Sample Category Title

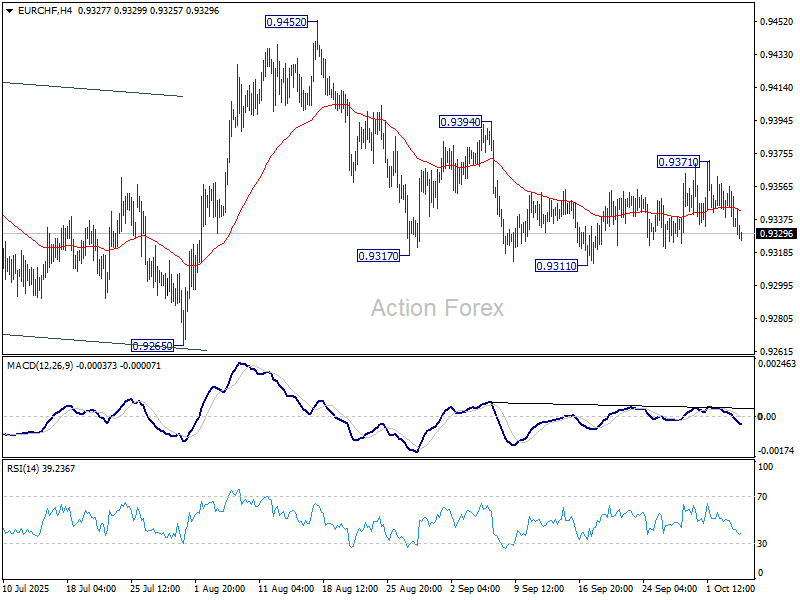

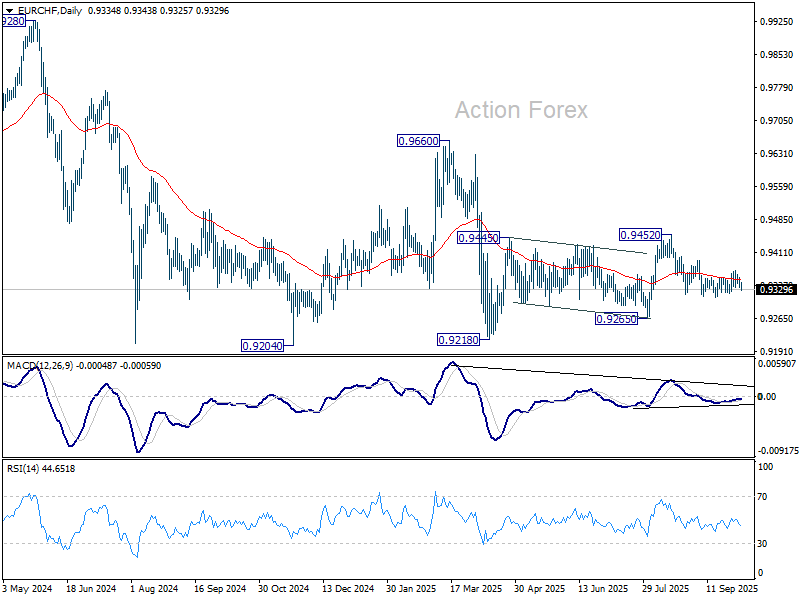

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9329; (P) 0.9345; (R1) 0.9355; More...

EUR/CHF dips mildly today but stays above 0.9311 support and intraday bias stays neutral. As price actions from 0.9311 are corrective looking, fall from 0.9452 is likely still in progress. On the downside, break of 0.9311 will target 0.9265 support next. For now, risk will stay on the downside as long as 0.9394 resistance holds, in case of another recovery.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

Japan Steals the Show as US Shutdown Delays Critical Data

The week kicked off on a positive note in Japan after the ruling LDP chose Sanae Takaichi as its next leader — she is now set to become the country’s next prime minister and is known for her preference for easy fiscal and monetary policies. Easier fiscal policy and more government spending are, of course, not great news for Japanese bonds, which have already seen yields rise steadily since 2020. The 20-year JGB yield, near 0% five years ago, is now approaching 2.70% — it jumped 6bp this morning, while the 30-year yield surged 12bp, hitting multi-decade highs last seen in August.

On the currency front, the Japanese yen slipped on expectations of a softer Bank of Japan (BoJ) path — and possibly fewer rate hikes. The USDJPY soared past the 150 mark. In equities, the Nikkei jumped more than 4% to a fresh all-time high on optimism that looser fiscal and monetary policies, along with a weaker yen, will continue to support Japanese equities. Defence stocks, in particular, rallied strongly on speculation that the new government could increase military spending beyond previous expectations. Japan Steel Works, for instance, jumped nearly 14%.

It was, in short, a great start to the week for Japanese equities — and much less so for Japanese bonds. Note, however, that rising JGB yields can threaten global risk appetite by narrowing the risk premium between JGBs and other assets. Still, strong dovish Federal Reserve (Fed) expectations and ongoing AI enthusiasm should help maintain appetite for US equities, while European markets may continue to benefit from the positive echoes of the global AI rally and softer BoJ bets joining the dovish Fed narrative.

S&P 500 and Nasdaq futures are in the green as I write, with the Nasdaq supported by Hon Hai (Foxconn) — one of Nvidia’s key server production partners — which reported an 11% rise in quarterly sales.

