Sample Category Title

Weekly Focus – US Government Shuts Down Amid Labour Market Focus

The US labour market is the focus in markets and for the economic outlook. This week we received some weak signals from the private ADP employment report and the Challenger report. The ADP report showed private employment growth stalling in both August and September against expectations of continued moderate rises. The Challenger report revealed that firms' hiring plans continued to drop sharply. On the other hand, actual layoffs continued to decline while the JOLTs job openings data landed close to expectations. Hence, the US job market indicators are sending mixed signals. Overall, most indicators are consistent with the view that job growth is slowing mainly due to weaker supply growth and not indicating an urgent need for more demand stimulus. This was also underscored by the ISM manufacturing data that remained at 49 as expected. Yet, the risk picture of the US labour market is shifting to the downside. Due to the government shutdown, we will not receive the September labour market report, which could have a significant impact on the view of the labour market and Federal Reserve outlook.

US politics remains in focus following the government shutdown and the supreme court ruling on Fed's Lisa Cook. The government shut down as deep partisan divisions have prevented Congress and the White House from reaching a funding agreement. The direct macroeconomic impact is expected to be limited, but markets are likely to focus on two key implications: delays in the publication of US economic data, and the potential layoffs of public sector workers as highlighted by the White House. While these factors may not significantly alter the macroeconomic outlook, they could, all else being equal, modestly increase the likelihood of the Fed considering a rate cut in October. At the October meeting Fed governor Lisa Cook will attend since the Supreme Court temporarily blocked Trump's attempt to remove her, deferring the case until January 2026. This marks a significant victory for both Governor Cook and the independence of the Federal Reserve.

In the euro area, inflation rose to 2.2% y/y in September from 2.0% y/y as expected. The main reason for the rise in inflation was base effects on energy prices that drove up energy inflation. This was visible as core inflation held steady at 2.3% y/y. Monthly price increases in services and core goods were like recent months so there was not much new in the September report, but a continuation of the recent inflation developments. The unemployment data was also similar to recent months with almost no change in the number of unemployed persons, despite the unemployment rate rising to 6.3% from 6.2%. As this week's data was close to expectations it supports view that the ECB is done cutting rates.

In Asia, the Chinese PMIs came out better than expected and suggests that the weakness over the summer was partly affected by temporary weather events. It also revealed that Chinese exports continued to cope well despite the US tariffs, while domestic demand suffers and needs further stimulus. In Japan, the Tankan business survey showed stable but high business conditions, which means BoJ can continue hiking the policy rate in our view.

Next week we have a very light calendar with no tier-1 global macro data scheduled but we might get the delayed US labour market report if the government shutdown ends. We do receive the private University of Michigan consumer confidence as well as FOMC minutes in the US, sentix and retail sales in euro area, and wage data in Japan.

Sunset Market Commentary

Markets

US yields currently are changing between +1.5 bps (2-y) and 0.5 bps (30-y). Similar story for the German yield curve (2-y +0.5 bps; 30 y -1 bp). This looks like being the new normal, potentially for some time to come. Admittedly, the US services ISM still to be released after finishing this report, gives markets one of the few timely indicators bringing some ‘new eco news’. However, with markets currently almost fully discounting two additional 25 bps rate cuts for the two remaining Fed meetings (end Oct; Dec), we don’t expect an outsized reaction. Even a big (positive?) surprise probably isn’t enough for markets to change their expectations on some additional ‘risk management’ Fed easing going forward. There were few comments from Fed members on policy today. In this respect markets now look forward to next week’s Minutes of the 17 September Fed policy meeting to get some insight on the internal debate on the need/pace of further easing. This insight for sure will be interesting. Even so, it remains a bit of old news and the huge dispersion in the dots suggests that some more detailed comments won’t solve the issue of contradicting views and the absence of visibility on the Fed reaction function going forward. Maybe, the most valuable market information on the ‘real’ demand/supply balance in US interest markets might come from the mid-month US auction series next week (3-y, 10-y, 30-y). Regarding ECB policy, Belgian ECB council member Pierre Wunsch reiterated that the central bank currently is in ‘ a good place’. Aside from the current policy stance, the governor of the National Bank of Belgium showed quite some criticism on the implications of the protracted period of low policy rates that preceded the inflation, including in terms of fiscal discipline in a number of countries. Wunsch also raised questions on the effectiveness of massive asset purchases and the consequences of the bank making losses for a long period. On markets outside FI, overall low volatility keeps US and European indices (Eurostoxx 50) near all-time highs, but momentum eases compared to stronger dynamics earlier this week. On FX markets, the dollar is still holding tight ranges (DXY 97.8, EUR/USD 1.1735 from 1.1715). The yen weakened slightly this morning after balanced comments from governor Ueda. Markets now keep a close eye at the nomination of a new LDP leader/Prime minister. Will the yen be able to resume its rebound once this political event risk is out of the way? Sterling this week avoided a test of the key EUR/GBP 0.8769 area, but at 0.8723 and with an attempt of the UK currency to regain the 0.87 mark failing, the picture for sterling still looks vulnerable.

