Sample Category Title

Risk-On Rebound as U.S. Shutdown Nears End

Global risk appetite improved markedly today, with strong gains in Asia carrying over into European trading and U.S. futures pointing higher. Investors found renewed confidence amid signs of political progress in Washington, where the Senate approved the first stage of a bipartisan deal to end the monthslong government shutdown.

The agreement would fund federal operations through January 30 next year and could potentially reverse some of the permanent layoffs that occurred during the 35-day impasse. The development offered a welcome relief to markets reeling from last week’s tech-led selloff, noting that a resolution to the shutdown could restore data flow and remove a key source of uncertainty for investors.

If the Senate’s amended measure clears the House of Representatives and wins President Donald Trump’s signature, the deal would avert further disruptions to federal services and allow normal budget processes to resume. The prospect of restored government operations is also raising hopes that upcoming economic releases will help clarify the Fed’s policy outlook ahead of its December meeting.

The renewed optimism was clearly reflected in the currency markets, where high-beta and commodity-linked currencies led gains. Aussie outperformed, followed by Kiwi and Loonie, as investors re-engaged with risk-sensitive trades.

At the other end of the spectrum, Yen weakened further, extending losses from the Asian session. The currency was weighed by both improved global sentiment and fresh political pressure on the BoJ, after a senior economic adviser to Prime Minister Sanae Takaichi urged policymakers to postpone any rate hike until at least January. His comments reinforced the view that fiscal priorities remain dominant in Tokyo, keeping near-term BoJ tightening expectations subdued.

Swiss Franc also softened as investors rotated out of safe havens, while Dollar traded lower. Meanwhile, Euro and Sterling are trading in the middle.

In Europe, at the time of writing, FTSE is up 0.89%. DAX is up 1.78%. CAC is up 1.34%. UK 10-year yield is up 0.016 at 4.485. Germany 10-year yield is up 0.004 at 2.676. Earlier in Asia, Nikkei rose 1.26%. Hong Kong HSI rose 1.55%. China Shanghai SSE rose 0.53%. Singapore Strait Times fell -0.09%. Japan 10-year JGB yield rose 0.023 to 1.702.

Fed’s Daly: Policy must avoid trading one mistake for another

San Francisco Fed President Mary Daly said the FOMC has appropriately reduced policy rates by a total of 50bps this year as part of a "prudent risk management approach", noting that the adjustments provide “needed insurance” for the labor market while keeping policy “modestly restrictive” to further curb inflation.

In an essay published today, Daly posed the central question now facing the Fed: Will more rate cuts be needed? She argued that while policymakers must remain alert to inflation risks—drawing lessons from the 1970s and the post-pandemic surge—they must also avoid overcorrecting and stifling growth.

“We don’t want to work so hard to not be the 1970s that we cut off the possibility of the 1990s,” she wrote, warning that an excessive focus on inflation history could trade one mistake for another.

Daly emphasized that getting policy right will require “an open mind” and careful evaluation of evidence on both sides of the debate.

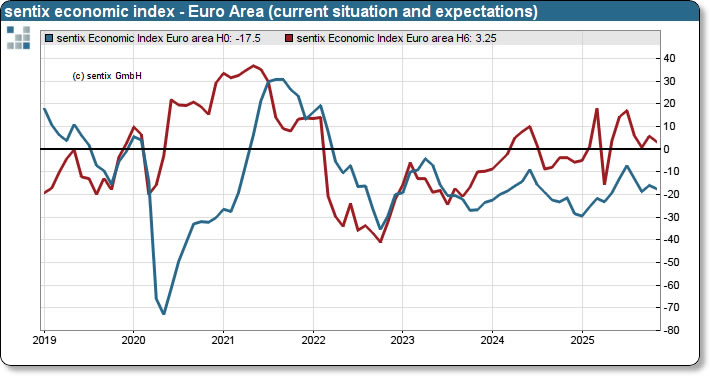

Eurozone Sentix falls to -7.4, growth outlook darkens, debt fears persist

Eurozone investor sentiment deteriorated again in November, reinforcing concerns that the bloc’s economy remains mired in stagnation. Sentix Investor Confidence Index fell sharply to -7.4 from -5.4 in October, missing expectations of -3.9. Current Situation Index dropped to -17.5 from -16.0. Expectations slipped to 3.3 from 5.8.

Sentix said there was “little sign of an autumn upturn” and that the Eurozone “continues to languish, with no signs of momentum for the future.” The survey noted that the persistence of such gloomy assessments points to an ongoing process of contraction, with the path to 2026 seemingly “predetermined” as the economy remains unable to break free from its slump.

Still, one faint positive emerged from the report: inflation concerns eased notably. The Sentix inflation barometer rose 9 points to -11, suggesting investors see central banks acknowledging weak growth conditions and possibly adjusting policy accordingly. However, Sentix warned that ballooning government debt remains a structural problem, keeping the fiscal policy barometer deeply negative at -32 and limiting how far refinancing conditions can realistically fall.

BoJ summary show split narrows as members debate near term rate hike

The BoJ’s Summary of Opinions from October 29–30 meeting revealed a growing consensus among policymakers that conditions are nearly in place for a rate hike. Eight opinions either called for raising interest rates soon or outlined conditions under which borrowing costs should rise in the near term—marking the clearest sign yet that the BoJ is preparing for its next move.

Several members emphasized that while immediate action may not be necessary, the Bank “should not miss the timing to raise the policy interest rate.” Others noted that a hike would likely follow if global economic conditions remained stable and corporate wage-setting momentum was sustained. One view stated that “conditions for taking a further step toward normalizing the policy rate have almost been met,” but stressed the need to confirm that underlying inflation is firmly entrenched.

Still, some members urged caution. One participant argued that the BoJ should take “a little more time” to assess the impact of U.S. tariffs and Japan’s new fiscal direction before tightening policy further. The minutes reinforce market expectations that the Bank is leaning toward a rate increase either in December or early 2026, contingent on wage data and external stability.