Over the weekend, OPEC announced it will raise oil output by 137,000 barrels per day in November, following a similar increase in October. Since the move had already been priced in after a 7% selloff in US crude last week, oil prices rebounded nearly 2% in Asia, flirting with the $62 per barrel level. The bounce followed a break below the summer’s sideways trading range around $62, on expectations of this very production hike. The broader outlook, however, remains tilted to the downside, with a greater likelihood of prices slipping below $60 than climbing back above $65 per barrel.

Now, let’s turn to what hasn’t been announced. The US official jobs data was not released last Friday as the government remains shut, and the data scheduled for this week will also be delayed if the shutdown continues — a scenario currently given a 60%–80% chance. The US dollar is better bid this morning, mostly due to the sharp selloff in the yen, but fundamentally, none of the traditional currencies looks particularly appetizing.

The dollar faces headwinds from trade tensions, political uncertainty and debt concerns. Sterling remains hard to love amid fiscal and political risks ahead of the Autumn Budget. The yen, once a safe haven, is grappling with its own debt and political challenges, and the euro, while relatively stronger, remains clouded by French political turmoil, as the new government faces early no-confidence risks. Among traditional currencies, the Swiss franc remains the standout safe haven — though the Swiss National Bank (SNB) is showing its teeth to the bulls, warning it could sell francs to counter excessive appreciation.

As a result, assets without government ties — like gold and Bitcoin — are seeing renewed inflows. Gold rallied to a fresh record high this morning, trading around $3’945 per ounce, and is likely to test the $4’000 level soon. Some strategists, including those at Goldman Sachs, see it heading toward $5’000 per ounce. Silver rose to $48.50, with bulls eyeing a break above the $50 psychological mark, and Bitcoin briefly traded above $125’000 over the weekend. These assets are likely to continue trending higher, not least thanks to a broadly softer US dollar.

Zooming out from currencies, this week’s macro calendar is relatively light. China remains closed for the Golden Week holiday until Thursday. ECB President Lagarde and BoE Governor Bailey speak today. The Reserve Bank of New Zealand (RBNZ) is expected to announce a 25bp rate cut at its meeting on Wednesday, and the FOMC will release the minutes of its latest meeting a few hours later.

And yes — there’s still a slim chance that the US jobs report could be released on Friday, but I wouldn’t bet my shirt on it.

In the absence of key data, US investors will focus on Wednesday’s FOMC minutes for any hint of further dovishness, and on the start of the earnings season, which kicks off this week. Expectations are upbeat but still largely beatable. The S&P 500 is expected to deliver 6.3% revenue growth and nearly 8% profit growth in Q3, with technology earnings seen surging 21%, utilities and financials rising 17.5% and 11% respectively, while energy and consumer staples are expected to post around a 3% decline due to trade frictions and weaker energy prices.

The first earnings will land on Thursday, with Delta, Levi’s, and Pepsi, followed by BlackRock on Friday.

Yen Slumps on Takaichi’s LDP Victory

In focus today

In the euro area, focus tuns to the August retail sales data and the October Sentix confidence indicator. The consumers have been cautious recently and retail sales will show if that persisted in August. It is expected that spending rose 1.3% y/y (0.1% m/m). The Sentix investor confidence indicator is expected to show an improvement to -7.7 from -9.2.

This week features a light calendar with no tier-1 global macro data scheduled. However, the delayed US labour market report could be released if the government shutdown ends. Key events include the University of Michigan consumer confidence survey and FOMC minutes in the US, and wage figures from Japan.

Economic and market news

What happened since Friday

In Japan, Saturday, the governing Liberal Democratic Party (LDP) chose a new president who is also likely to become the new PM. In her third attempt on the presidency, Abenomics loyalist Sanae Takaichi was elected as party leader against polls, which had continuity candidate Shinjiru Koizumi as favourite. Takaichi stands for a bigger fiscal package than other candidates and will not rule out lowering the VAT-rate, a move popular among opposition parties. She will now try to form a coalition in the lower house to become the first female PM In Japan. As a nationalist and advocate for amending Japan's pacifist constitution, continuing the current alliance with the small Buddhist party, Komeito, might not be straight forward, and thus political uncertainty lingers. A snap election also cannot be completely ruled out, even if that exact move backfired for the LDP last year. Takaichi has previously been critical of BoJ hikes, which is also reflected in BoJ pricing and yen weakness this morning. Investors now only see about 25% chance of an October hike and USD/JPY is back at 150, up from 147.5. With high inflation and a weak yen as bigger political issues these days, we do not think she will stand in the way of higher interest rates, but normalising BoJ policies might take even longer with Takaichi as PM.

In the US, the ISM report on the non-manufacturing sector for September revealed a PMI of 50.0 (cons: 51.7, prior: 52.09 The data highlights weakening momentum in services, with declines in business activity and new orders. Meanwhile, the prices index remains sharply elevated at 69.4 (prior: 69.2). The employment index showed a slight recovery to 47.2 (prior: 46.5), although it's worth noting this metric has historically shown limited correlation with monthly NFP data.

In Norway, the SA unemployment rate remained steady at 2.1% in September, as expected. While the number of unemployed persons dropped by 3-400 m/m, total unemployment (all types) rose by 100 persons, presenting mixed signals. New vacancies increased to 40 200, with the 3-month moving average at 42 400, indicating a renewed pick up in labour demand. The Norwegian housing market continues to look robust with house prices rising 0.4% m/m, taking the annual growth to 5.5%. Although price growth came in slightly below Norges Bank's forecast of 0.6%, the impact is insufficient to influence monetary policy.

