Sample Category Title

Weekly Focus – A Cut in the Dark

The US government remains in shutdown and hence, we continue to have very little data on the state of the economy. Nevertheless, there is a widespread expectation, which we share, that the Fed will deliver a rate cut next week. In the absence of new information, the Fed will emphasise the weak job growth in August which has not been contradicted by the indicators that we do have about developments since. We will receive a much-delayed inflation number for September as well as PMI data for October today (after the time of writing), which could of course influence the decision, but we think the bar is high for the Fed to change its mind on the rate cut. Lowering the Fed Funds target to 4% will still mean that monetary policy is restrictive. The Fed might discuss slowing or ending the reduction of its bond holdings, not least given recent volatility in the repo market. It could also be interesting to hear how the Fed sees the situation for US regional banks.

The ECB will also deliver a rate decision in the coming week, and we see no reason to expect a different message than the "we're in a good place" in terms of interest rates and the economy that ECB president Christine Largarde highlighted at the September meeting. Since then, we have seen an increase in headline inflation to 2.2% y/y, but that is driven by base effects and should not affect the outlook. Inflation is expected to head down as wage growth slows and as a consequence of the stronger EUR. October PMI data for the euro area was stronger than expected driven by the German service sector, and markets are pricing only a small probability of a rate cut over the coming year, which we think that Lagarde is unlikely to push against.

Even as the ECB is finalising its monetary policy statement on Thursday, we will get data on GDP growth in Q3 and inflation in Germany and Spain in October, before the total euro area number Friday. On GDP, we estimate growth of 0.1% q/q as in Q2, after the strong Q1 driven not least by export to the US ahead of the tariff hikes. However, the October PMIs show a promising start to Q4 in terms of growth. On inflation, we expect it to slow to 2.1% y/y with a chance that it could be lower, and we also forecast core inflation to decline from 2.4% to 2.3%.

Trade tensions between China and the US have increased in recent weeks, with China increasing export controls on rare earth minerals and Donald Trump threatening 100% tariff on imports from China from 1 November. The US and Chinese presidents are set to meet next week, and we see a good chance that they can reach a deal. If they do not, there could be a risk-off market reaction. China outlined its next five-year plan this week and re-emphasised the need to boost domestic consumer spending but did not provide a concrete target or new means to reach that.

In Japan, Sanae Takaichi has formed a minority government that is likely to push for easing of fiscal policy, although it is not clear how much it can achieve. Takaichi is opposed to tightening of monetary policy which is one reason why we expect the Bank of Japan to keep rates unchanged at is meeting Thursday despite inflation rising in September and having exceeded the target for 42 months now.

ECB Preview – In a Good Place But Ready to Act

- We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 30 October in line with consensus and market pricing.

- Data has been close to expectations since the September meeting, and we therefore expect no shift in communication on the assessment of the economic outlook nor in the 'meeting-by-meeting' approach. We will pay close attention to any new details on the 'good place' assessment and what could change it.

- We expect a limited market reaction during the press conference.

