Sample Category Title

Sunset Market Commentary

Markets

Risk-off remains the by default bias on global markets today even as there was little in the way of hard economic news to guide trading. High (US tech) valuations and low visibility on Fed policy are most often mentioned. Whatever the reason, yesterday’s selling/risk-off in the US also again spilled over to Asia this morning. In this move Japan was an underperformer in equities (Nikkei -3.21%) but also LT Japanese government bonds again showed signs of stress with several LT yields (40-y 3.68%, 10-y 1.75%) testing/touching multi-year lows. Admittedly political tensions between Japan and China probably are part of the reason for the underperformance of Japanese equities. Even so, it is striking that selling accelerates even as the new government is discussing big additional fiscal stimulus. The lingering debate on fiscal sustainability apparently makes that more fiscal stimulus is no longer a support for local risk assets. Later today, BOJ governor Ueda reported on a meeting with PM Takaichi. He labelled the meeting as candid and good. He indicated that there was no request from the PM on BOJ policy. This suggests that the BOJ can proceed with gradual policy normalization according to what it deems necessary. While confirming the BOJ’s independence, it also is another indication that there is little room for an Abenomics 2.0 policy with both fiscal and monetary stimulus.

Whatever the domestic issues potentially being at work in Japan, the risk-off also again rotated further into European and US equity markets. The EuroStoxx 50 again is ceding 1.7%. The index again trades below the March top, a first technical warning. US indices also again are ceding between 0.5% (S&P) and 1.0% (Dow/Nasdaq). As indicated there was little macro news to ‘explain’ the selling. The weekly US private ADP job report showed an average 2500 of private job losses in the four weeks ended Nov 1, to be compared with a 14.3k average weekly loss in the previous weekly release. The direct impact on global markets was limited. The US curve bull steepens with yields easing between 5.0 bps (2 & 5y) and 1.8 bps (30-y). Also the German/EMU yield curve steepens slightly (2-5-y German yield minus 3 bps; 30-y +0.5 bp). The outperformance at the short end to some extent probably is somewhat of a correction after EMU money markets recently sharply reduced the probability of a final ECB rate cut next year. Still hardly any directional moves in the major USD cross rates. EUR/USD is going nowhere near 1.16. DXY holds near 99.5 (marginal daily decline). The yen still underperforms with USD/JPY trading north of 155 and EUR/JPY even touching all-time record levels at 180+.

News & Views

Usage of the Bank of England’s long-term repo facility (six months) dropped to a three-month low during today’s weekly operation. Financial institutions borrowed around £1.28bn, down from £6bn the week before and the lowest since August 26. The steep drop comes after the BoE raised the cost of drawing on the facility to Bank Rate + 3 bps from 0 bps. That decision was already announced in June and intends “to balance incentives for participants” between the short-term repo and long-term repo facilities. The central bank’s short-term (one week) repo received £92bn of usage last week, the second highest since the BoE introduced it on the same day it started to sell gilts from its portfolio in 2022. Threadneedle Street seeks to shift towards a repo-led model for providing liquidity instead of outright bond buying.

The Hungarian central bank (MNB) kept the policy rate unchanged, once again, at 6.5%. It said that tight monetary conditions remain warranted due to risks to the inflation environment as well as trade and geopolitical tensions, with the latter in particular a risk for HUF weakness. The MNB said that the currency’s strengthening since the beginning of the year is beginning to show in purchase prices and added that FX market stability is of key importance in reducing inflation expectations – which remain elevated among households. Inflation itself stood at 4.3% last month with government price-dampening measures masking actual inflationary pressures. The central bank expects the inflation rate to ease into the 3% +/- 1ppt tolerance range by end-2025 and decrease further in early 2026. Growth should pick up next year amid improving exports and continued strong consumption dynamics. The government’s increased budget deficit (to 5%) in 2025 and 2026, the central bank said, is having a stimulating effect on domestic demand. Today’s expected policy outcome fails to inspire HUF. The forint remains near a 1.5 yr high around EUR/HUF 384.3.

BoE’s Pill: Don’t over-interpret data noises

BoE Chief Economist Huw Pill warned against putting too much emphasize on single data points today.

At a panel, he said, " policymakers should be cautious about over-interpreting the latest news in data, because there is a lot of noise in the data flow, and partly because of some of the challenges our colleagues in the Office for National Statistics have faced."

Pill said admitted that underlying inflation pressure might not be as intense as the 3.8% headline inflation suggested. However, he cautioned that other inflation related data had not slowed as much as expected.

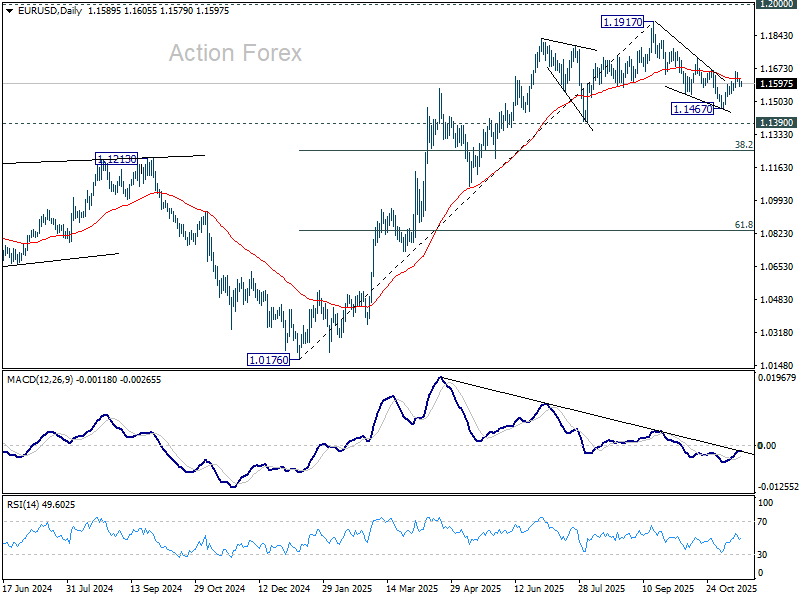

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1576; (P) 1.1600; (R1) 1.1619; More…