In Sweden, the services PMI surged in September, rising from 53.8 to 57.7, pushing the composite PMI up from 54.2 to 57.1. A strong services PMI, with a notable recovery in the employment index, signals potential upside risks to employment. The indicator is not the most reliable, but it still offers an encouraging sign. The composite PMI also indicates some upside risks to our GDP-forecast and suggests that the recovery will pick up speed before year-end. Price pressures remain contained.

In commodities space, OPEC+ agreed to increase oil output by 137,000 barrels per day in November - a modest hike despite speculation of faster increases. While the market might be relieved, we think the big picture in the oil market is more important. OPEC+ continues to increase supply amid low prices, greatly limiting upside potential for oil prices.

In the Israel-Palestine conflict, Hamas has accepted key elements of Trump's 20-point Gaza peace plan, including a ceasefire and Israel's initial withdrawal. However, critical issues, such as Hamas's willingness to disarm, remain unresolved. High-stakes talks between delegates from Hamas, Israel, the US, and Qatar are set to take place in Egypt today to finalise the plan's implementation.

Equities: Equities ended last week higher again, marking yet another strong stretch of performance and fresh record highs across major indices. The key challenge for equities right now is simply the pace of the rally, markets are increasingly running ahead of fundamentals.

Healthcare was the standout sector last week, with the pharma industry surging more than 10% in both Europe and the US. It's a textbook example of what can happen when a deeply oversold and under owned sector finally gets a hint of positive news flow. This sharp turnaround also vindicates our earlier decision to move from neutral to overweight in healthcare. In contrast, energy lagged significantly as oil prices extended their decline, leading to substantial sector dispersion. Despite five consecutive up-days for global equities, defensives outperformed, largely due to healthcare's strength. Interestingly, volatility crept slightly higher through the week, with the VIX rising modestly each day despite the equity gains. The US government shutdown narrative and lack of key data likely contributed to the mild uptick in implied volatility.

This morning, Japanese equities are up more than 4% as markets react to news of a new prime minister, reviving memories of Abenomics-style policy shifts. Futures are also pointing higher in both Europe and the US.

FI and FX: Despite a relatively calm end to last week in the fixed income and FX markets and despite the fact that Israel and Hamas are set to begin negotiations today, gold prices continue to climb, reaching new highs.

In Japan, the election of Sanae Takaichi triggered an equity rally, while the JPY weakened further. Meanwhile, in the US, attention remains on the duration of the government shutdown and its economic implications, particularly given the postponement of key data releases. The Fed's response to these developments remains a critical focus for markets.

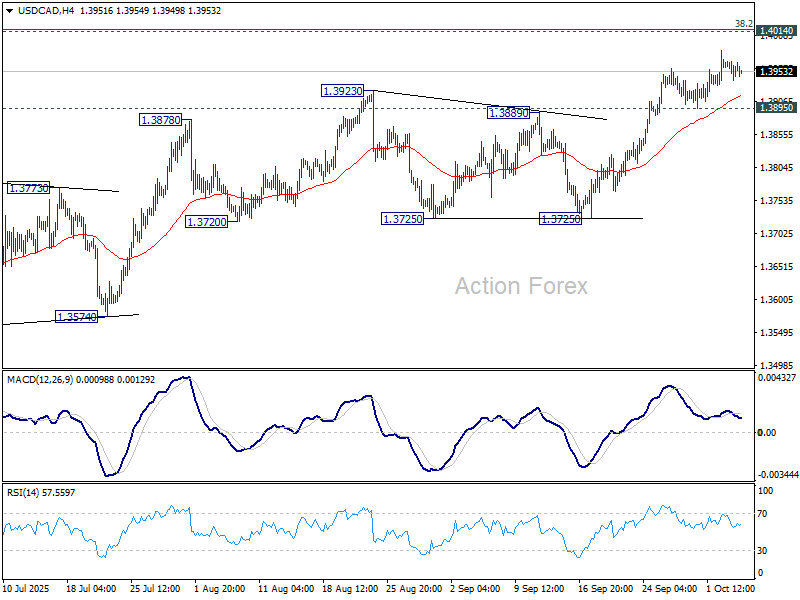

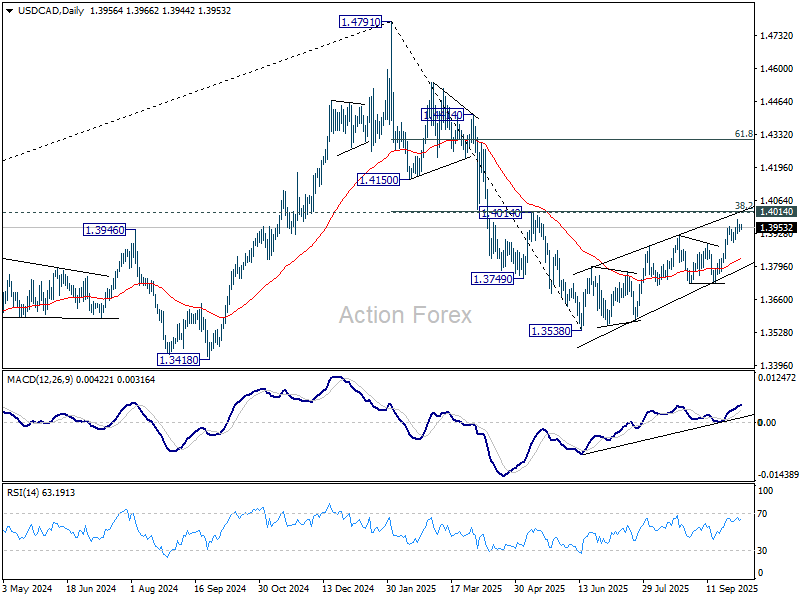

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3935; (P) 1.3954; (R1) 1.3968; More...