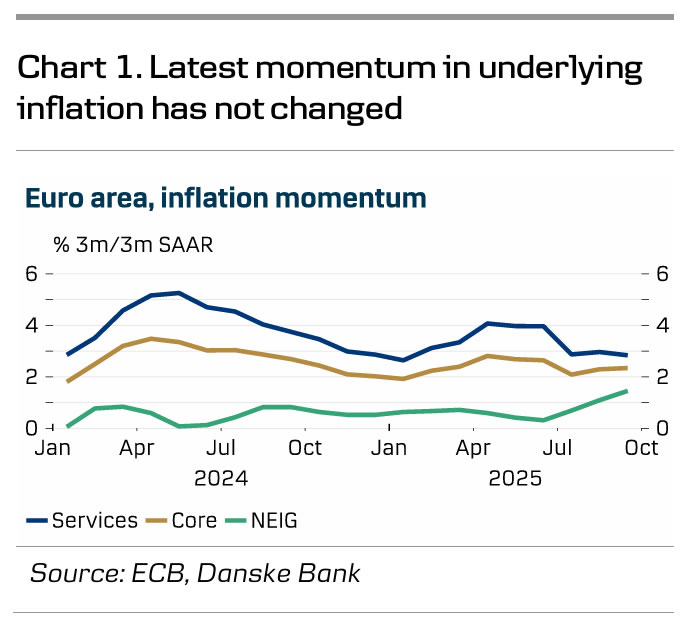

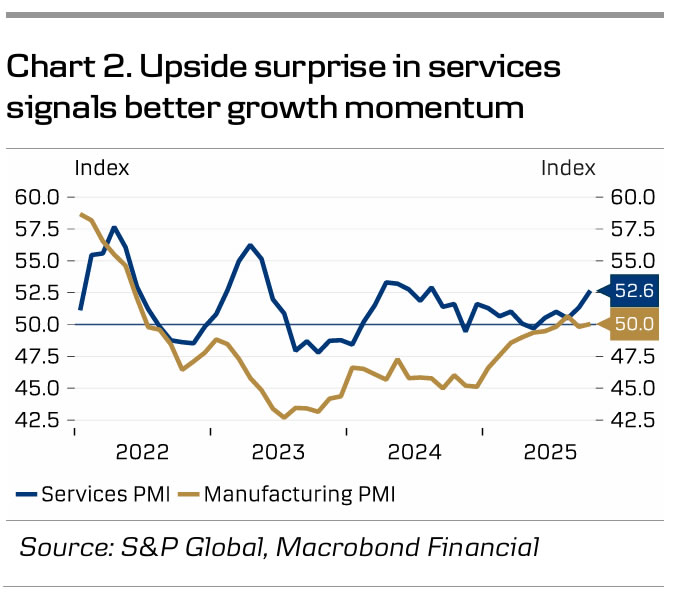

We expect the ECB to leave the deposit rate unchanged at 2.0% at the meeting on 30 October, in line with market pricing and consensus. Macro data since the September meeting has been close to expectations, suggesting the outlook has not changed. The September PMIs rose as expected while October PMIs surprised on the upside due to a strong increase in the services sector (see chart 2). PMIs suggest a slightly better growth momentum than the ECB staff projections, which forecasted 0.0% q/q GDP growth in Q3 and 0.2% q/q in Q4. Inflation ticked up to 2.2% y/y in September due to base effects while the momentum of underlying inflation was highly similar to that in recent months (see chart 1). September inflation thus aligned with staff projections for Q3 in both core and headline. Hence, we expect Lagarde to repeat the 'meeting-by-meeting' and 'data-dependent' approach.

Governing Council members continue to state that the ECB is 'in a good place', but there is growing divergence among members regarding the inflation outlook. This was evident in the minutes from the September meeting, where several members highlighted downside risks to inflation and expressed concerns regarding the euro's strength and households' persistently high savings rates. On the other hand, some members emphasised the potential inflationary effects of expansionary fiscal policies in the region and rising food inflation. We still see a clear majority of GC members that do not expect more cuts despite inflation projections being below target in both 2026 and 2027, but we are also hearing more dovish comments from e.g. Villeroy saying that a rate cut is more likely than a hike. Yet, with medium-term inflation expectations anchored close to 2%, decent October PMIs, and private consensus inflation expectations at 2% for 2027 we think the bar for another rate cut is high. This is also supported by the ECB seeing growth risks as balanced after having highlighted downside risks to growth since September 2023. Still, we do see a risk that the sentiment in the GC could change after the December staff projections if they show inflation below target on the full forecast horizon, including 2028.

Markets are currently pricing 2bp worth of cuts in 2025 and 10bp in 2026, leaving a 50% probability of one more rate cut. This chance of a cut has thus been lowered compared to before the September meeting when markets were pricing 8bp for 2025 and 8bp for 2026. While we see upside risks to current market pricing as we expect the ECB to remain on hold throughout 2026, we have recently taken profit on our payer positions in the short end of the EUR-swap curve as we see the risks as more balanced. At the press conference we will pay attention to communication about details on the 'good place' assessment by Lagarde and what potentially could change that view. However, we expect Lagarde to reiterate the place assessment but say that it is not fixed and that the ECB is ready to act.

Sunset Market Commentary

Markets

Euro area PMIs for October were on tap and came in to the strong side of expectations. Economy-wide activity picked up to 52.2 from 51.2, a 17-month high, driven by the services sector (52.6 from 51.3) on a steeper increase in new orders and employment. Germany in particular printed a sharp increase in services activity (54.5 from 51.5). Manufacturing output quickened to a 2-month high of 51.1 and with order books stabilizing after September’s drop it helped the total manufacturing index climb out of contraction territory. Exports remains a weak point but backlogs stabilized, thereby ending a period of depleting stretching back to April 2023. Input cost inflation eased again but manufacturers increased their selling (output) prices for the first time in six months, joining the services sector. Firms remain cautious on the outlook though. France stands out in virtually every (sub)series, and not in a good way. The PMI owners say economic growth in the euro area is currently much weaker than it could have been because of the French drama. Either way, the overall takeaway is an across-the-board solid beat. It lifted European yields to their highest levels in two weeks (+/- 5 bps), both at the front and long end of the curve before dropping from their intraday highs in the wake of US inflation numbers printing a tad below expectations. Headline US CPI rose by 0.3% m/m, core by 0.2%, resulting in a 3% annual reading. Energy was a main contributor (+1.5% m/m). Apparel & household furnishings, one of the categories watched for tariff-related inflationary effects, rose 0.7% and 0.5% respectively. The market reaction is telling: the 2-yr yield dropped up to 7 bps before paring most of the losses. Money markets at some point were even mulling the possibility of the Fed going big at one of the remaining two meetings this year. That seems farfetched based on this sole economic data point but its revealing of the markets’ mindset. Longer term US bond yields ease 1-2.5 bps. Enter the PMIs to wipe out all of the remaining CPI-driven losses. The US version followed the European and UK example by coming in better than expected. The services gauge picked up to 55.2, the manufacturing series to 52.2. The overall PMI (54.8) is this year’s second-highest reading. The strong start to Q4 (2.5% annualized growth) comes with weaker confidence for the year ahead though. Input cost inflation rose but output prices didn’t follow amid firms competing for sales. The flurry of eco data offers no clear guidance for EUR/USD, with the pair simply holding steady around 1.162.