Intraday bias in EUR/USD stays neutral at this point. Fall from 1.1917 could have completed as a three wave correction at 1.1467. Above 1.1655 will target 1.1727 resistance first. Firm break there will solidify this bullish case and bring retest of 1.1917 high. However, break of 1.1561 will revive near term bearishness and target 1.1467 low instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

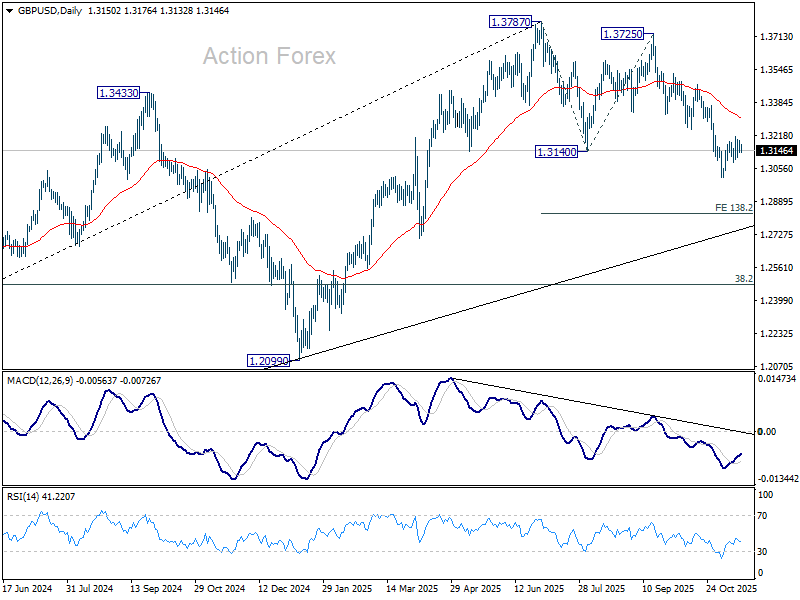

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3130; (P) 1.3161; (R1) 1.3187; More...

Intraday bias in GBP/USD stays neutral and more consolidations could be seen. Further decline is expected as long as 1.3247 support turned resistance holds. Break of 1.3008 will resume the fall from 1.3787, and target 138.2% projection of 1.3787 to 1.3140 from 1.3725 at 1.2831. Nevertheless, firm break of 1.3247 will suggest that fall from 1.3787 has completed as a corrective move already.

In the bigger picture, the break of 55 W EMA (now at 1.3182) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2824) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