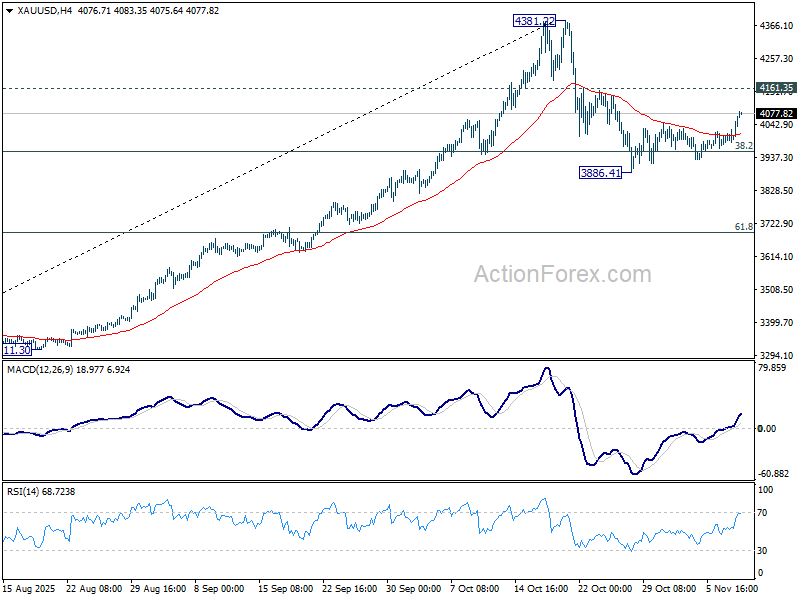

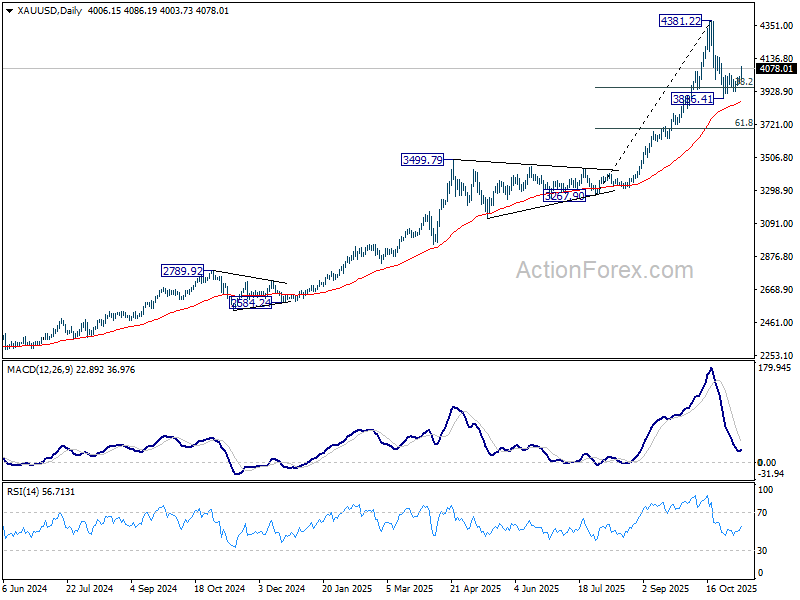

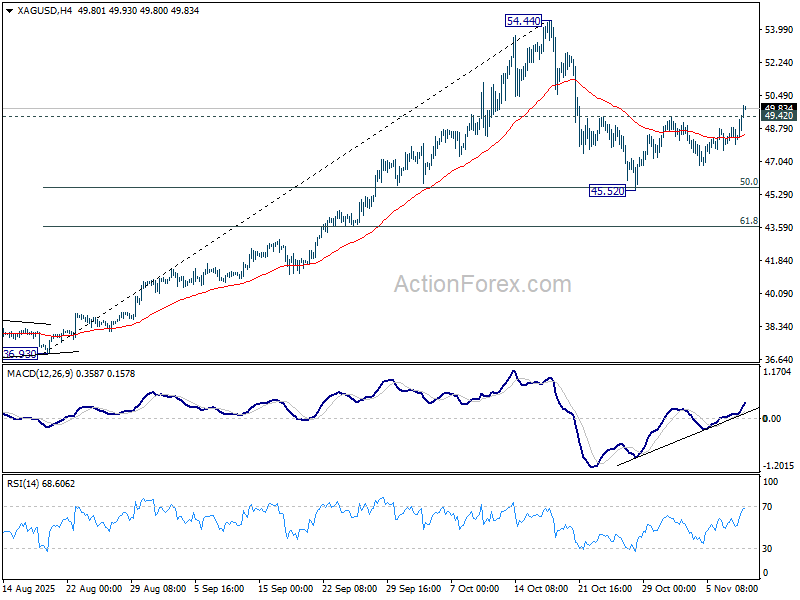

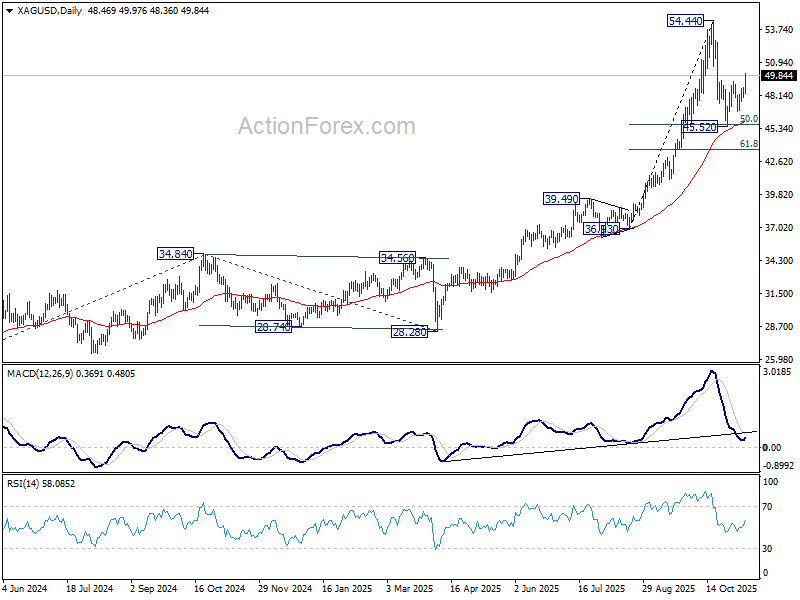

Gold and Silver rebound ahead of 55 D EMAs, first leg of consolidations done.

Gold and Silver advanced sharply today, recovering from recent lows as traders interpreted both technical signals and fresh political developments in Washington as reasons to buy. The rally suggests the first corrective leg from October’s highs may be over, with both metals finding firm support at their moving averages.

The rebound gained a fundamental boost from news that the prolonged U.S. government shutdown could soon end. Reports indicated that centrist Senate Democrats agreed to back a short-term funding bill that would reopen parts of the government through January 30. The agreement, if passed, would restart the flow of federal data—potentially reinforcing market expectations for another Fed rate cut in December.

Renewed rate-cut bets lent support to metals already positioned near key technical floors. Investors also saw the reopening deal as a sign that policy paralysis in Washington may ease, removing one near-term drag on market confidence.

Technically, Gold has broken decisively above its 55 4H EMA, indicating that the pullback from 4,381.22 likely completed at 3,886.41, ahead of 55 D EMA. Decisive break above 4,161.35 resistance would confirm upside momentum toward 4,381.22. However, strong resistance is expected near that level, to bring another fall to extend the consolidation, before the longer-term uptrend resumes.

