Sample Category Title

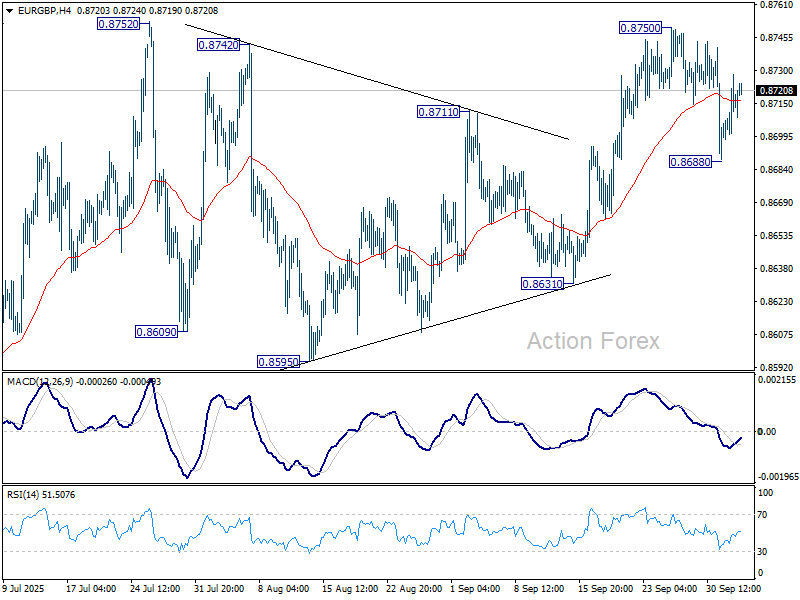

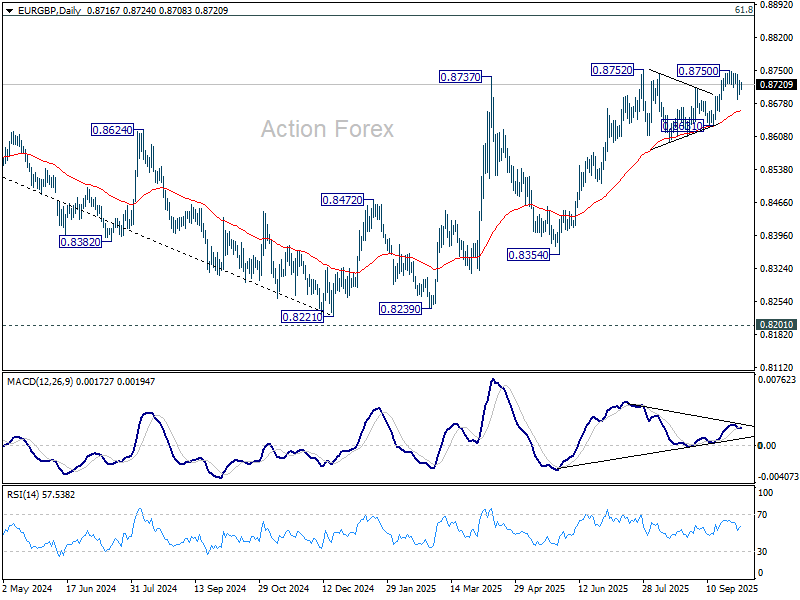

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8699; (P) 0.8715; (R1) 0.8734; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the upside, firm break of 0.8750 will resume larger rise to 0.8867 fibonacci level. However, decisive break of 0.8688 will turn bias back to the downside for 0.8631 support. Firm break there will indicate near term bearish reversal.

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8533) will argue that the pattern has completed and bring retest of 0.8221 low.