Further rise could be seen in USD/CAD with 1.3895 support intact. But strong resistance is expected from 1.4014 cluster to complete the corrective rally from 1.3538. On the downside, below 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

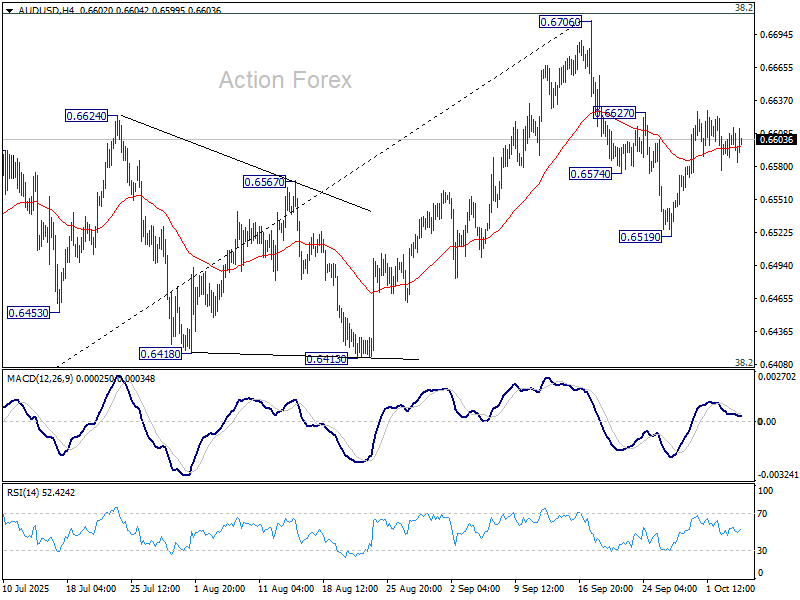

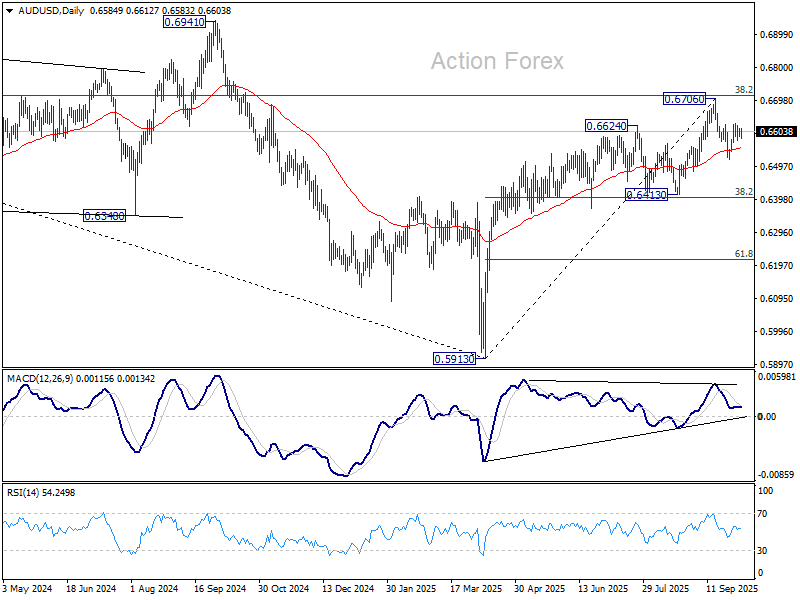

AUD/USD Daily Report

Daily Pivots: (S1) 0.6589; (P) 0.6602; (R1) 0.6614; More...

Intraday bias in AUD/USD remains neutral for the moment. On the upside, firm break of 0.6627 resistance will suggest that pullback from 0.6706 has completed as correction, after drawing support from 55 D EMA (now at 0.6554). That will keep the larger rally from 0.5913 alive and bring retest of 0.6706 high. However, on the downside, sustained trading below 55 D EMA will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

