Sample Category Title

AUD/USD Daily Report

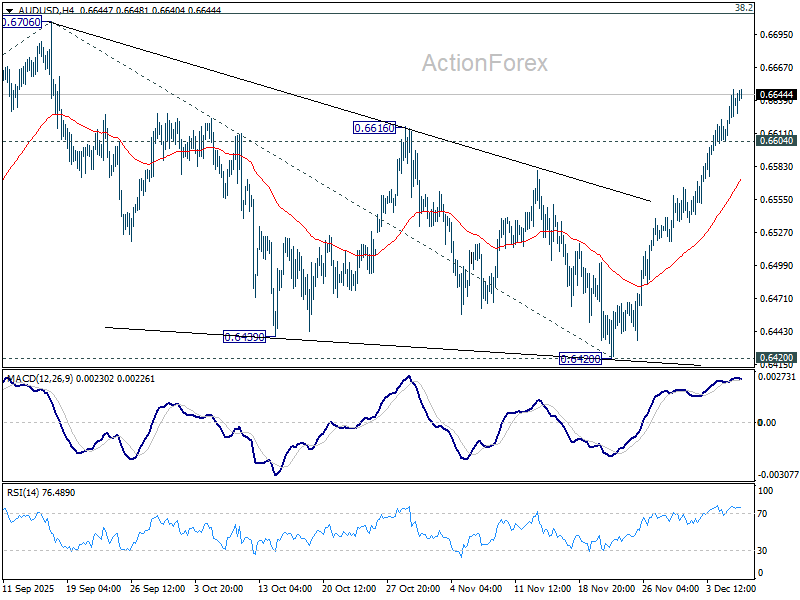

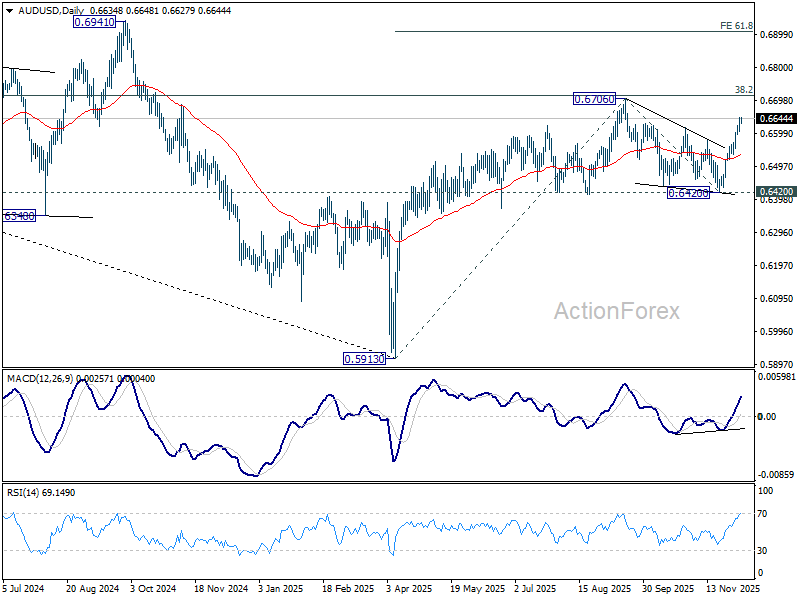

Daily Pivots: (S1) 0.6614; (P) 0.6632; (R1) 0.6658; More...

Intraday bias in AUD/USD remains the upside for retesting 0.6706 high. As noted before, rise from 0.5913 might be ready to resume. Decisive break of 0.6706 will confirm and target 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. On the downside, below 0.6604 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

Dollar Softens Ahead of High-Stakes Central Bank Week; EU–China Trade Tensions Simmer

Dollar weakened mildly in Asian trading as the new week began, but the move lacked conviction, with most major pairs still confined to familiar ranges. With a light data calendar on tap today and little in the way of market-moving headlines, early-session flows were cautious. Eurozone Sentix Investor Confidence is the only notable release in Europe, while the U.S. calendar is completely empty.