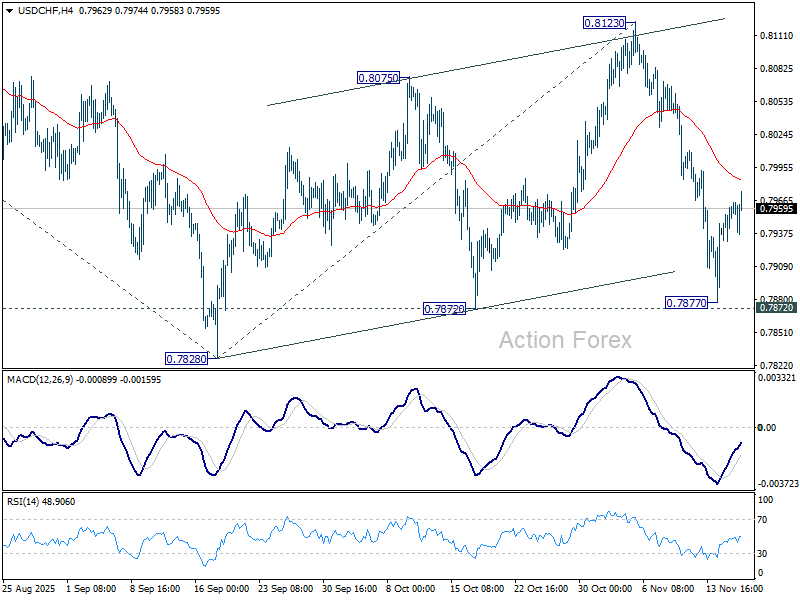

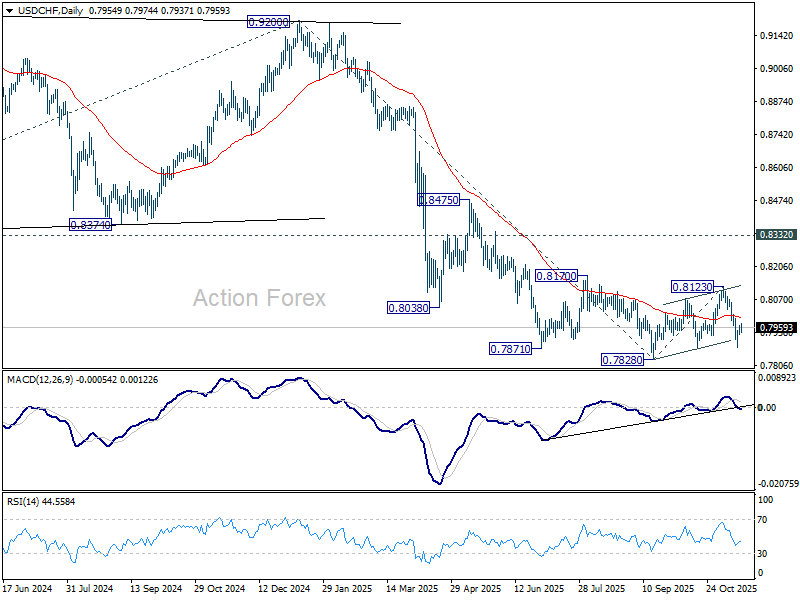

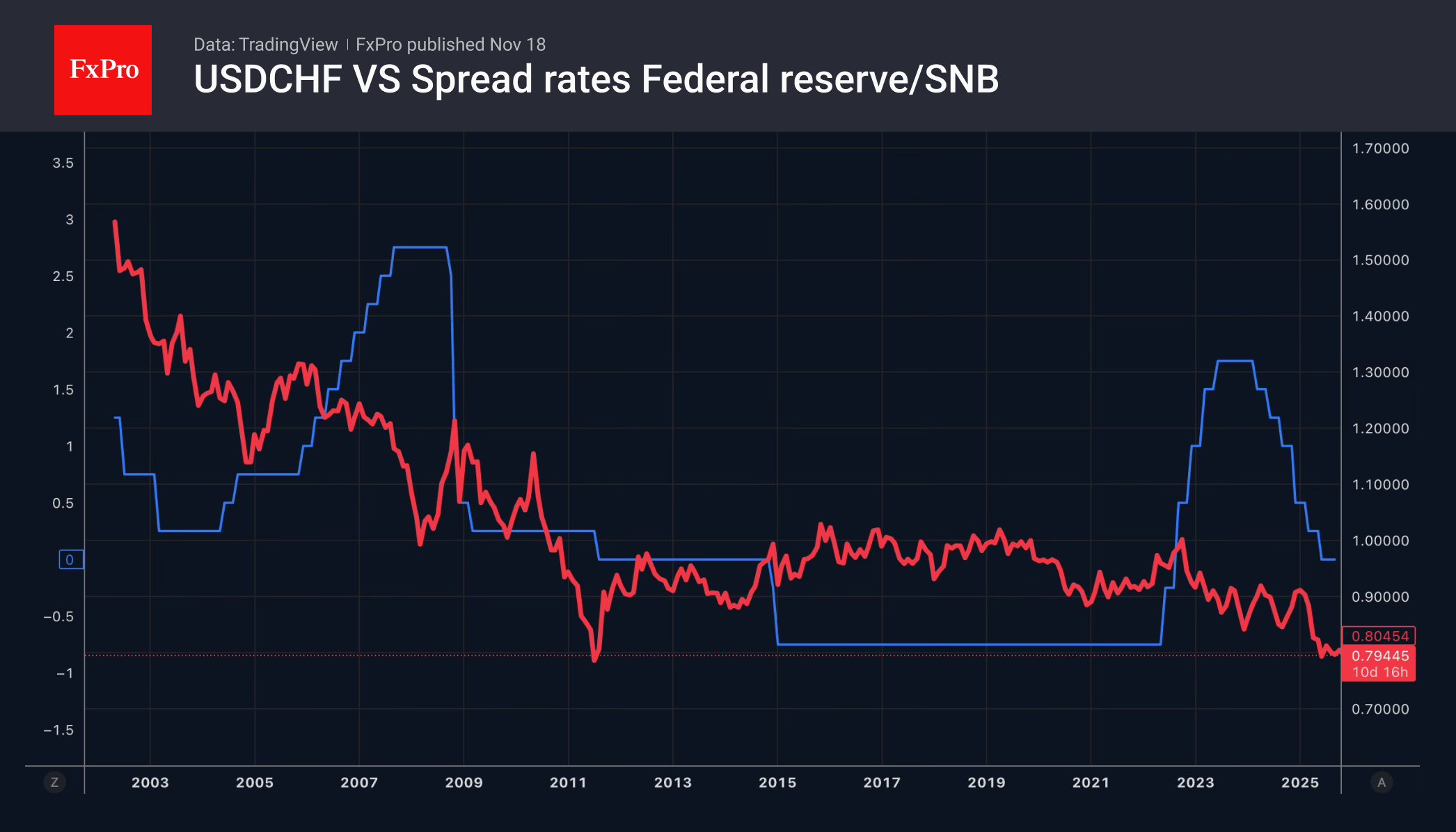

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7941; (P) 0.7953; (R1) 0.7975; More…

Intraday bias in USD/CHF remains neutral for the moment. As noted before, corrective rebound from 0.7828 could have completed with three waves up to 0.8123. Break of 0.7872 support will pave the way through 0.7828 to resume the larger down trend. Next near term target is 38.2% projection of 0.9200 to 0.7828 from 0.8123 at 0.7599. However, sustained break of 55 4H EMA (now at 0.7984) will mix up the outlook.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