News & Views

With polling stations opening in the Czech Republic, the ANO movement appears poised for victory with around 30% support in election polls. The key question now revolves around its choice of coalition partners, which will shape the contours of future policy. Potential allies include SPD, Stačilo, and Motorists—all critical of the EU and NATO. Parties need at least 5% of the vote to enter parliament. One thing is already clear: the upcoming four-year electoral cycle will bring no meaningful progress on euro adoption in the Czech Republic. Earlier this year, both the Ministry of Finance and the Czech National Bank recommended that the government should refrain from setting a target date for euro adoption. If the next Czech electoral cycle is once again a non-starter, the earliest realistic date for joining the eurozone would be 2034.

The United Nation’s FAO Food price Index declined slightly for a second straight month in September, from 129.7 to 128.8. That’s nevertheless still the third highest reading since February 2023. Drops in sugar and dairy prices led the decline. The FAO Sugar Price Index (-4.1%) reached its lowest level since March 2021 driven by higher-than-expected sugar production in Brazil and favourable harvest prospects in India and Thailand, following ample monsoon rains and expanded plantings. The FAO Dairy Price Index declined by 2.6%, partly reflecting waning demand for ice cream in the Northern Hemisphere and higher production prospects in Oceania. The FAO Meat Price Index was the only to increase (+0.7% M/M; +6.6% Y/Y). Cereal and vegetable oil prices recorded declines of respectively 0.6% and 0.7% in September.

US September ISM Services PMI Miss Expectations – Market Reactions

In the absence of Bureau of Labor Statistics data, preventing a more interesting day, participants are focusing on today's ISM Services PMI report closely

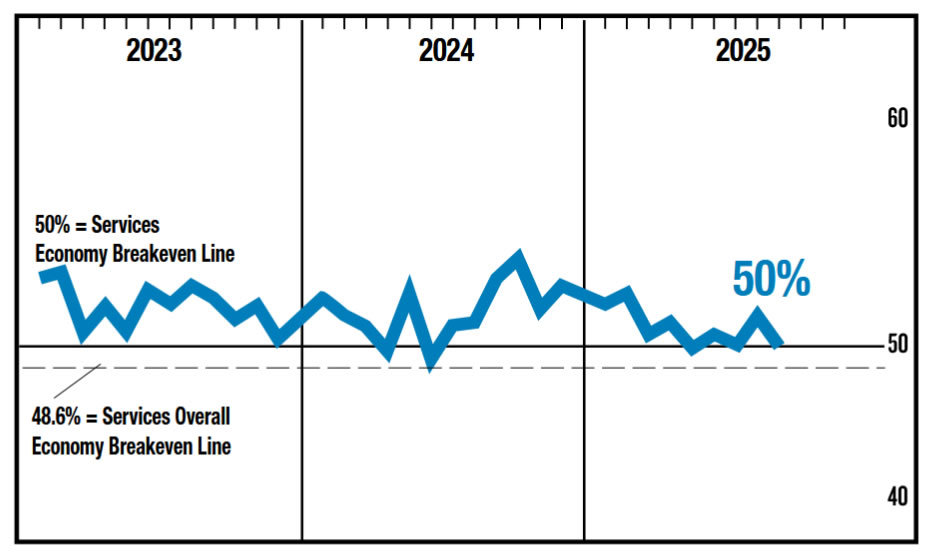

Markets just received the report for the US ISM Services PMI, which slipped right around contraction territory at 50.0, missing expectations of 51.6 and down from the prior 52.0.