That calm will not last. Market activity is almost certain to pick up sharply as the week progresses, with four major central bank meetings on deck. The headline event is Wednesday’s FOMC decision, where markets are fully priced for another 25bps “risk-management” cut. But RBA, BoC and SNB decisions also carry potential for surprise—even if none are expected to move rates this week.

This cluster of central bank risk suggests the FX market could see unusually choppy conditions, especially as investors reposition around forward guidance rather than the policy moves themselves. With Fed communication still unclear regarding the 2026 path and RBA pricing now tilting toward the possibility of a hike next year, volatility clusters may emerge across USD-majors and AUD-crosses.

Away from central banks, traders will also keep a close eye on geopolitics—particularly the brewing tensions between the EU and China. French President Emmanuel Macron used his state visit to Beijing earlier this month to issue an unusually blunt warning: unless China takes steps to narrow its rapidly growing trade surplus with Europe, the EU may resort to U.S.-style tariffs.

Macron described the current trade imbalance as “unsustainable,” arguing that China is “killing its own customers” by dramatically reducing imports from Europe. He stressed that European industry is trapped between Trump's protectionism and China’s competitive pressure in industrial goods, calling it a “life or death” moment for the region’s manufacturing base.

In early Monday trading, Euro and Swiss Franc sit on the firmer side, followed by Yen, reflecting a mild preference for defensives. On the weaker side are Loonie and Dollar, followed by Sterling, while Aussie and Kiwi hold the middle ground. These early rankings are unlikely to hold for long, with the central bank bonanza almost certain to reorder the field.

In Asia, Nikkei rose 0.18%. Hong Kong HSI is down -1.02%. China Shanghai SSE is up 0.55%. Singapore Strait Times is down -0.41%. Japan 10-year JGB yield is up 0.002 at 1.955.

Japan’s wage picture improves but real incomes growth stays negative at -0.7%

Japan’s economic data delivered a familiar combination of improving nominal pay but still-depressed real incomes. Real wages fell -0.7% yoy in October, the 10th consecutive decline, though the rate of contraction moderated for the second month. Officials highlighted that fewer part-time roles and a higher share of full-time employees—who earn more—helped support headline income levels. Yet inflation of 3.4% yoy, driven mainly by food prices, continued to outpace wage gains.

Nominal earnings were considerably stronger, rising 2.6% yoy and beating forecasts for 2.2%. That marks a three-month high and extends the run of increases to 46 straight months, giving policymakers some evidence that wage momentum is holding up. Regular pay also expanded a robust 2.6% yoy, while bonus-driven special payments surged 6.7% yoy, providing a further boost. strain, limiting the lift to consumption.

The bigger disappointment came from growth data. Japan’s Q3 GDP was revised down to -2.3% annualized, from the initial -1.8%, making it the weakest quarter since 2023.

China’s exports rebound sharply by 5.9% yoy, US shipments remain deep in double-digit decline

China’s November trade data delivered a stronger-than-expected rebound, with exports surging 5.9% yoy to USD 330.35B, sharply reversing October’s -1.1% decline. The improvement marks the strongest performance since early 2024.

However, the headline strength masks continued weakness in China–U.S. trade, where shipments plunged -28.6% yoy, extending a run of eight straight months of double-digit declines. Despite the one-year tariff truce, effective levies remain elevated—averaging 47.5% on Chinese goods entering the U.S. and around 32% on American goods entering China—keeping bilateral flows under heavy pressure.

A clear divergence across regions stood out. Exports to ASEAN partners climbed more than 8% yoy, while shipments to the EU jumped nearly 15% y/y, underlining a rotation in China’s export momentum toward other major markets.

Imports, however, rose a softer-than-expected 1.9% yoy, pointing to still-cautious domestic demand despite policy easing efforts. With exports outpacing imports, China’s trade surplus widened to USD 111.68B in November.

Fed cut locked in, but guidance uncertain; RBA, BoC and SNB to hold the line

The week ahead brings one of the heaviest central bank line-ups, with the Fed, RBA, BoC and SNB all on deck. Yet only one of them—the Federal Reserve—is expected to move. Markets are firmly positioned for a 25bps risk-management cut, taking Fed funds to 3.50–3.75%, while the other three major central banks are widely expected to hold steady. Even so, the messaging from all four will matter for shaping early-2026 expectations.