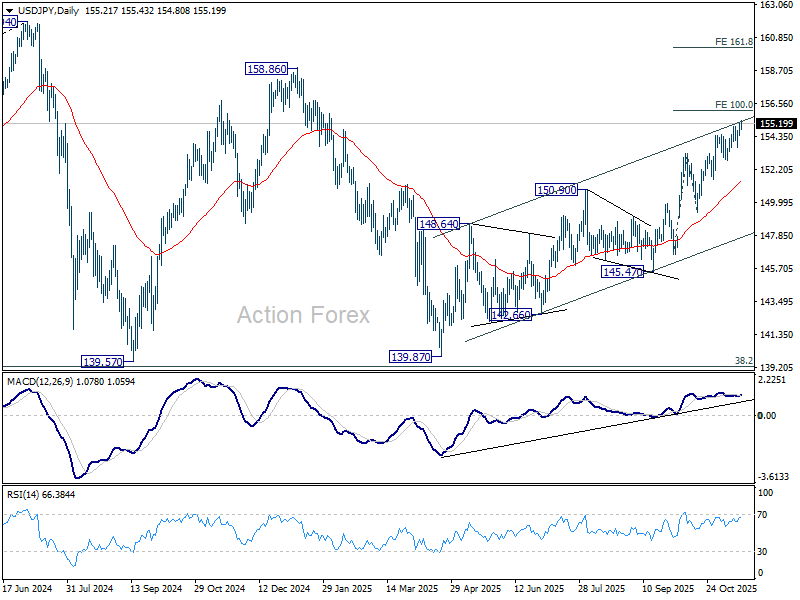

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.43; (P) 154.86; (R1) 155.70; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise is part of the rally from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 153.60 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.45).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Tech Slide Continues, Yen Still Lacks BoJ Signal

Global markets remain under pressure today as risk sentiment deteriorates further across regions. Europe opened firmly lower, tracking the broad declines seen earlier in Asia, while U.S. futures point to another weak session. Today’s tone is one of cautious de-risking, with markets showing little appetite to buy dips ahead of several major event risks.

Technology stocks continue to drive the weakness. Selling pressure on Nvidia stayed intense ahead of the company’s third-quarter results due after Wednesday’s close. Nvidia has been the symbolic leader of the AI-driven market rally, and the reaction to its earnings could determine whether sentiment stabilizes or slips into a deeper correction. With concerns over market breadth, excessive valuations, and shaky AI fundamentals resurfacing, traders are positioning defensively.

Attention is on Thursday’s U.S. non-farm payrolls release — the first since the government reopened. Today’s initial jobless claims, at 232k, and continuing claims, at 1.957m, produced almost no market reaction. That muted response raises doubts about how strongly markets will react to the delayed NFP, though the potential for a volatility shock should not be dismissed.

In Japan, the highly anticipated meeting between Prime Minister Sanae Takaichi and BoJ Governor Kazuo Ueda offered far less clarity than markets had hoped. Traders were looking for sharper messaging on policy direction given rising political pressure on the central bank. Instead, the meeting produced broad, non-committal remarks that did little to shift expectations.

Ueda reiterated that Japan’s wage-price dynamics are improving thanks to both government policy and the BoJ’s supportive stance. He described the central bank as “gradually adjusting” monetary support to ensure a stable path toward the 2% inflation goal. Takaichi, he said, appeared to accept his assessments. Yet nothing in his comments hinted at a change in stance or timeline.

Asked about the timing of the next rate hike, Ueda repeated that decisions will be made “appropriately” based on incoming data — a stance that leaves the market no clearer about whether a December move is even on the table. Given the political backdrop, traders remain convinced that January or later is more likely.

In FX, Dollar holds the top spot for the week so far, followed by Loonie and Sterling. At the other end of the spectrum, Aussie is the weakest performer, with Yen and Swiss Franc next in line. Kiwi and Euro sit squarely in the middle.

In Europe, at the time of writing, FTSE is down -1.39%. DAX is down -1.42%. CAC is down -1.40%. UK 10-year yield is up 0.006 at 4.543. Germany 10-year yield is down -0.015 at 2.701. Earlier in Asia, Nikkei fell -3.22%. Hong Kong HSI fell -1.72%. China Shanghai SSE fell -0.81%. Singapore Strait Times fell -0.86%. Japan 10-year JGB yield rose 0.015 to 1.749.

RBA minutes show no clear bias toward next move

RBA minutes from the November 3–4 meeting underscored a Board that sees the economy as “broadly in balance” and saw no justification to adjust the cash rate at this stage. While the central projection remains aligned with the RBA’s employment and inflation objectives, policymakers stressed that the next move in rates is not predetermined. Members agreed it was “not yet possible to be confident” about whether holding steady or easing further would become the more likely scenario.

The minutes outlined several conditions that could support keeping policy unchanged. One is a stronger-than-expected recovery in "demand" that lifts employment. Another is if incoming data suggest the economy’s "supply capacity" is weaker than previously assessed — potentially due to persistently high inflation or softer-than-expected productivity growth. A third is a reassessment of whether monetary policy is still "slightly restrictive". Any of these outcomes, the RBA said, would "limit the scope for further easing".

But the Board also detailed circumstances that could justify another rate cut. A material weakening in the labor market remains the clearest trigger. A second downside risk is if GDP growth disappoints — for example, if households turn "more cautious about spending" than currently assumed. In these cases, excess capacity would likely reappear, cooling inflation and warranting additional support.

Overall, the minutes confirm a central bank in wait-and-see mode. The RBA is not ruling out further easing, but neither is it leaning strongly toward it. The next several months of data — particularly on productivity, inflation persistence, and household spending — will be crucial in determining whether the Board holds steady or reopens the easing path in 2026.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.43; (P) 154.86; (R1) 155.70; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current rise is part of the rally from 139.87. Next target is 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance. However, considering bearish divergence condition in 4H MACD, firm break of 153.60 support will indicate short term topping, and bring deeper pullback to 55 D EMA (now at 151.45).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Dollar Preparing for Battle

- The hawks in the Fed are pulling the blanket over themselves, but the doves are not giving up without a fight.

