Sample Category Title

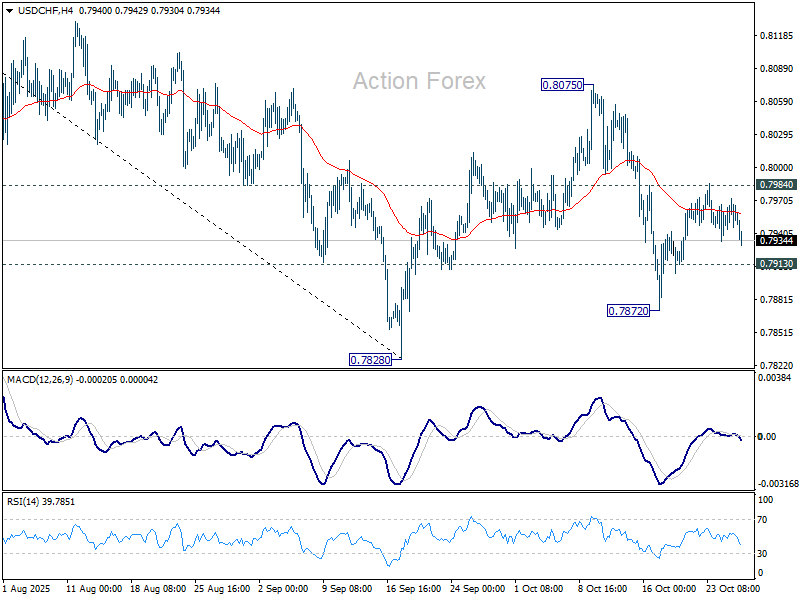

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7942; (P) 0.7957; (R1) 0.7970; More…

USD/CHF dips mildly today but stays in established range. Intraday bias stays neutral and deeper decline is still in favor with 0.7984 resistance intact. On the downside, below 0.7913 will turn bias to the downside for 0.7872 support, and then 0.7828 low. However, firm break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