Today’s PMIs and US inflation were mere appetizers going into next week’s main dish. The ongoing US government shutdown strips us from the durable goods orders, Q3 GDP and PCE inflation releases & jobless claims but we have the euro area to fill in some of the gaps. EA GDP and inflation numbers are due with releases scattered across the week. Key central banks decide over policy: the Fed (-25 bps expected to 3.75-4%) and the Bank of Canada (-25 bps to 2.25%) on Wednesday, and the BoJ (unchanged at 0.5%) and ECB (unchanged at 2%) on Thursday. The highly anticipated in-person meeting between presidents Trump and Xi will be closely watched for any signs of a trade thaw. The earnings season shifts into higher gear (Caterpillar, Alphabet, Meta, Microsoft, Apple, Amazon …).

News & Views

October Czech confidence data improved further. The composite indicator rose 2.1 points to 104, the best level since June 2021 on both improving business (up 1.8 to 103.4) and consumer confidence (+ 3.9 to 107.4). Confidence in the economy increased in industry and slightly in selected service sectors. It declined in trade and construction. The share of consumers expecting the overall economic situation to deteriorate over the next twelve months fell significantly compared to September. Households expecting their financial situation to improve over the same horizon also increased. The Czech koruna trades marginally softer today at EUR/CZK 24.33, but in a broader perspective holds a solid performance recorded earlier this year (YTD 3.5% gain).

UK PMIs showed somewhat faster UK output growth in October, with the composite PMI rising from 50.1 to 51.1. That corresponds to still-sluggish growth nonetheless (0.1%). The upturn was supported by another modest improvement in the services sector (51.1 from 50.8) and a first limited expansion in manufacturing output in 12 months. New business volumes also increased and contributed to the slowest rate of private sector job shedding since May. Input prices moderated to the lowest since November 2024 and output inflation slowed, driven by a more modest rise in service sector prices. The upcoming budget remains a source of caution in businesses’ behavior.

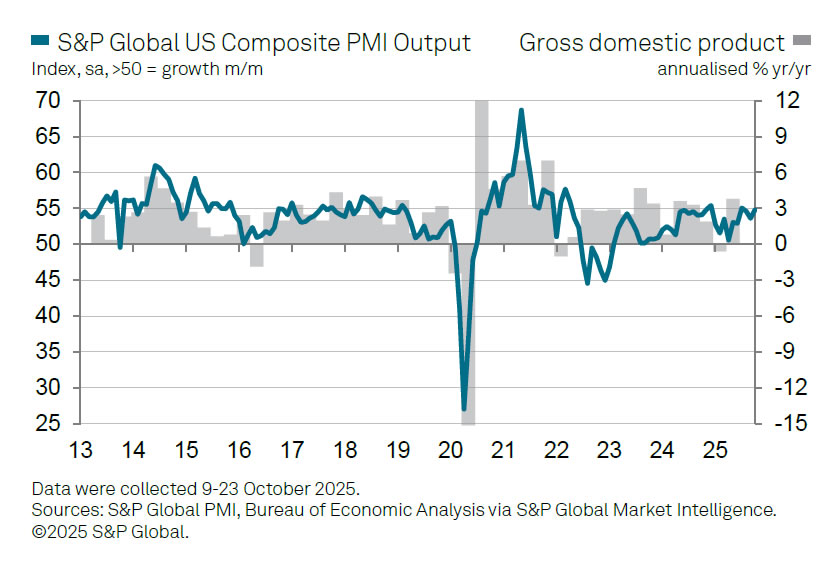

US PMI composite rises to 54.8, points to sustained strong economic growth

US business activity expanded at a solid pace in October, with PMI Composite rising from 53.9 to 54.8. Both sectors showed improvement as Manufacturing edged up from 52.0 to 52.2 and Services climbed from 54.2 to 55.2, signaling a broad-based pickup in momentum.

According to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, the data point to “sustained strong economic growth” at the start of the fourth quarter, consistent with an annualized expansion of around 2.5% — similar to the pace seen in Q3.

However, optimism about the future weakened noticeably. Williamson noted that business confidence fell to one of the lowest levels in three years, as companies expressed growing concern over the economic fallout from tariffs and uncertain policy direction.

Price trends offered a mixed picture. Input costs continued to rise sharply, reflecting the pass-through of tariffs, yet firms struggled to raise prices amid competitive pressures. As a result, selling price inflation cooled to its lowest since April.