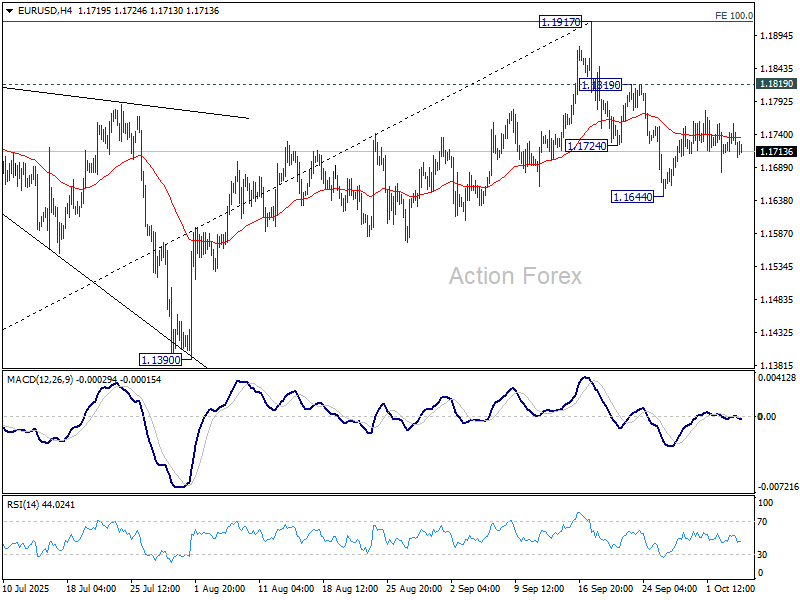

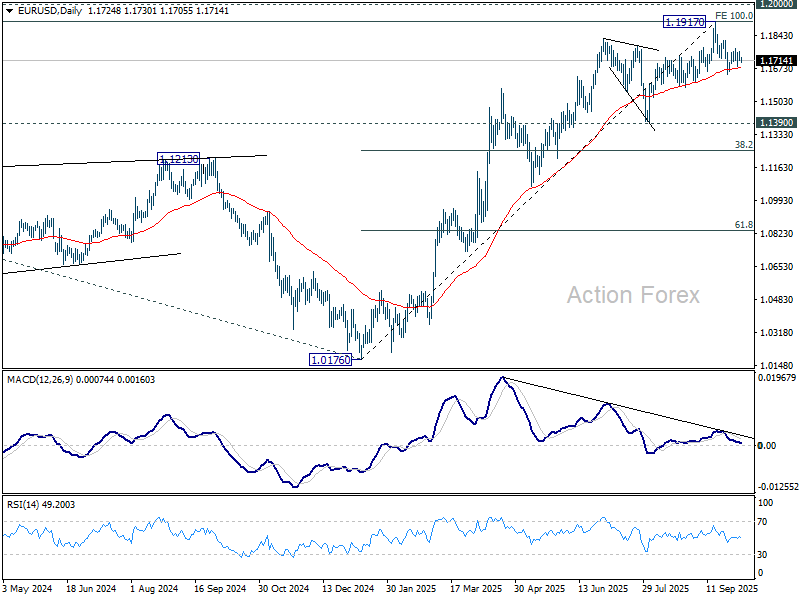

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1717; (P) 1.1738; (R1) 1.1763; More...

Intraday bias in EUR/USD remains neutral for the moment, and further fall is in favor as long as 1.1819 resistance holds. Break of 1.1644 and sustained trading below 55 D EMA (now at 1.1679) will indicate medium term topping at 1.1917, on bearish divergence condition in D MACD. Further fall should then be seen to 1.1390 support. Nevertheless, break of 1.1819 will retain near term bullishness and bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

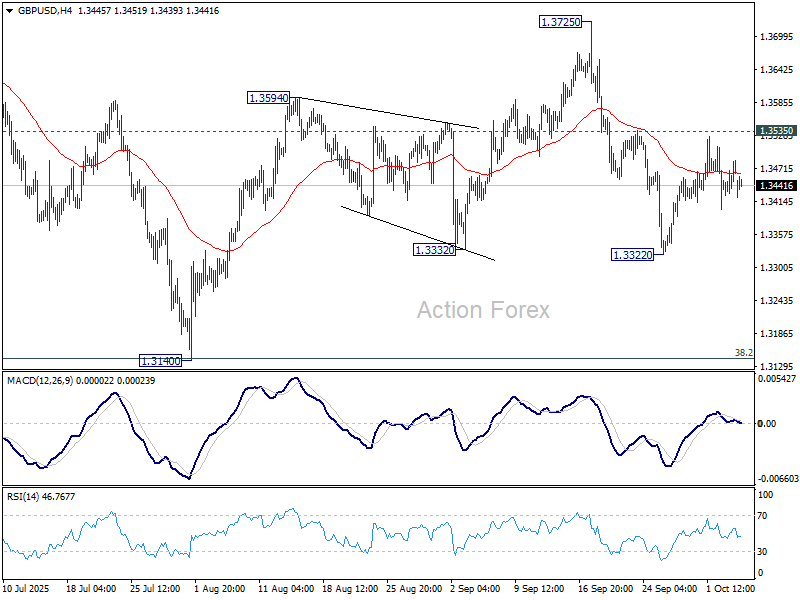

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3438; (P) 1.3462; (R1) 1.3502; More...