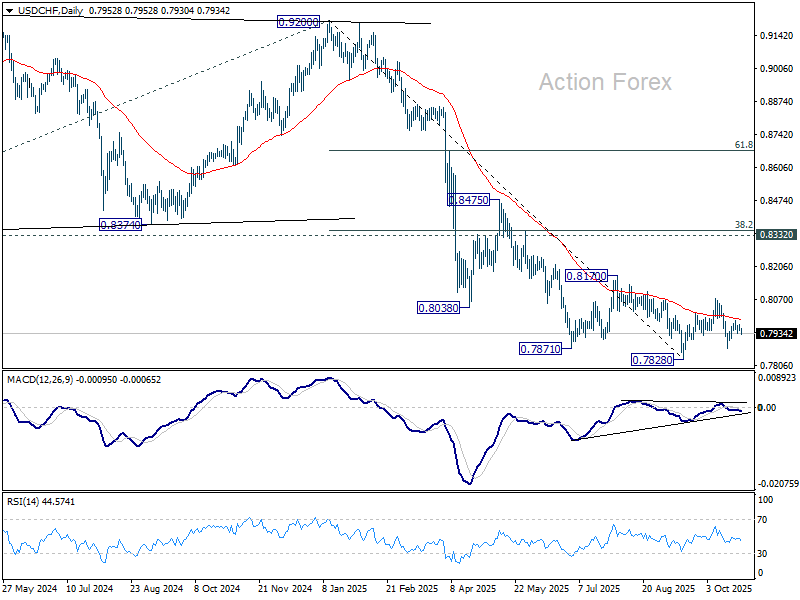

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

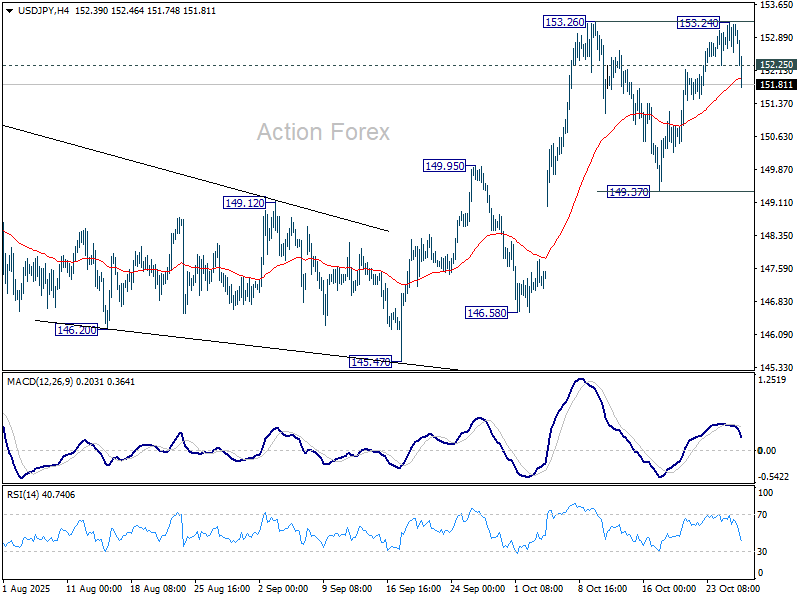

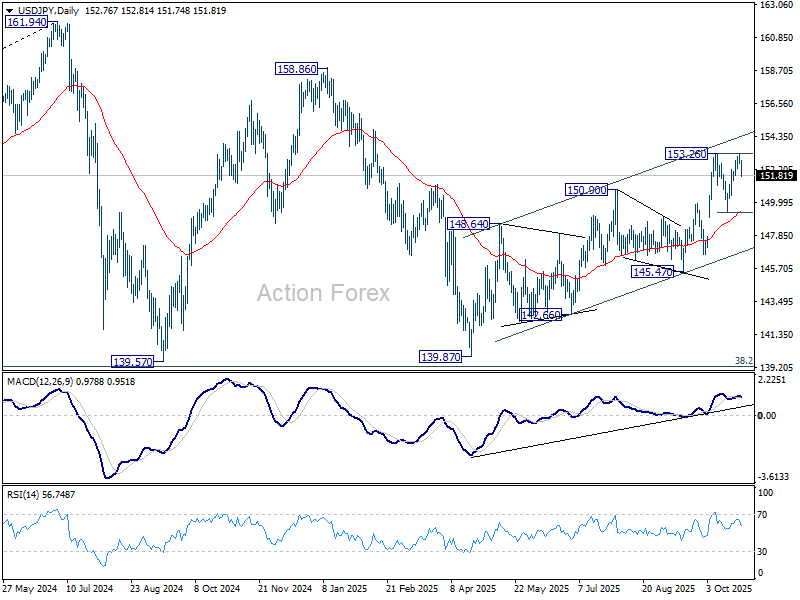

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.54; (P) 152.90; (R1) 153.23; More...

USD/JPY's break of 152.25 minor support and then 55 4H EMA (now at 151.95) suggests that rise from 149.37 has completed after rejection by 153.26 resistance. Fall from 153.24 should be then third leg of the corrective pattern from 153.26. Intraday bias is back on the downside for 149.37 support next. For now, risk will stay mildly on the downside as long as 153.24 holds, in case of recovery.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Smooth Trump–Takaichi Meeting Triggers Profit Taking in Nikkei and Yen Shorts

Yen rebounded notably today while Nikkei 225 cooled from its record highs, as investors took profits following a smooth meeting between U.S. President Donald Trump and Japan’s new Prime Minister Sanae Takaichi. The summit concluded with the signing of two new agreements that reaffirm the deep strategic and economic partnership between the two allies, while offering little in the way of market surprises.

The first accord — described by Trump as ushering in a “new golden age” of U.S.–Japan relations — builds on the series of bilateral deals signed earlier this year, emphasizing joint investments and defense cooperation. The second, more technical agreement focuses on critical minerals, outlining a framework to secure reliable supplies of rare earth elements essential to advanced manufacturing and clean energy production. Both leaders hailed the outcomes as proof of a durable alliance amid shifting regional dynamics.

For markets, however, the tone was less about fresh catalysts and more about consolidation. Japanese equities eased as traders locked in profits after an exceptional run. Yen’s rebound came as part of a broader defensive tilt across currency markets. With major risk events looming, investors shifted toward safe havens such as Yen and Swiss franc. The move also reflected short-term position adjustments after extended weakness in the Japanese currency.

In the U.S., political attention turned back to the Fed after Treasury Secretary Scott Bessent confirmed that the list of candidates to replace Chair Jerome Powell has been narrowed to five. The finalists include Fed Governors Christopher Waller and Michelle Bowman, National Economic Council Director Kevin Hassett, former Fed Governor Kevin Warsh, and BlackRock executive Rick Rieder.

Trump said he expects to announce his choice by the end of the year, even though Powell’s term doesn’t expire until May. The incumbent could remain as a Fed governor until 2028 if he chooses not to depart entirely. Markets took the news calmly, viewing the process as orderly but politically significant for the long-term direction of U.S. monetary policy.

For now, traders are tightening positions ahead of Wednesday’s FOMC decision, where a 25-basis-point cut to 3.75–4.00% is fully priced in. With the Fed staying in a data blackout due to the ongoing government shutdown, investors will focus heavily on Chair Powell’s tone for clues on whether another reduction in December remains on the table.