US: Headline and Core Inflation Rise 3% Annualized in September

The Consumer Price Index (CPI) rose 0.3% month-on-month (m/m) in September, a tick below the consensus forecast in Bloomberg. On a twelve-month basis, CPI rose to 3.0% (from 2.9% the month prior).

- Higher prices at the pump (+4.1% m/m) were partly responsible for the sustained strength in headline inflation, while food prices (+0.2% m/m) moderated thanks to a slowing in grocery costs and 'food away from home'.

Excluding food and energy, core inflation rose 0.2% m/m, a step down from the 0.3% m/m readings in the two prior months and a tick below the consensus forecast. The twelve-month change was up 3.0%, while the three-month annualized rose by a slightly faster 3.6%.

Services inflation moderated in September – rising 0.20% m/m – following a hotter 0.35% m/m gain the month prior. The deceleration was largely led by a cooling in primary shelter costs (+0.15% m/m vs 0.4% m/m in August), which grew at their slowest monthly rate since January 2021. Price growth for non-housing services (+0.3% m/m vs. +0.4% m/m in August) also eased but are still running just under 5% annualized over the last three months.

- Higher travel costs (+1.8% m/m) remain a notable contributor to the sustained strength in non-housing services, thanks to a further uptick in airfares (+2.7% m/m) and hotel costs (+1.8% m/m). Price growth for recreational services (+0.4% m/m) also accelerated on the month.

Tariff passthrough continued to materialize in core goods prices, which were up 0.2% m/m and would have been even larger if not for the pullback in used vehicle prices (-0.4% m/m) and educational goods (-0.8% m/m). Price gains were most notable in apparel (+0.7% m/m), appliances (+0.5% m/m), and recreational commodities (+0.4% m/m).

With the shutdown ongoing, this morning's CPI release was done so that the government could meet its statutory requirements in adjusting Social Security payments for next year, which are benchmarked to Q3 CPI data.

- Because the Bureau of Labor Statistics conducted the September CPI survey ahead of the government shutdown, there are no concerns with data quality.

- However, collection rates could very well be impacted for the October survey, given that data gathering is still suspended with the shutdown ongoing. At a minimum, this suggests there could be issues with data quality in the next release, and the longer the shutdown drags on, the greater the risk that the October report is skipped entirely.

Key Implications

September's inflation report came in a bit softer than expected, thanks to a sharp cooling in primary shelter costs. Elsewhere, there were plenty of signs to suggest that elevated inflationary pressures are likely to persist in months ahead. Tariff passthrough continued to mount, with 75% of goods categories experiencing price gains last month (up from 67% in August). Meanwhile, price growth for non-housing services remained firm, particularly in categories tied to discretionary consumer spending.

With the softening labor market becoming a more pointed concern for policymakers, we don't feel that today's elevated inflationary pressures will deter the FOMC from delivering on another quarter-point rate cut next week. However, hotter readings on subsequent inflation prints could have implications for future decisions, particularly given the growing divide among FOMC members. For now, markets are still priced for another 50 basis points of easing by year-end – a view that aligns to our forecast.