The services sector — which makes up the bulk of US economic activity — is closely monitored as it reflects both consumer and business demand momentum,

PMIs, particularly for the services sector, had been holding strong despite tariffs starting to bite into companies' profit-margins and activities, but things are starting to change.

Now a few months after the July tariff implementation, the data is reflecting more and more the Trump Policies.

The essential Services PMI is now at the border of contraction.

Markets also received the Global PMI report about 15 minutes ago (53.9 vs 53.6 exp) but this one is less of a mover.

Discover the reactions in the main assets classes including US Equities (Nasdaq), US Treasuries, and the DXY just below.

A few market reactions

Everything seems to be selling off for now!

A global market picture after the September Services PMI report, October 3, 2025 – Source: TradingView

Safe Trades!

US ISM services sinks to 50, GDP barely expanding by 0.4%

US services activity slowed sharply in September, with ISM Services PMI falling from 52.0 to 50.0, missing expectations of 52.0. Business activity dropped from 55.0 into contraction at 49.9, its first negative reading since May 2020. New orders tumbled from 56.0 to 50.4. The weakness suggests that demand conditions in the largest part of the US economy have cooled significantly.

Employment remained in contraction for a fourth straight month at 47.2, underscoring persistent softness in labor conditions. Prices paid ticked higher to 69.4, staying well above the 60 mark for a 10th month.

Industry-level data reinforced the slowdown: only ten industries reported growth in September, two fewer than August, while the number in contraction rose to seven. Based on historical correlations, ISM said the September PMI level corresponds to a modest 0.4% annualized GDP increase.

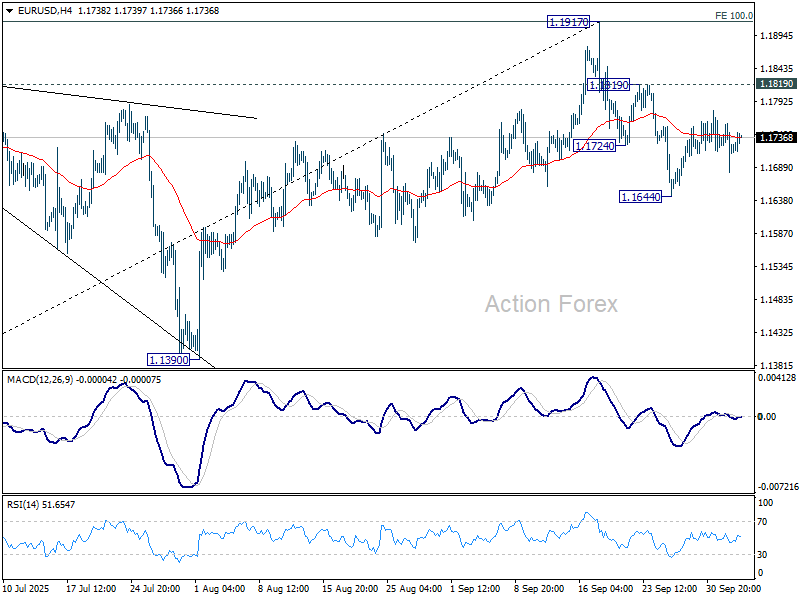

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1680; (P) 1.1720; (R1) 1.1756; More...