- USD may fall on a sell-the-news trade and CHF has become one of the favourites.

The decline in the chances of a Fed rate cut in December from 72% to 48% over the past couple of weeks should have sent the EURUSD into a knockout. However, the futures market anticipates that by the end of the cycle, the federal funds rate will have fallen to 3.25%, down from its current level of 3.75%. Moreover, the question of December remains open. ‘Dove’ Christopher Waller continues to insist on a rate cut amid signs of weakness in the labour market. On the contrary, the Fed ‘hawks’ are inclined to leave everything as it is.

Kansas City Fed President Jeffrey Schmid’s concerns about inflation go beyond tariffs. Rising energy and healthcare costs, as well as higher insurance premiums, suggest that inflation will not return to 2% from its current 3% for some time. Cleveland Fed President Beth Hammack notes that inflation has exceeded the Fed’s target for more than four years. The scale of the tariff increase means that high prices cannot be considered a temporary phenomenon.

A decisive battle is expected between the FOMC’s ‘hawks’ and ‘doves’ in December. October served as a rehearsal. Following the previous meeting, Jerome Powell was forced to dash the market’s illusions about a rate cut at the end of the year. Investors fear that the Fed’s overly hawkish rhetoric in the minutes will dash hopes for easing next month. These speculations are supporting dollar purchases.

Following the publication of the minutes on 20 November, the US employment figures for September will be released. They will be released with a huge delay, but the trend is important here. If the labour market continues to cool, this will once again make easing in December the main scenario, playing into the hands of EURUSD buyers. Conversely, positive non-farm payrolls will strengthen the dollar.

Meanwhile, the White House has finally lowered tariffs on Swiss goods from 39% to 15%. Expectations surrounding this event have made the franc the main favourite on the Forex market. However, according to Commerzbank, the USDCHF peak is unlikely to be too deep. Most of the good news is already priced in. The future of the pair will depend on the interest rate differential between the Fed and the Swiss National Bank.

EUR/USD Declines as Market Awaits Key US Employment Data

The EUR/USD pair extended its losses for a third consecutive session, falling to 1.1591 on Tuesday. The downward pressure persists as investors await a backlog of delayed US economic data, expected to provide crucial signals on the Federal Reserve's interest rate path. The market's primary focus is the delayed September employment report, which traders will scrutinise for signs of a softening labour market.

The rhetoric from Federal Reserve officials remains mixed, contributing to the market's indecision. Several officials have recently expressed scepticism about the need for a December rate cut, citing persistent inflationary pressures. However, this was counterbalanced by Governor Chris Waller, who confirmed his support for a cut, and Vice Chair Philip Jefferson, who advocated for a gradual approach due to rising labour market risks.

This conflicting guidance has led to a repricing of rate expectations. Futures markets now imply only a 43% probability of a 25-basis-point cut in December, a significant decline from the odds priced at the start of the month. The US dollar has found broad support, strengthening against commodity-linked currencies like the Australian and New Zealand dollars.