For the Fed, Wednesday’s FOMC meeting is unquestionably the anchor event. The cut itself is not up for debate; market pricing still hovers near 90% change. What matters is what comes with it. One area to watch is the voting split, where attention will fall on whether ultra-dove Governor Stephen Miran again pushes for a 50bps move, and how many officials favor staying on hold. Any widening of dissent would reveal how fragmented the Committee has become.

The second focal point is the new economic projections. Back in September, the median dot implied only one more 25bps cut in 2026. With substantial macro uncertainty and incomplete data due to the government shutdown earlier this quarter, there may be caveats around precision. Still, the Fed’s broad views on growth, employment and inflation will deliver valuable clues on how policymakers interpret the recent slowing in activity.

Markets will also look to Chair Jerome Powell’s press conference, though expectations are modest. Powell is unlikely to lift the fog surrounding 2026. Internally, there is neither clarity nor consensus on how far or how fast cuts might proceed next year, especially as political noise grows louder ahead of leadership transition. His message may therefore lean heavily on data dependence.

In Australia, the RBA is expected to keep the cash rate unchanged at 3.60% on Tuesday. But the tone will be anything but neutral. October CPI surprised sharply to the upside at 3.8%, while trimmed-mean inflation ticked up to 3.3%. Combined with still-firm labor-market conditions, the inflation-control narrative has reclaimed center stage. Rate-cut expectations have evaporated in just two weeks.

Australia’s Big Four banks all expect the RBA to stay on hold, with three of them declaring the cutting cycle over. Reuters’ latest poll shows fewer than one-third of economists still expect one more cut by mid-2026—down from above 60% in November. Meanwhile, futures markets now price over a 70% chance of a rate hike by end-2026, marking a dramatic shift in sentiment.

Markets therefore expect a more hawkish-tilted message at the RBA’s final meeting of the year. While the base case remains “steady through 2026,” the balance of risk has clearly pivoted toward the upside. Acknowledging stronger demand momentum and sticky inflation may be enough to reinforce the idea that the next move could be up, not down.

The BoC follows on Wednesday, also expected to stay put at 2.25%. After signaling in October that the easing cycle had effectively ended, recent data—especially a string of strong labor-market reports—has given policymakers no reason to reopen the door to cuts. A Reuters poll taken even before the latest jobs surge showed 18 of 29 economists expecting no rate changes until at least 2027. That conviction has only strengthened.

Rounding out the week, the SNB meets Thursday and is widely expected to hold at 0.00%. Chair Martin Schlegel has repeatedly stressed that the threshold for returning to negative rates is very high. While Switzerland’s November CPI dipped back to 0.0% yoy, concerns about deflation are partially offset by recent Swiss Franc weakness and the US–Swiss trade deal, which slashes tariffs on Swiss exports from 39% to 15%. SNB will almost certainly stick to its current stance: ready to act if needed, but seeing no justification to move now.

Here are some highlights for the week:

- Monday: Japan labor cash earnings, current account, Q3 GDP final; China trade balance; Swiss SECO consumer climate; Eurozone Sentix investor confidence.

- Tuesday: Australia NAB business confidence, RBA rate decision; Germany trade balance.

- Wednesday: Japan PPI, China CPI, PPI; US employment cost index; BoC rate decision; FOMC rate decision.

- Thursday: New Zealand manufacturing sales; Japan BSI manufacturing;Australia employment; SNB rate decision; ; Canada trade balance; US trade balance, jobless claims.

- Friday: New Zealand BNZ manufacturing; UK GDP, trade balance.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6614; (P) 0.6632; (R1) 0.6658; More...

Intraday bias in AUD/USD remains the upside for retesting 0.6706 high. As noted before, rise from 0.5913 might be ready to resume. Decisive break of 0.6706 will confirm and target 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. On the downside, below 0.6604 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

China’s exports rebound sharply by 5.9% yoy, US shipments remain deep in double-digit decline

China’s November trade data delivered a stronger-than-expected rebound, with exports surging 5.9% yoy to USD 330.35B, sharply reversing October’s -1.1% decline. The improvement marks the strongest performance since early 2024.