For the day so far, Yen leads the performance board, followed by Swiss Franc and Sterling. Dollar is the weakest major currency, trailed by Loonie and Aussie. Euro and Kiwi sit in the middle. The configuration reflects a cautious pre-FOMC tone.

In Asia, at the time of writing, Nikkei is down -0.78%. Hong Kong HSI is up 0.08%. China Shanghai SSE is up 0.14%. Singapore Strait Times is up 0.60%. Japan 10-year JGB yield is down -0.025 at 1.649. Overnight, DOW rose 0.71%. S&P 500 rose 1.23%. NASDAQ rose 1.86%. 10-year yield closed flat at 3.997. a

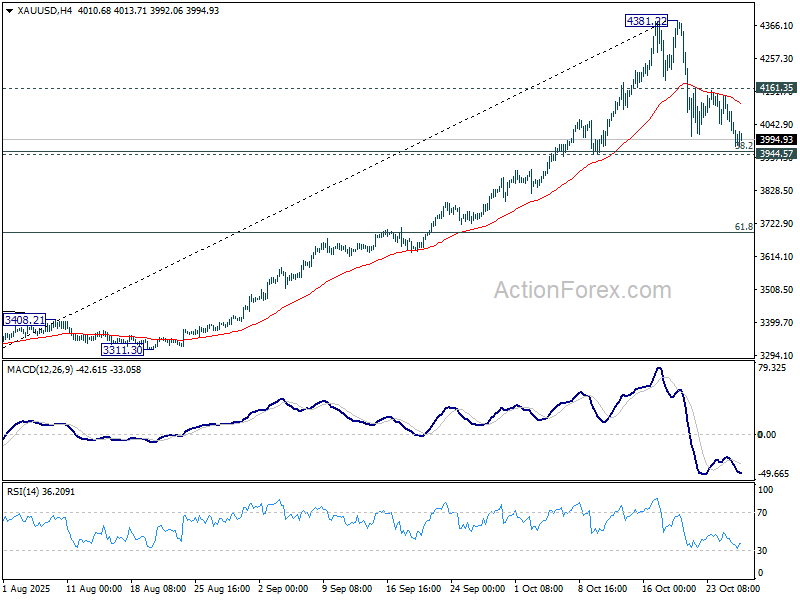

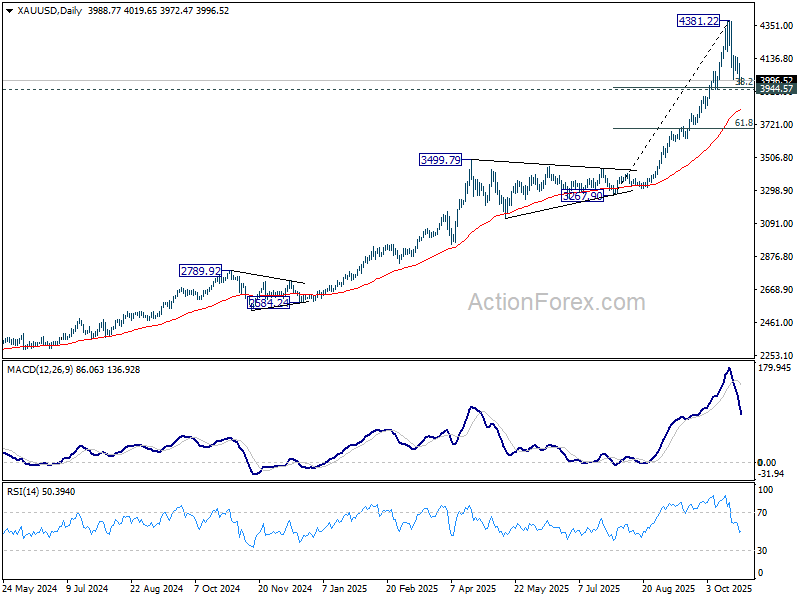

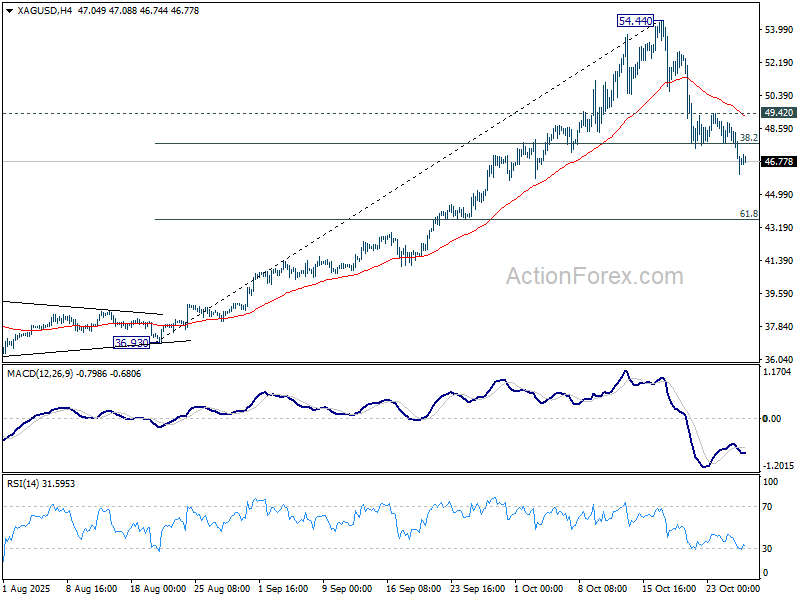

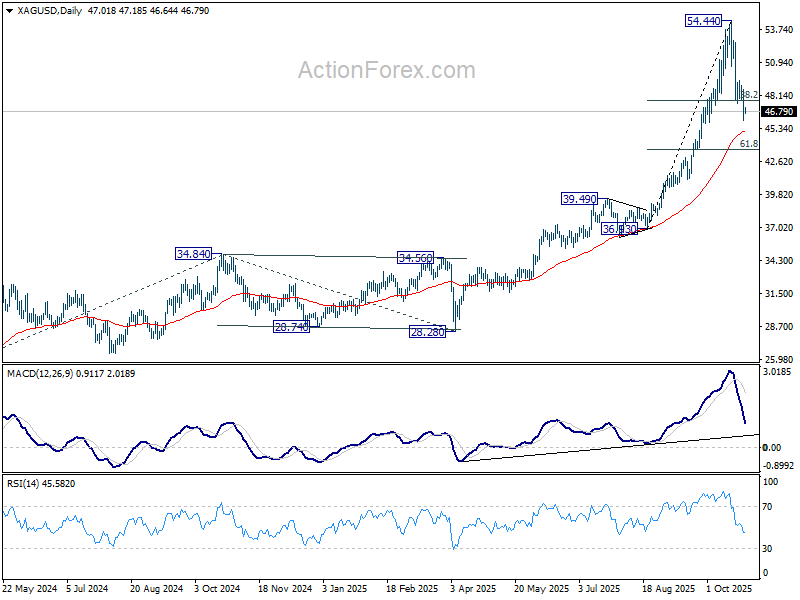

New record possibly delayed to 2026 as Gold and Silver enters extended consolidation phase

Gold and Silver came under renewed pressure at the start of the week. Gold briefly dropped below 4,000 mark before stabilizing, while Silver’s decline gathered pace after breaking key retracement support.

The timing of the selloff coincides with the announcement of a new U.S.–China framework deal designed to avert a major tariff escalation in November. The prospect of easing trade tensions has reduced demand for defensive assets, encouraging investors to rotate into equities and risk currencies. Optimism over the pending Trump–Xi summit has also supported broader market confidence.

Markets now await two pivotal events: Fed’s policy meeting tomorrow and the Trump–Xi summit on Thursday. These will likely set the near-term tone for the broader markets, including precious metals. Price behavior around these events will reveal whether the current pullback gathers further momentum.