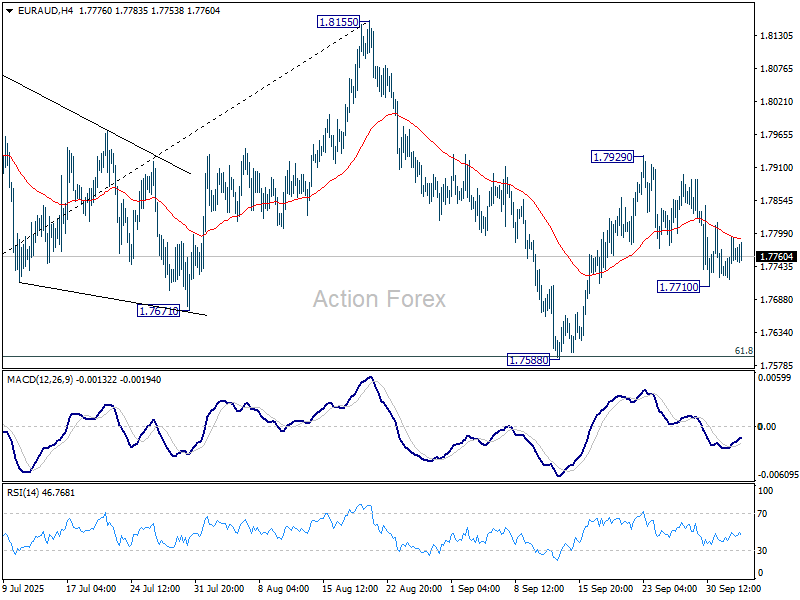

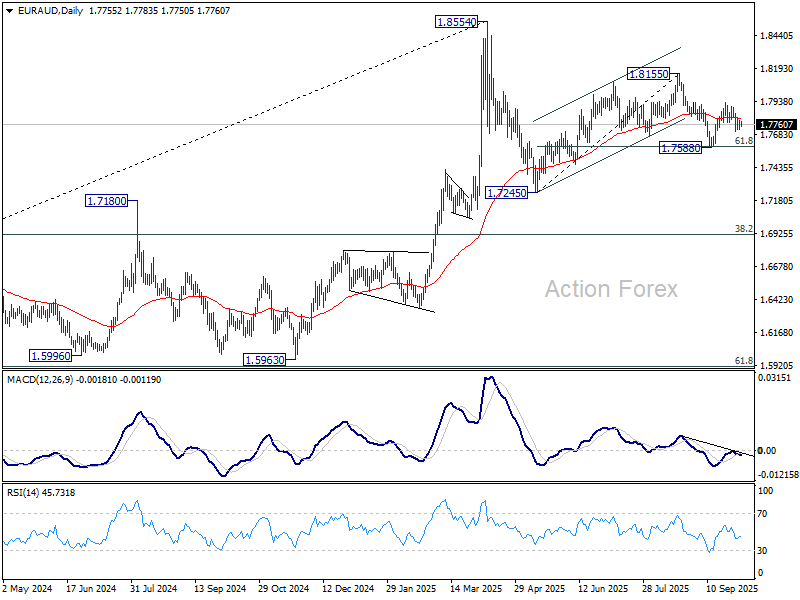

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7725; (P) 1.7760; (R1) 1.7796; More...

Intraday bias in EUR/AUD stays neutral and outlook is unchanged. On the upside, above 1.7929 will resume the rebound from 1.7588 to retest 1.8155. However, sustained break of 61.8% retracement of 1.7245 to 1.8155 at 1.7593, will resume the fall from 1.8155 to 1.7245 resistance, as part of the corrective pattern from 1.8554 high.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