Intraday bias in GBP/USD stays neutral at this point, and further decline remains in favor. On the downside, break of 1.3322 will resume the fall from 1.3725 to 1.3140 support. On the upside, though, firm break of 1.3535 will argue that pullback from 1.3725 has already completed, and bring stronger rise to retest 1.3725/87 key resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3166) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

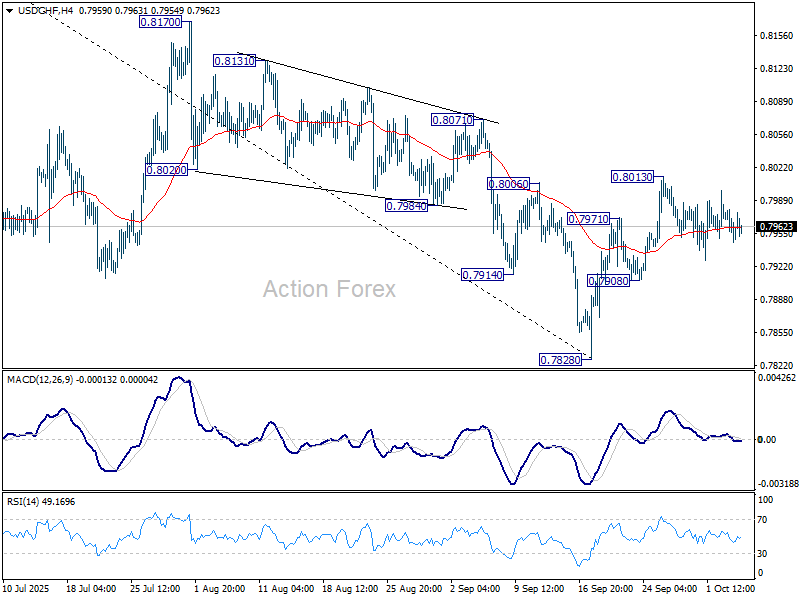

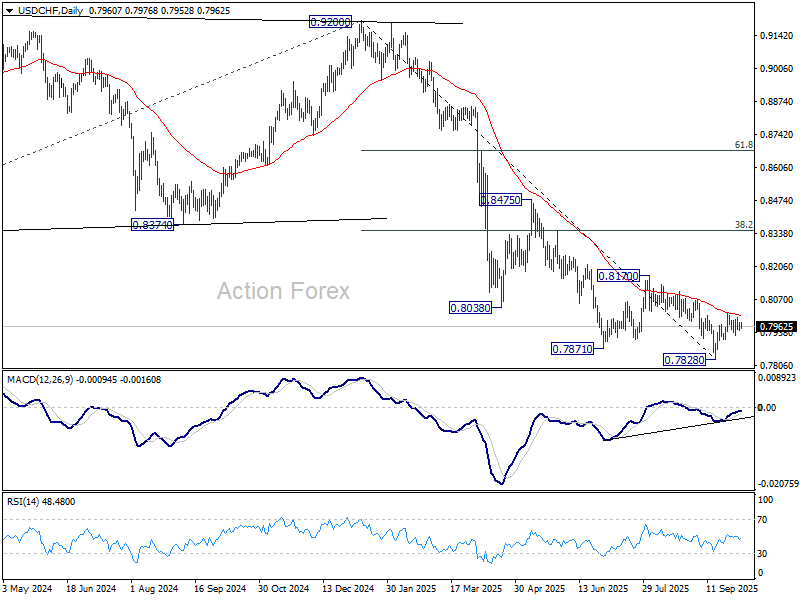

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7938; (P) 0.7963; (R1) 0.7978; More…

Range trading continues in USD/CHF and intraday bias remains neutral. On the upside, sustained trading above 55 D EMA (now at 0.8006) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

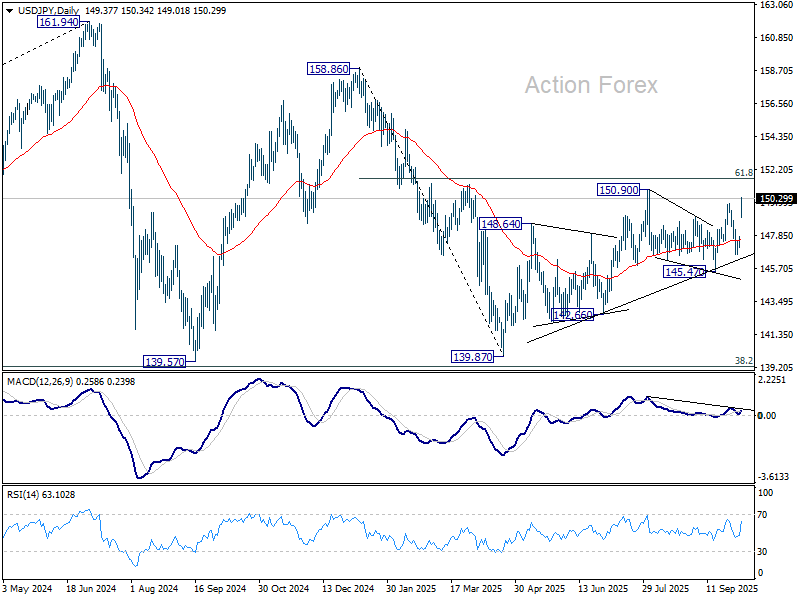

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.11; (P) 147.47; (R1) 147.84; More...

USD/JPY's strong rally and break of 149.95 resistance revived the case that corrective pattern from 150.90 has already completed at 145.47. Intraday bias is back on the upside for 150.90 first. Firm break there will resume larger rally from 139.87 to 151.22 fibonacci level. Sustained break there will carry larger bullish implication. On the downside, below 149.01 will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

Yen Nosedives as Nikkei Surges on Takaichi Optimism; Asia in Holiday Lull

Japan occupies the spotlight in otherwise subdued Asian trading, with much of the region quiet due to Mid-Autumn Festival holidays. Nikkei 225 jumped sharply to another record high, powered by euphoria surrounding Prime Minister-in-waiting Sanae Takaichi, whose pro-growth agenda and fiscal expansion plans have ignited investor optimism.