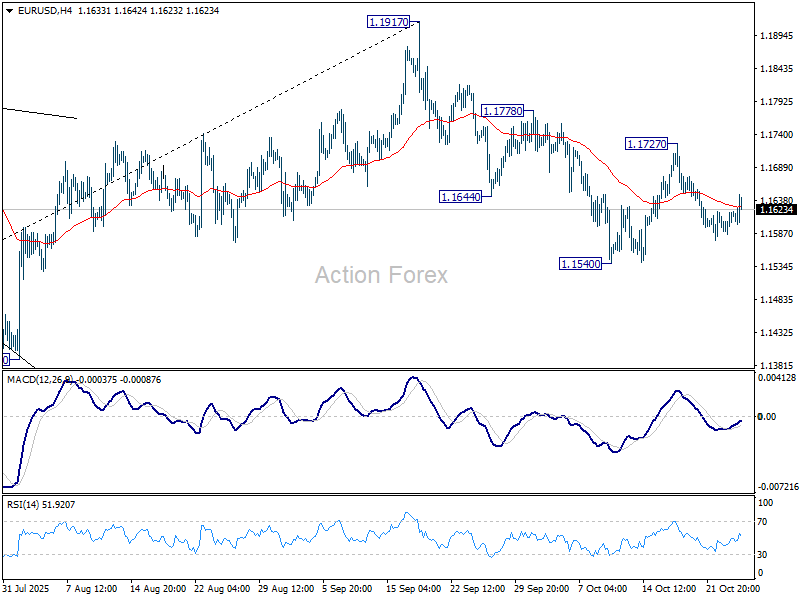

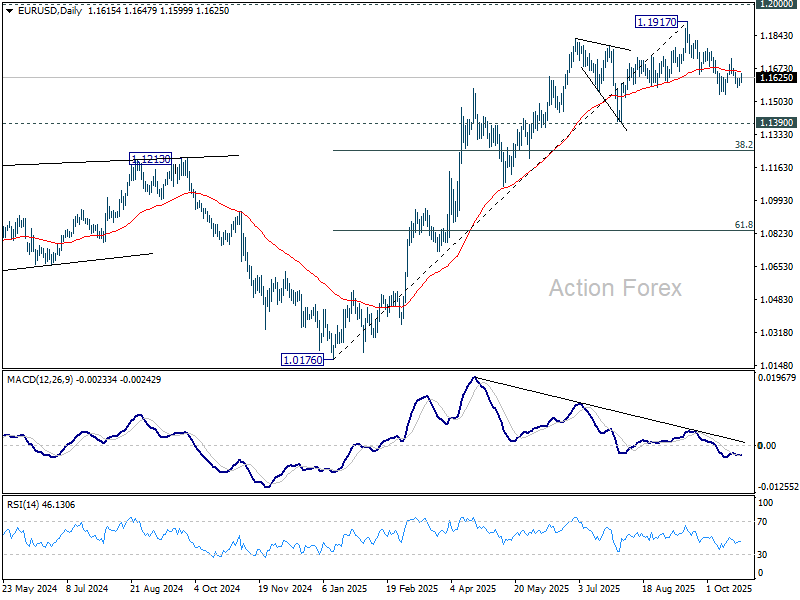

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1595; (P) 1.1608; (R1) 1.1630; More…

Outlook in EUR/USD remains unchanged and intraday bias stays neutral. Further decline is expected with 1.1727 resistance intact. Break of 1.1540 will resume the fall from 1.1917 to 1.1390 support, or even further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252. On the upside, though, break of 1.1727 resistance will turn bias back to the upside for 1.1778, and then retest of 1.1917 high instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1290) holds, the up trend from 0.9534 (2022 low) is still expected to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

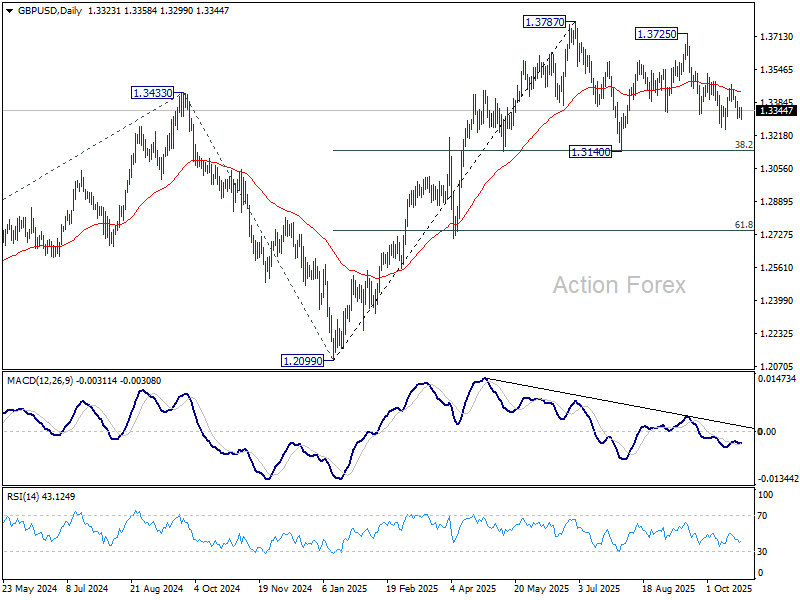

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3301; (P) 1.3333; (R1) 1.3358; More...

Intraday bias in GBP/USD remains neutral for the moment and outlook is unchanged. Fall from 1.3725 could extend lower and break of 1.3247 will target 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected there to contain downside to complete the corrective pattern from 1.3787. On the upside, break of 1.3170 resistance will turn bias back to the upside for 1.3526 resistance. Firm break there will target 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3191) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