Silver’s structure shows a similar setup. Its decline from 54.44 seems to have ended at 45.20, ahead of 55 D EMA. Sustained trade above 49.42 resistance would target a retest of 54.44. As with Gold, resistance there should limit gains and set the stage for another short-term retreat—potentially toward 45.52—before the broader bullish trend resumes later.

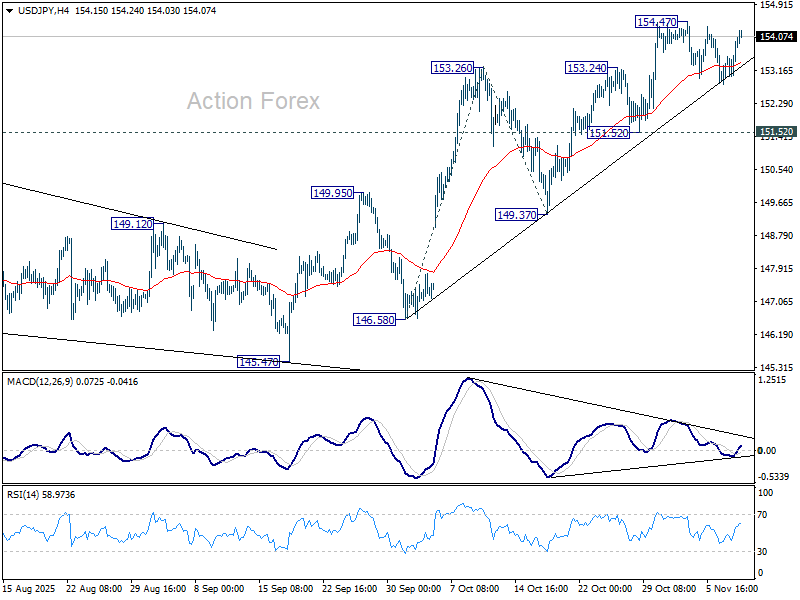

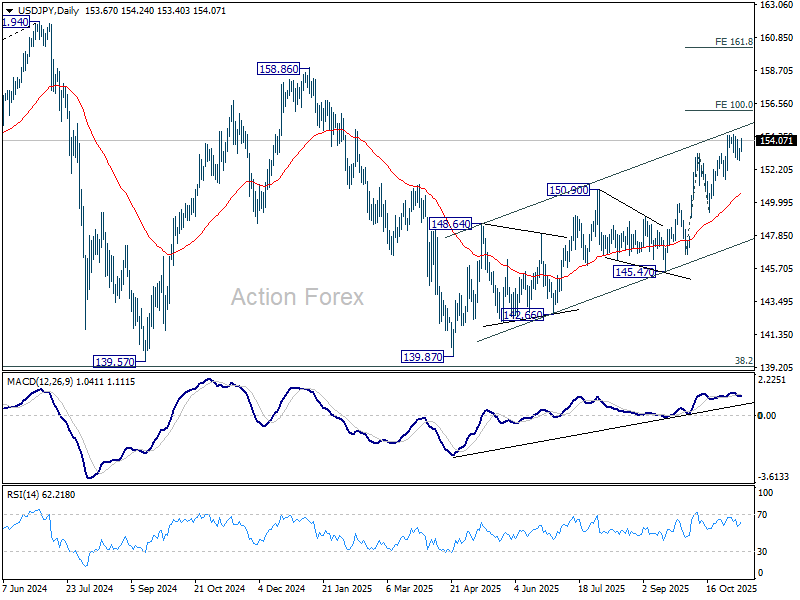

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.97; (P) 153.28; (R1) 153.75; More...

USD/JPY rebounded notably today but stays below 154.47 resistance. Intraday bias remains neutral and more consolidations could still be seen. Further rally is expected as long as 151.52 support holds. Above 154.47 will resume larger rise from 139.87 and target 100% projection of 146.58 to 153.26 from 149.37 at 156.05. Break there will pave the way to 158.85 key structural resistance.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 149.37 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Fed’s Daly: Policy must avoid trading one mistake for another

San Francisco Fed President Mary Daly said the FOMC has appropriately reduced policy rates by a total of 50bps this year as part of a "prudent risk management approach", noting that the adjustments provide “needed insurance” for the labor market while keeping policy “modestly restrictive” to further curb inflation.

In an essay published today, Daly posed the central question now facing the Fed: Will more rate cuts be needed? She argued that while policymakers must remain alert to inflation risks—drawing lessons from the 1970s and the post-pandemic surge—they must also avoid overcorrecting and stifling growth.

“We don’t want to work so hard to not be the 1970s that we cut off the possibility of the 1990s,” she wrote, warning that an excessive focus on inflation history could trade one mistake for another.

Daly emphasized that getting policy right will require “an open mind” and careful evaluation of evidence on both sides of the debate.

Gold and Silver rebound ahead of 55 D EMAs, first leg of consolidations done.

Gold and Silver advanced sharply today, recovering from recent lows as traders interpreted both technical signals and fresh political developments in Washington as reasons to buy. The rally suggests the first corrective leg from October’s highs may be over, with both metals finding firm support at their moving averages.

The rebound gained a fundamental boost from news that the prolonged U.S. government shutdown could soon end. Reports indicated that centrist Senate Democrats agreed to back a short-term funding bill that would reopen parts of the government through January 30. The agreement, if passed, would restart the flow of federal data—potentially reinforcing market expectations for another Fed rate cut in December.

Renewed rate-cut bets lent support to metals already positioned near key technical floors. Investors also saw the reopening deal as a sign that policy paralysis in Washington may ease, removing one near-term drag on market confidence.

Technically, Gold has broken decisively above its 55 4H EMA, indicating that the pullback from 4,381.22 likely completed at 3,886.41, ahead of 55 D EMA. Decisive break above 4,161.35 resistance would confirm upside momentum toward 4,381.22. However, strong resistance is expected near that level, to bring another fall to extend the consolidation, before the longer-term uptrend resumes.

Silver’s structure shows a similar setup. Its decline from 54.44 seems to have ended at 45.20, ahead of 55 D EMA. Sustained trade above 49.42 resistance would target a retest of 54.44. As with Gold, resistance there should limit gains and set the stage for another short-term retreat—potentially toward 45.52—before the broader bullish trend resumes later.

Dollar Plays on Bets

- The US dollar is losing confidence again.

- The Fed doubts that interest rates will be lowered.

- The Bank of Japan intends to continue the cycle.

- The yen is testing the authorities’ resolve.