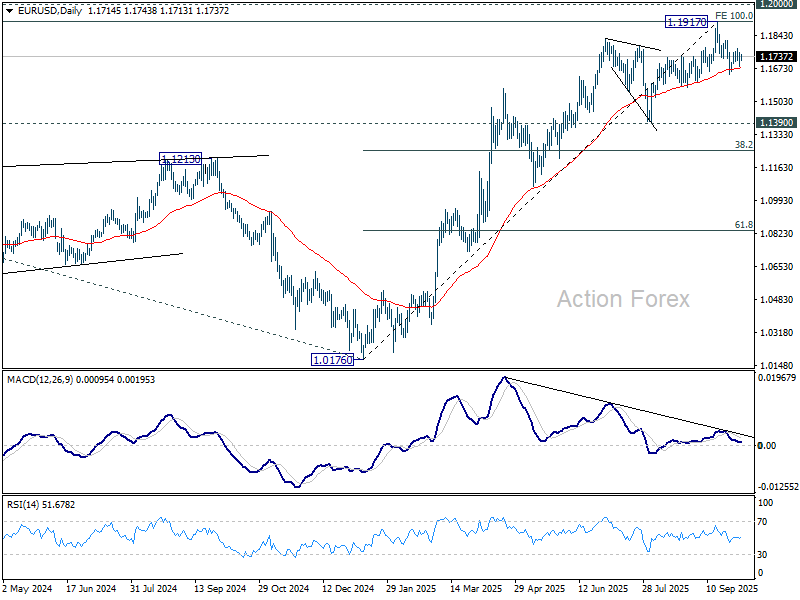

Outlook in EUR/USD is unchanged and intraday bias remains neutral for the moment. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1675) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next. Nevertheless, break of 1.1819 will bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

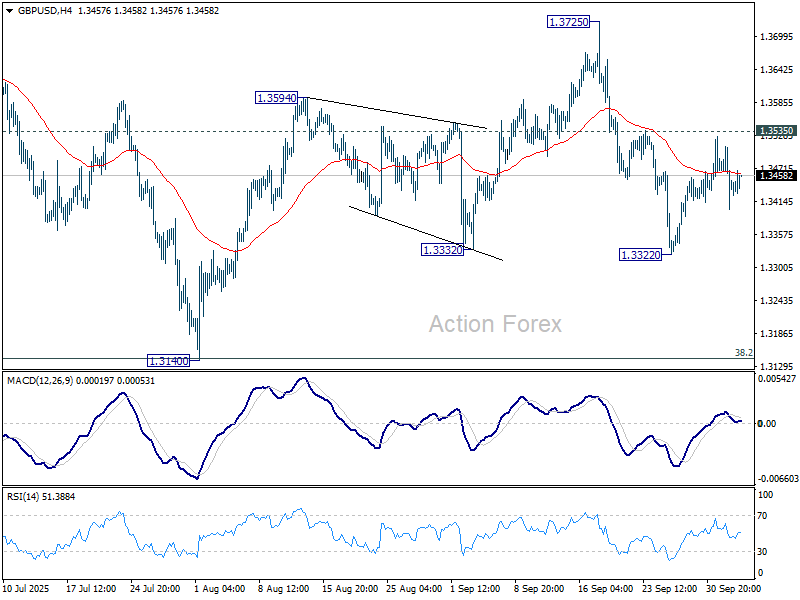

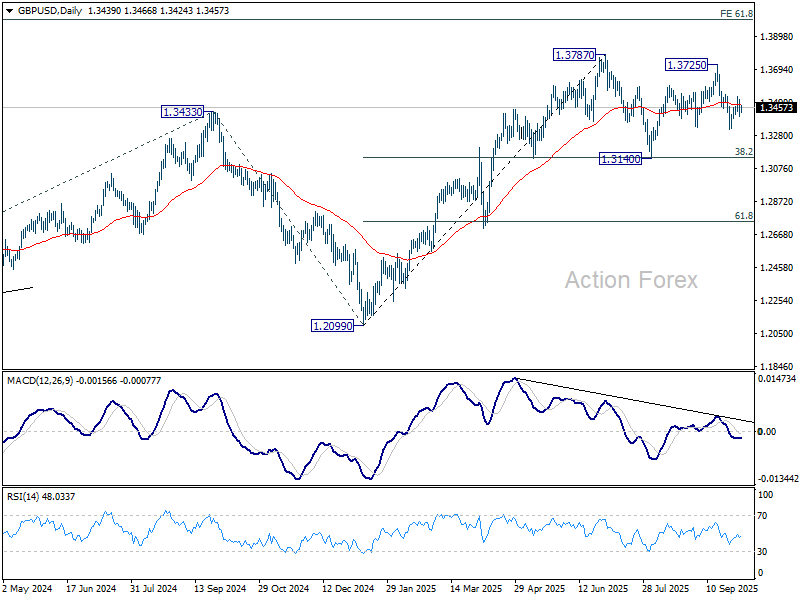

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3391; (P) 1.3451; (R1) 1.3501; More...