However, the headline strength masks continued weakness in China–U.S. trade, where shipments plunged -28.6% yoy, extending a run of eight straight months of double-digit declines. Despite the one-year tariff truce, effective levies remain elevated—averaging 47.5% on Chinese goods entering the U.S. and around 32% on American goods entering China—keeping bilateral flows under heavy pressure.

A clear divergence across regions stood out. Exports to ASEAN partners climbed more than 8% yoy, while shipments to the EU jumped nearly 15% y/y, underlining a rotation in China’s export momentum toward other major markets.

Imports, however, rose a softer-than-expected 1.9% yoy, pointing to still-cautious domestic demand despite policy easing efforts. With exports outpacing imports, China’s trade surplus widened to USD 111.68B in November.

Japan’s wage picture improves but real incomes growth stays negative at -0.7%

Japan’s economic data delivered a familiar combination of improving nominal pay but still-depressed real incomes. Real wages fell -0.7% yoy in October, the 10th consecutive decline, though the rate of contraction moderated for the second month. Officials highlighted that fewer part-time roles and a higher share of full-time employees—who earn more—helped support headline income levels. Yet inflation of 3.4% yoy, driven mainly by food prices, continued to outpace wage gains.

Nominal earnings were considerably stronger, rising 2.6% yoy and beating forecasts for 2.2%. That marks a three-month high and extends the run of increases to 46 straight months, giving policymakers some evidence that wage momentum is holding up. Regular pay also expanded a robust 2.6% yoy, while bonus-driven special payments surged 6.7% yoy, providing a further boost. strain, limiting the lift to consumption.

The bigger disappointment came from growth data. Japan’s Q3 GDP was revised down to -2.3% annualized, from the initial -1.8%, making it the weakest quarter since 2023.

Research China – A Two-Speed Economy

The latest data in China has changed little to the overall picture of a two-speed economy with domestic demand looking weak while exports and tech continue to power ahead.

Growth is set to be close to the government's 5% target again this year but finishes the year on a weak note. We look for new stimulus to lift growth in the first half of 2026 and that the target will again be set around 5%.

We stick to our growth forecast of 4.9% in 2025 followed by 4.8% in 2026. In 2027 we project 4.7% growth.

More important will be the composition of growth and we expect to see more of the same with domestic demand still not strong enough to match supply keeping overcapacity and deflationary pressures as lingering problems.

In the new Five-Year Plan, China doubles down on tech and puts more weight on boosting consumer demand. It will require new and more forceful measures to stabilize housing, though, which may take some time still.

US-China tensions have eased again but we expect a continued bumpy road ahead. Tensions with EU have intensified this year and we see little respite in 2026.

The question of reunification with Taiwan still lingers but we see limited risk of military conflict during Trump's Presidency.