So far, technical and macro signals both point to a more extended corrective phase than initially anticipated. Rather than a quick pause before resuming the uptrend, Gold and Silver may need to spend the rest of the year to form a base, laying the groundwork for a new leg higher in 2026.

In Gold’s case, the decline still fits within a corrective structure to the rally from 3,267.90. The metal remains above 3,944.57 cluster support (38.2% retracement of 3267.90 to 4381.22 at 3955.93). A rebound from current level and break of 4,161.35 resistance would suggest the pullback from 4,381.22 is complete, targeting a retest of the record high. However, strong resistance is likely to cap gains near the previous peak, keeping Gold confined to a range between roughly 3,944 and 4,381.

However, decisive break below 3,944.57 would bring deeper correction to 55 D EMA (now at 3,818.40) where stronger demand should emerge to form a base.

Silver’s decline has been more pronounced. The metal has already violated 38.2% retracement of 36.93 to 54.44 at 47.75. Still, it remains a correction of the rise from 36.93, rather than a larger one. A drop toward 55 D EMA (now at 45.16) is likely, but solid support is expected there. A rebound through 49.42 would mark the end of this corrective leg and bring stronger rise to retest 54.44.

However, sustained weakness below 55 Day EMA would imply Silver has entered a larger corrective phase to the rise from 28.28.

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.54; (P) 152.90; (R1) 153.23; More...