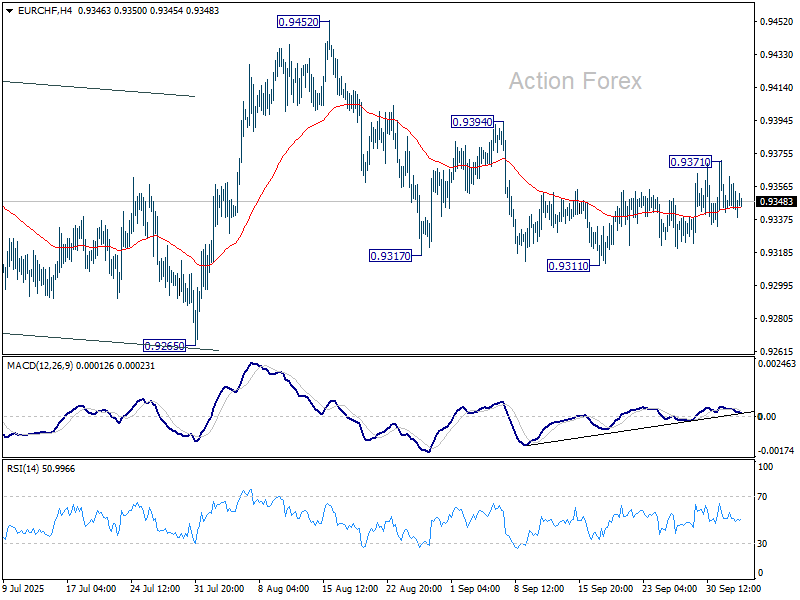

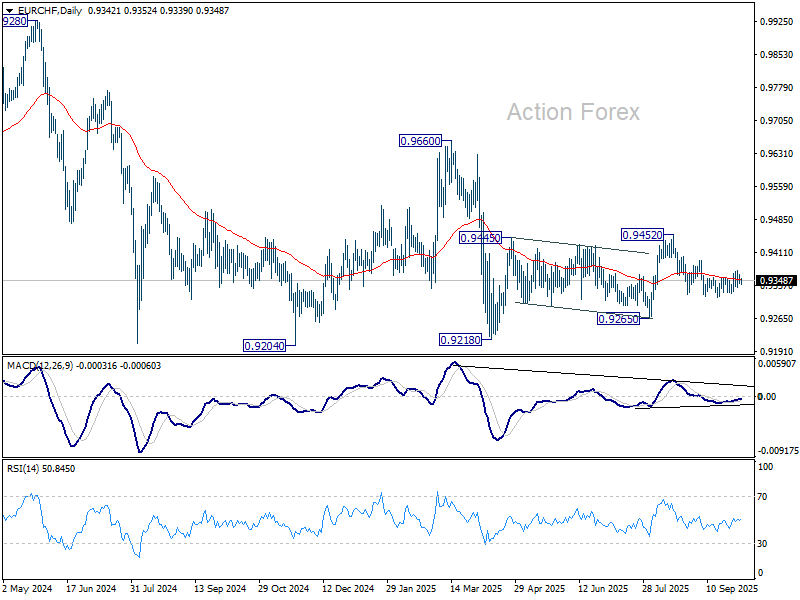

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9337; (P) 0.9351; (R1) 0.9362; More...

Range trading continues in EUR/CHF and intraday bias remains neutral. On the upside, above 0.9371 will target 0.9394 resistance. Firm break there should confirm that the pullback from 0.9452 has completed, and bring retest of this resistance. Nevertheless, break of 0.9311 will resume the fall from 0.9452 to 0.9265 support.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

Yen Underperforming After ‘Balanced’ Comments from BOJ Ueda

Markets

The US government shutdown to a large degree translated into a ‘market info shutdown’. US data releases including jobless claims and factory orders were delayed, depriving investors of some potential drivers. Especially jobless claims over the previous weeks showed some (intraday) market moving potential. With no key data in other developed economies like the EMU or the UK, this only reinforced the low volatility environment. This not only applies to US equity markets but also to interest rate markets and FX. A measures of US bond market volatility has dropped to the lowest level since end 2021! As a point in case. US yields yesterday changed between + 0.4 bp (2y) and -2.1 bps (30-y). German yields in similar directionless trading eased between 0.3 bps (2-y) and -2.5 bps (30-y). For now, the adagio ‘no news is good news’ reigns. The S&P 500 closed at a marginal new all-time record. The EuroStoxx 50 decisively confirmed Wednesday’s break into uncharted territory (+1.15%). A similar low-volatility narrative also plays in the major dollar cross rates. The dollar didn’t budge despite a positive risk sentiment and the prospect/hope of Fed easing. DXY gained marginally (97.85) but perfectly holds in the 96.21/98.83 short-term consolidation range. Idem for EUR/USD (close 1.1715 from 1.1732). Even the yen, one of the more outspoken directional trades in major FX this week, wasn’t able to maintain its momentum. After a failed test of the 150 area end last week, the yen rebounded yesterday after running into resistance in the USD/JPY 146.60 area. Comments supportive of a (potential) rate hike at the end of this month from deputy government Uchida, didn’t help further yen gains.

Most Asian equity markets continue a (tech-driven) rally this morning with Japan one of the outperformers. China and South Korea are closed. Still the dollar gains marginally, with the yen this time underperforming after ‘balanced’ comments from BOJ governor Ueda (see below). An unexpected rise in the Japanese unemployment rate in this respect probably also doesn’t help (2.6% from 2.3%). Later today, the US labour market data won’t be published due to the shutdown, but markets at least have the US services ISM as one of the few remain guides in the run-up to the October 29 Fed decision. US confidence indicators recently suggested a further loss of momentum including softer labour market conditions. Today’s services ISM is expected at 51.7 (from 52) with the employment index near 46.5. With two follow-up 25 bps Fed rate cuts almost fully discounted, there is far less room for a similar reaction compared to this week’s ADP miss. Maybe it might still have some limited impact on the dollar, more than on US interest rates, with USD/JPY most sensitive even as Japanese domestic factors (LDP leadership vote) are in play.