The US dollar is in a tug-of-war. On the one hand, the Supreme Court is likely to rule that Donald Trump’s tariffs are illegal. This will further undermine confidence in the greenback, as was the case in the first half of the year due to pressure from the White House on the Fed.

On the other hand, according to New York Fed President John Williams, the Fed’s verdict at the last FOMC meeting in 2025 will be the result of a balance of several forces. Inflation in the US is high and shows no signs of slowing down. However, the economy remains stable.

The futures market interpreted this rhetoric as ‘hawkish’ and lowered the chances of a federal funds rate cut in December to 63% from 95% two weeks earlier. At the same time, there is still significant room for further repricing. The EURUSD will likely fall if interest rates are not cut.

Nevertheless, the loss of confidence in the US dollar and the preservation of the euro’s main trump cards allow the main currency pair to look to the future with optimism. The eurozone economy is improving, and the ECB has likely brought its cycle of policy easing to a close. Divergences in GDP growth and monetary policy suggest that the EURUSD uptrend is sustainable.

Meanwhile, speculators have decided to test the Japanese government’s resolve. Despite several bearish signals for USDJPY, the pair has continued to rise. The minutes of the last BoJ meeting showed its readiness to raise the overnight rate in December. It was noted that the conditions for continuing the normalisation cycle had been met. If there are no shocks to the global economy and financial markets, the rate will be raised. Indeed, inflation and wages continue to show no signs of slowing down, despite the introduction of tariffs.

Hints of an overnight rate hike, coupled with falling US stock indices and a deterioration in global risk appetite, should have helped the yen. However, speculators are pushing USDJPY quotes up in the hope of currency intervention by the official Tokyo authorities. A quick reversal could enable traders to make a substantial amount of money.