USD/JPY's break of 152.25 minor support and then 55 4H EMA (now at 151.95) suggests that rise from 149.37 has completed after rejection by 153.26 resistance. Fall from 153.24 should be then third leg of the corrective pattern from 153.26. Intraday bias is back on the downside for 149.37 support next. For now, risk will stay mildly on the downside as long as 153.24 holds, in case of recovery.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

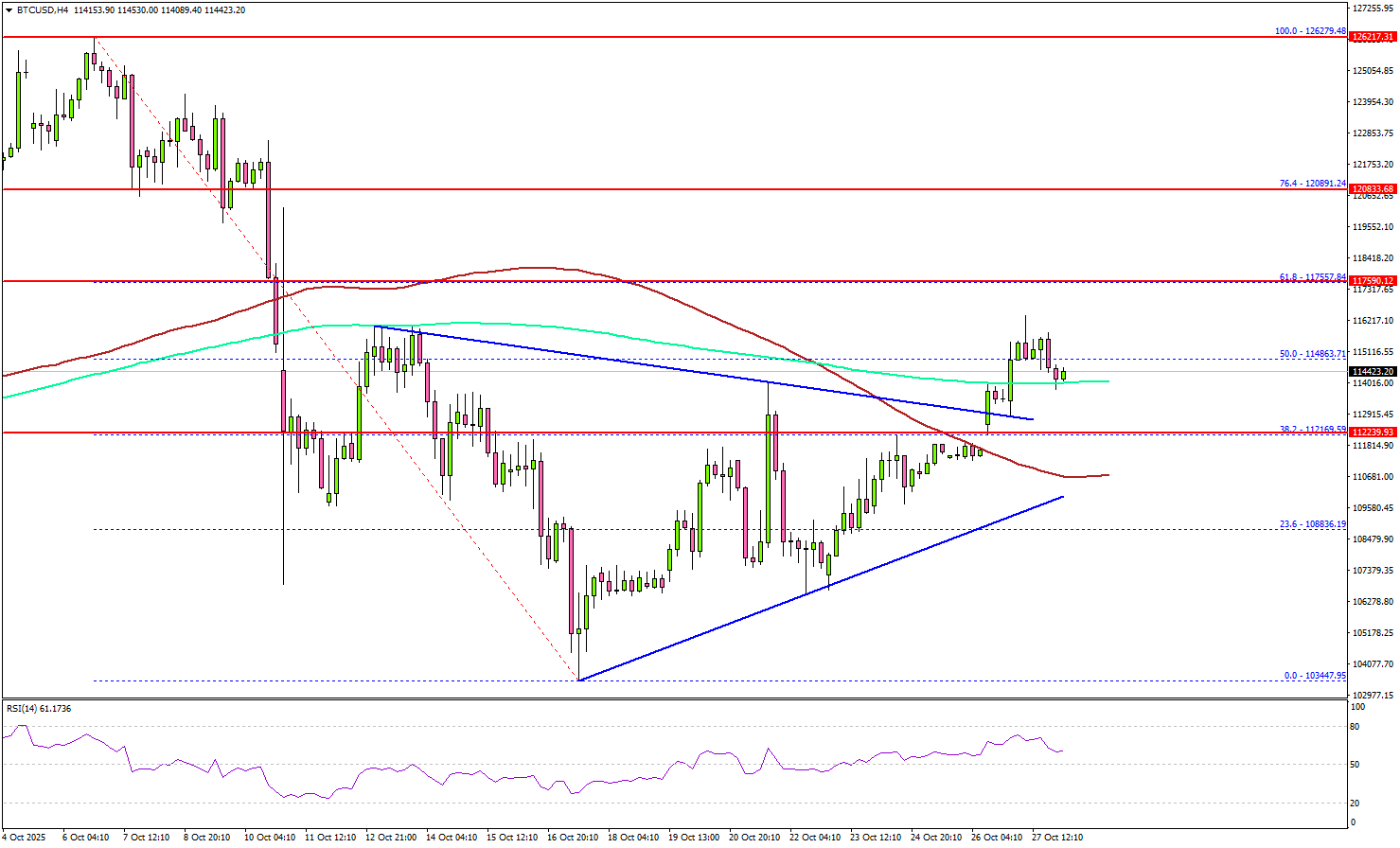

Bitcoin Jumps, Breakout Above Resistance Reinforces Bullish Momentum

Key Highlights

- Bitcoin started a fresh surge above $113,000 and $114,000.

- BTC/USD cleared a key contracting triangle with resistance at $112,900 on the 4-hour chart.

- Ethereum also started a decent increase above $4,000.

- XRP price is back above $2.420 but faces hurdles near $2.6850.