News & Views

Bank of Japan governor Ueda kept options open for the end-of-the month policy meeting. In a speech for local business leaders, he didn’t extend market momentum endorsing a 25 bps rate hike instead sticking to official guidance. “If the baseline scenario for economic activity and prices outlined so far is realized, the bank, in accordance with improvement in economic activity and prices, will continue to raise the policy rate”. On the economic front, the central bank monitors the global economy and the impact of US tariffs on Japan’s corporate profits. On the price front, wage and food inflation require attention. Ueda made no reference to domestic political uncertainty, but for sure keeps a close eye on local LDP leadership elections this weekend. The risk of snap parliamentary elections ahead of the next BoJ meeting is still a tail risk.

Bank of Canada deputy governor Mendes indicated that markets are too focused on the central bank’s “preferred” core inflation measures. They were introduced in 2016 under former governor Poloz with two of the three original ones remaining (trimmed mean and median). They show annual price pressures around 3%, but the BoC sees underlying inflation in the vicinity of 2.5%. Mendes argued that the way the central bank measures inflation will be part of next year’s framework renewal. As an example, he suggested revising inflation gauges so they all “pre-exclude mortgage interest costs”. The BoC revamped its cutting cycle in September after a six-month pause with money markets 50/50-split over the possibility of a new rate cut (to 2.25%) at the end of this month.

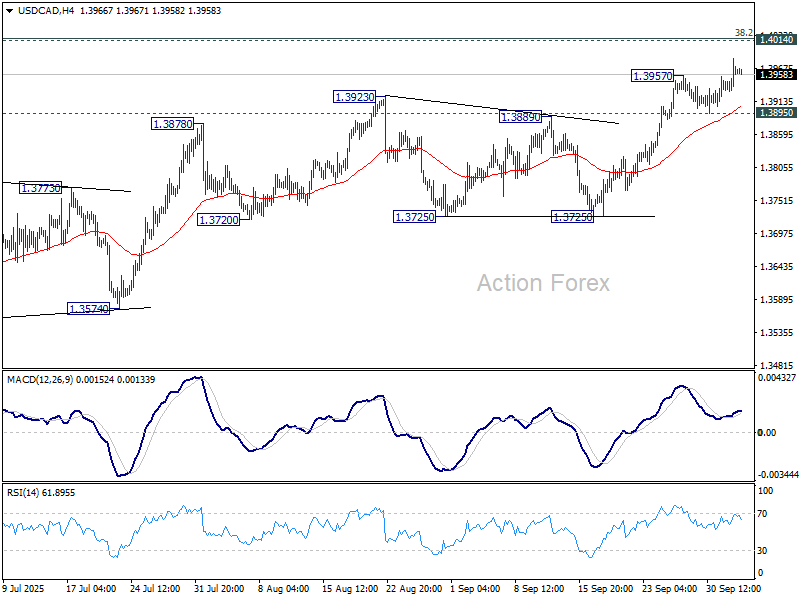

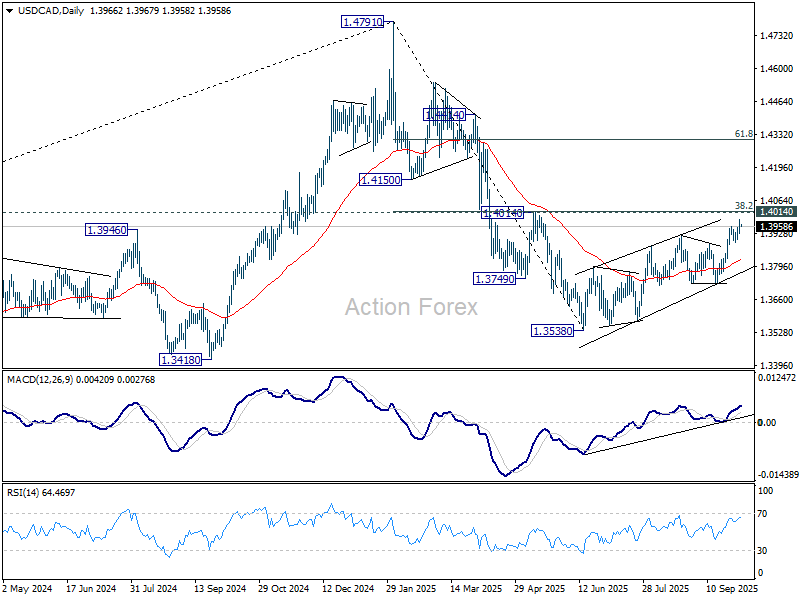

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3938; (P) 1.3962; (R1) 1.3991; More...