EUR/USD Holds Firm at Support, Raising Odds of Additional Gains

Key Highlights

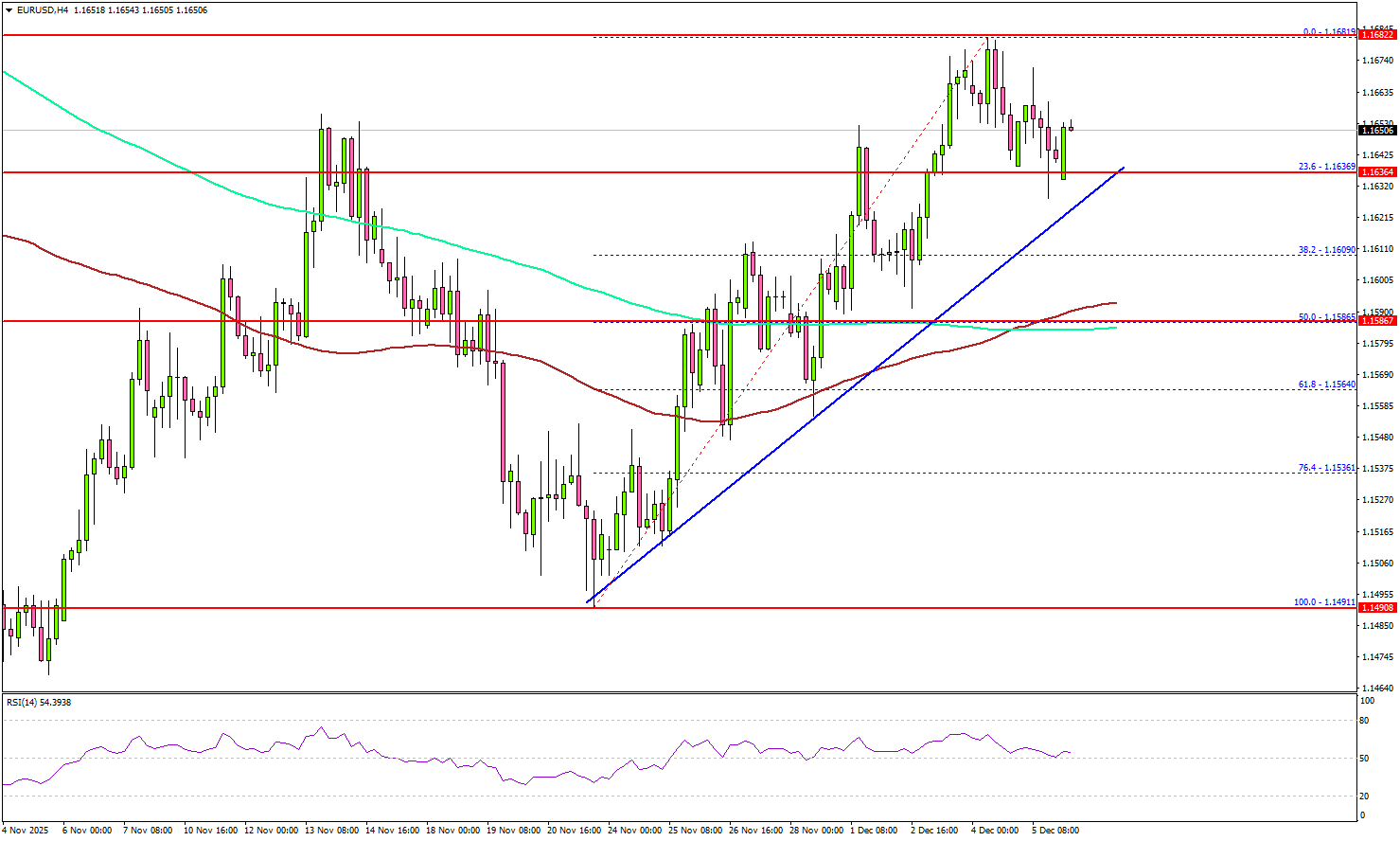

- EUR/USD gained pace for a move above the 1.1620 resistance.

- A key bullish trend line is forming with support at 1.1630 on the 4-hour chart.

- GBP/USD started consolidating gains above 1.3300.

- USD/JPY might start a fresh increase if it clears the 156.00 resistance.

EUR/USD Technical Analysis

The Euro started a decent increase above 1.1550 against the US Dollar. EUR/USD cleared the key barrier at 1.1600 to enter a positive zone.

Looking at the 4-hour chart, the pair gained pace for a move above 1.1620. It traded as high as 1.1681 and settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

It is now consolidating gains above 1.1620. There is also a key bullish trend line forming with support at 1.1630. Immediate resistance sits near 1.1660. The first key hurdle is seen near 1.1680.

A close above 1.1680 could open the doors for a move toward 1.1725. Any more gains could set the pace for a steady increase toward 1.1780.

On the downside, there is key support at 1.1630 and the trend line at 1.1620. The next support is 1.1580 and the 100 simple moving average (red, 4-hour). A close below the 100 simple moving average (red, 4-hour) could spark a bearish move and send the pair to 1.1510. Any more losses might call for a test of 1.1465.

Looking at GBP/USD, the pair rallied above 1.3300 and recently started a consolidation phase. The main support sits at 1.3260.

Upcoming Key Economic Events:

- Euro Zone Sentix Investor Confidence for Dec 2025 - Forecast -7.4, versus -7.4 previous.