Bitcoin Price Technical Analysis

Bitcoin price found support near $103,500 and started a fresh increase against the US Dollar. BTC climbed above $108,000 and $110,000 to enter a positive zone.

Looking at the 4-hour chart, the price surpassed the 50% Fib retracement level of the downward move from the $126,279 swing high to the $103,447 low. During the increase, the price broke a key contracting triangle with resistance at $112,900.

BTC settled above $113,000, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). If the price extends gains, it could face resistance at $116,500.

The main hurdle is now forming near $117,550 and the 61.8% Fib retracement level of the downward move from the $126,279 swing high to the $103,447 low. A successful close above $117,550 might start another steady increase. In the stated case, the price may perhaps rise toward the $118,800 level. Any more gains might call for a test of $120,000.

Immediate support sits at $112,200. A downside break below $112,200 might start another decline. The next major support is $111,500. Any more losses might call for an extended decline toward the $108,800 support zone.

Looking at Ethereum, the price was able to follow Bitcoin and climbed above the $4,000 resistance region.

Today’s Key Economic Releases

- US House Pricing Index for August 2025 (MoM) - Forecast +0.1%, versus -0.1% previous.

- S&P/Case-Shiller Home Price Indices for August 2025 (YoY) - Forecast +1.9%, versus +1.8% previous.

New record possibly delayed to 2026 as Gold and Silver enters extended consolidation phase

Gold and Silver came under renewed pressure at the start of the week. Gold briefly dropped below 4,000 mark before stabilizing, while Silver’s decline gathered pace after breaking key retracement support.

The timing of the selloff coincides with the announcement of a new U.S.–China framework deal designed to avert a major tariff escalation in November. The prospect of easing trade tensions has reduced demand for defensive assets, encouraging investors to rotate into equities and risk currencies. Optimism over the pending Trump–Xi summit has also supported broader market confidence.

Markets now await two pivotal events: Fed’s policy meeting tomorrow and the Trump–Xi summit on Thursday. These will likely set the near-term tone for the broader markets, including precious metals. Price behavior around these events will reveal whether the current pullback gathers further momentum.

So far, technical and macro signals both point to a more extended corrective phase than initially anticipated. Rather than a quick pause before resuming the uptrend, Gold and Silver may need to spend the rest of the year to form a base, laying the groundwork for a new leg higher in 2026.

In Gold’s case, the decline still fits within a corrective structure to the rally from 3,267.90. The metal remains above 3,944.57 cluster support (38.2% retracement of 3267.90 to 4381.22 at 3955.93). A rebound from current level and break of 4,161.35 resistance would suggest the pullback from 4,381.22 is complete, targeting a retest of the record high. However, strong resistance is likely to cap gains near the previous peak, keeping Gold confined to a range between roughly 3,944 and 4,381.

However, decisive break below 3,944.57 would bring deeper correction to 55 D EMA (now at 3,818.40) where stronger demand should emerge to form a base.

Silver’s decline has been more pronounced. The metal has already violated 38.2% retracement of 36.93 to 54.44 at 47.75. Still, it remains a correction of the rise from 36.93, rather than a larger one. A drop toward 55 D EMA (now at 45.16) is likely, but solid support is expected there. A rebound through 49.42 would mark the end of this corrective leg and bring stronger rise to retest 54.44.

However, sustained weakness below 55 Day EMA would imply Silver has entered a larger corrective phase to the rise from 28.28.

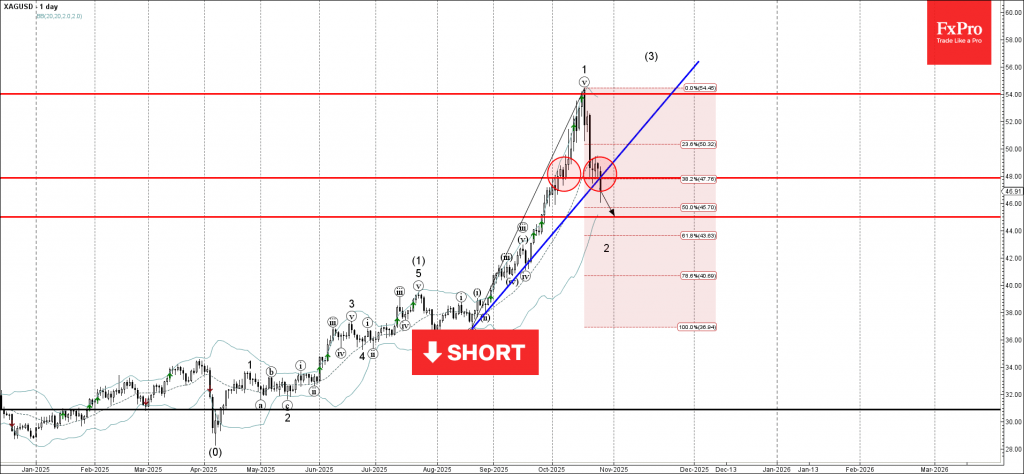

Silver Wave Analysis

Silver: ⬇️ Sell

- Silver broke support zone

- Likely to fall to support level 45.00

Silver recently broke the support zone between the support trendline from August, support level 48.00 and the 38.2% Fibonacci correction of the upward impulse from August.