USD/CAD's rally resumed by breaking through 1.3957 and intraday bias is back on the upside. Strong resistance is expected from 1.4014 cluster to complete the corrective rebound from 1.3538. On the downside, break of 1.3895 support will turn bias back to the downside for 1.3725. However, sustained break of 1.4014 will carry larger bullish implications.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 (2025 high) at 1.3069. However, sustained break of 1.4014 will argue that fall from 1.4791 has completed, and bring stronger rally to 61.8% retracement at 1.4312.

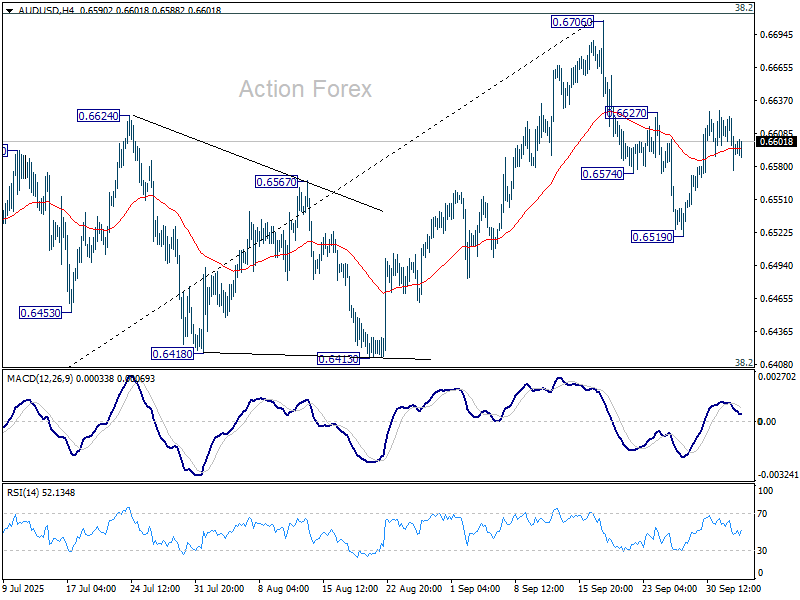

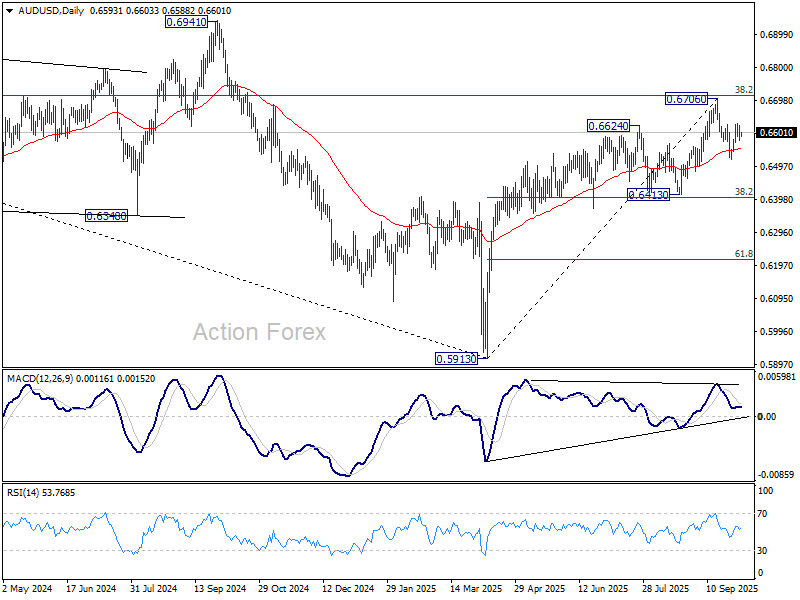

AUD/USD Daily Report

Daily Pivots: (S1) 0.6574; (P) 0.6599; (R1) 0.6622; More...

Intraday bias in AUD/USD remains neutral and outlook is unchanged. On the upside, firm break of 0.6627 resistance will suggest that pullback from 0.6706 has completed as correction, after drawing support from 55 D EMA (now at 0.6554). That will keep the larger rally from 0.5913 alive and bring retest of 0.6706 high. However, on the downside, sustained trading below 55 D EMA will confirm rejection by 0.6713 fibonacci resistance, and bring deeper fall to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