Outlook in GBP/USD remains unchanged and intraday bias stays neutral for the moment. On the upside, firm break of 1.3535 resistance will suggest that pullback from 1.3725 has completed, and bring stronger rally to 1.3725/87 key resistance zone. On the downside, though, break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

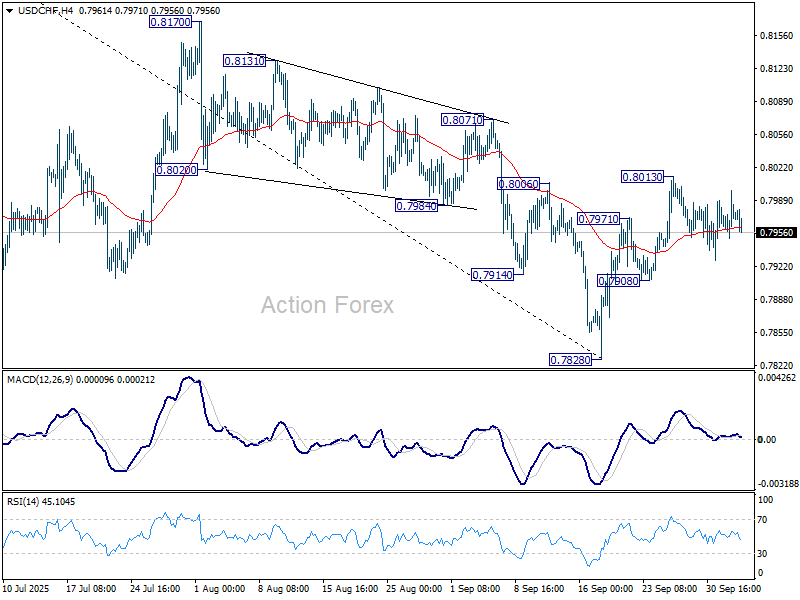

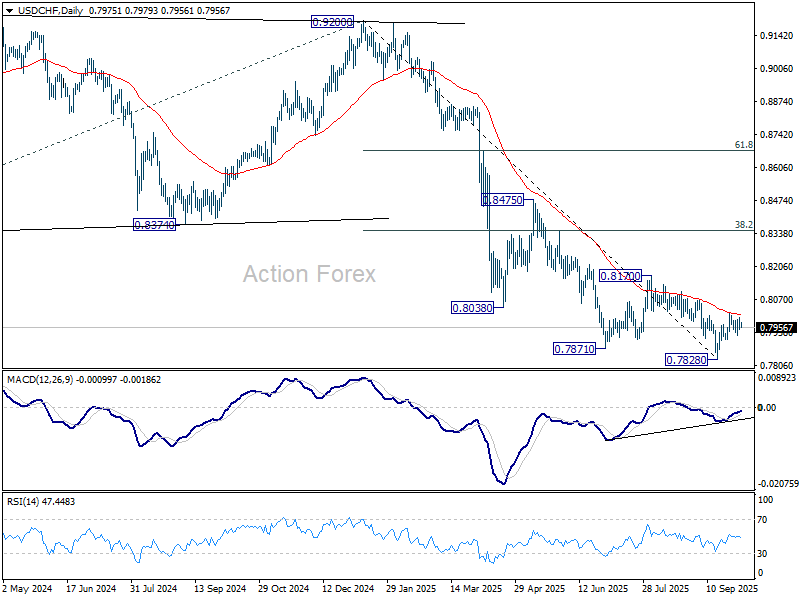

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7953; (P) 0.7977; (R1) 0.8002; More…

Intraday bias in USD/CHF remains neutral as sideway trading continues. On the upside, sustained trading above 55 D EMA (now at 0.8011) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