That optimism came at the expense of the Japanese Yen, which weakened broadly as traders embraced risk and pared back bets on further BoJ tightening in the near term. Renewed skepticism about the central bank’s willingness to hike again, coupled with surging equity sentiment, drove JPY to the bottom of the major currency rankings.

Elsewhere, Aussie and Kiwi outperformed, buoyed by the upbeat risk tone. New Zealand Dollar also found an additional lift after the NZIER’s RBNZ Shadow Board showed a majority calling for a 25 bps cut—not a larger move—at this week’s policy meeting.

Dollar was slightly firmer alongside the Canadian Dollar, with traders keeping one eye on the ongoing U.S. government shutdown and its potential implications. However, the moves were modest, and overall FX conditions remained rangebound amid light holiday liquidity. Among European majors, Sterling lagged, while Euro and Franc were little changed.

With the exception of pronounced Yen weakness, most pairs drifted in narrow ranges, reflecting a market caught between regional optimism and the lack of fresh catalysts ahead of the week’s key central bank updates including Fed and ECB minutes.

In Asia, at the time of writing, Nikkei is up 4.67%. Hong Kong HSI is down -0.61%. China is still on holiday. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield is up 0.005 at 1.670.

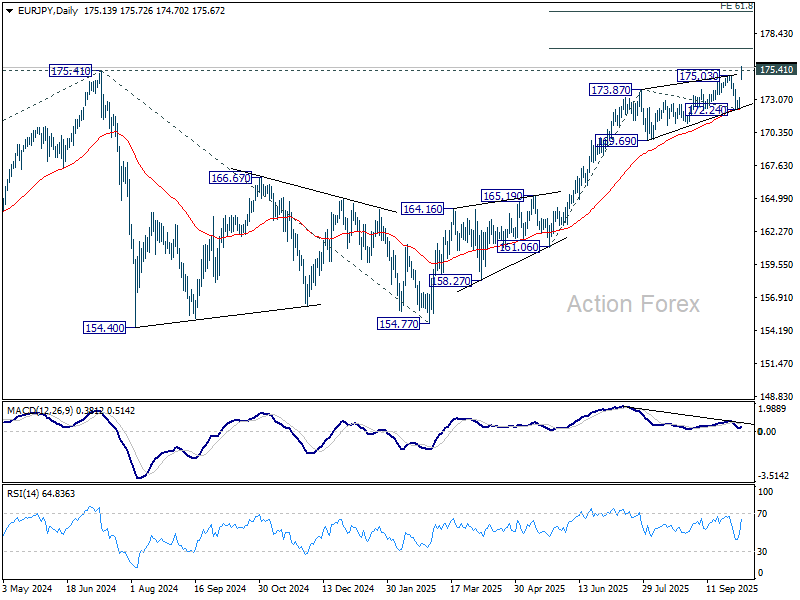

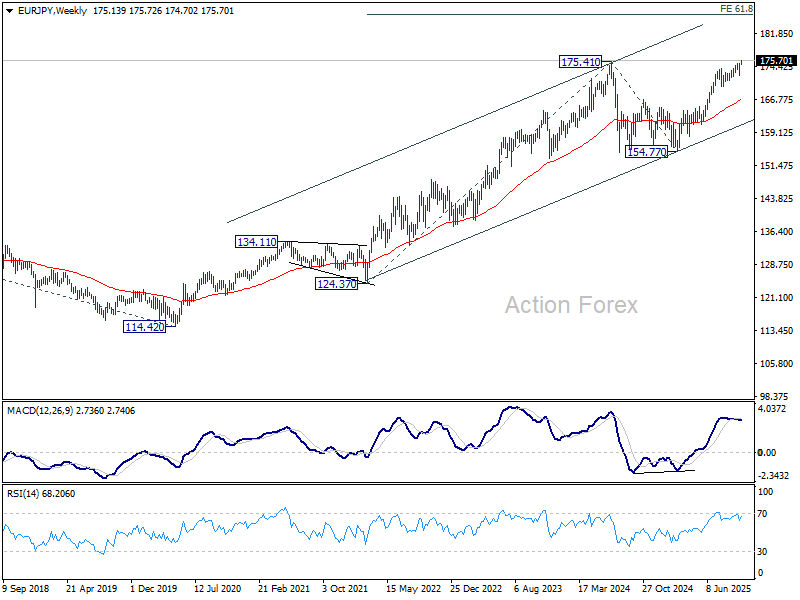

Takaichi victory spurs Yen selloff; EUR/JPY targets 180

Yen tumbled sharply in the Asian session as Nikkei 225 soared over 2,000 points, or 4%, to a new record high, after the Liberal Democratic Party elected Sanae Takaichi as its new leader. Markets quickly priced in expectations that Japan’s first female prime minister will pursue aggressive fiscal stimulus and stronger coordination with the private sector to revive growth.

A Takaichi administration is widely expected to overhaul Japan’s economic framework, emphasizing investment expansion and demand creation through public–private partnerships. Her longstanding support for Abenomics-style fiscal expansion has fueled optimism for renewed spending momentum, particularly in infrastructure and industrial policy.