Good News for Crypto Bargain Hunters

Market Overview

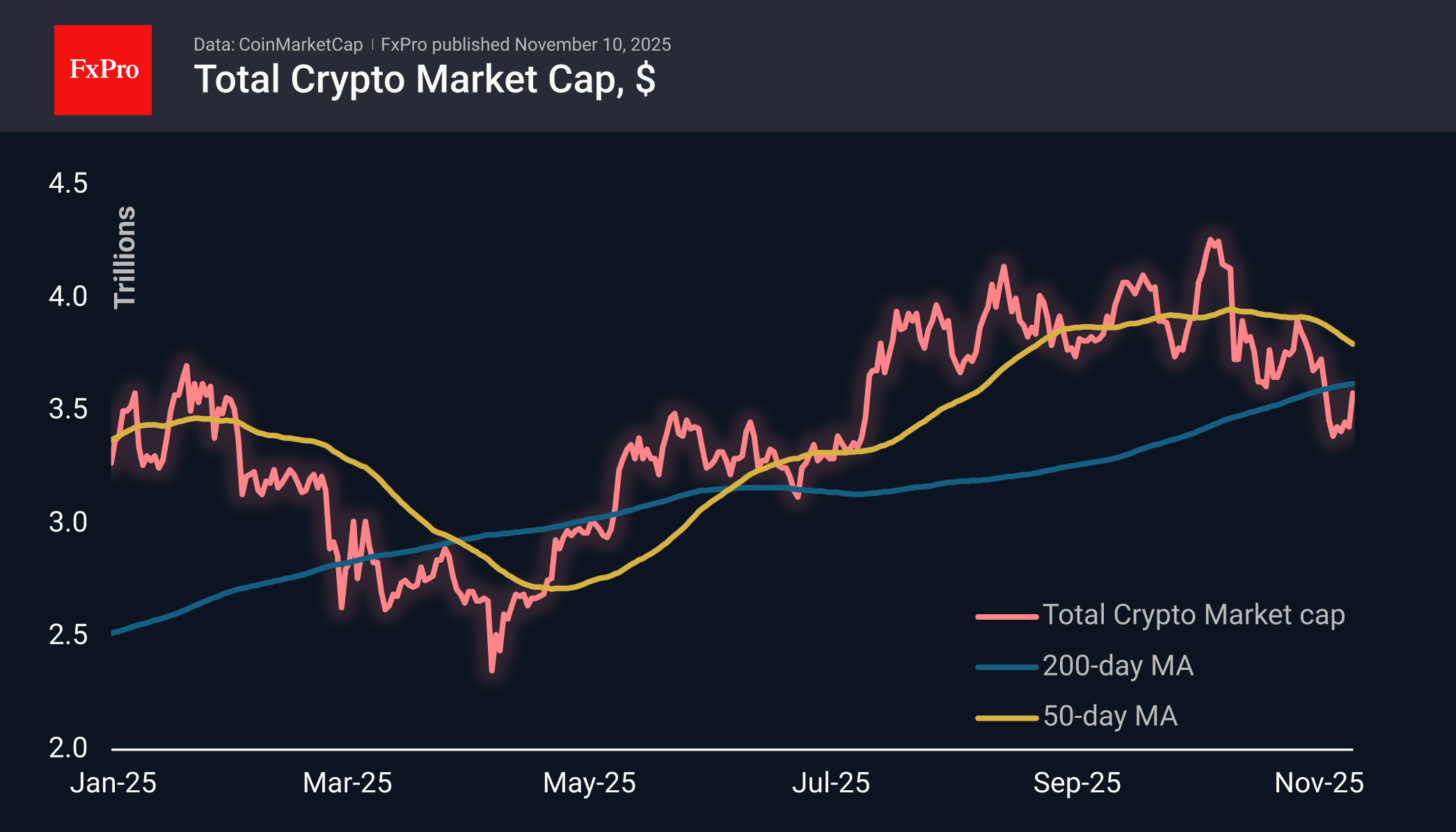

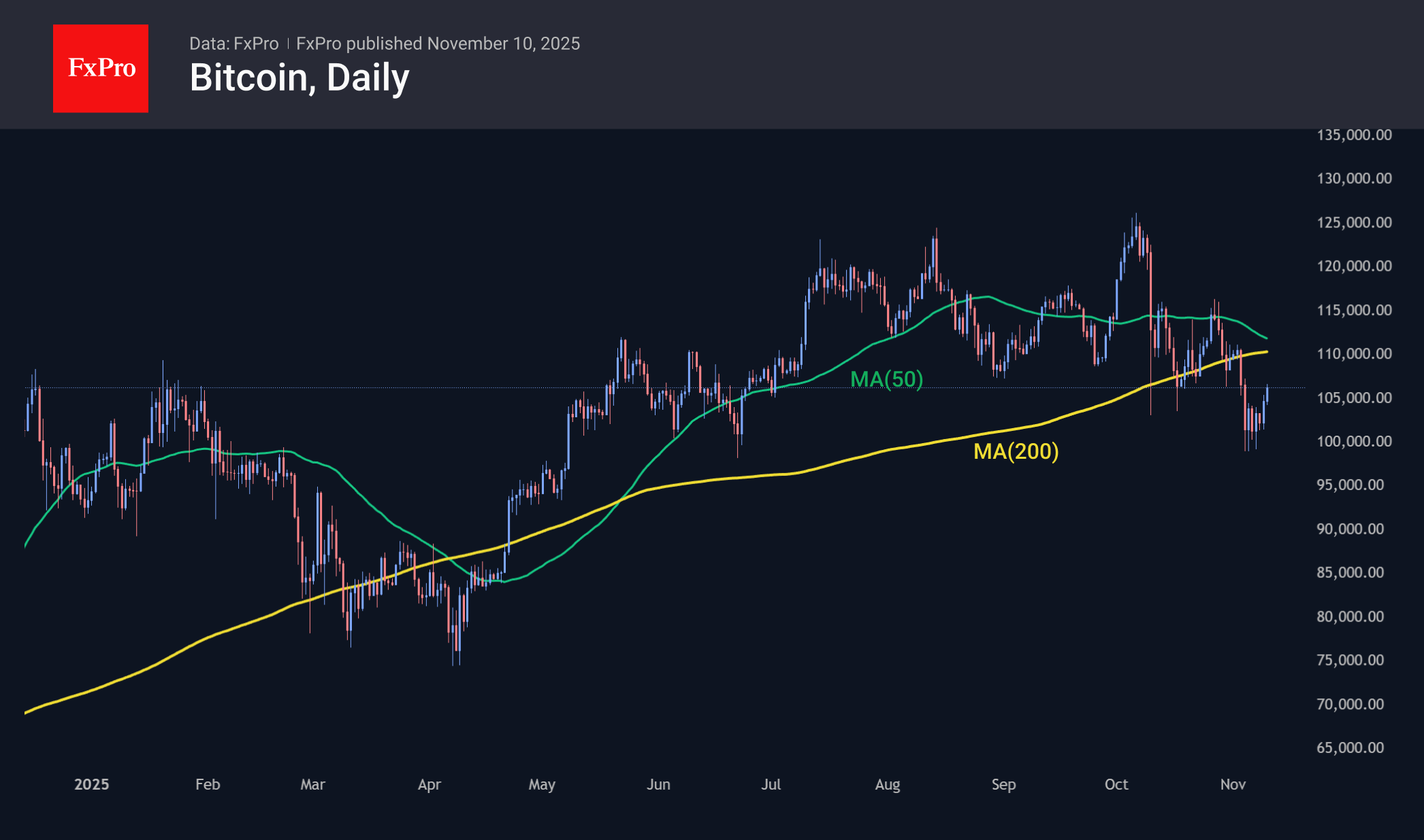

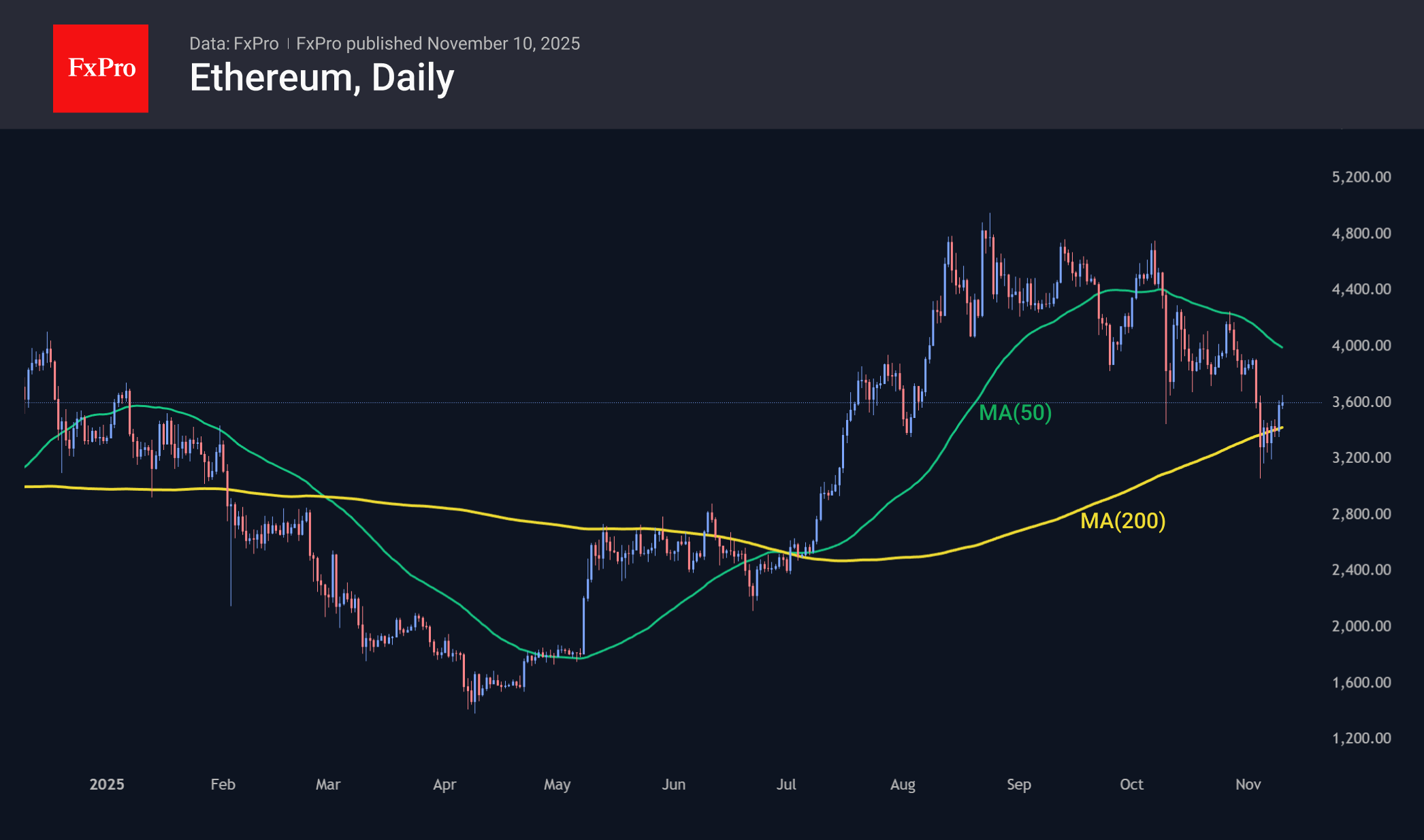

The crypto market jumped 4.5% in the last 24 hours, following reports of progress in ending the US government shutdown and promises by the US president to distribute $2,000 checks to families, with the funds received from tariffs. The positive effect of this news has been amplified by the fact that a more than 20% pullback from the peak has fuelled greed. Among the top coins, Ethereum (+5.8%) and XRP (+8%) are growing steadily, outperforming Bitcoin, which is up 4.5%.