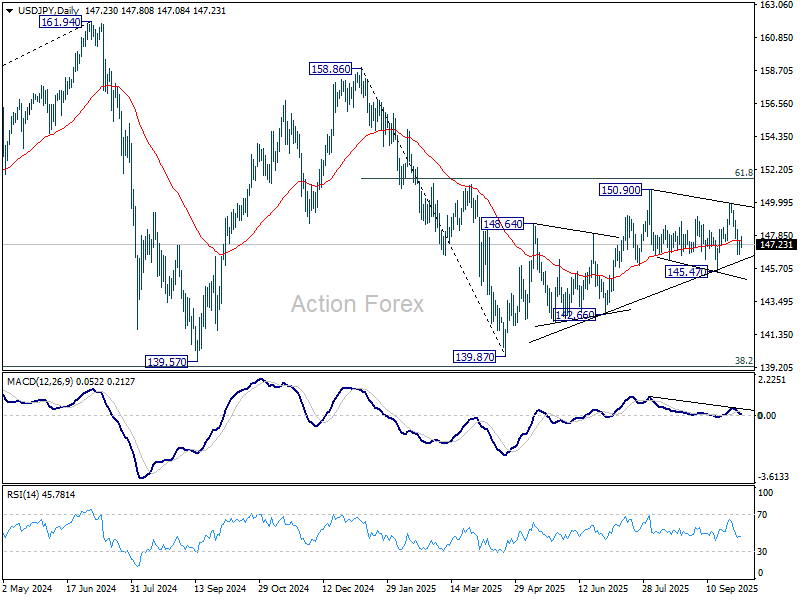

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.73; (P) 147.13; (R1) 147.65; More...

Intraday bias in USD/JPY stays neutral at this point. For now, price actions from 150.90 are still seen as a corrective pattern. On the upside, above 148.12 minor resistance will bring stronger rally to 149.95 first. Firm break there should resume larger rally from 139.87 through 150.90. On the downside, though, below 146.58 will bring deeper fall to 145.47 support. Decisive break of 145.47 will indicate near term reversal, and bring deeper fall to 142.66 support next.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

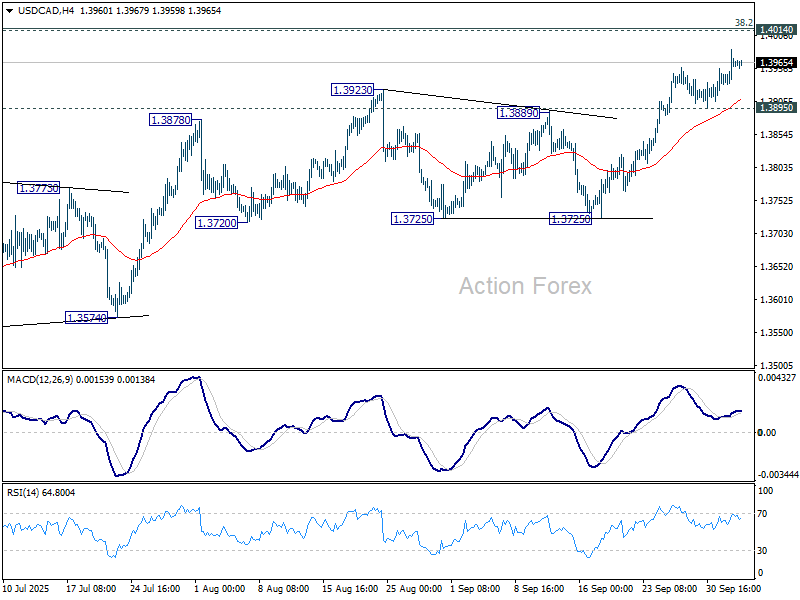

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3938; (P) 1.3962; (R1) 1.3991; More...

Intraday bias in USD/CAD remains on the upside and further rise could be seen. But strong resistance is expected from 1.4014 cluster to complete the corrective rebound from 1.3538. On the downside, break of 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

Loonie Sinks as WTI Oil Nears $60, OPEC+ Hike Looms

Canadian Dollar remains the weakest major currency this week, pressured by a combination of falling oil prices and dovish stance of the BoC. Canada’s key export driver slumped to a four-month low with WTI crude threatening to break below 60 handle. That decline comes just as the BoC’s own communications reinforced expectations of more easing ahead.