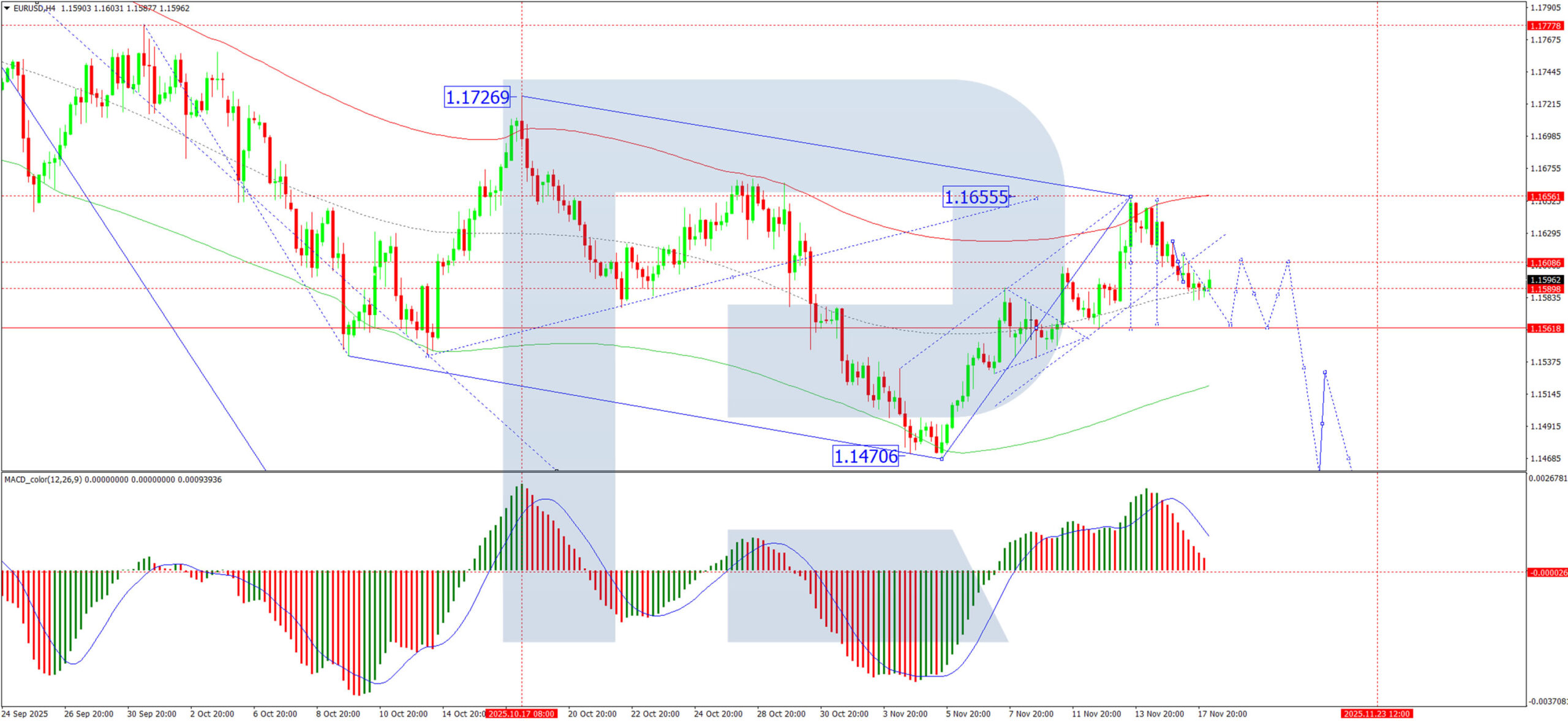

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, EUR/USD has breached its growth wave channel at 1.1605, opening the path for a downward move. We anticipate an initial decline to 1.1564, followed by a technical pullback to retest the 1.1605 level from below. This retest is likely to present a fresh selling opportunity before the downtrend resumes towards the primary target of 1.1560. The MACD indicator confirms this bearish outlook. Its signal line, while above zero, is pointing decisively downward, indicating that selling momentum is overpowering any residual strength.

H1 Chart:

On the H1 chart, the pair has broken downwards from a consolidation range around 1.1600, confirming the second leg of a bearish impulse. The immediate target for this move is 1.1560. Upon reaching this level, a corrective bounce back towards 1.1600 is a distinct possibility. The Stochastic oscillator supports this corrective view. Its signal line is rising from the 20 level towards the 50 level, suggesting that short-term downward pressure may be exhausted, paving the way for a temporary rebound.

Conclusion

The EUR/USD remains under pressure amid a strengthening US dollar and uncertain Fed policy. While conflicting comments from officials have created volatility, the overall technical structure is bearish. The breach below 1.1605 suggests further losses are likely, with an initial target at 1.1560. Any near-term rebounds towards the 1.1600/05 resistance zone are expected to be temporary, offering potential opportunities to re-enter the prevailing downtrend.