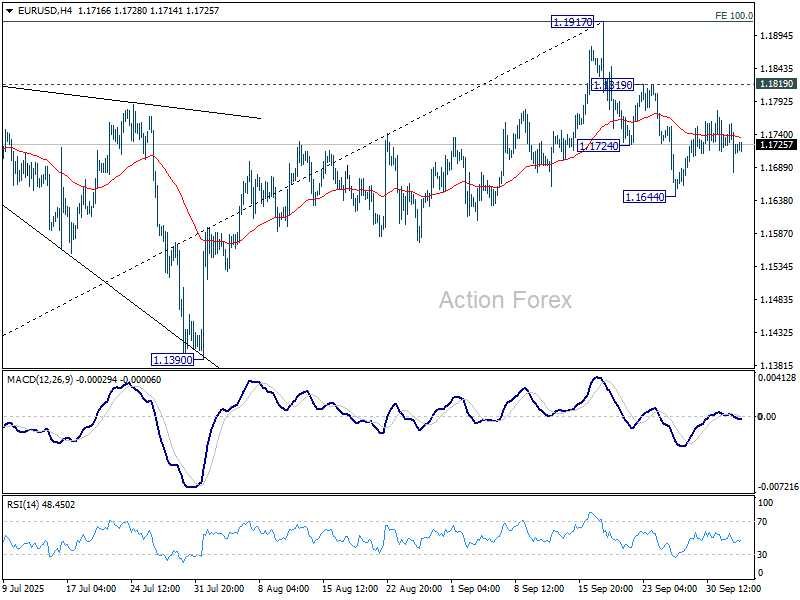

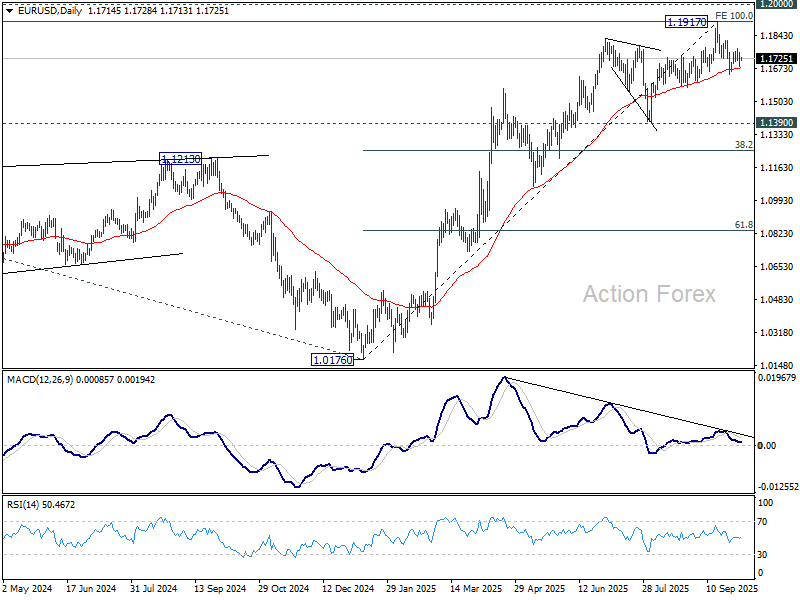

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1680; (P) 1.1720; (R1) 1.1756; More...

Intraday bias in EUR/USD remains neutral and outlook is unchanged. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 1.1675) will argue that 1.1917 was already a medium term top. Deeper fall should then be seen to 1.1390 support next. Nevertheless, break of 1.1819 will bring retest of 1.1917 high instead.

In the bigger picture, rise from 1.0176 (2025 low) is seen as the third leg of the pattern from 0.9534 (2022 low). 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916 was already met. For now, further rally will remain in favor as long as 1.1390 support holds, and firm break of 1.2000 psychological level will carry larger bullish implications. However, firm break of 1.1390 will suggest that rise from 1.0176 has already completed and bring deeper fall to 55 W EMA (now at 1.1231).