Global Markets Hold Firm with Focus on Upcoming Fed Meeting

Markets were calm last week with no major surprises. Fed Chair Powell did not discuss the economy or monetary policy, so traders didn’t get any new signals on inflation or interest rates. Even so, equities continued their recovery as risk appetite improved, although trading volumes stayed light.

U.S. data was slightly positive. The ISM Manufacturing PMI beat expectations, consumer sentiment improved, and the Core PCE Price Index was close to forecasts, showing inflation is easing. Talks to end the war in Ukraine continued but had little effect on markets.

The U.S. dollar weakened as investors expect the Federal Reserve to cut interest rates this week. In Japan, the 10-year bond yield continued to rise, which the market is watching carefully, though it has not caused major issues yet. Bitcoin stayed under pressure, and gold remained quiet.

Markets This Week

U.S. Stocks

The recovery in the Dow continued last week, with no negative news to disrupt the recent buying ahead of this week’s Federal Reserve meeting. The 10-day moving average is pointing higher, and the uptrend is expected to continue unless the Fed surprises the market with a statement that lowers expectations for interest rate cuts in 2026. Resistance levels are at 48,000, 48,500, and 49,000, while support is seen at 47,000, 46,500, 46,000, and 45,000.

Japanese Stocks

Japanese stocks rose marginally last week, following the gains in U.S. markets. However, the advance was limited as expectations for a Bank of Japan interest rate hike increased after comments from Governor Kazuo Ueda. The Nikkei is likely to continue trading sideways around the 50,000円 level, offering range-trading opportunities, with slightly more downside risk if the yen continues to strengthen. Resistance is at 51,000円, 51,500円, and 52,000円, while support is at 49,000円, 48,000円, and 47,000円.

USD/JPY

The yen strengthened last week, continuing to reverse some of the gains seen since Takaichi became Prime Minister, as expectations for a Japanese interest rate hike next week increased. The market is finding support ahead of 154, so some buying may return this week, though there is downside risk if the Federal Reserve surprises markets by signaling faster-than-expected interest rate cuts for 2026. Resistance is at 156, 157, and 158, while support is at 154, 153, and 152.

Gold

Gold remained strong, supported by expectations of lower U.S. interest rates and continued safe-haven demand. Resistance at the upper Bollinger Band limited gains as traders waited for the Federal Reserve meeting. The metal is finding support at the 10-day moving average and looks likely to continue higher in the current environment. Resistance is at $4,250, $4,350, and $4,380, while support is at $4,150, $4,100, and $4,050.

Crude Oil

Hopes that lower U.S. interest rates will support demand, along with uncertainty around the Ukraine–Russia conflict, helped WTI move higher and push back above $60. The recent downward trend has now been broken, so a range-trading approach between $58 and $62 looks more suitable this week. Resistance remains at $65, $66.50, $70, and $75, while support is at $55 and $50.

Bitcoin

Bitcoin traded sideways last week as the market showed diverging views on its long-term outlook after the drop from record highs back below $100,000. The 10-day moving average is now pointing sideways, so a range-trading strategy remains the best approach in the short term. Resistance is at $95,000 and $100,000, while support is at $85,000, $80,000, and $75,000.

This Week’s Focus

- Monday: Japan GDP, China Trade Balance, U.S Factory Orders

- Tuesday: Australia RBA Interest Rate Decision, Japan BOJ Gov Ueda Speaks

- Wednesday: U.S. Fed Interest Rate Decision

- Thursday: Australia Unemployment Rate, U.S. Trade Balance

- Friday: U.K. GDP

The focus this week will be the U.S. Federal Reserve’s interest rate decision, where the market expects a 0.25% rate cut. The statement that follows will be especially important, as traders look for clues on the timing of further cuts in 2026 and how the Fed views the economy and inflation trends. Apart from the Fed meeting, there are few major data releases, and the market is gradually shifting its attention toward the start of the holiday season.