Bitcoin surpassed the $106K mark, breaking out of the $99K–$104K consolidation zone, where it spent most of last week. At the same time, the first cryptocurrency is trading below its 50- and 200-day moving averages. Moreover, a death cross is forming there, as the first of these averages is about to fall below the latter.

The technical picture for Ethereum is more favourable, as the bulls did not allow the coin to consolidate below the 200-day MA and pushed it up on the latest positive news. From current levels near $3,600, the nearest target for buyers appears to be $4,000, which promises to be a significant indicator of market health.

News Background

Following the market crash on October 10-11, whales sold 32,500 BTC, while small investors actively bought on the dips. This is an alarming sign for Bitcoin, as historically, prices tend to follow the direction of whales, according to Santiment.

Bitcoin’s deleveraging phase is ‘largely complete’ after the sell-off. The first cryptocurrency could rise to $170,000 over the next 6-12 months, according to JPMorgan’s forecast.

The ‘sluggish dynamics’ of the crypto market are linked to the rebalancing of hodlers’ portfolios. This may have a negative impact in the short term, but is beneficial in the medium and long term, said Galaxy Digital founder Mike Novogratz.

ARK Invest CEO Cathie Wood said she was forced to revise her long-term forecast for Bitcoin for 2030 from $1.5 million to $1.2 million. She cited the rapid growth of stablecoins, which are displacing BTC among investors in emerging markets.

According to a survey by the Alternative Investment Management Association (AIMA) and PwC, 55% of traditional hedge funds owned cryptocurrencies in 2025. Last year, the figure was 47%.

Ripple denied plans to hold an IPO. The company does not intend to go public in the near future, following the example of several participants in the cryptocurrency industry.

Dollar Index Pulls Back from a Key High

As the Dollar Index (DXY) chart shows, the index is currently trading below its 5 November high, which formed after a false bullish breakout (marked by an arrow) above the 1 August peak — a scenario previously outlined in the post “The Dollar Index Near a Key High.”

According to Trading Economics, trader sentiment at the start of the week is being shaped by expectations of comments from ECB and Federal Reserve officials regarding the outlook for monetary policy.

A statement has already come from Reserve Bank of Australia Deputy Governor Andrew Hauser, who noted that financial conditions in the country are now close to a neutral rate — one that neither stimulates nor restrains economic growth. The Australian dollar strengthened following his remarks.

Technical Analysis of the DXY Chart

The previously drawn ascending channel remains relevant for the Dollar Index, with several important technical features:

→ The channel median has switched its role from support to resistance (as indicated by its colour change from blue to red).

→ The QL line, which divides the lower half of the channel into quarters, is currently acting as support for the DXY.

→ The index has fallen below the psychological level of 100 points.

It appears that the 3.7% rally in the Dollar Index since mid-September has attracted sellers, while late buyers may have been trapped near the top of the recent move.

Additional support may be found near 99.45, where a double-top pattern (A–B) previously formed. However, if this level is breached, the DXY could extend its decline towards the lower boundary of the channel.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Eurozone Sentix falls to -7.4, growth outlook darkens, debt fears persist

Eurozone investor sentiment deteriorated again in November, reinforcing concerns that the bloc’s economy remains mired in stagnation. Sentix Investor Confidence Index fell sharply to -7.4 from -5.4 in October, missing expectations of -3.9. Current Situation Index dropped to -17.5 from -16.0. Expectations slipped to 3.3 from 5.8.

Sentix said there was “little sign of an autumn upturn” and that the Eurozone “continues to languish, with no signs of momentum for the future.” The survey noted that the persistence of such gloomy assessments points to an ongoing process of contraction, with the path to 2026 seemingly “predetermined” as the economy remains unable to break free from its slump.

Still, one faint positive emerged from the report: inflation concerns eased notably. The Sentix inflation barometer rose 9 points to -11, suggesting investors see central banks acknowledging weak growth conditions and possibly adjusting policy accordingly. However, Sentix warned that ballooning government debt remains a structural problem, keeping the fiscal policy barometer deeply negative at -32 and limiting how far refinancing conditions can realistically fall.

Gold Climbs to Two-Week High

On Monday, gold advanced by more than 1% to 4,050 USD per ounce, reaching a fresh two-week high. The rally was fuelled by mounting concerns over the health of the US economy.

A softening US dollar provided further support for the precious metal, enhancing the affordability of dollar-denominated assets for international buyers.

Data released on Friday revealed that the University of Michigan’s consumer sentiment index had fallen to its lowest level in nearly three and a half years. This decline is largely attributed to the ongoing US government shutdown, which has now become the longest in the nation’s history. Investors are closely monitoring the situation as the US Senate moves closer to approving a Democratic-backed proposal to reopen the government.

Amid the economic uncertainty, market expectations for the Federal Reserve’s next move remain divided. The probability of a 25 basis point rate cut in December is currently priced at approximately 67%, unchanged from the end of last week.

Technical Analysis: XAU/USD

H4 Chart:

On the H4 chart, XAU/USD is forming a consolidation range around 3,988 USD. A breakout to the upside is expected to initiate a growth wave towards 4,075 USD, which may then be followed by a decline to 4,020 USD (testing the level from below). A subsequent breakdown from this range could extend the correction towards 3,660 USD, where the downward move is anticipated to conclude. This would potentially set the stage for a new upward wave targeting 4,400 USD. The MACD indicator supports this outlook, with its signal line above zero and pointing upward, suggesting continued near-term bullish momentum.

H1 Chart:

On the H1 chart, the market is also consolidating around 3,988 USD. An upward breakout is likely to propel prices towards 4,075 USD, after which a decline to at least 4,020 USD is expected. The Stochastic oscillator aligns with this view, as its signal line is positioned above 80 and appears poised to reverse downward towards 20, indicating potential for a near-term pullback.

Conclusion

Gold is trading at a two-week high, supported by economic concerns and a weaker US dollar. While the near-term technical structure suggests potential for further gains towards 4,075 USD, a subsequent correction towards 4,020 USD is anticipated. The broader outlook remains constructive, with a deeper corrective move towards 3,660 USD expected to present a buying opportunity ahead of a potential resumption of the broader uptrend.

Gold Hits 2-Week Highs, China CPI Accelerates, Diageo Appoints New CEO and FTSE 100 Consolidates. US Government Shutdown in...