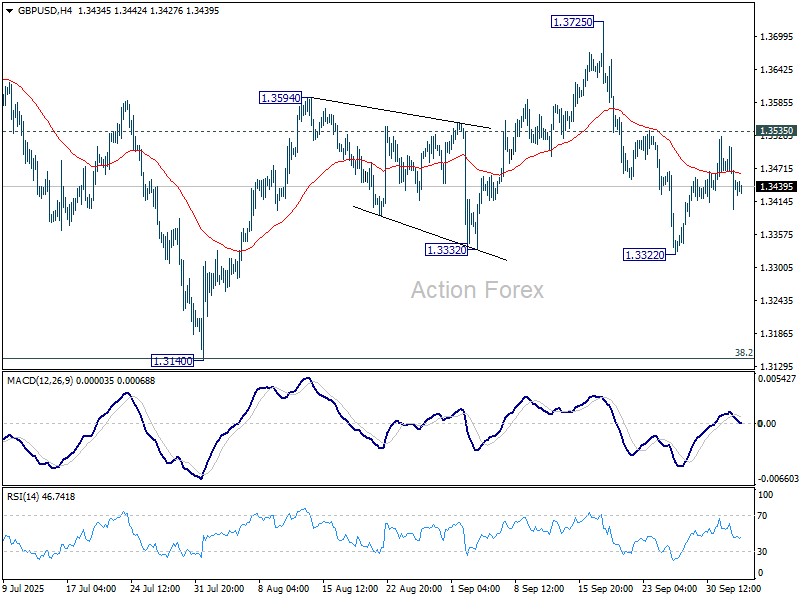

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3391; (P) 1.3451; (R1) 1.3501; More...

Intraday bias in GBP/USD remains neutral and outlook is unchanged. On the upside, firm break of 1.3535 resistance will suggest that pullback from 1.3725 has completed, and bring stronger rally to 1.3725/87 key resistance zone. On the downside, though, break of 1.3322 will resume the fall from 1.3725, as the third leg of the corrective pattern from 1.3787, and target 1.3140 support.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could be seen from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3155) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

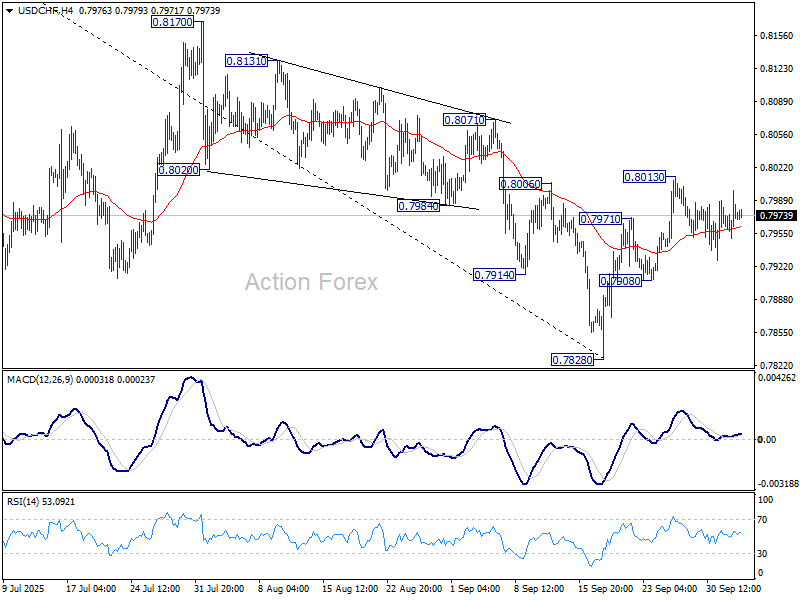

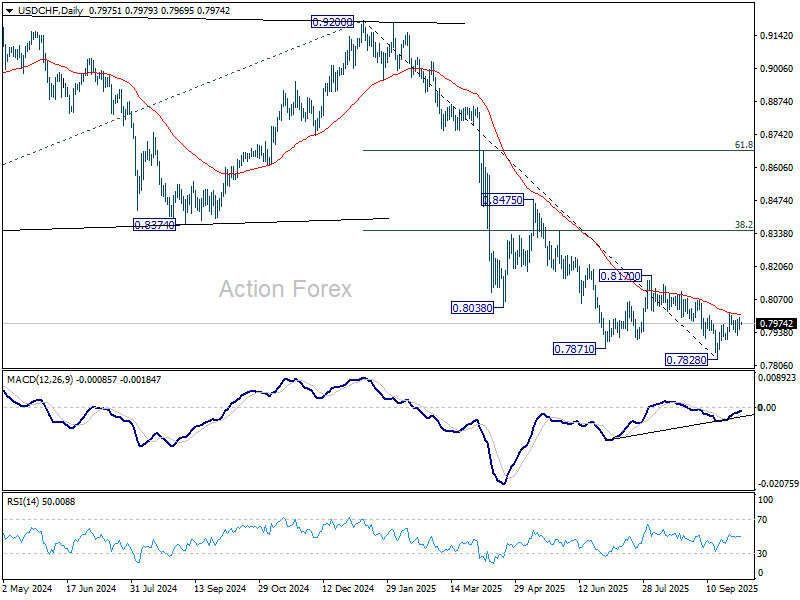

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7953; (P) 0.7977; (R1) 0.8002; More…