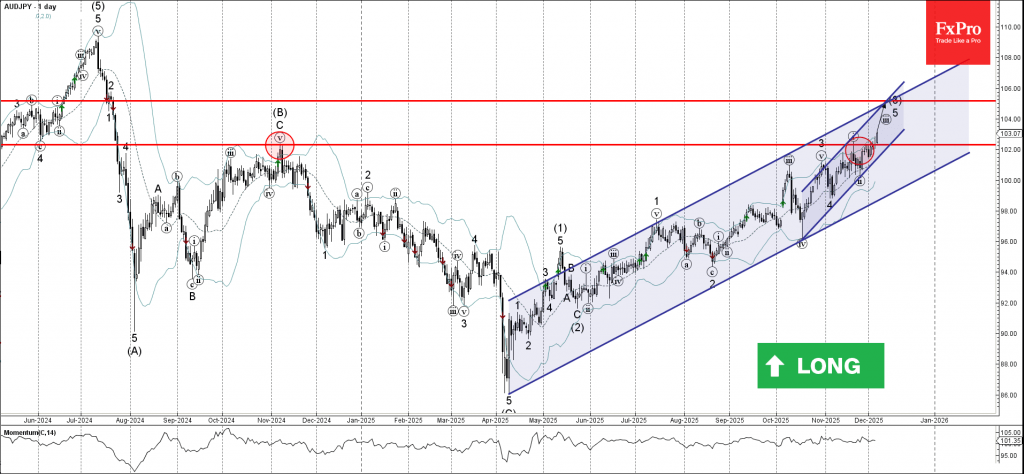

AUDJPY Wave Analysis

AUDJPY: ⬆️ Buy

- AUDJPY broke long-term resistance level 102.30

- Likely to rise to resistance level 105.20

AUDJPY currency pair recently broke above the long-term resistance level 102.30 (former multi-month high from November).

The breakout of the resistance level 102.30 accelerated the active impulse waves iii and 5 – which belong to the intermediate impulse wave (3) from May.

Given the overriding daily uptrend and the strongly bullish Australian dollar sentiment, AUDJPY currency pair can be expected to rise to the next resistance level 105.20.

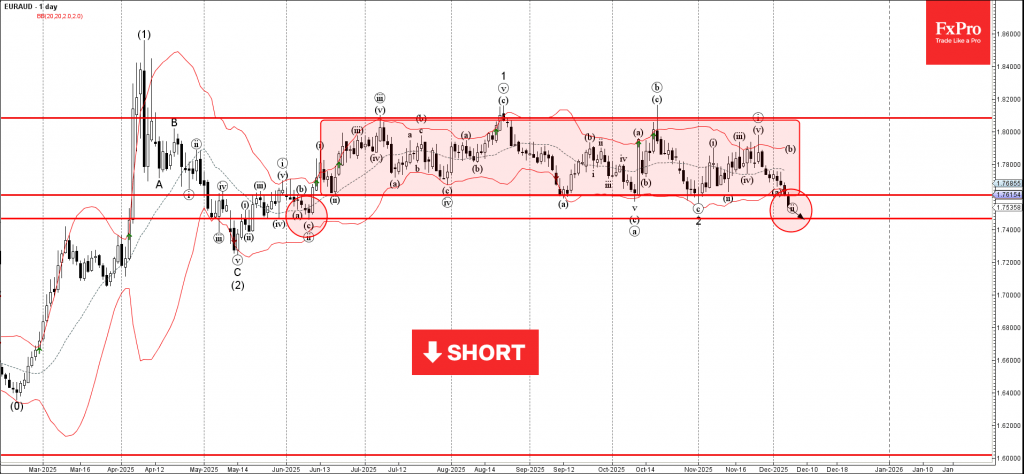

EURAUD Wave Analysis

EURAUD : ⬇️ Sell

- EURAUD broke the support level 1.7600

- Likely to fall to support level 1.7465

EURAUD currency pair recently broke the support level 1.7600 (which is the lower boundary of the sideways price range inside which the pair has been trading from June).

The breakout of the support level 1.7600 accelerated the active short-term correction ii from the end of November.

Given the strongly bullish Australian dollar sentiment seen today, EURAUD currency pair can be expected to fall to the next support level 1.7465 (former monthly low from June).