The oil market itself is under heavy pressure from expectations of a large OPEC+ output hike. Reports suggest the group could raise production by as much as 500,000 barrels per day in November—triple the October increase—in a bid to reclaim lost market share. Such a move would come at a time when analysts already warn the market may be tipping into sizeable surplus through Q4 and into 2026.

For the BoC, September summary of deliberations confirmed concerns that the economy is losing momentum. Policymakers noted further softening in the labor market and more convincing signs that core inflation pressures are easing. In addition, the removal of most retaliatory tariffs has reduced the risk of renewed cost-push inflation. Against that backdrop, the decision to cut rates to 2.50% was straightforward, and officials left the door open to additional easing.

Still, not all forecasts are bearish for the Canadian Dollar. A recent Reuters poll of 38 FX analysts showed a median projection for the Loonie to strengthen around 2.8% to 1.36 per U.S. Dollar by the end of 2025. That view rests on the assumption that the Fed will embark on a more aggressive easing path in 2026, while the BoC, having moved earlier, may conclude the cycle sooner.

Canada’s growth backdrop remains fragile but not disastrous. GDP contracted at an annualized pace of -1.6% in Q2, but subsequent monthly data suggest the economy may have avoided slipping into a technical recession.

So far this week, Loonie is at the bottom of the FX performance table, followed by Dollar and Swiss Franc. Yen continues to lead despite today’s mild retreat, with Kiwi and Aussie also among the outperformers. Euro and Sterling remain stuck in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.54%. DAX is down -0.17%. CAC is down -0.10%. UK 10-year yield is down -0.026 at 4.688. Germany 10-year yield is down -0.008 at 2.696. Earlier in Asia, Nikkei rose 1.85%. Hong Kong HSI fell -0.54%. China was on holiday. Singapore Strait Times rose 0.38%. Japan 10-year JGB yield fell -0.002 to 1.665.

Eurozone PPI down -0.3% mom, -0.6% yoy, energy drag while regional divergence widens

Eurozone producer prices fell by -0.3% mom and -0.6% yoy in August, weaker than expectations of flat monthly growth and a smaller -0.4% yoy decline. The drop underscores the continued disinflationary forces in the pipeline, particularly as energy prices remain soft.

Breaking down the Eurozone data, prices fell -1.3% mom for energy and -0.1% for both intermediate and durable consumer goods. In contrast, modest increases were seen in capital goods (+0.1%) and non-durable consumer goods (+0.1%).

Across the EU as a whole, PPI slipped -0.4% mom and -0.4% yoy. At the country level, the steepest monthly declines were recorded in Denmark (-1.3%), the Netherlands and Romania (both -1.0%), and Austria (-0.8%). Meanwhile, Estonia (+5.4%), Finland (+1.9%) and Slovakia (+1.3%) bucked the trend with notable gains.

Eurozone PMI signals 0.4% Q3 GDP growth, backs ECB hold

Eurozone services activity strengthened in September, with PMI Services finalized at 51.3, up from 50.5 in August and marking an eight-month high. Composite PMI also edged higher to 51.2, the best in 16 months.

Country breakdowns in Composite highlighted broad-based improvement. Spain led with a 53.8 reading, while Germany and Ireland both came in at 52.0, representing multi-month highs. Italy held at 51.7, while France lagged with a decline to 48.1, its weakest in five months.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that business activity “picked up more strongly” in September, and that the rebound was “broad-based geographically.” The uptick in new business suggests expansion could continue into October, though backlogs have yet to recover.

Crucially, price pressures eased but remained slightly above average. De la Rubia said the data support policymakers who resist further cuts, as inflation in services is still sticky. With the composite PMI holding in expansionary territory throughout Q3, HCOB’s nowcast points to quarterly GDP growth of around 0.4%.

UK PMI suggests summer bounce a flash in the pan, supports BoE dovish shift

UK business activity slowed sharply in September, with the final Services PMI dropping to 50.8 from August’s 16-month high of 54.2, marking a five-month low. The Composite PMI mirrored the downturn, slipping to 50.1 from 53.5, also a five-month trough.