Asia Market Wrap - Nikkei Up 1.2%

Stock prices went up and government bonds (Treasuries) went down because people felt hopeful about a possible deal to end the longest US government shutdown. This good feeling came after a chaotic week where investors worried about whether Artificial Intelligence (AI) company stocks were too expensive.

The major MSCI Asia Pacific Index gained almost 1%, with twice as many stocks rising as falling. Japan's Nikkei stock average also climbed more than 1% on Monday, following the positive feeling from US stock futures because traders hoped the US shutdown would soon be over.

The Nikkei ended the day up 1.26% at $50,911.76.

In Japan, large tech-related companies like Advantest, Tokyo Electron, and SoftBank Group all saw gains. While these big stocks helped push the Nikkei up, a market expert noted they weren't gaining as strongly as they did last month.

However, smaller chip-related stocks surged, showing investors were still very eager for technology shares. For example, Kioxia Holdings jumped over 10%, and Towa rocketed up almost 24% to its daily maximum limit.

Another big mover was Mercari, the flea market app operator, which jumped over 18% after reporting a 70% increase in quarterly profit. On the flip side, Honda Motor fell almost 5% after the automaker sharply cut its yearly profit prediction by 21% on Friday. Its competitor, Toyota Motor, managed to recover from earlier losses and finished the day slightly higher. Overall, on the Tokyo Stock Exchange, a large majority of stocks (76%) went up.

China CPI Surprise

China's consumer prices (the cost of goods and services for people) went up by 0.2% compared to a year ago in October 2025. This was a surprise, as experts expected no change, and it bounced back after prices fell 0.3% the month before. This increase was the first since June and the fastest rise since January.

The cost of things other than food accelerated its climb (from 0.7% to 0.9%), boosted by government programs encouraging people to trade in old items for new ones and more spending during the Golden Week holiday, which both helped domestic buying. Costs continued to increase for things like housing, clothes, healthcare, and education. Also, the cost of transportation fell less steeply than before.

Regarding food, prices still dropped, but it was the smallest drop in three months (down 2.9% versus down 4.4%). Crucially, Core inflation (which ignores volatile food and energy costs) rose by 1.2%, which is the highest level in 20 months. Looking month-to-month, consumer prices also increased by 0.2%, which is the highest increase in three months.

European Session - European Shares Higher, Diageo Appoint New CEO

The FTSE 100 index in Britain is expected to open higher on Monday, with early futures showing a gain of 0.84%. The DAX index was also trading higher, up around 0.5% at the time of writing.

In company news: Diageo, the world's largest spirits company, appointed Dave Lewis (the former head of Tesco) as its new CEO, concluding a long search and bringing in an outsider to lead the company during tough times for the drinks business.

Separately, the mining company Ferrexpo announced that its production and exports have been stopped because recent Russian attacks on Ukraine's energy system damaged the power supply to the miner's operations in a critical area.

Also, the owner of Upper Crust, SSP Group, said that its Chair and director, Mike Clasper, plans to step down after the company's annual meeting in January 2026.

Finally, JTC announced it has accepted the fourth improved offer from the British private equity firm Permira, valuing the company at £2.3 billion (or $3.09 billion).

On the FX front, the value of the US dollar went down on Monday. This happened because investors felt more hopeful after the Senate took steps to potentially reopen the federal government, which overshadowed some recent bad economic news.

The US dollar index dropped slightly, by 0.1%, to 99.643.

Other currencies reacted slightly to this: the euro was a little weaker at 1.1559, and the British pound sterling was also slightly softer at 1.3148.

The offshore Chinese yuan stayed mostly the same against the dollar at 7.1204 during Asian trading.

Meanwhile, the currencies of Australia and New Zealand gained ground: the Australian dollar was up 0.4% at 0.6520, and the New Zealand dollar (kiwi) rose 0.1% to 0.5632.

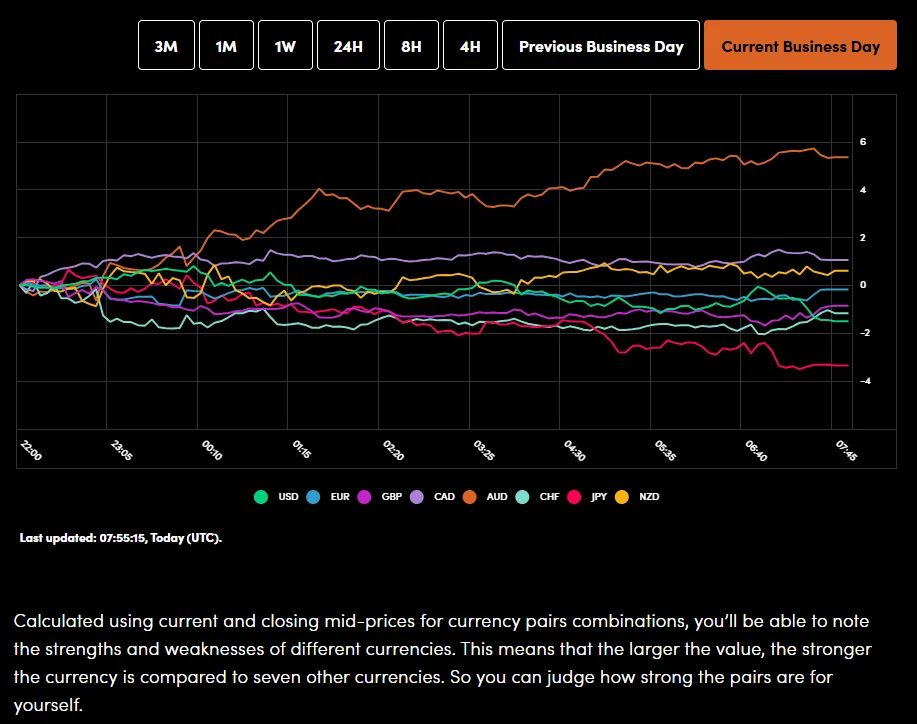

Currency Power Balance

Source: OANDA Labs

Oil prices went up on Monday. This rise was mostly due to the hope that the US government shutdown would end soon. If the government reopens, it's expected to increase demand for oil in the US, which is the world's biggest oil user. This positive news helped overcome worries about the fact that global oil supplies are increasing.

Specifically, Brent crude oil futures rose 45 cents (or 0.71%) to trade at 64.08 per barrel. The price for US West Texas Intermediate (WTI) crude oil also increased by 48 cents (or 0.80%) to reach 60.23 per barrel.

Gold prices jumped to a two-week high on Monday due to a combination of two major factors.

First, the market expected the US Federal Reserve to cut interest rates again in December. Lower interest rates make non-interest-paying assets like gold more appealing compared to interest-bearing investments, such as bonds.