The breakout of this support zone accelerated the active minor correction 2 of the extended impulse wave (3) from August.

Silver can be expected to fall further toward the next support level 45.00, the breakout of which can lead to further losses toward the round support level 40.00.

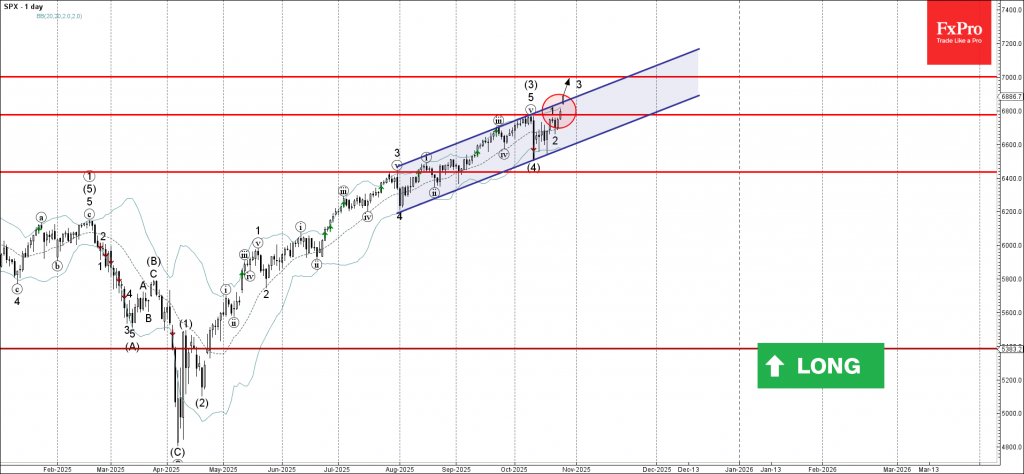

S&P 500 Wave Analysis

S&P 500 index: ⬆️ Buy

- S&P 500 broke resistance level 6800.00

- Likely to rise to resistance level 7000.00

S&P 500 index opened today with the upward gap which broke the key resistance level 6800.00 (which stopped the previous impulse wave (3) at the start of October, as can be seen from the daily S&P 500 index chart below).

The breakout of the resistance level 6800.00 accelerated the active minor impulse wave 3 of the medium-term impulse sequence (5) from the start of this month.

Having just broken out of the daily up channel from August, S&P 500 index can be expected to rise to the next round resistance level 7000.00, target price for the completion of the active impulse wave 3.

Sunset Market Commentary

Markets

Friday’s risk rally continued going into the start of a busy week. US and Chinese negotiators have agreed on key matters during trade talks in the sidelines of the ASEAN leaders summit in Malaysia. Some of the sticky points that have been resolved include a resumption of Chinese purchases of US soybeans and a delay (allegedly by one year) of the tighter Chinese export controls on rare earths. In return the US shelves the threat of an additional 100% tariff on Chinese imports. They pave the way for an extension to the trade truce when Trump and Xi meet later this week. Additional positive headlines came from Brazil, which according to president Lula is closing in on having a definitive resolution to the trade conflict. All this follows Indian newspaper Mint mid-last week reporting that the world’s 4th largest economy is closing in on a deal that would cut levies to 15% from the current 50%. The constructive trade vibes hurl US stock markets to yet another record high, unhindered by the additional 10% Canadian levy Trump introduced. The Nasdaq outperforms by rising 1.3%. European stocks add up to 0.5% (EuroStoxx50). The French CAC40 lags peers, perhaps over renewed political concerns. The Socialist Party will decide by the end of the week whether or not to topple Lecornu II. It ties the PM and his government’s fate to a wealth tax to be introduced in the 2026 budget. It would be another major win for the Socialists, after securing a suspension to the pension reform until after the presidential elections in 2027. It underscores the difficulty of addressing a spiraling debt-deficit problem in the fractured French parliament where every party can basically act as kingmaker. Moody’s last Friday downgraded the rating outlook to negative from stable for that exact reason. The OAT/swapspread (80 bps) holds steady today and remains the euro area’s highest (topping Italy). Core bond yields in general continue to bottom out, jumpstarted by Friday’s PMIs. Doing so marks an end to the diverging message brought by equity and FI markets since the beginning of October. Treasuries underperform with yields adding up to 2.7 bps in a bear flattener. European yields gapped higher at the open but currently trade more or less flat. FX markets show little direction. Looming key events such as the Fed and ECB policy meeting could act as a paralyzing force, though we doubt they’ll produce tidal shifts in the market. EUR/USD treads water around 1.164. EUR/GBP is similarly going nowhere around 0.873. The NZD and especially AUD as important trade partners to China are the key beneficiaries from the US/Sino trade thaw. AUD/USD rises to 0.655. Gold and silver drop materially with the former at risk of losing support at 4k.

