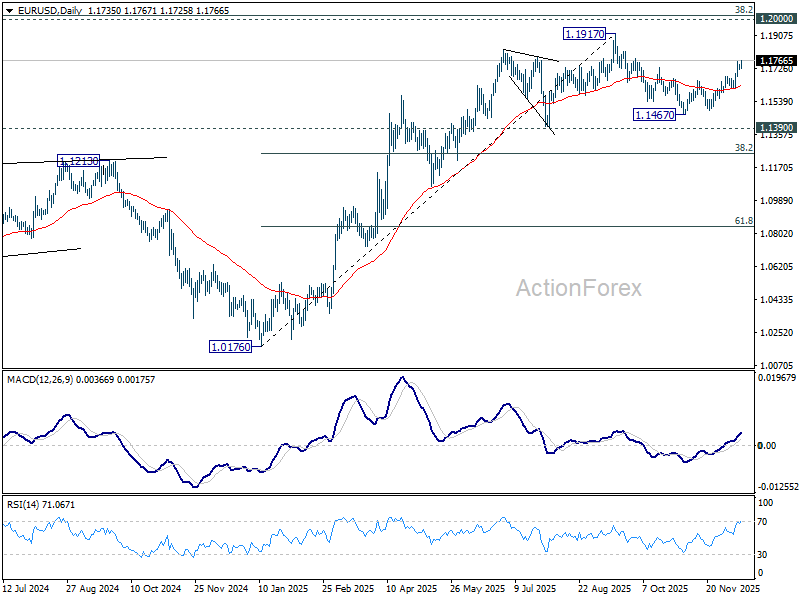

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1737; (R1) 1.1753; More….

EUR/USD's rise from 1.1467 continues today despite some loss of momentum as seen in 4H MACD. Intraday bias stays on the upside for retesting 1.1917 high. On the downside, though, below 1.1718 minor support will turn bias neutral and bring some consolidations first.

In the bigger picture, as long as 55 W EMA (now at 1.1373) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