Second, a wave of weak economic reports increased global slowdown worries, pushing investors to buy gold because it's traditionally viewed as a safe asset during times of economic uncertainty.

Following this optimism, the price of spot gold climbed 1.8% to reach 4,070.99/oz, and US gold futures for December delivery similarly rose 1.8% to 4,079.70/oz.

Economic Calendar and Final Thoughts

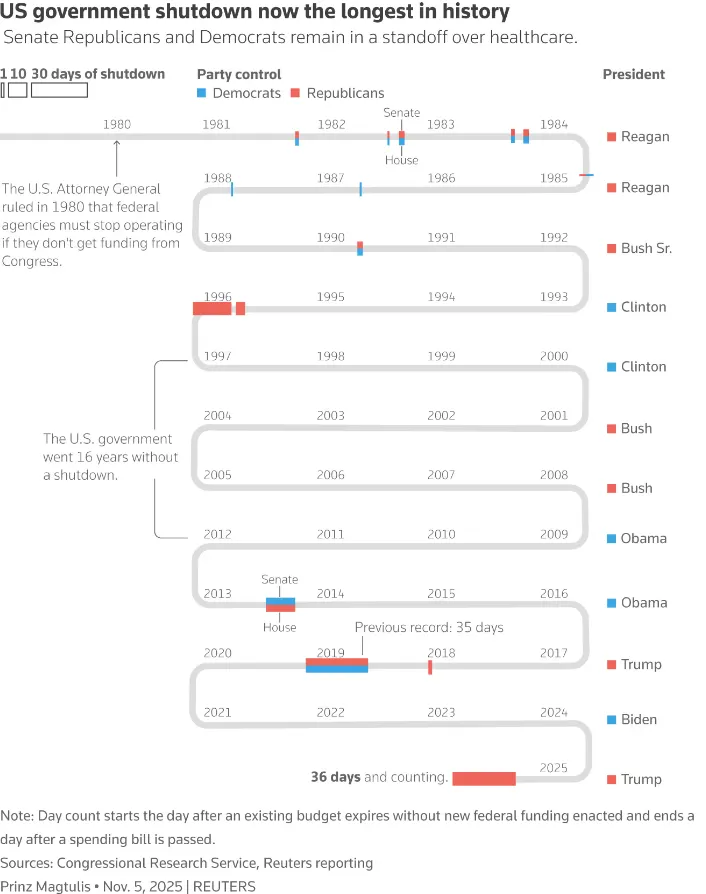

On Sunday, the US Senate took a step toward ending the 40-day federal government shutdown and getting federal workers back to work. This shutdown has stopped paychecks for government employees, slowed down food aid, and caused problems with air travel.

In a key vote, the senators advanced a bill that originally came from the House of Representatives. This bill will be changed to fund the government until January 30th and will also include three complete, long-term spending bills. The shutdown has been severely hurting the US economy: federal workers in areas like airports, law enforcement, and the military haven't been paid, and the central bank has been struggling because the government hasn't been releasing much economic data.

Source: LSEG

Despite all these problems, the overall mood of investors remained hopeful on Monday.

Outside of political news, this week is very quiet for new US economic data. Also, tomorrow is a public holiday, Veterans' Day, in the US The main piece of data that will be released is the NFIB small business optimism index tomorrow. We will also hear from several officials from the Federal Reserve (the Fed) this week.

Currently, the chance that the Fed will cut interest rates by 0.25% in December has dropped to 64%. Since there won't be much new US data to change minds, and because Fed officials usually suggest they should be cautious about cutting rates quickly, that probability may drop even lower, close to 50%.

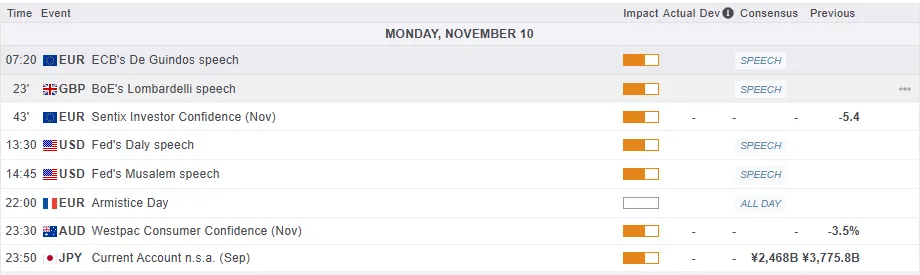

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - FTSE 100 Index

From a technical standpoint, the FTSE 100 is moving lower after market open but remains bullish as the index continues to print higher highs and higher lows.

As things stand the FTSE is trading inside a wedge pattern and a breakout could be the precursor for the next major move.

A wedge breakout could lead to a 220-point rally and needs to be monitored.

For now though, The index is kind of in no mans land.

The period-14 RSI is approaching the 50-neutral. If this level on the RSI holds, this could lead to a retest of the top of the wedge.

Alternatively, a move lower here could bring the lower end of the wedge pattern into focus and potentially the 100-day MA as well which rests at the 9616 handle.

FTSE 100 Index Daily Chart, November 10. 2025

Source: TradingView.com (click to enlarge)

Nasdaq 100 Rebounds as Traders Anticipate End of the US Shutdown

As the chart shows, the Nasdaq 100 index (US Tech 100 mini on FXOpen) has started the week on a positive note amid growing expectations that the longest government shutdown in US history may soon come to an end.

According to Reuters, a bill has been introduced in the Senate proposing amendments to extend government funding until 30 January. The news acted as a bullish catalyst for equity markets. Still, the question remains – is the risk truly behind us?

Technical Analysis of the Nasdaq 100

Analysing the hourly chart of the Nasdaq 100 (US Tech 100 mini on FXOpen) on 4 November, we:

→ Drew an ascending channel;

→ Noted signs of momentum exhaustion, as mentioned in our previous headline.

Since then, price action has evolved as follows:

→ The lower boundary of the channel provided support (1), prompting a brief rebound;

→ The 25,770 level acted as resistance (2) on two occasions, strengthening the bears’ confidence to push for a downside breakout — which ultimately succeeded.

The index’s subsequent movements have now more clearly outlined the formation of a descending channel (shown in red).

From the demand-side perspective:

→ After a false bearish breakout below 24,680 (showing characteristics of a Liquidity Grab pattern), the market staged an aggressive rally from point B;

→ Today’s session opened with a bullish gap, and the price has moved above the red median line.

From the supply-side perspective:

→ The 25,500 level, where sellers gained control during the previous channel breakout, may now act as resistance;

→ If the A→B move is viewed as an impulse, today’s rally appears to be a corrective rebound consistent with Fibonacci proportions — suggesting that downward momentum could resume within the red channel.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.