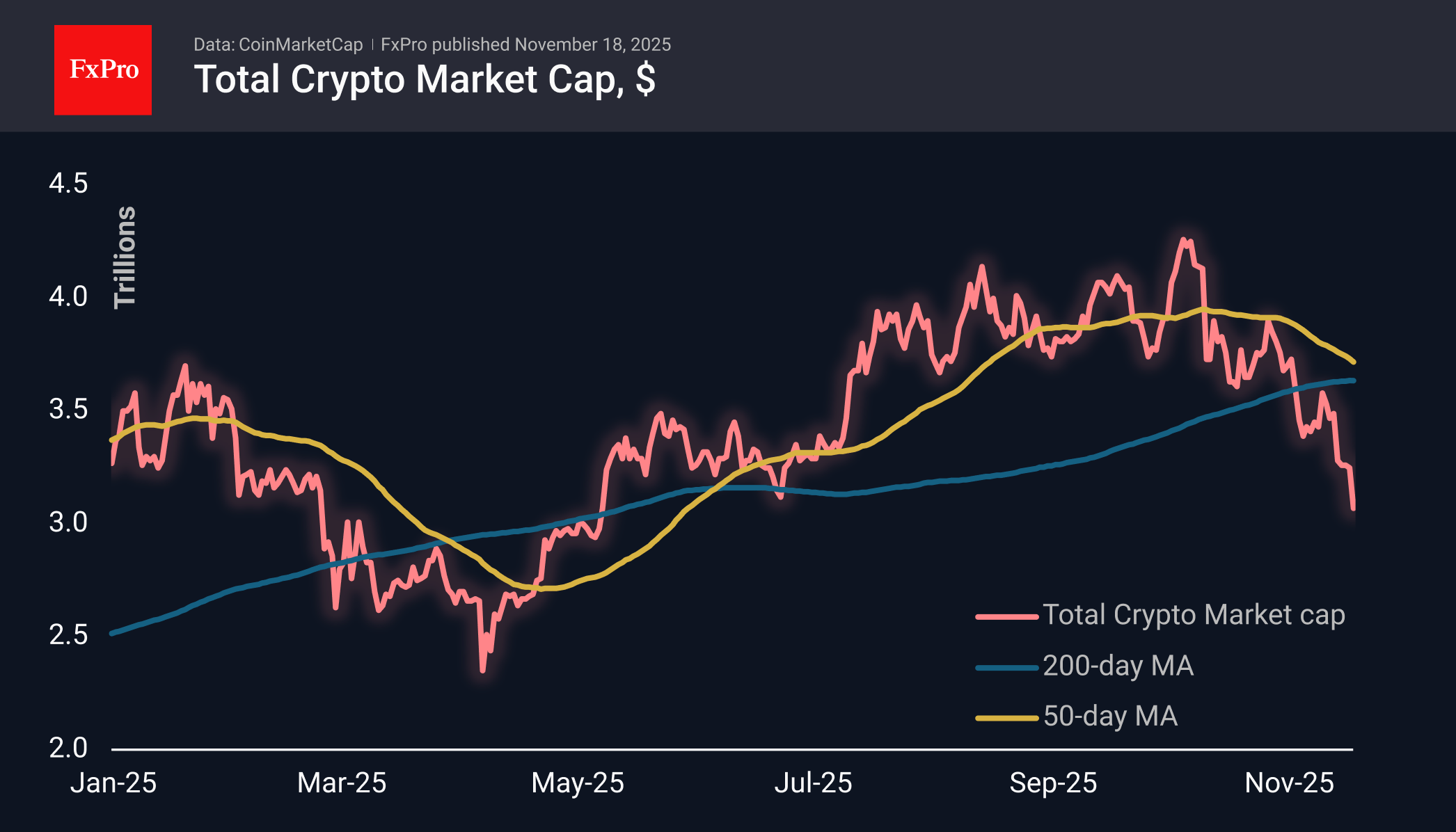

Crypto Market Accelerates Decline

Market Overview

The crypto market is experiencing a sharp decline, losing another 4% over the past 24 hours and falling back to $3.07 trillion, its lowest level since early May. The decline is accelerating relative to the trend observed since 10 October. At this stage, the market is being dragged down by major coins — Bitcoin, Ethereum, XRP — which are losing more than 5%, while some altcoins remain in the shadows. It is unlikely that this should be considered a sign of strength for coins such as Monero (+2.7%), Tron (-1.8%) or Bitcoin Cash (-2.4%). It would be more accurate to say that the bears have not yet reached them.

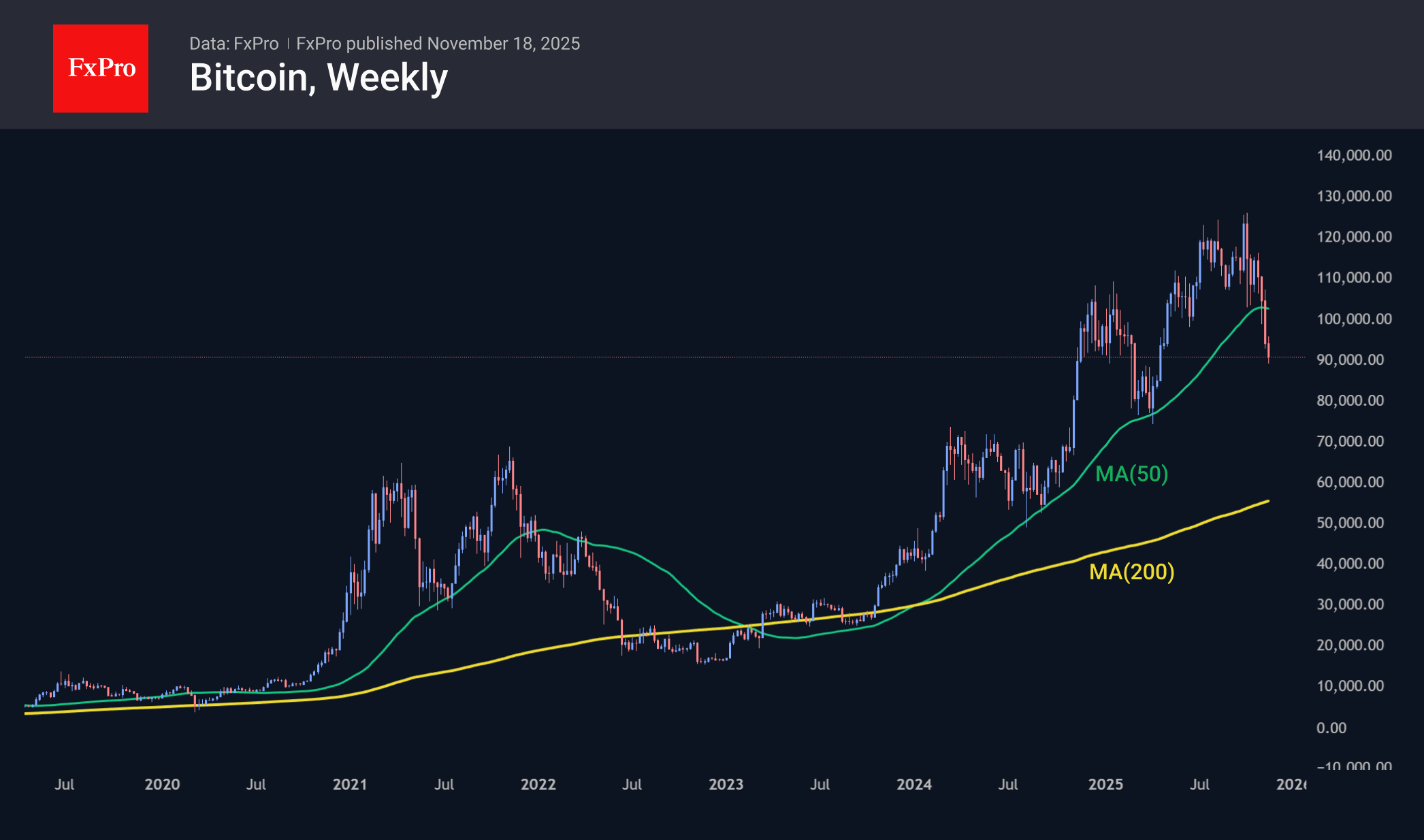

Bitcoin fell below $90K, trading at its lowest levels since the end of April. As expected, the dip below the 50-week moving average at the end of last week triggered sellers, confirming the breakdown of the bullish trend that had lasted for the previous two years. Now, the working scenario appears to be a chance for BTC to dip to its 200-week moving average. In 2022, this path took 9 weeks and over 30 weeks to form the bottom.