USD/CHF is still bounded in sideway trading and intraday bias stays neutral. On the upside, sustained trading above 55 D EMA (now at 0.8011) will suggest that rise from 0.7828 is already correcting whole fall from 0.9200. Further rise should the be seen to 0.8170 resistance and possibly above. However, break of 0.7908 will turn bias back to the downside for retesting 0.7828 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

AI Doesn’t Care About Shutdowns

Yesterday was yet another day investors swung between political shenanigans in the US and AI hype. Mood was not necessarily great in the early hours of trading across the Pacific after Trump’s threat to fire thousands of federal employees if the government shutdown drags on. And the government shutdown doesn’t sound like it will end soon, as Democrats are pushing for the extension of Affordable Care Act subsidies that will expire in a few months, while Republicans don’t want to move ahead without securing funding. Bets on Polymarket suggest that this shutdown could last between 10 to 29 days – potentially becoming the second-longest in US government history – something you could barely guess by looking at the market’s performance.

Yes, the US 10-year yield flirted with the 4% mark on some safe-haven inflows and the US dollar remains offered into its 50-DMA, but the major US indices barely blinked! The S&P 500 and Nasdaq both hit fresh ATHs yesterday, boosted by OpenAI’s secondary share sale that pushed the company’s valuation to around $500bn. Employees were allowed to sell up to $10bn worth of shares, but they only sold $6.6bn – meaning a large chunk of shareholders preferred to hold rather than sell at current prices. That signals they expect the company to grow bigger – which is understandable.

As such, OpenAI has become one of the world’s most valuable startup (overtaking Elon Musk’s SpaceX). The company reportedly expects to make about $20bn in recurring revenue by the end of the year, giving it a valuation of ~25x sales. That’s high, but not shocking given its reach and potential, and lower than many tech startups trade at.

Since OpenAI isn’t listed, the news echoed across related sectors. Microsoft and Nvidia both have exposure to OpenAI – and Nvidia will also supply chips for its massive data center project. Appetite for Microsoft was soft yesterday, but Nvidia notched another record high – following rallies in SK Hynix and Samsung on similar news that OpenAI will use their chips in upcoming US data centers. Elsewhere, AMD jumped 3.5% on news of teaming up with Intel. As such, VanEck’s Semiconductor ETF hit a fresh high. Happy days.

Valuations are high, and some investors wonder whether this is another tech bubble. But a bubble – by definition – isn’t a bubble until it bursts. That leaves global investors with an unbearable FOMO – fear of missing out on a further rally – which keeps valuations elevated. Prospects of multiple Federal Reserve (Fed) rate cuts in the coming months also help support risk assets.

Now speaking of that, markets are pricing in two more Fed rate cuts before year-end, but the Fed needs data to confirm that the US economy requires these cuts. The data that will determine this is the jobs data – because that’s where weakness is most apparent as GDP grew 3.8% last quarter and the Fed’s preferred inflation gauge is still trending near 3% (above its 2% target). So it’s a bit of a shame that the BLS won’t release the September jobs report today because the government is shut down.

Instead, private data fills the gap. ADP reported job losses of 32k on Wednesday, keeping Fed doves in charge of the market. Meanwhile, Challenger job cuts fell 25% YoY, giving mixed signals about the labour market’s heath. Consequently, the weak ADP euphoria will soon fade, and official data should arrive sooner rather than later to tell investors whether the US really needs those two rate cuts.

In the meantime, ISM non-manufacturing data will be in focus before the weekly closing bell. It won’t replace the good, old jobs report, but a softer-than-expected set could give Fed doves a hand, keeping US yields and the dollar under pressure while supporting equities. A strong print could give some support to US yields and the dollar and weigh on equities – but the market’s tilt suggests bad news will likely move markets more than good news.

In FX: the US dollar may have spent the week under pressure, but EURUSD will likely end the week without having successfully cleared the 1.18 resistance, suggesting that the shutdown and dovish Fed bets are fully priced in, and a fresh catalyst will be needed for the pair to reach the 1.20 mark. The same is true for sterling: Cable is back below 1.35 and remains unappealing due to budget pressures. The UK 10-year gilt yield is not only near Liz Truss “mini-budget” crisis levels but is also diverging undesirably from the US 10-year yield. That’s a drag on sterling, as higher yields narrow fiscal headroom, raise the chance of further tax hikes or spending cuts, and lower UK growth expectations.

Elsewhere in commodities, gold consolidates near its ATH while US crude broke below the $62pb support, snapping a floor that had held since August, on expectations of more OPEC supply. Trend and momentum indicators remain comfortably negative, and the RSI is not yet flashing oversold conditions – meaning bears may be tempted to test the $60pb level. That should act as solid support.