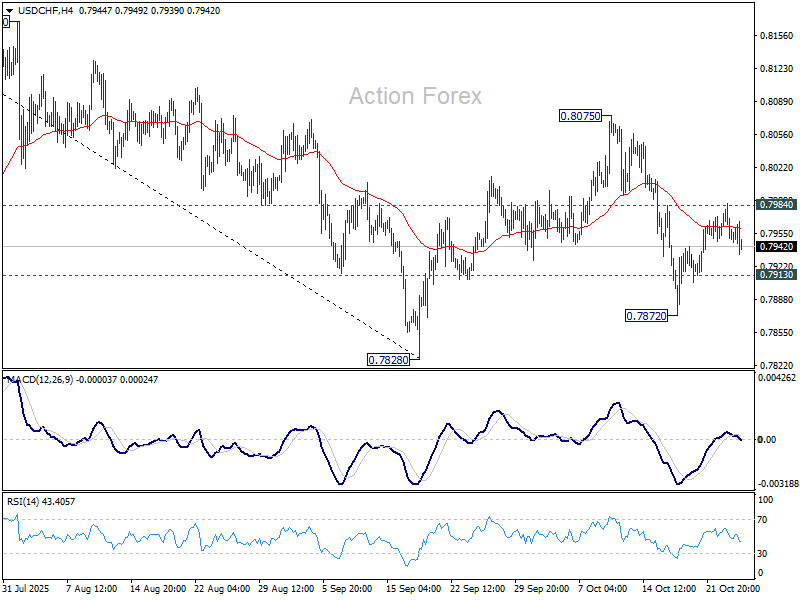

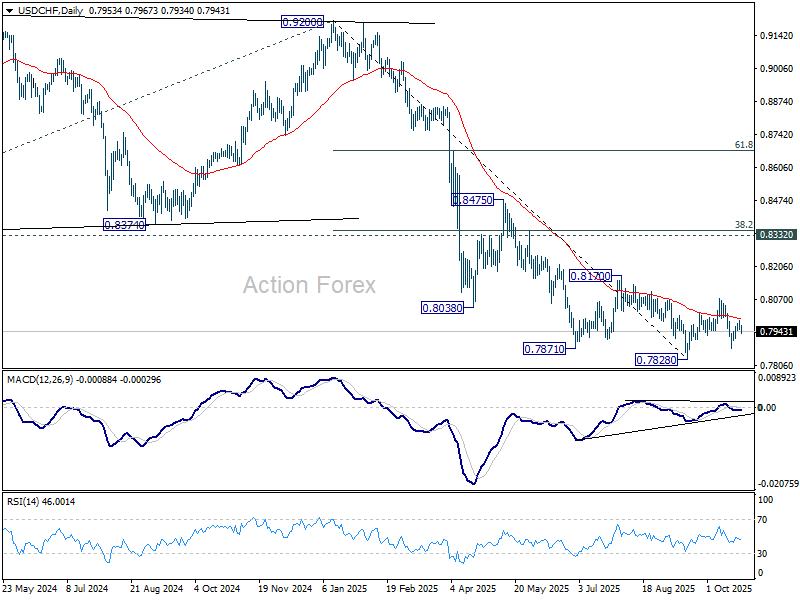

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7939; (P) 0.7963; (R1) 0.7976; More…

Intraday bias in USD/CHF remains neutral for the moment. With 0.7984 resistance intact, further decline is in favor. On the downside, below 0.7913 minor support will turn bias to the downside for 0.7872 and then 0.7828 low. Firm break there will resume larger down trend. However, break of 0.7984 will suggest that corrective pattern from 0.7828 is extending with another rising leg, and target 0.8075 again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

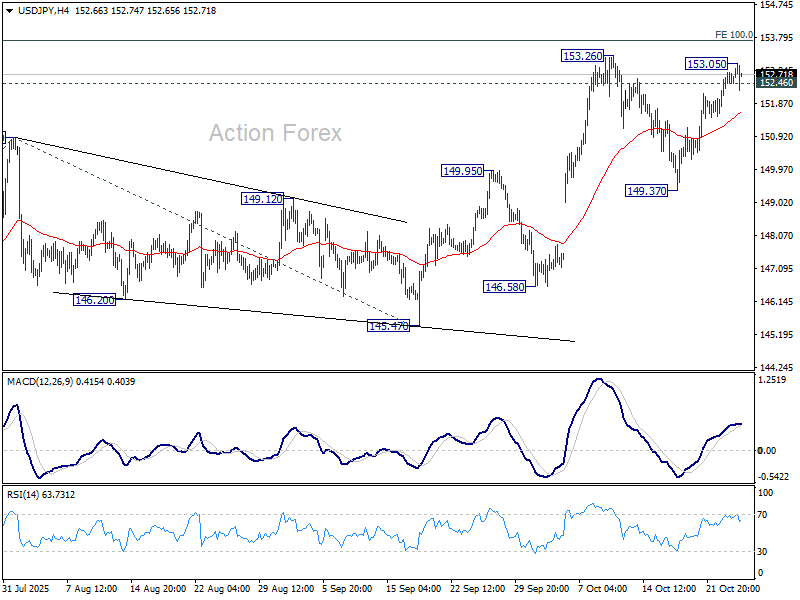

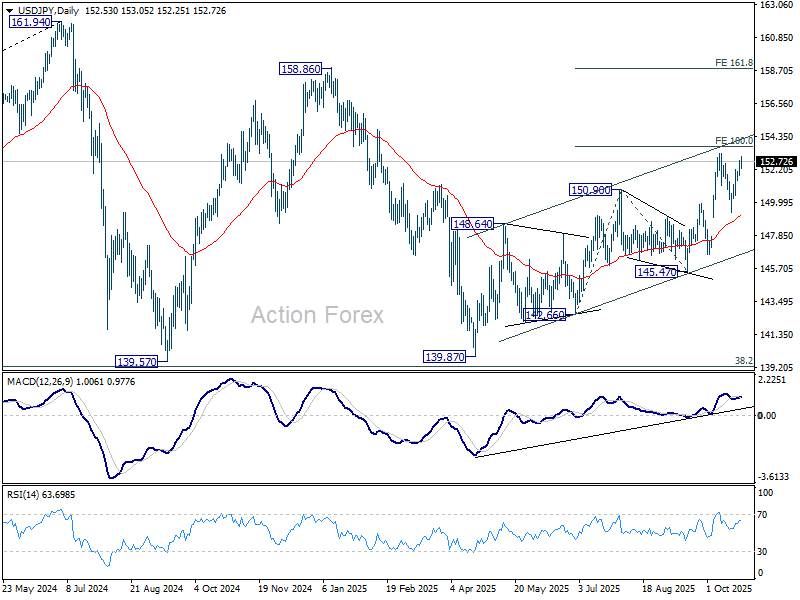

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.01; (P) 152.40; (R1) 152.99; More...