Traders also anticipate that Takaichi will urge the BoJ to maintain its accommodative stance, dampening expectations for further tightening in the near term. Despite recent data supporting a mildly hawkish case, policymakers may tread carefully amid heightened political and fiscal uncertainty during the leadership transition.

Technically, EUR/JPY broke decisively above 175.41 (2024 high), confirming the resumption of its long-term uptrend. The next target lies at 38.2% projection of 161.06 to 173.87 from 172.24 at 177.13. Firm break there will open the path to 61.8% projection at 180.15.

In the medium term, EUR/JPY's rise from 114.42 (2020 low) should now be heading to 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31.

Bitcoin hits record as ‘Uptober’ hype and debasement trade drive demand

Bitcoin surged to a fresh record high over the weekend and held firm in early Asian trading. The move came as risk-on sentiment in U.S. equities spilled over into digital assets. More importantly, the latest rally also reflects a sense of seasonal optimism.

Traders are apparently leaning into Bitcoin’s well-known tendency to outperform in October — a pattern affectionately dubbed “Uptober” by crypto enthusiasts. The self-reinforcing psychology of this historical trend appears to be drawing momentum traders back into the market.

At the same time, speculation is mounting that the U.S. government shutdown could boost demand for hard assets and decentralized stores of value. Some investors see Bitcoin as part of a broader “debasement trade,” alongside Gold, amid concerns about fiscal instability.

Technically, the short-term focus is on 38.2% projection of 74,373 to 124,553 from 108,627 at 125,995. Decisive break above this level would confirm and solidify buying momentum, paving the way toward 61.8% projection at 137,838. For now, the broader outlook remains firmly bullish as long as the 108,627 support holds.

RBNZ to cut, but how deep? Fed and ECB minutes watched too

A center of focus for the week is on New Zealand, where the RBNZ’s October 8 meeting is expected to deliver another rate cut. The question isn’t whether it will ease, but by how much. After a run of dismal data and a deeper-than-expected -0.9% contraction in Q2 GDP, markets have all but concluded that policymakers must act decisively to cushion the economy.

Money markets are fully pricing a 25 bps cut to 2.75%, yet odds for a larger 50 bps move have climbed to 44.5%, up sharply from 25% a week earlier. Views among analysts remain split. Westpac stands out in projecting a half-point cut to 2.50%, arguing that the RBNZ risks falling behind the curve. Others favor a smaller, “insurance-style” move coupled with strong forward guidance signaling further easing ahead.

For traders, this meeting could be one of the most volatile in months. That policy nuance will determine how New Zealand Dollar trades post-decision. A cautious 25 bps cut with dovish tone could support Kiwi temporarily, while a surprise 50 bps move might spark a knee-jerk sell-off before stabilizing on speculations of a floor in the cycle. Either way, volatility is set to surge.

Attention will also pivot to central-bank minutes elsewhere. The Fed’s September FOMC minutes and the ECB’s meeting accounts will reveal how policymakers are parsing the impact of tariffs, inflation, and fiscal uncertainty. Together, they form the week’s macro backbone.

At the Fed, the September meeting delivered a 25 bps cut to 4.00–4.25%, with a 8–1 vote—new Governor Stephen Miran pushing unsuccessfully for a larger 50 bps move. Even dovish voices like Christopher Waller and Michelle Bowman backed the more measured option, highlighting a consensus for steady but cautious easing.

Markets will watch whether the minutes expose any growing urgency within the FOMC. While officials acknowledge that tariff-related price pressures could last longer, most agree the risks are moderate. The greater debate likely centers on labor-market slack and whether deteriorating employment data justify accelerating cuts.

Complicating matters, the U.S. government shutdown continues into its second week, delaying critical data and keeping investors blind to the economy’s near-term health. In this environment, another “insurance cut” in October looks increasingly probable, as policymakers seek to offset potential fiscal drag and uncertainty. But we'd need to hear more comments from Fed officials this week to verify this view.

Meanwhile, the ECB’s September accounts are expected to confirm that officials are broadly content with the deposit rate at 2.00%, reinforcing the sense of policy stability in Europe. The release could turn out to be a non-event.

Other key releases—Eurozone Sentix confidence, Japan’s household spending and cash earnings, Canada’s employment, and U.S. Michigan sentiment and inflation expectations—will round out the week.

Here are some highlights for the week:

- Monday: Swiss unemployment rate; Eurozone Sentix investor confidence, retail sales; UK PMI construction.

- Tuesday: Australia Westpac consumer sentiment; Japan household spending; Germany factory orders; Swiss foreign currency reserves; Canada trade balance, Ivey PMI; US trade balance.

- Wednesday: Japan labor cash earnings, current account; RBNZ rate decision; Germany industrial production; FOMC minutes.

- Thursday: Germany trade balance; ECB meeting accounts.

- Friday: New Zealand BNZ manufacturing; Japan PPI; Swiss SECO consumer climate; Canada employment; US U of Michigan consumer sentiment.

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.11; (P) 147.47; (R1) 147.84; More...

USD/JPY's strong rally and break of 149.95 resistance revived the case that corrective pattern from 150.90 has already completed at 145.47. Intraday bias is back on the upside for 150.90 first. Firm break there will resume larger rally from 139.87 to 151.22 fibonacci level. Sustained break there will carry larger bullish implication. On the downside, below 149.01 will turn intraday bias neutral again first.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.