Tim Moore, Economics Director at S&P Global Market Intelligence, said service providers saw a “disappointing end” to Q3 as weak consumer confidence, postponed investment decisions, and falling exports weighed on demand. He warned that the summer’s output surge now looks like a “flash in the pan,” with political and economic uncertainty again restraining the sector. Export orders were particularly weak, as European demand remained subdued.

The report also flagged another month of job losses, extending a year-long trend, alongside weaker business confidence and softer cost pressures. These signs of slackening labor conditions and easing inflation are likely to reinforce the “more dovish shift” in the BoE’s policy debate, with calls growing for further rate cuts into 2025.

BoJ's Ueda reiterates further hikes if baseline holds, flags three uncertainties

BoJ Governor Kazuo Ueda said in a speech today that Japan’s real interest rates remain “significantly low,” and if the Bank’s baseline scenario holds, policy rates will continue to rise. He highlighted that rising labor shortages and firmer medium- to long-term inflation expectations should eventually push underlying CPI toward 2% in the second half of the Bank’s forecast horizon.

Ueda acknowledged, however, that uncertainties remain significant. Chief among them are US economic developments, tariff impact on Japan, and food price inflation.

He warned that tariffs could hurt US firms’ profits and in turn slow employment and income growth — risks that may already be showing in weaker US job data. If firms pass on costs instead, higher consumer prices could sap private demand.

At home, the Tankan survey suggested resilience in services, where the tariff impact is limited, but profit projections for export-heavy industries such as autos showed steep declines.

Food prices are another area of concern. While much of the recent rise has been driven by temporary factors, Ueda cautioned that wage and distribution cost pass-through is increasingly evident. That raises the possibility of more persistent inflation in food.

Japan unemployment rate rises to 2.6%, highest in over a year

Japan’s unemployment rate rose more than expected in August, climbing to 2.6% from 2.3% a month earlier. That marked the highest reading since July 2024 and exceeded expectations of 2.4%.

Number of unemployed increased by 150k to 1.79 million, a 13-month high, while employment fell by -210k to 68.10 million. The labor force edged down by -40k to 69.89 million, though the participation rate improved to 64.0% from 63.9%. Still, the data underscored growing strain in the labor market as job creation weakens and unemployment rises.

Complementary data from the labor ministry showed the job-to-applicant ratio slipping to 1.20 from 1.22, its lowest since January 2022. The decline points to waning demand for labor.

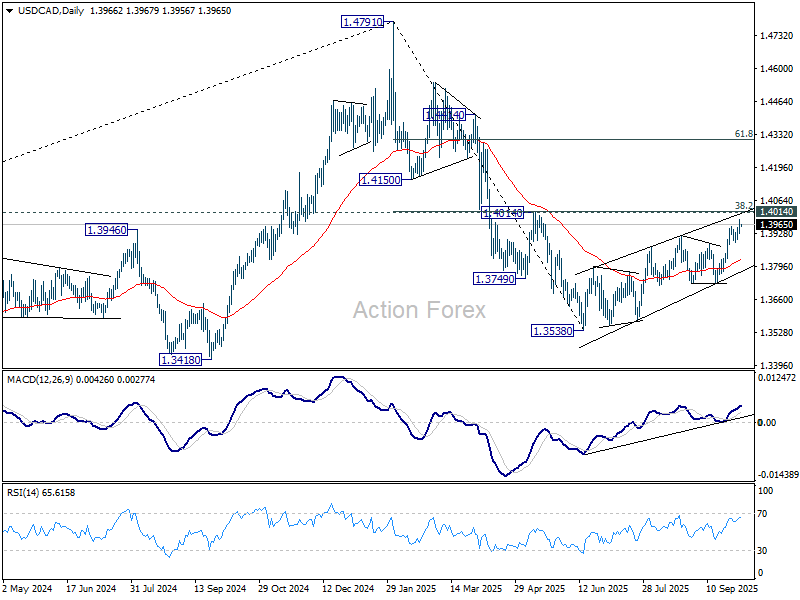

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3938; (P) 1.3962; (R1) 1.3991; More...

Intraday bias in USD/CAD remains on the upside and further rise could be seen. But strong resistance is expected from 1.4014 cluster to complete the corrective rebound from 1.3538. On the downside, break of 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.