Intraday bias in USD/JPY is turned neutral with current retreat, and some consolidations would be seen. Another rise is in favor as long as 55 4H EMA (now at 151.56) holds. Above 153.05 will target 153.26, and then 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

Dollar Slips as Softer Core Inflation Reinforces Bets on Two More Fed Cuts This Year

Dollar eased in early U.S. session after the latest inflation report came in slightly softer than expected, reinforcing expectations of continued monetary easing by the Fed. The pullback was modest, but sentiment turned more dovish as traders focused on the dip in core inflation, which may be seen as evidence that price pressures have peaked during the summer. While still early to call a full victory on inflation, the data injected a sense of guarded optimism into markets.

Rate expectations shifted quickly, with futures markets now nearly fully pricing a December rate cut following next week’s anticipated 25bps reduction. Fed funds futures indicate a 99% probability that policy rates will be lowered to the 3.50–3.75% range by year-end.

Elsewhere, U.S. stock futures rose modestly after the release, buoyed by expectations of a friendlier rate environment. DOW edged closer to its record highs, though whether buying momentum can sustain through the session remains to be seen. Meanwhile, Treasury yields tumbled, with the 10-year yield falling back sharply after briefly testing 4.0%, signaling that the market may have just given its final “kiss goodbye” to that level for now.

In commodities, Gold staged a modest recovery, continuing to defend the 4,000 mark despite muted momentum. The metal remains supported by lower yields and lingering geopolitical concerns, though traders appear hesitant to extend the rally until the Dollar’s next clear directional move.

Across the currency markets, commodity-linked currencies continue to lead weekly performance — Kiwi remains the strongest, followed by Aussie and Loonie. Yen stays under broad pressure, trailed by Sterling and Euro. Dollar and Swiss Franc are holding mid-pack, though momentum suggests Dollar could slide further before the weekly close if risk appetite persists.

In Europe, at the time of writing, FTSE is up 0.12%. DAX is up 0.21%. CAC is down -0.34%. UK 10-year yield is down -0.02 at 4.415. Germany 10-year yield is up 0.03 at 2.619. Earlier in Asia, Nikkei rose 1.35%. Hong Kong HSI rose 0.74%. China Shanghai SSE rose 0.71%. Singapore Strait Times rose 0.13%. Japan 10-year JGB yield fell -0.002 to 1.659.

US CPI rises to 3.0%, but Core eases, both miss expectations

US inflation ticked higher in September, but the details of the report suggested price pressures are cooling beneath the surface. Headline CPI accelerated to 3.0% yoy, up from 2.9% but slightly below expectations of 3.1%. That marks the highest level since January.

Though, core CPI — excluding food and energy — slowed from 3.1% to 3.0%, undershooting forecasts and easing from 3.1% in the previous two months. After holding at 3.1% for two consecutive months, the core rate could be entering into a gradual downtrend.

On a monthly basis, headline prices rose 0.3% mom, while core prices increased just 0.2%, both softer than expected. Energy costs were again the key driver of the headline gain, with the gasoline index surging 4.1% and the broader energy index up 1.5%. Food prices also continued to edge higher, rising 0.2% as grocery costs climbed more sharply than dining-out prices.

UK PMI composite improves to 51.1, but indicates just sluggish 0.1% GDP growth

The latest UK flash PMI data offered a glimmer of optimism for the economy, with Manufacturing jumping from 46.2 to 49.6 in October — its highest level in 12 months. Services rose from 50.8 to 51.1, lifting the Composite index from 50.1 to 51.1. The survey suggests business conditions are slowly improving after a soft September, marking the first sign of renewed momentum since midyear.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, said the data “brings hope that September was a low point,” noting the first manufacturing growth in over a year and stronger consumer demand for services. He added that inflationary pressures are easing back toward levels “consistent with the Bank of England’s 2% target,” while job losses are moderating and business confidence is ticking up slightly.

Still, the overall pace of expansion remains modest, consistent with GDP growth of only about 0.1%. Export weakness persists due to global trade disruptions tied to U.S. tariff policy. Firms are also cautious ahead of the November 26 Budget, with many delaying hiring and investment decisions. While the PMI data point to stabilization, the recovery remains fragile and heavily dependent on fiscal clarity and external demand.