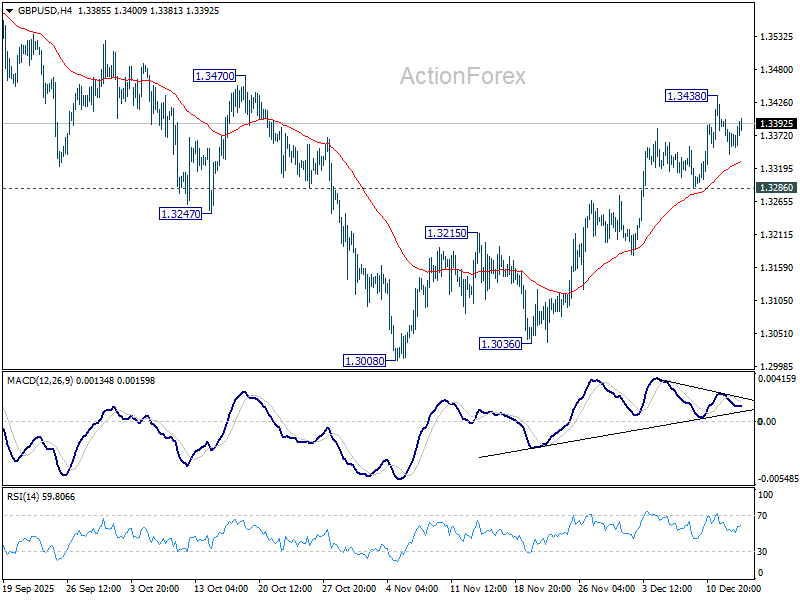

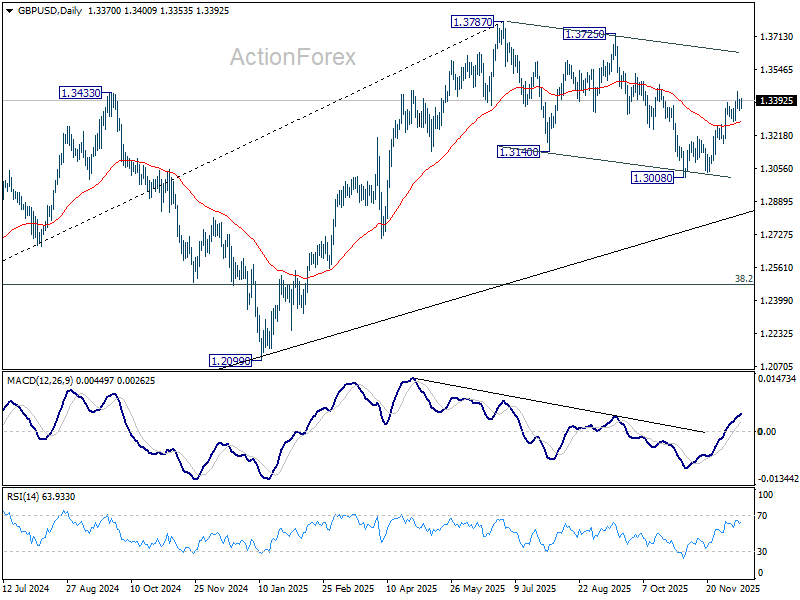

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3342; (P) 1.3371; (R1) 1.3400; More...

GBP/USD is extending consolidations below 1.3438 and intraday bias stays neutral. With 1.3286 support intact, further rally is expected. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3428 and firm break of 1.3470 resistance will pave the way back to retest 1.3787 high. However, sustained break of 1.3286 support will mix up the near term outlook.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

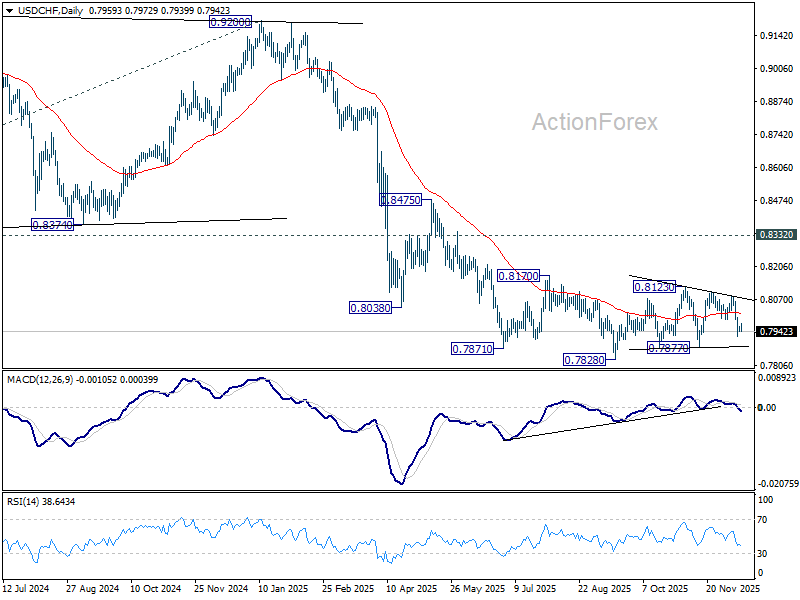

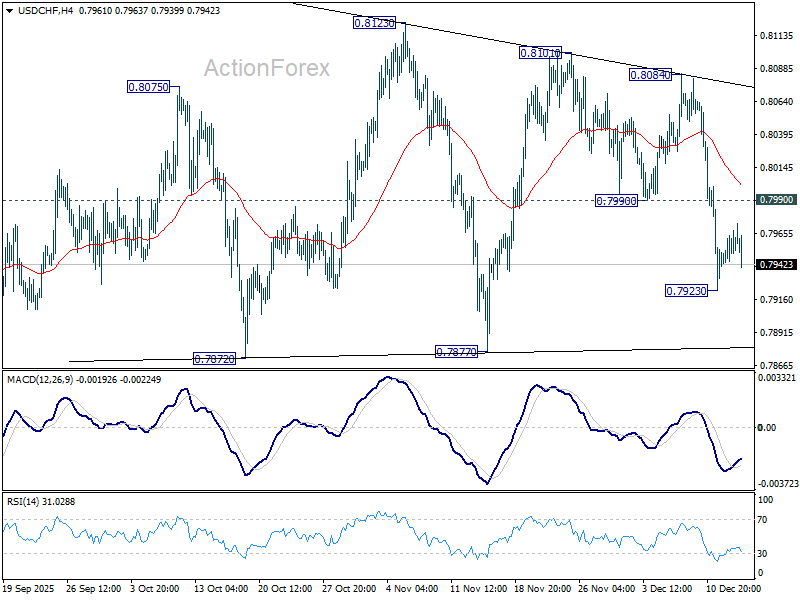

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7946; (P) 0.7955; (R1) 0.7970; More…

No change in USD/CHF's outlook and intraday bias stays neutral. Corrective pattern from 0.7828 is still extending. On the downside, below 0.7923 will target 0.7877 support. On the upside, though, break of 0.7990 support turned resistance will bring stronger rebound towards 0.8084.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.