News & Views

The Confederation of British Industry’s October retail sales report shows that the sector remains in a prolonged downturn with annual sales volumes falling for a thirteenth consecutive month. Persistent uncertainty ahead of the Autumn Budget is deepening the strain on retailers and other distribution firms that are still grappling with the effects of last year’s fiscal decisions. Weak demand conditions were also reflected in further sales declines across wholesaling and motor trades given overall poor consumer confidence. CBI data suggested there was a small increase in online retail sales volumes but would contract next month. The CBI measure comparing sales with a year earlier improved marginally in October, from -29 to -27 but remains firmly negative. The gauge for expected sales for the month ahead slipped from -36 to -39.

Slovak debt management agency Ardal today announced a new 12-yr EUR benchmark deal which will follow in the near future, subject to market conditions. Ardal already did one other new (15-yr) benchmark this year in February raising €3bn. They raised another combined €6.7bn via multiple regular auctions and retail bond offerings. This year’s funding need consists of €6.55bn redemptions and an expected state budget deficit of €6.7bn. Next year’s outlook suggest a somewhat lower gross bond issuance (€10bn) with redemptions (€4.9bn) and the expected budget deficit (€5.1bn) both being lower. Slovakia has an A+ credit rating at S&P (negative outlook, confirmed last Friday) and A- and the equivalent A3 at Fitch and Moody’s (both stable outlook).

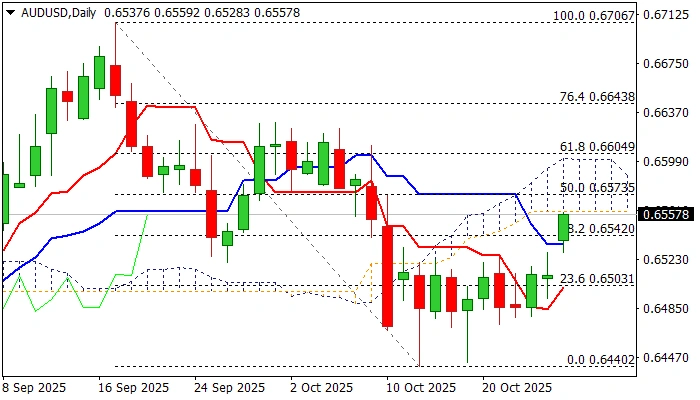

AUD/USD: Fresh Risk Appetite Lifts Australian Dollar to Two-Week High

AUDUSD opened with a gap higher and hit two-week high in almost 1% advance in early Monday trading.

Fresh risk appetite dominated in the market at the start of the week, as growing optimism of US-China trade deal, fueled demand for riskier assets and inflated risk-sensitive Aussie dollar.

Softer US dollar on cooler than expected US inflation in September (report released on Friday) also contributes to fresh strength.

Monday’s acceleration pressures significant resistance at 0.6560 (base of daily Ichimoku cloud, spanned between 0.6560 and 0.6600) where increased headwinds could be expected, as daily studies are mixed (north-heading 14-d momentum is still in the negative territory / stochastic is overbought against rising RSI that moved above 50 and MA’s turning to bullish setup).

Bullish scenario requires penetration of daily cloud and rise above nearby 0.6573 Fibo barrier (50% retracement of 0.6706/0.6440) to strengthen near-term structure and open way for attack at next key barriers at 0.6600 zone (cloud top / Fibo 61.8%).

Conversely, failure at cloud base may keep an action on hold, but biased higher while holding above 100DMA (0.6533).

Investors await Fed’s rate decision, due on Wednesday (0.25% rate cut is widely expected, with focus on speech of Fed chief Powell, expected to provide signals of central bank’s next steps, as well as release of US PCE Index on Friday, Fed’s preferred inflation gauge).

Res: 0.6560; 0.6573; 0.6600; 0.6629.

Sup: 0.6542; 0.6533; 0.6500; 0.6472.