UK retail sales rise 0.5% mom in September, hitting highest level mid-2022

UK retail activity surprised to the upside in September, with sales volumes rising 0.5% mom, defying expectations of a -0.2% mom decline. The gain marked the fourth consecutive monthly increase, lifting total sales to their highest level since July 2022. Stronger non-store and clothing sales helped offset weakness in fuel and other discretionary categories.

Over the third quarter, retail volumes grew 0.9% compared with the previous quarter, confirming a steady rebound in household demand through the summer. The good weather in July and August was cited as a key driver, boosting clothing sales and supporting outdoor-related spending. Online and non-store retailers also enjoyed sustained gains.

Eurozone PMI composite hits 17-mont high, services lead while France drags

Eurozone business activity accelerated in October, with PMI Composite rising to a 17-month high of 52.2 from 51.2, signaling the strongest expansion since mid-2024. The pickup was driven by services, where PMI Services index jumped from 51.3 to 52.6, a 14-month high, while Manufacturing finally edged up to the neutral 50.0 mark after months of contraction.

However, the upturn remains uneven across major economies. Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that France has increasingly become a drag, with its rate of contraction accelerating for two straight months amid political turmoil and budget disputes under Prime Minister Sébastien Lecornu. In contrast, Germany’s outlook "brightened significantly", helping to lift the bloc’s overall figures. Still, manufacturing has been “stagnating for practically six months,” de la Rubia said, and weak new orders leave “little hope of a turnaround.”

Inflation trends offer some comfort for policymakers. Price pressures in the services sector — a key focus for the ECB — “remain moderate,” with sales price inflation slightly higher but still near long-term averages. The PMI data are therefore unlikely to alter the ECB’s cautious stance, reinforcing expectations that officials will hold off on further rate cuts until clearer signs of sustained disinflation emerge.

Japan CPI core Rises to 2.9%, ending three-month slowdown

Japan’s inflation picked up in September, with core CPI (excluding fresh food) rising from 2.7% to 2.9% yoy, matching expectations and marking the first acceleration in four months. The key gauge has stayed at or above the BoJ’s 2% target since April 2022. Headline CPI also rose from 2.7% to 2.9% yoy, in line with the core measure.

Underlying momentum was uneven. Core-core CPI, which strips out both energy and fresh food and is considered a closer measure of domestic demand, slowed to 3.0% from 3.3% yoy, suggesting that broader inflationary pressures are gradually easing.

Food prices continued to rise, but at a slower pace — non-fresh food prices gained 7.6%, down from 8.0% in August. Rice prices, which spiked earlier this year, rose 49.2%, their fourth consecutive month of deceleration after peaking at more than 100% growth in May.

Meanwhile, service prices, a metric closely watched by the BoJ for its link to wage growth, increased 1.4%, slightly below August’s 1.5%.

Japan PMI composite falls to 50.9, weak Yen keeps inflation hot

Japan’s private sector lost further momentum in October, with both manufacturing and services activity softening, according to S&P Global’s Flash PMI survey. The Manufacturing PMI slipped from 48.5 to 48.3, extending its contraction, while Services PMI fell from 53.3 to 52.4. As a result, Composite index eased from 51.3 to 50.9, signaling the slowest pace of overall growth since May.

Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, said the survey showed the first decline in new business in 16 months. While the services sector remained the key driver of growth, its fading strength “will be a point of concern” as manufacturing continues to struggle. The factory sector’s downturn deepened, with new orders falling at the fastest pace in 20 months.

Inflationary pressures, however, remained elevated. Both input costs and output charges continued to rise at historically strong rates, driven by higher wage, fuel, and material costs, and alongside by a weaker Yen.

Australia PMI composite ticks up to 52.6, easing inflation keeps RBA on easing track

Australia’s private sector activity sent mixed signals in October, according to the S&P Global Flash PMI survey. Manufacturing PMI slipped back into contraction, falling from 51.4 to 49.7, while Services PMI rose to 53.1 from 52.4, lifting the Composite PMI modestly from 52.4 to 52.6. The data suggest that overall business activity grew at a slightly faster pace at the start of Q4, though the underlying picture remains uneven across sectors.

According to Jingyi Pan, Economics Associate Director at S&P Global Market Intelligence, the divergence between sectors was striking. Manufacturing “notably worsened,” with new orders dropping further and factories shedding jobs amid pressure on profit margins.

In contrast, services activity expanded at a solid pace, but even there, new business growth and hiring momentum slowed, and business confidence weakened.

On a positive note, price pressures continued to ease, with output price inflation falling to a five-year low. This cooling in inflation dynamics should reassure the RBA, which remains on track to pursue further monetary easing.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.01; (P) 152.40; (R1) 152.99; More...

Intraday bias in USD/JPY is turned neutral with current retreat, and some consolidations would be seen. Another rise is in favor as long as 55 4H EMA (now at 151.56) holds. Above 153.05 will target 153.26, and then 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there would prompt upside acceleration to 161.8% projection at 158.80.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.