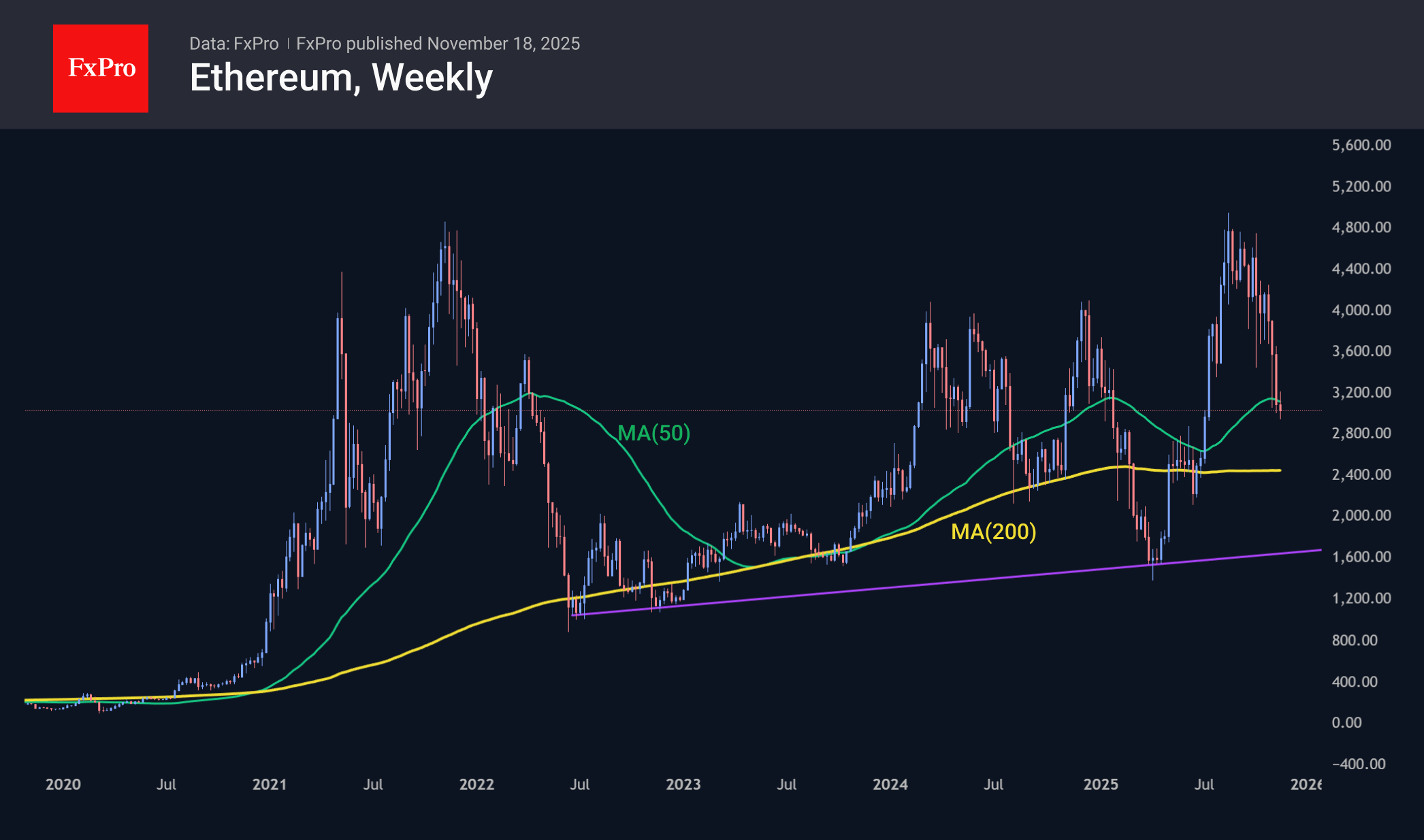

Ethereum fell below $3,000, following Bitcoin, which rolled back below its 50-week moving average. In this case, the 200-week average (approximately $2,300) will deter sellers, and we are considering a decline to $1,700 as a working pessimistic scenario.

News Background

According to CoinShares, global investment in crypto funds declined by $2.036 billion last week, marking the third consecutive week of outflows. Investments in Bitcoin fell by $1.378 billion, in Ethereum by $689 million, in XRP by $16 million, and in Solana by $8 million. Investments in Sui rose by $6 million, in Litecoin by $3 million, and in ETFs with multiple crypto assets by $31 million.

The fall of Bitcoin from its record highs in October was triggered by the capitulation of short-term holders, rather than the distribution of coins by long-term investors, according to XWIN Research.

Ethereum is entering a Supercycle phase like the one that brought Bitcoin a hundredfold increase since 2017, said BitMine CEO Tom Lee. In his opinion, the market decline is attributed to issues with several large market makers attempting to provoke liquidations in Bitcoin.

The inflow of stablecoins to Binance reached $9 billion in 30 days. The indicator is close to historical peaks, which previously preceded strong market movements, notes CryptoOnchain analyst. In his opinion, capital in standby mode can quickly change the market dynamics in favour of the ‘bulls’.

Strategy’s business model is entirely dependent on funds buying its shares and is built on ‘fraud,’ said Peter Schiff, a well-known cryptocurrency critic and gold advocate. Since July, Strategy’s shares have fallen by more than 50%, and recently, its capitalisation has fallen below the value of its assets.